Japanese Capital Takes Flight in Indian Skies: India’s First JOLCO Leasing Deal

Simrat Singh | Finserv@vinodkothari.com

IndiGo has reportedly entered into a transaction to lease two aircraft through a Japanese Operating Lease with Call Option (JOLCO) structure, marking the first instance of an Indian airline accessing Japanese equity-backed aircraft financing. The structure involves Japanese investors and banks funding the acquisition of the aircraft through a leasing special purpose vehicle (SPV), which then leases the aircraft to the airline through a GIFT City based entity. This development comes barely a month after India notified the Protection of Interests in Aircraft Objects Rules, 2026, in January 2026 under an Act having the same name. The statute was itself notified in April 2025. Separately, India had made amendments to insolvency laws to fall in line with the Cape Town Convention [see MCA Notification dated 03.10.2023]. Notably, India had signed the Convention in the year 2008.

The Cape Town Convention is all about creditor protection by providing clear and swift remedies to secure their interests in high value mobile equipment such as aircrafts. These legislations gave domestic legal effect to Cape Town Convention and its Aircraft Protocol Rules (discussed below). Aircraft lessors globally value their ability to repossess an aircraft if the airline in a domestic jurisdiction has suffered an insolvency event. The legal certainty of lessor’s rights is a major factor in international leasing transactions. This legal certainty, though already vindicated in rulings such as Kingfisher1 could have been a major factor in consummation of this deal.

In this write-up, we briefly examine the JOLCO structure, the rationale for structuring the arrangement as an operating lease to enable depreciation benefits for the lessor and the importance of the Cape Town Convention in facilitating such cross-border aircraft leasing transactions.

Introduction

Leasing is one of the most common ways of financing acquisition of aircraft by the global aviation sector. The share of leased aircraft has increased significantly over time, rising from around 10% of the global fleet in the 1970s to nearly 58% by the end of 2023. Against this global average, India exhibits an even higher reliance on leasing, with approximately 80% of its commercial aircraft fleet being leased.

India’s aviation sector has witnessed rapid growth in recent years. The country has emerged as one of the fastest-growing aviation markets in the world, recording around 241 million air passengers in 2024, making it the fifth-largest aviation market globally. Not only has air travel become a very commonly used mode of travel in a prosperous country, the Country has also enabled major infrastructural facilities by adding new airports, expanding existing ones, etc. The number of operational airports in India has increased from 74 in 2014 to about 163 by 2025.

Thus, leasing plays a dominant role in India’s aviation sector, with the majority of airline fleets being leased rather than owned. Historically, this market has been heavily reliant on overseas leasing hubs such as Ireland, with aircraft acquisitions commonly financed through structures such as export credit supported Loan Covered Risk Amount (LCRA) financing. Recognising this dependence, the Government of India launched Project RAFTAAR under the Ministry of Civil Aviation to develop an aircraft leasing ecosystem at GIFT City, with a working group of industry experts that included Mr. Vinod Kothari, which gave various proposals aimed at promoting aircraft leasing from India. (The report can be read here). The green shoots from this strategic initiative have now clearly started growing and blooming, with the number of registered aircraft lessors in IFSC growing to 33, which has leased 242 aviation assets including 90 aircrafts and 67 engines as on March 2025.

The JOLCO structure

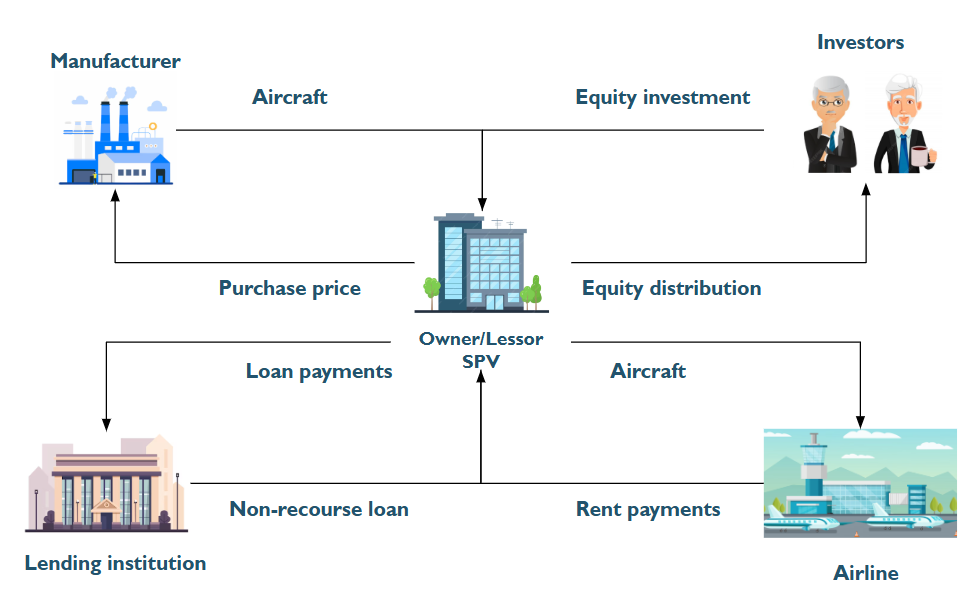

A JOLCO transaction involves Japanese equity investors (institutions, HNIs etc.) and banks financing the acquisition of an aircraft through a SPV. The investors invest in the SPV through a Tokumei Kumiai structure which essentially grants a tax-pass through to the SPV, allowing the investors to claim income/losses of the SPV and depreciation on the SPV assets. The SPV uses the equity and bank debt to purchase the aircraft from the manufacturer and subsequently leases the aircraft to the airline (in the present case to the GIFT City WOS of the airline which will then sub-lease it to the airline) under a long-term operating lease arrangement with tenure of 8-10 years.

The airline pays periodic lease rentals to the SPV (in present case to GIFT City WOS which then in turn pays to the SPV) [see Fig 2 below], which are applied towards servicing the bank debt and providing returns to the equity investors. The structure includes a call option in favour of the airline, allowing it to purchase the aircraft at a pre-agreed price at the end of the lease term. The main advantage of this structure for the lessor-investors is the tax relief availed by them under Japanese tax laws (discussed below) and for the lessee, the reduced lease rentals as compared to other models.

While the structure includes a call option in favour of the airline, this does not necessarily convert the lease into a finance lease. The call option is not a bargain purchase option, but is exercisable at a pre-agreed price that reflects the expected fair value of the aircraft at the end of the lease term. Since ownership does not automatically transfer and the option price is not nominal, the residual value risk/asset based risk remains with the lessor during the lease term. Accordingly, the arrangement continues to be characterised as an operating lease, allowing the lessor to retain tax ownership and claim depreciation under Japanese tax laws. Another reason for incorporating a call option is that the investors typically have no operational capability or commercial intent to take delivery of the aircraft at the end of the lease term. Since the aircraft is owned purely as a financial investment, the investors generally prefer that the airline either extend the lease or exercise the purchase option. The call option therefore provides a practical exit mechanism for the investors at the end of the lease period. The other conditions of the lease agreement, such as redelivery, are also designed so as to ensure that the call-option is exercised.

Rationale for selecting it as operating lease

JOLCO is an operating lease, which means the lessor SPV retains the risks and rewards of the asset. This retention is critical from a tax perspective, as it enables the Japanese investors to claim depreciation on the aircraft under Japanese tax rules. Japanese tax rules permit a declining balance depreciation method that front-loads expense recognition. For aircraft assets, the rates enable up to 20% depreciation2 annually which means that in the initial years the investors can claim a substantial amount of depreciation. This is contrasted with the typical tenure of the lease period which is around 10 years. For instance, if an aircraft costing USD 100 million allows depreciation deductions of USD 40 million over the initial 3 years, the rentals during the corresponding period will be much lesser, leaving the difference as a tax shelter. This depreciation expense, net of the lease rentals, will be offsetted against the investors’ taxable domestic income in Japan, generating tax benefits that form a significant component of the investors’ overall return. Since part of the return in JOLCO is derived from these tax claims, the investors are able to accept relatively lower lease rentals, reducing the effective financing cost for the airline. Interest payments on the loan are also tax deductible for the investors.

Fig 1: Structure of a JOLCO deal

A finance lease structure would not achieve the same outcome, as it transfers the risks and rewards of ownership to the lessee and may be characterised as a financing arrangement rather than a true lease. In such cases, the economic ownership of the asset may be regarded as residing with the user of the asset i.e. the airline, which could disallow the ability of the lessor investors to claim depreciation on the aircraft.

Role of GIFT CITY

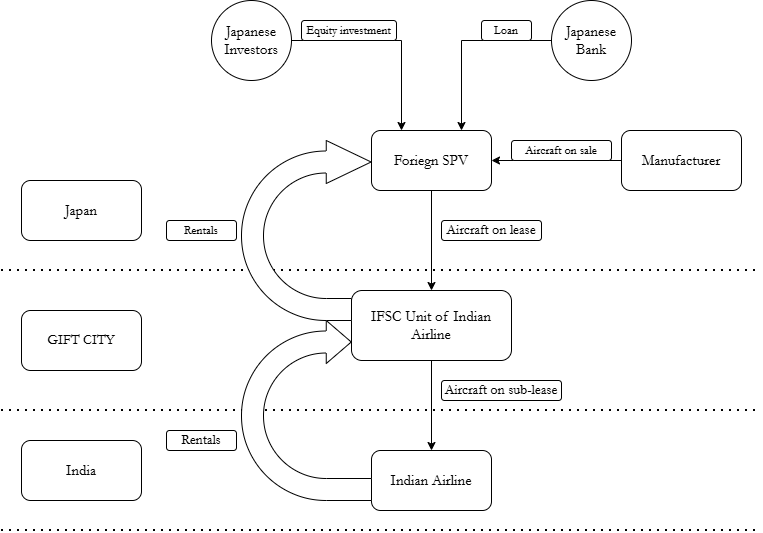

In the present JOLCO deal, the aircraft is expected to be leased by the Japanese SPV to the airline’s IFSC-based wholly owned subsidiary at GIFT City, which will then sub-lease it to the airline. Routing the transaction through GIFT City instead of a direct transaction between the Indian airline and foreign lessor ensures no tax leakage. The same is explained below:

- If the aircraft were leased directly by the Japanese SPV to IndiGo, the lease rentals would be characterised as ‘royalty’ for the use of industrial equipment under Section 9(1)(vi) of the Income Tax Act, 1961. Since the payer is an Indian resident and the aircraft is used in India, such royalty is deemed to accrue or arise in India, triggering withholding tax of 10% under Section 195;

- The insertion of an IFSC leasing entity at GIFT City helps mitigate this tax friction through provisions introduced specifically to develop India as an aircraft leasing hub:

- First, when the Indian airline pays lease rentals to the IFSC leasing entity, those payments do not attract withholding tax where the IFSC unit is availing the tax holiday under Section 80LA;

- Second, royalty income received by a non-resident lessor from the IFSC unit engaged in aircraft leasing is exempt from tax in India [see section 10(4F)]. As a result, lease rentals paid by the IFSC entity to the Japanese SPV would not be taxable in India;

- Third, the IFSC also provides capital gains relief for transfer of aircraft leased by IFSC units, enabling tax-efficient exit of the asset at the end of the lease cycle. In addition, the Government of Gujarat has waived stamp duty on aircraft leasing and financing transactions executed in IFSC, reducing transaction costs at the state level.

See more on aircraft leasing in GIFT IFSC here.

Fig 2: Deal structure

Significance of Cape Town Convention and IBC

For cross-border aircraft leasing transactions, lenders and lessors place much weightage on their ability to repossess the aircraft in the event of airline default. Financers require legal certainty that their ownership or security interests can be quickly enforced if payments stop. The Cape Town Convention on International Interests in Mobile Equipment establishes a uniform framework for registering and enforcing such interests including mechanisms such as time-bound possession. The importance of such protections became evident during the Go Air Insolvency where aircraft lessors faced significant difficulty repossessing aircraft due to the moratorium under the IBC (See our article on Go Air insolvency and Cape Town Convention here).

In April 2025, India enacted the Protection of Interests in Aircraft Objects Act, 2025 and notified its rules in January 2026, giving domestic legal effect to the Cape Town Convention and its Aircraft Protocol Rules. The legislation is intended to align India’s aviation financing framework with global standards and facilitate quicker repossession and enforcement of lessor rights, improving investor confidence in leasing transactions involving Indian airlines. Upon a combined reading of the 2023 notification and the Protection of Interests in Aircraft Objects Act, 2025, the moratorium under Section 14 of the IBC will not prevent enforcement of rights in respect of aircraft objects covered under the Cape Town framework. Consequently, upon default by the lessee, creditors and lessors may exercise the remedies available under Articles 8 to 10 of the Cape Town Convention, including repossession, deregistration and export of the aircraft. This was important specially since the NCLAT ruling of Go Air3 upheld the moratorium on Go Air, which left international lessors in a limbo.