Need for strategic vision in CSR spending by companies

– Pammy Jaiswal, Partner | corplaw@vinodkothari.com

| The article was also published in the CRA E-Bulletin and can be viewed here |

Background

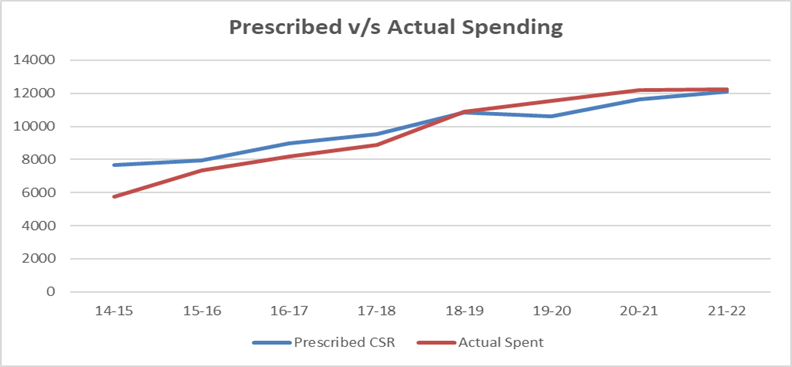

While the sense of ‘Corporate Social Responsibility’ (‘CSR’) might have been the result of the statute, first on a “comply or explain” basis, and later, as a mandate, it is heartening to note that companies are now not looking at CSR as a mere compulsion, but are seeing this as an instrument for social bridge-building. As is well known, the provisions were introduced, arguably as a unique case globally, in 2014 under the Companies Act, 2013 (‘Act’). From that year till FY 2021-2022, companies have spent approximately INR 1,39,202 crores[1] on CSR activities. In fact, it is pleasantly surprising to note that companies have been targeting to spend their minimum obligations; the gap between the prescribed spending and the actual spending has consistently been narrowing as can be seen from the graph given below. With the introduction of the Companies Corporate Social Responsibility Policy (Amendment) Rules, 2021[2], read with the changes under section 135 of the Act pursuant to the Companies (Amendment) Act, 2019[3], an element of penalty for not doing the needful has been added, at the same time permitting companies to overspend their obligation and claim a set off within the next 3 years, there are several companies which are spending more than their targets.

Data Source: India CSR Outlook Reports

Having said that, it will be important to discuss whether spending itself will help attain the motive for which the CSR framework was introduced? CSR is a part of a larger business responsibility and sustainability. If companies confine their CSR ideologies to simply adding up to a requirement of spending amount, will the society get back what it ought to be getting back form a responsible business? Should companies look at CSR beyond mere spending, and construct a CSR vision based on the negative footprints created by their activities, if any, or otherwise, create social impact relevant to their businesses?

Sustainable business is also a sign of a responsible business since the former includes incorporating certain practices and mechanisms which helps to strategize the company’s objectives without compromising on the social and environmental needs. We may also refer to the recently introduced Corporate Sustainability Reporting Directives[4] (‘CSRD’) by the European Union which highlights one of the facts that carrying out CSR along with responsible and sustainable business practices are integral to a company’s long term sustainability targets.

This write up dwells on the need to look at CSR with a focus on business responsibility, and spending with a strategic vision which should guide companies while choosing their CSR activities. While the larger conspectus will still be limited by Schedule VII, however, it should be obvious that not everything in Schedule VII is the right CSR spend for a particular company. Therefore, the flavor of this article is not to bifurcate between an eligible spending versus a non-eligible CSR spending, but rather to draw the attention of the readers to the fact that if companies are guided by a particular CSR vision, based on their business footprints on the society and the environment, the much needed impact will be visible to the world at large and India can set an example before the world of what a visioned CSR spending can do to the society!

The CSR framework in India: Lawmakers’ intent

So when the provisions of the CSR were first introduced under the Act in the year 2014, the then Minister of Corporate Affairs (‘MCA’) said in one of his statements that “the government has left the canvas wide open for the companies to decide on their own about CSR activities they wish to undertake to comply with the new norms[5]. At the same time, he also mentioned that “Industry would be free to choose programmes and strategies best aligned to their corporate philosophy and businesses.

Further, taking the same forward the then MCA Additional Secretary said that “when it came to embedding CSR into business strategy, the execution and mainstreaming of strategy was of paramount importance.”[6]

Accordingly, this makes it clear that the thought of introducing the CSR framework was to give back or pay back or replenish the resources that the companies are taking from the society. Whether it is the human resources or other materialistic resources that it takes to run its business, it must also think to repair and restore these resources to the extent possible.

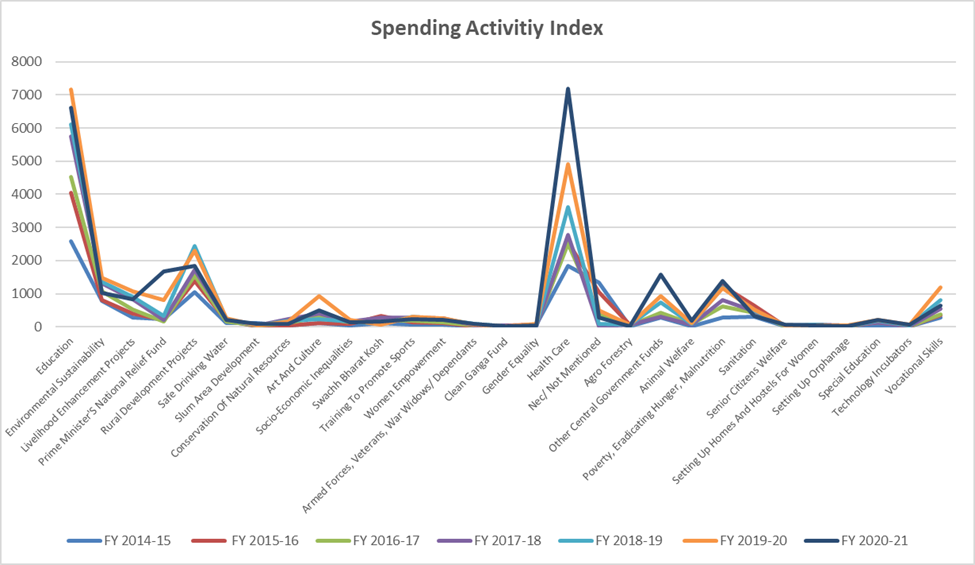

Given this fact, it is also interesting to note the spending index on CSR since the year of its introduction. As can be seen from the graph depicted below, spending has been the highest in education and healthcare, while the least amount has been spent on conservation of natural resources, training to promote sports, women empowerment, special education or senior citizen welfare. Further, the peak of healthcare activity was during the COVID break in 2019-2020 and 2020-2021 where companies had spent the most.

Based on the said graph, it is following have been the most popular activities:

i. Health care

ii. Education

iii. Rural development

iv. Art and culture

v. Eradicating poverty, hunger and malnutrition

On the other hand, the following activities have been least popular:

i. Socio-economic inequalities

ii. Setting up orphanages

iii. Special education

iv. Agroforestry

v. Senior citizen welfare

Data Source: csr.gov.in

Compliance with CSR obligations: Gaps under the present-day approach

It is important to note that while companies have been diligent enough to ensure that their CSR spending obligations are fulfilled, however, quite often it has been noted that the same is looked at from a very narrow perspective. Ideally, where the business houses should have aligned their business objectives with their CSR vision, the present day approach in several cases is deduced to a mere tallying to add up to the minimum CSR budget , or obliging to the wishes of the local bodies and commitments made by the promoters and companies. In some other cases, CSR spending has been left to be treated as a tick box compliance or even furthering the marketing needs of the companies. The same has been discussed in brief below:

- Tally Approach

It has been observed that several companies simply focus on adding up to the CSR spending to meet the minimum CSR spending obligations. While the spending is on Schedule VII activities, however, on a closer look, it will be evident that there is no nexus between the business activities of the company and the activities undertaken by them as CSR. Companies completely disregard the aspect of tallying the CSR activities undertaken by them with the business objectives.

- Promoter commitments to local bodies

Quite often we also come across cases where companies receive requisitions or appeal letters from local bodies or associations for contributing towards certain philanthropic activities. Given the prior commitments by promoters/ senior management for the same, companies spend the CSR funds without recognizing any need for identifying the same as CSR in the first place or even if covered under CSR, then completely disregarding the connection with the negative footprints of business activities.

- Means for marketing the activity rather than undertaking the activity itself

Often companies end up spending in activities that it contends to be a CSR activity, without actually spending much on the activity itself. In these cases, it is seen that the companies, knowingly or unknowingly, use the funds for marketing of either ideas or products related to the business which has a potential to do social good, however, missing out on doing the activity that can make a difference. Here, it is important to note that stressing on and asking people to do good versus taking initiatives to carry out the activities itself, the companies tend to use the funds on the former while it should either have been a mix of the two with the latter using a major portion of the funds or the latter activity itself.

- Tick box approach

Yet another gap, as is commonly observed, is the approach of companies for carrying out CSR activities as a tick box compliance. Companies simply spend the funds for activities without any monitoring over the same. These cases are akin to donation and charitable contributions rather than falling under the CSR activities.

Having discussed the above shortcomings, it is also significant to mention that not all cases suffer from the aforesaid gaps. However, there are companies which, due to certain limitations or may be lack of understanding, fail to comply with the CSR framework in spirit. Therefore, it is now imperative to discuss the vision-oriented approach with the readers to unequivocally bring the understanding on the same page.

Fulfilling CSR obligations: Vision-oriented approach

As discussed above, aligning the business objectives with the CSR practices will lead to achieve CSR targets as envisaged by the company from the very beginning. As compared to the approach where every activity undertaken is looked at on a standalone basis without any holistic perspective, a vision-oriented approach would lead to strategizing the responsible business needs with that of the social and environmental needs.

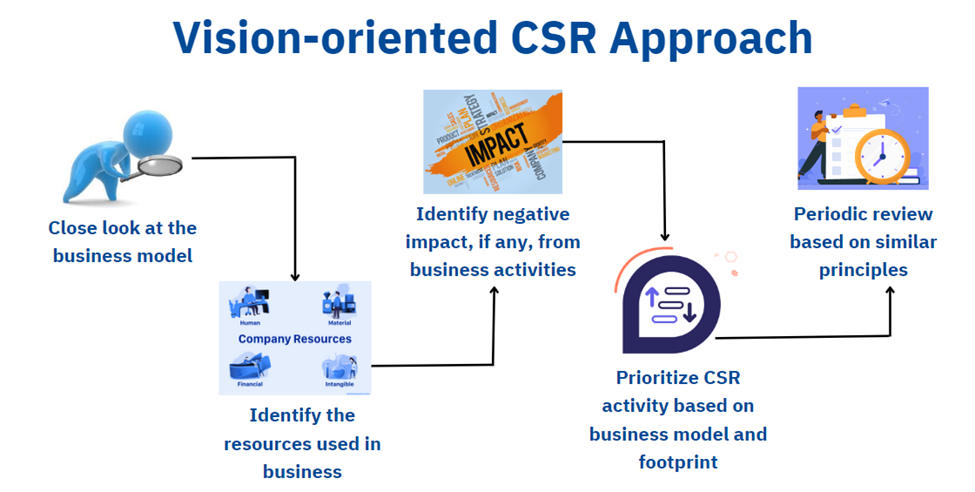

Every business house is using some resource in some form, whether it is the natural resources, human resources, environmental engagements, etc. Therefore, instead of choosing any random activity from Schedule VII, companies should rather formulate a blueprint of their holistic CSR impact targets based on the footprints of their business activity. The following steps may act as a guide to initiate the approach for having a vision-oriented CSR in a company:

Step 1 – Take a close look at the business model of your company;

Step 2 – Identify the resources used for running the business starting from the base level;

Step 3 – Identify the negative impact, if any, caused by the business activities, if whichever form;

Step 4 – Prioritize the selection of the appropriate activity from Schedule VII, based on the business model and footprint which may further include:

- Neutralisation/ resurrection where the business leaves behind pollution or depletion of natural resources;

- Local area development where company in question employs or engages substantial local resources;

- Mass engagement, upliftment, livelihood enhancement drives where companies have mass franchise/ consumer goods, etc.

- Other activities, if it does not fall under any of the above categories.

Step 5 – Periodic review based on the same principles.

Considering the activities which are best aligned with one’s business model is what is required to be understood by companies while choosing the activity under Schedule VII. For example, if a company is engaged in mining activities, it is obvious that there are several environmental and social impacts created therefrom. Therefore, amongst the entire list of the activities under Schedule VII, activities related to environmental protection, sustainability, livelihood enhancement projects, etc. more than anything else.

Similarly, if we talk about the cement sector in India, the carbon emissions from the cement industry in India is lower when compared to the other cement industries in the world, however, neutralizing carbon footprint is surely one of the most important initiatives by this sector. On a limited study of a few large-scale companies in this sector we found that the major spending from this sector is in rural development, livelihood enhancement projects including education, health, and donation to PMCARES Fund. However, besides the advancement in technology in the business processes, the responsible CSR could be by focusing their CSR targets on activities such as afforestation, green cover, livelihood enhancement, health-oriented activities.

As far as the plastic manufacturing industries are concered, one of the most evident footprints of this sector is linked with environmental concerns, therefore, undoubtedly, this sector should think of a strategy to neutralize its footprint on the environment.

Lastly, if we discuss about the manufacturing sector in general as compared to the service sector or trading sector, it is obvious that except for those units wherein the companies have either shifted their technology to pollution free techniques or the set-up itself is such that is pro-environment, in other cases, the most common issue is the pollution caused in the local areas as well as the inconvenience causes to the local people. In such cases, in addition to the activities for controlling pollution like increasing green cover, planting trees, or other tech-savvy devices which can help control pollution, focus should also be on the effect on the human resources or locals living around the factory premises. Whether it be in terms of health projects, or vocational training, or educational projects, etc., should also be seen as a sign of a responsible business from the companies’ point of view.

Conclusion

While many companies already have undertaken strategic based CSR which gels well with their core competencies as well as the business models, however, considering that there are still gaps in the present-day approach, it is imperative to raise this concern now so that the concept of a vision-oriented CSR becomes familiar to those who are required to undertake CSR. The said concern was also raised by one of the drafting persons of the National Guidelines on Responsible Business Conduct in the year 2020[7]. It may also not be surprising if the lawmakers bring this requirement as a part of the CSR framework itself in the near future. Therefore, it will be a better idea to understand the concept and the requirements so as to initiate the implementation of a vision or strategy based CSR.

[1] https://www.csr.gov.in/content/csr/global/master/home/home.html

[2] To view the same, click here, effective from 22nd January, 2021

[3] To view the same, click here, effective from 22nd January, 2021

[4] To read about CSRD click here effective from 5th January, 2023

[5] To read the article click here

[6] To read the article click here

[7] https://www.downtoearth.org.in/interviews/governance/csr-in-india-long-term-vision-is-a-must–69359

Leave a Reply

Want to join the discussion?Feel free to contribute!