– Pammy Jaiswal and Payal Agarwal | corplaw@vinodkothari.com

Pursuant to SEBI (Prohibition of Insider Trading) Amendment Regulations, 2025, SEBI has amended UPSI definition, effective from June 10, 2025 inserting a longer list of information, some of which may seem purely operational or business-as-usual for listed companies. Several questions arise: Whether each of this information will be regarded as “deemed UPSI”, thereby requiring compliance officers to do the drill of structured digital database entry to even trading window closure every time such an event occurs? What are the immediate actionables on the company? Whether the list of UPSI gets restricted only to the prescribed events or has to be tested for price sensitivity?

In this video, Ms. Pammy Jaiswal and Ms. Payal Agarwal discuss and analyse the scope of amendments, what it means for listed entities and the actionables that follow:

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-07 15:41:402025-06-07 15:49:46Upsurge in list of UPSI | SEBI (Prohibition of Insider Trading) (Amendment) Regulations, 2025

Loan write-offs in case of banks has been a consistent practice, and has been sharply criticized in several forums. Loan write-offs constitute a significant amount: Between FY 2015 and FY 2024, Scheduled commercial banks wrote off loans worth ₹12.3 lakh crore, with a ₹9.9 lakh crore written off in just the last five years (FY 2020 to FY 2024).

Year

Amount (in INR Crore)

2023-24

1,70,270

2022-23

2,08,037

2021-22

1,74,966

2020-21

2,02,781

2019-20

2,34,170

Total

9,90,224

Table 1: Loan write-offs by banks in the last 5 years (FY 20 – 24)

On the other hand, global supervisors and developmental bodies have always advocated a sound loan write-off policy for uncollectable loans. In its 2014 paper, IMF says:

“Banking supervisors should have a general policy requiring timely write-off of uncollectible loans and assist banks in formulating sound write-off criteria. The benefits of timely write-offs of uncollectible loans are numerous … A bank should write off a loan or portion of a loan when it is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted. This does not have to be preceded by exhausting all legal means and giving up contractual rights on cash flows. This also does not mean that the loan has absolutely no recovery or salvage value, but rather that it is not practical or desirable to defer writing off this essentially worthless asset even though partial recovery may be realized in the future.”

The IMF paper also discusses the potential downside of the write-off – that the reported NPLs would be lower, however, it argues that the write-off gives a better picture of the provision coverage.

European regulators have also extensively recommended loan-write off policy. In a 2017 paper1, European Central Bank says:

“An entity should write off a financial asset or part of a financial asset in the period in which the loan or part of the loan is considered unrecoverable. For the avoidance of doubt, a write-off can take place before legal actions against the borrower to recover the debt have been concluded in full. A write-off does not involve the bank forfeiting the legal right to recover the debt; a bank’s decision to forfeit the legal claim on the debt is called “debt forgiveness”.

The World Bank in a 2019 paper2 has, likewise, given several benefits of a write-off as compared with provisioning:

“An ambitious NPL write-off policy provides several benefits for banks and the financial system.

Firstly, by resolving NPLs banks can focus on core business (i.e., financial intermediation) in terms of time and resources. By efficiently dealing with NPLs, including writing off, the bank can allocate its productive resources to new lending, instead of becoming an asset management company of “bad assets”.

Secondly, while the main aim is the liquidation of assets with low recovery prospects, the consequence of an NPL write-off typically is a decrease of the NPL ratio in banks. Country experience shows that this is a particularly efficient way to decrease the NPL ratio quickly …

Thirdly, there are no negative effects on financial statements, provided that loans are already fully provisioned and losses already recorded in the P&L statements. Fourthly, a decrease in NPL ratio should improve a ratings agency assessment of credit risks in the bank or in the financial system.”

IFRS 9 (Indian version Ind AS 109) specifically permits write-off, though its precursor, IAS 39 did not have a specific provision.

Originally, write-off in India seems to have been inspired by tax considerations, as a mere provisioning qualifies for a conditional and limited tax deduction under sec. 43D of the Income-tax Act. On the contrary, write-off as a bad debt can be fully claimed. Therefore, as back as in 2009, the RBI advised:

“Therefore, the banks should either make full provision as per the guidelines or write-off such advances and claim such tax benefits as are applicable, by evolving appropriate methodology in consultation with their auditors/tax consultants. Recoveries made in such accounts should be offered for tax purposes as per the rules.”

Similar paras appear in the Prudential circular of 2007 and 2008 too.

What is the genesis of the word “technical write-off”? Is it coming from global jurisdictions? It does not seem so. As per our research, the 2009 circular of the RBI (cited above) permitted banks to write off advances at HO level, even though they are outstanding at the branch level [this, in present day parlance would mean, write-off in books of account, though still outstanding in the customer’s MIS LAN).

The RBI stated:

“Banks may write-off advances at Head Office level, even though the relative advances are still outstanding in the branch books. However, it is necessary that provision is made as per the classification accorded to the respective accounts. In other words, if an advance is a loss asset, 100 percent provision will have to be made therefor.”

This write-off, done at HO level but not at branch level, has been referred to as prudential or technical write off, that is written-off technically, but not written-off really. In the forms appended to Master Circulars of 2011 onwards, the word “technical write off” appears with the meaning referring to advances which are written off at HO level.

FAQs on Write off

Below are some of the pertinent questions on write-offs:

Para 4.1.3 of the IRACP Circular defines a loss asset as follows:

“A loss asset is one where loss has been identified by the bank or internal or external auditors or the RBI inspection, but the amount has not been written off wholly. In other words, such an asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted although there may be some salvage or recovery value.”

This loss asset has been placed as a category under NPAs.

The Technical Write-off Framework states:

“Technical write-off for this purpose shall refer to cases where the non-performing assets remain outstanding at borrowers’ loan account level, but are written-off (fully or partially) by the RE only for accounting purposes, without involving any waiver of claims against the borrower, and without prejudice to the recovery of the same.”

The Prudential Circular provides that loss assets are either to be written off, or to be fully provided for. On the other hand, the Compromise Framework clearly refers to full or partial write off.

The intent of the two is the same – to write down what is worthless. However, the Prudential Circular is referring to the degradation of an NPA – from substandard, to doubtful, to loss, where it comes to a stage where there is a trivial recovery value. The end result is the same – the first one is a mandatory prudential requirement; under the Technical Write-off Framework, accounting write-off is purely optional.

Can a lender do a partial write off? Or write off means the entire amount due from the borrower needs to be written off?

Response:

Very clearly, the technical Write-Off Framework provides the option for a partial write-off. Further, in terms of para 5.4.4 of Ind As 109

“An entity shall directly reduce the gross carrying amount of a financial asset when the entity has no reasonable expectations of recovering a financial asset in its entirety or a portion thereof. A write-off constitutes a derecognition event [see paragraph B3.2.16(r)].“

Further, para B3.2.16(r) provides that,

“The following examples illustrate the application of the derecognition principles of this Standard- (r) Write-off. An entity has no reasonable expectations of recovering the contractual cash flows on a financial asset in its entirety or a portion thereof.“

Therefore, accounting norms also allow for partial write offs and to the extent the loan has been written off, the lender can derecognise the loan asset from their books.

What is the approach towards write off? In case of secured loans, and in case of unsecured loans?

Response:

The key to determination of write-off is the extent of recovery in an impaired loan. That is, what is considered not recoverable is written off. So, the task is to recognise (a) an impaired loan; (b) make a fair estimate of recoverable amounts from the loan; (c) apply a suitable discounting factor; and thus, find the fair value of the loan. The difference between the POS and such fair value becomes the amount of the write-off.

In case of secured loans, the focus is on the value of the collateral, the haircut on its valuation due to sale of repossessed collateral, legal expenses and costs on recovery, the time taken, etc.

What is the stage of write off – only when the asset turns an NPA or can the write off be done before it is recognised as NPA?

Response:

The Technical Write-off Framework refers to technical write off in case of NPAs. The IRACP Circular (applicable upon Banks) also refers to a loss asset as a sub-category of NPAs. However, under the SBR Directions (relevant for NBFCs), loss asset is not a sub-category of NPA but is defined as a separate asset class:

(i) an asset which has been identified as loss asset by the NBFC or its internal or external

auditor or by the Reserve Bank during the inspection of the applicable NBFC, to the extent it is not written off by the applicable NBFC; and

(ii) an asset which is adversely affected by a potential threat of non-recoverability due to

either erosion in the value of security or non-availability of security or due to any fraudulent act or omission on the part of the borrower.

That, however, does not imply that a lender cannot have a policy of recognition of impairment before an asset turns NPA. This will depend on the nature of the asset. For example, in case of personal loans, if a lender recognises a loan as impaired after 60 DPD, the lender may do a write off. Of course, there is no justification to do a write off if the loan is not considered impaired, on the basis of the parameters that may be applicable to the said loan.

There are two facilities to a borrower – can one be written off while the other one continues? What will be the basis for the same?

Response:

Yes. It is possible that one loan is backed by a tangible collateral, say, home loan or gold loan, while the other loan is unsecured. While the borrower may default on the unsecured loan, he may be maintaining performance on the secured loan, in order not to lose the collateral. If the value of the collateral, on the basis of principles discussed above, is good, it is possible to conclude that no write-off is required in case of the secured loan, while write-off may be done in case of the unsecured one.

If one facility to a borrower is written off, can the other continuing facility, which is not in default, be treated as performing/standard?

Response:

Even though one loan (having a DPD status of 90+ days) is written off, the borrower’s liability to pay and the lender’s right to recover continue. The borrower is a defaulter. NPA classification is based on borrower, and not on facility. Hence, the other facility will remain NPA.

After write-off, can the lender give a fresh loan to the borrower?

Response:

We find it quite difficult to justify giving a fresh credit facility to a borrower who caused a write-off. However, para 12 of the Technical Write-off Framework allows giving of new loans to a borrower whose account has been written off after a minimum cooling period decided in accordance with the lender’s Board-approved policy.

In case a borrower has been written off by a particular lender, can another lender extend a fresh loan to such borrower? Would the cooling period provision be applicable in such a scenario?

Response:

The response to this seems affirmative, as the language of the Technical Write-off Framework suggests that bar on taking fresh exposure during the cooling off period is on the RE involved in the arrangement, however, it does not suggest any prohibition on other lenders to take fresh exposure during this period.

Of course, other lenders will have to take their own informed credit call and carry out the credit assessment in view of the impaired credit history of the borrower.

What is the difference between:

write off and waiver

Write off and restructuring

Response:

Waiver is the exhaustion of all rights to recoverability of the loan amount as compared to write offs where the lender writes off the amount only for accounting reasons but retains the legal right to recover money.

What should be the contours of the write-off policy? If there is an SOP for write off, what will the SOP contain?

Response:

The write off policy must contain the following aspects:

Condition precedent for write offs – this may include:

Efforts taken for a one-time settlement;

death of the borrower with absence of insurance;

achievement of a certain number of days past due before writing off);

Deterioration in the collateral value

a stipulation that if the monthly recovery drops below a certain % of the loan outstanding only then will the loan be written-off;

untraceability of borrower;

absence of guarantor support;

minimum time elapsed since last recovery;

exhaustion of all possible legal remedies etc.

Approval authority for the write-off – an approval matrix should be drawn for this purpose based on:

Size

Nature of loan

DPD status

Determining the write off amount – this will be based on the extent of security available, recovery efforts already taken, recovery costs associated etc.

Reporting Mechanism for write offs – to the board and CICs

The SOP on the other hand should provide for the following:

Recovery efforts taken and exhausted before arriving at the write off decision

Determination process of the write off amount

Recovery efforts to be taken after write off etc.

Who should approve the write off?

Response:

The delegation of powers for approving write-offs should be clearly articulated in the Policy (Para 5 of Annex to the technical Write off Framework). To ensure objectivity and avoid any potential conflict of interest or a ‘judge in its own case’ scenario, the write-off should, as a general principle, be approved by an authority which is at least one-level higher than the sanctioning authority of the original exposure. The approving authority should be determined based on factors such as the size of the exposure/write-off, the nature and duration of the borrower relationship. The policy should provide adequate flexibility while maintaining robust checks and balances.

What evidence of uncollectability is required to be put on record for write-off action?

Response:

The assessment will be borrower-specific. A detailed record of all the recovery actions taken, outcomes, and reasoned justification that all reasonable recovery measures have been exhausted, and further recovery is impractical, shall be maintained. This shall include reminders, follow-ups, legal notices, enforcement actions, and other efforts undertaken.

An aggressive lending policy, backed by an aggressive write off policy – what implications does it have for the lender, or for the system? In a situation where the lender is witnessing high levels of write off, is there a need to revisit the lending policy ?

Response:

Lending has to be responsible, that is, lenders have to assess the prospects of recovering the loan in view of the borrowers’ cashflows. Lenders determine their lending spreads based on expected losses of the portfolio. Therefore, the cost of defaults is charged on the borrowers. Aggressive lending, in a way, involves the cost of the defaults being passed on to those who mean to pay. The assessment of the borrowers’ ability to pay is not merely an ex ante assessment – it is also benefited by the feedback from performance of the existing pools. Therefore, if a pool is having significant and excessive write off, lenders need to reexamine their lending practices.

Reporting

When the lender writes off the loan, is the lender required to notify the same on the CIC portal?

Response:

Yes, as per the data formats laid down in Annex IV of Master Direction – Reserve Bank of India (Credit Information Reporting) Directions, 2025, a credit institution is required to report written-off amount (total and principal). When an account is reported as written-off and the borrower makes the complete payment, i.e., through settlement or otherwise, the ‘Credit Facility Status’ field in CIC reporting shall be reflected as ‘Post Write Off Closed’.

How long will a lender be required to report write offs to CICs ?

Response:

It may be operationally challenging for lenders to report write-off cases indefinitely. However, considering that the idea of CIC reporting is borrower behaviour, the borrower continues to be a defaulter. Therefore, merely because a loan is written off in accounting books should not mean it should be taken off CIC records.

Accounting

Is there accounting guidance on how the amount of write off/partial write off is to be computed?

Response:

As per Paragraph B5.4.9 of Ind AS 109,

“a financial asset, or a portion thereof, is required to be written off when there is no reasonable expectation of recovering the contractual cash flows. The standard allows for partial or full write-offs, depending on recoverability assessments. For example, if 30% is expected to be recovered via collateral and no further recovery is reasonably expected, then the remaining 70% is to be written off.”

However, Ind AS 109 does not prescribe a specific methodology for computing the amount to be written off, nor does it provide distinct guidance for unsecured lending. In such cases, since no collateral is involved, the amount can be determined based only on how much recovery is reasonably expected from the borrower. For this purpose, the lenders must have a SOP in place which will determine the write off amount based on the expectation of recovery, cost of recoveries, DPD status, borrower history etc.

When an asset is written off, what happens to the specific provision made against the asset, which is outstanding?

Response:

When a loan is written off, the entire amount that is being written off is charged to P/L

When a loan is written-off, the gross carrying amount of the loan is reduced to zero. The specific provision already created against it is utilised (i.e. reversed) against the carrying amount. In other words, as the loan is written off, so is the specific provision against such loan.

What is the impact of write off on the impairment for ECL?

Response:

A write off is a case of incurred loss, whereas ECL is made for expected loss. Expected loss should precede incurrence of the loss, since ECL is forward looking. Therefore, the extent of write off should force a lender to re-examine and calibrate the ECL estimation, such that a write off does not exceed the ECL against such assets..

Is it justifiable to say that there was no SICR and the asset was written off?

Response:

Sans any Significant Increase in Credit Risk (SICR), a financial asset remains in Stage 1 under Ind AS 109. It is generally not prudent to write off a Stage 1 asset, as a write-off requires the lender to have no reasonable expectation of recovering the asset, in whole or in part, a condition that ordinarily implies the asset is credit-impaired and therefore classified under Stage 3. That said, as discussed in above, a write-off before an asset turns to NPA may still be possible, provided there is objective evidence of impairment based on the lender’s internal credit risk assessment, particularly in cases such as short-tenure personal loans or unsecured retail loans, where credit deterioration may manifest earlier than 90 DPD.

What will be the accounting treatment for the recoveries received after an account has been written off?

Response:

Any amount received (principal or interest) after a loan account has been written off will be shown as income in the P/L.

Tax treatment

What will be the tax treatment for write off in the books of the lender?

Response:

For Banks and NBFCs, the tax treatment of loan write-offs is primarily governed by Sections 36(1)(vii) of the Income Tax Act, 1961 (‘IT Act, 1961’). As per Section 36(1)(vii), these entities can claim a tax deduction for bad debts or parts thereof that are actually written off as irrecoverable during the financial year. There are conditions as evidence of the amount having been taken in computation of income, as also reference to accounting standards – ICDS – under sec. 145 (2).

In addition, deduction is allowed for provision, upto limits, under Section 36(1)(viia).

Hence, if there is a write off, the same is deductible against income. However, if the write off was preceded by a provision, and the entity has claimed the benefit of the provision u/s 36 (1) (viia), then the write off should be first adjusted against such provision.

Further, in terms of Section 43D of the Income tax Act, an amount which has already been written off and subsequently recovered will be chargeable to tax in the previous year in which it is credited by the lender to its P/L account or in the year it is actually received, whichever is earlier.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-06 17:15:452026-03-12 13:24:18Gone but Not Forgotten: FAQs on Loan Write-offs

ESG Debt Securities have been formally recognised in India through its inclusion in the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (‘NCS Regulations’) vide the 3rd Amendment Regulations, 2024. While the term was defined under Reg 2(1)(oa) of the NCS Regulations, the framework for issuance and listing of the same was awaited to be specified by SEBI [Reg 12A of NCS Regulations]. SEBI has, through a circular dated 5th June 2025, notified the framework for issuance and listing of ESG Debt Securities (‘Framework’). The Framework is applicable for issuance of ESG Debt Securities with effect from 5th June, 2025, that is the date of the circular. Further, the Framework is applicable to ESG Debt Securities other than Green Debt Securities (GDS), for which the existing framework specified by SEBI continues to be applicable. Our article SEBI revises framework for green debt securities discusses the same.

In this article, we discuss the meaning of ESG Debt Securities and the Framework as specified by SEBI.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Payal Agarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPayal Agarwal2025-06-06 13:41:232025-06-06 13:45:38ESG Debt Securities: Framework for Issuance and Listing in India

The Reserve Bank of India (RBI) has continually worked to strengthen the Know Your Customer (KYC) framework to ensure inclusion. Recognizing challenges in periodic KYC updation, especially in remote areas where bank branches and ATMs are scarce, the RBI has proposed pragmatic measures involving Business Correspondents (BCs). These initiatives aim to ease the KYC process for beneficiaries of government schemes and rural banking customers.

Via these regulations the RBI has also proposed additional measures for REs to increase the effectiveness of periodic KYC updation, while reducing hardship on customers; these are also discussed in this article.

BC allowed to perform KYC Periodic Updation

RBI identified a significant backlog in periodic KYC updation, particularly in accounts opened for the credit of Direct Benefit Transfer (DBT), Electronic Benefit Transfer (EBT), scholarship payments, and those under the Pradhan Mantri Jan Dhan Yojana (PMJDY).

To address this, RBI’s proposed framework allows authorized BCs to assist customers with certain types of KYC updation, improving service access for those in underserved locations. However, the ultimate responsibility for KYC updation still remains with the bank. Once the bank receives the updated information from the BC, it must update its records and intimate the customer upon completion. This is mandated under paragraph 38(c) of the RBI’s Master Direction on KYC.

Updated KYC Periodic Updation Process

Self-declaration for No Change / Address Change

Customers can submit a self-declaration through a BCs if:

There’s no change in their KYC details, or

Only the address has changed.

Collection and Recording of Self-declarations

Electronic Mode:

Banks are expected to enable their BC systems to record and store self-declarations and supporting documents electronically.

Physical Mode (in case electronic facilities are not available):

BC will authenticate the customer’s physical self-declaration and documents.

These will be forwarded promptly to the concerned bank branch.

Acknowledgment receipt shall be issued to the customer.

Transaction Flexibility for Low-Risk Accounts

In line with the KYC directions and Anti-Money Laundering (AML) standards, customers are categorized into low, medium, and high-risk categories. The risk categorization helps to determine the extent of ongoing monitoring, transaction limits, and enhanced due diligence required for each customer category.

The frequency of the periodic updation depends on the risk categorisation of the customer –

High Risk Customers

Every 2 years

Medium Risk Customers

Every 8 years

Low Risk Customers

Every 10 years

RBI vide this guideline proposes that, low risk customers will be allowed time till June 2026 or one year from when their periodic KYC is due, whichever is later to complete the periodic KYC.

For example, if a customer’s KYC was due in September 2025 and it remains pending, the bank can allow the customer to continue the transactions in their accounts upto September 2026. If the due date of the periodic updation was earlier, say May 2025 then the customer could continue to transact until June 2026.

Timely Intimations and Reminders to Customers

Periodic KYC updation is a regulatory requirement under Para 12 of KYC Directions where REs are required to periodically update the customer’s KYC records after on-boarding the customer. REs face several practical challenges in completing periodic KYC updation, such as the customer being unaware about these requirements or reluctance and misconceptions towards sharing personal documents or information.

With respect to this, RBI has proposed that, REs must issue at least three advance KYC due notices (including one by letter) at appropriate intervals, using available communication channels. If the customer still does not complete periodic KYC, three additional reminders must be sent.

All communications should contain easy to understand instructions for updating KYC, escalation mechanism for seeking help, if required, and the consequences, if any, of failure to update their KYC in time. REs are also required to maintain detailed records of these notifications and reminders.

Conclusion

By enabling simplified and decentralized KYC updation, these measures address both operational challenges and the broader goals of financial inclusion.

As the financial ecosystem evolves, such regulatory measures remain crucial for building a secure, inclusive, and customer-friendly financial environment.

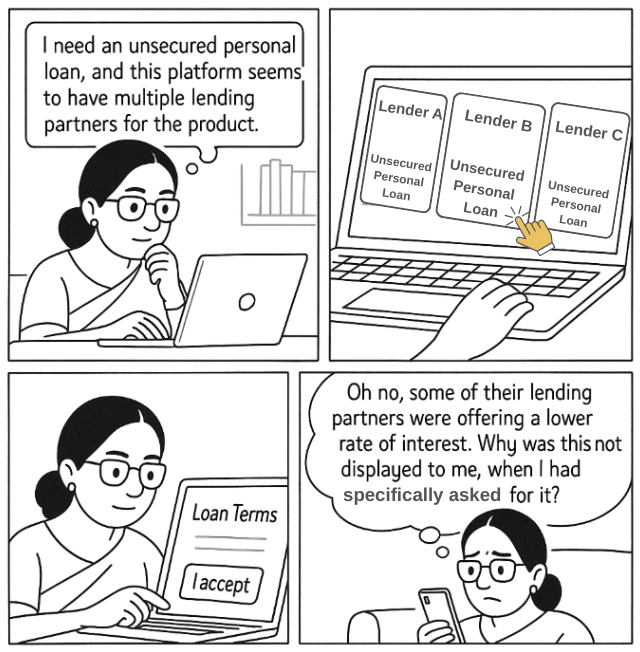

Consider this: you’re out shopping on a Saturday afternoon for a perfect pair of jeans. You stop by a store that retails multiple brands and boasts the best variety. With a salesperson to guide you, you make your pick after careful diligence and comparison, and finally check out. Hours later, however, you discover that certain brands were selling better trousers at a lower price point, in the very same store, but these were deliberately obscured from your vision. Now, you feel duped, hurt and confused.

It’s still the same product. However, what has changed is your ability to make an informed choice. What’s worse, indeed, is that you were made to believe that you had an informed choice.

A sincere consumer, shopping for trousers from a multi-brand store.

Multi-lender LSPs (MLLs)

Drawing parallels from the above, in the lending space, a similar tale unfolds. There is an emerging class of platforms that operate as Multi-lender LSPs (MLLs). These MLLs undertake the sourcing function for multiple lenders against a given product. For instance, Partner ‘A’ may act as a sourcing agent via its platform for unsecured personal loans offered by Lenders X, Y, and Z.

In this case, the consumer may be onboarded onto the platform and be under the impression that they are making an informed choice, and receiving an impartial display of all options for the given loan product. If this is indeed the case, then there is no issue. However, it is possible that due to factors including (a) certain Lender-LSP Arrangements, and (b) differences in the commission received from various lenders, the loan product of a particular lender may be pushed to the borrower. The borrower may also be influenced towards making a particular selection through the use of deceptive design practices designed to subvert their decision-making process (Dark Patterns – for more, see our resource here).

Here, the lack of choice and transparency, and insufficient disclosure in the sourcing process would be an unfair lending practice. And unlike a simple pair of trousers, here the consumer’s hard-earned money and personal finances are at stake.

A similar tale unfolds on a multi-lender platform.

Requirements for REs under the Digital Lending Directions, 2025

Para 6 of the DL Directions

In order to protect the borrower and their right to choose, the RBI vide the Digital Lending Directions, 2025 (‘DL Directions’) has prescribed additional requirements upon REs contracting with such MLLs (refer to our article on the DL Directions here).

These requirements under Para 6 of the DL Directions are applicable upon “RE-LSP arrangements involving multiple lenders”, and pertain to:

The borrower being provided a digital view of all the loan offers which meet the borrower’s requirements.

A view of the unmatched lenders as well.

The digital view would have to include the KFS, APR, and penal charges if any of all the lenders, to display terms in a comparable manner.

The content displayed should be unbiased and objective, free from the influence of any dark patterns or deceptive design practices designed to favour a given product.

The RBI’s annual report for FY 2024-2025 also reveals that the rationale behind these additions was to mitigate risks arising out of LSPs that display the loan offers in a discretionary way, and “which seldom display all available loan offers to the borrower for making an informed choice”. These requirements were, of course, first published via the Draft Guidelines on ‘Digital Lending – Transparency in Aggregation of Loan Products for Multiple Lenders’ (our team’s views on the same may be found here).

Multi-lender LSP v. LSP working for multiple lenders – Is there a difference?

Although this may not be immediately apparent from the language, the “RE-LSP arrangements involving multiple lenders” being contemplated here (in our view) are not RE-LSP arrangements where a single LSP is contracting with multiple REs, each for a separate product, but rather the MLLs described above.

For example, consider a scenario where the LSP works with Lender ‘A’ for vehicle loans, Lender ‘B’ for personal loans, Lender ‘C’ for gold loans and so on. Would this then be considered a Multi-lender LSP requiring compliance under Para 6 of the DL Directions? In our view, no.

Here, because each borrower has only a single lender for a particular product, there is no question of their ability to choose being prejudiced, or there being a need to draw a comparison between the terms offered by multiple lenders. Hence, the requirements under Para 6 of the DL Directions would not be applicable upon REs contracting with such LSPs.

Such requirements would only become relevant in the case where the LSP is undertaking sourcing for multiple lenders against a particular product. In such a case, because the borrower is under the impression that they have a choice, it becomes crucial to protect the borrower’s ability to make that choice (in an informed, transparent, and non-discriminatory manner).

Consumer Protection Act, 2019

Additionally, with reference to the above scenario, under Section 2(9) of the Consumer Protection Act, the following (amongst others) have been recognised as consumer rights (upon violation of which the consumer can seek redressal):

Right to be informed: “the right to be informed about the quality, quantity, potency, purity, standard and price of goods, products or services, as the case may be, so as to protect the consumer against unfair trade practices”

Access to competitive prices: “the right to be assured, wherever possible, access to a variety of goods, products or services at competitive prices”.

In our view, with respect to MLLs, this may be interpreted to mean that the borrower has a right to be informed of the comparable options and to receive an impartial, unbiased, and competitive display of the terms to enable their decision-making.

Finally, it is to be noted that such MLLs, would also qualify as “E-Commerce Entities” under the Consumer Protection (E-Commerce) Rules, and the said rules inter alia cast a duty upon such entities to ensure that they do not adopt any unfair trade practice, whether in course of business on its platform, or otherwise [Rule (4)(2)]. Under the E-commerce Rules, a “marketplace e-commerce entity” is an e-commerce entity providing an information technology platform to facilitate transactions between buyers and sellers. Marketplace e-commerce entities are required to ensure that:

All the details about the sellers necessary to help the buyer make an informed decision at the pre-purchase stage are “displayed prominently in an appropriate place on its platform”

To the extent MLLs would meet this definition, they would also need to ensure the same.

The identity of a corporate entity may undergo various changes, either pursuant to merger, demerger, sale of one or more divisions or undertakings, conversion into LLP etc. Usually, in corporate restructuring, the assets and liabilities forming part of an undertaking are shifted to another undertaking, say, the successor entity. Generally, these kind of transactions are covered under the ambit of Related Party Transactions (“RPTs”) under the provisions of Companies Act, 2013 (“Act”) and SEBI Listing Regulations given that the restructuring involves related party(s) and RPTs have always been an evergreen and ever-evolving aspect of corporate functioning that has been put to guardrails by the law makers by involving specific disclosures and approvals.

However, MCA vide its General Circular No, 3O/2O14 dated July 17, 2014has provideda relaxation to unlisted companies from the applicability of section 188 of the Act for the transactions arising out of corporate restructuring since the same are being dealt under the specific provisions of the Act. On the other hand, for listed companies Regulation 23 of Listing Regulations requires seeking prior approval of Audit Committee/Shareholders, as applicable, for RPTs and no relaxations have been granted by SEBI to listed companies in this specific regard. This gives rise to doubt whether a transaction under a scheme of corporate restructuring will qualify as an RPT or not.

Accordingly, in the present write-up, the following issues have been dealt with:

Identification of a transaction under a corporate restructuring as an RPT;

Rationale for segregation of an RPT from a scheme; and

Process for approval and disclosure of RPTs arising out of corporate restructuring.

Identification of a Transaction

Definition of RPT is not the subject matter of this write-up as the same has been dealt with by us in several of our write-ups along with FAQs which can be accessed athttps://vinodkothari.com/article-corner-on-related-party-transactions/. Instead of diving into the details, let’s simply understand that any transaction involving a transfer of resources, services or obligations between parties falling under the following matrix will be considered as an RPT.

A and B Limited (‘B’) are related parties with A holding a 51% stake in B’s share capital;

B holds a 20% stake in C Limited (‘C’); and

A holds 0.33% in C.

A scheme of arrangement has been proposed between these companies, under which an undertaking of Company A will be transferred to Company C. As consideration for this transfer, shares of Company C will be issued to the shareholders of Company A.

This arrangement involves two distinct transactions:

Transfer of Undertaking: The first transaction involves the transfer of an undertaking (a bundle of assets and its related liabilities) from Company A to Company C, in exchange for shares of Company C. This constitutes a “transfer of resources” as defined under Regulation 2(zc) of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, and therefore qualifies as an RPT.

Issuance of Shares and Dilution of Shareholding: A key aspect of the scheme is the issuance of shares by Company C to the shareholders of Company A. As a result of this issuance, the shareholding of Company B in Company C will be diluted, falling below the 20% threshold.

This raises a question: Does such dilution constitute an RPT?

For a transaction to be classified as a related party transaction, there must be a transfer of resources, services, or obligations between related parties. In this case, while Company B and Company C are related parties, there is no actual transfer of resources, services, or obligations between them as part of this transaction. The dilution of shareholding occurs as a consequence of the share issuance, not due to a direct transaction between B and C.

Conclusion:

Therefore, while the transfer of the undertaking qualifies as an RPT, the dilution of Company B’s shareholding in Company C does not constitute a related party transaction and hence does not require separate approval under the SEBI Listing Regulations.

Transfer of an undertaking under a scheme of demerger

A Limited (“A”), a diversified conglomerate with operations across multiple sectors, owns B Limited (“B”), its wholly owned subsidiary engaged in automobile manufacturing. Recently, B expanded into the electric vehicle (EV) segment. Following a strategic review, B has decided to demerge its EV business from its core automobile operations.

As part of this restructuring, the EV undertaking will be transferred to C Limited (“C”), a newly incorporated, wholly owned subsidiary of A. Post-demerger, C will become the Resultant Company, focusing exclusively on the EV business.

RPT Implication

The transfer of the EV business from B to C constitutes a transaction between two wholly -owned subsidiaries of the same listed entity (A) and hence, there cannot be said to be any effective transfer of resources so as to be considered as an RPT.

However, since company C will be incorporated after the approval of the scheme by the shareholders a question may arise as to when the approval needs to be placed between the shareholders for RPT. Since, a pre approval of RPT is mandatory the approval has to be taken beforehand from the shareholders

Exemption from Approval

Since both B and C are wholly owned subsidiaries of A, there is no effective change in ownership or effective transfer of resources. Accordingly, this transaction falls under the exemption provided in Regulation 23(5) of the SEBI Listing Regulations, which exempts RPTs between wholly owned subsidiaries of a listed entity from the approval requirements.

Conclusion

While the transfer qualifies as an RPT under the SEBI Listing Regulations, it is exempt from the approval process due to the continued ownership within the same shareholders thereby resulting in no change of resources. This allows the company to realign its structure without involving regulatory hindrances. Also refer to our write up on RPTs: Wholly-owned but not wholly-exemptto understand the application of RPT Controls for transactions with Wholly Owned Subsidiary.

Scheme of arrangement involving Creditors

A Limited (‘A’) is a Listed Company;

A Limited (‘A’) and B Limited (‘B’) are related parties with A holding a 51% stake in B’s share capital;

B holds 20% stake in C Limited (‘C’); and

A holds 0.33% in C.

C is facing a severe liquidity crunch and thereby, C is unable to service/ settle the o/s debt obligations. As a result, a scheme of arrangement has been proposed in which an undertaking of C will be transferred to B. Further, the consideration for the present arrangement as is required to be disbursed by B shall be used for servicing the remaining creditors of C (i.e., the creditors belonging to the remaining undertaking of C)

This arrangement involves two distinct transactions:

Transfer of Undertaking: The first transaction involves the transfer of an undertaking from Company C to Company B, in exchange for shares of Company B used to discharge its liability. This constitutes a “transfer of resources” as defined under Regulation 2(zc) of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, and therefore qualifies as a RPT.

Issuance of Shares to creditors: A key aspect of the scheme is the issuance of shares by Company B to the creditors of Company C against their outstanding loans to C. The transaction is between two unrelated parties, However, one may argue that the purpose and effect of this is to benefit C (by way of reducing its outstanding debt obligations) which is a related party of B and from A’s perspective this will be a transaction between a subsidiary (B) and a person, the purpose of which is to benefit a related party of the subsidiary (C).

There will be two kinds of creditors in the above scenario:

Creditors pertaining to the demerged undertaking: After the transfer of undertaking to company B all the liabilities pertaining to the undertaking will also be transferred, as a result, the creditors of company C will become creditors of company B, thereby removing the doubts of C being benefited by this transaction.

Other Creditors: At the time of receiving the consideration, these creditors will still be creditors of company C, thereby benefiting C by reducing its outstanding debt obligations and accordingly will constitute an RPT. However, separate approval can be avoided and clubbed alongside approval sought under point 1 above.

Dilution of director’s shareholding under a Scheme

A Limited (‘A’) is a listed company;

A and B Limited (‘B’) are related parties with B being a WOS of A;

Mr. X (Independent Director of B) holds a 2% stake in C Limited (‘C’); and

A and C have entered into a scheme of arrangement whereby an undertaking of C is transferred to A.

The transaction between A and C will qualify as an RPT because:

The first party to the transaction is the listed company itself (A), and

The second party (C) qualifies as a related party of the subsidiary (B) in terms of Section 2(76)(v) of the Companies Act, 2013.

With respect to the dilution of Mr. X’s shareholding in C, as a result of the scheme, it is clarified that this will not pose any concern, as already discussed earlier in this article.

Transfer of undertaking under a scheme of amalgamation

A and B are peer entities, with A being backed by foreign promoters who wish to divest one of their business verticals. Scheme of amalgamation has been proposed for both entities to merge their operations, with the business being run through a newly incorporated entity i.e. C. All of A’s resources related to this vertical will be transferred to C and both A and B will become shareholders in the newly formed company with A holding 40% and B holding 60%. B will be dissolved as a result of this scheme.

In the above scenario, C will be an associate company of A and accordingly will be considered as a related party of A. However, if we take a broader view this transaction is between A and B with both being an unrelated party. This scheme will definitely affect the shareholders of A and approval of shareholders for the scheme will be a prerequisite for this transaction. However, from the RPT angle this does not seem to fundamentally affect the shareholders as the transaction is between two unrelated parties.

Despite the above facts, this transaction will be governed by the provisions of regulation 23 and will have to follow a separate approval process, independent of the scheme approval, as this falls under the RPT matrix. Alternatively this transaction would not have been required to take a separate approval if the transfer of undertaking was between A and B removing C from the scenario.

Transfer of undertaking in a Scheme of Merger

A Limited and B Limited are related parties, with B forming part of the promoter group of A. A Limited operates in the Agriculture sector, while B Limited is primarily engaged in marketing and logistics services, assisting A in distributing and promoting its agricultural outputs globally. A proposal has been placed to merge the operations of B into A.

Since the transfer of resources occurs between A and B, which are related parties, the transaction qualifies as an RPT as there is transfer of resources of B into A.

Decoding the underline basis for considering the RPT angle in scheme of arrangements

The first checkpoint for a transaction to be categorised as an RPT is transfer of resources, services and obligations with the involvement of a related party either at the level of the listed entity or of its subsidiary. Further, the following takeaways can be understood from the casses discussed above:

A scheme of arrangement can involve transactions that qualify as RPTs for one or more parties directly participating in the scheme.

Even if a listed company is not a direct party to the scheme, it may still be subject to RPT regulations if its subsidiary is a party to the scheme and is transacting with a related party of the listed entity or its subsidiary.

Under a scheme of Corporate Restructuring resources are generally transferred from the transferror company to the transferee company. For instance, in a scheme of merger, both assets and liabilities, which qualify as “resources” and “obligations” respectively, are transferred from one entity to another, typically in exchange for shares of the transferee company and/or for a cash consideration.

It is important to carefully consider the meaning of “transfer” in the context of a scheme of arrangement. The concept should not be limited to the movement of assets and liabilities between two separate legal entities but also the receipt of consideration which results in a change in shareholding or even control.

In a scheme involving two WOS of a listed company, there may be a transfer of resources from one WOS to another. However, since both entities are ultimately owned by the same parent, there is no real change in the ownership or even an effective transfer of resources. Hence, these cases remain outside the purview of an RPT.

In the case of a transfer of an asset by a subsidiary, which is not a WOS, in which the listed entity holds a 51% stake to an associate company in which the listed entity holds only a 20% stake, the transaction results in a change in partial ownership of the asset outside the listed entity’s structure. Although the transfer may occur between two investee entities of the listed company, it effectively leads to divestment of a portion of economic interest. Hence, results in a transfer of resources. Therefore it is suggested that the RPT implications must be independently evaluated for each party, including listed entities with indirect exposure through subsidiaries.

Once a transaction is identified as a RPT the primary concern that arises is whether it has been undertaken on an arm’s length basis. A natural question that follows is whether the fair valuation requirement under Section 230(2) of the Companies Act, 2013 is sufficient to satisfy this test. While the section mandates the submission of a valuation report covering all properties, assets, and shares involved in a scheme, it is important to note that a scheme of arrangement is structurally distinct from a plain bilateral transaction. A scheme often involves strategic, composite, or long-term considerations that may justify deviations from pure fair value. Therefore, the assessment of arm’s length nature, both in terms of properties transferred and the consideration offered, must be undertaken in the context of the terms and conditions of the scheme as a whole, rather than simply putting the share exchange ratio for approval under the RPT agenda.

One of the major reasons for evaluation of a scheme from RPT perspective is its separate approval. This ensures that the scheme is not used as a turnaround for an RPT approval which would not have been approved, had it been proposed outside the framework of scheme. Following are two key reasons supporting the requirement of separate shareholders approval for a RPT:

Exclusion of Related Parties from Voting:

The law prohibits related parties from voting on RPTs. If we assume that approval of the overall scheme automatically includes approval of the RPT, it would allow related parties to influence the vote—undermining the very purpose of this restriction.

2. Exclusion of Related Parties from Voting:

The minimum information required to be presented to shareholders for approving an RPT may not be adequately disclosed if the approval process is merged with that of the scheme. This compromises transparency and does not ensure that shareholders are fully informed about the transaction.

Approval of transactions qualified as RPT

SEBI vide its master circular no. SEBI/HO/CFD/POD-2/P/CIR/2023/93 dated June 20, 2023has specified the requirements that listed companies have to comply before submission of any scheme of arrangement to NCLT for its approval. However, an issue which goes unanswered in the aforesaid circular is whether a separate approval of Audit Committee/Shareholder is required for an RPT arising out of a scheme or will the approval of a scheme from the shareholders which includes a RPT will suffice and be considered as a due compliance of Regulation 23 of SEBI Listing Regulations.

This matter was placed before SEBI for Discussionin its Board meeting dated September 28, 2021, However, no decision has been notified yet.

For listed companies, the following are two key reasons supporting the requirement of separate shareholders approval for a RPT:

Exclusion of Related Parties from Voting:

The law prohibits related parties from voting on RPTs. If we assume that approval of the overall scheme automatically includes approval of the RPT, it would allow related parties to influence the vote—undermining the very purpose of this restriction.

Disclosure Requirements:

The minimum information required to be presented to shareholders for approving an RPT may not be adequately disclosed if the approval process is merged with that of the scheme. This compromises transparency and does not ensure that shareholders are fully informed about the transaction.

The position of unlisted companies is clear in this regard as the Ministry has already issued a clarification, However, SEBI has not provided any relaxations of similar nature to the listed entities. Therefore, it can be said that RPTs under a scheme of arrangement will require a separate approval of the Audit Committee or/and shareholders, as applicable, independent from the approval of the scheme by the shareholders.

Audit Committee: Under the provisions of Regulation 23 of the SEBI Listing Regulations and the relevant sections of the Companies Act, the Audit Committee must approve any transaction involving related parties before it is executed. This ensures transparency and compliance with regulatory requirements.

It is important to note that even if a transaction is not directly entered into by the listed entity but occurs as part of a corporate restructuring scheme involving a subsidiary and it’s the subsidiary who is entering into a transaction with any related party, the prior approval of the listed entity’s Audit Committee is still required. Specifically, if the transaction exceeds the threshold limits defined in Regulation 23(2) of the SEBI Listing Regulations, the Audit Committee’s approval must be obtained before proceeding.

The approval of the committee in case a transaction is not material may be taken in the same meeting which is held for consideration of the scheme before it is submitted to the stock exchanges.

Shareholders’ Approval: In case the transaction under a scheme of arrangement reaches the materiality threshold of Regulation 23 of Listing Regulations, the same will have to be approved by the shareholders of the Company before submission of scheme to NCLT.

A pertinent point to note is that in this case the company has to seek shareholders approval two times, one before submission of scheme to NCLT for RPT and the other for the Scheme at the meeting called by NCLT.

Conclusion

In schemes involving corporate restructuring, especially when related parties are involved, the primary legal considerations are fairness, transparency, and ensuring that the rights of minority shareholders and creditors are not prejudiced. It is crucial for the entities to provide independent fairness opinions, detailed disclosures, and valuations.

[1]A being a listed company all the RPTs have to be identified from A’s perspective

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-03 19:58:202025-08-01 00:49:34Dissecting RPT controls in a corporate restructuring

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-03 19:16:112026-01-13 17:24:1912 hours Certificate Course on Nuts and Bolts of Related Party Transactions

With the continuous growth and the emergence of large non-banking financial companies (NBFCs) in India, the Reserve Bank of India (RBI) has extended certain bank-level regulations to these institutions with the intention to make them manage their various risks. Among these various risks, liquidity risk is a critical one, which could lead to the breakdown of a financial institution, and if a contagion builds, it may affect the entire financial system too. No financial institution is entirely immune to it, even a well-performing NBFC with minimal NPAs could face a run on it if it experiences a liquidity crunch. The larger an institution, the greater impact its failure could have on the broader economy.

To address the above concerns, the RBI under the Para 89 read with Annex XXI of the Scale-Based Regulation (SBR) Directions[1] mandates certain large NBFCs (as discussed below) to maintain a Liquidity Coverage Ratio (LCR).

This article provides a practical guide to the LCR requirements under the SBR Directions, including the regulatory requirements to be followed, and tries to provide insights into its proper implementation by the NBFCs, subject to these norms.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-06-03 19:13:052025-06-04 12:17:13Surviving the Squeeze: Liquidity Coverage Ratio for NBFC liquidity management

The economic device of purchasing an asset, and generating revenue by leasing it out is surely nothing new. However, through innovative leverage of accounting and tax norms, market participants devise offerings that continue to add novelty to this age-old practice. Today, there is an emerging business-opportunity with respect to leasing of electronic devices, which is gaining popularity due to associated tax benefits, short-tenures, and mass-market potential. In this article, we walk the reader through the quintessential features of this model, and the tax rules that make it possible.

Many are likely familiar with the CTC car-leasing model, which is considered a unique by-product of the Indian taxation system, and has been in vogue for several decades now. It entails a reduction in the employee’s taxable income due to the rules pertaining to valuation of perquisites [see Rule 3(2)(A) of the Income Tax Rules].

However, this arrangement is typically only made available to employees meeting a certain salary threshold, as it entails a significant financial contribution, and time commitment, on part of the employee (the time commitment is also of note here because it would require the employee to hold their position long enough to make pay-outs continuously for the tenure of lease).

As a result, the incentives and benefits associated with this CTC car leasing model do not percolate to employees who are not able to make said commitments/do not meet said thresholds.

Likely as a response to this market gap, there is now an emerging model of CTC leasing where the employer obtains a lease for electronics such as smartphones, laptops and tablets, and makes it available to the employees, while treating such lease payments as a part of the employee’s CTC. That is to say, the employer pays the lease rentals, but the same constitutes a part of the CTC – therefore, on a CTC basis, it is the employee who is actually paying the lease rentals. At the end of the lease tenure, the lessor may make the assets available to the employee for purchase at the residual value / other agreed value as specified in the contract. The leasing of such assets to the employer, and the making available of such assets by the employers, to the employees, will be referred to as CTC Device Leasing.

Much of the value associated with CTC Device Leasing is linked once again to the reduction in taxable income for the employee, for, in the absence of the same, the employee may simply obtain those assets through any prevailing EMI schemes (consider also the fact that these EMI schemes may offer more competitive interest rates due to the absence of GST component). However, in that case, the employee earns the gross CTC, and pays tax on the same. To illustrate:

Assume an employee’s agreed CTC is Rs 100,000 a month, and the employer arranges for him a top-class laptop costing Rs 1 lakh, paying lease rentals of Rs 12000 a month for a year. Since this payment of Rs 12000 is a part of the CTC, the employer will now have to pay a salary of Rs 88,000 a month, which is taxed as his salary. However, for the employer, the CTC is Rs 1 lakh. At the end of the 12-month rental period, the employee gets to own the laptop from the lessor.

II. Unpacking the CTC Device Leasing Model

a. Tax and GST Aspects

The reduction in the taxable income may be due to any one or more of the criteria mentioned under Rule 3(7) of the Income Tax Rules, and the legality of the same (i.e. whether that specific facility qualifies for the exemptions) would need to be evaluated on a case-to-case basis. However, generally speaking, reference in the case of mobile phone leasing (which is a common asset class being made available under this modell) is made to Rule 3(7)(ix) of the rules, read with Section 17 of the Income Tax Act, which would provide that

“Taxable value of perquisite shall be computed on the basis of cost to the employer (under an arm’s length transaction) less amount recovered from the employee. However, expenses on telephones including a mobile phone incurred by the employer on behalf of employee shall not be treated as taxable perquisite”[1]

Here, it becomes necessary to examine the burden on the employer under the device leasing model. In the CTC car-leasing model for instance, the employer remains “cost-agnostic”. Because under that model regardless of whether the benefit is given to the employee by deducting ‘x’ amount from their CTC component beforehand, or by paying said ‘x’ component to the employee, the financial obligation viz. expense for the employer remains unchanged. However, because in CTC car-leasing the employer is not able to claim ITC on the GST paid to the Lessor with the Lease rentals (due to it being blocked credit under Section 17(5) of the CGST Act), the cost is passed on to the employee, from whose salary along with lease rentals are also deducted the GST amount.

Under CTC Device Leasing, the employer is similarly cost-agnostic with the key difference being that employers are able to claim the ITC on the inputs (as it is not blocked credit). Hence, the employer would deduct only the actual lease rentals net-off from GST from the employee’s salary.

b. Residual Value considerations

As has been mentioned above, at the end of the lease tenure, the lessor typically would make the asset available to the employee for purchase basis its residual value. An important consideration here is that unless the lessor is a financial sector entity, they would usually not wish to keep a very low residual value (10% or below) lest the lease be considered a “financial lease” as per accounting norms, and thus eventually require the lessor to obtain an NBFC registration (as the transaction would be considered substantively a financing transaction, with the assets being financial assets, and income from the assets posing concerns with respect to the PBC criteria).

However, a higher residual value could also correspond to a decrease in the tax benefit for the employee, because the option to purchase the asset would be exercised post the lease tenure by the employee themselves, and such payout being made by the employee directly against the residual value, may not qualify for the exemptions under the Income Tax Rules. Hence, there is a delicate balance the lessors would have to maintain, to ensure viability of the business-model, while also ensuring that the structure remains compliant with tax law.

c. Trend-Cycling & Data Protection

One practical consideration here is that the tenure of the lease in CTC leasing models gives the employer an added employee-retention benefit. However, in the case of device leasing, the lease tenures may need to account for the “trend-cycles”, whereby younger workforce (in particular) may have a preference towards upgrading the device as and when newer models are released (for e.g. new iPhone models are typically released within a year of the previous launch). If the lease tenure exceeds this time-span, the facility may lose some of its charm.

Another consideration here, would pertain to the deletion of the employee’s data from the device, having regards to applicable data protection law, in case the employee does not exercise the purchase

option / the possession of device is transferred to another employee (for e.g. due to employee’s exit from the company).

III. Concluding Notes – Impact on Leasing Volumes and Industry in India

Because this model is in its nascent stage, it may be too soon to predict what its impact would be on leasing volumes in India. However, as the data captured in our report, available here, may reveal – the growth of leasing volumes in India has been very low. The use of leasing appears to be kept afloat by models such as CTC car leasing, and now maybe through device leasing.

However, one can surely expect this model to be popular with the lessors who would be able to enter the leasing space without making significant capital expenditures / taking on large borrowings, and to some extent may even be able to lease by obtaining the assets through their own funds rather than borrowings, and use the churn (due to the short tenure) to keep the leasing going.

[1]See CBDT Resource on Income Tax Rules, available at: https://incometaxindia.gov.in/_layouts/15/dit/pages/viewer.aspx?grp=rule&cname=cmsid&cval=103120000000007059&searchfilter= .

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-05-30 17:26:332025-06-04 17:48:56A brief on the law and mechanics of CTC based Device Leasing