Transacting by exception: Listed cos in India give substantive carve outs for RPTs

The article has been published in ICSI – WIRC-E Newsletter (June-July 2020 edition):

Refer page 43 of ICSI – WIRC-E Newsletter

The article has been published in ICSI – WIRC-E Newsletter (June-July 2020 edition):

Refer page 43 of ICSI – WIRC-E Newsletter

Our related research on the similar topics may be viewed here –

Our related research on similar topics can be viewed here –

-by Smriti Wadehra

(smriti@vinodkothari.com)

-Updated as on 29th September, 2020

Pursuant the proposal of Union Budget of 2019-20, the MCA vide notification dated 16th August, 2019 amended the provisions of Companies (Share Capital and Debentures) Rules, 2014 [1].(You may also read our analysis on the notification at Link to the article) The said amended Rules faced a lot of apprehensions, especially, from the NBFCs as the notification which was initially expected to scrap off the requirement of creation of DRR for publicly issued debentures had on the contrary, rejuvenated a somewhat settled or exempted requirement of creation of debenture redemption fund as per Rule 18(7) for NBFCs as well.

As per the notification, the Ministry imposed the requirement for parking liquid funds, in form of a debenture redemption fund (DRF) to all bond issuers except unlisted NBFCs, irrespective of whether they are covered by the requirement of DRR or not. In this regard, considering the ongoing liquidity crisis in the entire financial system of the Country, parking of liquid funds by NBFCs was an additional hurdle for them.

Creation of DRR is somewhat a liberal requirement than creation of DRF, this is because, where the former is merely an accounting entry, the latter is investing of money out of the Company. Further, the fact the notification dated 16th August, 2019 casted exemption from the former and not from the latter, created confusion amidst companies. The whole intent of amending the Rule was to motivate NBFCs to explore bond markets, however, the requirement of parking liquid funds outside the Company as high as 15% of the amount of debentures of the Company was acting as a deterrent for raising funds by the NBFCs.

Considering the representations received from various NBFCs and the ongoing liquidity crunch in the economy of the Country along with added impact of COVID disruption, the Ministry of Corporate Affairs has amended the provisions of Rule 18 of Companies (Share Capital and Debenture) Rules, 2014 vide notification dated 5th June, 2020 [2]to exempt listed companies coming up with private placement of debt securities from the requirement of creation of DRF.

What is DRR and DRF?Section 71(4) read with Rule 18(1)(c) of the Companies (Share Capital and Debentures) Rules, 2014 requires every company issuing redeemable debentures to create a debenture redemption reserve (“referred to as DRR”) of at least 25%/10% (as the case maybe) of outstanding value of debentures for the purpose of redemption of such debentures. Some class of companies as prescribed, has to either deposit, before April 30th each year, in a scheduled bank account, a sum of at least 15% of the amount of its debentures maturing during the year ending on 31st March of next year or invest in one or more securities enlisted in Rule 18(1)(c) of Debenture Rules (‘referred to as DRF’). |

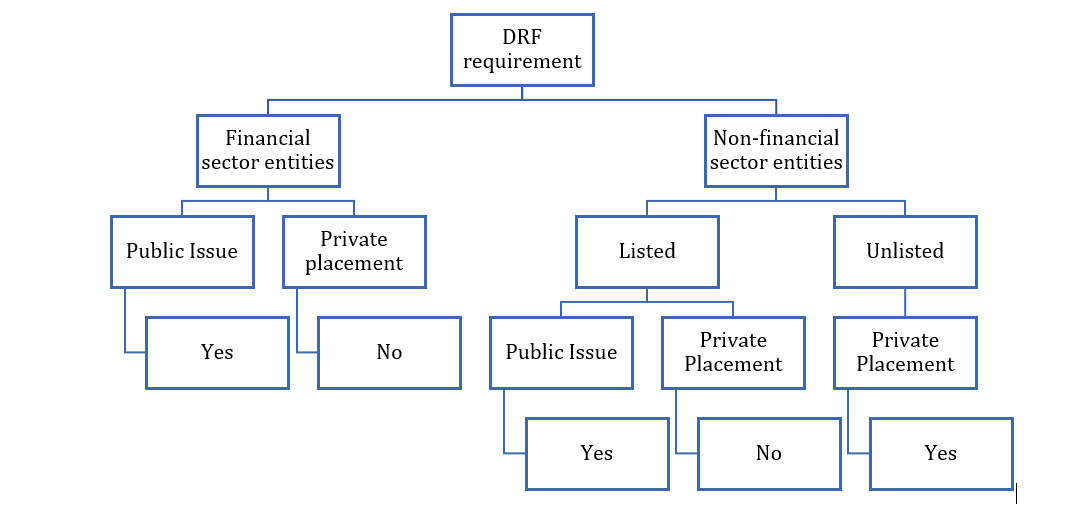

The notification has mainly exempted two class of companies from the requirement of creation of DRF:

However, the unlisted non-financial sector entities have been left out. In a private placement, the securities are issued to pre-selected investors. Raising debt through private placement is a midway between raising funds through loan and debt issuances to public. Like in case of bilateral loan arrangements, but unlike in case of public issue, the investors get sufficient time to assess the credibility of the issuer in private placements, since the investors are pre-identified.

The intent behind DRF is to protect the interests of the investors, usually when retail investors are involved, with respect to their claims on maturity falling due within a span of 1 year. This is not the case for investors who have invested in privately placed securities, where the investments are made mostly by institutional investors.

Further, companies chose issuance through private placement for allotment of securities privately to pre-identified bunch of persons with less hassle and compliances. Hence, the requirement of parking funds outside the Company frustrates the whole intent.

Further, it is a very common practice to roll-over the bond issuances, hence, it is not that commonly bonds are repaid out of profits; the funds are raised from issuance of another series of securities. This is a corporate treasury function, and it seems very unreasonable to convert this internal treasury function to a statutory requirement.

Though, in our view, the relaxation provided in case of private issuance of debt securities is definitely a relief, especially during this hour of crisis, but we are not clear about the logic behind excluding unlisted non-financial sector entities.

Even though, the financial sector (76%) entities dominate the issuance of corporate bonds, however, the share of the non-financial sector entities (24%) is not insignificant. Therefore, ideally, the exemption in case of private placements should be extended to unlisted non-financial sector entities as well.

A brief analysis of the amendments is presented below:

Pursuant to the MCA notification dated 16th August, 2019, the below mentioned class of companies were required to either deposit or invest atleast 15% of amount of debentures maturing during the year ending on 31st March, 2020 by 30th April, 2020. This has been extended till 31st December, 2020 for this FY 2019-20 by MCA due to the COVID-19 outbreak. However, pursuant to the amendment introduced by MCA notification dated 5th June, 2020 the status of DRF requirement stands as amended as follows:

| Particulars | DRF requirement as MCA circular dated 16th August, 2019 | DRF requirement as per MCA circular dated 5th June, 2020 |

| Listed NBFCs which have issued debt securities by way of public issue | Yes. | Yes. Deposit or invest before 31st December, 2020 |

| Listed NBFCs which have issued debt securities by way of private placement | Yes | Not required as exempted. |

| Listed entities other than NBFC which have issued debt securities by way of private placement | Yes | Not required as exempted |

| Listed entities other than NBFC which have issued debt securities by way of public issue | Yes | Yes. Deposit or invest before 31st December, 2020 |

| Unlisted companies other than NBFC | Yes. | Yes. Deposit or invest before 31st December, 2020 |

Please note that the aforesaid shall be applicable from 12th June, 2020 i.e. the date of publication of the notification in the official gazette. In this regard, if for instance companies which have been specifically exempted pursuant to the recent notification, have already invested or deposited their funds to fulfil the DRF requirement may liquidated the funds as they are no longer statutorily require to invest in such securities.

A brief analysis of the DRR and DRF provisions as amended by the MCA notification dated 16th August, 2019 and 5th June, 2020 has been presented below:

| Sl. No. | Particulars | Type of Issuance | DRR as per erstwhile provisions | DRR as per amended provisions | DRF as per erstwhile provisions | DRF as per amended provisions |

| 1. | All India Financial Institutions | Public issue/private placement | × | × | × | × |

| 2. | Banking Companies | Public issue/private placement | × | × | × | × |

| 3.

|

Listed NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank | Public issue | √

25% of value of outstanding debentures |

× | √ | √ |

| Private Placement | × | × | √ | × | ||

| 4. | Unlisted NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank | Private Placement |

× |

× |

× |

× |

| 5.

|

Other listed companies | Public Issue | √

25% of value of outstanding debentures |

× | √ | √ |

| Private Placement | √

25% of value of outstanding debentures |

× | √ | × | ||

| 6. | Other unlisted companies | Private Placement | √

25% of value of outstanding debentures |

√

10% of the value of outstanding debentures |

√ | √ |

[1] http://www.mca.gov.in/Ministry/pdf/Circular_25032020.pdf

[2] This table includes analysis of provisions of DRR and DRF as per CA, 2013 and amendments introduced vide MCA notification dated 16th August, 2019 and 5th June, 2020.

Erstwhile provisions- Provisions before amendment vide MCA circular dated 16th August, 2019

Amended provisions- Provisions after including amendments introduced vide MCA circular 5th June, 2020

[1] https://www.mca.gov.in/Ministry/pdf/ShareCapitalRules_16082019.pdf

Abhirup Ghosh

– Updated as on 16th June, 2020

On 8th June, 2020, RBI issued the Draft Framework for Securitisation of Standard Assets taking into account existing guidelines, Basel III norms on securitisation by the Basel Committee on Banking Supervision as well the Report of the Committee on the Development of Housing Finance Securitisation Market chaired by Dr. Harsh Vardhan.

With this, one of the main areas of concern happens to be capital relief for securitisation. The concerns arise not just for new exposures but also existing securitisation exposures, as Chapter VI (dealing with Capital Requirements) shall come into immediate effect, even for the existing securitisation exposures.

Earlier, due to the implementation of Ind-AS, concerns arose with respect to capital relief treatment as most of the securitisation exposures did not qualify for derecognition under Ind-AS. However, on March 13, 2020, RBI came out with Guidance on implementation of Ind-AS, which clarified the issue by stating that securitised assets not qualifying for derecognition under Ind AS due to credit enhancement given by the originating NBFC on such assets shall be risk weighted at zero percent. However, the NBFC shall reduce 50 per cent of the amount of credit enhancement given from Tier I capital and the balance from Tier II capital.

Once again, the issue of capital relief arises as the draft guidelines may cause an increase in capital requirements for existing exposures.

The Draft Framework lays down qualitative as well as quantitative criteria for determining capital requirements. As per Para 70, lenders are required to maintain capital against all securitisation exposure amounts, including those arising from the provision of credit risk mitigants to a securitisation transaction, investments in ABS or MBS, retention of a subordinated tranche, and extension of a liquidity facility or credit enhancement. For the purpose of capital computation, repurchased securitisation exposures must be treated as retained securitisation exposures.

The general provisions for measuring exposure amount of off-balance sheet exposures are laid down under para 71-78 of the Draft Framework.

The quantitative conditions are however, laid down in paragraphs 79 (a) and (b). The intention here is to delve into the impact of the quantitative conditions only, keeping aside the qualitative conditions for the time being.

The first condition (79(a)) is that significant credit risk associated with the underlying exposures of the securities issued by the SPE has been transferred to third parties. Here, significant credit risk will be treated as having transferred if the following conditions are satisfied:

Taking each of the two points at a time.

The first clause contemplates a securitisation structure with at least three tranches – the senior, the mezzanine and the equity. Despite the presence of three tranches, the condition for risk transfer has been pegged with the mezzanine tranche only, however, nothing has been discussed with respect to the thickness of the mezzanine tranche (though the draft Directions has prescribed a minimum thickness for the first loss tranche).

If the language of the draft Directions is retained as is, qualifying for capital relief will become very easy. This can be explained with the help of the following example.

Suppose a securitisation transaction has three tranches, the composition and proportion of which has been provided below:

| Tranche | Rating | Proportion as a part of the total pool | Retention by the Originator | Effective retention of interest by the Originator |

| Senior Tranche – A | AAA | 85% | 0% | 0% |

| Mezzanine Tranche – B | AA+ | 5% | 50% | 2.5% |

| Equity/ First Loss Tranche – C | Unrated | 10% | 100% | 10% |

| 12.5% |

As may be noticed, both the senior and mezzanine are fairly highly rated as the junior most tranche has a considerable amount of thickness and represents a first loss coverage of 10%. Additionally, it also retains 50% of the Mezzanine tranche. Therefore, effectively, the Originator retains 12.5% of the total pool, yet it will qualify for the capital relief, by virtue of holding upto 50% of the Mezzanine tranche, despite retaining 10% in the form of first loss support.

The second clause contemplates a situation where there are only two tranches – that is, the senior tranche and the equity tranche. The clause says that in absence of a mezzanine tranche, the retention of first loss by the Originator should not be more than 20% of the total first loss tranche.

Given the current market conditions, it will be practically impossible to find an investor for the first loss tranche, hence, the entire amount will have to be retained by the Originator. Also, it is very common to provide over-collateral or cash collateral as first loss supports in case of securitisation transactions, even in such cases a third party’s participation in the first loss piece is technically impossible.

Also, there is a clear conflict between this condition and para 16 of the draft Directions, which gives an impression that the first loss tranche has to be retained by the originator itself, in the form of minimum risk retention.

Therefore, in Indian context, if one were to take a holistic view on the conditions, they are two different extremes. While, in the first case, capital relief is achievable, but in the second case, the availing capital relief is practically impossible. This will make the second condition almost redundant.

In order to understand the rationale behind these conditions, please refer to the discussion on EU Guidelines on SRT below.

As noted earlier, this part of the draft Directions shall be applicable on the existing transactions as well. Here it is important to note that currently, most of the transaction structures in India either have only one or two tranches of securities, and only a fraction would have a mezzanine tranche. In all such cases, the entire first loss support comes from the Originator. Therefore, almost none of the transactions will qualify for the capital relief.

In the hindsight, the originators have committed a crime which they were not even aware of, and will now have to pay a price.

The moment, the Directions are finalised, the loans will have to be risk-weighted and capital will have to be provided for.

This will have a considerable impact on the regulatory capital, especially for the NBFCs, which are required to maintain a capital of 15%, instead of 9% for banks.

This requirement states that the minimum first loss tranche should be the product of (a) exposure (b) weighted maturity in years and (c) the average slippage ratio over the last one year.

The slippage ratio is a term often used by banks in India to mean the ratio of standard assets slipping to substandard category. So, if, say 2% of the performing loans in the past 1 year have slipped into NPA category, and the weighted average life of the loans in the pool is, say, 2.5 years (say, based on average maturity of loans to be 5 years), the minimum first loss tranche should be [2% * 2.5%] = 5% of the pool value.

In India, currently the thickness of the first loss support depends on the recommendations of the credit rating agencies (CRAs). Typically, the thresholds prescribed by the CRAs are thick enough, and we don’t foresee any challenge to be faced by the financial institutions with respect to compliance with this point.

The guidelines for evidencing significant risk transfer, as provided in the draft Guidelines, are inspired from the EU’s Guidelines on Significant Risk Transfer. The EU Guidelines emphasizes on significant risk transfer for capital relief and states that a high level, the capital relief to the originator, post securitisation, should commensurate the extent of risk transferred by it in the transaction. One such way of examining whether the risk weights assigned to the retained portions commensurate with the risk transferred or not is by comparing it with the risk weights it would have provided to the exposure, had it acquired the same from a third party.

Where the Regulatory Authority is convinced that the risk weights assigned to the retained interests do not commensurate with the extent of risk transferred, it can deny the capital relief to the originator.

Under three circumstances, a transaction is deemed to have achieved SRT and they are:

In case, the originator wishes to achieve SRT with the help of 1 & 2, the same has to be notified to the regulator. If as per the regulator, the risk weights assigned by the originator does not commensurate with the risks transferred, the firms will not be able to avail the reduced risk weights.

The underlying assumptions behind the SRT conditions have been elucidated in the EU’s Discussion Paper on Significant Risk Transfer in Securitisation.

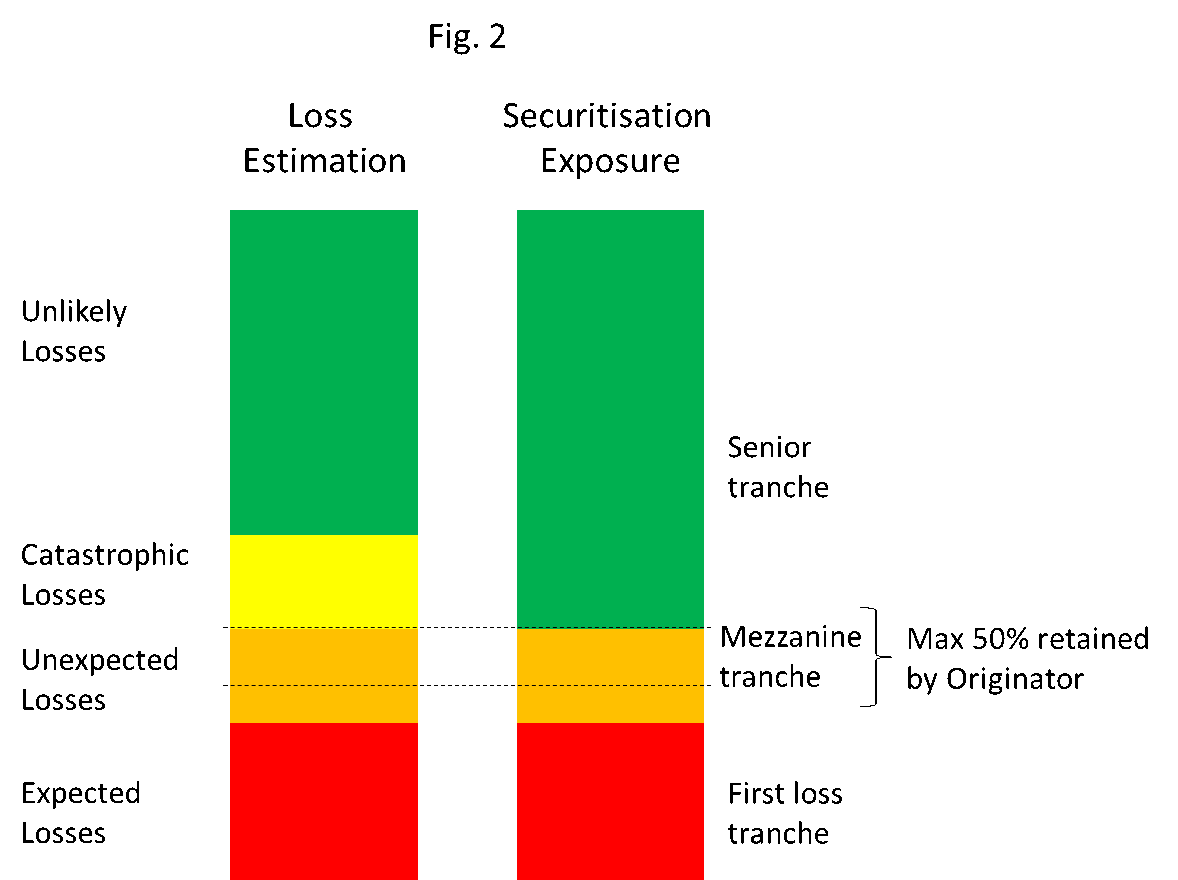

The following graphics will illustrate the conditions better:

In figure 1, the mezzanine tranche is thick enough to cover the entire unexpected losses. If in the present case, 50% of the total unexpected losses are transferred to a third party, then the transaction shall qualify for capital relief.

Unlike in case of figure 1, in figure 2, the mezzanine tranche does not capture the entire unexpected losses. The thickness of the tranche is much less than what it should have been, and the remaining amount of unexpected losses have been included in the first loss tranche itself.

Unlike in case of figure 1, in figure 2, the mezzanine tranche does not capture the entire unexpected losses. The thickness of the tranche is much less than what it should have been, and the remaining amount of unexpected losses have been included in the first loss tranche itself.

In the present case, even if the mezzanine tranche does not commensurate with the unexpected losses, the transaction will still qualify for capital relief, because, if the first loss tranche is retained by the originator, it will have to be either deducted from CET1/ assign risk weights of 1250%

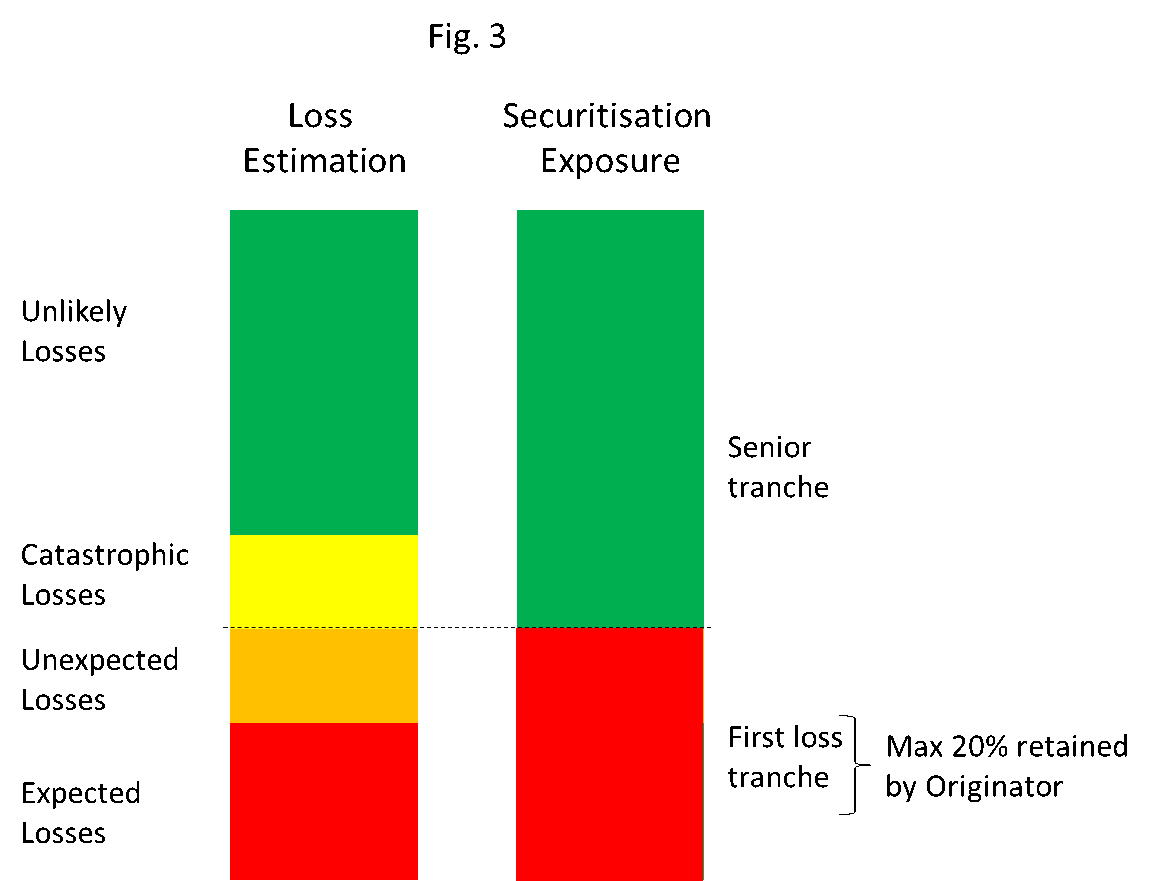

In figure 3, there is no mezzanine tranche. In the present case, the first loss tranche covers the entire expected as well as the unexpected losses. In order to demonstrate a significant risk transfer, the originator can retain a maximum of 20% of the securitisation exposure.

In figure 3, there is no mezzanine tranche. In the present case, the first loss tranche covers the entire expected as well as the unexpected losses. In order to demonstrate a significant risk transfer, the originator can retain a maximum of 20% of the securitisation exposure.

Currently, the draft Directions do not provide any logic behind the conditions it inserted for the purpose of capital relief, neither are they as elaborate as the ones under EU Guidelines. Some explicit clarity in this regard in the final Directions will provide the necessary clarity.

Also, with respect the mezzanine test, in the Indian context, the condition should be coupled with a condition that the first loss tranche, when retained by the originator, must attract 1250% risk weights or be deducted from CET 1. Only then, the desired objective of transferring significant risks of unexpected losses, will be achieved.

Further, as pointed out earlier in the note, there is a clear conflict in the conditions laid down in the para 16 and that in the first loss test in para 79, which must be resolved.

2 hours of talk and discussion on

12th June, 2020, from 11.30 to 13.30 hrs

By

Vinod Kothari

See details here – https://vinodkothari.com/webinar-on-securitisation-and-sale-of-standard-assets/

Team, Vinod Kothari Consultants P. Ltd.

Major changes have been proposed by the RBI in the regime on what has become a major part of the business model of NBFCs and MFIs in the country – direct assignments (DAs). We have separately dealt with the Draft Directions on Securitisation of Standard Assets in a write up titled “New regime for securitisation and sale of financial assets”

The term DA is so very typical of the Indian scene – globally, the practice of loan trading, loan sales or so-called whole-loan transfers has largely been out of the regulatory domain. However, in India, the motivation to shift from securitisation to DAs were partly the RBI Guidelines of 2006 which regulated securitisation but did not regulate DAs, and partly, the tax issues on securitisation that began prominent around 2011-12 or so. However, the DA model has, over the years, been a sizeable part of securitisation volumes in India, and is the mainstay of transfer of priority-sector loans from NBFCs to banks. Now that NBFCs have been permitted a major push for MSE lending by several GoI schemes, NBFCs are eagerly looking for another round of DA drive, and therefore, it is important to see whether the proposed regulatory regime for loan sales will facilitate NBFC-originated loans to end up on the books of banks and other investors.

Team, Vinod Kothari Consultants

On Monday, 8th June, 2020, the RBI released, for public comments, two separate draft guidelines, one for securitisation of standard assets, and the other for sale of loans. Once implemented, these guidelines will replace the existing regulatory framework that has stood ground, in case of securitisation for the last 14 years, and 8 years in case of direct assignment. We have separately dealt with the Draft Directions on Securitisation of Standard Assets in a write up titled “Originated to transfer- new RBI regime on loan sales permits risk transfers”