Appraising post IPO governance requirements

Appraising post IPO governance requirements

Other ‘I am the best’ presentations can be viewed here

Our other relevant resources –

Other ‘I am the best’ presentations can be viewed here

Our other relevant resources –

Other ‘I am the best’ presentations can be viewed here

Other ‘I am the best’ presentations can be viewed here

Our other resources on related topics –

Yutika Lohia

yutika@vinodkothari.com

In today’s time, leasing has become an indispensable element of businesses – Any and every asset movable or immovable, equipment or software can be taken on lease. Colloquially, lease refers to an arrangement where a property owned by one is given for use by another, against regular rentals. In India, there are two types of lease transactions-financial lease and operating lease. Typically, a financial lease is a disguised financial transaction whereas operating lease is akin to rental contracts.

While leasing has gained much importance and relevance over the years, its feasibility and viability depends a major deal on its tax implications – they could easily make or break the deal. The technical aspects with respect to taxation on implementation makes it all the more significant. Issues like depreciation, lease rentals, tax deduction at source and exposure to GST are key concerns. Further, though leases are classified as finance or operating, it is important to note that such distinction is essentially from an accounting perspective – the Income Tax Act, 1961, however, does not distinguish between the two.

A rather significant but overlooked aspect of leasing is the ‘tax deduction at source’ (‘TDS’). As is known TDS is a key element of the Indian taxation framework which aims to collect tax at the source of generation of income. In case of a lease transaction, the lessee is required to deduct tax under 194-I of the Income Tax Act at the time of payment of lease rentals to the lessor.

While there are several judicial precedents dealing with TDS vis-à-vis lease transactions, the Hon’ble High Court of Karnataka in a recent order, in the case of Commissioner of Income Tax vs. Texas Instruments India Pvt Ltd (2021),[1] concluded that in case of a financial lease, the lease financing company did not provide any particular service as a driver or otherwise for the purpose of usage of the car. The only transaction entered between the assessee and the lease financing company was to make payments of the amount due to the company. To say there was a mere financing arrangement and therefore section 194-I of the IT Act shall not be applicable in case of a financial lease transaction.

In this article we shall discuss the above stated ruling in detail.

The Assessee, Texas Instruments India Pvt Ltd being in the business of manufacture and export of computer software had taken motor vehicle on finance lease for its employees. It considered the lease rentals as business expenditure and claimed deduction of the same under the head income from business and profession. TDS was not deducted on the finance lease rentals as the assessee contested that the same did not fall under the provision of section 194-I or 194-C of the IT Act.

However, the Assessing Officer disallowed the claimed expenditure on the grounds that the lease rentals were being paid to the vendor under the contract and therefore the payment/ expenses would be attracting the provisions of section 194-C.

Aggrieved by the order of the A.O., the Assessee preferred an appeal before to the CIT(A). Upon such appeal, the CIT(A) overturned the A.O’s order and held that the payments made by assessee were not in the nature of service rendered by the leasing company for the carriage of goods or passengers. The CIT(A) also held that the assets were in the disposition of the Assessee.

Following such order, the matter was appealed before the Income tax Appellate Tribunal (ITAT) where it was held that provisions of Section 194-C will not be applicable on lease rentals.

Once again, the matter was taken for appeal before the Hon’ble Karnataka High Court where it was held that the leasing financing company did not provide any particular service as a driver or otherwise for the purpose of usage of car. The maintenance was carried by the employees of the assessee. The only transaction entered between the assessee and the leasing company was to make payments of the amount due to the company. Since no services were being provided by the leasing company and is a mere financing agreement, provisions of section 194-C and 194-I shall not be applicable.

Section 194-I of the IT Act 1961 governs tax deduction at source in case of lease rentals. As already mentioned, Income Tax Act does not draw any line of distinction between financial lease and operating lease, let us understand whether TDS needs to deducted on lease rentals in case of both financial lease and operating lease.

Section 194-I of the IT Act explains rent as follows:

“rent” means any payment, by whatever name called, under any lease, sub-lease, tenancy or any other agreement or arrangement for the use of (either separately or together) any

(a) land; or

(b) building (including factory building); or

(c) land appurtenant to a building (including factory building); or

(d) machinery; or

(e) plant; or

(f) equipment; or

(g) furniture; or

(h) fittings,

whether or not any or all of the above are owned by the payee;

Rent has been broadly defined under section 194-I and shall be applicable when asset is given for use for any payment under lease, sub lease, tenancy, or any other arrangement or agreement.

(1) Any person responsible for paying any sum to any resident (hereafter in this section referred to as the contractor) for carrying out any work (including supply of labour for carrying out any work) in pursuance of a contract between the contractor and a specified person shall, at the time of credit of such sum to the account of the contractor or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct an amount equal to—

(i) one per cent where the payment is being made or credit is being given to an individual or a Hindu undivided family;

(ii) two per cent where the payment is being made or credit is being given to a person other than an individual or a Hindu undivided family,

of such sum as income-tax on income comprised therein.

XX

The judgement highlights that by virtue of the fact that no services were provided by the leasing company and that it was a mere financing agreement, section 194-C and 194-I would not be applicable in the given case.

Therefore, it seeks attention on the fact whether TDS has to be deducted on financial lease rentals.

Also, one must contemplate whether TDS should have been deducted under section 194-A of the IT Act as the lease transaction was considered as a mere finance agreement. This remains unanswered.

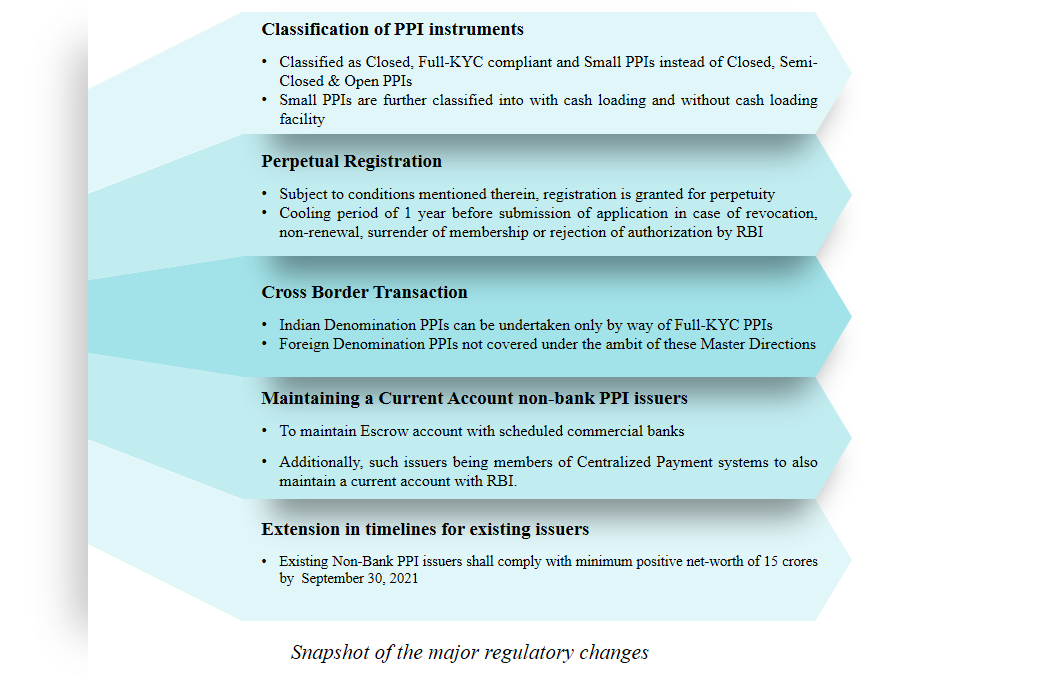

The Reserve Bank of India (RBI) on August 27, 2021, issued the Master Directions on Prepaid Payment Instruments[1] (‘Master Directions’) repealing the Master Directions on Issuance and Operation of Prepaid Payment Instruments[2] (‘Erstwhile Master Directions’) with immediate effect. These Master Directions have been issued keeping in mind the recent updates to the Erstwhile Master Directions.

In this write-up we aim to cover the major regulatory changes brought about by the Master Directions.

The Erstwhile Master Directions classified PPIs into three categories namely closed ended PPIs which could be issued by anyone and required no RBI approval, semi-closed PPIs and open ended PPIs which could be issued only by Banks. The new Master Directions have also classified PPIs in three categories i.e. Closed-ended PPI, Small PPIs and Full-KYC PPIs. However, since closed-ended PPIs are not a part of the payment and settlement system, they are not regulated by the RBI. A brief snapshot of the nature of the other two types of PPIs is presented below:

| Basis | Small PPI | Full KYC PPIs | |

| With cash loading facility | Without cash loading facility | ||

| Issuer | Banks and non-banks after obtaining minimum details of PPI holder (mobile number verified with OTP; self-declaration of name and unique identity/identification number of any OVD) | Banks and non-banks after completing KYC of holder | |

| Identification Process | Verification of mobile number through an OTP

Self-declaration of name and unique identify number of any OVD as recognized in KYC Master Directions |

Video-based Customer Identification Process | |

| Nature of PPI | Reloadable and can be issued in electronic form.

Electronic payment transactions have been divided into two categories- transactions that do not require physical PPIs and those which require. Hence, even cards could be issued. |

Reloadable and can be issued in card or electronic form.

Loading/Reloading shall be from a bank account / credit card / full-KYC PPI.

|

Reloadable and can be issued in electronic form.

Electronic payment transactions have been divided into two categories- transactions that do not require physical PPIs and those which require. Hence, even cards could be issued. |

| Maximum amount that can be loaded | In a month: INR 10,000

In a year: INR 120,000 |

No maximum limits | |

| Maximum outstanding amount at any point of time | INR 10,000 | INR 200,000 | |

| Limit on debit during a month | INR 10,000 per month | No limit | No limit |

| Usage of funds | For purchase of goods and services only.

Cash withdrawal or fund transfer not permitted

|

Transfer to source or bank account of PPI holder, other PPIs, debit or credit card permitted subject to:

Pre-registered benefit – maximum INR 200,000 per month per beneficiary

Other cases – maximum INR 10,000 |

|

| Cash Withdrawal | Not permitted | Permitted subject to limits:

INR 2000 per transaction and INR 10,000 per month |

|

| Conversion | To be converted into full-KYC PPIs within a period of 24 months from the date of issue of the PPI. | Small PPI with cash loading can be converted into Small PPI without cash loading, if desired by the PPI holder. | Not applicable |

| Restriction on issuance to a single person | Cannot be issued to same person using the same mobile number and same minimum details more than once. | No such restriction | No such restriction |

| Closure | Funds transferred back to source or Holders bank account after complying with KYC norms

|

Funds transferred to pre-designated bank account or

PPIs of the same issuer |

|

The concept of ‘Small PPI’ and ‘Full-KYC PPI’ cannot be said to be a new introduction, rather, it is more of a merger of the existing variety of semi closed PPIs in Small PPI and the open ended PPI to Full KYC PPI. However, an important change that has been inserted is the recognition of non-bank PPI issuers to issue Full KYC PPI, who were earlier not allowed to issue open ended PPIs.

2. Validity of Registration

Earlier, the Certificate of Authorisation was valid for five years unless otherwise specified and was subject to review including cancellation of the same. However, under the Master Directions, the authorisation is granted for perpetuity (even for existing authorisation which becomes due for renewal) subject to compliance with the following conditions:

Also, the concept of ‘cooling period’ was introduced in December 2020[3], for effective utilisation of regulatory resources. PPI issuer whose CoA is revoked or not-renewed for any reason; or CoA is voluntarily surrendered for any reason; or application for authorisation has been rejected by RBI; or new entities that are set-up by promoters involved in any of the above categories; will have a one year cooling period. During the said cooling period, entities shall be prohibited from submission of applications for operating any payment system under the PSS Act.

3. Cross border transactions in Indian denomination

The Erstwhile Master Directions provided that Cross Border Transactions in INR denominated PPIS was allowed only by way of KYC compliant semi-closed and open PPIs which met the conditions specified therein. However, under the Master Directions, such issuances have been permitted only in the form of Full-KYC PPI and other conditions as prescribed earlier have not been altered.

4. Maintenance of Current Account

Apart from maintaining an escrow account with a scheduled commercial bank, non-bank PPI issuer that is a member of the Centralised Payment Systems operated by RBI i.e. non-bank issuers as covered under Master Directions on Access Criteria for Payment Systems[4] which have been allowed to access Real Time Gross Settlement (RTGS) System and National Electronic Fund Transfer (NEFT) Systems and any other such systems as provided by RBI, shall also be required to maintain a current account with the RBI.

Transfer from and to such current account is permitted to be credited or debited from the escrow account maintained by the PPIs.

5. Ensuring additional safety norms

6. Miscellaneous

7. Effect on existing issuers

The timeline for complying with the minimum positive net-worth of 15 crores by non-bank PPI issuers has been extended and shall now be met with by September 30, 2021 instead of March 31, 2020. Non-bank issuers shall submit the provisional balance sheet indicating the positive net-worth and CA certificate to the RBI on or before October 30, 2021, failing which they may not be permitted to carry on their business.

In this write-up we have aimed to cover the gist of changes introduced in the Master Directions as compared to the Erstwhile Master Directions. The changes made in the regulatory framework for the PPIs have created a level playing field for banks and non-banks, especially, with respect to issuance of full KYC PPIs. Comparatively, the new directions are way more liberal than the earlier one, which only indicates how bullish the regulator must be with respect to PPIs.

[1] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12156#MD

[2] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11142

[3] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=12001&Mode=0

[4] MD51170116C65788DE8A564165B74D5FECE0626A73.PDF (rbi.org.in)

Other ‘I am the best’ presentations can be viewed here

Our other resources on related topics –