Snapshot of SEBI Board Meeting dated 29th September, 2020

SEBI in its Board Meeting held on 29th September, 2020 has approved amendments in various Regulations which shall come into effect by way of amendment in the respective Regulations. The brief highlights of the same are as below:

Strengthening role of Debenture Trustees

SEBI, in the recent past, has brought in certain amendments in order to strengthen the role of DTs so as to protect interest of debenture holders. The latest amendment in the existing DT Regulations was made by SEBI (Debenture Trustees) (Amendment) Regulations, 2017 which aimed to streamline provisions of DT Regulations with the CA, 2013 and other SEBI Regulation and also to enable DTs to secure the interest of investors.

The Board Meeting approved that DTs shall convene meeting of debenture holders for enforcement of security, joining of inter-creditor agreement (ICA) etc. The requirement of forming a ICA comes from the RBI Prudential Framework for Resolution of Stressed Assets and the Resolution Framework for COVID-19 related stress. By virtue of these notifications, there is a mandatory requirement of Inter-Creditor Agreements (ICA) by the lending institution governed by the RBI, for the purpose of invocation of a resolution plan of any defaulting borrower. The aforesaid frameworks recognize that even other lenders to the borrower which are other than the lending institutions, such as debenture trustee, may sign the ICA, if they so desire. In line with the same, SEBI is proposing the DTs to convene meeting for joining ICA to safeguard the interests of the debenture holders.

Keeping the same intent, DTs are also bestowed with the responsibility of monitoring the asset cover for debentures and obtain half yearly certificate from statutory auditor. The Board approved following additions to the responsibility of DTs:

- DTs to exercise independent due diligence of the assets of the company on which charge is being created

- DTs shall convene meeting of debenture holders for taking required action for enforcement of security, joining the inter-creditor agreement etc.

- Carry out continuous monitoring of asset cover including obtaining mandatory certificate from statutory auditor on half yearly basis

- Creation of recovery expense fund at the time issuance of debt securities for utilisation in the event of default or to take legal action to enforce the security.

Pursuant to the text of the Board Meeting, it seems that SEBI is going to introduce a new concept of ‘recovery expense fund’ for creating fund for expenses that might be required to recover debts due to debenture holders in case of default.

Apart from the aforesaid, the existing provisions of the Companies Act, 2013 does have a requirement of transferring funds by specified class of companies to Debenture Redemption Reserve (‘DRR’) and also transfer certain amount of funds for debentures maturing during the next year to specified account/securities (‘hereinafter referred to as DRF’). However, these funds/reserves are for recovery of debts, whereas, recovery expense fund is a pool of fund for incurring expenses for recovering debts by DTs. Nevertheless, introduction of a separate fund requirement for any event of default seems to be a new compliance burden on companies. Further, whether such fund has to be created as an internal book entry transfer within the company like in case of DRR or transfer it outside the company in trust of the DT, is something we have to look for. Definitely, companies like NBFCs and HFCs which are frequently involved in raising funds through debentures shall have a new compliance to be ensured, if such amendment is made effective.

Amendments in SEBI (Delisting of Equity Shares) Regulations, 2009

SEBI (Delisting of Equity Shares) Regulations 2009 provides for voluntary delisting of equity shares from stock exchanges which provide the overall framework for voluntary delisting by a promoter or acquirer through a process referred to as Reverse Book Building. The Board Meeting has approved of exempting listed subsidiary from complying with the book building process if following conditions are met:

- The listed subsidiary is a wholly owned subsidiary of the company by virtue of scheme of arrangement

- The listed subsidiary is a subsidiary of the company for a minimum of 3 years

- The listed subsidiary and the holding company should be in the same line of business

- The shares of listed subsidiary and the holding company should be listed on recognised stock exchange for a minimum of 3 years

- Votes casted by public shareholders of listed subsidiary for delisting of securities should be 2 times in favour of the number of votes cast against it.

- The company should be compliance of provisions relating to scheme of arrangement under SEBI (LODR) Regulations, 2015

The process of Reverse Book Building is a price discovery mechanism in order to provide a price on which the public shareholders can exit from the company. Accordingly, the intent of exempting a wholly-owned listed subsidiary from undergoing the said mechanism seems logical by virtue of the fact that such a company will have a sole shareholder.

Disclosure by Informants under PIT Regulations

SEBI vide SEBI (PIT) (Third Amendment) Regulations, 2019 had introduced Chapter III under the existing PIT Regulations providing for a mechanism to submit by a person, a voluntary information with SEBI about alleged violation of insider trading laws. The procedural requirements to be followed by an informant while submitting the information with SEBI have been provided in the said chapter along with the format of the disclosure prescribed under Schedule D of the Regulations.

The aforesaid provisions however do not provide for any limitation period for submitting such an information with SEBI. Accordingly, SEBI has decided to provide for a time period of 3 years. The manner of calculating the said period shall come clear only once the amended text is released. Further, the Meeting approved to make changes in Schedule D of the Regulations so as to require informants to specifically disclose details such as:

- Details of securities;

- Trades by suspect;

- UPSI based on which insider trading is alleged;

Disclosure of forensic audit by listed entities

SEBI has in the past ordered forensic audit for various companies, however, there was no requirement of disclosing the same by the company to the investors at large, except if considered material by the company under Part B of Schedule III of SEBI (LODR) Regulations, 2015. Accordingly, SEBI at its Board Meeting has decided to direct companies to disclose initiation and submit report of forensic audit along with comments of management to the stock exchange without applying any test of materiality.

Though it is not clear as of now, however, it seems that SEBI will introduce this disclosure requirement as an amendment to Schedule III Part A Para A of SEBI (LODR) Regulations, 2015 as it is to be disclosed by the company without applying any test of materiality i.e. deemed to be material.

SEBI intends to bring transparency for investors especially public investor holding larger interest in listed entities to have information about lapses in the company, which otherwise was not being disclosed by the company. SEBI requires every listed entity to disclose following w.r.t. forensic audit:

- Initiation of forensic audit along with name of entity initiating forensic audit along with reasons, if any

- Final forensic audit report on receipt by the listed entity along with comments of the management.

Adding Strain to Injury: Amendments impose Additional procedural requirements for insolvency applications

–Megha Mittal

On 24th September, 2020, the Ministry of Corporate Affairs notified the Insolvency and Bankruptcy (Application to Adjudicating Authority) (Amendment) Rules, 2020 (“Amendment Rules”)[1] in exercise of its powers under section 239 of the Insolvency and Bankruptcy Code, 2016 (“Code”), thereby requiring an advance copy of all applications filed before under section 7, 9 or 10 of the Code, to be served to the Corporate Debtor and the Insolvency and Bankruptcy Board of India (“IBBI”).

By way of the said Amendment Rules, it is now required that-

- An application intended to be filed under section 7, 9 or 10, has to be served to the Corporate Debtor and the Board, prior to filing before the Adjudicating Authority (“AA”)

- The application filed before the AA must contain a proof of service to the Corporate Debtor and the Board;

- Disclosure by the Insolvency Professional (IP) with respect to the ongoing assignments at the time of filing;

- The application to be filed by the Operational Creditor must contain a certificate by the bank/ financial institution, where the creditor has its accounts, with respect to the sums which have been received by the Operational Creditor from the Corporate Debtor.

In this Article, we analyse the Amendment Rules, more specifically the requirement of advance notice, and its implications.

Service of the Application- ensuring a fair chance to be heard

NCLT and Principles of Natural Justice

The NCLT is a quasi-judicial body, constituted under section 408 of the Companies Act, 2013, and is subject to powers and duties set out under the National Company Tribunal Rules, 2016, as well as the Companies Act- One such duty is to ensure that the Rules of Natural Justice are abided by[2].

The Rules of Natural Justice, viz, (i) Rules against bias[3]; and (ii) the right to be heard[4] are not derived from any statute or constitution- it is based on common and moral law to ensure there is no contempt of justice. One of the components of the right to be heard is a “proper notice”, which ensures that the person who would be affected upon filing of the application is given notice of such filing to show cause against the proposed action. As such, whenever an application is filed, under any statute, or before any authority, it is a pre-requisite to serve an advance copy to the respondent.

Hence, the requirement to serve an advance copy of the application, to the corporate debtor existed prior to the Amendment Rules.

Additional service upon IBBI

The Amendment Rules now provide that an advance copy of the application has to be served on the Board as well, which in the humble view of the Author, seems to be a superfluous requirement.

First, the Central Government (MCA) has failed to provide any stated objectives or purpose behind such a requirement. While it may be argued that the same is for ensuring proper records and data, it must be noted that those applications which are eventually admitted, are anyway required to be informed to Board. The extant reporting requirement under the IBBI (Insolvency Process for Corporate Persons), Regulations, 2016 (“CIRP Regulations”), inter-alia intimation to IBBI in Form A, disclosure requirements forms CIRP-1, already ensure that sufficient information is provided to the Board to execute its functions as such.

However, if the objective behind such additional requirement was merely record keeping, the same could have also been provided for by integration or a simple cross-linking process with the already existing data rooms, from where the regulatory bodies may extract information as and when required. For instance, the e-filing portal of NCLT may make necessary arrangements such that once an application is filed on the portal, the information regarding such filing is simultaneously given to the Board.

Such a set-up would not only fulfil the understandable objective behind the Amendment Rules, but only waive off this additional burden levied upon the applicants. This would also be in concurrence with consistent suggestions of stakeholders towards creation of a common repository of data related to the Code.

It further remains unanswered whether in case of any supplementary filing and/ or rectified filing upon directions of the Bench, such advance service would be required again? In absence of any stated objective behind such Amendments, it would be difficult to comment if at all such re-servicing of a copy of the application would be required.

Readers may recall that a similar requirement of impleading the MCA in all applications filed under the Code was made mandatory by an order of the Hon’ble NCLT, Principal Bench, dated 22.11.2019[5] but later on nullified by an over-ruling order of the Appellate Tribunal[6] as one leading to duplicity of information and records. Similarly, the requirement of advance notice to the Board seems to be of a similar nature, and hence, in view of the Author, should not be added as a mandate.

Other Amendments

In addition to the service requirements as discussed above, the Amendment Rules also introduce further reporting obligations on the IPs and the Operational Creditors- the same has been discussed herein below-

Reporting of ongoing assignments by IPs

The Amendment Regulations, by way of an additional clause in Form 2, now requires that while giving consent to act as an RP, the Insolvency Professional must disclose the number of ongoing assignments that s/he has undertaking as on the day of filing of application.

In view of the Author, while the same is not required as information of similar nature is already required to be provided in Form IP-1. Hence, the same may be removed for the sake of brevity.

Obtaining Certificate by Banks/ Financial Institutions

As per Form 5 under Rule 6, of the NCLT Rules, an application filed by an operational creditor, other than creditors having their account with a foreign bank/ institution, must annex a copy of the relevant accounts from the banks/financial institutions maintaining accounts of the operational creditor confirming that there is no payment of the relevant unpaid operational debt by the operational debtor,if available.

Hence, the operational creditors could simply self-certify their bank statements and submit the same on affidavit, as being a part of the application.

However, the Amendment Rules have substituted the above requirement with a new form, namely Form 5A, which is a certificate required to be obtained from the bank/ financial institution that the amount for which the application is being filed, has not been received by the creditor.

The Author is of the view that the said requirement would only lead to needless complication and delays. This would not only impose an additional requirement upon the creditors, but would also burden the banks/ financial institutions who may receive requests for such certificate in large volumes. Hence, it is suggested that the earlier modus shall continue, and the requirement of such certificate may be done away with.

Further, it is also pertinent to note that recent amendment in section 4 of the Code, whereby the minimum default amount for filing an application under the Code, was increased from Rs. 1 lakhs to Rs. 1 crore already led to a massive sweep-out of OCs from the purview of IBC. Further procedural burden, for example requirement of a bank certificate, would only make recourse a tougher for the OCs.

Implications

From the discussion above, we can gather that a common element through-out the Amendment Rules is increased disclosure/ reporting/procedural requirements. The Author humbly states that while the consistent efforts of the Government and Board, and the common suggestions from the stakeholders has been directed towards easing the superfluous, more-than-needed reporting and disclosure requirement, the Amendment Rules come as a complete deviation.

While the objectives, purpose of advance service is neither explicitly stated not implied from the text, it must be noted that the same is not a substitution of existing regulations, but an additional requirement for concerns already covered. The Amendments infact lead to elongated procedures, which do not serve any additional purpose.

In this pretext the Author is of the humble view that the Amendment Rules do not provide any ease, clarification and/ or assistance in the filing process. As such, the Central Government may consider a roll-back of the same.

[1] https://www.ibbi.gov.in/uploads/legalframwork/27e336abe5b5328297a2ba5b35b39fac.pdf

[2] Sec 424 (1) of the Companies Act, 2013

[3] Nemo judex causa in sua

[4] Audi Alteram Partem

[5] Read our views on this order, in our article- https://vinodkothari.com/2019/11/mandatory-impleadment-of-mca-as-a-respondent/

[6] By an order dated 22.05.2020

Eligibility and disclosures under rights issue rationalized

– Qasim Saif, Executive

Background

SEBI has on 23rd September 2020 released a press release[1] intimating about amendments to be made in SEBI ICDR Regulations, 2018 (“ICDR Regulations”/ “Regulations”) 2018. Further, on 28th September 2020, SEBI issued a notification bringing the SEBI (ICDR) (Fourth Amendment) Regulations, 2020[2] (“Amendment”) which was notified in official gazette on 1st October 2020. The Amendment is specifically focused for matters in relation to rights issue by listed entities. Several changes have been made which includes increasing the threshold for applicability, truncated disclosures in the letter of offer, removing the requirement for appointing a compliance officer, etc. At various places, the amendment is for the purpose of clarification or straightening of language of the Regulations.

In this article we have discussed the major amendments along with the probable impact.

Areas for amendments

1. Increase in issue size for checking applicability

Erstwhile, ICDR Regulations were applicable in case of a rights issue for a size exceeding INR 10 crores. Further, the draft letter of offer (“draft LOF”) in such cases is required to be filled with SEBI for its observations. In other cases, i.e. where the issue size is less than INR10 crores the letter of offer (“LOF”) is to be filled with SEBI for information and dissemination on the SEBI’s website in accordance with Regulation 3. As a matter of temporary relaxation, SEBI vide its Circular dated 21st April, 2020 (April Circular) increased the aforesaid threshold to INR 25 crore for issues opening on or before March, 2020.

By virtue of the Amendment, the limit of INR 10 crores under Regulation 3 has been increased to INR 50 crores. This would mean that while the general conditions and compliance will now be applicable to issue size of INR 50 crore or more, listed companies with a lower issue size will be required to file the LOF with SEBI for informative purpose.

As a result of the Amendment, while the applicability threshold has been increased, however, the companies with a lower issue size are still required to prepare the LOF in terms of the requirements of the ICDR Regulations and file the same with SEBI. Accordingly, while the change will surely be of relief to the entities which are now outside the applicability these Regulations, however, preparation of the LOF in terms of these Regulations will still be required.

Further to this, it should also be noted that practically filling of draft LOF for the purpose of obtaining observations from SEBI and then making prescribed changes generally takes several months. Accordingly, now since many entities will not be required to take the observations from SEBI, the same should help entities raise funds faster.

2. Relaxation in eligibility to make right issue, for members of promoter group and promoter or director of company who are director in entities, which were earlier debarred by SEBI

Regulation 61 of ICDR Regulations state that an issuer shall not be eligible to make a rights issue of specified securities:

a) if the issuer, any of its promoters, promoter group or directors of the issuer are debarred from accessing the capital market by the Board;

b)if any of the promoters or directors of the issuer is a promoter or director of any other company which is debarred from accessing the capital market by the Board.

c) if any of its promoters or directors is a fugitive economic offender.

Further, explanation to the said Regulations state that “the restrictions under (a) and (b) above will not apply to the promoters or directors of the issuer who were debarred in the past by the Board and the period of debarment is already over as on the date of filing of the draft letter of offer.”

However, the language of the said explanation did not cover promoter group or other entities where the promoter or director of the issuer holds similar and which is debarred by SEBI. This lacuna in the language of the existing text gives an impression to result in a permanent restriction on right issue if the members of the promoter group were debarred or unless the concerned person vacated the post in the other entity which was debarred by SEBI from accessing the capital market.

The explanation shall now read as follows “the restrictions under (a) and (b) above will not apply to the persons or entities mentioned therein who were debarred in the past by the Board and the period of debarment is already over as on the date of filing of the draft letter of offer.” After the amendment, all the mentioned persons or entities are now covered under the explanation and hence on completion of period of debarment, the issuer shall be eligible to undertake the right issue.

The above amendment is much needed clarification in the language rather than a relaxation

3. Firm arrangement towards 75% of finance of capital expenditures only

Regulation 62 (1) (c) of ICDR Regulations require that issuer shall make firm arrangements of finance through verifiable means towards seventy five per cent of the stated means of finance for the specific project proposed to be funded from right issue, excluding the amount to be raised through the proposed rights issue or through existing identifiable internal accruals.

The Amendment introduces an explanation to the said clause stating “For the purpose of this regulation ‘finance for the specific project’ shall mean finance of capital expenditures only.”

The addition of explanation provides a clarity on calculation of amount that the company has to make firm arrangement for. The explanation also provides a simplification in compliance, as in most projects the capital expenditure are highly predictable unlike revenue expenditure that vary significantly and may not be estimated accurately.

4. Removing the requirement to appoint a Compliance officer.

The Regulation 69 (8) of the ICDR Regulations require appointment of Compliance Officer by the issuer who shall be responsible for monitoring the compliance of the securities laws and for redressal of investors’ grievances. The said regulation has been omitted by the amendments.

Further the name of Part IV of Chapter III of ICDR Regulations has been suitably changed from “Appointment of Lead Managers, Other Intermediaries and Compliance Officer” to “Appointment of Lead Managers and Other Intermediaries”

Removing the requirement to appoint a compliance officer is a much needed amendment since the lead manager/ designated lead manager to the issue is any way required to ensure compliance with several applicable laws. Accordingly, it was a redundant practice to designate a compliance officer separately for a rights issue.

5. Changes in Disclosure requirements

Regulation 70 of ICDR Regulations require that certain disclosure be made under LOF and Draft LOF. The SEBI has proposed that specified entities shall be required to make disclosures in format provided under Part A or Part-B of Schedule VI.

Disclosure requirements under Part B of Schedule VI have been rationalized to avoid duplication of information in LOF, especially the information which is already available in public domain and is disclosed by the companies in compliance with the disclosure requirements under SEBI listing regulations.

However, the Issuer not fulfilling the conditions above will be required to make disclosures in the format given in Part B-1 of Schedule VI, the disclosures in Part B-1 would be more detailed than that in Part B, however it shall be truncated as compared to Part A, that is applicable for IPO or FPO.

The Part-B of Schedule VI states that following entities shall be eligible to make disclosers under the given format –

1) Issuer has been filing periodic reports, statements and information in compliance with listing regulations for the last one year (instead of the last three years as required earlier) immediately preceding the date of filing Draft LOF or LOF as the case may be.

2) Statement above shall be available on website of Stock Exchanges.

3) the issuer has investor grievance-handling mechanism which includes meeting of the Stakeholders’ Relationship Committee at frequent intervals, appropriate delegation of power by the board of directors of the issuer as regards share transfer and clearly laid down systems and procedures for timely and satisfactory redressed of investor grievances

The mentioned rationalization of disclosures would not only save the listed entities from duplication of task of providing same information that is already disclosed repeatedly but will also ease the accessing of reports by the stakeholders. The decluttering of the disclosures would be beneficial for all, Issuer, investor as well as regulators.

6. Relaxation in Minimum 90% subscription criteria

Regulation 86(1) of ICDR Regulations require that the minimum subscription to be received in the right issue shall be at least ninety per cent of the offer through the offer document, the said limit was temporally relaxed to 75% by the April Circular.

The amendment proposes to remove mandatory requirement of minimum 90% subscription in case the issue is for the purpose of financing other than capital expenditure for a project, provided that the promoters undertake to subscribe fully to their portion of rights entitlement.

The said relaxation should help the issuers looking for financing their business by right issue, specifically for general financing needs of business. The condition that the promoters would be needed to subscribe their entitlements completely would help safeguard the interest of other subscribers.

7. Application in plain paper to contain all the disclosures under the ICDR Regulations

Regulation 78 of ICDR Regulation allow shareholders to make application on plain paper in case he/she has not received application from for the right issue. SEBI has included a proviso to the regulation stating that “SCSBs shall accept such application forms only if all details required for making the application as per these regulations are specified in the plain paper application”.

On a general basis an application form contains following details to be entered by the shareholder-

– Name of Issuer

– Name and address of the Equity Shareholder including joint holders;

– Registered Folio Number/DP and Client ID no.;

– Number of Equity Shares held as on Record Date;

– Number of Rights Equity Shares entitled to;

– Number of Rights Equity Shares applied for;

– Number of additional Rights Equity Shares applied for, if any;

– Total number of Rights Equity Shares applied for;

– Total amount paid

– Particulars of cheque/demand draft;

– Savings/Current Account Number and name and address of the bank where the Equity Shareholder will be etc.

8. FTRI in case of pending Show Cause Notice

Regulation 99 of the ICDR Regulations provide for eligibility criteria for Fast Track Rights Issue (FTRI). FTRI is a faster method of raising funds through right issue whereby the issuer is not required to file draft LOF to SEBI for observations, this makes the process of right issue comparatively faster, enabling issuer to get funds faster.

Clause (h) of the aforesaid regulation restricts the rights issue in case show cause notice have been issued or prosecution proceedings have been initiated by the Board and pending against the issuer or its promoters or whole-time directors.

The amendment provides that the above clause shall now exclude the cases where notice is issued in regards to proceedings for imposition of penalty. However it shall be necessary that disclosures along with potential adverse impact on the issuer are made in the letter of offer.

The said amendment would help compliant companies against whom SCN is issued for violations that are not of serious nature and require only imposition of penalty. As discussed FTRI facilitates faster and cheaper raising of finance by the company, the relaxation would promote the companies to undertake right issue for fund raising activities.

Conclusion

Rights issue has been constantly gaining popularity in India with corporate giants such as Reliance Industries, Shriram Transport Finance and Bajaj electrical have chosen the same as a way to raise funds during the pandemic. In order to promote the right issue as a way of raising funds and ease the funding for listed companies the SEBI has made the amendment.

The Amendments are in the directions to make the offer by way of rights issue easier and do away with disclosures or compliance requirements which were duplicated or redundant. Further, the relaxation in minimum subscription and eligibility criteria for FTRI should come to the rescue of the listed entities to raise funds in the times when most businesses are facing liquidity issues.

[1] https://www.sebi.gov.in/sebiweb/home/HomeAction.do?doListing=yes&sid=6&ssid=23&smid=0

[2] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/sep-2020/1601363043311.pdf#page=1&zoom=page-width,-16,610

Our related write ups can be viewed here-

https://vinodkothari.com/2020/04/highlights-of-sebis-temporary-relaxations-for-rights-issue/

https://vinodkothari.com/2020/04/mof-amends-fdi-norms-for-rights-issue-and-insurance-sector/

[1] https://www.sebi.gov.in/sebiweb/home/HomeAction.do?doListing=yes&sid=6&ssid=23&smid=0

[2] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/sep-2020/1601363043311.pdf

Valuation approaches and methods

Abhirup Ghosh

| Approach | Method | Description | Application |

| Cost/ Asset based approach | Replacement cost method | This method is based on the concept of replacement i.e. Similar Utility. It considers the cost involved in replacing the assets of the Company at the same level on the date of valuation as the value of the Business of the Company. It is also known as substantial value. | · The subject company is not directly income generating or application of income approach or market approach is not feasible.

· The basis of value used in valuation assignment is dependent on the cost approach. E.g. replacement value, liquidation value. · For checking the reasonableness of the value derived from other approaches. |

| Reproduction cost method | In this approach the value of the Company is the cost involved in creating the exact replica of the subject Company from scratch as on the date of valuation. | ||

| Summation method | It is also called as the Underlying assets approach. Summation Method involves the separate valuation of each category or component of assets of the subject Company. The total value of the subject Company is the additive sum (therefore the name summation) of the values of the individual asset categories. Whatever categories of assets are encompassed in the subject Company are summed (or added in) the summation valuation. | ||

| Net assets value method/ Book value method | Here the book value assets and liabilities are considered. The liabilities and fictitious assets are reduced from the total assets arrive at the net assets value of the Company. This value is also equivalent to the net worth of the Company. | ||

| Adjusted net asset value method | A variation of the NAV method. Here the assets and liabilities are adjusted and considered at their fair values instead of their book values. | ||

| Market approach | Comparable company method | Here the value of a company is evaluated by using trading multiples derived from publicly traded companies like the subject Company.

Some common multiples used for valuing a company under this method are:

· Price to sales Multiple · Price Earnings Ratio · Price to Book Value · EV/Sales · EV/EBITDA |

· Subject Asset or Similar asset is actively publicly traded.

· Subject assets or substantially similar asset has been sold transaction appropriate for consideration under basis of value. · There are recent / frequent transactions in substantially similar assets. |

| Comparable transaction method | In this method the value is derived based on pricing metrics of mergers and acquisitions involving controlling interests in companies (public and private) in the same or similar line of business as the subject company. | ||

| Income approach | Capitalisation of earnings method | In this method, the past profits of the Company are capitalized at expected return on equity. Also known as Profit Earning Capacity Value. Alternatively, instead of the capitalization at the expected return on equity, the PE multiple is also applied to arrive at the value of the Company. | Can be applied where there is no market comparable for the subject company. |

| Discounted cash flow method | Under Discounted cash flow (DCF) Method, the total value of a business is calculated as the present value of its expected future cash flows over the projected period and present value of terminal value / Cash flows i.e. the free cash flows are discounted by an appropriate discounting factor. Under DCF method, two variants are used to value a company and its equity one is free cash flow to the firm (FCFF) and other is free cash flow to equity (FCFE). |

Related wrote-ups:

Sec 29A in the Post-COVID World- To stay or not to stay

-Megha Mittal

If the Insolvency and Bankruptcy Code, 2016 (‘Code’) is the car driving the ailing companies on road to revival, resolution plans are the wheels- Essentially designed to explore revival opportunities for an ailing entity, the Code invites potential resolution applicants to come forward and submit resolution plans.

Generally perceived as an alluring investment opportunity, resolution plans enable interested parties to acquire businesses at considerably reduced values. An indispensable aspect of these Resolution Plans, however, is the applicability of section 29A, which restricts several classes of entities, including ex-promoters of the corporate debtor, from becoming resolution applicants- for the very simple purpose of preventing re-possession of the corporate debtor at discounted rates. Hence, section 29A is seen as a crucial safeguard in revival of the corporate debtor, in its true sense.

In the present times, however, we cannot overlook the fact that the unprecedented COVID disruption, has compelled regulators around the globe, to reconsider the applicability and continuity of several laws, including those considered as significant; and one such provision is section 29A of the Code.

In a recent paper “Indian Banks: A Time to Reform?” dated 21st September,2020, the authors, Viral V Archarya and Raghuram G. Rajan, the former Deputy Governor and Governor of the Reserve Bank of India, have discussed banking sector reforms in view of the COVID disruption, calling for privatisation of Public Sector Banks, setting up of a ‘Bad Bank’[1] amongst other suggested reforms. In the said Paper, they also suggest that “for post-COVID NCLT cases to allow the original borrower to retain control, with the restructuring agreed with all creditors further blessed by the court. Another alternative might be to allow the original borrower to also bid in the NCLT-run auction”- thereby setting a stage for holding back applicability of section 29A in the post COVID world.

In this article, the author makes a humble attempt to analyse the feasibility and viability of doing-away with section 29A in the post-COVID world.

Stop crazy lending, lazy lending, write Rajan and Acharya

– Vinod Kothari

Raghuram Rajan and Viral Acharya, both having got the first-hand experience of holding the reins at the RBI, have prescribed several urgent measures to restore the health of the banking system. Neither do we have the fiscal space to support the banking system with fresh doses of capital, nor can we afford any more spikes in the almost top-of-the-world GNPA ratios. The duo, who have written several articles in the past, wrote this piece[1] on 21st Sept. 2020.

In a strongly worded write-up, the two celebrated academics of the financial world, have clearly taken it out on the bureaucracy and the government. The authors say while advocacy for comprehensive banking sector reforms have been done in the past, the onus of not making it happen is clearly on the government itself: “There are strong interests against change, which is why many would-be reformers are cynical, and either have given up, or recommend revolutionary change that has little chance of being implemented. We are more optimistic that a middle road is achievable, given that the greatest stumbling block has been the government, the bureaucracy, and the interests within it. With the enormous strains on government finances from the slow growth pre-COVID and the subsequent effects of the pandemic, the country has to transform the banking

sector from being a drain on government resources and an impediment to growth to becoming an engine of growth. This will not happen through incremental reforms. The status quo is fiscally untenable.”

The authors are unsparing when they clearly say the Department of Financial Services should be scrapped. The authors recommend that “Winding down Department of Financial Services in the Ministry of Finance is essential, both as an affirmative signal of the intent to grant bank boards and management independence and as a commitment not to engage in “mission creep” when compulsions arise to use banks for serving costly social or political objectives.” They also say that despite clear recommendations of the Nayak Committee in 2014[2], nothing has changed in terms of autonomy of the banks in the country. The authors may be resonating the bitterness of many senior bankers when they say: “Parliamentarians of all parties are not immune to the lure of public sector banks – the banks are often asked to arrange the logistics for their fact-finding committee meetings in enjoyable locales across the country. And Finance Ministry bureaucrats are reluctant to let go of the power that allows a young joint secretary to order the chairpersons of national banks around”

No more crazy lending, lazy lending

Banks in India cannot afford to have the false sense of having safe assets by “lazy lending”. The term, coined by Dr Rakesh Mohan, the-then Deputy Governor of RBI[3], refers to bankers choosing to invest in risk-free government bonds, even when the opportunity cost of capital for them is much higher. At the same time, banks also cannot afford to do “crazy lending”, by lending to riskiest of borrowers as more credit-worthy borrowers choose to rely on capital markets, and thereby, pile up non-performing loans on their balance sheets.

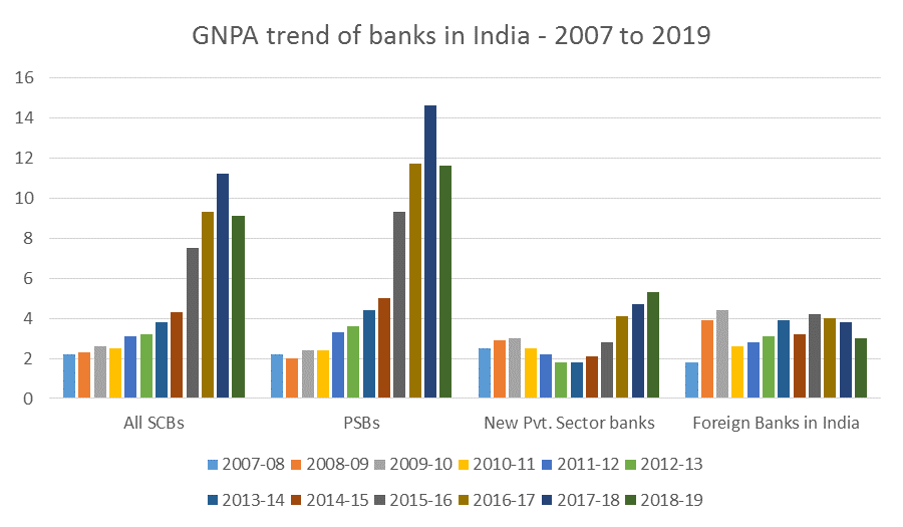

Indian banks, particularly PSUs, have managed to pile up bad loans on their balance sheet. There were sizeable NPAs even before the Covid. Six months of covid-moratorium meant virtually no cashflows, and as the servicing burden on the borrowers has increased over these months, most banks will be forced to use the loan restructuring option following covid-disruption[4]. The contention that the covid-disruption will become the alibi to restructure loans that were even otherwise fragile does not require much evidencing.

Source: Handbook of statistics on the Indian Economy, 2019-20[5]

Rajan and Acharya refer to the well-known ever-greening problem of Indian banking – with the bankers supporting bad loans by sequential doses of further lending, and the promoters continuously stripping the assets out and diverting profits and cashflows, leaving the borrower to be a “zombie”. Authors say that banks, by keeping the zombies alive, do a double damage to the system – on one hand, the bankers continue to focus on bad loan management and therefore, spend less time and resources to creating healthy loans, and on the other, the presence of half-dead firms discourages healthy industries as well.

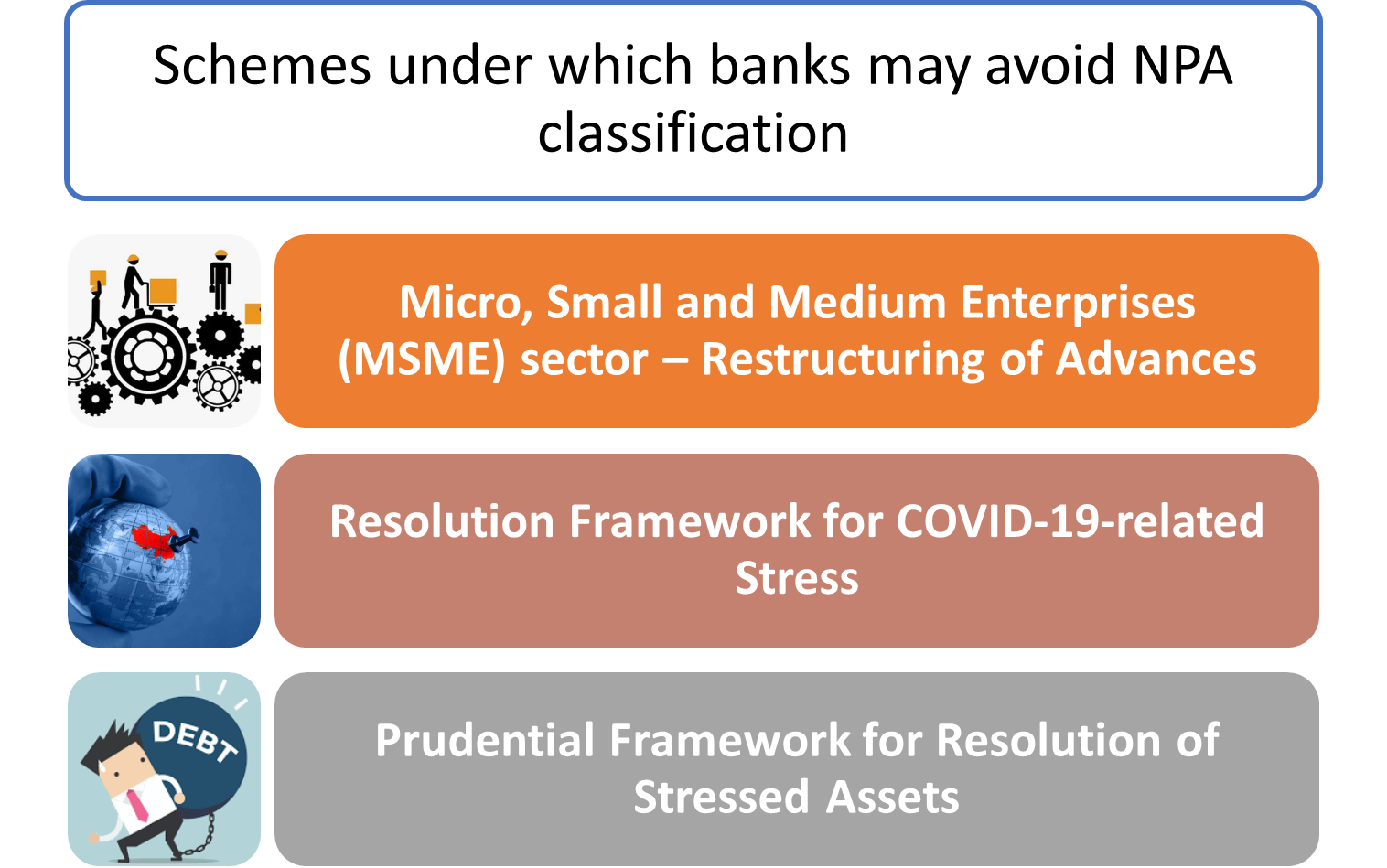

While banks over the world have converged to IFRS, which provides for an “expected loss” model, the Indian banking system is still driven by the regulatory requirement of provisioning, in form of the so-called IRAC (Income recognition and asset classification) norms. However, periodically, the RBI comes with schemes whereby banks can avoid classifying a loan as an NPA.

“With forbearance in the form of delayed provisioning, not only does the firm’s condition deteriorate, but the banker has to take a large loss when he eventually restructures the loan. So instead the banker holds off, under-provisioning mounts, and what was meant to be temporary regulatory forbearance inevitably creates banker demand for more, near-permanent forbearance”, say the authors. The authors say that fear-struck bankers are more comfortable in letting the NCLT process take over the bankers’ resolution, since, in that case, the decisions are made by the NCLT-appointed professional, and not by the bank, who may thus get sheltered by the proverbial 3 Cs that haunt bankers.

Arguing for the need to revisit sec. 29A of the Insolvency Code, Rajan and Acharya say that the provision are needed at the time when the defaulting borrower was to be prevented from buying bank his own assets and potentially scaring other buyers. But in the present scenario of pandemic stress, this will also prevent the promoter whose business faltered for no fault of his. The authors also reflect the reality when the say the NCLT “already has a large backlog of cases, some of which have dragged on for much longer than the targeted duration for bankruptcy. It cannot possibly handle the volume of distress that will have to be dealt with post-pandemic without a significant expansion of the number of its judges and benches. Unfortunately, the quantum of trained personnel that is needed may simply not exist.”

The authors also advocate the retention of the debtors’ control, at least in the post-pandemic restructurings. Notably, the creditors’ in control model that India has adopted, is inspired by the UK approach, whereas the USA has a debtor-in-control approach.

The authors are also in favour of a larger predominance of out-of-court resolutions: “Ideally though, there should be greater use of out-of-court restructuring and the NCLT should be used to stamp the out-of-court restructuring with legal finality. Only if an out-of-court restructuring could not be agreed upon between the creditors and the borrower would the firm be forced into a bankruptcy auction. The shadow of bankruptcy would then improve the ease and quality of the negotiation out of bankruptcy, as it does in other countries. But this requires bankers, especially public sector bankers, to be able to negotiate”

Creation of “bad bank”

The bad bank experience has had a limited success in India. IDBI created SASF in 2004. However, neither did it help the bad loans, nor IDBI. Subsequently, India has worked on a private sector model of so-called “bad banks”, in form of the ARCs. However, the transfer of loans to ARCs may mostly take the form of security receipts, which is paper-for-paper. It is only in the recent past that banks have insisted on all-cash loan transfers.

Hence, authors argue that what may be more effective is a transparent market for bad loans. Notably, the draft Directions for Sale of Loans, issued by the RBI for public comments on 08th June, 2020[6], provided, among other things, an auction-based disposal of bad loans. There is apparently also a discussion on permitting foreign investors to invest in bad loans directly.

Additionally, the authors also suggest the creation of a “public credit registry”. Currently, there are multiple registries in India working with significant overlaps and lack of cohesiveness. CERSAI, NeSL, and CRILC are such registries, each intended to serve different purposes. However, it will not be a high hanging fruit to combine them into a loan registry, where the information about a loan, its collateral, performance, etc. are all pooled into a single database. Authors say that KAMCO, Korea, after completion of its asset management task, is now evolving itself into a loan registry.

Authors suggest that selling of loans will bring transparency and price discovery. Currently, RBI’s regulatory framework has been restraining banks from selling loans, mainly on the concerns of originate-to-hold model.

The authors contend that if a transparent pricing could emerge by creating a secondary market, a bad bank could emerge by the market mechanism itself. These market-based bad banks can have sectoral focus, rather than a generic pool of NPAs as is currently the case. The authors also cite global examples of warehousing bad loans to find a more opportune time for disposing them.

Move from asset-based lending to cashflow-based lending

Lending can be, as it traditionally has been, focused on the on-balance sheet assets and collateral, or may be focused on the cashflows of the business. In case of asset-based lending, the lender focuses on balance sheet ratios such as leverage and loan-to-value. In cash-flow based lending approach, the lender focuses on liquidity and debt-servicing ability.

An RBI Expert Group led by Shri U K Sinha recommended a cash-flow based lending structure for MSME funding[7].

Recently, large Indian banks announced plans to move to cashflow-based lending, such as SBI. SBI Chairman Rajnish Kumar stated “SBI will switch to a cash flow-based lending model beginning April 2020 from a mechanism where loans are given against assets”[8].

The authors have recommended a transition from asset based lending to (also) cash flow based lending. The authors mention that “Banks could rely more on loan covenants for large borrowers, tied to liquidity and leverage ratios (instead of lending purely against assets). This would set up “trip wire” points for enhancing loan collateralization, rather than requiring it from the beginning; in case of small borrowers, reliance on GST invoices and utility payment bills, among other cashflow information, can facilitate such a transition.”

Group-lending limits

The authors talk about the problem relating to certain promoters running large conglomerates while sitting on thin slices of equity. Due to this the following problems are highlighted by the authors, namely, a) this creates systemic risk in the banking system, b) leads to concentration of corporate power and a complex maze of related party transactions between financial and real subsidiaries of the group that are often the veil behind which frauds are perpetrated.

The authors recommend that highly indebted groups should not be allowed to expand their footprint significantly by using bank money to bid on new projects. Group lending norms should be enforced as the economy recovers. Further, the authors state that aggregate permissible system exposures should be linked to the aggregate debt equity ratio for the group (including non-bank borrowing and foreign borrowing). Over-leveraging by specific promoters or groups needs to be limited if the Indian banking system’s health is to be restored.

[1] https://faculty.chicagobooth.edu/-/media/faculty/raghuram-rajan/research/papers/paper-on-banking-sector-reforms-rr-va-final.pdf

[2] https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/BCF090514FR.pdf

[3] https://www.rbi.org.in/scripts/BS_SpeechesView.aspx?Id=310

[4] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11941&Mode=0

Our write up & FAQs on the framework may be viewed here: https://vinodkothari.com/2020/08/resolution-framework-for-covid-19-related-stress-resfracors/

https://vinodkothari.com/2020/09/faqs-on-resolution-of-loan-accounts-under-covid-19-stress/

[5] https://rbidocs.rbi.org.in/rdocs/Publications/PDFs/58TB5A66F26A72F460687373406F1D51C43.PDF

[6] https://www.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=957

[7] https://www.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=924

[8] https://www.financialexpress.com/industry/banking-finance/sbi-to-shift-to-cash-flow-based-lending-by-april-2020/1797095/