https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-23 13:08:452026-06-23 14:48:09The Sale That Was Never About the Product

In order to regulate mis-selling concerns for both products/ services of regulated entities and third-parties by a regulated entity, amendments have been issued ‘Advertising, Marketing and Sale of Financial Products and Services by Regulated Entities’, via two sets of amendment directions for NBFCs:

Reserve Bank of India (Non-Banking Financial Companies – Responsible Business Conduct) Second Amendment Directions, 2026 (‘RBC Amendment Directions’/’Amendment Directions’)

(Refer to our detailed write up on the Amendment Directions here, our youtube video here. Further we are also hosting a half day workshop on June 26, 2025 (Physical-Bengaluru) where we will be discussing the Amendment Directions in details. The Brochure for the workshop can be accessed through here)

Refer to our FAQs on the Amendment Directions and the UFS Amendment Directions below

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-22 17:58:112026-06-25 11:43:45FAQs on Advertising, Marketing and Sale of Financial Products and Services, and agency activities: NBFCs

– Vinita Nair and Saloni Khant | corplaw@vinodkothari.com

With the backdrop of the outflow of billions of foreign funds and the RBI’s multipronged approach to draw foreign funds (Read our article: RBI attempts to woo fleeing foreign investors), RBI notified the FEM (Non-debt Instruments) (Third Amendment) Rules, 2026 effective from June 12, 2026. All foreign individuals who are persons resident outside India PROIs are now permitted to purchase and sell equity instruments[1] of a listed Indian company subject to an individual limit of 10% and aggregate limit of 24%. Corresponding amendments made in FEM (Mode of Payment and Reporting of Non-Debt Instruments) (Amendment) Regulations, 2026 effective from June 13, 2026, which provides the manner of mode of payment and remittance of sale proceeds etc.

Eligibility and permissible limits for investing in equity instruments of listed companies

Who can invest?

All individual PROI. Earlier it was limited to NRI and OCIs.

What are the revised investment limits?

Investment Limits

Erstwhile limits (only for NRI and OCI) as other PROI not permitted to invest

Revised limits for all individual PROI (including NRI and OCI)

Individually

5%

10%

Aggregate

10% (Could be increased to 24% by passing a special resolution)

24% (No need to pass a special resolution for increasing the limits )

For private sector banks, the limits for NRIs are stricter and remain the same. This may be a gap or a deliberate move to remain aligned with the limit of investments beyond 5% requiring the approval of the RBI under the RBI (Commercial Banks – Acquisition and Holding of Shares or Voting Rights) Directions, 2025. The limits are on both repatriation and non-repatriation basis. For other sectors, investment on non-repatriation basis is permitted without any limits and treated akin to domestic investment.

Individual limit – 5 percent of the total paid up capital

Aggregate limit – 10 percent of the total paid up capital both

NRI holdings shall be allowed up to 24 percent of the total paid up capital both on repatriation and non-repatriation basis subject to passing of a special resolution.

Limit applicable to individuals registered as Cat II FPIs

The individual limit stated above is a combined limit for investment made under different schedules.

Consequence of breach of individual limit of 10%:

Divestment required within 5 trading days of settlement of trade crossing threshold. In case of non divestment, investment is considered to be FDI.

Investor to intimate investee company and depositories through AD Cat-1 Bank within 7 trading days of such settlement date.

Sale beyond the prescribed period will be treated as contravention of NDI Rules.

When is government approval required?

Acquisition of control of an Indian investee entity by a citizen/ entity of a country sharing land border with India (LBC investor).

Control means the right to appoint the majority of the directors / control the management or policy decisions.

Acquisition of ownership of an Indian investee entity by an LBC investor.

Ownership means beneficial holding of more than 50% of the equity instrument of such company.

Acquisition of beneficial ownership by a citizen of an LBC.

Beneficial ownership primarily refers to more than 10% entitlement of shares/ capital/ profits of the investor company. (Rule 9(3)(b) of the PML (Maintenance of Records) Rules 2005.

All individual PROIs can transfer by sale/ gift to any PROI or may sell on stock exchange.

When is government approval required?

In case of sale or gift to another PROI, prior Government approval is required to be obtained for any transfer in case the company is engaged in a sector which requires Government approval.

Same 3 scenarios as above, involving LBC investor.

Mode of payment for investment

Consideration may be paid by inward remittance from abroad through banking channels or out of funds held in any repatriable deposit account maintained in accordance with the FEMA (Deposit) Regulations,2016 – for e.g. NRE, FCNR (B) or SNRR a/c.

A repatriable rupee account maintained in accordance with the FEMA (Deposit) Regulations,2016, required to be designated by an individual PROI to be used exclusively for investments permitted under Schedule III.

Remittance of sale proceeds

The sale proceeds (net of taxes) of equity instruments may be remitted outside India or may be credited to the designated rupee account of the person concerned.

Reporting requirements

To be done by AD Category-1 Bank to RBI in Form LEC (Individual Foreign Investor – IFI) for purchase/ sale of listed equity instruments by individual PROIs including NRIs, OCIs. The designated link office of the AD bank shall furnish to RBI, a report on a daily basis, for their entire bank.

[1] Equity instruments comprises equity shares, convertible debentures, preference shares and share warrants issued by an Indian company [Rule 2(k) of FEM (NDI) Rules]

The interplay between the insolvency proceedings under Insolvency and Bankruptcy Code, 2016 (‘IBC’) and cheque dishonour proceedings under Section 138 of the Negotiable Instruments Act, 1881 (‘NI Act’) has been one of the most debated areas. While the IBC seeks to provide a financially distressed debtor with a “breathing space” by way of moratorium on legal proceedings, Section 138 of the NI Act aims to maintain trust in cheque-based transactions by imposing criminal liability for dishonour of cheques.

The Supreme Court’s landmark decision in P. Mohanraj v. Shah Brothers Ispat Pvt. Ltd. appeared to settle the issue by holding that the protection of the moratorium under Section 14 of the IBC extends to the proceedings under Sections 138/ 141 of the NI Act against the corporate debtor. However, the recent decision in Dineshchand Surana v. UCO Bank has reopened the discussion by questioning certain aspects of the reasoning adopted in P. Mohanraj and referring the matter to a larger Bench for consideration.

In this write up we have made an attempt to discuss the evolving judicial approach towards the applicability of IBC moratorium to proceedings under Section 138 of the NI Act.

In P. Mohanraj, a three-judge bench of the Supreme Court examined- “whether the institution or continuation of a proceeding under Section 138/141 of the Negotiable Instruments Act can be said to be covered by the moratorium provision, namely, Section 14 of the IBC?”

While examining the provisions of NI Act vis-a vis IBC, the Court held as follows:

As per section 14 (1), AA shall mandatorily impose a moratorium to prohibit the actions specified in clauses (a) to (d), such as legal proceedings against the corporate debtor, transfer of its assets, enforcement of security interests, and recovery of property from its possession, subject to the exceptions provided in sub-sections (2) and (3).

Proceeding under Sections 138 and 141 of the NI Act are covered by the moratorium imposed under Section 14(1)(a) of the IBC insofar as they are instituted or continued against the corporate debtor.

The term “proceedings” under Section 14(1)(a) was given a broad interpretation and was not restricted only to civil proceedings. The Court held that it includes proceedings arising from transactions that may affect or deplete the assets of the corporate debtor .

While section 138 proceedings are criminal in nature, the Court described them as “quasi-criminal” because their primary objective is to ensure payment and not the punishment. The Court observed that the purpose of Section 138 is to secure payment of the cheque amount and maintain confidence in commercial transactions, while the penal consequences are mainly a means of enforcing compliance.

While prosecution under Section 138 may result in compensation payable by the corporate debtor, continuation of such proceedings during CIRP could adversely affect the assets available for resolution and defeat the purpose of the moratorium.

The Court emphasised that the moratorium under Section 14 is intended to provide the corporate debtor a “breathing space” and preserve its assets during CIRP proceedings. However, the protection is not extended to the natural persons associated with the CD, such as, its directors, signatories, and other persons responsible under Section 141 of the NI Act. Therefore, cheque dishonour proceedings may continue against such individuals even though they are stayed against the company

The Court clarified that upon cessation of the moratorium, the suspended proceedings against the corporate debtor may revive and continue in accordance with law.

Thus, the judgment was significant because it treated Section 138 proceedings as ‘civil sheep in a criminal wolf’s clothing’, that is having a predominantly debt-recovery character, thereby bringing them within the protective umbrella of IBC.

Subsequent judicial developments

Referring to the judgement in P. Mohanraj, courts consistently maintained that upon commencement of CIRP against a CD, it is the CD that enjoys protection during CIRP, however, the directors and other officers of CD cannot evade personal liability under the NI Act merely because insolvency proceedings have commenced against the company.

The controversy resurfaced in Dineshchand Surana v. UCO Bank[1], wherein an appeal was preferred before the Supreme Court against the judgment dated 18.10.2023 passed by Madras High Court. In this case, the appellant, the Managing Director of Surana Power Limited, relying on P. Mohanraj, submitted that the expression “legal action or proceeding in respect of any debt” in Sections 96 and 101 is wide enough to include Section 138 proceedings, as the moratorium extends to any legal proceeding relatable to recovery of debt. He also contended that the objective of the moratorium under Part II and Part III is the same i.e. to prevent depletion of assets and provide breathing space and accordingly the reasoning in P. Mohanraj should equally apply to personal insolvency. However, the High Court rejected the same, holding that proceedings under Section 138 of the NI Act are not debt recovery proceedings and therefore do not fall within the scope of the moratorium under Section 96. The Court further observed that Section 138 is a penal provision providing for imprisonment and fine, and hence cannot be equated with recovery proceedings.

The Supreme Court undertook a detailed examination of the nature of cheque dishonour proceedings and expressed reservations about the reasoning adopted in P. Mohanraj.

The Bench observed that proceedings under Section 138 cannot be viewed merely as mechanisms for debt recovery. According to the Court, the main purpose of Section 138 is to maintain public confidence in commercial transactions by attaching penal consequences to cheque dishonour. Therefore, the criminal aspect of the provision is not secondary to the compensation aspect. While the Court observed that the purpose under both Part II and Part III is to provide breathing space to restructure assets and liabilities, however, the Court was also conscious that certain liabilities are not protected by the moratorium even though their consequence might deplete the debtor’s assets; the rationale being that the moratorium is intended to shield the debtor from recovery actions and civil claims, and not from the consequences of criminal misconduct. Accordingly, the mere possibility that a criminal proceeding may ultimately result in a financial burden on the debtor cannot, by itself, bring such proceedings within the ambit of the moratorium.

Further, the Court also explained that proceedings under Section 138 have two separate elements:

Compensatory element, which aimed at ensuring payment of the cheque amount and compensation to the complainant, therefore, should be within the moratorium.

Criminal element, which aimed at punishing the offence of cheque dishonour through penal consequence, and Moratorium under Part III of IBC does not apply to criminal proceedings.

In view of the above, the Court observed that while the insolvency moratorium may impact the compensatory aspect, it does not necessarily bar or suspend the criminal prosecution.

Since this understanding appeared to differ from the reasoning in P. Mohanraj, which had treated Section 138 proceedings as primarily compensatory and therefore subject to moratorium, the matter was referred to a larger Bench for authoritative determination.

The decision in P. Mohanraj brought clarity to the law by holding that proceedings under Section 138 of the NI Act against a CD are covered by the moratorium under Section 14 of the IBC. At the same time, the Court made it clear that this protection is available only to the CD and not to its directors, signatories, or other persons responsible for the company’s affairs. This position was thereafter consistently followed by courts.

However, in Dineshchand Surana, the Supreme Court revisited the nature of Section 138 proceedings and questioned the basis of the reasoning adopted in P. Mohanraj. The Court observed the 2 tier aspects of Section 138 proceeding, i.e (a) compensatory aspect, and (b) a criminal aspect. This led the Court to raise a significant question as to if the moratorium is intended to protect the debtor’s assets and therefore affects the recovery aspect, should it also stop the criminal prosecution?

It is important to note here that the difference between the two judgments is not about who can be prosecuted. Both judgments recognise that directors and other persons in charge of the company can continue to face proceedings under the NI Act. The real issue is whether the moratorium should stop a Section 138 case against the corporate debtor itself merely because the proceeding also involves recovery of money.

Therefore, the key question before the larger Bench is whether Section 138 proceedings should be stayed completely during the moratorium, as held in P. Mohanraj, or whether only the compensatory aspect should be affected while the criminal prosecution continues, as suggested in Dineshchand Surana.

If the larger Bench agrees with the view expressed in Dineshchand Surana, criminal prosecution under Section 138 may continue against the CD, even during the moratorium, while only the recovery or compensation aspect will be subject to moratorium. Even then, the authors are of the view, given that a corporate entity cannot be imprisoned; the impact would be limited to imposition of fine; and then, it might involve questions surrounding vicarious liability on the directors, etc. and the effect of section 14 on such fines. The decision of the larger Bench will therefore be crucial in determining how the objectives of the IBC will be aligned with the consequences under NI Act.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-19 12:45:542026-06-19 12:48:06Section 138 of NI Act Proceedings During Moratorium: The Evolving Jurisprudence from P. Mohanraj to Dineshchand Surana

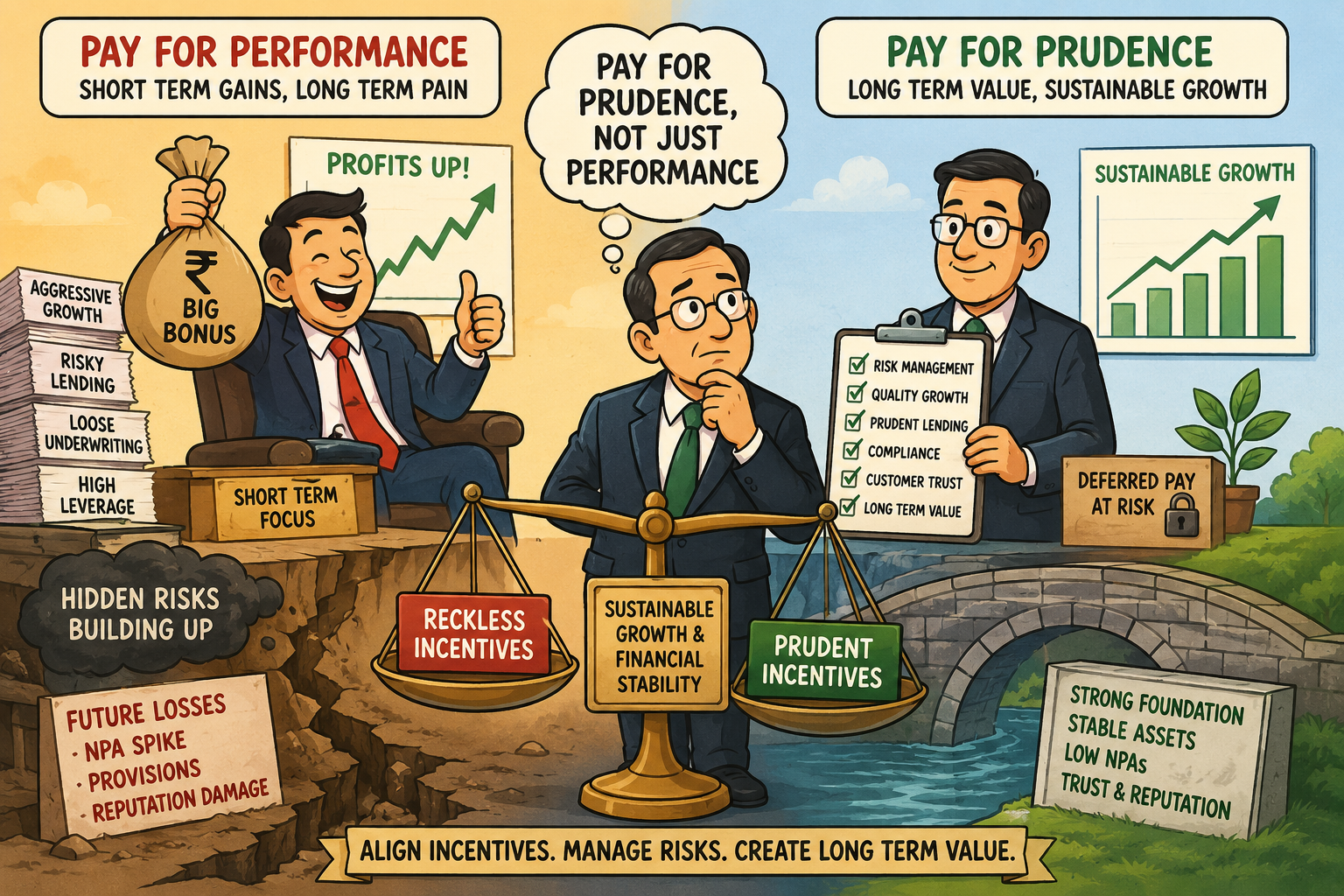

On 9 March 2026, the Reserve Bank of India imposed a monetary penalty of ₹2.70 lakh on a financial institution for violations regarding the payment of the entire variable remuneration to certain KMPs upfront, without deferring any portion, in breach of applicable compensation guidelines. While the quantum of the penalty is insignificant relative to the Company’s scale of operations, it reflects the RBI’s clear regulatory emphasis on ensuring that NBFC compensation practices are aligned with prescribed regulatory requirements.

Compensation structures in financial institutions, like any other institution, have traditionally been designed to reward performance. Higher profits, stronger business growth, and increased market share have often translated into higher incentives and bonuses for senior management. However, the manner in which institutions reward their key personnel can significantly influence the risks they choose to take. Where the remuneration is excessively linked to short-term profitability, it may encourage risk-taking without adequate regard to long-term consequences, particularly where the underlying risks may materialise only several years later.

The Lessons of History: From Performance to Prudence

The 2008 Global Financial Crisis (GFC) illustrated the above mechanism. Mortgage originators earned fee income upfront on loan disbursements while credit risk was securitised and passed to counterparties; traders at large investment banks received annual cash bonuses tied to mark-to-market gains while systemic risks accumulated on balance sheets. When those risks materialised, bonus recipients were under no obligation to return payments.

Mr Raghuram Rajan (2006), writing before the GFC , identified competitive pressures pushing financial sector executives toward risk strategies concealed within opaque compensation structures, specifically, strategies that generate near-certain short-term income while accumulating rare but catastrophic risks.

In a landmark 2011 study, Fahlenbrach and Stulz revealed a shocking paradox – banks where CEOs owned the most stock actually suffered the worst losses during the crash. Because their personal wealth was tied to share prices, these executives took massive, highly concentrated gambles to boost short-term returns. The conclusion of their research was clear that how an executive is paid is just as critical as how much they are paid.

Why only financial institutions? Rather, every Company is covered

Section 178(4)(c) of the Companies Act, 2013, requires the Nomination and Remuneration Committee (NRC) of every prescribed class of company to formulate the criteria for, and recommend to the Board, a policy relating to the remuneration of directors, KMPs, and other employees. While RBI has prescribed a more structured framework for banks and NBFCs, the underlying principles are equally relevant to non-financial entities and are consistent with the remuneration governance framework envisaged under Section 178 of the Companies Act, 2013. In any company, compensation is often linked to performance metrics such as profits, revenue growth, operational targets, or share price performance. Where such performance is subsequently found to have been achieved through misconduct, inaccurate reporting, regulatory breaches, or unsustainable business practices, malus and clawback mechanisms enable the company to reduce or recover variable remuneration.

Where an industrial company’s CEO makes poor strategic decisions, the primary losers are shareholders. Where an NBFC’s senior management makes poor credit or investment decisions, the losses spread to depositors (in deposit-taking NBFCs), borrowers facing credit contraction, financial system counterparties, and, at sufficient scale, the broader economy.

Consider a hypothetical Middle Layer NBFC. In FY2023, its loan book grew by 35%, driven by aggressive commercial lending and disbursements. Net interest margin expands, provisions are low, and PAT rises sharply. The board approves variable pay of ₹8 crore for the MD and ₹3-5 crore for the senior credit team, paid immediately in April 2023.

By FY2025, borrower stress in the commercial segment becomes apparent. NPA recognition in the FY2023-24 begins. Provisions of ₹400-600 crore are required across two financial years, erasing the PAT that justified the FY2023 bonuses. The credit decisions that drove FY2023 profitability and the bonuses are the same decisions that drove FY2025 impairment.

Under a properly designed deferral and clawback framework, a material portion of the FY2023 variable pay would remain unvested in FY2024 and FY2025. As NPA ratios deteriorate beyond prescribed thresholds, malus provisions would cancel unvested amounts. If fraud or deliberate misreporting in origination is subsequently found, clawback provisions would enable recovery of amounts already paid. In the absence of such provisions, the incentive structure is undisturbed: gains are privatised, losses are socialised.

Building Blocks of Sound Compensation Governance

A simple principle: individuals who generate profits should also bear the consequences of the risks taken to generate those profits.

A. Variable Pay

Variable pay is the performance-linked component of remuneration. Two dimensions are critical: the quantum that is the share of variable pay relative to fixed pay must be material enough to serve as a genuine incentive without dominating compensation to the point of creating perverse incentives to maximise near-term metrics. Secondly, the variable pay must be assessed against risk-adjusted, institution-wide outcomes, not merely individual disbursement volumes, gross fees, or absolute PAT. Variable pay must be capable of being reduced to zero in poor performance periods.

B. Deferral of Compensation

Deferral withholds a portion of variable pay for payment at a future date, subject to the absence of adverse risk outcomes during the deferral window. The purpose is to ensure that remuneration remains exposed to the consequences of decisions throughout the period over which those decisions actually materialise. The deferral period must be calibrated to the risk horizon.

C. Share-Linked Instruments

Awarding a portion of variable pay in share-linked instruments like stock options, ESOPs, phantom stock, stock appreciation rights aligns executive incentives with the long-term market value of the institution. An executive holding significant unvested equity is personally exposed to the consequences of decisions that may impair the institution’s stock price years after they are taken.

D. Malus

The term “malus” originates from the Latin word meaning bad or adverse, reflecting a mechanism that reduces or cancels remuneration before it vests. It is the primary ex-post adjustment tool during the deferral period.

The malus period must cover, at minimum, the entire deferral period, otherwise the deferral itself is meaningless. For malus to operate as a genuine deterrent, the policy must specify quantitative triggers rather than purely discretionary language.

E. Clawback

“Clawback” literally denotes the act of taking back something previously given, and refers to the recovery of remuneration that has already vested or been paid. It operates after the deferral period and is therefore more operationally complex. It requires enforceable contractual provisions in individual employment agreements (a policy reference alone is insufficient), may face legal challenges in certain jurisdictions, and demands investigation processes before invocation.

Malus and clawback are complementary, not substitutes. Malus stops deferred pay from flowing out during the risk-materialisation window; clawback reverses compensation already received where subsequent investigation reveals misconduct or misreporting that was not apparent at the time of payment.

Global Compensation Frameworks: Numbers, Not Principles

All major jurisdictions that have addressed financial institution compensation have converged on prescriptive parameters such as minimum deferral percentages, defined deferral periods, mandatory clawback windows, and MRT identification beyond the C-suite.

European Union: Capital Requirements Directive V (Art. 94)

Variable remuneration for MRTs is capped at 100% of fixed remuneration, extendable to 200% with shareholder approval. A minimum of 40% of variable pay must be deferred, rising to 60% where variable pay is ‘of a particularly high amount’, for at least four to five years (five years for senior managment). Malus and clawback provisions are mandatory during the deferral and retention periods. Payout schedules must be ‘sensitive to the time horizon of risks.’

CPS 511 is among the most granular remuneration standards globally. For Significant Financial Institutions (SFIs): (i) the CEO must defer 60% of variable pay for a minimum of six years; (ii) other senior managers must defer 40% of variable pay for at least four years; (iii) the clawback window extends to a minimum of two years from the date of payment or vesting. Clawback criteria explicitly include ‘material misstatements of financial statements.’ CPS 511 also requires boards to link individual accountability (under the Banking Executive Accountability Regime) directly to the deferral and clawback framework.

Under the Senior Managers and Certification Regime, each Senior Manager holds a personal ‘Statement of Responsibilities.’ SYSC 19D mandates that MRTs face: (i) malus and clawback for a minimum of five to seven years (seven years for Senior Managers); (ii) minimum deferral of 40% of variable pay (rising to 60% for higher amounts); and (iii) a minimum deferral period of four years.

Similar requirement: the NBFC framework is principle-based.

Nomination & Remuneration Committee (NRC)

Required

Required (Para 30)

Similar requirement.

NRC-Risk Management Committee Coordination

Mandatory; compensation outcomes to be aligned with capital adequacy and cost-to-income ratio

Required (Para 31)

Banks have more prescriptive alignment requirements.

Variable Pay – Minimum Share

At least 50% of total compensation for senior executives and MRTs

No prescribed minimum

Significant flexibility for NBFCs.

Variable Pay – Maximum Cap

Maximum 300% of fixed pay

Not prescribed

No regulatory cap for NBFCs.

Fixed vs Variable Pay Structure

Quantitatively prescribed

Principle-based (Para 33)

Banks subject to detailed limits.

Deferral of Variable Pay

Minimum 60% deferred

Deferral contemplated (Para 35)

NBFCs have no specified percentage.

Deferral Period

Minimum 3 years

Not specified

NBFCs may determine internally.

Deferral of Cash Component

At least 50% of cash component deferred (subject to threshold exemption)

Not specified

No equivalent requirement for NBFCs.

Vesting Schedule

No faster than a pro rata cumulative basis over deferral period

Not specified

Banks are subject to structured vesting norms.

Share-linked Instruments

Minimum 50%–67% of variable pay depending on pay structure

Not required

No specific requirement for NBFCs.

Alternative to Share-linked Instruments

All-cash permitted only in limited cases; variable pay capped at 150% of fixed pay

Not prescribed

No comparable restriction for NBFCs.

Material Risk Taker (MRT) Identification

Mandatory identification beyond KMPs

Not prescribed

The NBFC framework does not define MRTs.

Control Function Independence

Implied through governance framework

Specifically required (Para 35(4))

Explicit requirement under NBFC Directions.

Malus and Clawback Framework

Mandatory

Mandatory (Para 37)

A framework is required for both.

Malus/Clawback Scope

Must cover at least deferral and retention periods

No prescribed period

Banks have detailed implementation standards.

NPA-specific Malus Trigger

Mandatory prohibition on unvested variable pay where NPA divergence exceeds RBI disclosure threshold

Not prescribed

Unique requirement for banks.

Guaranteed Bonus

Prohibited except for a sign-on bonus for new hires

Prohibited except for a sign-on bonus (Para 36)

Broadly aligned.

Hedging of Variable Pay

Prohibited

Not prescribed

No express prohibition for NBFCs.

Compensation Disclosure Requirements

Prescribed under governance framework

No specific disclosure framework

Banks are subject to greater transparency obligations.

Alignment with Risk Outcomes

Detailed linkage to risk, capital and performance metrics

Principle-based requirement

Banks have significantly greater regulatory prescription.

Conclusion

The regulation of compensation is fundamentally a question of governance. While remuneration frameworks are intended to reward performance, financial sector experience has repeatedly demonstrated that performance measured over a short horizon may not accurately reflect the risks embedded in business decisions. Accordingly, modern compensation regulation seeks to align remuneration outcomes not merely with current profitability, but with the sustainability of that profitability over time.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-17 12:29:342026-06-17 16:02:40Pay for Performance Or Pay for Prudence?

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-16 15:51:542026-06-16 18:41:02From Consent to Compensation: RBI’s Directions for REs on Sales Practices

By way of Highlights, the UFS Amendments introduce a unified framework for agency business of banks and NBFCs, and referral activities of banks. Specifically, the Amendments provide that agency/referral activities will be undertaken without risk participation, and in case of referral, the bank will be limited to simply connecting the customer with the external provider (TPPSP), and will not be involved in the sale process. The physical or electronic machinery of the bank will not be used for third party product sales.

Our interpretation of the regulated entity’s (RE’s) participation being on no-risk basis is that if the agency or referral fees are linked with the profits or performance of the product/service offered by the third party, the agent or referring entity indeed gets subjected to risk.

We also give specific details about insurance distribution, a lucrative add-on income opportunity for most regulated entities.

Unified Framework for Agency Business

RBI has formally defined “Agency Business” as an arrangement where a Bank/ NBFC acts as an agent of a third-party product or service provider (TPPSP) for the distribution of financial products and services. Thus, banks/NBFCs under agency business can only distribute financial products or services.

The RBI has not covered non-financial products and services under the purview of the UFS Directions, however, the same is not restricted in case of NBFCs.

The distribution of financial products and services would include marketing, sales, promotion, customer onboarding support, grievance facilitation and after-sales services.

The arrangement must be undertaken without any risk participation by the NBFC.

For such TPPS that require higher and continuous customer interactions, the Agency Business arrangement may be used instead of Referral Services. However, REs may undertake only such third-party product or services under referral route where continued customer interactions such as distribution, grievance redressal, post sales services are not required to be undertaken.

Undertaking Insurance Agency business by Banks/NBFCs/HFCs

Banks may act as an insurance broker departmentally

NBFCs and eligible HFCs may undertake insurance distribution under the corporate agency or broking model without prior RBI approval.

Prior approval/registration from IRDAI and compliance with applicable IRDAI regulations remain mandatory. Here, it may be noted that the RBI NOC is generally required at the time of making an application to IRDAI.

Insurance distribution must:

Be undertaken on a fee basis;

Involve no risk participation;

Be clearly disclosed to customers by disclosing the products on the website of the NBFC;

Be supported by robust grievance redressal mechanisms of the insurer. The NBFC may facilitate the redressal of grievances.

Earlier, the Reserve Bank of India (Non-Banking Financial Companies – Undertaking of Financial Services) Directions, 2025 (‘UFS Direction’), provided that no incentive (cash or non-cash) should be paid to the staff engaged in insurance broking/ corporate agency services by the insurance company. The same has now been deleted. However, it may be noted that this requirement has been covered under para 101U of the RBC Amendment Directions.

Does Insurance Distribution include a lender acting as master policyholer?

The UFS Amendment Directions uses the terms ‘Agency Business’ to mean an arrangement under which an NBFC acts as an agent of a third-party product or service provider (TPPSP), without risk participation, to facilitate the sale of the latter’s financial products or services (e.g., insurance, mutual fund, pension fund, etc.) to its own customers Para 32 clarifies that an NBFCs intending to undertake insurance distribution can do so only in the capacity of a Corporate Agent (“CA”) or an Insurance Broker, in accordance with the applicable regulations issued by the Insurance Regulation Development Authority of India (‘IRDAI’). This disallows any unregulated or informal distribution arrangements, including informal referral models or structures that may resemble the outsourcing of distribution without appropriate licensing.

The question arises as to whether NBFCs may act as a master policyholder for group insurance or through Insurance Self-Network Platforms (‘ISNP’), in accordance with the applicable IRDAI regulations.

In our view, the amendment does not restrict the NBFCs from acting as the Master Policy Holder for group insurance policy covering lender-borrower groups, as permitted under the IRDAI_Master_Circular_on_Protection_of_Policyholders_interests_2024 as while acting as a master policyholder, the NBFC cannot draw any commission from the insurance company, it solely acts as a policyholder for the benefit of its customers. In this capacity, the NBFC facilitates enrolment, premium collection, and claims support, without undertaking solicitation in the capacity of an agent or broker.

With respect to ISNP Platforms, only insurance intermediaries are permitted to take registration for operating an ISNP. Therefore, in our view NBFCs shall still be permitted to operate ISNPs.

Further, the recent Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025 has introduced the concept of Managing General Agent (“MGA”) (which is still not implemented by IRDA) by including the same within the definition of “insurance intermediary”. Given that the MGA construct involves undertaking core functions such as underwriting support (assessment of risk only), product design, and distribution facilitation on behalf of insurers, it may fall within the broader ambit of “insurance distribution business”. While the regulatory contours around MGAs are still evolving, NBFCs have not been expressly restricted from acting as MGAs via this amendment, subject to clarity from the IRDAI on permissibility, registration requirement etc. Read our article on Managing General Agents here.

No Routing of Funds through the NBFC/HFC

The UFS Directions earlier provided that the premium shall be paid by the insured directly to the insurance company without routing through the NBFC. This requirement has now been deleted under the present UFS Amendment Directions. It may however, be noted that Section 64VB of the Insurance Act, 1938 provides that,

Where an insurance agent collects a premium on a policy of insurance on behalf of an insurer, he shall deposit with, or dispatch by post to, the insurer,the premium so collected in full without deduction of his commission within twenty-four hours of the collection excluding bank and postal holidays.

Accordingly, in case the NBFC/HFC acts as the corporate agent and collects any insurance amount, the same must be deposited with the insurance company within a period of 24 hours.

Enhanced Disclosures in case of undertaking insurance agency business

The UFS Amendment Directions introduce an explicit requirement for NBFCs to make clear, upfront disclosures to customers that insurance distribution activities are undertaken strictly on a fee-based model and without any risk participation. Unlike the earlier framework where disclosure obligations were largely confined to financial statements (such as notes to accounts) and did not necessarily extend to customer-level communication at the point of sale. While the quantum or percentage of fees is not required to be disclosed, an appropriate disclaimer should be incorporated in the relevant loan documentation and/or on the website/ application through which loan journey is conducted, clarifying that the NBFC does not assume any risk participation in the insurance product and is acting solely in the capacity of an agent for the insurer.

Illustrative Disclaimer- “The Company acts solely as an agent of the insurer for distribution of insurance products. The Company does not underwrite or assume any insurance risk, and all claims, benefits, and liabilities under the insurance policy are the sole responsibility of the respective insurer.”

Mutual Fund Distribution Framework Revised

NBFCs may distribute mutual funds subject to:

Compliance with applicable SEBI regulations and code of conduct;

Compliance with the RBC Directions;

Distribution being undertaken solely on a fee-based, non-risk participation basis and with upfront disclosure to the customer.

Mutual fund houses whose products are distributed must maintain robust grievance redressal systems. The NBFC may also facilitate the redressal of grievances.

MF products should be clearly disclosed to customers by disclosing the products on the website or other digital channels of the NBFC.

Nothing has been specifically provided for Banks in this regard

Pension Distribution / NPS Services

Eligible NBFCs (other than Base Layer NBFCs) meeting prescribed CRAR requirements and having reported profits in the previous financial year may act as Points of Presence (PoPs) for NPS.

Registration with PFRDA remains mandatory.

Activities must be undertaken on a fee basis without risk participation and in compliance with RBI’s RBC Directions and PFRDA guidelines.

Referral business in case of Banks

A specific definition of “Referral Services” has been introduced to mean an arrangement under which a bank may refer its customers to a TPPSP by making available information about the financial products or services offered by the TPPSP. This definition has not been introduced in the case of NBFCs/HFCs.

Banks may refer customers only to products and services regulated by financial sector regulators and must comply with the instructions of the relevant regulator.

Banks may market and refer the TPPS to their customers, but cannot sell under the referral arrangement. This should be made explicitly clear upfront through a disclaimer to the customers.

The name or brand of the bank shall not feature in any of the product/ service documents. This ensures that customers do not misconstrue the product as being offered or backed by the bank.

Banks must publicly disclose the list of TPPSPs and products covered under referral arrangements on their website, mobile application and other digital banking channels.

Product onboarding, servicing and other TPPS-related processes cannot be integrated into the bank’s platform. The bank may only provide a link redirecting the customer to the TPPSP’s platform.

Banks must undertake proper due diligence before entering into referral arrangements with TPPSPs. Particular emphasis is placed on assessing reputational risks associated with the TPPSP.

Banks must ensure that the TPPSP has robust customer grievance redressal mechanisms in place before referring customers.

Grievance Redressal Mechanism

Under the erstwhile IRDAI (Registration of Corporate Agents) Regulations, 2015, corporate agents were permitted only to provide guidance and advisory to customers on issues arising during the course of an insurance contract. However, pursuant to the IRDAI (Protection of Policyholders’ Interests, Operations and Allied Matters of Insurers) Regulations, 2024, it has been mandated that every insurer and distribution channel shall establish robust procedures and effective mechanisms for the efficient and timely resolution of policyholder and/or claimant grievances.

In alignment with the above, the RBI, through its UFS Amendment Directions, has required NBFCs to ensure that the insurance companies whose products are distributed by them have adequate and effective customer grievance redressal mechanisms in place. Additionally, NBFCs may facilitate the redressal of such grievances.

Policy Mandate

The UFS Amendment Directions proposes to delete Para 6 of the UFS Direction, which requires NBFCs to put in place a broad Board-approved policy governing the distribution of third-party financial products, including insurance products. A closer reading indicates that the change is primarily structural rather than substantive, as the underlying policy requirement has already been added within the RBI’s RBC Amendment Directions, through the insertion of Para 101A, which mandates every regulated entity to adopt a comprehensive policy covering advertising, marketing, and sales of both its own and third-party financial products and services.

It is also relevant to note that, independent of RBI requirements, sectoral regulators already mandate similar requirements. For instance, IRDAI requires corporate agents to maintain an open architecture policy and a grievance redressal policy. As such, most NBFCs engaged in these activities are likely to have comparable policies already in place. Consequently, we understand that where an NBFC has already adopted policies to comply with the RBC Amendment Directions or applicable sectoral regulations, those frameworks would adequately satisfy the regulatory expectation.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-16 12:29:402026-06-17 11:16:53Agency and referral activities of NBFCs and Banks: RBI June 2026 Amendments

Section 56(2)(viib) of the Income-tax Act, 1961, popularly known as the “Angel Tax” provision, was introduced to prevent the routing of unaccounted money through the issue of shares at a high premium. In an important ruling discussed below, the Delhi ITAT held that this anti-abuse provision should be applied only to transactions that fall within its intended purpose and should not be mechanically invoked in genuine transactions between group companies.

Facts of the case

OYO issued CCPS to its holding company Oravel Stays Ltd. following a court-approved demerger of its India hotel business.

Oravel’s holding reduced from 100% to 99.6% solely due to the demerger — parent-subsidiary relationship maintained throughout.

Shares issued at substantial premium based on DCF valuation report.

Capital infused was FEMA-compliant downstream foreign investment.

AO alleged shares were issued in excess of FMV and made an addition of ₹3,885.52 crore under Section 56(2)(viib).

Issues Before the Tribunal

Whether Section 56(2)(viib) applies to shares issued by a subsidiary to its holding company.

Whether AO can reject DCF valuation and substitute NAV method.

Whether premium on conversion of CCPS into equity is taxable under Section 56(2)(viib).

AO’s Findings

Rejected DCF valuation citing negative net worth, losses and aggressive COVID-era projections.

Treated excess consideration over FMV as taxable income under Section 56(2)(viib).

ITAT’s Findings

Section 56(2)(viib) being an anti-abuse provision cannot extend to bona fide holding-subsidiary capital infusions absent any money laundering concerns.

AO acted beyond jurisdiction by rejecting merchant banker’s DCF report — tax authorities lack expertise to redo such valuations.

FEMA-compliant downstream investment cannot be treated as unaccounted money — foundational assumption of Section 56(2)(viib) fails.

Key Takeaways

Section 56(2)(viib) must be interpreted purposively — it targets unaccounted money, not genuine intra-group restructurings.

AO cannot disregard a registered valuer/merchant banker report without strong and cogent reasons.

FEMA compliance creates a strong presumption of genuineness against Angel Tax application.

Entire addition of ₹3,885.52 crore deleted by ITAT.

Note: Section 56(2)(viib) of the Income-tax Act, 1961 has been omitted with effect from 1 April 2025 and accordingly is no longer applicable from Assessment Year 2026–27 onwards.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-14 13:26:062026-06-24 11:38:49Workshop on RBI Directions on Responsible Business Conduct and Third Party Product Selling

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2026-06-13 13:00:382026-06-24 11:39:38Workshop on Insider Trading Regulations for Compliance Officers

Loading…

Loading…