Basics about formation of Nidhi companies

By CS Megha Saraf

Nidhi as the Hindi word denotes “sampatti” is a type of public company which may be incorporated with an exclusive object of cultivating the habit of thrift and savings amongst its members, deposits from, and lending to, its members only, for their mutual benefit. The same is a type of company which may be incorporated under Section 406 of the Companies Act, 2013, read with the applicable rules, as a public company with a minimum paid-up equity share capital of Rs. 5 lakhs. Although the activities of a Nidhi company is similar to that of a non-banking financial company, as to accepting deposits and granting loans, however, they have been exempted from the purview of the RBI Act, 1934 by virtue of the RBI Master Direction- Exemptions from the provisions of RBI Act, 1934.

Requirements for incorporating a Nidhi company

In order to incorporate a Nidhi company, it shall have:

- atleast 200 members;

- Net Owned Funds of Rs. 10 lakhs or more;

(Note: Net Owned Funds= aggregate of paid up equity share capital + free reserves – accumulated losses and intangible assets appearing in the last audited balance sheet)

- Unencumbered term deposits of atleast 10% of the outstanding deposits;

- Ratio of Net Owned Funds to deposits not more than 1:20;

- Issuance of shares of nominal value of atleast Rs. 10 each;

- To allot a minimum of 10 equity shares or shares equivalent to Rs. 100.

In order to clarify point no. 4, let us take an example; Company X has 20 equity shares of face value of Rs. 10 each. Mr. A, an individual shall be required to subscribe atleast 10 equity shares in order to deposit Rs. 2000 in the Company. Further, as evident, such subscription of equity shares shall not provide any interest to the deposit holder, but, shall form part of the shareholders’ funds of the company.

Requirements w.r.t deposits and loans

As mentioned above, the objective of a Nidhi company is to take deposits and provide loans to its members. The Ministry of Corporate Affairs (“MCA”) being the regulator of Nidhi companies has regulated the norms for taking deposits and providing loans which are as follows:

Deposits

The Nidhi company shall be allowed to accept deposits with the following timelines:

- Fixed deposits- 6 to 60 months

- Recurring deposits- 12-60 months

- Recurring deposits relating to mortgage loans- Maximum period shall correspond to the repayment period of loans granted.

Interest rate on deposits

- Savings Account- Maximum 2% above the rate allowed by nationalized banks

- Fixed and Recurring deposits- At par with the RBI rate

Loans

A Nidhi company can provide loan to its members as per the following ceiling limits:

- Where total amount of deposits from its members is less than Rs. 2 Cr- Rs. 2 lakhs

- Where total amount of deposits from its members is more than Rs. 2 Cr but less than Rs. 20 Cr- Rs. 7.50 lakhs

- Where total amount of deposits from its members is more than 20 Cr but less than Rs. 50 Cr- Rs. 12 lakhs

- Where total amount of deposits from its members is more than Rs. 50 Cr- Rs. 15 lakhs

Interest rates of loans

The interest charged on any loan given by a Nidhi company shall not exceed 7.5% above the highest rate of interest offered on deposits by Nidhi and shall be calculated on reducing balance method.

General restrictions or prohibitions

Similar to a NBFC, there are certain restrictions or prohibitions on Nidhi companies as well.

Some of the major restrictions or prohibitions of a Nidhi company are that it shall not:

- carry on the business of chit fund, hire-purchase finance, leasing finance, insurance or acquisition of securities issued by any body corporate;

- open any current account with its members;

- accept deposits from or lend to any person, other than its members;

- carry on the business other than the business of borrowing or lending in its own name;

- take deposits or lend money to any body corporate;

- issue of advertisements in any form soliciting deposits;

- pay brokerage in order to mobilize deposits from members or for deployment of funds or for granting loans

Compliances to be made by Nidhi companies

Nidhi companies shall be required to do the following compliances:

- Filing of return of statutory compliances in e-Form NDH-1– Within 90 days of the close of first F.Y. and where applicable, the second F.Y.

- Filing of non-compliance with the conditions mentioned w.r.t incorporation of a Nidhi company such as minimum no. of members, Net Owned Funds etc. in e-Form NDH-2– Within 30 days of the close of first F.Y.

- Filing of half-yearly return in e-Form NDH-3– Within 30 days of the conclusion of each half year.

To read our other articles click here

New lease accounting standard kicks off from 1st April, 2019

Financial Services Division

(finserv@vinodkothari.com)

The Ministry of Corporate Affairs (MCA) has put a small announcement on its website that the new lease accounting standard, IndAS 116 will get implemented from 1st April 2019. The new Standard, globally implemented in several countries from 1st Jan 2019, is called IFRS 16. The Standard eliminates the 6-decade old distinction between financial and operating leases, from lessee accounting perspective, thereby putting all leases on the balance sheet. The phenomenon of off-balance sheet lease transactions was one of the burning analyses after bankruptcy of Enron in 2001, and since then, had been erupting off and on, until the global standard setter decides to push the new standard on the rule book in Jan 2016, effective 1st Jan 2019.

After the introduction of IFRS 16, the ICAI came out with an exposure draft on the new standard in 2017 and kept it open for comments for some days. However, nothing further was heard about it thereafter.

The exposure draft and the final published Ind AS 116 are same except for the below mentioned change which has been incorporated in the final published Ind AS 116:

| Para 47 dealing with presentation in books of lessee: | |

| In Exposure Draft | Text of published Ind AS 116 |

| Para 47 A lessee shall either present in the balance sheet, or disclose in the notes: | Para 47: A lessee shall either present in the balance sheet, or disclose in the notes: |

| (a) right-of-use assets separately from other assets. | (a) right-of-use assets separately from other assets. If a lessee does not present right-of-use assets separately in the balance sheet, the lessee shall: |

| (i) include right-of-use assets within the same line item as that within which the corresponding underlying assets would be presented if they were owned; and | |

| (ii) disclose which line items in the balance sheet include those right-of-use assets. | |

| (b) lease liabilities separately from other liabilities. | (b) lease liabilities separately from other liabilities. If a lessee does not present lease liabilities separately in the balance sheet, the lessee shall disclose which line items in the balance sheet include those liabilities. |

(above para is same as para 47 IFRS 16, thereby making IFRS 16 and Ind AS 116 exactly same now, except for the fair value option for investment property- ref para 1 of comparison with IFRS 16 )

Giving the above option makes it clear how the lessee is going to show the asset in books.

For example, if A takes Aircraft-1 on lease and owns Aircraft-2, A can either include both of them in PPE or can show Aircraft-1 in PPE and Aircraft-2 just below PPE under the head ROU.

Correspondingly, a lease liability can be disclosed separately, if not disclosed separately, then disclose which line item in BS includes the lease liability.

Globally, several jurisdictions have implemented the Standard with effect from 1st January, 2019. A list of jurisdictions which have already adopted can be viewed here.

Some of the key takeaways from the implementation of this Standard are:

- Currently, there are two accounting standards for lease transactions, first, Ind AS 17, which is applicable to the Ind AS compliant companies and second, AS 19, which is applicable to the remaining classes of companies. Ind AS 116 proposes to replace Ind AS 17, therefore, the companies which are not covered by Ind AS shall continue to follow old accounting standard.

- The applicability of this standard shall have to be examined separately for the lessor and the lessee, that is, if the lessor is Ind AS compliant and lessee is not Ind AS compliant, then lessor will follow Ind AS 116 whereas lessee will follow AS 19.

- The new standard changes treatment of operating leases in the books of the lessees significantly. Earlier, operating leases remained completely off the balance sheet of the lessee, however, vide this standard, lessees will have to recognise a right-to-use asset on their balance sheet and correspondingly a lease liability will be created in the liability side.

- Lease of low value assets and short tenure leases (up to 12 months) have been carved out from the requirement of recognition of RTU asset in the books of the lessee.

- No change in the accounting treatment in case of financial leases.

- No change in the lessor’s’ accounting.

While leasing has not been greatly popular in India compared to the world, there has been a substantial pick up in interest over recent years. Therefore, a question comes – will the new standard put a death knell to the feeble leasing industry in India? To the extent the demand for leasing comes from off balance sheet perspective for a lessee, the standard may have some impact. However, there are many economic drivers for lease transactions – such as the ease of usage, tax benefits, better residual realisation, etc. Those factors remain unaffected, and in fact, the focus of lease attractiveness will shift to real economic factors rather than balance sheet cosmetics.

The apparent question that arises here is whether the new standard unsettle the taxation framework for lease transactions in India, especially direct taxes – the answer to this question is negative. The tax treatment of lease transaction does not depend on the treatment of the transaction in books of accounts. Instead, it depends on whether the transaction is case a true lease or is merely a disguised financial transaction. There will be no impact on the indirect taxation framework as well.

Securitisation laws prevailing in various countries are listed below :

- Singapore:

- Monetary Authority of Singapore (MAS) Guidelines on Securitisation (The guidelines were finalized in 2000)

- Amendment in 2018

http://www.mas.gov.sg/~/media/MAS/Regulations%20and%20Financial%20Stability/Regulations%20Guidance%20and%20Licensing/Finance%20Companies/Notices/MAS%20Notice%20832%20%20Amendment%20%202018.pdf - Amendment in 2007

http://www.mas.gov.sg/~/media/MAS/Regulations%20and%20Financial%20Stability/Regulations%20Guidance%20and%20Licensing/Commercial%20Banks/Regulations%20Guidance%20and%20Licensing/Notices/MAS%20Notice%20628%20(2007).pdf - News on Securitisation

https://vinodkothari.com/2013/11/sing/ - Rules on Securitisation

https://vinodkothari.com/seclawsg/

- USA:

- 15 U.S. Code § 78o–11. Credit risk retention:

https://www.law.cornell.edu/uscode/text/15/78o-11 - Dodd-Frank Wall Street Reform and Consumer Protection Act [Public Law 111–203] [As Amended Through P.L. 115–174, Enacted May 24, 2018]

https://legcounsel.house.gov/Comps/Dodd-Frank%20Wall%20Street%20Reform%20and%20Consumer%20Protection%20Act.pdf - Securitisation Market

https://vinodkothari.com/secusa/ - Laws on Securitisation

https://vinodkothari.com/seclawus/

- Australia:

- Australian Prudential Standard (APS) 120 made under section 11AF of the Banking Act 1959 (the Banking Act) By Australian Prudential Regulation Authority

https://www.apra.gov.au/sites/default/files/aps_120_securitisation.pdf - Covered Bonds issued under Part II, Division 3A of the Banking Act 1959 (Cth)

https://www.legislation.gov.au/Details/C2017C00067 - Laws on Securitisation

https://vinodkothari.com/seclawaustral/ - Securitisation Market

https://vinodkothari.com/austral/

- Indonesia:

- Bank Indonesia Regulation No. 7/4/PBI/2005 Prudential Principles in Asset Securitisation for Commercial Banks

https://www.bi.go.id/en/peraturan/perbankan/Pages/bir%207405.aspx - Securitisation Market

https://vinodkothari.com/secindon/

- Hong Kong:

- There is no specific legislative regime for securitisation. Securitisation is subject to various Hong Kong laws, depending on the transaction structure, transaction parties, underlying assets, and the nature of the offering of the securities

- Securitisation Market

https://vinodkothari.com/sechong/

- Canada:

- Office of the Superintendent of Financial Institutions, Government of Canada

http://www.osfi-bsif.gc.ca/Eng/fi-if/rg-ro/gdn-ort/gl-ld/Pages/CAR18_chpt7.aspx - Securitisation Market

https://vinodkothari.com/seccanad/

- European Union:(UK, Germany, France,Italy, Sweden, Poland, Spain, Greece, Finland, Malta)

- Regulation(EU) 2017/2402 (the Securitisation Regulation) as on December 12,2017

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32017R2402 - Regulation (EU) 2017/2402 of the European Parliament and of the Council of September 30, 2015

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A52015PC0472 - Securitisation Market:

https://vinodkothari.com/europe/

- UK: https://vinodkothari.com/secuk/

- GERMANY: https://vinodkothari.com/germany/

- SWEDEN: https://vinodkothari.com/secswede/

- POLAND: https://vinodkothari.com/secpolan/

- SPAIN: https://vinodkothari.com/secspain/

- FINLAND: https://vinodkothari.com/secfinla/

- Italy:

- Law 130 of 30 April 1999, Italian securitisation law

https://www.housing-finance-network.org/fileadmin/user_upload/hfn/Country_Law/Law-Italy/2006-00281.pdf - Securitistion Market

https://vinodkothari.com/secitaly/

- Greece:

- GREEK LAW 3156/2003

http://www.greeklawdigest.gr/topics/finance-investment/item/317-securitization-law-bonds-l-3156-2003

- France:

- Order No. 2017-1432 of October 4, 2017 , Modernizing the Legal Framework for Asset Management and Debt Financing (Initial Version)

https://www.legifrance.gouv.fr/affichTexte.do?cidTexte=JORFTEXT000035720833&categorieLien=id

Version in force on 26/03/2019

https://www.legifrance.gouv.fr/affichTexte.do?cidTexte=JORFTEXT000035720833&dateTexte=20190326 - Securitisation Market:

https://vinodkothari.com/france/

- Japan: Securitisation in Japan is governed by laws and regulations applicable to specific types of transactions such as the Civil Code (Law No. 89, 1896), the Trust Act (Law No. 108, 2006) and the Financial Instruments and Exchange Law (Law No. 25, 1948) (FIEL).

- https://www.fsa.go.jp/common/law/fie01.pdf

- http://jafbase.fr/docAsie/Japon/CodCiv.pdf

- http://www.japaneselawtranslation.go.jp/law/detail_download/?ff=09&id=1946

- Laws on Securitisation

https://vinodkothari.com/seclawjapan/ - Securitisation Market

https://vinodkothari.com/japan/

- China:

- Administrative Rules for Pilot Securitization of Credit Assets(the Administrative Rules) on April 2005

http://www.cbrc.gov.cn/EngdocView.do?docID=1720 - Securitisation Market

https://vinodkothari.com/secchina-2/

- Ireland:

- European Union (General Framework For Securitisation And Specific Framework For Simple, Transparent And Standardised Securitisation) Regulations 2018 (Central Bank of Ireland)

http://www.irishstatutebook.ie/eli/2018/si/656/made/en/pdf

- South Africa:

- In South Africa, securitisations are regulated according to the securitisation regulations issued under the Banks Act 94 of 1990 (the Banks Act)

https://www.resbank.co.za/Lists/News%20and%20Publications/Attachments/2591/Banks+Amendment+Act+2007%5B1%5D.pdf

- Government Gazette 30628 of 1 January 2008 (Securitisation Regulations)

https://www.resbank.co.za/Lists/News%20and%20Publications/Attachments/2734/30628%20sec%20schemes%202008.pdf - Laws on Securitisation

https://vinodkothari.com/seclawsa/ - Securitisation Market

https://vinodkothari.com/secafric/

- Morocco:

- Law No. 33-06 on Securitization

- Draft amendment of Law on Securitization

http://www.sgg.gov.ma/portals/0/AvantProjet/8/Projet_loi_Amendement-titrisation_Ang.pdf

Consolidation of new ECB and Trade Credit framework: RBI issues Master Direction 2019

Vallari Dubey

corplaw@vinodkothari.com

Introduction

With the backdrop of revision of various frameworks for raising funds outside India (other than by way of equity participation), RBI has issued the Master Direction – External Commercial Borrowings, Trade Credits and Structured Obligations on 26th March, 2019, in supersession of the existing Master Direction – External Commercial Borrowings, Trade Credit, Borrowing and Lending in Foreign Currency by Authorised Dealers and Persons other than Authorised Dealers dated 1st January, 2016 (last updated on 22nd November, 2018).

The new Master Direction seeks to consolidate all applicable circulars and notifications in respect of the following:

- External Commercial Borrowing framework (ECB framework) covered in the Master Direction as Part I

- Trade Credit framework covered as Part II

- Structured Obligations covered as Part III.

The first set of changes was introduced through the Foreign Exchange Management (Borrowing and Lending) Regulations, 2018 on 17th December, 2018. Thereafter, the New ECB framework was issued on 16th January, 2019 and the Trade Credit Policy on 13th March, 2019.

New Master Direction

The erstwhile Master Direction included provisions pertaining to borrowing and lending in foreign currency, which has now been removed and is solely dealt with by Foreign Exchange Management (Borrowing and Lending) Regulations, 2018. Further, it replaces the erstwhile ECB framework and Trade Credit framework with the recently issued frameworks, separately.

The revised ECB policy and Trade Credit Policy were issued, coinciding with Foreign Exchange Management (Borrowing and Lending) Regulations, 2018.

The changes introduced pursuant to new ECB policy and Trade Credit policy have been covered by our colleagues extensively in the following write ups:

- RBI revises ECB framework – aligns with FEM (Borrowing and Lending) Regulations, 2018

- RBI revises Trade Credit Policy Framework.

Few important additions in the revised frameworks, now consolidated under the Master Directions include Standard Operating Procedure for Untraceable Entities for Ad Banks, ECB for entities under resolution under IBC, ECB for resolution applicants, Late Submission Fee for late submission of returns.

Conclusion

The revision of the Master Direction which was originally issued in 2016 was quite anticipated in light of the recent changes made by RBI. Although the new Master Direction does not introduce any additional change in the ECB and Trade Credit framework, it unifies all the applicable policy frameworks, thereby giving more clarity.

SEBI proposes to restructure the issuance of shares with DVRs

By Nikita Snehil and Shaifali Sharma | corplaw@vinodkothari.com

Vinod Kothari & Company

The basic principle behind the issuance of shares with differential voting rights, commonly known as ‘DVRs’ in India and dual class shares or ‘DCS’ in the international context, is to enable the companies to raise capital without dilution of control and decision-making power in company. In promoter/ founder led companies where promoters/ founders are instrumental in the success of the company, such structures enable them to retain decision-making powers and rights vis-a-vis other shareholders either through retaining shares with superior voting rights or issuance of shares with lower or fractional voting rights to public investors.

The concept was first recognized under the Companies (Amendment) Act, 2000 followed by similar provisions adopted by the Companies Act, 2013. However, the current practical scenario depicts a different picture, as the provisions of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 does not permit DVRs with higher or superior voting rights. However, subject to certain conditions, DVR shares with lower voting rights are permitted. Till date, only 5 listed companies have used this structure in India. Strict pre-condition and corporate governance norms, unavailability of investors due to lack of awareness are some grounds of company’s reluctance from adopting such idea.

SEBI’s Consultation Paper to restructure the issuance of DVRs

On December 19, 2018, Mr. Ajay Tyagi, Chairman of SEBI, had said in an interview that SEBI has made a sub-committee for reintroducing Differential Voting Rights on shares, which will make recommendation on the same by next month. Post this, SEBI on March 20, 2019, has come out with a Consultation Paper[1] on issuance of shares with Differential Voting Rights. The Consultation Paper provides that the matter of issuance of shares with DVRs was deliberated in the Primary Market Advisory Committee of SEBI (‘Committee’) and a group (‘DVR Group’) was constituted amongst the Committee members to do an in-depth study of the proposal of introduction of shares with DVRs in Indian Scenario.

The Consultation Paper addresses the norms for issuance of shares with DVRs under two categories –

- issuance by companies whose equity shares are already listed on stock exchanges;

- companies with equity shares not hitherto listed but proposed to be offered to the public.

The basic moto behind allowing shares with differential voting rights is to raise equity without dilution of promoter control i.e., to allow the promoters/ founders to maintain control as they would hold shares with superior voting rights.

Therefore, considering SEBI’s proposed structure, there shall be four categories of companies which can issue DVRs:

- Equity listed cos – as per this Consultation Paper;

- Unlisted cos, which are intending to get their equity listed — as per this Consultation Paper;

- Unlisted cos, not intending to list their equity shares – as per Section 43 of the Companies Act, 2013 (‘Act’) read with Rule 4 of the Companies (Share Capital and Debenture) Rules, 2014;

- Private Cos — exempted from applicability Section 43 of the Act, if either its memorandum or articles of association so provides- vide notification number G.S.R. 464(E) dated 5th June 2015.

Need for DVRs in India

In order to maintain the current growth phase in India, it is pertinent for the companies to raise capital to sustain this growth. For companies with high leverage or asset light models, they may prefer equity over debt capital. Raising DVRs will reduce the dilution of founder/ promoter stake which would otherwise be a case in capital raised by equity.

The protection of founder/ promoter’s stake/ control is especially relevant for new technology entities which have asset light models, with little or no need for debt financing. However, these entities generally raise funds through equity which dilutes the promoter’s/ founder’s stake, thereby diluting control. Considering the issue, the Consultation Paper states that retaining founder’s interest & control in the business is of great value to all shareholders and the same can be achieved by:

- Issue of shares with superior voting rights (‘SR’) to founders and/or

- Issue of shares with lower or fractional voting rights (‘FR’) to raise funds from private/ public investors.

International Scenario

The global market has witnessed a mixed response to the concept of DVRs, while many countries have permitted the listing of companies with Dual Class Shares or DCS (internationally used term for DVRs), some countries like UK, Australia, Spain, Germany and China do not permit the Issuers with DCS structure for listing. Singapore and Hong Kong have recently permitted DCS structures with detailed checks and balances. Considering the international scenario, the Consultation Paper has provided a detailed comparison of the issuance & listing of DCS structure in internal jurisdictions, the summary of which is presented below:

- 700 public companies in the US have DCS structures, predominant listed ones being Google, Facebook, Snapchat, Nike and Alibaba. There is ongoing debate in the SEC about the continuation of DCS[2].

- Hong Kong and Singapore recently allowed DCS to encourage more new technology firms to list.

- In the UK[3], DCS structures were used in the 1960s to protect corporations from hostile takeovers or for the Queen to have ‘golden share’, before institutional investors expressed strong opposition to such structures. DSC is presently not allowed in the UK.

- Over the past decade, a number of European governments have implemented or debated the use of different voting rights.

- US, Canada, HK, Singapore, Denmark, Spain, Sweden and Italy allow dual-class shares. Germany, Spain, China, Australia disallow listing of shares of companies with DCS structures.

Recommendations of the DVR Group

Ø Pre-conditions

A company would be entitled to issue DVR Shares, subject to following pre-conditions:

- issue of DVR Shares must have been be authorized in the AoA of the company; and

- the issue of DVR Shares should be authorized by a special resolution passed at a general meeting of the shareholders.

- for companies already listed, by way of e-voting as per Companies Act, 2013

- The notice should mention specific matters, including but not limited to, size of issuance, ratio of the difference in the voting rights, rights as to differential dividends, if any, sunset clause, coattail provisions, etc., as made applicable by SEBI regulations to be notified in this regard.

Ø Requirements for both the categories

Category I: Companies whose equity shares are already listed – issuance of FR Shares;

Category II: Companies whose equity shares are proposed to be listed – issuance of SR shares.

| Eligibility

|

Requirements for Category I | Requirements for Category II |

| Conditions | Cos whose shares have been listed on a SE for atleast a year, may issue FR Shares.

Note: listed cos are still not allowed to issue SR Shares. |

Unlisted cos may issue SRs, only to promoters. |

|

First issuance of FR/ SR shares |

||

| Type of issuance | Through a) rights issue; b) bonus issue pro rata to all equity shareholders; or c) a Follow-on Public Offer (“FPO”) of FR shares. | An unlisted co. where the promoters hold SR Shares shall be permitted to do an Initial Public Offer (“IPO”) of only ordinary equity shares provided the SR Shares are held by the promoters for more than one year prior to filing of the draft offer document with SEBI. |

|

Subsequent issues of FR Shares once FR Shares are already listed |

||

| Type of issuance | A company that has already listed FR Shares shall be eligible to do:

a) rights issue; b) bonus issue; c) preferential issue; d) QIP of FR Shares of the same class;

|

A company whose SR Shares and ordinary equity shares are already listed shall be permitted to issue FR Shares in terms of the applicable provisions for issue of FR Shares by listed companies – which means same as Category I.

Note: Issuance of SR shares not allowed post listing. |

| Depository Receipts | A company whose FR Shares are listed for at least one year shall be eligible to issue depositary receipts where the underlying shares are FR Shares. | — |

| Convertible Instruments | A company can issue convertible instruments which will convert into FR Shares subject to applicable regulatory considerations. | — |

| Voting and other rights | The FR shares shall not be treated at par with the ordinary equity shares.

Max ratio

The FR Shares shall not exceed a ratio of 1:10, i.e. one vote as applicable to one Ordinary Equity Share, would be voting entitlement on 10 FR Shares. The ratio can be in full numbers from 1:2 to 1:10.

At any point of time, the co. can only have one class of FR Shares. |

The SR Shares shall be treated at par with the ordinary equity shares in every respect except in the case of voting on certain matters.

Max ratio

The SR Shares shall be of a maximum ratio of 10:1, i.e. ten votes for every SR Share held. The ratio can be in whole numbers from 2:1 to 10:1. A ratio once adopted by a company shall remain valid for any subsequent issuances of SR Shares.

A co. can issue only one class of SR Shares.

Any rights or bonus issue by the co. post-listing shall be offered only as ordinary equity shares to the holders of the SR Shares.

On certain matters to be notified by regulations, the SR Shares would be treated as having only one vote. The initial list of the same is set out in the coattail provisions set out in the Committee Report (the same has been explained later in this Article).

|

| Dividends | The company may, at its discretion, decide to pay additional dividend per FR Share compared to dividend paid on ordinary Equity Share, which shall be higher than the dividend per

ordinary Equity Share and the same shall be stated in the terms of the offering. No dividend may be payable on FR Shares for such years where no dividend has been declared by the company for the ordinary equity shares.

|

Post IPO, the SR shares shall be eligible for the same dividend and other rights as ordinary equity shares, except for superior voting rights. |

| Minimum Public Shareholding | The co. should comply with the req of Securities Contracts (Regulation) Rules, 1957 (“SCRR”) and other applicable regulations formulated in this regard. | The co. shall comply with the SCRR and other applicable regulations formulated, for the ordinary equity shares that will be listed.

Post-listing, the voting rights with the promoters through the SR Shares and ordinary equity shares shall not exceed 75% of the total voting rights. |

| Pricing | The pricing of FR shares shall be in accordance with regulatory considerations applicable to

mode of issuance of FR Shares |

— |

| Face Value | The face value of a company’s FR Shares shall be the same as that of its

ordinary equity shares. |

The face value of a company’s SR Shares shall be the same as of that of the ordinary equity shares. |

| Number of FR / SR Shares | The number of FR Shares that may be issued by a company shall be subject to

provisions of the Companies Act, 2013 and the rules framed thereunder |

A company shall be permitted to issue any number of SR Shares of the same class prior to an IPO, subject to provisions of the Companies Act, 2013. |

| Lock-in period | — | All SR Shares shall remain under a perpetual lock-in after the IPO. |

| Pledge of shares | — | Creation of any encumbrance over SR Shares including pledge, lien, negative lien, non-disposal undertaking, etc. shall not be permissible.

In other words, no third-party interest may be created over the SR Shares and any instrument purporting to do so would be void ab initio. |

| Fasttrack issuance

|

A company shall be eligible to issue FR Shares in a rights issue or an FPO through the fasttrack method in case it meets the eligibility criteria of fast-track issuances. | — |

| Conversion of FR / SR shares

[Also known as ‘Sunset Clause in case of SR Shares] |

The FR Shares can be converted into ordinary equity shares only in cases of schemes of

arrangement. |

The validity of SR shares is 5 years from the date of listing of ordinary shares. Which means, such shares shall be compulsory converted into ordinary shares on the 5th year anniversary of the listing of such ordinary shares i.e. superior rights will fall under the standard rule of ‘one-share one-vote’. Conversion shall be done in the following manner:

For promoters: at any time prior to the 5th year anniversary of the listing of the Ordinary Shares or such extended period as decided by the shareholders by passing special resolution.

For other than promoters: on completion of the 5th year anniversary of the listing of the Ordinary Shares or such extended period of 5 years with the approval of shareholders by way of special resolution in the meeting where all members vote on one-share-one vote basis.

Besides the aforementioned validity of 5 years, the SR shares shall be converted into ordinary shares on the merger or acquisition of the company or sale of such shares by the identified promoters who hold such shares or in the case of demise of the promoter(s). |

| Extinguishment | The FR Shares can be extinguished only through buy-back by the company or reduction of capital in accordance with applicable laws. | — |

| Delisting | The company can delist the FR Shares in accordance with the SEBI (Delisting of Equity Shares) Regulations, 2009. However, in the event ordinary equity shares of the company are delisted, the company shall be mandatorily required to delist the FR Shares. | — |

| Listing and Trading | The FR Shares shall be held in dematerialized form. However, FR Shares can be

issued in physical form, if such FR Shares have been issued pursuant to a bonus issue and the underlying shares are held in physical form.

The FR Shares shall be listed and traded on all SEs where ordinary equity shares of the co. are listed with a separate identifier from the ordinary equity shares. |

All SR Shares shall be held in dematerialized form and shall be listed on the main board platform of the recognized SEs.

For listing of SR Shares, exemption will be granted from Rule 19(2)(b) of SCRR.

The SR Shares, however, cannot be traded except upon conversion into ordinary equity shares. |

| Post-Issue Disclosures | The shareholding pattern filed by the co. with the SEs shall provide the details of the FR Shares separately and in the format specified by SEBI and the SEs | The shareholding pattern to be filed by the co. with the SEs shall provide the details of both ordinary equity shares and SR Shares in the format specified by SEBI and the stock exchanges. |

| ESOPs | A co. can issue ESOPs of FR Shares post the listing of such shares, subject to applicable laws. | — |

| Bonus issue by the co. which has issued FR shares | If a co. which has issued FR shares, issues bonus shares, then it shall issue to FR shareholders bonus FR shares in the same proportion in which bonus shares are issued on ordinary equity shares. | — |

| Applicability of other SEBI Regulations | SEBI regulations in respect of buy-back, and takeovers shall apply to FR Shares, subject to such modification as may be required in the context of FR Shares. The FR Shares once listed shall not be delisted on a standalone basis and may be delisted as and when the ordinary equity shares are delisted. | SEBI regulations in respect of buy-back, and takeovers shall be applicable to SR Shares, subject to such modification as may be required in the context of SR shares. |

Ø ”Coattail” Provisions for issuance of SR shares

Post-IPO, the SR Shares shall be treated as ordinary equity shares in terms of voting rights (i.e. one SR share-one vote) in the following circumstances:

- provisions relating to appointment or removal of independent directors and/or auditor;

- in case there is a change in control of the company;

- any contract or agreement of the company with any person holding the SR Shares, in excess of the materiality threshold prescribed under Regulation 23 of the SEBI (Listing Obligations and Disclosure Requirement) Regulations, 2015;

- voluntary winding up of the company;

- any material changes in the company’s AoA or MoA, including but not limited to, undertaking variation in the voting rights of the shareholders, changing the principal objects of the company, granting special rights in favour of a particular shareholder or shareholder groups and such other items as may be prescribed by the SEBI;

- initiation of a voluntary resolution plan under the Insolvency and Bankruptcy Code, 2016;

- extension of the validity of the SR Shares post completion of 5 years from date of listing of ordinary equity shares; and

- any other provisions notified by SEBI in this regard from time to time.

Conclusion

The major benefits of DVRs structure highlighted in the DVR Group Report are as follows:

- DVRs promote fund raising without diluting control;

- In a promoter led companies, DVR structure will enable such promoters to retain control, the decision-making powers and other rights in the company;

- DVRs structure acts as defense mechanism for hostile takeover.

The recommendations by DVRs Group seems to extend a hand of opportunity to listed companies and those companies including, newly incorporated companies, who intend to issue DVRs but do not have a consistent track record of distributable profits as stated in the existing ICDR regulations, i.e. 3 years.

The Sunset Clause in case of SR shares shall keep a check on the tenure of the DVRs, however, the provisions requiring companies issuing the DVRs to observe better corporate governance practices is missing in the proposed structure of DVRs. Further, there might be instances where the interest of minority shareholders could be adversely affected by the holder of SR shares, therefore, certain checks and balances to prevent the misuse of the instruments should be imposed by SEBI to protect the interest of the shareholders as well as the genuine issuers.

[1] https://www.sebi.gov.in/reports/reports/mar-2019/consultation-paper-on-issuance-of-shares-with-differential-voting-rights_42432.html

[2] http://www.pionline.com/article/20180216/ONLINE/180219888/sec-commissioner-calls-for-curb-on-dual-class-forever-shares#

[3] https://ecgi.global/sites/default/files/working_papers/documents/SSRN-id2138949.pdf

Indefinite deferral of IFRS for banks: needed reprieve or deferring the pain?

Vinod Kothari (vinod@vinodkothari.com); Abhirup Ghosh (abhirup@vinodkothari.com)

On 22 March, 2019, just days before the onset of the new financial year, when banks were supposed to be moving into IFRS, the RBI issued a notification[1], giving Indian banks indefinite time for moving into IFRS. Most global banks have moved into IFRS; a survey of implementation for financial institutions shows that there are few countries, especially which are less developed, where banks are still adopting traditional GAAPs. However, whether the Notification of the RBI is giving the banks a break that they badly needed, or is just giving them today’s gain for tomorrow’s pain, remains to be analysed.

The RBI notifications lays it on the legislative changes which, as it says, are required to implement IFRS. It refers to the First Bi-monthly Monetary Policy 2018-19[2], wherein there was reference to legislative changes, and preparedness. There is no mention in the present notification for preparedness – it merely points to the required legislative changes. The legislative change in the BR Act would have mostly been to the format of financial statements – which is something that may be brought by way of notification. That is how it has been done in case of the Companies Act.

This article analyses the major ways in which IFRS would have affected Indian banks, and what does the notification mean to the banking sector.

Major changes that IFRS would have affected bank accounting:

- Expected Credit Loss – Currently, financial institutions in India follow an incurred credit loss model for providing for financial assets originated by them. Under the ECL model, financial assets will have to be classified into three different stages depending on credit risk in the asset and they are:

- Stage 1: Where the credit risk in the asset has not changed significantly as compared to the credit risk at the time of origination of the asset.

- Stage 2: Where the credit risk in the asset has increased significantly as compared to the credit risk at the time of origination of the asset.

- Stage 3: Where the asset is credit impaired.

While for stage 1 financial assets, ECL has to be provided for based on 12 months’ expected losses, for the remaining stages, ECL has to be provided for based on lifetime expected losses.

The ECL methodology prescribed is very subjective in nature, this implies that the model will vary based on the management estimates of each entity; this is in sharp contrast to the existing provisioning methodology where regulators prescribed for uniform provisioning requirements.

Also, since the provisioning requirements are pegged with the credit risk in the asset, this could give rise to a situation where the one single borrower can be classified into different stages in books of two different financial institutions. In fact, this could also lead to a situation where two different accounts of one single borrower can be classified into two different stages in the books of one financial entity.

- De-recognition rules – Like ECL provisioning requirements, another change that will hurt banks dearly is the criteria for derecognition of financial assets.

Currently, a significant amount of NPAs are currently been sold to ARCs. Normally, transactions are executed in a 15:85 structure, where 15% of sale consideration is discharged in cash and the remaining 85% is discharged by issuing SRs. Since, the originators continue to hold 85% of the SRs issued against the receivables even after the sell-off, there is a chance that the trusts floated by the ARCs can be deemed to be under the control of the originator. This will lead to the NPAs coming back on the balance sheet of banks by way of consolidation.

- Fair value accounting – Fair value accounting of financial assets is yet another change in the accounting treatment of financial assets in the books of the banks. Earlier, the unquoted investments were valued at carrying value, however, as per the new standards, all financial assets will have to be fair valued at the time of transitioning and an on-going basis.

It is expected that the new requirements will lead to capital erosion for most of the banks and for some the hit can be one-half or more, considering the current quality of assets the banks are holding. This deferment allows the banks to clean up their balance sheet before transitioning which will lead to less of an impact on the capital, as it is expected that the majority of the impact will be caused due to ECL provisioning.

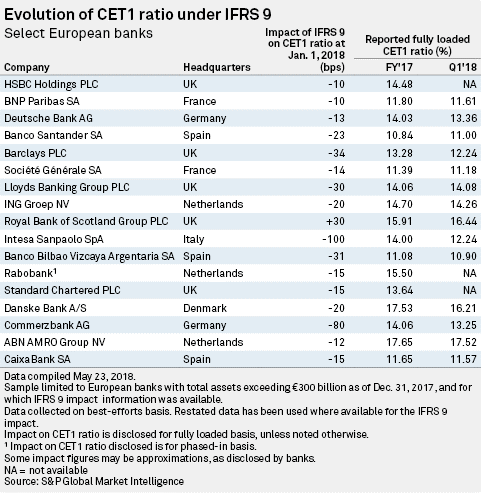

World over most of the jurisdictions have already implemented IFRS in the banking sector. In fact, a study[3] shows that major banks in Europe have been able to escape the transitory effects with small impact on their capital. The table below shows the impact of first time adoption of IFRS on some of the leading banking corporations in Europe:

Impact of this deferment on NBFCs

While RBI has been deferring its plan to implement IFRS in the banking sector for quite some time, this deferral was not considered for NBFCs at all, despite the same being admittedly less regulated than banks. The first phase of implementation among NBFCs was already done with effect from 1st April, 2018.

This early implementation of IFRS among NBFCs and deferral for banks leads to another issue especially for the NBFCs which are associates/ subsidiaries of banking companies and are having to follow Ind AS. While these NBFCs will have to prepare their own financials as per Ind AS, however, they will have to maintain separate financials as per IGAAP for the purpose of consolidation by banks.

What does this deferment mean for banks which have global listing?

As already stated, IFRS have been implemented in most of the jurisdictions worldwide, this would create issues for banks which are listed on global stock exchanges. This could lead to these banks maintaining two separate accounts – first, as per IGAAP for regulatory reporting requirements in India and second, as per IFRS for regulatory reporting requirements in the foreign jurisdictions.

—

[1] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11506&Mode=0

[2] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=43574

[3] https://www.spglobal.com/marketintelligence/en/news-insights/research/european-banks-capital-survives-new-ifrs-9-accounting-impact-but-concerns-remain