Global Securitisation Markets in 2020: A Year of Highs in the midst of Turmoil

-Vinod Kothari (vinod@vinodkothari.com)

[Revised March 2021]

Even as the pandemic disrupted life and economies across the globe, securitisation activity in different countries scaled new highs, at least in certain asset classes.

Securitisation in USA

Agency and non-agency RMBS

Agency RMBS was the star performer, at least in terms of new issuance volumes. Data available till Nov 2020 suggests that the new issuance volumes for 2020 will be about double of what it was in 2019, and the highest ever achieved in history. There are two reasons primarily responsible, of which the first one is quite obvious – historically low mortgage rates, particularly for refinancing activity. Second reason is that during the pandemic, there was extensive use of technology in mortgage origination and documentation, which led to far faster and simpler turnarounds for the borrowers.

Non-agency RMBS, however, is expected to end about 40% lower than 2019 volumes. Origination levels were halted because of shut-downs and the prevailing economic situation. Lenders put caution on the forefront as 30-day delinquencies continued to soar up.

Figure 1: US RMBS Issuance [By author, based on SIFMA data]

As may be clear, the issuance of agency MBS in 2020 was almost double of last year, whereas as non-agency securities were 45% lower or almost half of the number in 2019.

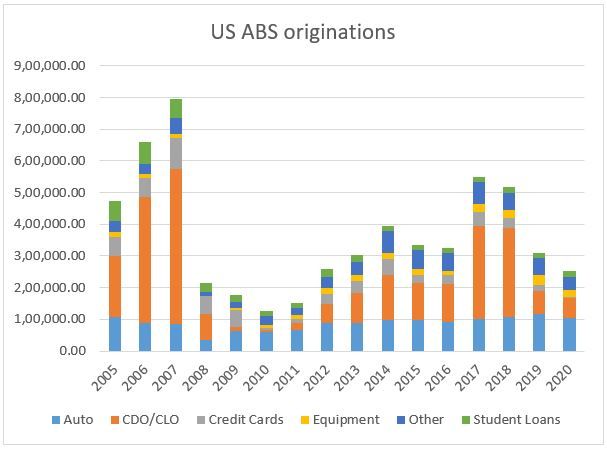

Asset-backed securities

The issuance volumes across all other classes of asset backed securities were down – from about 6% in case of auto-ABS to about 90% in case of credit cards ABS.

Figure 2: ABS issuance in USA

The CLO market was among the asset classes very badly affected, with the 2020 issuance less than 40% of the number in 2019. The decline in origination volumes of asset classes like credit cards is attributed to tighter lending standards by banks, and of course, lesser spending by individuals on travel or amusement, due to lock down.

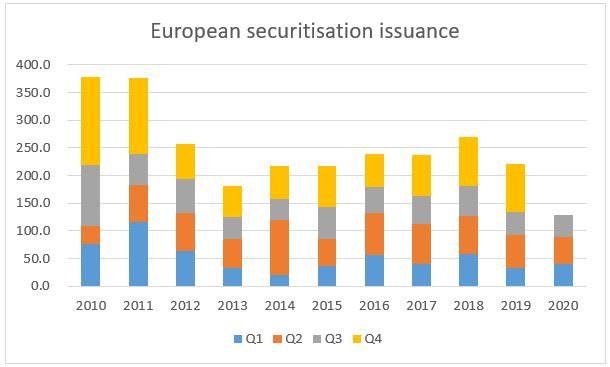

Securitisation in Europe

Euro area will end with a GDP contraction estimated at 7.7% in 2020[1].

As per data prepared by AFME, new issuance in 2020 in Europe was down by about 11.9% compared to 2019[2].

EU regulators proposed some amendments to securitisation regulations, by amending Capital Requirements Regulations. “Securitisation can play an important role in enhancing the capacity of institutions to support the economic recovery, providing for an effective tool for funding and risk diversification for institutions. It is therefore essential in the context of the economic recovery post COVID-19 pandemic to reinforce that role and help institutions to be able to channel sufficient capital to the real economy.”[3] Accordingly, three amendments are proposed to securitisation regulatory framework: more risk-sensitive treatment for STS on-balance-sheet securitisation; removal of regulatory constraints to the securitisation of non-performing exposures; and recognition of credit risk mitigation for securitisation positions.

Figure 3: European securitisation issuance

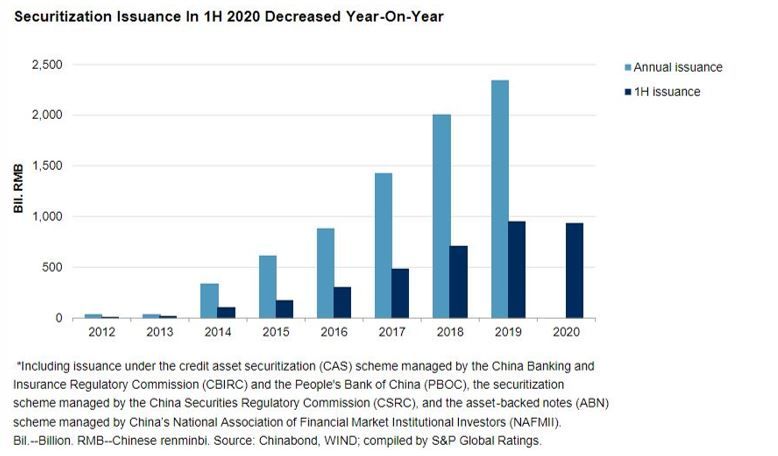

Securitisation in China

Securitisation in China is expected to be about 10-15% lower than the volumes in 2019. A report from S&P recorded first half of 2020 to be almost the same as first half of 2019, but given the concerns and tightened lending by banks, it is expected that lower RMBS issuance will keep overall issuance levels low in 2020[4].

Figure 4: Securitisation Issuance in China – from S&P report

Securitisation in India

Indian securitisation statistics are typically collated on April-March basis. For Q2, Q3 and Q4 of calendar year 2020, securitisation activity [in Indian parlance, securitisation also includes bilateral portfolio transfers, called direct assignment] was highly subdued, as shadow-banking entities which are the major originators of transactions had stopped lending due to the prevailing lock-down. In addition, there were moratoriums imposed by the RBI whereby payments under existing loans were permitted to be withheld for a period of 5 months.

However, once the lockdowns have gradually been lifted, there is a very strong resurgence of economic activity. The Govt. had provided a sovereign guarantee for an additional 20% lending on existing lending facilities, subject to limits. While the non-banking financial entities are not needing significant funding by way of securitisation, there is a strong investor appetite.

This period has also been associated with defaults or credit events by some of the originators, and sale of the ABS investments held by some mutual funds. Hence, the market has seen servicer transitions, as also tested the (il)liquidity of investments in securitisation transactions.

Rating activity

As may be expected, there have been major rating actions during the year as performance of most asset classes was disrupted due to the pandemic. Rating agency S&P reported 2551 structured finance rating actions, which included 1950 downgrades owing to the impact of the pandemic[5]. Moody’s, in a report, states that once Covid-led payment holidays abate, there will be increasing pressures on retail-focused ABS transactions. RMBS transactions, consumer ABS etc are likely to see rising delinquencies.

Moody’s also forecasts the default rates in non-investment grade corporates to increase to 9.7% (trailing average of 12 months) by March, 2021. This will be the highest default rate after 2009. This will result into substantial pressure on CLOs.[6]

[1] Moody’s estimate

[2] https://www.afme.eu/Publications/Data-Research/Details/AFME-Securitisation-Data-Report-Q4-2020

[3] https://oeil.secure.europarl.europa.eu/oeil/popups/printficheglobal.pdf?id=716379&l=en

[4] https://www.spglobal.com/ratings/en/research/articles/200811-china-securitization-performance-watch-2q-2020-the-worst-may-have-passed-11604587

[5] https://www.spglobal.com/ratings/en/research/articles/201218-covid-19-activity-in-global-structured-finance-as-of-dec-11-2020-11782903

[6] https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBS_1249099

Link to related articles:

Banking exposure to open the current account by the banks

-Siddarth Goel (finserv@vinodkothari.com)

Background

Declaration from current account customers

The RBI issued a circular dated August 06, 2020, whereby the regulator instructed all scheduled commercial banks and payments banks shall not open a current account for customers who have availed credit facilities in form of cash credit (CC)/overdraft (OD) from the banking system. The motive behind the circular being that all the transactions of borrowers should be routed through the CC/OD account.

The genesis of this circular was in RBI circular dated May 15, 2004, where banks were advised that at the time of opening of current accounts for their customers, they have to insist on a declaration form by the account-holder to the effect that he is not enjoying any credit facility with any other bank or obtain a declaration giving particulars of credit facilities enjoyed by such customer. The move was in essence to secure the overall credit discipline in banking so that there is no diversion of funds by the borrowers to the detriment of the banking system. Post-May 15, 2004, a clarification notification was issued by the regulator dated August 04, 2004, stipulating that in case there is no response obtained concerning NOC after waiting a minimum period of a fortnight, the banks may open current accounts of the customers.

Thus there was an obligation on banks to scrupulously ensure that their branches do not open current accounts of entities that enjoy credit facilities (fund based or non-fund based) from the banking system without specifically obtaining a No-Objection Certificate (NOC) from the lending bank(s). Further, the non-adherence by banks as per the circular is to be perceived as abetting the siphoning of funds and such violations which are either reported to RBI or noticed during the regulator inspection would make the concerned banks liable for penalty under Banking Regulation Act.

Establishment of CRILC

The RBI established a Central Repository of Information on Large Credits (CRILC). The CRILC was established in connection to the RBI framework “Early Recognition of Financial Distress, Prompt Steps for Resolution and Fair Recovery for Lenders: Framework for Revitalising Distressed Assets in the Economy“. As under the framework banks were required to furnish credit information to CRILC on all their borrowers having aggregate fund-based and non-fund based exposure of Rs. 5 Crores and above with them. Besides banks were required to furnish current accounts of their customers with outstanding balance (debit or credit) of Rs 1 Crore and above to the CRILC. The reporting under the extant framework was to determine SMA-0 classification, where the principal or interest payment is not overdue for more than 30 days but account showing signs of stress. An increase in the frequency of overdrafts in current accounts is one of the illustrative methods for determining stress.

Reposting of large credits

Post establishment of CRILC, a subsequent guideline on the opening of current accounts by banks was issued by the RBI via circular dated July 02, 2015, dealing with the same subject. To enhance credit discipline, especially for the reduction in NPA level in banks, banks were asked to use the information available in CRILC and not limit their due diligence to seeking NOC. Banks were to verify from the data available in the CRILC database whether the customer is availing of credit facility from another bank.

The chart below highlights the series and events and relevant circulars.

Credit Discipline- August 06, 2020 Circular

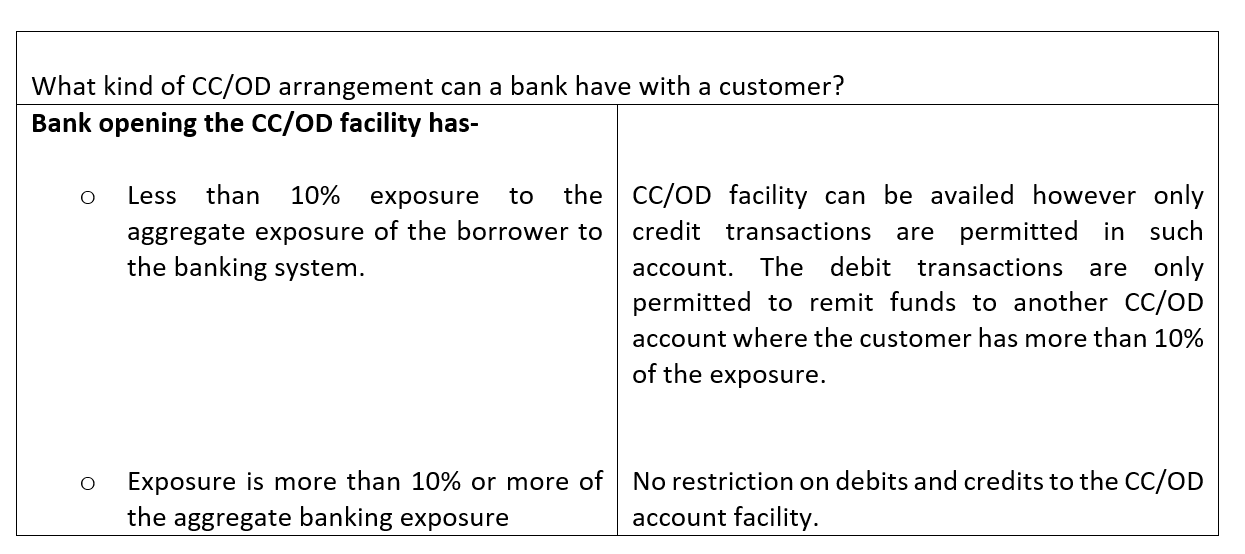

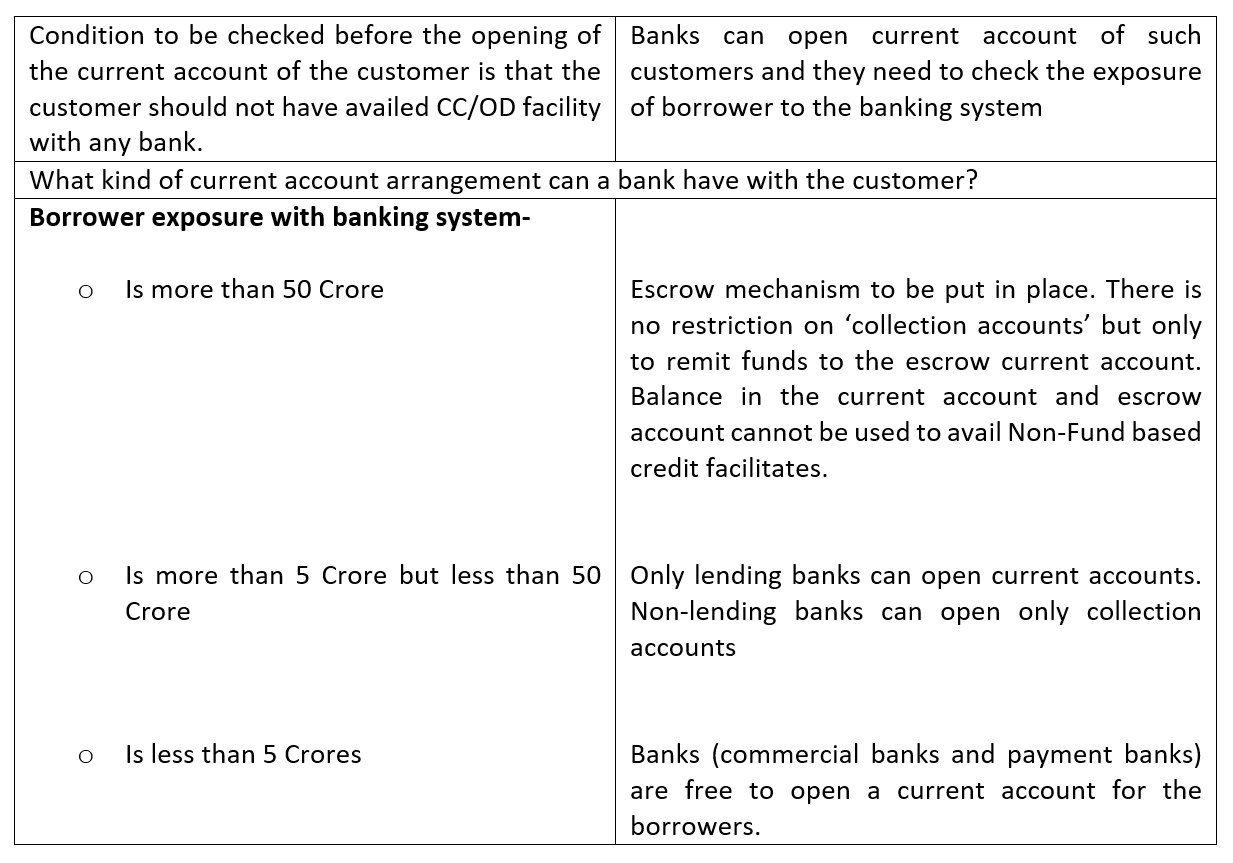

As per the circular dated August 06, 2020, issued by the regulator on Opening of Current Accounts by Banks – Need for Discipline (‘Revised Guidelines’), there are two aspects that need to be considered before opening a CC/OD facility or opening the current account of the customer. The Revised Guidelines provides a clear guiding flowchart for banks to follow when the customer approaches a bank for opening of the current account, the same has been categorised into two scenarios which could be considered by the banks to comply with the revised guideline.

Case 1: Customer wants to avail or is already having a credit facility in form of CC/OD

Case 2: Customer wants to open a current account or have an existing current account with the bank

Further, there is a requirement on banks to monitor all CC/OD accounts regularly at least quarterly, especially concerning the exposure of the banking system to the borrower. There has been an ambiguity surrounding what would amount to ‘exposure’ under the Revised Guidelines.

‘Exposure to the banking system’ under Revised Guidelines

The Revised Guidelines provides that exposure shall mean the sum of sanctioned ‘fund based and non-fund based credit facilities’. However, there is a regulatory ambiguity, since neither the term used by the RBI has been specifically defined in the Revised Guideline nor elsewhere under any other regulations. There is no straight jacket exclusive definition for determining as to what exposure banks should include determining funded and non-funded credit facilities. Therefore, based on back-tracing of regulatory regime an inclusive list can be of guidance for banks and borrowers especially large borrowers (like NBFCs and HFCs) and other financial institutions and corporates who rely on banking facilities (current account and CC/OD) extensively for their business.

The CRILC may not be the only source for banks while the collection of borrower’s credit information. Other modes could be information by Credit Information Companies (CICs), National E-Governance Services Ltd. (NeSL), etc., and even by obtaining customers’ declaration, if required. However, since the revised guideline stresses on borrowers having exposure more than 5 crores, therefore, information disseminated by the banks to CRILC is a good point to start with and to comply with under the revised guidelines. The circular dated July 02, 2015, draws reference to the Central Repository of Information on Large Credits (CRILC) to collect, store, and disseminate data on all borrowers’ credit exposures. The guideline further provided banks to verify the data available in the CRILC database whether the customer is availing credit facility from another bank. Further even under the Guidelines on “Early Recognition of Financial Distress, Prompt Steps for Resolution and Fair Recovery for Lenders” dated January 30, 2014, provided that credit information shall include all types of exposures as defined under RBI Circular on Exposure Norms.

The RBI Exposure Norms dated July 01, 2015, defines exposure as;

“Exposure shall include credit exposure (funded and non-funded credit limits) and investment exposure (including underwriting and similar commitments). The sanctioned limits or outstandings, whichever are higher, shall be reckoned for arriving at the exposure limit. However, in the case of fully drawn term loans, where there is no scope for re-drawal of any portion of the sanctioned limit, banks may reckon the outstanding as the exposure.”

The banking exposure norms provide for two exposures; namely credit and investment exposures. Further RBI Exposure Norms defines ‘credit exposure’ and ‘Investment Exposure’ as follows;

“2.1.3.3. Credit Exposure

Credit exposure comprises the following elements:

(a) all types of funded and non-funded credit limits.

(b) facilities extended by way of equipment leasing, hire purchase finance and factoring services.

2.1.3.4 Investment Exposure

- a) Investment exposure comprises the following elements:

(i) investments in shares and debentures of companies.

(ii) investment in PSU bonds

(iii) investments in Commercial Papers (CPs).

- b) Banks’ / FIs’ investments in debentures/ bonds / security receipts / pass-through certificates (PTCs) issued by an SC / RC as compensation consequent upon sale of financial assets will constitute exposure on the SC / RC. In view of the extraordinary nature of the event, banks / FIs will be allowed, in the initial years, to exceed the prudential exposure ceiling on a case-to-case basis.

- c) The investment made by the banks in bonds and debentures of corporates which are guaranteed by a PFI1(as per list given in Annex 1) will be treated as an exposure by the bank on the PFI and not on the corporate.

- d) Guarantees issued by the PFI to the bonds of corporates will be treated as an exposure by the PFI to the corporates to the extent of 50 per cent, being a non-fund facility, whereas the exposure of the bank on the PFI guaranteeing the corporate bond will be 100 per cent. The PFI before guaranteeing the bonds/debentures should, however, take into account the overall exposure of the guaranteed unit to the financial system.”

The Revised Guidelines, specifically define exposure in a footnote to the revised guideline stipulating that to arrive at aggregate exposures in the footnote as follows;

“‘Exposure’ for the purpose of these instructions shall mean sum of sanctioned fund based and non-fund based credit facilities”.

Further the RBI in its subsequent FAQs on revised guidelines dated December 14, 2020, guided on what could be included in aggregate exposure.

“4. Whether aggregate exposure shall include Day Light Over Draft (DLOD)/ intra-day facilities and irrevocable payment commitments, limits set up for transacting in FX and interest rate derivatives, CPs, etc.

All fund based and non-fund based credit facilities sanctioned by the banks and carried in their Indian books shall be included for the purpose of aggregate exposure.”

Further in FAQ No. 3 in the circular dated December 14, 2020, the RBI clarified that

“3. For the purpose of this circular, whether exposure of non-banking financial companies (NBFCs) and other financial institutions like National Housing Bank (NHB) shall be included in computing aggregate exposure of the banking system.

The instructions are applicable to Scheduled Commercial Banks and Payments Banks. Accordingly, the aggregate exposure for the purpose shall include exposures of these banks only”

While the regulator evaded assigning express meaning as to what could be included while determining banking exposure and took an inclusive view. However, from the foregoing, it is amply clear that the credit facilities should include credit exposures (funded and not funded) that have been sanctioned by banks. Therefore, only exposures to banks and payments banks are to be included while calculating exposures, any or all the exposure of a borrower to the other financial institutions like NHB, LIC Housing, SIDBI, NABARD, Mutual funds & other development Banks are neither commercial banks nor payments banks hence are to be excluded. [The list of licensed payments banks by the RBI can be viewed here. ]

CIRLC captures credit information of borrowers having aggregate fund-based and non-fund based exposures of Rs. 5 Crores and above including investment exposures. The banks are required to submit a quarterly return to CIRLC. It is pertinent to note that total investment exposure is to be indicated separately under the head total investment exposure. While there is a need for a detailed breakup on fund-based and non-fund based credit facilities in the CIRLC return. The table below is an indicative list of (funded and non-funded) loans to be submitted from the CIRLC return.

| Non-Funded credit exposure | Funded credit exposure |

| Letter of Credit | Cash Credit/ Overdraft |

| Guarantees | Working Capital Demand Loan (including CPs)* |

| Acceptances | Inland Bills |

| Foreign Exchange Contracts | Packing Credit |

| Interest Rate Derivatives (incl FX Interest Rate Derivatives) | Export Bills |

| Term Loan | |

| Credit equivalent of OBS/derivative exposure |

*CP to be included in WCDL only if part of working capital sanctioned limit. All other CPs are to be considered as investment exposure.

Therefore, all the investment exposures of banks to the borrower such as investments in corporate bonds, shares, PTCs issued by asset reconstruction companies and securitisation companies, and others are to be excluded while arriving at aggregate fund-based and non-fund based credit facilities as under the Revised Guidelines. Nevertheless, the PTCs issued by NBFCs or HFCs are investment exposure of banks on the underlying loan pools and not on the originator entity. Similarly, exposure of a bank in a co-lending transaction is exposure on the ultimate obligor and not the co-originating partner NBFC.

Our Other Related Articles

Banking Regulation (Amendment) Ordinance By Vallari Dubey – Vinod Kothari Consultants

RBI guidelines on governance in commercial banks – Vinod Kothari Consultants

RBI proposes to strengthen governance in Banks – Vinod Kothari Consultants

First phase of commencement of Companies (Amendment) Act, 2020

-Commencement notification dated 21st December, 2020

Smriti Wadehra, Manager and Henil Shah, Assistant Manger

The Ministry of Corporate Affairs vide its commencement Notification dated 21st December, 2020 has notified 45 sections of the Companies (Amendment) Act, 2020 [1]which recently received the President’s assent on 28th September, 2020[2]. The sections notified by the Ministry majorly relate to re-categorization of criminal offences into civil wrongs which is in line with the Government of India’s policy to decriminalise non-compliances that are technical and procedural nature thereby promoting ease of doing business.

A brief synopsis of the amendments is detailed below:

| Section No. of CAA, 2020 | Section No. of CA, 2013 | Pertains to | Existing Provisions | Amended Provisions |

| Shift from fine to penalty | ||||

| 9 | 56(6) | Any default in transfer and transmission of Securities | Fine on Company: Min Rs. 25,000 Max Rs. 5 Lakhs and

Fine on Officer of the company in default: Min- Rs.10,000 Max – Rs. 1 Lakhs.

|

The company and every officer of the company who is in default shall be liable to a penalty of Rs. 50,000. |

| 16 | 86(1) | Contravention of provisions relating to registration of charges | Fine on Company: Min- Rs. 1 Lakh Max- Rs. 10 Lakhs

Fine on officer in default: Imprisonment for a term which may extend to 6 months or with fine Min- Rs. 25,000 Max- Rs. 1 Lakh, or with both. |

Company shall be liable to a penalty of Rs. 5 Lakhs and every officer of the company who is in default shall be liable to a penalty of Rs. 50,000. |

| 17 | 88(5) | Failure to maintain Register of Members or debenture holders etc.

|

Fine on Company: Min- Rs. 50,000 Max- Rs. 3 Lakhs and where the failure is a continuing one, with a further fine of Rs. 1000 for every day,

Every officer of the company who is in default: Fine of min- Rs. 50,000 Max-Rs. 3 Lakhs where the failure is a continuing one, with a further fine of Rs. 1000 for every day.

|

Company shall be liable to a penalty of Rs. 3 Lakhs and every officer of the company who is in default shall be liable to a penalty of Rs. 50,000. |

| 18 | 89(5) | Failure to submit declaration in respect of beneficial Interest in any share

|

Person shall be punishable with fine which may extend to Rs. 50,000 and where the failure is a continuing one, with a further fine which may extend to Rs. 1000 for every day after the first during which the failure continues.

|

Person shall be liable to a penalty of Rs. 50,000 and in case of continuing failure, with a further penalty of Rs. 200 for each day after the first during which such failure continues, subject to a maximum of Rs. 5 Lakhs. |

| 18 | 89(6) | Declaration in Respect of Beneficial Interest in any Share

|

The company and every officer of the company who is in default shall be punishable with fine which shall not be less than Rs. 500 but which may extend to Rs. 1000 and where the failure is a continuing one, with a further fine which may extend to Rs. 1000 for every day after the first during which the failure continues.

|

The company and every officer of the company who is in default shall be liable to a penalty of Rs. 1000 for each day during which such failure continues, subject to a maximum of Rs. 5 Lakhs in the case of a company and Rs. 2 Lakhs in case of an officer who is in default. |

| 19 | 90(10) | Failure to declare significant beneficial ownership in the Company | Person shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 10 Lakhs or with both and where the failure is a continuing one, with a further fine which may extend to Rs. 1000 for every day after the first during which the failure continues.

|

Person shall be liable to penalty of Rs. 50,000 and in case of continuing failure, with a further penalty of Rs. 1000 for each day after the first during which such failure continues, subject to a maximum of Rs. 2 Lakhs. |

| 19 | 90(11) | Failure to maintain register of significant beneficial owners in a company

|

Company and every officer of the company who is in default shall be punishable with fine which shall not be less than Rs. 10 Lakhs but which may extend to Rs. 50 Lakhs and where the failure is a continuing one, with a further fine which may extend to Ra. 1000 for every day after the first during which the failure continues. | Company shall be liable to a penalty of Rs. 1 Lakhs and in case of continuing failure, with a further penalty of Rs. 500 for each day, after the first during which such failure continues, subject to a maximum of Rs. 5 Lakhs and every officer of the company who is in default shall be liable to a penalty of Rs. 25,000 and in case of continuing failure, with a further penalty of Rs. 200 for each day, after the first during which such failure continues, subject to a maximum of Rs.1 Lakh

|

| 20 | 92(6) | Certification of Annual Return not in conformity with the section

|

Company secretary in practice shall be punishable with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 5 Lakhs.

|

Company secretary in practice shall be liable to a penalty of Rs. 2 Lakhs. |

| 21 | 105(5) | Proxies | If for the purpose of any meeting of a company, invitations to appoint as proxy a person or one of a number of persons specified in the invitations are issued at the company’s expense to any member entitled to have a notice of the meeting sent to him and to vote thereat by proxy, every officer of the company who knowingly issues the invitations as aforesaid or wilfully authorises or permits their issue

shall be punishable with fine which may extend to Rs. 1 Lakh: Provided that an officer shall not be punishable under this sub-section by reason only of the issue to a member at his request in writing of a form of appointment naming the proxy, or of a list of persons willing to act as proxies, if the form or list is available on request in writing to every member entitled to vote at the meeting by proxy.

|

If for the purpose of any meeting of a company, invitations to appoint as proxy a person or one of a number of persons specified in the invitations are issued at the company’s expense to any member entitled to have a notice of the meeting sent to him and to vote thereat by proxy, every officer of the company who issues the invitation as aforesaid or authorises or permits their issue, shall be liable to a penalty of Rs. 50,000.

Provided that an officer shall not be liable under this sub-section by reason only of the issue to a member at his request in writing of a form of appointment naming the proxy, or of a list of persons willing to act as proxies, if the form or list is available on request in writing to every member entitled to vote at the meeting by proxy |

| 30 | 143(15) | Failure to report fraud under the section | Any auditor, cost accountant or company secretary in practice shall be punishable with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 25 Lakhs. | Any auditor, cost accountant, or company secretary shall,

(a) in case of a listed company, be liable to a penalty of Rs. 5 Lakhs; and (b) in case of any other company, be liable to a penalty of Rs. 1 Lakh |

| 35 | 172 | Non-compliance of any provisions of chapter relating to appointment and qualification of directors | Company and every officer of the company who is in default shall be punishable with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 5 Lakhs. | Company and every officer of the company who is in default shall be liable to a penalty of Rs. 50,000, and in case of continuing failure, with a further penalty of Rs. 500 for each day during which such failure continues, subject to a maximum of Rs. 3 Lakhs in case of a company

|

| 36 | 178(8) | Non-compliance of provisions relating to section 177 and 178 of the Act. | Company shall be punishable with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 5 Lakhs and every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 1 Lakh, or with both.

|

Company shall be liable to a penalty of Rs. 5 Lakhs and every officer of the company who is in default shall be liable to a penalty of Rs. 1 Lakh.

|

| 37 | 184(4) | Failure of disclosure of Interest by Director

|

Director shall be punishable with imprisonment for a term which may extend to 1 year or with fine which may extend to Rs. 1 Lakh, or with both. | Director shall be liable to a penalty of Rs. 1 Lakh.

|

| 38 | 187(4) | Failure to hold investments by the company in its own name

|

The company shall be punishable with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 25 Lakhs and every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 6 months or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 1 Lakh, or with both.

|

The company shall be liable to a penalty of Rs 5 Lakhs and every officer of the company who is in default shall be liable to a penalty of Rs. 50,000. |

| 39 | 188(5) | Related Party Transactions

|

Any director or any other employee of a company, who had entered into or authorised the contract or arrangement in violation of the provisions of this section shall-

(i) in case of listed company, be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 5 Lakhs, or with both; and (ii) In case of any other company, be punishable with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 5 Lakhs.

|

Any director or any other employee of a company, who had entered into or authorised the contract or arrangement in violation of the provisions of this section shall-

(i) in case of listed company, be liable to a penalty Rs. 25 Lakhs; and (ii) In case of any other company, be liable to a penalty of Rs. 5 Lakhs. |

| 41 | 204(4) | Contravention of provisions relating to secretarial Audit for bigger companies

|

The company, every officer of the company or the company secretary in practice, who is in default, shall be punishable with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 5 Lakhs. | The company, every officer of the company or the company secretary in practice, who is in default, shall be liable to a penalty of Rs. 2 Lakhs. |

| 42 | 232(8) | Merger and Amalgamation of Companies

|

If a transferor company or a transferee company contravenes the provisions of the section, the transferor company or the transferee company, as the case may be, shall be punishable with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 25 Lakhs and every officer of such transferor or transferee company who is in default, shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 3 Lakhs, or with both.

|

If a company fails to file the certified true copy of the order with the Registrar for registration within 30 days of the receipt of order, the company and every officer of the company who is in default shall be liable to a penalty of Rs. 20,000, and where the failure is a continuing one, with a further penalty of Rs. 1000 for each day after the first during which such failure continues, subject to a maximum of Rs. 3 Lakhs. |

| 57 | 405 | Failure to provide any information or statistic to CG | Company shall be punishable with fine which may extend to Rs. 25,000 and every officer of the company who is in default, shall be punishable with imprisonment for a term which may extend to 6 months or with fine which shall not be less than Rs. 25, 000 but which may extend to 3 lakh rupees, or with both.

|

The company and every officer of the company who is in default shall be liable to a penalty of Rs. 25,000 and in case of continuing failure, with a further penalty of Rs. 1000 for each day after the first during which such failure continues, subject to a maximum of Rs. 3 lakh rupees. |

| 63 | 450 | Punishment where no specific penalty or punishment is provided | Company and every officer of the company who is in default or such other person shall be punishable with fine which may extend to Rs. 10,000, and where the contravention is continuing one, with a further fine which may extend to Rs. 1000 for every day after the first during which the contravention continues. | Company and every officer of the company who is in default or such other person shall be liable to a penalty of Rs. 10,000 and in case of continuing contravention, with a further penalty of Rs. 1000 foreach day after the first during which the contravention continues, subject to a maximum of Rs. 2 lakhs in case of a company and Rs. 50,000 in case of an officer who is in default or any other person.

|

| Omission of imprisonment provisions | ||||

| 3 | 8(11) | Failure in fulfilment in requirement relating to formation of companies with Charitable Objects, etc.

|

Directors and every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 3 years or with fine which shall not be less than Rs. 25000 which may extend to Rs. 25 lakhs, or with both.

Provided that when it is proved that the affairs of the company were conducted fraudulently, every officer in default shall be liable for action under section 447.

|

Directors and every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 3 years or with fine which shall not be less than Rs. 25000 which may extend to Rs. 25 lakhs, or with both.

Provided that when it is proved that the affairs of the company were conducted fraudulently, every officer in default shall be liable for action under section 447.

|

| 6 | 26(9) | Issue of prospectus in contravention of provisions of section 26 of the Act | Every person who is knowingly a party to the issue of such prospectus:

shall be punishable with imprisonment for a term which may extend to three years or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 3 Lakhs or with both. |

Every person who is knowingly a party to the issue of such prospectus:

shall be punishable with imprisonment for a term which may extend to three years or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 3 Lakhs or with both.

|

| 7 | 40(5) | Default in complying with provisions relating to securities being dealt with in Stock Exchanges

|

Every officer of the company who is in default shall be punishable:

With imprisonment for a term which may extend to one year or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 3 Lakhs, or with both.

|

Every officer of the company who is in default shall be punishable :

With imprisonment for a term which may extend to one year or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 3 Lakhs, or with both.

|

| 14 | 68(11) | Non-compliance of buyback provisions | Every officer of the company who is in default shall be punishable:

With imprisonment for a term which may extend to 3 years or with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 3 Lakhs, or with both.

|

Every officer of the company who is in default shall be punishable:

With imprisonment for a term which may extend to 3 years or with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 3 Lakhs, or with both.

|

| 24 | 128(6) | Books of Account, etc., to be kept by Company

|

If the managing director, the whole-time director in charge of finance, the Chief Financial Officer or any other person of a company charged by the Board with the duty of maintenance of books of accounts of the company and contravenes such provisions, such persons of the company shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 5 Lakhs or with both.

|

If the managing director, the whole-time director in charge of finance, the Chief Financial Officer or any other person of a company charged by the Board duty of maintenance of books of accounts of the company and contravenes such provisions, such persons of the company shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 5 Lakhs or with both.

|

| 26 | 134(8) | Contravention of provision relating to the Financial Statements, Board’s Report, etc of the Company | Every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 3 years or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 5 Lakhs, or with both.

|

Every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 3 years shall be liable to a penalty of Rs. 50,000.

|

| 31 | 147(1) | Punishment for contravention of provision relating to appointment of auditors and audit of the Company | Every officer of the company who is in default shall be punishable:

with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 10,000 but which may extend to Rs. 1 Lakh, or with both.

|

Every officer of the company who is in default shall be punishable:

with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 10,000 but which may extend to Rs. 1 Lakh, or with both.

|

| 34 | 167(2) | Continuation of office by director after knowing his disqualifications | Director shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 5 Lakhs, or with both

|

Director shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 5 Lakhs, or with both

|

| 43 | 242(8) | Failure to comply with alteration in the charter documents by the Tribunal | Every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 6 months or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 1 Lakh, or with both.

|

Every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to 6 months or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 1 Lakh, or with both.

|

| 44 | 243(2) | Person who knowingly acts as MD or other director in the company while entering into agreements | Such person shall be punishable with imprisonment for a term which may extend to 6 months or with fine which may extend to Rs. 5 Lakhs, or with both.

|

Such person shall be punishable with imprisonment for a term which may extend to 6 months or with fine which may extend to Rs. 5 Lakhs, or with both.

|

| 49 | 347(4) | Disposal of Books and Papers of Company.

|

If any person acts in contravention of any rule framed or an order made under sub-section (3), he shall be punishable with imprisonment for a term which may extend to 6 months or with fine which may extend to Rs. 50,000, or with both.

|

If any person acts in contravention of any rule framed or an order made under sub-section (3), he shall be punishable with imprisonment for a term which may extend to 6 months or with fine which may extend to Rs. 50,000, or with both.

|

| 54 | 392 | Punishment for contravention of provisions of Chapter XXII relating to companies incorporated outside India | The foreign company shall be punishable with fine which shall not be less than Rs. 1 lakh but which may extend to Rs. 3 lakh and in the case of a continuing offence, with an additional fine which may extend to Rs. 50, 000 for every day after the first during which the contravention continues and every officer of the foreign company who is in default shall be punishable with imprisonment for a term which may extend to 6 months or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 5 lakhs, or with both | The foreign company shall be punishable with fine which shall not be less than Rs. 1 lakh but which may extend to Rs. 3 lakhs and in the case of a continuing offence, with an additional fine which may extend to Rs. 50, 000 for every day after the first during which the contravention continues and every officer of the foreign company who is in default shall be punishable with imprisonment for a term which may extend to six months or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 5 lakhs, or with both |

| 61 | 441 | Compounding of certain offence | Any officer or other employee of the company who fails to comply with any order made by the Tribunal or the Regional Director or any officer authorised by the Central Government under sub-section (4) shall be punishable with imprisonment for a term which may extend to 6 months, or with fine not exceeding Rs. 1 lakh, or with both | If any officer or other employee of the company who fails to comply with any order made by the Tribunal or the Regional Director or any officer authorised by the Central Government under sub-section (4), the maximum amount of fine for the offence proposed to be compounded under this section shall be twice the amount provided in the corresponding section in which punishment for such offence is provided.

|

| Amendment in penal provisions | ||||

| 20 | 92(5) | Failure to file Annual Return within the specified time | Company and its every officer who is in default shall be liable to a penalty of Rs. 50,000 and in case of continuing failure, with further penalty of Rs. 100 for each day during which such failure continues, subject to a maximum of Rs. 5 Lakhs. | Company and its every officer who is in default shall be liable to a penalty of Rs. 10,000 and in case of continuing failure, with further penalty of Rs. 100 for each day during which such failure continues, subject to a maximum of Rs. 2 Lakhs in case of a company and Rs. 50,000 in case of an officer who is in default. |

| 22 | 117(2) | Failure to file resolution or agreement with the Registrar | Penalty on Company: Rs. 1 Lakh and in case of continuing failure, with further penalty of Rs. 500 for each day after the first during which such failure continues, subject to a maximum of Rs. 25 Lakhs.

Every officer of the company who is in default including liquidator of the company, if any, shall be liable to a penalty of Rs. 50,000 and in case of continuing failure, with further penalty of Rs. 500 for each day after the first during which such failure continues, subject to a maximum of Rs. 5 Lakhs. |

Penalty on Company: Rs. 10,000 and in case of continuing failure, with further penalty of Rs. 100 for each day after the first during which such failure continues, subject to a maximum of Rs. 2 Lakhs.

Every officer of the company who is in default including liquidator of the company, if any, shall be liable to a penalty of Rs. 10,000 and in case of continuing failure, with further penalty of Rs. 100 for each day after the first during which such failure continues, subject to a maximum of Rs. 50,000. |

| 28 | 137(3) | Failure to file a copy of Financial Statement to be Filed with Registrar

|

Company shall be liable to a penalty of Rs. 1000 for every day during which the failure continues but which shall not be more than Rs. 10 Lakhs, and the MD and the CFO of the company, if any, and, in the absence, any other director who is charged by the Board with the responsibility of complying with the provisions of this section, and, in the absence of any such director, all the directors of the company, shall be liable to a penalty of Rs. 1 Lakh and in case of continuing failure, with further penalty of Rs. 100 for each day after the first during which such failure continues, subject to a maximum of Rs. 5 Lakhs. | Company shall be liable to a penalty of Rs. 10,000 and in case of continuing failure, with a further penalty of Rs. 100 for each day during which such failure continues, subject to a maximum of Rs. 2 Lakhs, and the MD and the CFO of the company, if any, and, in the absence any other director who is charged by the Board with the responsibility of complying with the provisions of this section, and, in the absence of any such director, all the directors of the company, shall be liable to a penalty of Rs. 10,000 and in case of continuing failure, with further penalty of Rs. 100 for each day after the first during which such failure continues, subject to a maximum of Rs. 50,000. |

| 29 | 140(3) | Failure to file resignation with the company and Registrar | The auditor shall be liable to a penalty of Rs. 50,000 or an amount equal to the remuneration of the auditor, whichever is less, and in case of continuing failure, with further penalty of Rs. 500 for each day after the first during which such failure continues, subject to a maximum of Rs. 5 Lakhs. | The auditor shall be liable to a penalty of Rs. 50,000 or an amount equal to the remuneration of the auditor, whichever is less, and in case of continuing failure, with further penalty of Rs. 500 for each day after the first during which such failure continues, subject to a maximum of Rs. 2 Lakhs. |

| 33 | 165(6) | Failure to comply with restriction on maximum number of Directorships

|

Person shall be liable to a penalty of Rs. 5000 for each day after the first during which such contravention continues. | Person shall be liable to a penalty of Rs. 2000 for each day after the first during which such violation continues, subject to a maximum of Rs. 2 Lakhs. |

| 50 | 348(6) | Information as to pending liquidations | If a Company Liquidator contravenes the provisions of this section, the Company Liquidator shall be punishable with fine which may extend to five thousand rupees for every day during which the failure continues.

|

Where a Company Liquidator, who is an insolvency professional registered under the Insolvency and Bankruptcy Code, 2016 is in default in complying with the provisions of this section, then such default shall be deemed to be a contravention of the provisions of the said Code, and the rules and regulations made thereunder for the purposes of proceedings under Chapter VI of Part IV of that Code.

|

| Omission of penal provisions | ||||

| 8 | 48(5) | Failure to protect rights of the members during variation of Shareholders’ Rights | Fine on Company: Which shall not be less than Rs. 25,000 but which may extend to Rs. 5 Lakhs and

Every officer of the company who is in default shall be punishable: with imprisonment for a term which may extend to 6 months or with fine which shall not be less than Rs. 25,000 but which may extend to Rs. 5 Lakhs, or with both. |

Omitted |

| 10 | 59(5) | Default in complying with order of Tribunal w.r.t. rectification of register of members | Fine on Company: Which shall not be less than Rs. 1 Lakh but which may extend to Rs. 5 Lakhs and

Every officer of the company who is in default shall be punishable: With imprisonment for a term which may extend to 1 year or with fine which shall not be less than Rs. 1 Lakh but which may extend to Rs. 3 Lakhs, or with both. |

Omitted |

| 13 | 66(11) | Failure to publish the order of reduction of capital of the Company | Fine on Company: not be less than Rs. 5 Lakhs but which may extend to Rs. 25 Lakhs

|

Omitted |

| 15 | 71(11) | Failure to comply with order of Tribunal for discharge of assets of the Company | Every officer of the company who is in default shall be punishable: With imprisonment for a term which may extend to 3 years or with fine which shall not be less than Rs. 2 Lakhs but which may extend to Rs. 5 Lakhs, or with both. | Omitted |

| 46 | 284(2) | Promoters, directors etc. to cooperate with Company Liquidator | Where any person, without reasonable cause, fails to discharge his obligations under sub-section (1), he shall be punishable with imprisonment which may extend to six months or with fine which may extend to fifty thousand rupees, or with both

|

If any person required to assist or cooperate with the Company Liquidator under sub-section (1) does not assist or cooperate, the Company Liquidator may make an application to the Tribunal for necessary directions.

On receiving an application under sub-section (2), the Tribunal shall, by an order, direct the person required to assist or cooperate with the Company Liquidator to comply with the instructions of the Company Liquidator and to cooperate with him in discharging his functions and duties |

| 47 | 302(4) | Dissolution of company by Tribunal | If the Company Liquidator makes a default in forwarding a copy of the order within the period specified in sub-section (3), the Company Liquidator shall be punishable with fine which may extend to five thousand rupees for every day during which the default continues.

|

Omitted |

| 48 | 342(6) | Prosecution of Delinquent Officers and Members of Company

|

If a person fails or neglects to give assistance required by sub-section (5), he shall be liable to pay fine which shall not be less than Rs. 25,000 but which may extend to Rs. 1 Lakh.

|

|

| 50 | 348(7) | Information as to Pending Liquidations.

|

If a Company Liquidator makes wilful default in causing the statement referred to in sub-section (1) audited by a person who is not qualified to act as an auditor of the company, the Company Liquidator shall be punishable with imprisonment for a term which may extend to 6 months or with fine which may extend to Rs. 1 Lakh, or with both. | Omitted |

| Amendments relating to dissolution of company | ||||

| 47 | 302(3) | Dissolution of company by tribunal | A copy of the order shall, within thirty days from the date thereof, be forwarded by the Company Liquidator to the Registrar who shall record in the register relating to the company a minute of the dissolution of the company

|

The Tribunal shall, within a period of thirty days from the date of the order—

(a) forward a copy of the order to the Registrar who shall record in the register relating to the company a minute of the dissolution of the company; and (b) direct the Company Liquidator to forward a copy of the order to the Registrar who shall record in the register relating to the company a minute of the dissolution of the company.

|

| 51 | 356 | Powers of Tribunal to declare dissolution of company void | It shall be the duty of the Company Liquidator or the person on whose application the order was made, within thirty days after the making of the order or such further time as the Tribunal may allow, to file a certified copy of the order with the Registrar who shall register the same, and if the Company Liquidator or the person fails so to do, the Company Liquidator or the person shall be punishable with fine which may extend to ten thousand rupees for every day during which the default continues.

|

The Tribunal shall—

(a) forward a copy of the order, within thirty days from the date thereof, to the Registrar who shall record the same; and (b) direct the Company Liquidator or the person on whose application the order was made, to file a certified copy of the order, within thirty days from the date thereof or such further period as allowed by the Tribunal, with the Registrar who shall record the same |

[1] https://www.mca.gov.in/Ministry/pdf/AmendmentAct_29092020.pdf

[2] http://egazette.nic.in/WriteReadData/2020/223873.pdf

Our other write ups covering Companies (Amendment) Act, 2020:

- Highlights of Companies (Amendment) Bill, 2020: https://vinodkothari.com/2020/03/highlights-of-the-companies-amendment-bill-2020/

- Companies (Amendment) Act, 2020 PowerPoint presentation: https://vinodkothari.com/2020/09/companies-amendment-act-2020/

- Enforcement Status of Companies (Amendment) Act, 2020:https://vinodkothari.com/2020/12/enforcement-status-of-companies-amendment-act-2020/

Presentation on Decoding Due Date for AGM Extension

Our related Content:

Enforcement Status of Companies (Amendment) Act, 2020

Important Links:

- The Companies (Amendment) Act, 2020 : https://www.mca.gov.in/Ministry/pdf/AmendmentAct_29092020.pdf

- MCA notification dated December 21, 2020: https://www.mca.gov.in/Ministry/pdf/AmendmentAct_29092020.pdf

- MCA notification dated January 22, 2021: http://egazette.nic.in/WriteReadData/2021/224637.pdf

- MCA notification dated March 18, 2021: http://www.mca.gov.in/Ministry/pdf/CommencementNotification_18032021.pdf

Our other write ups covering Companies (Amendment) Act, 2020:

- Highlights of Companies (Amendment) Bill, 2020: https://vinodkothari.com/2020/03/highlights-of-the-companies-amendment-bill-2020/

- Companies (Amendment) Act, 2020 PowerPoint presentation: https://vinodkothari.com/2020/09/companies-amendment-act-2020/

MCA issues rules to squeeze out minority shareholding held in dematerialized form

Shaifali Sharma | Vinod Kothari and Company

Understanding minority squeeze out

‘Minority squeeze out’ demonstrates the power of majority shareholders to forcibly acquire shares from minority shareholders and drive them out to gain absolute control over the company.

Section 236 of the Companies Act, 2013 (‘Act, 2013’) sets out a process of squeezing out minority shareholder whereby any shareholder of the company, either alone or along with person acting in concert, holding 90% or more of the total issued equity share capital, may acquire the remaining equity shares of the company by giving an offer to the minority shareholders. This “Rule of Majority” principle was recognized in a landmark case Foss v. Harbottle, where it was held that that the minority shareholders are bound by the decision of the majority shareholders and the Courts do not interfere in the internal matters of the Company. However, the powers of majority should be exercised in reasonable manner which do not result into oppression of minority. Thus, the inherent protection under the law is that the acquisition shall take place at a fair value or higher value as determined by the valuer in accordance with Rule 27 of the (Compromise, Arrangements and Amalgamation) Rules, 2016 (‘CAA Rules, 2016’).

The section 236 was incorporated under the Act, 2013 on the recommendation of the Dr. J.J. Irani Committee Report on Company Law, 2005[1] for the reason reproduced below:

“The law should enable companies to purchase the stake of minority shareholders in order to prevent exploitation of such shareholders where a promoter has bought back more than 90% of the equity. Such purchase should, however, on the basis of a fair offer. Appropriate valuation rules for this purpose should be prescribed, or, the last known price prior to delisting, could be made the benchmark for such acquisitions.”

The purpose is to ensure a seamless takeover of a company, since in view of very smallholding of the minority shareholders; the minority shareholders neither will be able to participate in the management of the company nor will be able to seek redressal of their rights or have a meaningful participation in the company’s working. Therefore, to provide fair exit to the minority shareholders and to allow majority shareholders to exercise full control over the company, section 236 has been inserted under the Act, 2013.

This write-up endeavours to analyse (1) the existing process of acquiring minority shares held in physical form, (2) the practical difficulties for acquiring minority shares held in demat form and (3) the new rules introduced vide MCA notification[2] dated 17.12.2020 setting out the procedure of transferring minority shares held in demat form.

Modus Operandi of purchase of minority shareholding held in physical form

- Intimation to the Company

The acquirer holding 90% of the issued equity share capital of a company to inform the company of its intention to oust the minority shareholders in accordance with provisions of Section 236 of Act, 2013. At the same time, the minority shareholders can also offer their shares to be acquired to the acquirer in compliance prescribed provisions.

- Determining the fair value of shares for acquisition

Fair value of the shares of the Company whose shares are being transferred in accordance with Rule 27 (Compromise, Arrangements and Amalgamation) Rules, 2016.

Fair value of the shares of the company to be offered to the minority shareholders shall be calculated by a registered valuer in accordance with Rule 27 of the CAA Rules, 2016 which provides for evaluation criteria for listed companies as well as unlisted companies.

- Transfer Agent

The company whose shares are being transferred to the acquirer, shall act as a transfer agent for receiving and paying the price to the minority shareholders and for taking delivery of the shares and delivering such shares to the majority.

- Depositing of amount in separate account operated by the Company

The majority shareholders are required to deposit an amount equal to the value of shares to be acquired by them, in a separate bank account to be operated by the company for payment to the minority shareholders, for atleast 1 year for payment to the minority shareholders and such amount shall be disbursed to the entitled shareholders within sixty days and even thereafter by the company.

- Despatch of offer letter and consideration by the company

The offer letter received from the acquirer will be dispatched to the shareholders along with the consideration.

- Physical delivery of shares

Minority shareholders shall on receipt of offer letter, provide for physical delivery of their shares to the company within the offer period.

The point of relevance is that, the word used is “physical delivery of shares” and not physical share certificates. Accordingly, physical delivery would cover delivery of both, shares held in physical form as well as shares held in dematerialized form by minority shareholders.

- In case of shares held in physical form, physical delivery will be evidenced by receipt of share certificates by the Company;

- In case of shares held in dematerialized form, physical delivery will be evidenced by the receipt of Delivery Instruction Slips (DIS) in favor of the acquirer. Upon submission of DIS, the Depository Participant processes the DIS and debits the clients account with the said number of shares. Simultaneously, the target demat account is credited with the same number of shares.

7. Failure to tender physical delivery of shares

In the absence of a physical delivery of shares by the shareholders within the time specified by the company, such shares shall be taken as cancelled and the transferor company shall be authorized to issue shares in lieu of the cancelled shares and complete the transfer by following the applicable transfer provision and dispatching the amount paid by the acquirer in advance.

Impracticability to acquire minority shareholding held in dematerialized form

In order to ensure smooth implementation of acquisition of minority shareholding, the Act, 2013 empowers the company whose shares are being transferred to issue new shares in lieu of the undelivered shares within the time specified.

While in case of shares held in physical form, section 236(6) of the Act, 2013 is clear to state that share certificates shall deemed to be cancelled for non-receipt of physical delivery of shares and the company is authorized to issue new shares in lieu of cancelled share certificates, however, there is a difficulty in implementing the same in case of shares held in dematerialized form.

The law is silent on the procedure to be followed by the company for transferring the shares held by minority shareholders in dematerialized form, in the absence of receipt of DIS from minority shareholders. The Depositories, without any clear instructions from Ministry of Corporate Affairs (‘MCA’) or Securities Exchange Board of India (‘SEBI’), does not permit transfer of shares to the demat account of acquirer by virtue of DIS signed by the company on behalf of the minority shareholder.

Therefore, the intent of the law behind the enforcement of section 236 remains unfulfilled in case of shares held in dematerialized form as the company would not be able to give effect to the transfer in the absence of any definitive procedure laid out to give effect to the same.

MCA new rules on purchase of minority shareholding held in dematerialized form

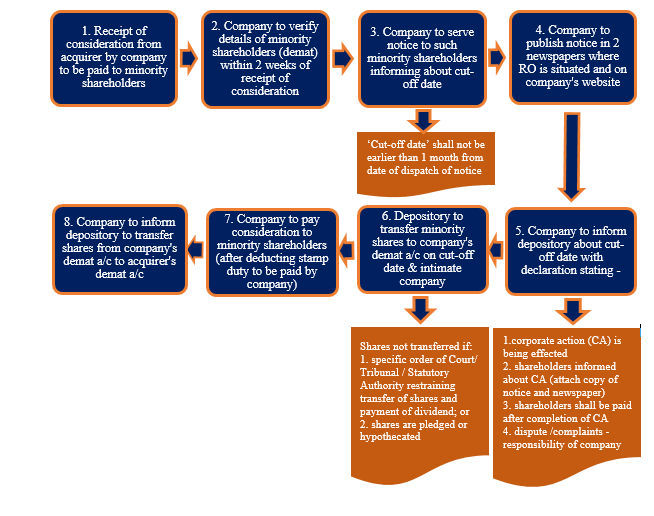

MCA has finally woken up to the need to enable companies to purchase minority shareholding held in demat form. The CAA Rules, 2016 has been amended vide MCA notification dated 17.12.2020 where a new Rule 26A has been introduced to provide process for purchase of minority shareholding held in demat form. The detailed step-by-step process highlighting the actionable for transferor company is explained below:

- Company to verify the details of minority shareholders holding shares in dematerialized form

The company shall within 2 weeks from the date of receipt of the amount equal to the price of shares to be acquired by the acquirer, verify the details of the minority shareholders holding shares in dematerialised form.

- Company to send notice to minority shareholders informing cut-off date

The company shall send notice to minority shareholders by registered post or by speed post or by courier or by email informing about a cut-off date on which the shares of minority shareholders shall be debited from their account and credited to the designated demat account of the company, unless the shares are credited in the account of the acquirer, as specified in such notice, before the cut-off date.

The cut-off date shall not be earlier than 1 month after the date of sending of the said notice. Also, if the cut-off date falls on a holiday, the next working day shall be deemed to be the cut-off date.

- Newspaper publication of notice served to minority shareholders

A copy of the notice served to the minority shareholders shall also be published simultaneously in two widely circulated newspapers (one in English and one in vernacular language) in the district in which the registered office of the company is situated and also be uploaded on the website of the company, if any.

- Company to inform depository about the cut-off date along with a list of declarations

Immediately after newspaper publication of notice, the company shall inform the depository w.r.t cut-off date and submit the following declarations stating that:

- The corporate action is being effected in pursuance of the provisions of section 236 of the Act;

- the minority shareholders whose shares are held in dematerialised form have been informed about the corporate action [a copy of the notice served to such shareholders and published in the newspapers to be attached];

- the minority shareholders shall be paid by the company immediately after completion of corporate action;

- any dispute or complaints arising out of such corporate action shall be the sole responsibility of the company.

For the purposes of effecting transfer of shares through corporate action, the Board of Directors of the company shall authorise the Company Secretary, or in his absence any other person, to inform the depository and to submit the documents as may be required.

- Depository to transfer the minority shares to company on the cut-off date

Except for the shares already credited in the account of the acquirer before the cut-off date by shareholders, the depository shall transfer of shares of the minority shareholders into the designated demat account of the company on the cut-off date and intimate the company.

Note: In case a specific order of Court or Tribunal, or statutory authority restraining any transfer of such shares and payment of dividend, or where such shares are pledged or hypothecated under the provisions of the Depositories Act, 1996, the depository shall not transfer the shares of the minority shareholders to the designated demat account of the company.

- Company to make payment to minority shareholders

The company shall immediately upon transfer of shares by the depository, disburse the price of the shares so transferred, to each of the minority shareholders after deducting the applicable stamp duty, which shall be paid by the company, on behalf of the minority shareholders, in accordance with the provisions of the Indian Stamp Act, 1899.

- Depository to transfer the minority shares from company’s demat account to acquirer’s demat account

One the payment is successfully disbursed to minority shareholders, the company shall inform the depository to transfer the shares of such shareholders, kept in the designated demat account of the company, to the demat account of the acquirer.

Note: The company shall continue to disburse payment to the entitled shareholders, where disbursement could not be made within the specified time, and transfer the shares to the demat account of acquirer after such disbursement.

A pictorial presentation giving step-by-step procedure to the above requirements is summarized below:

Concluding Remarks

The majority shareholders enjoy the right to squeeze out minority shareholders to gain control over the company in toto and attain a greater flexibility in decision making. While the process of acquisition of minority shares held in physical form is clearly established in the Act, 2013, however, companies were facing it practically difficult to implement in case minority shares are held in demat form. In the absence of any clear guidelines, squeezing out minority shareholders turned out as a challenge to implement.

The new rules notified by MCA are certainly a laudable solution facilitating the majority shareholders to smoothly acquire the shares held by minority shareholders in demat form.

Other reading materials on the similar topic:

- ‘Comparative Analysis of provisions enabling majority shareholders to squeeze out minorities’ can be viewed here

- ‘Minority Squeeze Out: A strong new provision under section 236 of the Companies Act, 2013’ can be viewed here

- ‘Takeover under Companies Act, 2013’ can be viewed here

- Presentation on ‘Minority-outs under Companies Act, 2013’ can be viewed here

Our Youtube Channel: https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

[1] H-ttp://www.nfcg.in/pdf/23-Irani%20committee%20report%20of%20the%20expert%20committee%20on%20Company%20law,2005.pdf

[2] http://egazette.nic.in/WriteReadData/2020/223774.pdf