Indicative List of Policies for NBFCs (Base and Middle layer)

Team Finserv | finserv@vinodkothari.com

Loading…

Loading…

Team Finserv | finserv@vinodkothari.com

Loading…

Dayita Kanodia | Finserv@vinodkothari.com

Trade receivables form an important part of working capital, and given the increasing trend toward the provision of buyers’ credit, occupying an ever-increasing part thereof. Traditionally, it is funded by usual modes of working capital funding. However, businesses have been searching for alternative modes of receivables financing.

Read more →ITAT Ruling Clarifies Taxation on Disproportionate Interest share in Loan Transfers

– Dayita Kanodia | Finserv@vinodkothari.com

Direct Assignment of a loan or transfer of loan exposures refers to the process where financial institutions, such as banks, purchase a pool of loans or assets from other entities, typically NBFCs, without the involvement of a third-party intermediary. In this arrangement, the buying institution directly acquires the ownership of the loans or assets and the associated rights, including the right to receive future payments from the borrowers. This method allows the selling NBFC to offload its loans, thereby freeing up capital, while the purchasing institution gains the opportunity to enhance its loan portfolio and earn interest income from the acquired loans. This Direct Assignment is essentially what is popularly known as the transfer of loan exposure.

The RBI issued the transfer of loan exposures directions in 2021 regulating all transactions among regulated entities involving transfer of loan exposures.

Pursuant to a transfer of loan, it is not necessary that the future interest income arising from the loans would be shared in the same proportion as that of the transfer. For instance, if an NBFC assigns 90% of the loan portfolio to a bank, there is no mandate that all interest income received in the future would be shared in the same proportion of 90:10. Generally, the borrower is not made aware of the transfer and therefore it is important that the NBFC continues to service the loan. In such cases it is only fair that the NBFC gets a higher proportion of interest. Accordingly, it is quite common in direct assignment transactions to have a disproportionate interest share.

The question which now arises is whether this excess interest income retained by the NBFC would be taxable under the provisions of the income tax act.

A recent ITAT ruling of May 7, 2024 clarifies the taxation treatment for disproportionate interest share in case of loan transfers. In this case, NBFC assigned 90% of the loan portfolio to a bank via the direct assignment route. However, the bank was not receiving the entire interest on the 90% loan assigned but was only entitled to a fixed percentage of share while the NBFC retained the excess interest. Accordingly, the revenue department was of the view that the assessee was responsible to deduct TDS on the excess interest allowed to be retained by the NBFC under section 194A of the Income Tax Act.

The revenue department further raised the question on deduction of TDS under SEction 194J and 194H of the Income Tax Act.

For the deciding the fate of the NBFC under section 194A of the Income Tax Act, the following was observed by the ITAT:

The next issue which was adjudicated in the case was whether the interest allowed to be retained with the NBFC was a consideration for rendering professional / technical services by the transferor NBFC to the transferee bank.

As per section 194J of the Act, any person, not being an individual or HUF, who is responsible for paying to a resident any sum, inter alia, by way of fees for professional services or fees for technical services shall at the time of credit of such sum to the account of payee deduct tax at source.

For this purpose the ITAT observed the following:

The last issue in this case to be decided before the ITAT was whether the retained interest would fall in the category of commission or brokerage and was liable to TDS under section 194H of the Income Tax Act.

As per section 194H of the Act, any person, not being an individual or HUF, who is responsible for paying to a resident, any income by way of commission or brokerage, shall at the time of credit of such income to the account of the payee deduct tax.

For determining the tax treatment under this section, the ITAT observed the following:

In conclusion, the recent ITAT ruling has provided significant clarity on the taxation treatment of disproportionate interest shares in loan transfers, particularly in the context of Direct Assignment transactions.

In this case, the ITAT emphasized that the interest retained by the NBFC was not a result of any money borrowed or debt incurred by the bank. Additionally, it was clarified that the interest retained did not constitute fees for professional or technical services rendered by the transferor NBFC, nor did it fall within the ambit of commission or brokerage.

As the financial landscape continues to evolve, such judicial pronouncements play a crucial role in fostering transparency, compliance, and fairness in taxation.

Vinod Kothari (finserv@vinodkothari.com)

The FinTech sector is booming and is a market disruptor as well as facilitator, based on the report published by Inc42, the estimated market opportunity in India fintech is around $2.1 Tn+ and currently there are 23 FinTech “unicorns” with combined valuation of $74 Bn+ and 34 FinTech “soonicorns” with combined valuation of $12.7Bn+.

The unprecedented growth of the fintech sector has transformed guarantees specifically First Loss Default Guarantees (FLDG) into a commonly employed tool for emerging players like fintechs. They leverage these guarantees to take exposures on loan transactions using low-cost funding from established entities such as large NBFCs and Banks. Fintechs issue guarantees that enable them to garner trust from prominent lenders, facilitating the origination of new loans through their digital platforms.

One of the crucial concerns in DLG arrangements is navigating the complexities surrounding capital treatment and NPA accounting covering both lenders and guarantors. In this article, we delve into an in-depth exploration of these crucial issues.

We organise this section into the following parts:

Capital requirement is linked with the credit risk on the exposure: hence, before getting into the regulatory prescription, let us examine what is impact on the credit risk of the lender. For capital rules, a guarantee is regarded as a case of credit risk mitigation, provided the guarantee satisfies several conditions (e.g., it should be explicit, enforceable, guarantor’s financial resources adequate, etc). The lender, on the basis of the guarantee, shifts the risk of the first (or subsequent, as may be the nature of the guarantee) layer of the losses to the guarantor. Thus, there is a substitution of risk from the borrowers in the pool to the guarantor. The remaining exposure remains unprotected – hence, to that extent, there is no credit risk transfer. Therefore, if the risk weight of the guarantor is lesser than the risk weight of the underlying pool, there was a case to expect a reduction in the capital requirements.

The regulatory prescription is as follows: DLG Guidelines states that for the purpose of capital computation, i.e., computation of exposure and application of Credit Risk Mitigation benefits on individual loan assets in the portfolio shall continue to be governed by the extant norms. The “extant norms” for this purpose would be the norms on credit risk mitigation. These norms are applicable in case of banks [see part 7 of the Basel III Master circular ] However, in case of NBFCs, there is no equivalent.

However, FLDG is expected to be backed by either a cash deposit, or a bank guarantee. If it is backed by cash deposit, cash is to be assigned 0 risk weight. Similarly, if it is backed by a bank guarantee, the risk shifts to the bank, and therefore, a 20% risk weight as applicable to banks may be assigned by the NBFC. Note that the above risk weights are only for the part backed by the guarantee. That is, if there is a 5% FLDG, the 5% of the loan pool will be risk weighted as above, and the remaining 95% will attract the risk weight applicable to the borrower pool.

When we talk about capital treatment, the same would depend on the capital rules applicable to the guarantor entity. If the guarantor entity is an RBI regulated lender, it will be covered by the capital rules. If the guarantor not a regulated lender, it is unlikely to have any capital rules.

We discussed above the nature of a structured default loss guarantee. A structured DLG (first loss, second loss, or subsequent loss) integrates the risk of a pool of loans and then strips the same into multiple tranches. Therefore, it becomes a case of structured risk transfer.

The generic rule in case of any structured risk transfer is that the acquirer of the first loss tranche acquires the risk of the entire pool. Therefore, a first loss default guarantor is required to keep capital on the pool size (and not the size of the guarantee). However, the size of the guarantee is the loss limit of the guarantor – therefore, the capital requirement, computed by applying the risk weight to the pool size, will be limited to the size of the guarantee. We discuss this further below.

First Loss

If the guarantee is first loss in nature, then, as the principle goes, the RE will have to maintain capital on the entire pool, since, it is exposed to all the risks associated with all loan accounts individually, subject to a ceiling on the the amount of guarantee it has provided.

For instance, if the guarantor provides a 5% FLDG for a pool of loans aggregating to Rs. 100 crores, and the regulatory capital requirement of the guarantor is 15%, then the capital required to be maintained against such pool is:

Lower of

= Rs. 5 crores.

As per the RBI FAQs, RE providing DLG shall deduct “the full amount of the DLG which is outstanding” from its capital. The above is in line with the RBI FAQs on the subject.

This prescription should be taken as applicable in case of first loss guarantees.

Further, the apparent question that arises here is in what proportion should the capital be reduced from Tier I and Tier II. In absence of any specifications in this regard in the regulations or the FAQs, it is only logical to deduct the capital from the Tier I and Tier II in their respective ratios. That is, if the Tier I is 10% and Tier II is 5%, then the capital reduction should also happen in the ratio of 2:1.

Second Loss

If the guarantee is second loss in nature, then, the losses will start piling up on the guarantor only once the first loss support is exhausted. Unlike the other case, here, the guarantor is not exposed to all the risks associated with all loan accounts individually. Therefore, the capital will have to be maintained on the amount of guarantee provided instead of the entire pool.

Using the same example, as used in the earlier case, the capital requirement for the RE will be:

Rs. 100 crores * 5% * 15% = Rs. 0.75 crores.

Of course, this is applicable only where the first loss guarantee is sufficient to absorb losses upto a level sufficient to absorb a certain multiple of “expected losses”. Usually, the multiple should be sufficient so as to render the second loss facility to achieve an investment grade rating.

Expected credit losses are for the potential for the loan or pool of loans to result in credit losses. If the lender has the benefit of first loss guarantee, the situation is that to the extent of the FLDG, the lender has exposure on the guarantor, and for the remaining pool size, the lender has exposure on the borrowers.

As regards a potential credit loss on the guaranteed amount, the RBI rules require the guarantee to be either fully backed by cash, or backed by a bank guarantee. Hence, the question of any credit loss on the same does not arise.

Hence, the lender will be exposed to losses only on so much of the expected credit losses as exceed the FLDG cover. For instance, if the FLDG is 5%, and the ECL estimated by the lender is 6.8%, the lender may create ECL provision only for 1.8%.

Note that ECL for any pool is a dynamic number – while estimations of the default probabilities and the exposure change over time, there are also changes due to unwinding of the discounting factor applied in computing present value of the ECL. Therefore, ECL estimation is bound to change every reporting period. For that matter, FLDG will remain fixed as 5% of the originated pool, but this number will also be dynamic as the loan pool matures – partly due to amortisation of the pool, and partly due to utilisation of the guarantee. Therefore, on an ongoing basis, the lender may compare the ECL with the percentage of FLDG still available, and create ECL for the differential amount.

If the guarantor is covered by ECL requirements, the guarantor needs to estimate the losses likely to be caused to the guarantor. As against the guarantee, the payoff of the guarantor may be (a) fixed guarantee fees (b) right to get a variable fee, usually linked with the excess spreads from the pool.

Note that ECL computation is required not only for loans, but also for financial guarantees. Therefore, the guarantor will need to compute the expected credit losses from the underlying loans using exactly the same basis as if the loans were on the books of the guarantor. Of course, the maximum ECL will be the limit of the guarantee.

In this regard, the RBI has clearly specified that no benefit will be given for provisioning requirements – that is, the regulatory provisioning will continue irrespective of the guarantee.

As regards the guarantor, while a financial guarantee is regarded as a direct credit substitute, however, there are no explicit provisioning requirements. To the extent the guarantee has already been utilised, it will be taken as a loss (even though recovery may happen subsequently, but it will be contingent).

Given that the recoveries are against an outstanding asset, receipts from DLG invocation should not be treated as income. The recoveries made from the accounts, for which the lender has already invoked DLG, in our view,should be recorded as a liability. This is because any recoveries from borrowers after receiving DLG payout would be liable to be remitted back to the DLG provider, and the lender will only hold it in trust. Hence creating a back to back obligation on the RE. It is important to note that, in general, a lender may not relinquish their legal right to recover a loan, even after the loan has been written off. Consequently, the obligation to pass on the recoveries from the borrower may also persist indefinitely.

To support this perspective, we suggest that the lender establish a timeline in agreement with the DLG provider. This timeline should specify the duration during which any recoveries from loans, for which DLG payouts were made, will be passed on to the DLG provider. After the specified period, the lender will no longer be obligated to transfer such recoveries. Consequently, upon completion of the agreed period, the RE can write off the liability associated with the credit protection payouts received.

Through the DLG Guidelines RBI has stated that the NPA classification would be the responsibility of the RE and would be as per the extant asset classification and provisioning norms irrespective of any DLG cover available at the portfolio level [para 7 of the DLG Guidelines]. The amount invoked by the DLG cannot be set off against the underlying individual loans and thus, asset classification and provisioning would not be affected by any DLG cover. However, any future recovery by the RE from the loans on which the DLG cover was invoked and realised can be shared with the DLG provider in terms of their contractual arrangements.

Accounting-wise, if the amount has been recovered, it is set off from the outstanding pool However, there is a departure here between accounting treatment and the NPA/capital requirements, as the RBI expects the NPA recognition to be continued in the books of the lender.

Similarly, capital requirements will also remain unaffected. However, it will be wrong to show the amount recovered from the guarantor as a liability as it is not a liability – though there may be an understanding that any recovery from the loans will be paid back to the guarantor. It is also wrong to treat the amount received from the guarantor as income, as the payment consists of both interest and principal.

It shall be noted that despite the FLDG being invoked against the borrowers outstanding amount, the capital requirements and asset classification remain unaffected. Further, reporting to CIC and NESL pertains to the borrowers performance, and therefore, the invocation of FLDG shall not influence these reporting. Repayment as well as defaults of the borrower should continue to be reported without any impact from FLDG invocation. Therefore, the borrowes account will continue to be classified as NPA and reported accordingly to the CIC and other relevant reporting entities.

Related Articles –

FAQs on Default Loss Guarantee in Digital Lending

Lend, Recover, Replenish: A guide to revolving lines of credit

An examination of the RBI Guidance Note on Operational Risk Management and Resilience

Subhojit Shome & Archisman Bhattacharjee | finserv@vinodkothari.com

Loading…

Related articles –

The who’s who of structured finance is joining the 12th edition of our flagship event, the Securitisation Summit on May 15, 2024, in Mumbai. Be shoulder-to-shoulder with leading originators, investors, lawyers, rating agencies, consultants, regulators, mediators, market makers, and everyone else who matters.

For details of the event and to book your seat, please visit our Summit page – HERE

Lenders asked to mend ways immediately

Team Finserv | finserv@vinodkothari.com

If fairness lies in the eyes of the beholder, the RBI’s eye is getting increasingly customer-centric. This fiscal year, the RBI has issued circulars aimed at fostering fairness and transparency in lending practices; these come at the backdrop of circulars last year on penal interest, adjustable rates of interest, release of security interests, strengthening customer service by Credit Information Companies and Credit Institutions, and establishing a framework for compensating customers for delayed updation or rectification of credit information. Recently on April 15, 2024, the RBI introduced a circular on Key Facts Statement (KFS) for Loans & Advances, with the goal of enhancing transparency and reducing information asymmetry regarding financial products offered by various regulated entities. This initiative aims to empower borrowers to make well-informed financial decisions.

A new Circular, dated 29th April 2024 Fair Practices Code for Lenders – Charging of Interest comes down on some of the practices related to computation of rates of interest by lenders. . This Circular is all about stopping lenders from doing things that aren’t fair when it comes to charging interest.

The Circular applies to a wide range of financial institutions including Banks, Co-operative Banks, NBFCs, and HFCs. It is worth noting that this Circular comes into effect immediately upon its issuance.

| Practices observed | Regulatory stipulation |

| Lenders charge interest from the date of execution of the loan, or the date of sanction, even though disbursement has not taken place as yet | Interest may be charged only from the date of disbursement |

| Interest is charged from a particular date, even though it is clear that the cheque was handed over to the borrower several days after the said date | Interest may be charged from the date when the cheque is handed over to the borrower |

| In some cases, one or more EMIs were received in advance; however, the interest was computed on the loan amount, without considering the advance payment | Interest shall be charged after netting off the advance EMI from the disbursement amount |

Manisha Ghosh l manisha.ghosh@vinodkothari.com

In a move aimed at fostering transparency and consumer-centric practices in digital lending, the Reserve Bank of India (RBI) issued draft guidelines for digital loan aggregators on 26th April, 2024 titled ‘Digital Lending – Transparency in Aggregation of Loan Products from Multiple Lenders’. Comments are due on the same. This regulatory framework underscores the importance of empowering borrowers with complete information during the credit process to make an informed decision.

Read more →-Vinod Kothari and Anita Baid | finserv@vinodkothari.com

Loading…

Our related resources on the topic:

All-inclusive APR disclosure; third-party payments also included; no lender-induced changes during the validity period of KFS

-Team Finserv | finserv@vinodkothari.com

(Updated as on May 1, 2024)

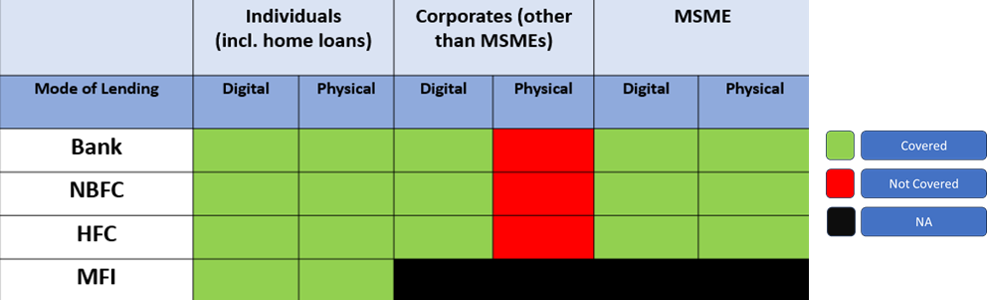

The RBI vide its Statement on Developmental and Regulatory Policies dated February 08, 2024 announced its decision to mandate Regulated Entities (REs) to provide Key Fact Statement (KFS) for retail and Micro, Small & Medium Enterprise (MSME) loans.

Following the aforesaid, RBI issued a notification dated April 15, 2024 (Circular) to “harmonise” the instructions in this regard for all REs.

Since the intent of the RBI is to harmonise similar requirements, the KFS Circular overrides similar extant requirements in case of lending by banks to individuals, and digital lending.

Contents

| Meaning and Intent |

| Scope and Applicability |

| Contents of KFS |

| Meaning of Retail Lending |

| Meaning of MSME Lending |

| Validity period and Cooling off period |

| Annualised Percentage Rate |

| Other Requirements |

1. What is KFS?

2. How will KFS help transparency?

The intent is to have simple transparent, and comparable (STC) terms of the loan communicated to the customer upfront. The standardised format provides is simple and concise and has all the necessary details of the loan – annual percentage rate, fees, recovery mechanism, and associated risks in a straightforward format.

3. Has the format of KFS and other disclosures been prescribed?

Yes, the format for KFS has been prescribed in Annex A of the Circular. Further, formats for computation of APR and amortization schedule to be given to the borrower has also been prescribed in Annex B and C of the Circular respectively.

4. Which all entities are covered by the new requirement?

The following entities will be covered under the scope of the Circular –

5. In what kind of loans will KFS be mandatorily applicable?

Coverage of the Circular

6. Will the KFS norms be applicable on Housing Loans as well?

In case of housing loans extended by HFCs, sharing of most important terms and conditions (MITC) are applicable (Para 85.8 read with Annex XII of the HFC Master Directions). MITC is akin to KFS, however, the format of KFS is more focused on interest rate and other charges as well as a few qualitative terms of the loan, whereas MITC provides several other relevant details.

The Circular is addressed to HFCs as well. Further, meaning of “retail lending” (see below) includes home loans as well. In the absence of any other clarification, we would advise lenders to prepare MITC as well as KFS in case of home loans.

6A. Whether the Circular has to be complied with in case any loan is advanced to MSMEs?

The Circular is applicable in case of all retail and MSME term loan products extended by all REs. However, in our view if the RE doesn’t distinguish between MSME and other categories of borrowers for the same loan product, then there is no requirement to provide KFS only to MSME borrowers. In this case, the lender should also not avail the benefit of any guarantee scheme provided in case of MSME lending.

The Circular in our view only seems to apply in case the RE has a separate MSME loan product.

7. What happens to the existing circulars on Digital Lending and Microfinance Lending?

The existing provisions for KFS and APR in the Digital Lending Guidelines, MFI Directions and Display of Information by Banks circular shall stand repealed.

8. When does the new requirement become applicable?

The Circular is applicable with effect from October 1, 2024 to all new retail and MSME term loans sanctioned. Further, digital loans, MFI loans and bank finance extended to individuals post the said applicability date would also require to be aligned with the new requirement.

It would, therefore, appear that extant requirements continue to apply from now until 30th September.

It would actually be better for lenders to transition into the new requirement before 1st October, at least on a parallel basis – this will serve as a dry run upto the new requirement from 1st October.

9. In case of banks, what is the applicability of this Circular?

The KFS Circular applies to banks for (a) all loans to individuals, as covered by Display of information by banks; (b) any loans to MSMEs; (c) any microfinance loans; (d) any digital loans.

10. Whether loans under digital lending need to comply with the Circular or will they continue to follow extant guidelines?

The Circular applies to digital loans as well. In fact, it repeals Para 5.1 and 5.2 of the digital lending guidelines dealing with APR and KFS provisions. However, until October 1, 2024, the existing guidelines may continue to be followed.

11. In case of co-lending transactions, is the compliance on the originating co-lender or the funding co-lender?

While specific details of co-lending arrangements are required to be shared with the borrower; the borrower interface is typically done by the originating co-lender. Hence, the originating co-lender should be making the requisite disclosures. Funding co-lenders may ensure that the originating co-lender is making the requisite disclosures.

12. What are the contents/format of KFS?

13. KFS is intended to be a “standardised format”. What is the significance of the format being standardised? Does the lender have the discretion to add/delete fields?

The Circular prescribes for a “standardised format” for KFS. The intent behind this standardisation is to enhance transparency and to facilitate the comparability of the loan terms offered by different lenders. The RBI refers to the KFS as a “standardised format”. Therefore, in our view, the comparability of the KFS will be compromised if it was loaded with new details or subjectivities not envisaged in the standard format.

14.Can the lender, for instance, add clauses like “this is not a sanction letter; the grant of the loan is eventually subject to sanction by the lender’s internal credit committee”, or similar conditionalities?

It is important to note that the format of the KFS is standardised. Therefore, the KFS is expected to remain limited to the fields given in the standardised format. However, the KFS may be an annexure to a sanction letter – see below.

15. Is the present practice of issuing sanction letter redundant? Can a lender issue a sanction letter in addition to KFS?

The KFS is a summarised version of the terms of the loan. However, the grant of the loan itself may have several conditions, typically comprised in the sanction letter. The RBI’s Fair Practices Code refers to a sanction letter – NBFCs shall convey in writing to the borrower in the vernacular language as understood by the borrower by means of sanction letter or otherwise, the amount of loan sanctioned along with the terms and conditions including annualised rate of interest

Hence, first, the sanction letter does not become redundant. Secondly, if there are conditionalities or compliances relating to the loan, the same may be contained in the sanction letter. For example, the borrower may be required to complete some conditions precedent. There are normally several conditions subsequently, commonly called “post-disbursement conditions”. Each of these may be contained in the sanction letter.

15A. The charges mentioned in KFS are an amount X. The KFS also says this amount can be varied by the company. Can the variation of this amount in future be done without the borrower’s consent?

Charges mentioned in KFS may relate to charges payable at the time of the taking the loan, charges over the term of the loan, and may include contingent charges too. Para 8 of the Circular also says that whatever is not disclosed cannot be charged without the explicit of the borrower.

Therefore,

(a) there is no question of charging something that is not a part of the KFS, without the borrowers’ explicit consent.

(b) as for amounts already disclosed, while the company would have reserved the right to vary, however, in our view, these charges cannot be varied as this would disrupt the comparability and standardisation of the KFS.

15B. The KFS circular applies from 1st October 2024 – can the company impose charges not already a part of the loan agreement and make them applicable before 1st October?

Since the KFS circular is coming with the perspective of fairness in practices, and given the fact that the prospective applicability date is merely to allow companies time to adhere to and transition to the new paradigm, the move as proposed will be seen as a way to take undue advantage of the applicability date.

16. Does the issuance of a KFS amount to a binding commitment on the part of the lender to lend?

The language of Explanation below clause 5 of the KFS Circular may give such an impression. It says: “Validity period refers to the period available to the borrower, after being provided the KFS by the RE, to agree to the terms of the loan. The RE shall be bound by the terms of the loan indicated in the KFS, if agreed to by the borrower during the validity period.”

However, in our view, the KFS is only the terms of the loan. The binding force of the KFS during the “validity period” is only on the terms, and not on the grant of the loan itself. If the conditions precedent for availing the loan have been satisfied, the lender will be bound by the terms as contained in the KFS; however, the grant of the loan itself is based on conditions precedent may still form part of the sanction letter.

17. Is it permissible for REs to include additional terms in the KFS alongside those outlined in the standardized format?

The purpose of requiring a standardized KFS for borrowers is to guarantee consistency in loan terms across different lenders, enabling borrowers to make fair comparisons. Therefore, we believe that REs should avoid subjectivity and strictly follow the standardized format outlined in the notification.

18. Can REs charge fees/charges not mentioned in the KFS?

The answer to this is positive as REs can charge fees/charges not mentioned in the KFS with the explicit consent of the borrower.

19. What are Equated Periodic Installments and how are they computed?

Equated Periodic Installment (EPI) refers to a fixed amount comprising both principal and interest repayments that a borrower must pay at regular intervals over a predetermined number of periods to repay a loan fully. These payments ensure the gradual amortization of the loan. When these installments are made on a monthly basis, they are commonly known as Equated Monthly Instalments (EMIs).

20. What is the meaning of retail loans?

Further, it may be noted that credit card receivables, though extended to individuals, are excluded from the purview of the Circular.

21. Give some examples of loans which are not retail lending?

Some examples of loans not considered as retail lending are –

22. What is lending to MSMEs?

Loans to entities satisfying the following conditions and holding Udyam registration as MSMEs:

| Investment in Plant & Machinery or Equipment | Turnover | |

| Micro Enterprise | Upto 1 crore | Upto 5 crore |

| Small Enterprise | Upto 10 crore | Upto 50 crore |

| Medium Enterprise | Upto 50 crore | Upto 250 crore |

23. Are all loans to MSMEs covered under the scope of the Circular?

The Circular explicitly states its applicability solely to “MSME Term Loans”. Therefore, we understand that working capital loans or lines of credit extended by REs to MSMEs fall outside the scope of the Circular.

24. What is a Validity Period?

The validity period refers to the timeframe within which the borrower, upon receiving the KFS from the RE, can agree to the loan terms. In case the borrower accepts the terms outlined in the KFS during this validity period, the RE is bound by these terms as indicated in the statement.

25. How long should the Validity Period be?

In terms of the notification, the KFS must possess a validity period of a minimum of three working days for loans with a tenor of seven days or more, and one working day for loans with a tenor of less than seven days.

26. What if the customer does not accept the terms during the validity period?

The RE is only bound by the terms mentioned in the KFS if the same is accepted by the borrower during the validity period. Accordingly, if the borrower fails to accept the KFS terms during the validity period, the RE reserves the right to change the terms after the end of such period.

27. Where will the validity period be disclosed?

Going by the standardised format for KFS provided by RBI, there is no requirement to mention the validity period in the KFS. However, to ensure that the borrower is aware of the same, the validity period can be mentioned in the covering note or sanction letter.

28. What will be considered a Working Day?

Working days would mean Monday to Friday of the week excluding public holidays.

29. What is the difference between the validity period and cooling off period in case of digital loans?

| Validity Period | Cooling off Period |

| Applicable for digital as well as physical loans. | Applicable only for digital loans. |

| Pre-disbursement phase | Post-disbursement phase |

| Provided to the borrower to accept the terms of the loan as indicated in the KFS | Provided to the borrower for exiting digital loans without any pre-payment penalty in case a borrower decides not to continue with the loan. |

| The RE is bound by the terms of the loan if accepted by the borrower during the validity period. | Grants the borrower the right to repay the principal and the proportionate APR during this period. |

30. Is it necessary to provide a validity period to borrowers before approving top-up loans, even if the terms of the top-up loan are identical to those of the existing loan?

Yes, the notification is applicable from October 01, 2024. Accordingly, after this date, KFS should be provided for all top-up loans. Subsequently, following this date, KFS should be furnished for all top-up loans. As a result, borrowers must also be provided with a validity period to accept the terms of the top-up loan.

31. What is APR?

Annual Percentage Rate (APR) is the annual cost of credit to the borrower that includes interest rate and all other charges associated with the loan.

32. What are the components of APR?

The following are the components of APR –

Excluding

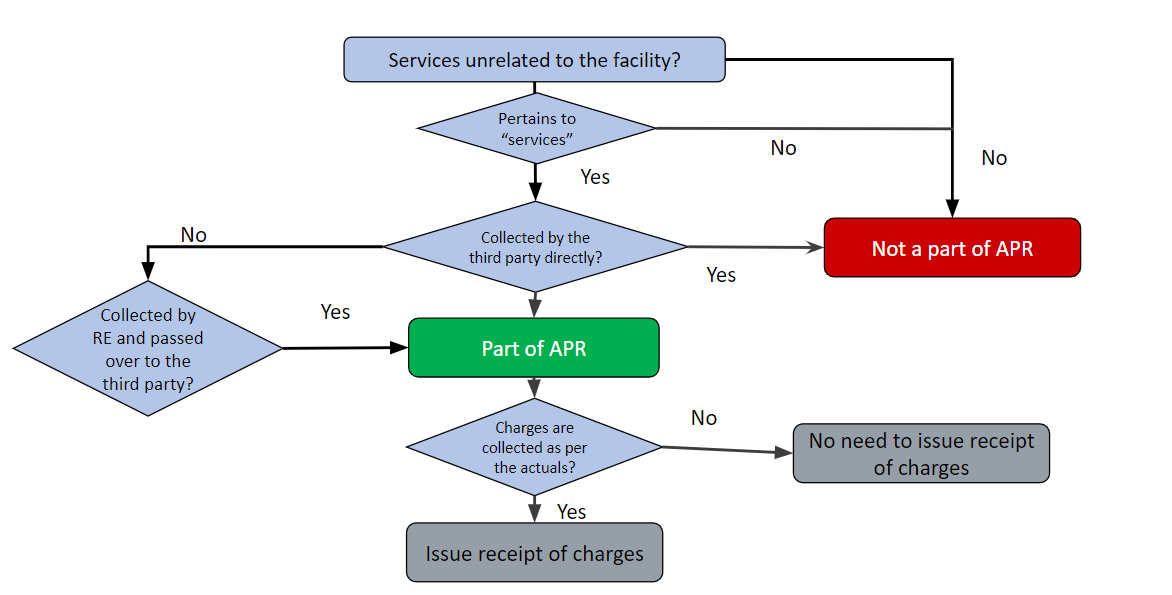

33. Are charges recovered on behalf of third party also a part of the lender’s APR?

Yes, the charges that borrowers pay to the RE, which are passed on to third-party service providers based on actual expenses, like insurance or legal charges, will also be included in the calculation of APR. See the discussion below.

33A. What is the meaning of the expression “service providers”? Can statutory charges such as stamp duty etc also be a part of APR?

The Circular uses the following language: “Charges recovered from the borrowers by the REs on behalf of third-party service providers on actual basis, such as insurance charges, legal charges etc., shall also form part of the APR and shall be disclosed separately.” In our view, the expression “service providers” has been used consciously, to refer to some entities providing services either in relation to the loan, or the subject matter of the loan.

Stamp duty is a statutory charge and is in the nature of a tax/duty payable to the statutory authorities. It cannot be contended that the state is providing any specific service either in relation to the loan or the subject matter of the loan. Hence, in our view, it is only the charges payable in respect of services, recovered by the lender, which should be forming part of the APR.

34. Should charges not directly linked/integrated with the loan, also form part of the APR? Will the answer remain the same even if such charges are deducted from the disbursement amount ?

As regards the inclusion of charges within APR, the essential basis should be the definition of APR, defining it as “the annual cost of credit to the borrower which includes interest rate and all other charges associated with the credit facility”. Therefore, a lender providing a credit facility imposes charges, in addition to interest, by whatever name called, including for third party services which are related to the credit facility or the subject matter of the credit facility, should be forming part of the APR. This will, of course, not include contingent charges such as delinquency penalties, repossession charges, etc.

The charges imposed by lenders may, illustratively, be as follows:

The charges for third-party services, which are typically related to the loan or the subject matter of the loan may be as follows:

The mode of collection of these charges does not matter – that is, these may be charged separately, or may be deducted from the disbursement.

35 .Whether statutory dues would form part of APR?

See answer above.

36. If, for instance, the borrower is required to place a security deposit/cash collateral, which is free of interest, is the impact of the same also captured in the APR?

While the placing of the security deposit may impact the overall cost of the borrower, but in our view, it is inappropriate to incorporate this cashflow as a part of the loan cashflows.This is because in our view the positive and negative cash flows arising out of the loan payments and security deposit, respectively, should not be co-mingled.

37. In case of loans for vehicles, it is common practice to require the borrower to make a down payment to the supplier. Is the same also captured in the APR?

The APR is computed on the loan amount; down payment is not a part of the loan.

37A In which all cases insurance charges paid to the third party will form a part of the APR ?

We take some illustrative situations below:

37B If cash flows are not at uniform period of time, how will the APR be calculated?

If cash flows are not at uniform periods of time, lenders generally use the XIRR method to calculate interest. Note that IRR formula fails to capture non-equidistant cashflows. However, XIRR is annually compounded rate. It may be converted into a monthly rate by using “nominal” formula, or de-compounding from a year to a month, and then multiplying the result by 12. It should be noted that XIRR is generally greater than APR.

37C In case of a demand loan, will the APR be computed based on the sanctioned amount or on the disbursed amount?

For demand loans, the APR should be calculated based on the sanctioned amount. This reflects the potential maximum cost of credit to the borrower if the borrower chooses to utilize the entire sanctioned amount.

38. Lenders quite often get payouts or subvention from third parties, say vendor, OEM, insurance companies, etc., which supplement the returns of the lender. Are these also disclosed as a part of the APR?

In our view, there is no reason to include payouts by third parties, that is, other than the borrower, as a part of the borrower’s cost of credit.

Having said this, if there are discounts/subventions being given by a vendor, the lender should make a fair disclosure of the discount, showing the same as a deduction from his cost of interest.

Graphical illustration summarising APR

39. What are the disclosure requirements?

Following additional disclosures are to be made by the REs along with KFS –

40. What are the other requirements as per the Circular?

As per the Circular REs are obligated to do the following –

41. In case of digital loans how will RE be able to explain the contents of KFS to the borrower?

For digital loans, REs may have the option to exhibit a pre-recorded video within their application or present a document that elucidates the contents of the KFS.

42. What will be the impact of this circular in existing loans?

REs will not be required to issue KFS in existing loans. However, compliance with this circular will be required for any new loan or top-up loan provided to existing customers.

43. Para 7 of the Circular provides that charges recovered from the borrowers by the REs on behalf of third-party service providers on actual basis shall also form part of the APR and has to be disclosed separately. So does this imply that any amount over and above the actuals will not form a part of APR?

In case the RE is collecting charges that are over and above the actuals, the same is int he form of charges levied by the RE itself and by default should always be included in the APR computation. However, in case of collection of charges on actuals on behalf third-party service provider, the RE shall be required to provide receipt and related documents will have to be provided to the borrower, within a reasonable time.

44. The KFS also needs to disclose the phone number and email id of the grievance redressal officer. So, will it be sufficient compliance with the regulations if a generic email id of the grievance redressal cell is provided ?

As per the KFS format provided, a generic email id and phone number can be provided by the RE in the KFS subject to the customer complaints being redressed within one working day.

45. The KFS must reveal whether the loan is currently or potentially subject to transfer to another RE entity or securitization. Therefore, if an RE fails to disclose this information while providing the KFS to the borrower, does it mean the RE is barred from transferring or securitizing the loan?

In case, the RE has revealed its intention to not transfer/securitise the loan but subsequently after disbursal intends to transfer/securitise the loan, it has to obtain the borrowers approval.

46. The Circular has prescribed that if the charges/fee payable cannot be determined prior to sanction, an upper ceiling may be prescribed by the RE. How will this upper ceiling be determined by the RE ?

The upper ceiling should be mentioned by the REs considering the maximum amount of charges that can be levied.

47. The Circular also extends to all HFCs. Henceforth, do HFCs solely need to furnish the KFS, or is there still an obligation to supply the MITC to borrowers as per the HFC directions?

The HFC directions require MITC to be provided to all borrowers for home loans. Additionally, the relevant provision of the HFC directions that mandates MITC provision has not been repealed. Therefore, until further regulatory clarity is provided on the subject, HFCs are obligated to furnish both MITC and KFS to borrowers.

48. What are the actionables for REs?

The immediate actionables for an RE shall be as follows:

49. Is there a requirement to issue a new KFS at the time part pre-payment or restructuring?

In the case of pre-payment of loan, pre-payment charges, if any should be disclosed to the borrower in the KFS under contingent charges which do not form a part of the APR. Subsequently, if there is pre-payment or part pre-payment by the borrower there is no need to issue new KFS, APR or repayment schedule since the pre-payment happens at the option of the borrower.

The intention of the Circular is to promote standardisation and comparability of loan terms. In the case of restructuring, the terms pursuant to such restructuring are borrower specific and therefore not comparable. Accordingly, we do not see a need to again provide a new KFS.

The KFS has to be provided again at the time of levy of additional charges not mentioned in the original KFS.

Our other resources on the topic are:-

Watch our Webinar on the topic here:

– Team Finserv | finserv@vinodkothari.com

The Reserve Bank of India on 19th December 2023 issued a notification[1] imposing a bar on all regulated entities[2] (REs) with respect to their investments in AIFs. We had covered the same in our earlier write-up. The Circular has already created some bloodshed as several banks took a hit in their Q3 results. Though late, yet welcome, the RBI has now come with some relief by a March 27 2023 circular. The following Highlights are based on the original circular, as amended by the March 27th circular :-

Direct or indirect investments:

Investments through mutual funds and FOFs exempt:

Priority distribution model or structured AIFs

In our view, there is a need to review the regulatory mechanism for AIFs, as currently, AIFs are being used as instruments of regulatory arbitrage.

[1] https://rbi.org.in/Scripts/NotificationUser.aspx?Id=12572&Mode=0

[2] Commercial Banks (including Small Finance Banks, Local Area Banks and Regional Rural Banks), Primary (Urban) Co-operative Banks/State Co-operative Banks/ Central Co-operative Banks, All-India Financial Institutions, Non-Banking Financial Companies (including Housing Finance Companies)

Other articles related to the topic: