Watts to Wealth: NITI Aayog’s ₹45,500 Cr Securitisation Plan for power sector

Dayita Kanodia and Simrat Singh | Finserv@vinodkothari.com

Background

Under the National Monetisation Pipeline (NMP) 2.0, released on February 23, 2026 NITI Aayog has proposed securitisation of ₹45,500 crore of future cash flows in the power sector as part of the overall ₹16.72 lakh crore monetisation target for 5 year period FY 2026-FY 2030.

The NMP was introduced in 2021, which provided a framework to unlock value from brownfield and greenfield public-sector assets and reinvest these resources into new infrastructure creation. NMP 1.0 achieved 90% of its ₹6 Lakh Crores monetisation target in the 4 year period FY 2021 – FY 2025. Now, NMP 2.0 seeks to carry forward this vision with a higher target and greater reserve of assets.

NMP 2.0 seeks to use a wide range of monetisation modes for raising finance, including InvITs, PPP user models, disinvestment, IPOs, FPOs, Leasing, private placement of securities, securitisation etc.

Securitisation as a mode of monetisation

Securitisation is being envisaged for the power sector since the sector has predictable and stable revenue streams ideal for securitisation. Further, securitisation would be suitable for operational PSU assets that do not require developmental or major operational support. The identified asset classes and targets are:

- Operational hydro power stations of NHPC and SJVN – ₹12,000 crore;

- Power Guarantee Corporation of India Limited (PGCIL) transmission assets – ₹33,500 Crores;

Under NMP 2.0, for securitisation to be counted as monetisation, transactions must comply with certain guidelines, including the following:

- No charge on the PSU’s balance sheet;

- No corporate guarantee;

- Repayment backed solely by securitised cash flows;

- Escrow mechanism for cash flow ring-fencing;

- Proceeds earmarked for capex or debt reduction;

- First charge on cash flows to lenders, with residual cash flows retained by the PSU.

The securitisation proceeds will be retained by the respective PSUs and deployed towards capital expenditure and capacity addition.

Mechanics and Regulatory Considerations

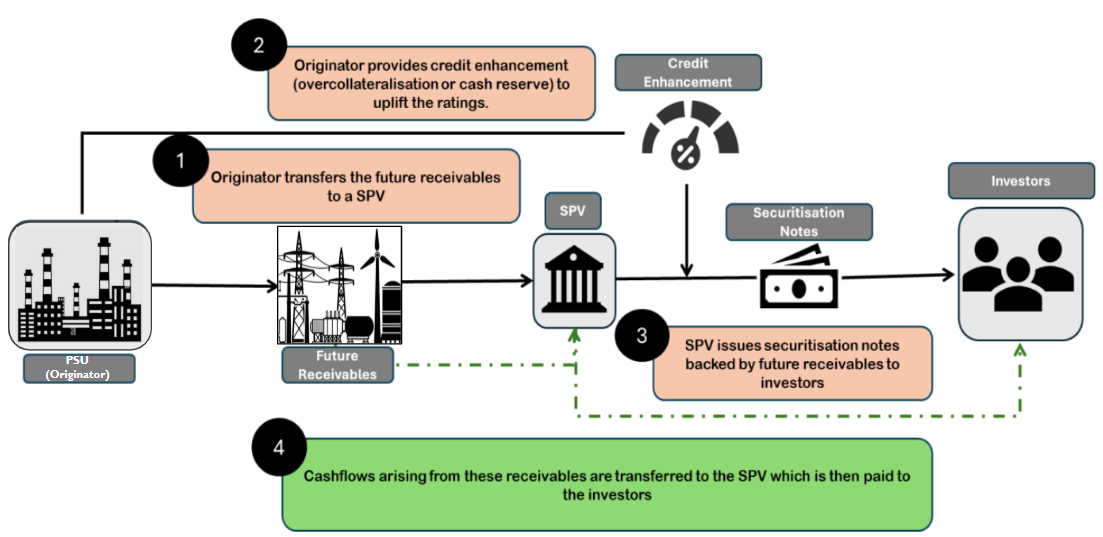

Securitisation under NMP 2.0 would essentially be a future flows securitisation; a topic we dealt with in our white paper. Under this, future cash flows are converted into tradable securities and the issuers can raise upfront capital from the issuance of these securities, effectively monetising their future income. The process generally involves the following steps:

- Identification of Future Receivables: The originator (which would be the PSU in the present case) identifies a pool of receivables expected to arise over time.

- Transfer to SPV: The rights to these future receivables are legally assigned or pledged to a bankruptcy-remote SPV. This separation ensures that the cash flows are shielded from the originator’s insolvency risk;

- Structuring and Credit Enhancement: The SPV issues securities backed by the expected future flows.

- Payment of interest and principal to the investors: The investors will need to be regularly serviced by cash flows generated from the underlying receivables. On maturity, the principal payments would also be made to the investors.

If the transaction is structured as per the conditions above, it may look like the following:

Typically the credit enhancement is overcollateralisation and structural credit enhancement by issuing multiple classes of notes (i.e. class A and B notes) is usually missing. There may be a DSRA/Cash reserve too to take care of any mismatches. See our write-up on future flows here.

Regulatory framework:

Future flow securitisation in India sits at the intersection of RBI and SEBI regulations, but does not fit neatly within either. The RBI’s SSA Directions apply only to RBI-regulated lenders (banks, NBFCs, financial institutions) and presuppose the transfer of existing financial assets. Therefore, securitisations under the NMP 2.0 where non-financial sector PSUs are involved will fall outside the SSA regime.

Further, in case capital market issuance or listing is contemplated, securitisation transactions fall under the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008.

However, post the 2025 amendments, SEBI has defined eligible “debt/receivables.” Under this definition, only specified categories (such as mortgage debt, leasing receivables, trade receivables, rental receivables, etc.) are currently permitted. Accordingly, the assets under NMP 2.0 will not fall under the definition of eligible assets as per the SEBI SDI Framework unless specifically notified by SEBI.

Further, conditions such as obligor track record requirements and minimum holding period norms designed for traditional loan securitisations may be structurally incompatible with pure future receivable structures.

It may be noted that it is essential for a securitisation transaction to fall within the purview of either RBI’s SSA Directions or the SEBI SDI Framework from the purview of taxation.

Taxation is governed by Section 115TCA of the Income Tax Act, 1961, which grants pass-through status to securitisation trusts created under the RBI SSA Directions or SEBI SDI Framework. Income received by investors is thus taxed as if they had directly earned the underlying income, ensuring single-level taxation.

Therefore, if a future flow securitisation falls outside both the RBI and SEBI frameworks, the SPV may be taxed under general trust taxation principles, potentially at the maximum marginal rate. This creates a material tax inefficiency. Accordingly, for future flow securitisation to be viable at scale, regulatory eligibility under the SEBI SDI framework and, thereby, access to Section 115TCA pass-through treatment becomes critical.

Further, it may also be noted that under the SSA Directions, for making any investment in securitisation transactions which are outside the purview of the SSA Directions, full capital will need to be maintained.

This discourages banks from making investments in securitisation transactions outside the purview of the SSA Directions.

Accordingly, for the success of NMP 2.0, the following two amendments are necessary:

- Amendment in the definition of eligible assets to permit future flows

- Necessary amendment in the SSA Directions to encourage bank participation in the securitisation notes issued by non-financial sector entities.

InvITs

InvITs are used to monetise mature and revenue-generating brownfield assets, primarily in the road and power transmission sector, by transferring them into a trust that raises capital from institutional and retail investors. The sponsoring PSU (eg. NHAI) receives upfront proceeds from units issued by the InvIT. See our whitepaper on infrastructure securitisation here.

Notably, the NMP 2.0 also proposes monetisation of approx ₹3,35,000 Crores worth of highway assets under the InvIT/TOT models. This would be done through NHIT or another similar publicly listed InvIT.

Three types of highway stretches are identified for this purpose, along with respective monetisation targets:

- Stretches where user fee is accruing to NHAI – ₹2,31,900 Crores;

- Projects at the end of their concession periods – ₹60,000 Crores; and

- Under-construction stretches where user fee will accrue to NHAI – ₹43,600 Crores.

Under the NMP, the total monetisation value under InvIT mode is calculated based on the market approach, i.e. funds raised by the InvIT against the underlying asset portfolio. In the case of highways, the proceeds from TOT and InvIT projects shall flow to NHAI and shall ultimately accrue to the Consolidated Fund of India.

Conclusion

Using future flow securitisation as a means for funding infrastructure has been common worldwide. Such transactions include the securitisation of metro ticket receivables in China, where the proceeds from the securitisation of future ticket receivables were used to repay the bank loans taken by the originator for building the metro infrastructure.1

Further, in Indonesia, toll road receivables were securitised to build the Jakarta-Bogor-Ciawi toll road.2

The NMP 2.0 proposes to use securitisation for financing. However, it is essential that necessary regulatory amendments be carried out to ensure sucess of this mode of financing and for promoting many more similar future projects.