Foreign nationals to comply with stringent MCA norms

– Team Corplaw | corplaw@vinodkothari.com

Our write-ups on corporate laws: https://vinodkothari.com/category/corporate-laws/

– Team Corplaw | corplaw@vinodkothari.com

Our write-ups on corporate laws: https://vinodkothari.com/category/corporate-laws/

– Team Corplaw | corplaw@vinodkothari.com

– Team Finserv (finserv@vinodkothari.com)

Relevant links:

Our write-ups on financial interests – https://vinodkothari.com/category/financial-services/

Corplaw Team | corplaw@vinodkothari.com

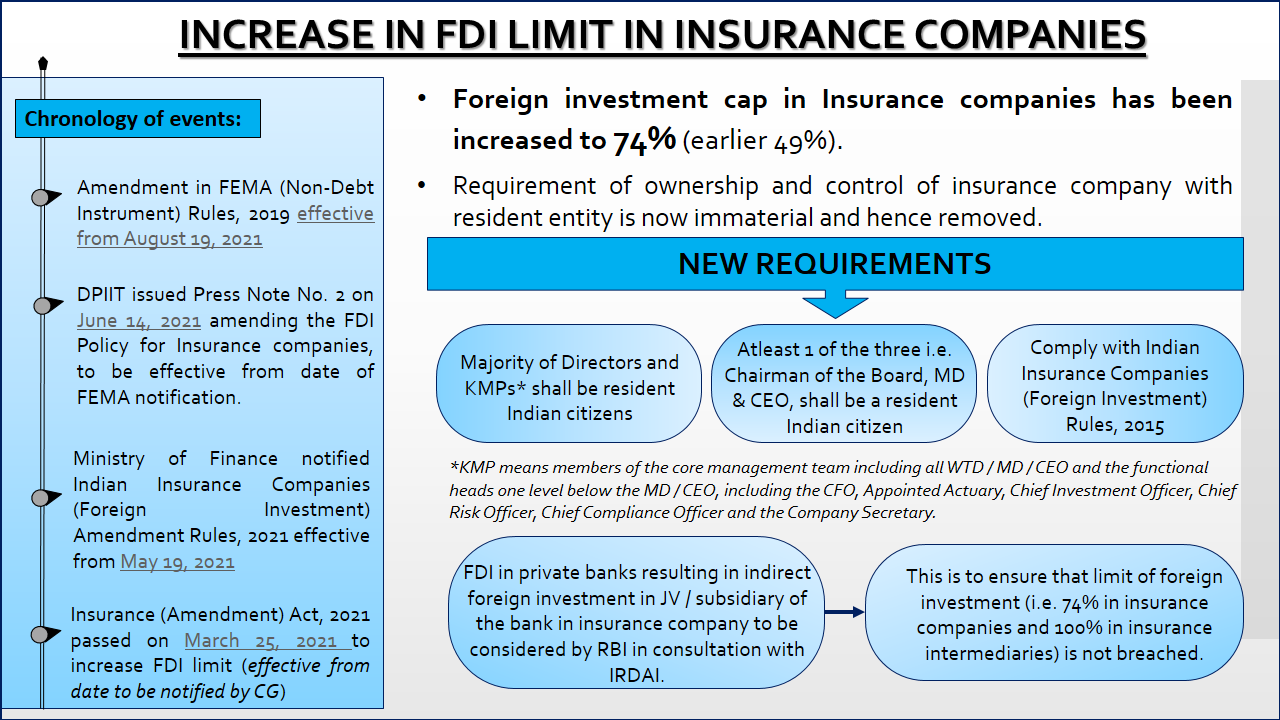

Amendment in Foreign Exchange Management (NDI) Rules, 2019 effective August 19, 2021- https://egazette.nic.in/WriteReadData/2021/229165.pdf

DPIIT Press Note on June 14, 2021 amending the FDI Policy for Insurance companies which shall be effective from date of FEMA notification – https://dpiit.gov.in/sites/default/files/pn2-2021.pdf

Consequential amendment in Indian Insurance Companies (Foreign Investment) Rules, 2015 are on May 19, 2021 – https://financialservices.gov.in/sites/default/files/Indian%20Insurance%20Companies%20(Foreign%20Investment%20)(amendment)%20Rules,%202021.pdf

Insurance (Amendment) Act, 2021 is passed on March 25, 2021 to increase FDI limit – https://financialservices.gov.in/sites/default/files/Insurance%20(Amendment)%20Act%202021%2025_3_2021.pdf

Proposes segregation of regulatory and the operational part in rules and regulations respectively

FCS Vinita Nair |Senior Partner, Vinod Kothari & Company

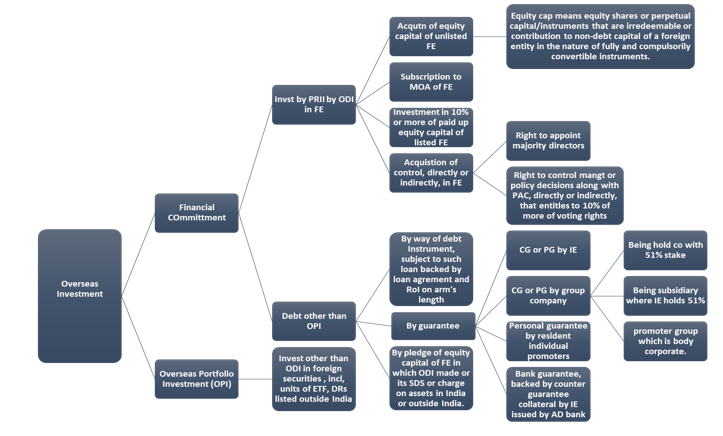

Investments by Indian entities outside India is a very common phenomenon and several companies have presence outside India by virtue of forming a Joint Venture (‘JV’) and Wholly Owned Subsidiaries (‘WOS’)

With the enforcement of amendment proposed in Finance Act, 2015 in October, 2019[1] powers vested with Central Government (CG) and Reserve Bank of India (RBI) with respect to permissible Capital Account Transaction were revisited. Power to frame rules relating to Non-Debt instruments (‘NDI’) were vested with CG and to frame regulations relating to debt instruments were vested with RBI. The scope of NDI inter alia covers all investment in equity instruments in incorporated entities: public, private, listed and unlisted; acquisition, sale or dealing directly in immoveable property.

RBI intends to combine erstwhile FEMA (Transfer or Issue of Foreign Security) Regulations, 2004[2] (‘erstwhile ODI regulations’) and FEMA (Acquisition and Transfer of immoveable property outside India) Regulations, 2015[3] into FEMA (Non-debt Instruments – Overseas Investment) Rules, 2021[4] (‘NDI Rules’) and FEMA (Overseas Investment) Regulations, 2021[5] (‘OI Regulations’) and has rolled out the draft regulations for public comments to be sent by August 23, 2021[6].

NDI Rules will provide the regulatory framework for making of overseas investment covering the permissions, conditions for making overseas investment, restrictions from making Overseas Direct Investment (‘ODI’), pricing guidelines, transfer, liquidation and restructuring of ODI. While the NDI Rules will be framed by CG, however, the same will be administered by the RBI.

OI Regulations, on the other hand, will provide only the operational part covering conditions for undertaking Financial Commitment (‘FC’), other than investment in equity capital, consideration in case of acquisition or transfer of equity capital of a Foreign Entity (‘FE’), mode of payment, obligations of Persons Resident in India (‘PRII’), reporting requirements, consequence of delay in reporting and restrictions on further FC/ transfer.

Under the erstwhile ODI regulations, currently in force, there is a concept of direct investment outside India in JV and WOS that excludes portfolio investment and FC. NDI Rules combine the two to define FC and separately defines the term Overseas Portfolio Investment (‘OPI’). Overseas Investment (‘OI’) is FC + OPI.

The classification as ODI depends on the nature of instruments in which investment is made, the nature of the entity in which investment is made and whether control has been acquired or not.

The diagram below provides a snapshot of the same.

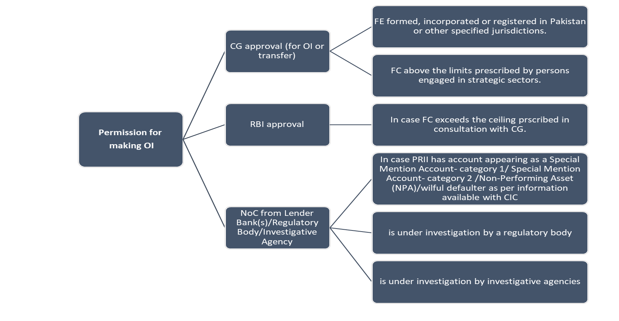

The NDI Rules provides investments that require prior approval of Central Government, RBI and NOC from lender banks/ regulatory body etc. The Erstwhile ODI Regulations only mandated prior approval of RBI in case eligibility conditions stipulated were not met by the Indian party or resident individual.

Our other videos and write-ups may be accessed below:

YouTube:

https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

Other write-up relating to corporate laws:

https://vinodkothari.com/category/corporate-laws/fema/

[1] https://egazette.nic.in/WriteReadData/2019/213265.pdf

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=2126&Mode=0

[3] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10257&Mode=0

[4] https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=4024

[5] https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=4023

[6] https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52026

For entities owned and controlled NRIs investing on non-repatriation basis

Updated as on August 10, 2021

Shreya Masalia | Executive

Foreign investments in equity instruments by a person resident outside India (PROI) is governed by Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (NDI Rules)[1] and the Consolidated FDI Policy[2] as amended from time to time. Foreign investments can be made on a repatriation basis or non-repatriation basis.

Repatriation and Non-Repatriation Basis

When the proceeds on investments made in India by a PROI can be transferred abroad after the exclusion of all applicable taxes refers to investments made on a repatriable basis and are regarded as foreign direct investment (FDI) or foreign portfolio investment based on the thresholds and other conditions laid down under NDI Rules.

In case of Investments on a non-repatriable basis, the same is not eligible to be remitted outside India (rule 2(ad) of NDI Rules r.w. para 2.1.31. of the FDI Policy, 2020). Subject to the provisions of schedule IV to the NDI Rules, investments made by a Non-Resident Indian(NRI) on a non-repatriation basis are deemed to be domestic investments and are considered on par with investments made by residents.

Downstream Investments by NRIs

Downstream Investment’ means investments made by an Indian entity or an Investment Vehicle in the capital instruments or the capital, as the case may be, of another Indian entity that has received investment from abroad. It includes entities in which a foreign entity which owns or controls more than 50% of the voting power by virtue of its investments, shareholding, or has power to appoint management of the company. Such a foreign entity is referred to as a foreign-owned and controlled company (FOCC) (explanation to rule 23 of NDI Rules r.w. Annexure 4 of the FDI Policy).

Where the investment received from an Indian company from a foreign entity is utilized to invest in the capital instrument of any other Indian company, it will be regarded as indirect foreign investment and the investor company will have to report the same in Form DI with the Reserve Bank of India within a period of 30 days from date of allotment of the equity instruments[3] (para 12 of FEMA (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019).

Need for a clarification

Though the investment made by an NRI on a non-repatriation basis was considered as on par with resident investments and were treated like domestic investments, the investment made by Indian entities owned and controlled by NRIs had no specific carve-out for the same. No clarity existed as to whether such an investment would attract the reporting and other compliance requirements of downstream investments.

Regulatory Changes

To address the ambiguity mentioned above, DIPP had released a press release dated March 19, 2021[4] amending the FDI Policy to provide that any investment in Indian entities by Indian entities which are owned and controlled by NRIs shall not form part of the calculation for indirect foreign investment.

On the same lines, the Ministry of Finance, vide notification dated August 06, 2021[5] amended the NDI Rules with immediate effect and inserted a new explaination to section 23(7)(i)(A) which provides that an investment made by an Indian entity which is owned and controlled by NRI’s on non-repartriation basis shall not be considered for calculation of indirect foreign investment.

Accordingly, the investment in Indian entities by Indian entities owned and controlled by NRIs will be considered at par with resident investments. Prior to the amendment, there was no clarity on whether what could be done directly under law was allowed indirectly too. The same has now been addressed.

[1] https://rbi.org.in/Scripts/BS_FemaNotifications.aspx?Id=11723

[2] https://dipp.gov.in/sites/default/files/FDI-PolicyCircular-2020-29October2020_1.pdf

[3] https://www.rbi.org.in/Scripts/BS_FemaNotifications.aspx?Id=11723

‘Technical’ contravention subject to minimum compoundable amount, format for public disclosure of compounding orders revised.

– CS Burhanuddin Dohadwala | corplaw@vindkothari.com

Introduction

Compounding refers to the process of voluntarily admitting the contravention, pleading guilty and seeking redressal. It provides comfort to any person who contravenes any provisions of FEMA, 1999 [except section 3(a) of the Act] by minimizing transaction costs. Reserve Bank of India (‘RBI’) is empowered to compound any contraventions as defined under section 13 of FEMA, 1999 (‘the Act’) except the contravention under section 3(a) of the Act in the manner provided under Foreign Exchange (Compounding Proceedings) Rules, 2000. Provisions relating to compounding is updated in the RBI Master Direction-Compounding of Contraventions under FEMA, 1999[1].

Following are few advantages of compounding of offences:

Present Circular

Pursuant to the supersession of FEM (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2017[2] (‘TISPRO”)and issuance of FEM (Non-Debt Instrument) Rules, 2019[3] [‘NDI Rules] and FEM (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019[4] [‘MPR Regulations’], RBI has updated the reference of the erstwhile regulations in line with the NDI Rules and MPR Regulations vide RBI Circular No.06 dated November 17, 2020[5] (‘Nov 2020 Circular’).

Additionally, the Nov 2020 Circular does away with the classification of a contravention as ‘technical’, as discussed later in the article.

Lastly, the Nov 2020 Circular modifies the format in which the compounding orders will be published on RBI’s website.

Compounding of contraventions relating to foreign investment

The power to compound contraventions under TISPRO delegated to the Regional Offices/ Sub Offices of the RBI has been aligned with corresponding provisions under NDI Rules and MPR Regulation as under:

| Compounding of contraventions under NDI Rules | |||

| Rule No. | Deals with | Corresponding regulation under TISPRO | Brief Description of Contravention |

| Rule 2(k) read with Rule 5 | Permission for making investment by a person resident outside India; | Regulation 5 | Issue of ineligible instruments |

| Rule 21 | Pricing guidelines; | Paragraph 5 of Schedule I | Violation of pricing guidelines for issue of shares. |

| Paragraph 3 (b) of Schedule I | Sectoral Caps; | Paragraph 2 or 3 of Schedule I | Issue of shares without approval of RBI or Government respectively, wherever required. |

| Rule 4 | Restriction on receiving investment; | Regulation 4 | Receiving investment in India from non-resident or taking on record transfer of shares by investee company. |

| Rule 9(4) | Transfer by way of gift to PROI by PRII of equity instruments or units of an Indian company on a non- repatriation basis with the prior approval of the Reserve Bank. | Regulation 10(5) | Gift of capital instruments by a person resident in India to a person resident outside India without seeking prior approval of the Reserve Bank of India. |

| Rule 13(3) | Transfer by way of gift to PROI by NRI or OCI of equity instruments or units of an Indian company on a non- repatriation basis with the prior approval of the Reserve Bank. | ||

| Compounding of contraventions under MPR Regulations | |||

| Regulation No. | Deals With | Corresponding regulation under TISPRO | Brief Description of Contravention |

| Regulation 3.1(I)(A) | Inward remittance from abroad through banking channels; | Regulation 13.1(1) | Delay in reporting inward remittance received for issue of shares. |

| Regulation 4(1) | Form Foreign Currency-Gross Provisional Return (FC-GPR); | Regulation 13.1(2) | Delay in filing form FC (GPR) after issue of shares. |

| Regulation 4(2) | Annual Return on Foreign Liabilities and Assets (FLA); | Regulation 13.1(3) | Delay in filing the Annual Return on Foreign Liabilities and Assets (FLA). |

| Regulation 4(3) | Form Foreign Currency-Transfer of Shares (FC-TRS); | Regulation 13.1(4) | Delay in submission of form FC-TRS on transfer of shares from Resident to Non-Resident or from Non-resident to Resident. |

| Regulation 4(6) | Form LLP (I); | Regulations 13.1(7) and 13.1(8) | Delay in reporting receipt of amount of consideration for capital contribution and acquisition of profit shares by Limited Liability Partnerships (LLPs)/ delay in reporting disinvestment / transfer of capital contribution or profit share between a resident and a non-resident (or vice-versa) in case of LLPs. |

| Regulation 4(7) | Form LLP (II); | ||

| Regulation 4(11) | Downstream Investment | Regulation 13.1(11) | Delay in reporting the downstream investment made by an Indian entity or an investment vehicle in another Indian entity (which is considered as indirect foreign investment for the investee Indian entity in terms of these regulations), to Secretariat for Industrial Assistance, DIPP. |

Technical contraventions to be compounded with minimal compounding amount

As per RBI’s FAQs[1] whenever a contravention is identified by RBI or brought to its notice by the entity involved in contravention by way of a reference other than through the prescribed application for compounding, the Bank will continue to decide (i) whether a contravention is technical and/or minor in nature and, as such, can be dealt with by way of an administrative/ cautionary advice; (ii) whether it is material and, hence, is required to be compounded for which the necessary compounding procedure has to be followed or (iii) whether the issues involved are sensitive / serious in nature and, therefore, need to be referred to the Directorate of Enforcement (DOE). However, once a compounding application is filed by the concerned entity suo moto, admitting the contravention, the same will not be considered as ‘technical’ or ‘minor’ in nature and the compounding process shall be initiated in terms of section 15 (1) of Foreign Exchange Management Act, 1999 read with Rule 9 of Foreign Exchange (Compounding Proceedings) Rules, 2000.

Nov 2020 Circular provides for regularizing such ‘technical’ contraventions by imposing minimal compounding amount as per the compounding matrix[1] and discontinuing the practice of giving administrative/ cautionary advice.

Public disclosure of compounding order

Compounding order by RBI can be accessed at the RBI website-FEMA tab-compounding orders[1]. In partial modification of earlier instructions issued dated May 26, 2016[2] it has been decided that in respect of the Compounding Orders passed on or after March 01, 2020 a summary information, instead of the compounding orders, shall be published on the Bank’s website in the following format:

| Sr. No. | Name of the Applicant | Details of contraventions (provisions of the Act/Regulation/Rules compounded)

(Newly inserted) |

Date of compounding order

(Newly inserted) |

Amount imposed for compounding of contraventions | Download order

(Deleted) |

It seems that the compounding order will not be available for download.

Conclusion:

The delegation of power is done for enhanced customer service and operational convenience. Revised format of disclosure of compounding orders will be more reader friendly. Delay in filing of forms under MPR Regulations on FIRMS portal is subject to payment of Late Submission Fees (LSF) as per Regulation 5. The payment of LSF is an additional option for regularising reporting delays without undergoing the compounding procedure.

Abbreviations used above:

FIRMS: Foreign Investment Reporting & Management System.

| Our other articles/channel can be accessed below:

1. Compounding of Contraventions under FEMA, 1999- RBI delegates further power to Regional Offices:

2. Other articles on FEMA, ODI & ECB may be access below: https://vinodkothari.com/category/corporate-laws/

3. You Tube Channel: |

[1] https://www.rbi.org.in/scripts/Compoundingorders.aspx

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10424&Mode=0

[1] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10424&Mode=0

[1] https://m.rbi.org.in/Scripts/FAQView.aspx?Id=80 (Q. 12)

[1] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=10190

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11253&Mode=0

[3] http://egazette.nic.in/WriteReadData/2019/213332.pdf

[4] https://www.rbi.org.in/Scripts/BS_FemaNotifications.aspx?Id=11723

[5]https://rbidocs.rbi.org.in/rdocs/notification/PDFs/APDIRS62545AA7432734B31BD5B59601E49AA6C.PDF