Further relaxations by SEBI due to Covid-19– third in a row!

Vinod Kothari & Company

corplaw@vinodkothari.com

Vinod Kothari & Company

corplaw@vinodkothari.com

-Kanakprabha Jethani (kanak@vinodkothari.com)

With the COVID-19 disruption taking a toll on the world, almost two billion people – close to a third of the world’s population being restricted to their homes, businesses being locked-down and work-from home becoming a need of the hour; “contactless” business is what the world is looking forward to. The new business jargon “contactless” means that the entire transaction is being done digitally, without requiring any of the parties to the transaction interact physically. While it is not possible to completely digitise all business sectors, however, complete digitisation of certain financial services is well achievable.

With continuous innovations being brought up, financial market has already witnessed a shift from transactions involving huge amount of paper-work to paperless transactions. The next steps are headed towards contactless transactions.

The following write-up intends to provide an introduction to how financial market got digitised, what were the by-products of digitisation, impact of digitisation on financial markets, specifically FinTech lending segment and the way forward.

Digitisation is preparing financial market for the future, where every transaction will be contactless. Financial entities and service providers have already taken steps to facilitate the entire transaction without any physical intervention. Needless to say, the benefits of digitisation to the financial market are evident in the form of cost-efficiency, time-saving, expanded outreach and innovation to name a few.

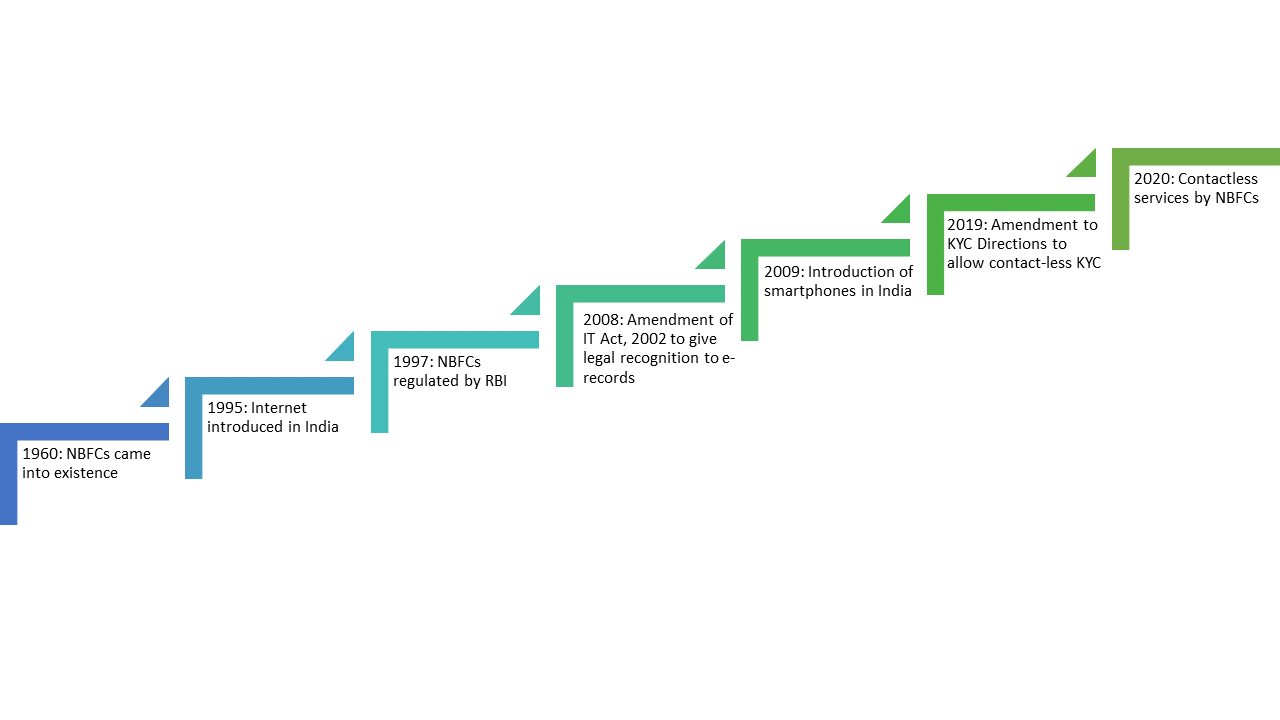

Before delving into how financial entities are turning contactless, let us understand the past and present of the financial entities. The process of digitisation leads to conversion of anything and everything into information i.e. digital signals. The entire process has been a long journey, having its roots way back in 1995, when the Internet was first operated in India followed by the first use of the mobile phones in 2002 and then in 2009 the first smartphones came into being used. It is each of these stages that has evolved into this all-pervasive concept called digitisation.

The process of digitization has seen various phases. The financial market, specifically, the NBFCs have gone through various phases before completely guzzling down digitization. The journey of NBFCs from over the table executions to providing completely contactless services has been shown in the figure below:

Before analysing the impact of digitisation on the financial market, it is important to understand the concept of ‘paperless’ and ‘contactless’ transactions. In layman terms, paperless transactions are those which do not involve execution of any physical documents but physical interaction of the parties for purposes such as identity verification is required. The documents are executed online via electronic or digital signature or through by way of click wrap agreements.

In case of contactless transactions, the documents are executed online and identity verification is also carried out through processes such as video based identification and verification. There is no physical interaction between parties involved in the transaction.

The following table analyses the impact of digitisation on financial transactions by demarcating the steps in a lending process through physical, paperless and contactless modes:

| Stages | Physical process | Paperless process | Contactless process |

| Sourcing the customer | The officer of NBFC interacts with prospective applicants | The website, app or platform (‘Platform’) reaches out to the public to attract customers or the AI based system may target just the prospective customers | Same as paperless process |

| Understanding needs of the customer | The authorised representative speaks to the prospects to understand their financial needs | The Platform provides the prospects with information relating to various products or the AI system may track and identify the needs | Same as paperless process |

| Suggesting a financial product | Based on the needs the officer suggests a suitable product | Based on the analysis of customer data, the system suggests suitable product | Same as paperless process |

| Customer on-boarding | Customer on-boarding is done upon issue of sanction letter | The basic details of customer are obtained for on-boarding on the Platform | Same as paperless process |

| Customer identification | The customer details and documents are identified by the officer during initial meetings | Customer Identification is done by matching the details provided by customer with the physical copy of documents | Digital processes such as Video KYC are used carry out customer identification |

| Customer due-diligence | Background check of customer is done based on the available information and that obtained from the customer and credit information bureaus | Information from Credit Information Agencies, social profiles of customer, tracking of communications and other AI methods etc. are used to carry out due diligence | Same as paperless process |

| Customer acceptance | On signing of formal agreement | By clicking acceptance buttons such as ‘I agree’ on the Platform or execution through digital/electronic signature | Same as paperless process |

| Extending the loan | The loan amount is deposited in the customer’s bank account | The loan amount is credited to the wallet, bank account or prepaid cards etc., as the case may be | Same as paperless process |

| Servicing the loan | The authorised representatives ensures that the loan is serviced | Recovery efforts are made through nudges on Platform. Physical interaction is the last resort | Same as paperless process. However, physical interaction for recovery may not be desirable. |

| Customer data maintenance | After the relationship is ended, physical files are maintained | Cloud-based information systems are the common practice | Same as paperless process |

The outcome of digitisation of the financial markets in India, was a land of opportunities for those operating in financial market, it has also wiped off those who couldn’t keep pace with technological growth. Survival, in financial market, is driven by the ability to cope with rapid technological advancements. The impact of digitisation on financial market, specifically lending related services, can be analysed in the following phases:

With mobile density in India reaching to 88.90% in 2019[1], the adoption of digital payments have accelerated in India, showing a rapid growth at a CAGR of 42% in value of digital payments. The value of digital payments to GDP rose to 862% in the FY 2018-19.

Simultaneously, of the total payments made up to Nov 2018, in India, the value of cash payments stood at a mere 19%. The shift from cash payments to digital payments has opened new avenues for financial service providers.

With everything coming online, and the demand for digital money rising, the need for service providers has also taken birth. Services for transitioning to digital business models and then for operating them are a basic need for FinTech entities and thus, there is a need for various kinds of service providers at different stages.

When payments system came online, financial service providers looked for newer ways of expanding their business. But the market was already operating in its own comfortable state. To disrupt this market and bring in something new, the FinTech service providers introduced the idea of easy credit to the market. When the market got attracted to this idea, digital lending products were introduced. With time, add-ons such as backing by guarantee, indemnity, FLDG etc. were also introduced to these products.

Consequent to digital commercialization, the need for payment service providers also generated automatically and thus, leading to the demand for digital payment products.

With digitization of non-banking financial activities, many players have found a place for themselves in financial markets and around. While the NBFCs went digital, the advent of digitization also became the entry gate to other service providers such as:

In order to enable NBFCs to provide financial services digitally, platform service providers floated digital platforms wherein all the functions relating to a financial transaction, ranging from sourcing of the customer, obtaining KYC information, collating credit information to servicing of the customer etc.

Such service providers operate on a business model that offers software solutions over the internet, charging their customers based on the usage of the software. Many of the FinTech based NBFCs have turned to such software providers for operating their business on digital platforms. Such service providers also provide specific software for credit score analysis, loan process automation and fraud detection etc.

For facilitating transactions in digital mode, it is important that the flow of money is also digitized. Due to this, the demand for payment services such as payments through cards, UPI, e-cash, wallets, digital cash etc. has risen. This demand has created a new segment of service providers in the financial sector.

NBFCs usually enter into partnerships with platform service providers or purchase software from SaaS providers to digitize their business.

The recent years have witnessed unimaginable developments in the FinTech sector. Innovations introduced in the recent times have given birth to newer models of business in India. The ability to undertake paperless and contactless transactions has urged NBFCs to achieve Pan India presence. The government has been keen in bringing about a digital revolution in the country and has been coming up with incentives in forms of various schemes for those who shift their business to digital platforms. Regulators have constantly been involved in recognising digital terminology and concepts legally.

In Indian context, innovation has moved forward hand-in-hand with regulation[2]. The Reserve Bank of India, being the regulator of financial market, has been a key enabler of the digital revolution. The RBI, in its endeavor to support digital transactions has introduced many reforms, the key pillars amongst which are – e-KYC (Know Your Customer), e-Signature, Unified Payment Interface (UPI), Electronic NACH facility and Central KYC Registry.

The regulators have also introduced the concept of Regulatory Sandbox[3] to provide innovative business models an opportunity to operate in real market situations without complying with the regulatory norms in order to establish viability of their innovation.

While these initiatives and providing legal recognition to electronic documents did bring in an era of paperless[4] financial transactions, the banking and non-banking segment of the market still involved physical interaction of the parties to a transaction for the purpose of identity verification. Even the digital KYC process specified by the regulator was also a physical process in disguise[5].

In January 2020, the RBI gave recognition to video KYC, transforming the paperless transactions to complete contactless space[6].

Further, the RBI is also considering a separate regime for regulation of FinTech entities, which would be based on risk-based regulation, ranging from “Disclosure” to “Light-Touch Regulation & Supervision” to a “Tight Regulation and Full-Fledged Supervision”.[7]

2019 has seen major revolutions in the FinTech space. Automation of lending process, Video KYC, voice based verification for payments, identity verification using biometrics, social profiling (as a factor of credit check) etc. have been innovations that has entirely transformed the way NBFCs work.

With technological developments becoming a regular thing, the FinTech space is yet to see the best of its innovations. A few innovations that may bring a roundabout change in the FinTech space are in-line and will soon be operable. Some of these are:

Digital business models have received whole-hearted acceptance from the financial market. Digitisation has also opened gates for different service providers to aid the financial market entities. Technology companies are engaged in constantly developing better tools to support such businesses and at the same time the regulators are providing legal recognition to technology and making contactless transactions an all-round success. This is just the foundation and the financial market is yet to see oodles of innovation.

[1] https://www.rbi.org.in/Scripts/PublicationsView.aspx?id=19417

[2] https://www.bis.org/publ/bppdf/bispap106.htm

[3] Our write on Regulatory Sandboxes can be referred here- https://vinodkothari.com/2019/04/safe-in-sandbox-india-provides-cocoon-to-fintech-start-ups/

[4] Paperless here means paperless digital financial transactions

[5] Our write-up on digital KYC process may be read here- https://vinodkothari.com/2019/08/introduction-of-digital-kyc/

[6]Our write-up on amendments to KYC Directions may be read here: https://vinodkothari.com/2020/01/kyc-goes-live-rbi-promotes-seamless-real-time-secured-audiovisual-interaction-with-customers/

[7] https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/WGFR68AA1890D7334D8F8F72CC2399A27F4A.PDF

–Megha Mittal & Shreya Jain

Frivolous initiation of insolvency process, merely for recovery of dues has been a persistent concern- catalyst being the seemingly low threshold of Rs.1,00,000/-.While murmurs about raising the threshold limit for initiating insolvency process have long been in the picture, the notification comes in the wake of recent outbreak of the novel COVID – 19 – the minimum default requirement now stands increased hundred times; from Rs. 1,00,000/- to Rs. 1,00,00,000.

Applicable from 24.03.2020, the Government, in exercise of its powers under section 4 of the Insolvency and Bankruptcy Code, 2016 (“Code”)[1] has specified Rs. 1,00,00,000 (Rupees One Crore) as the minimum amount of default for the purposes of triggering insolvency. Note that Rs. 1 Crore is the maximum threshold which the Central Government can prescribe under section 4.

The step has been widely touted as a relief for MSMEs in this time of crisis, however, this might have multiple implications. The authors have made a humble attempt to analyse its implications from a broader perspective, and if at such increase would be welcomed in absence of the ongoing crisis.

Vinod Kothari & Company

corplaw@vinodkothari.com

Vinod Kothari & Company

Below is a short snippet of the relaxed timelines issued by the securities market regulator in the wake of the disruption caused by COVID-19.

Team Vinod Kothari & Company | corplaw@vinodkothari.com

Updated on 29th March, 2020

Like all other public agencies, MCA has been taking a series of steps in the wake of the rapidly spreading COVID-19 and issued clarification[1] on spending of CSR funds for COVID 19 stating that the amount spent on COVID-19 by companies will count towards CSR spending. The activities falling under item nos. (i) & (xii) of Schedule VII of Companies Act, 2013 undertaken due to COVID 19 shall qualify as CSR activity which covers the following:

Subsequently, the Ministry on 28th March, 2020 has also clarified by way of an office memorandum, that companies contributing towards recently formed Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund (‘PM CARES Fund’) shall also qualify as CSR expenditure under item (viii) of Schedule VII of Companies Act, 2013.

Hence, this is the right occasion, and unarguably, one of the noblest causes, to use CSR funds in whatever way, one may think of for the welfare of society.

Notably, substantial CSR money remains unspent, very often for want of appropriate CSR projects. Many companies have to explain the same by finding some reason or the other. Currently the country is passing through an epidemic that has affected the whole world. Hence, companies may come forward and spend their unspent CSR budgets. Indeed companies are also welcome to over-spend this year’s budget pursuant to a proposal in the Companies Amendment Bill which permits carry forward of excess spending as well.

Questions are often being asked – can the company include the expenditure incurred for COVID-19 preparedness for its own employees and workmen – say, giving of masks, sanitizers, or similar expense, as a part of its CSR spending?

Our answer to this question is the same as what we have continuously answered as a part of our FAQs[2] on CSR that CSR is spending on a social cause. An employer spending for the well being, safety or welfare of employees is performing the employer’s legal or moral obligation. That cannot be regarded as CSR. However, if the company spends on COVID-19 preparedness, either by itself or through implementing agencies, for a wider section of public, and its employees or their families are also the beneficiaries of such an exercise, there is no denial as to eligibility of the same as CSR spending.

Our detailed write ups on CSR may be viewed here:

Draft CSR Rules Make CSR More Prescriptive

CAB, 2020: Bunch of Proposals for revamping CSR Framework

[1]http://www.mca.gov.in/Ministry/pdf/Covid_23032020.pdf

[2]https://vinodkothari.com/2019/11/faqs-on-corporate-social-responsibility/

Vinod Kothari and Company; corplaw@vinodkothari.com

Updated as on 23rd March, 2020

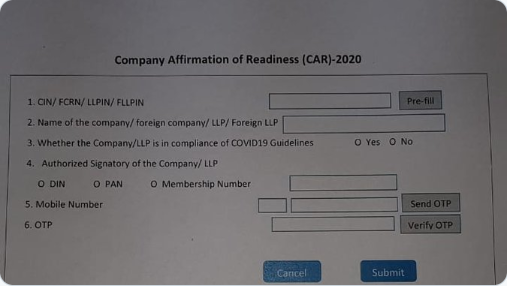

All companies and LLPs must have, by now, got mailers from the Ministry of Company Affairs about COVID-19 preparedness, and the need to file a web based form CAR 2020 i.e. Company Affirmation of Readiness towards COVID 19.

The MCA circular is nothing but a disaster management step from the Ministry, imploring upon all companies and LLPs to get sensitised to the need for handling this colossal challenge to humanity, India included. It will be an ironical travesty if the filing of the form is taken as a compliance requirement.

Therefore, in our view, what matters is the preparedness itself, not so much the task of having the so-called policy or the filing of the form itself.

However, the country has a few lakhs of companies, and the affirmation of preparedness by filing this form will be expected from all the companies. Hence, there is understandably a barrage of questions from clients and others.

We at Vinod Kothari & Company will be happy to contribute in our own little way; hence, if companies/LLPs have questions around this Form, we have thought it apt to put them down into this small guidance. We wish and pray that all of you stay safe during this challenging time.

Let us not even think of this as emanating from some power under the law. Neither do we have to search for such a power, nor question it. As human beings, not every action of ours arises out of legal obligations. It is a simple step by the Ministry towards sensitisation of the corporate sector, towards fulfilling an urgent social and human obligation.

Companies and LLPs are being advised to put in place an immediate plan to implement a ‘work from home’ policy as a temporary measure.

The object of having such a plan is to ensure social distancing as advised by WHO and other public health authorities in the recent outbreak of COVID-19 which is required for preventing the rapid spread and transmission of the disease at community level.

If there are no permanent employees, it is all peace as far as your company is concerned. Go and file the form and say you have taken necessary steps.

The Advisory suggests to have a plan to implement the work from home policy for the employees. In our view, the same is not required to be a written or formal policy. The word “policy” here should mean the steps to be taken by the organisation to provide the facility of working from home to its employees and the manner/ procedure to be followed to ensure the same. If there is a policy, typically, the policy is applied to all employees covered by it without discrimination. Further, the process and manner to be followed shall be different from organisation to organisation. Accordingly, in case of companies, the decision may be taken at management level, while in case of others, by the head of the organisation.

As we said above, we are not envisaging this to be a formal document. However, please do consider the following:

First of all, the actions expected are urgent – therefore, please do not wait for any formal processes or board resolutions. Whoever is in charge of putting administrative allocations may take such steps. Looking at the seriousness, it is expected that senior management is involved. However, it does not matter if there is any formal ratification or issue of circular, unless the organisation expects such formal internal documents.

8. Till what time the work from home policy to be adopted?

Till 31st March, 2020. The same shall be reviewed by the appropriate authorities based on the evolving situation.

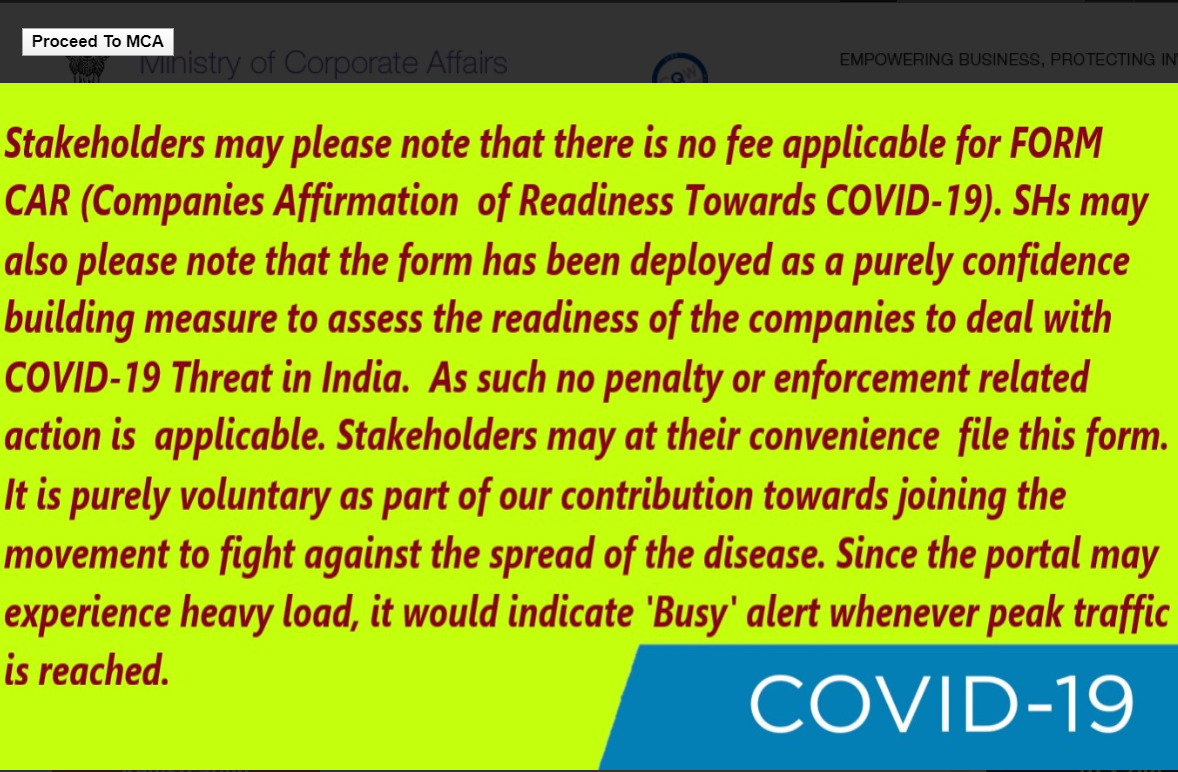

It is a web form deployed on 23rd March, 2020 by the Ministry. The same is a simple web based form requiring only an OTP based verification and does not require any digital signature for affirming or denying the adoption of work from home policy.

There is no fee for filing the form. Seriously, we don’t even imagine there can be a fee.

All companies and LLPs are expected to file the said form. There is no exclusion or exemption for OPCs, private companies or small companies. However, looking at the language of the applicability, partnership firms and proprietorship concerns have been kept outside the purview of filing CAR, 2020.

The web form CAR, 2020 is deployed on the MCA portal on 23rd March, 2020. Initially, the advice suggested to file it on the same day, however, later it was clarified that the same can be filed till 30th March, 2020.

As per the twitter handle of the Hon’ble Minister of Finance and Corporate Affairs the possible format of the form shall contain the following:

The step to step guide on filing CAR 2020 has been issued by MCA on 22nd March, 2020. The same can be viewed here.

The Advisory suggests all companies/ LLPs to file the form. The intent seems to include all the companies/ LLPs incorporated in India or companies/ LLPs not incorporated in India but having operations/ physical presence in India. The contents of the Form as provided in Query 9 above suggest the same.

There is no definition as such. However, it should mean the Advisory itself issued by the Govt. from time to time. One may refer to pages such as https://www.mygov.in/covid-19/?cbps=1.

As referred to above, it seems that the authorised signatory may be a director, CS, CFO or any other person authorised to file the form. However, who is eligible to give such authority is not clear. In our view, in case of companies which have given general authority to the CS/ any director/ CFO to file necessary forms with the regulatory authorities from time to time, such authorised persons may file the form. In case of others, the same may be filed by the MD/ head of the organisation who looks after the day to day affairs or any person authorised by such MD/ head of the organisation. Once again, we suggest there need not be a formal flow of authorisation, such as a resolution, for filing the form.

Since the form is an OTP verified form, the OTP is sent on the mobile no of the person who is authenticating the form and the same is prefilled on providing details of the authorised person.

There is no penalty for non-filing of the form. Further the Advisory is not coming from any statutory requirement but out of a social obligation only, non- filing of the same may not lead to any penal consequences.

The authorised signatory is not taking the burden upon himself. The signatory may, in turn, get confirmations from those who are involved, say, the HR head or similar positions.

Please note that shutdown does not mean shutdown of operation. Therefore, it still means work from home. The whole intent of shutdown is to control movement and not to control work.

As per the information uploaded on MCA’s website, the filing of the form is on voluntary basis. Therefore, the company/ LLP (s) may take a call on filing. However, if one throws a question on whether they are required to take steps to combat COVID-19 by following government guidelines, please note that we have no doubt on answering this is positive. Everyone including the companies and LLPs are mandatorily required to take steps during this health emergency.

Neha Gupta | finserv@vinodkothari.com

Loading…

Loading…

Vinita Nair | vinita@vinodkothari.com

Loading…