SEBI’s Plethora of Proposals

– Sourish Kundu, Executive | corplaw@vinodkothari.com

Read More:

Subsidiaries to refer LODR definition of “related party” – going too far with relationships?

– Sourish Kundu, Executive | corplaw@vinodkothari.com

Read More:

Subsidiaries to refer LODR definition of “related party” – going too far with relationships?

– Team Corplaw | corplaw@vinodkothari.com

SEBI in its Board meeting dated December 18, 2024, has approved amendments pertaining to BRSR, HVDLEs, DTs, SMEs, Intermediaries, etc. This article gives a brief overview of the approved amendments.

Immediate actionables for Listed entities:

VKCo comments: In addition to the corresponding obligations on the issuer, CP also proposed to mandate Depositories and Stock exchanges to provide requisite information to DTs, which is yet to be approved. The right to call information from issuers and market participants including corresponding obligations on them will enable DTs to perform their functions efficiently.

VKCo comments: While the introduction of model DTD is appreciated, the draft model DTD proposed in the CP was not aligned with the general market practices followed by the DTs as well as the applicable laws such as SEBI Listing Regulations, NCS Regulations, Indian Trust Act, etc.

Under this segment of changes discussed by SEBI, most of the proposals are in alignment with the Consultation Paper dated 31st October, 2024, except for few changes in relation with PSUs coming together with public enterprises under Public Private Partnership.

VKCo Comments: The proposal to enhance the extant threshold is encouraging in terms of governing the maximum value of outstanding debt while at the same time achieving the same without bearing the burden of compliance by an increased number of purely debt listed entities. Subsequently, effective implementation of such a proposal aligns it with the identification criteria of Large Corporates.

VKCO Comments: While this proposal is noteworthy, however, instead of rolling out a new chapter, there could have been certain modifications in the existing regulations by way of a proviso to align with the needs of an HVDLE. Further, one also needs to wait to see the fine print -of the provisions once the same is issued.

VKCo Comments: The proposal is welcome since it clearly sets the HVDLEs free from the barrier of once an HVDLE so always an HVDLE. This proposal sets a clear nexus between the compliance and the size of the debt outstanding, for the protection of which in the very first place, the compliance triggered.

VKCo Comments: Given the close construct of debt listed entities, it is often observed that the constitution of such committees becomes more of a hardship than in smoothing compliance and discussing specific matters. Accordingly, it looks appropriate to redirect the functions of NRC and RMC to the Audit Committee and that of the SRC to the Board.

VKCo Comments: The rationale completely aligns with the proposal made and seems to be justified. Further, as far as the exclusion is concerned, this seems more from excluding those members who are part of the board not on the basis of their appointment but their current tenure being served in a particular position in the company.

VKCo Comments – While the CP suggested two ways of seeking approval for material RPTs of an HVDLE. The Board has only considered the alternative mode of first seeking NOC of DT and thereafter approaching the shareholders. Further, as discussed in our related write up on the CP, there does not seem to be any incentive to first approach the DT and thereafter the DT to approach the NCD holders. Instead the approval of the NCD holders can be taken up directly by the HVDLE.

VKCo Comments: The inclusion of a voluntary provision in the legislation with respect to a comprehensive report like BRSR is not likely to be submitted given the huge details under the BRSR. However, an opportunity to submit BRSR can be a game changer for an HVDLE from the perspective of being able to raise funds based on its reporting standards in this regard.

One of the changes discussed by the Board is relaxation to HVDLEs set up under the PPP mode from composition requirements of directors. While this was not a part of the CP, however, even if we have to understand that change proposed, this looks like relaxing the composition requirement of the Board of Directors.

CHANGES NOT APPROVED:

VKCo Comments: This proposal was with an objective to align and standardize the filing of quarterly CG compliance report for bringing parity as in the case of equity listed entities

VKCo Comments: While SEBI refers to the introduction of similar exclusion for equity listed entities, however, it has also mentioned the subsequent amendment wherein the same was omitted. The proposal not being notified is in alignment with the position of equity listed entities, however, the same would have been a welcome change since it would have helped such entities to give preference to their principal statutes and not an ancillary one like LODR.

Our detailed write up on the CP can be accessed here.

Refer to our discussion on CP in: Laundry List: SEBI’s proposal to elongate list of deemed UPSIs

– Vinod Kothari and Payal Agarwal | corplaw@vinodkothari.com

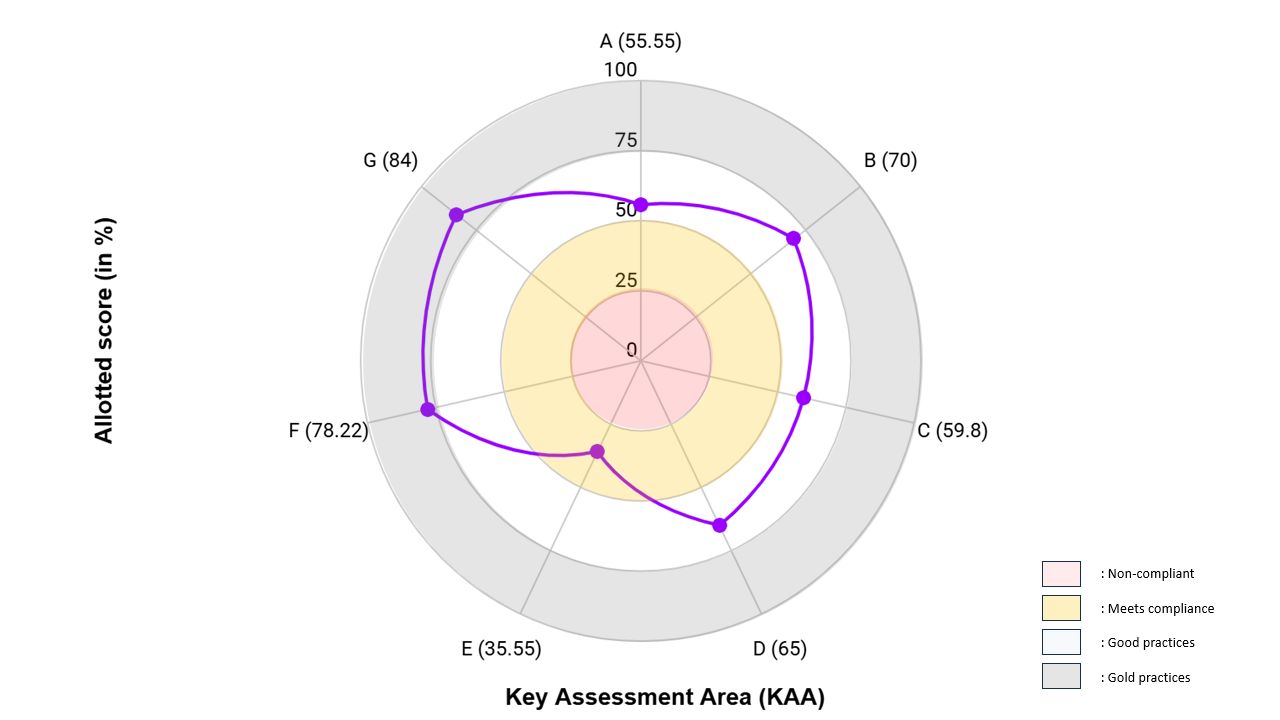

In risk assessment, effectiveness testing, compliance management, or other areas where qualitative assessment is required, one may be making abstract statements like: we have very effective controls; we have strong risk management practices; we have the best of the practices in compliance management, etc. However, very often, these may be pure abstractions. How do we use a structured approach which may allow us to give a more granular, methodical approach to benchmark ourselves?

Unlike quantitative parameters, there are no set methods or approaches to qualitative assessment. However, every qualitative assessment is also backed by identifying the elements that need to be studied, the ingredients or the check points in each of these elements, the weights of the respective elements in the overall assessment framework, assignment of scores based on the weights and observations for each of the checkpoints, eventually coming to an aggregate score. That is, a purely qualitative assessment may be converted into a score sheet.

One may create one’s own methodology; here is a suggested one. Before proceeding with the methodology, one may submit that the same methodology that may be used for effectiveness assessment may also be used for risk assessment. A good score in effectiveness is a positive indicator; a high score in risk assessment is a threat.

The suggested assessment methodology involves:

| Scoring Parameter | |

| Not compliant/ no practice exists for the same | 0 |

| Meeting minimum compliance/ practice | 1 |

| Good Practices (indicates industry practice) | 2 |

| Gold Practices (indicates leadership practices) | 3 |

| Check-points | Weights | Scores | Weighted Score |

| A1 | 3 (maximum) | 1 | 3 |

| A2 | 2 | 0 (minimum) | 0 |

| A3 | 3 | 3 (maximum) | 9 |

| A4 | 3 | 2 | 6 |

| A5 | 1 (minimum) | 2 | 2 |

| Total | 12 | 20 |

In the picture above, (0-25) is the area of non-compliance, depicting lapses in meeting the minimum legal requirements. (26-50) is the area of meeting the minimum compliance with law, (51-75) indicates that the company is moving towards the general industry practices, and a score beyond 75 shows that the company is adopting leadership practices in the respective compliance area.

A risk assessment chart may be similarly formed, wherein, a higher score indicates a higher level of risk. Also see an article on Compliance Risk Assessment.

Shaivi Bhamaria, Associate & Sakshi Patil, Executive | corplaw@vinodkothari.com

Loading…

Loading…

Refer to our related resources below:

Register your interest here – https://forms.gle/HGJxAb7e8ds2dMrF9

Our Related Resources:

Fill the google form to register here.

Loading…

Our resources on Insider Trading-

1. Mutual Fund units now under the net of insider trading regulations

2. FAQs on Insider Trading Framework for Mutual Funds

3. FAQs on Structured Digital Database

4. Prohibition of Insider Trading – Resource Centre

5. SEBI proposes to widen the definition of Connected Persons

Last updated on December 10, 2024

Team Corplaw | corplaw@vinodkothari.com

Loading…

Also, refer our resource on PIT here

Insider Trading Regulations amended in line with Consultation Paper

Heta Mehta | Executive | corplaw@vinodkothari.com

The concept of Trading Plan (‘TP’) that existed since May 2015 continued to remain unpopular due to the stringent conditions laid down in the Insider Trading Regulations. The framework was set to be reviewed based on empirical evidence and feedback post introduction and determine if SEBI needs to dilute or increase the regulatory requirement. In order to make it more realistic and captivating, SEBI’s Working Group suggested reforms vide Consultation Paper dated 24th November, 2023[1] that was approved by SEBI in its board meeting held on March 15, 2024. SEBI (Prohibition of Insider Trading) (Second Amendment) Regulations, 2024 notified on June 25, 2024 will be effective from September 24, 2024. As a concept, it is not unique to India, globally, both the US and UK have similar TP concepts with some or the other variations when compared to our legislation. This article discusses the amendments, including the rationale provided in the CP, relevant points discussed in the SEBI Board meeting and our analysis on the same.

Read more →Sanya Agrawal | corplaw@vinodkothari.com

Loading…

Our detailed article on the topic can be read here

Link to our PIT resource centre: https://vinodkothari.com/prohibition-of-insider-trading-resource-centre/

Anushka Vohra | Senior Manager

corplaw@vinodkothari.com

The SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’) impose certain restrictions and obligations on the DPs, one of which is contra trade restriction.

The DPs and their immediate relatives are restricted from entering into contra trade which refers to opposite trades executed viz. buy / sale within a shorter period of time usually within a period of 6 months with an intent to book short term profits. Where contra – trade is executed in violation of the restriction, the profit earned is to be disgorged for remittance to the IPEF.

In case of an individual DP (promoters / directors / etc. as recognized by the listed company), the immediate relatives also have certain obligations under the Regulations as their trades may be said to be influenced by the DPs. Similarly, in case of non-individual DPs (promoters), there may be other promoters and persons belonging to the promoter group who may act in concert with a particular non-individual promoter.

Having said that, it is important to understand the intent of contra trade, whether the same would apply individually on DPs based on trades executed against their PAN or the same would apply jointly on DPs and their immediate relatives or the entire promoter group inter-se. The same has been a matter of discussion in various Informal Guidance (‘IG’) of SEBI. We discuss the same briefly along with other illustrations.

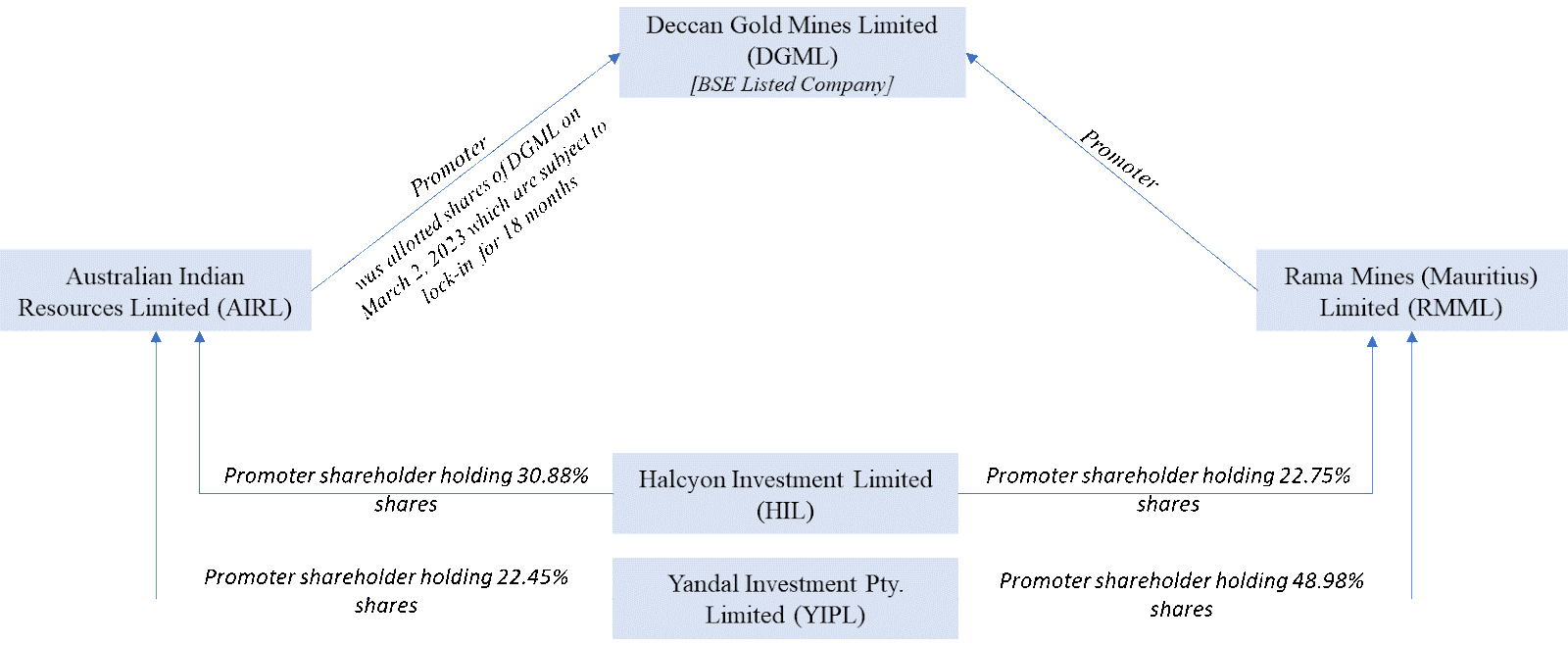

Generally, the concept of Persons Acting in Concert (‘PACs’) is used in the Takeover Code and under the PIT Regulations, the perspective so far has been PAN based. In the recent IG in the matter of Deccan Gold Mines Ltd[1], SEBI in its interpretative letter has given the view that contra trade restrictions would apply on the promoter group jointly, given the case in hand. The facts of the case have been represented diagrammatically below.

We see that the listed company is being held by two corporate promoters, which in turn are held by common shareholders. Here, RMML intended to sell its shareholding in open-market within 6 months of the allotment made to AIRL.

Since there is common control in both the promoter entities, it was stated that contra-trade restriction would apply jointly on both.

The intent of contra trade, as also mentioned above is to ensure that the persons who are privy to UPSI do not make short term profits in the securities of the listed company. For instance, if a DP has bought a security of the listed company in anticipation of a rise in prices that might be caused by the UPSI, such DP cannot sell such security within 6 months of the purchase. While trades can be executed by different DPs having different PAN, however where a single person is the “driving force” (as cited by the SAT in Shubhkam Ventures (I) Private Limited v. SEBI[2], it cannot be said that the persons acted in their individual capacity.

There have been instances in the past where SEBI has given the view that contra trade restrictions apply individually on DPs. The view seems to be supported by the interpretation of clause 10 of Schedule B of the Regulations, which states that:

The code of conduct shall specify the period, which in any event shall not be less than six months, within which a designated person who is permitted to trade shall not execute a contra trade. XXX

Previously, in 2020, in the matter of Raghav Commercial Ltd[3], SEBI in its interpretative letter took the view that the contra trade restrictions apply to trades made by promoters individually and not the entire promoter group.

Taking the case of individual DPs, in the matter of Star Cement Limited[4], while answering the question on applicability of contra trade restrictions – whether individually or to the entire promoter group, SEBI cited the above clause 10 stating that the same applies individually.

Reference of the above case was taken in 2019 in the matter of Arvind Limited[5], where contra trade restrictions were said to apply individually on DP through PAN, disregarding who took the trading decision. Our detailed article on the same can be read here.

The current case makes it quite clear that the facts of the case have to be considered to analyze whether there is a single person taking trading decision.

Let us take several other examples to understand the intent of contra trade.

1.

Whether Leg 2 will be contra to Leg1? Here we see that significant stake i.e. 50% is being held by Partner A (promoter of X Ltd) in the LLP. The trades of LLP can be said to be influenced by the decision of Partner A. This can be a case of common control and therefore Leg 2 becomes contra to Leg 1.

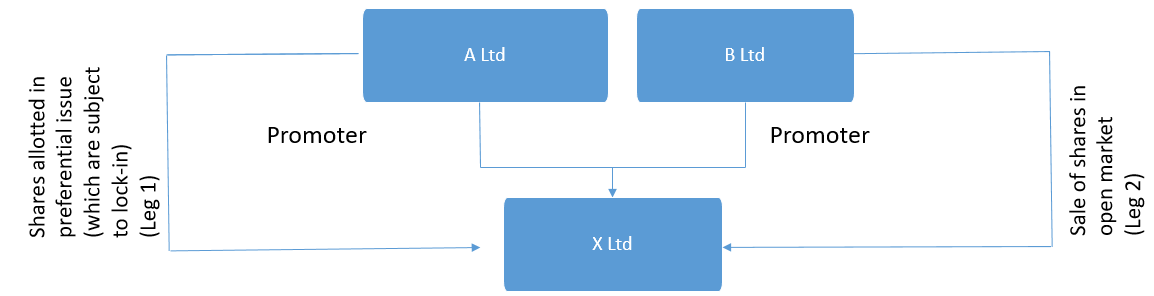

2.

In this case, we will have to see who is behind A Ltd and B Ltd. If both A Ltd and B Ltd are held by the same set of shareholders, Leg 2 would become contra to Leg 1.

Further, there are certain exemptions w.r.t. contra-trade restrictions that have been prescribed in the PIT Regulations and also in SEBI FAQs.

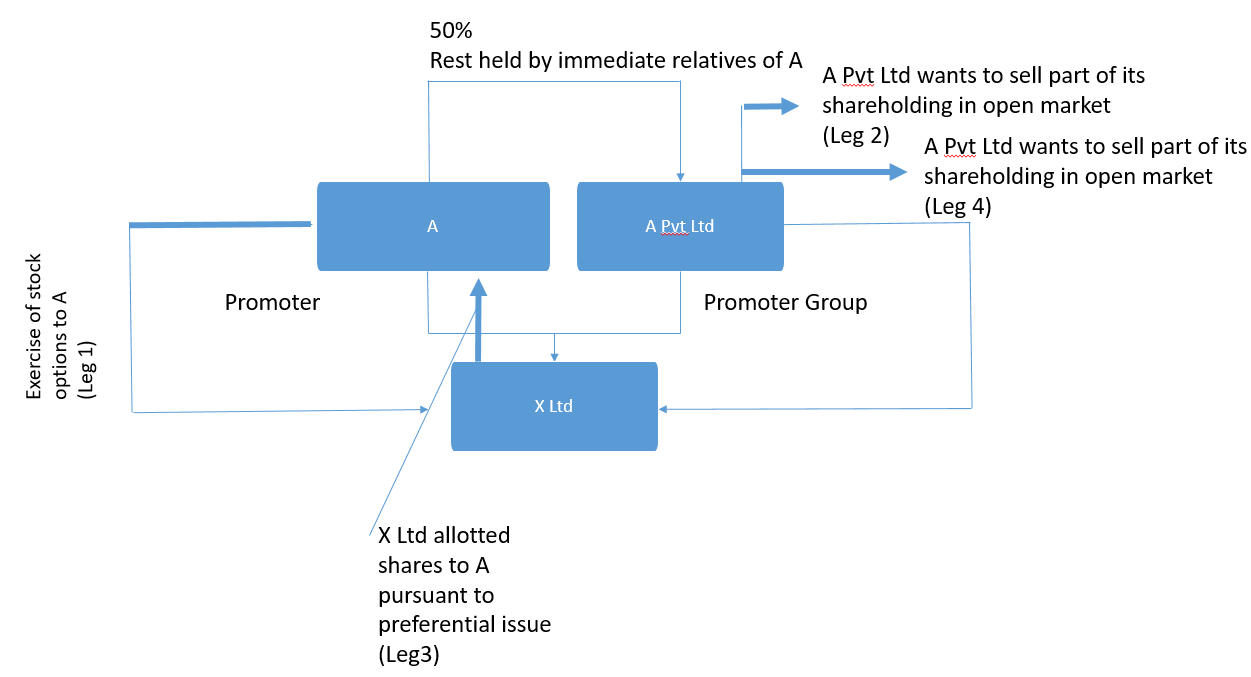

As per PIT Regulations, contra trade shall not apply for trades pursuant to exercise of stock options. SEBI Faqs further elaborate on the same stating that, in respect of ESOPs, subscribing, exercising and subsequent sale of shares, so acquired by exercising ESOPs (hereinafter “ESOP shares”), shall not attract contra trade restrictions.

Further trades pursuant to any non- market transaction is exempted (SEBI Faqs).

The rationale behind exemption is that for stock options and non-market transactions, the exercise price / purchase price is predetermined. The selling transaction pursuant to exercise of stock options or pursuant to acquisition of shares in non-open market is not influenced by purchases made basis some UPSI. The exercise price / acquisition price is already decided by the company.

Let us understand another example.

3.

In the above case, it is evident that A is the decision maker for A Pvt Ltd. Here, Leg 2 is not contra to Leg 1.Leg 4 is contra to Leg 3 as there is no exemption provided.

Often, it is also interpreted that contra-trade is applicable share wise. To take an example, suppose; first – stock options are acquired by a DP, second – open market purchase is done, third – stock options are sold (all three within a period of 6 months). Here, it is interpreted that third would not be contra to first and second. This is a wrong interpretation, as the moment the DP makes any open market purchase or already has the company’s shares in portfolio, the immunity w.r.t. selling shares acquired pursuant to exercise of stock options is lost. One cannot differentiate between the shares as what is important to establish for contra-trade is the intention to make short term profits. Such intention, also, is evident when trading decisions are made by a single person, irrespective of the different individuals executing trades.

Contra-trade is understood by different names in other jurisdictions. It is referred to as short swing in the US and reversal trade in some jurisdictions.

Section 16(b) deals with prohibition on short-swing trades by beneficial owner, director, or officer of the companies. The section reads as under:

“For the purpose of preventing the unfair use of information which may have been obtained by such beneficial owner[7], director, or officer by reason of his relationship to the issuer, any profit realized by him from any purchase and sale, or any sale and purchase, of any equity security of such issuer (other than an exempted security) or a security-based swap agreement involving any such equity security within any period of less than six months, unless such security or security-based swap agreement was acquired in good faith in connection with a debt previously contracted, shall inure to and be recoverable by the issuer, irrespective of any intention on the part of such beneficial owner, director, or officer in entering into such transaction of holding the security or security based swap agreement purchased or of not repurchasing the security or security-based swap agreement sold for a period exceeding six months.XXX”

Article 41 and 42 deals with contra trade restrictions. It reads as under:

Article 41 A shareholder that holds five percent of the shares issued by a company limited by shares shall, within three days from the date on which the number of shares held by him reaches this percentage, report the same to the company, which shall, within three days from the date on which it receives the report, report the same to the securities regulatory authority under the State Council. If the company is a listed company, it shall report the matter to the stock exchange at the same time.

Article 42 If the shareholder described in the preceding article sells, within six months of purchase, the shares he holds of the said company or repurchases the shares within six months after selling the same, the earnings so obtained by the shareholder shall belong to the company and be recovered by the board of directors of the company. However, a securities company that has a shareholding of not less than five percent due to purchase of the remaining shares in the capacity of a company that underwrites as the sole agent shall not be subject to the restriction of six months when selling the said shares.

If the company’s board of directors fails to comply with the provisions of the preceding paragraph, the other shareholders shall have the right to require the board of directors to comply.

If the company’s board of directors fails to comply with the provisions of the first paragraph and thereby causes losses to the company, the directors responsible therefore shall bear joint and several liabilities for the losses.

We had earlier in our article (supra) given the view that contra-trade should be seen jointly and not individually, considering the intent. To establish violation of PIT Regulations, one has to go beyond tracking trades based on PAN. It is important to know the decision maker behind the trades, in order to establish a clear nexus. It would be important to see whether such a view was taken by SEBI because of the case in hand or is it reflective of a new trend i.e. position of common control.

Link to our PIT Resource centre: Click here

[1] https://www.sebi.gov.in/enforcement/informal-guidance/oct-2023/in-the-matter-of-rama-mines-mauritius-ltd-under-sebi-prohibition-of-insider-trading-regulations-2015_78308.html

[2] https://www.sebi.gov.in/satorders/subhkamventures.pdf

[3] https://www.sebi.gov.in/sebi_data/commondocs/sep-2020/SEBI%20let%20Raghav%20IG_p.pdf

[4] https://www.sebi.gov.in/sebi_data/commondocs/jul-2018/StarCementGuidanceletter_p.pdf

[5] https://www.sebi.gov.in/sebi_data/commondocs/nov-2019/Inf%20Gui%20letter%20by%20SEBI%20Arvind_p.pdf

[6] https://www.govinfo.gov/content/pkg/COMPS-1885/pdf/COMPS-1885.pdf

[7] Every person who is directly or indirectly the beneficial owner of more than 10% of any class of any equity security (other than exempted security) [Ref. 16(a)(1)]

[8] http://www.npc.gov.cn/zgrdw/englishnpc/Law/2007-12/11/content_1383569.htm#:~:text=Article%201%20This%20Law%20is,of%20the%20socialist%20market%20economy.