https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2023-06-16 13:35:422023-06-23 15:53:44Workshop on SEBI LODR 2nd Amendment Regulations, 2023

The importance of transparency and timely dissemination of material information for a listed entity needs no emphasis, since most of these events and information may have a direct bearing on the price discovery of the securities of the listed entities and the investors’ decisions. The intent of Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“Listing Regulations”) is to ensure a seamless flow of information; the Regulation is complemented by Schedule III thereto, which provides an indicative list of the events or information in a listed entity that may be considered “material” and thereby, requires prompt disclosure by way of intimations to the stock exchange(s) in which the entity is listed.

While Para A of Part A of Schedule III specifies the list of information/ events which are “deemed” material, Para B specifies a list of information/ events which are to be tested based on the application of guidelines of materiality. Further, Para C requires intimation of any major development that is likely to affect the business and Regulation 30 also provides a residuary provision of intimation of any other information or event that does not fall either under Para A or Part B of Part A of the Listing Regulations, however, is material. The guidelines of materiality for the purpose of testing the events/ information under Para B of Part A of Schedule III are provided in sub-regulation (4) of Reg 30 and are supposed to be documented in the policy for determination of materiality (“Materiality Policy”) of the listed entity. The Materiality Policy of a listed entity plays a prominent role in determining the disclosure practices of a listed entity.

SEBI vide an amendment notification dated 14th June 2023 has notified (“Amendment Regulations”) several changes to the Listing Regulations which were earlier proposed in a Consultation Paper with respect to the disclosure of material events. The same has now been incorporated under the Listing Regulations itself. A few of these include :

Quantifying the meaning of “material”, thereby limiting discretion with the listed entities,

Requiring amendments in Materiality Policy;

Reducing timelines for disclosures;

Mandatory verification of market rumours by top 100 (250 from FY 24-25) listed entities;

Broadening and shuffling of the events/ information listed under Schedule III etc.

The Amendment Regulations are applicable from the 30th day of the publication of the notification, i.e., on and from 14th July, 2023. Further, the amendments are applicable only to the equity-listed entities, since debt-listed entities including High-value Debt Listed Entities are outside the scope of Regulation 30. We have listed some of the major amendments in this write-up.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Payal Agarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPayal Agarwal2023-06-16 00:55:492023-10-03 11:32:21Getting material on “material” events and information:

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-06-13 12:58:472023-08-30 12:35:43FAQs on Social Stock Exchange

The article was also published in the CRA E-Bulletin and can be viewed here

Background

Passing the torch, lighting the way – an expression that can be used to refer to succession planning. Be it a household, business organization or institution, succession planning is needed everywhere. In a household, as the family possessions and culture are passed on, it is simply termed as continuing the legacy. In an HUF, according to HUF laws, after the Karta (head of the HUF) dies, the senior most coparcener becomes the head of the HUF. In corporates, the larger the scale and complexity of business, the need for succession planning becomes much more important. Unlike in the case of a household, corporates involve the livelihood and interests of thousands of people, i.e., the shareholders, vendors, customers and other stakeholders. The intent of succession planning is not to oust the leader from his / her position but to prepare the next generation to become the future leaders. Succession planning is required to ensure smooth running of business. The torch bearer (leader here), has to groom his / her successor to take over his role.

In an organization, succession planning is an important element of corporate governance. In this write-up, the author has tried to emphasize on the need and importance of succession planning.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Anushka Vohrahttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngAnushka Vohra2023-05-25 16:22:202023-06-05 13:16:27Succession planning: failing to plan is planning to fail

The article was also published in the CRA E-Bulletin and can be viewed here

Background

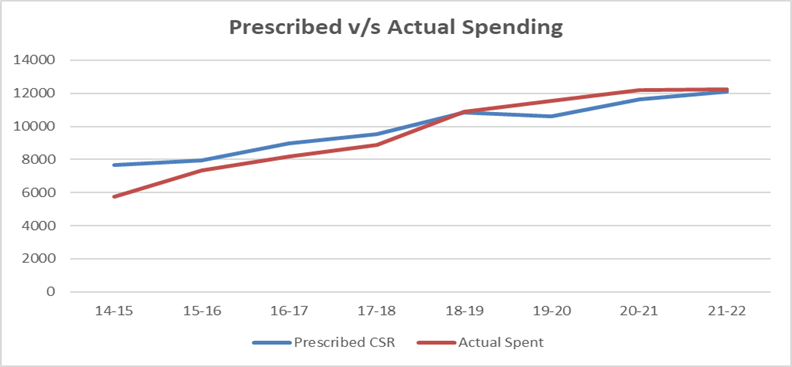

While the sense of ‘Corporate Social Responsibility’ (‘CSR’) might have been the result of the statute, first on a “comply or explain” basis, and later, as a mandate, it is heartening to note that companies are now not looking at CSR as a mere compulsion, but are seeing this as an instrument for social bridge-building. As is well known, the provisions were introduced, arguably as a unique case globally, in 2014 under the Companies Act, 2013 (‘Act’). From that year till FY 2021-2022, companies have spent approximately INR 1,39,202 crores[1] on CSR activities. In fact, it is pleasantly surprising to note that companies have been targeting to spend their minimum obligations; the gap between the prescribed spending and the actual spending has consistently been narrowing as can be seen from the graph given below. With the introduction of the Companies Corporate Social Responsibility Policy (Amendment) Rules, 2021[2], read with the changes under section 135 of the Act pursuant to the Companies (Amendment) Act, 2019[3], an element of penalty for not doing the needful has been added, at the same time permitting companies to overspend their obligation and claim a set off within the next 3 years, there are several companies which are spending more than their targets.

Data Source: India CSR Outlook Reports

Having said that, it will be important to discuss whether spending itself will help attain the motive for which the CSR framework was introduced? CSR is a part of a larger business responsibility and sustainability. If companies confine their CSR ideologies to simply adding up to a requirement of spending amount, will the society get back what it ought to be getting back form a responsible business? Should companies look at CSR beyond mere spending, and construct a CSR vision based on the negative footprints created by their activities, if any, or otherwise, create social impact relevant to their businesses?

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Pammy Jaiswalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPammy Jaiswal2023-05-07 18:18:572023-05-25 13:17:35Need for strategic vision in CSR spending by companies

As climate change and its impacts continue to remain one of the major concerns of any economy, transition finance is a step towards effectively transforming carbon emissions and combating climate change.

‘Transition Bonds’, as the word speaks for itself, are debt instruments that facilitate transition of a carbon-intensive business into decarbonizing business and eventually achieving the Net Zero emissions targets.

While it is true that change is the only constant, it cannot be denied that the same can often be challenging. Similar is the case with enterprises looking to metamorphosize their activities into a sustainable form. A huge amount of finance is required for carbon-intensive sectors to decarbonize and it is here that transition bonds find their application.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2023-05-06 15:35:012023-05-23 17:44:08Financing transition from “brown” to “green”

Legal Entity Identifier (LEI) Code is a unique 20-digit code used to identify legal entities that engage in financial transactions worldwide in order to improve the quality and accuracy of financial data systems for better risk management post the global financial crisis by establishing a global reference system.

Prior to the present SEBI Circular, all non-individual borrowers availing an aggregate exposure[1] of Rs. 5 crore and above from banks and financial institutions were mandated to obtain LEI Code over the prescribed timeline.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-05-04 14:35:492023-06-08 10:25:45Legal Entity Identifier Code now mandatory for bond issuers

Our Resource Centre on Related Party Transactions can be viewed here

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kotharihttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari2023-05-01 16:06:092023-05-01 16:23:46Evolution of concept of related parties and related party transactions

Loading…