Workshop on Insider Trading Regulations for Compliance Officers

See our resources on insider trading here: https://vinodkothari.com/prohibition-of-insider-trading-resource-centre/

See our resources on insider trading here: https://vinodkothari.com/prohibition-of-insider-trading-resource-centre/

– Payal Agarwal, Partner | corplaw@vinodkothari.com

An August 2025 Informal Guidance by SEBI for Welspun Corp Limited sought to clarify the applicability of contra trade on release of pledge. However, it goes on to say that: “…in case of creation of pledge/ revocation, the beneficial ownership does not change till pledge is invoked”. While the IG was specific to revocation of pledge, this seems to be creating a confusion on the contra trade restrictions on creation of pledge. In this article, we discuss the nature of pledge as a trade, and applicability of trading related restrictions on various stages of pledge. Also see a detailed article on treatment of various stages of pledge as trading under PIT Regulations.

Any opposite trade within 6 months of a prior trade attracts violation of contra-trade, except in case of specific waiver for a bona fide purpose. We discuss various combinations of trades within a span of 6 months to understand whether such trades attract contra-trade restrictions.

| Transaction 1 | Transaction 2 | Is it contra-trade? | Can a waiver be granted by CO? |

| Purchase of shares (Buy) | Creation of pledge (Sell) | Yes, opposite trades within 6 months | Yes, if the DP is able to demonstrate the urgency and bona fide nature of such transaction |

| Creation of pledge (Sell) | Purchase of shares (Buy) | Yes, opposite trades within 6 months | In such a case, it is very difficult to prove bona fide of the subsequent trades of purchase of shares after creation of pledge. |

| Creation of pledge (Sell) | Release of pledge | No, since the release of pledge does not result in an opposite trade per se, it is incidental to the primary trade of pledge creation and only restores back the position as it was prior to creation of pledge. | NA |

| Release of pledge | Creation of pledge with another person (Sell) | No | Yes, if the DP is able to demonstrate the urgency and bona fide nature of the underlying transaction for which the pledge is to be created |

| Purchase of shares (Buy) | Invocation of pledge (Sell) | No, since the invocation of pledge is not at the discretion of the shareholder. The relevant act of disposal of shares is taken into account as a “trade” upon creation of pledge itself, and hence, not considered as “trade” again, upon such invocation. | NA |

| Invocation of pledge (Sell) | Purchase of shares (Buy) | NA |

How does the Compliance officer verify/ensure that the purpose of the pledge is bonafide?

There cannot be any sure or one-size-fits-all response to this. Pledge is not for its own sake; pledge for an underlying transaction, which may be margin trading facility, borrowing, etc. The Compliance Officer should see whether that underlying transaction is within the regular business or activity of the pledgor. Whether the pledge is limited to the shares of the listed entity or has other securities? Whether the pledgee is an entity which is engaged in providing similar facilities to several unrelated entities? Whether the timing of the pledge is not indicating the advantage of a price spurt, etc.

The applicability of contra trade restrictions on the various stages of pledge are tabulated hereunder:

| Stage of pledge | Nature of trade (Acquisition/ Disposal) | Pre-clearance required? | TWC applicable? | Contra-trade restrictions applicable? | Remarks |

| Creation of pledge | Disposal | Yes | No, if the trade is bona fide | Yes | While creation of pledge amounts to trade, exemptions from TWC and contra trade may be availed if the trade is for bona fide purpose. |

| Release of pledge | Acquisition | No | No | No | No change in beneficial ownership, and no actual acquisition/ disposal – mere restoration of the position prior to creation of pledge |

| Notice of invocation of pledge | NA | NA | NA | NA | No dealing in securities, mere notice specifying intent |

| Invocation of pledge | Disposal, however, continuation of the prior action of creation of pledge | No | NA | No | Invocation of pledge is done by the pledgee upon default. Once a pledge is created, the pledgor has no control over the invocation of such pledge upon default. Further, since creation of pledge is itself considered as ‘disposal’, the same shares cannot be considered to have been ‘disposed’ again, upon invocation. |

| Sale of pledged securities | Disposal, however, continuation of the prior action of creation of pledge | No (however, intimation to CO post sale, if not covered by System Driven Disclosure) | NA | No | Sale of pledged securities is done by the pledgee, and is not under the control of the pledgor. Further, since creation of pledge is itself considered as ‘disposal’, the same shares cannot be considered to have been ‘disposed’ again, upon sale. |

– Team Corplaw | corplaw@vinodkothari.com

When it comes to insider trading regulation breaches, it is the adverse headline value which is far more punitive than the amount of penalties.

Bhagavad Gita says:

अकीर्तिं चापि भूतानि

कथयिष्यन्ति तेऽव्ययाम् |

सम्भावितस्य चाकीर्ति

र्मरणादतिरिच्यते 2/34

Reputation damage (अकीर्तिं ) for reputed people (सम्भावित ) is worse than death. That is to say, the more reputed one is, the more is the risk to reputational capital.

Therefore, every precedent teaches a lesson to all insiders and compliance officers to take calculated and conservative views, when it comes to timely disclosure of price sensitive information.

A recent order of the Supreme Court (dated December 2, 2025) dismissed an appeal against SAT on a matter involving selective dissemination of an unpublished price sensitive information, thereby, affirming the penalty of Rs. 30 lakh levied by SAT. The issue revolved around whether or not a media report, resulting into a selective, inadvertent dissemination of unpublished price sensitive information, requires prompt public disclosure by the listed entity.

The whole idea of fair disclosure of inside information is that there is no information asymmetry, as the same kills meaningful price discovery in the market. If there is a leakage of information, before any information is released by the company, that creates an asymmetry and non-democratic spreading of unconfirmed information or so-called rumour. In such a situation, the listed entity has to act and either confirm what is being rumoured, or deny, and it cannot remain silent. There, a stance that the information is not ripe for disclosure, does not work, as the information is already spreading. See our presentation on Verification of Market Rumour by listed entities & other related amendments and FAQs on Verification of Market rumour by Listed Entities.

With the recent amendments in the PIT Regulations clarifying that unverified events or information reported in print or electronic media cannot be considered as “generally available information”, this is no longer a question as to whether such information can escape the ambit of UPSI. In fact, regulations along with the stock exchange guidance have gone a long way in quantifying the market impact.

Reg 8(1) of PIT Regulations requires companies to put in place a Code for Fair Disclosure of Information, in accordance with the model Code provided under Schedule A. Para 1 of Schedule A requires prompt public disclosure of UPSI as soon as credible and concrete information comes into being in order to make such information generally available.This coincides with the requirement of disclosure of material events and information to the stock exchanges under Reg 30 of LODR.

Also, Para 4 of the Schedule 1 requires: Prompt dissemination of unpublished price sensitive information that gets disclosed selectively, inadvertently or otherwise to make such information generally available.

While Principle 1 pertains to a general principle of making material information available to the public, Principle 4 seeks to fill the information asymmetry in case of an inadvertent leak of UPSI.

In a May 2025 order, SAT has discussed the distinction between the application of disclosure requirements in the aforesaid principles:

“Principle-1 requires it to ipso facto make prompt disclosure, as and when a credible and concrete information comes into being in order to make it ‘generally available’. Thus, if the UPSI is concrete and credible, the company would have already made its disclosure to make it generally available. But before such a stage is reached, and the UPSI gets disclosed selectively, then in such a scenario, even though the company was not required to make disclosure in accordance with Principle-1, Principle-4 makes it obligatory to make prompt disclosure to make information generally available to ensure compliance with general Principle–2.”

In the said ruling, one of the contentions of the Appellants was that the material information, on account of being published in media sources, becomes generally available. However, SAT observed that, “Till the information is disclosed by the company, it remains unauthenticated.”. In the absence of a clarity on the matter by the company to the investors and public at large, speculative information will keep floating around. As such, “selective leakage of the information, howsoever accurate or otherwise or complete or in bits and pieces, does not discharge the company from its responsibility of making prompt disclosure to make it generally available, moreso when such information has been classified by company as UPSI.”

Thus, while Reg 30(11) of LODR provides discretion to the listed entities (except top 250 listed entities based on market capitalisation) w.r.t. responding to market rumours, such discretion cannot override the requirements of the PIT Regulations. Also see our FAQs on Verification of Market rumour by Listed Entities.

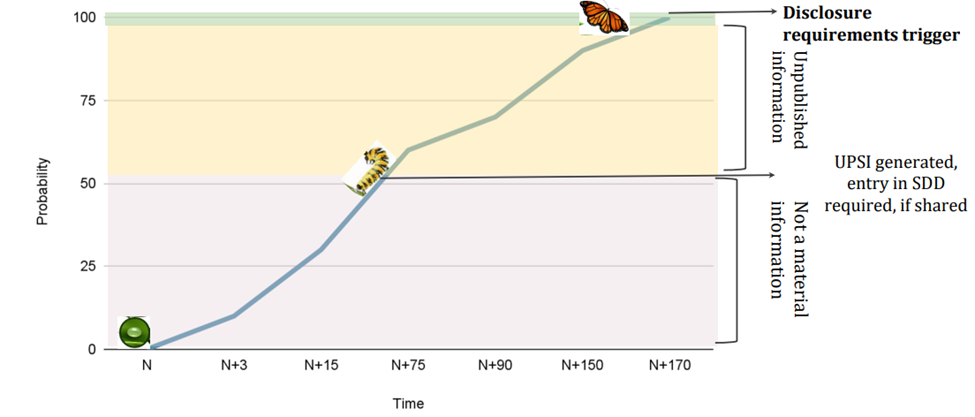

The metamorphosis of an internal development into UPSI and ultimately a disclosable event is based on its probability of occurrence, over that of non-occurrence. Generally speaking, once the probability of occurrence of an event is more than the probability of its non-occurence, UPSI may be said to have been germinated, thus, requiring preservation of such information and all related controls.

See our presentation on verification of market rumour by listed entities & other related amendments.

While the SEBI Listing Regulations appear to grant leeway to listed entities to remain silent on rumours floating in the market, such leeway is not absolute and the PIT Regulations still require the listed entities to ensure public dissemination of information, where a leak of UPSI has occurred. While the Supreme Court dismissed the appeal, citing that the same has been comprehensively dealt with by SEBI and SAT on the basis of the factual matrix, the proceedings signal the SC’s stand that the principles underlying the PIT Regulations have to be upheld at all times, and if going by the principles, it is essential for the listed entity to speak, it cannot remain silent.

In view of the significance of the subject, we are conducting a 12 hours Certificate Course on Insider Trading for Compliance Officers, see details here – https://vinodkothari.com/2025/11/12-hours-certificate-course-on-insider-trading-for-compliance-officers/

Our other resources:

Team Corplaw | corplaw@vinodkothari.com

Updated as on November 19, 2025

Also access our Resource Centre on PIT here:

– Pammy Jaiswal and Payal Agarwal | corplaw@vinodkothari.com

Pursuant to SEBI (Prohibition of Insider Trading) Amendment Regulations, 2025, SEBI has amended UPSI definition, effective from June 10, 2025 inserting a longer list of information, some of which may seem purely operational or business-as-usual for listed companies. Several questions arise: Whether each of this information will be regarded as “deemed UPSI”, thereby requiring compliance officers to do the drill of structured digital database entry to even trading window closure every time such an event occurs? What are the immediate actionables on the company? Whether the list of UPSI gets restricted only to the prescribed events or has to be tested for price sensitivity?

In this video, Ms. Pammy Jaiswal and Ms. Payal Agarwal discuss and analyse the scope of amendments, what it means for listed entities and the actionables that follow:

See our other resources at Prohibition of Insider Trading – Resource Centre

Loading…

Loading…

– Vinita Nair & Aisha Begum Ansari | corplaw@vinodkothari.com

Loading…

| Click here to register for the workshop – https://forms.gle/hFtagsmfBMpcgkP28 |

Loading…

Read our article on “Mutual Fund units now under the net of insider trading regulations“

Read our FAQs on “Insider Trading Framework for Mutual Funds“

Our PIT Resource Centre can be accessed here

– Team Corplaw | corplaw@vinodkothari.com

Loading…

Also read our article on “Mutual Fund units now under the net of insider trading regulations“

Our PIT Resource Centre can be accessed here