Presentation on Decoding Due Date for AGM Extension

Our related Content:

Our related Content:

Important Links:

Our other write ups covering Companies (Amendment) Act, 2020:

Shaifali Sharma | Vinod Kothari and Company

Understanding minority squeeze out

‘Minority squeeze out’ demonstrates the power of majority shareholders to forcibly acquire shares from minority shareholders and drive them out to gain absolute control over the company.

Section 236 of the Companies Act, 2013 (‘Act, 2013’) sets out a process of squeezing out minority shareholder whereby any shareholder of the company, either alone or along with person acting in concert, holding 90% or more of the total issued equity share capital, may acquire the remaining equity shares of the company by giving an offer to the minority shareholders. This “Rule of Majority” principle was recognized in a landmark case Foss v. Harbottle, where it was held that that the minority shareholders are bound by the decision of the majority shareholders and the Courts do not interfere in the internal matters of the Company. However, the powers of majority should be exercised in reasonable manner which do not result into oppression of minority. Thus, the inherent protection under the law is that the acquisition shall take place at a fair value or higher value as determined by the valuer in accordance with Rule 27 of the (Compromise, Arrangements and Amalgamation) Rules, 2016 (‘CAA Rules, 2016’).

The section 236 was incorporated under the Act, 2013 on the recommendation of the Dr. J.J. Irani Committee Report on Company Law, 2005[1] for the reason reproduced below:

“The law should enable companies to purchase the stake of minority shareholders in order to prevent exploitation of such shareholders where a promoter has bought back more than 90% of the equity. Such purchase should, however, on the basis of a fair offer. Appropriate valuation rules for this purpose should be prescribed, or, the last known price prior to delisting, could be made the benchmark for such acquisitions.”

The purpose is to ensure a seamless takeover of a company, since in view of very smallholding of the minority shareholders; the minority shareholders neither will be able to participate in the management of the company nor will be able to seek redressal of their rights or have a meaningful participation in the company’s working. Therefore, to provide fair exit to the minority shareholders and to allow majority shareholders to exercise full control over the company, section 236 has been inserted under the Act, 2013.

This write-up endeavours to analyse (1) the existing process of acquiring minority shares held in physical form, (2) the practical difficulties for acquiring minority shares held in demat form and (3) the new rules introduced vide MCA notification[2] dated 17.12.2020 setting out the procedure of transferring minority shares held in demat form.

The acquirer holding 90% of the issued equity share capital of a company to inform the company of its intention to oust the minority shareholders in accordance with provisions of Section 236 of Act, 2013. At the same time, the minority shareholders can also offer their shares to be acquired to the acquirer in compliance prescribed provisions.

Fair value of the shares of the Company whose shares are being transferred in accordance with Rule 27 (Compromise, Arrangements and Amalgamation) Rules, 2016.

Fair value of the shares of the company to be offered to the minority shareholders shall be calculated by a registered valuer in accordance with Rule 27 of the CAA Rules, 2016 which provides for evaluation criteria for listed companies as well as unlisted companies.

The company whose shares are being transferred to the acquirer, shall act as a transfer agent for receiving and paying the price to the minority shareholders and for taking delivery of the shares and delivering such shares to the majority.

The majority shareholders are required to deposit an amount equal to the value of shares to be acquired by them, in a separate bank account to be operated by the company for payment to the minority shareholders, for atleast 1 year for payment to the minority shareholders and such amount shall be disbursed to the entitled shareholders within sixty days and even thereafter by the company.

The offer letter received from the acquirer will be dispatched to the shareholders along with the consideration.

Minority shareholders shall on receipt of offer letter, provide for physical delivery of their shares to the company within the offer period.

The point of relevance is that, the word used is “physical delivery of shares” and not physical share certificates. Accordingly, physical delivery would cover delivery of both, shares held in physical form as well as shares held in dematerialized form by minority shareholders.

7. Failure to tender physical delivery of shares

In the absence of a physical delivery of shares by the shareholders within the time specified by the company, such shares shall be taken as cancelled and the transferor company shall be authorized to issue shares in lieu of the cancelled shares and complete the transfer by following the applicable transfer provision and dispatching the amount paid by the acquirer in advance.

In order to ensure smooth implementation of acquisition of minority shareholding, the Act, 2013 empowers the company whose shares are being transferred to issue new shares in lieu of the undelivered shares within the time specified.

While in case of shares held in physical form, section 236(6) of the Act, 2013 is clear to state that share certificates shall deemed to be cancelled for non-receipt of physical delivery of shares and the company is authorized to issue new shares in lieu of cancelled share certificates, however, there is a difficulty in implementing the same in case of shares held in dematerialized form.

The law is silent on the procedure to be followed by the company for transferring the shares held by minority shareholders in dematerialized form, in the absence of receipt of DIS from minority shareholders. The Depositories, without any clear instructions from Ministry of Corporate Affairs (‘MCA’) or Securities Exchange Board of India (‘SEBI’), does not permit transfer of shares to the demat account of acquirer by virtue of DIS signed by the company on behalf of the minority shareholder.

Therefore, the intent of the law behind the enforcement of section 236 remains unfulfilled in case of shares held in dematerialized form as the company would not be able to give effect to the transfer in the absence of any definitive procedure laid out to give effect to the same.

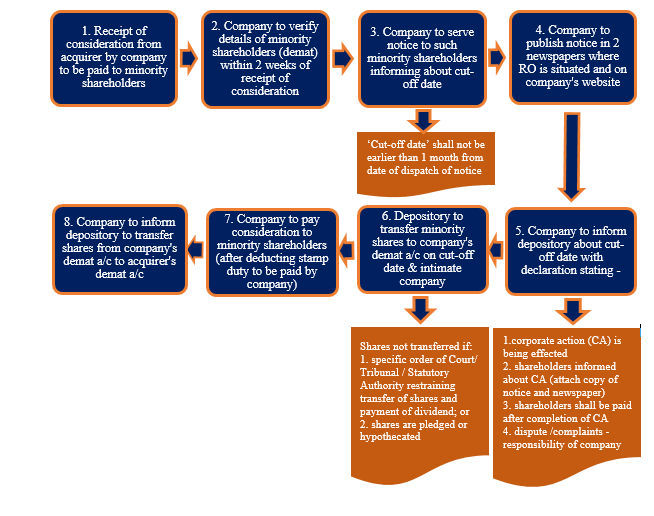

MCA has finally woken up to the need to enable companies to purchase minority shareholding held in demat form. The CAA Rules, 2016 has been amended vide MCA notification dated 17.12.2020 where a new Rule 26A has been introduced to provide process for purchase of minority shareholding held in demat form. The detailed step-by-step process highlighting the actionable for transferor company is explained below:

The company shall within 2 weeks from the date of receipt of the amount equal to the price of shares to be acquired by the acquirer, verify the details of the minority shareholders holding shares in dematerialised form.

The company shall send notice to minority shareholders by registered post or by speed post or by courier or by email informing about a cut-off date on which the shares of minority shareholders shall be debited from their account and credited to the designated demat account of the company, unless the shares are credited in the account of the acquirer, as specified in such notice, before the cut-off date.

The cut-off date shall not be earlier than 1 month after the date of sending of the said notice. Also, if the cut-off date falls on a holiday, the next working day shall be deemed to be the cut-off date.

A copy of the notice served to the minority shareholders shall also be published simultaneously in two widely circulated newspapers (one in English and one in vernacular language) in the district in which the registered office of the company is situated and also be uploaded on the website of the company, if any.

Immediately after newspaper publication of notice, the company shall inform the depository w.r.t cut-off date and submit the following declarations stating that:

For the purposes of effecting transfer of shares through corporate action, the Board of Directors of the company shall authorise the Company Secretary, or in his absence any other person, to inform the depository and to submit the documents as may be required.

Except for the shares already credited in the account of the acquirer before the cut-off date by shareholders, the depository shall transfer of shares of the minority shareholders into the designated demat account of the company on the cut-off date and intimate the company.

Note: In case a specific order of Court or Tribunal, or statutory authority restraining any transfer of such shares and payment of dividend, or where such shares are pledged or hypothecated under the provisions of the Depositories Act, 1996, the depository shall not transfer the shares of the minority shareholders to the designated demat account of the company.

The company shall immediately upon transfer of shares by the depository, disburse the price of the shares so transferred, to each of the minority shareholders after deducting the applicable stamp duty, which shall be paid by the company, on behalf of the minority shareholders, in accordance with the provisions of the Indian Stamp Act, 1899.

One the payment is successfully disbursed to minority shareholders, the company shall inform the depository to transfer the shares of such shareholders, kept in the designated demat account of the company, to the demat account of the acquirer.

Note: The company shall continue to disburse payment to the entitled shareholders, where disbursement could not be made within the specified time, and transfer the shares to the demat account of acquirer after such disbursement.

A pictorial presentation giving step-by-step procedure to the above requirements is summarized below:

Concluding Remarks

The majority shareholders enjoy the right to squeeze out minority shareholders to gain control over the company in toto and attain a greater flexibility in decision making. While the process of acquisition of minority shares held in physical form is clearly established in the Act, 2013, however, companies were facing it practically difficult to implement in case minority shares are held in demat form. In the absence of any clear guidelines, squeezing out minority shareholders turned out as a challenge to implement.

The new rules notified by MCA are certainly a laudable solution facilitating the majority shareholders to smoothly acquire the shares held by minority shareholders in demat form.

Other reading materials on the similar topic:

Our Youtube Channel: https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

[1] H-ttp://www.nfcg.in/pdf/23-Irani%20committee%20report%20of%20the%20expert%20committee%20on%20Company%20law,2005.pdf

[2] http://egazette.nic.in/WriteReadData/2020/223774.pdf

Shaivi Bhamaria | Vinod Kothari and Company

Reg. 31A of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘LODR Regulations’) lays down conditions pursuant to which promoters/ person belonging to promoter group of a listed entity can be reclassified as public shareholders. Reg. 31A (5) provides that if a public shareholder seeks to re-classify itself as promoter, it will have to make an open offer as per the provisions of SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

SEBI on November 23, 2020 has issued a Consultation Paper on Re-Classification of Promoter/ Promoter Group Entities and Disclosure of the Promoter Group Entities in the Shareholding Pattern[1] (‘Consultation Paper’) for public comments. At present SEBI has been granting relaxations from the requirements under reg. 31A of the LODR regulations on a case to case basis to promoters who have found reclassification difficult under current regulatory regime. The said Paper has been issued on the basis of the recommendations of the Primary Market Advisory Committee (‘PMAC’) of SEBI in order to regularise the provisions relating to reclassification and minimise the need for providing relaxation on case-to-case basis.

A summary of the present reclassification process is laid down below:

In the informal guidance given to Alembic Pharmaceuticals Limited[2] SEBI had exempted the company from obtaining approval of shareholder for reclassification of 5 promoters as public shareholders inter-alia on the grounds that:

Further, in the informal guidance given to Gujarat Ambuja Exports Limited[3], SEBI had exempted the company from obtaining approval of shareholder for reclassification of one its promoters on the grounds that:

It is pertinent to note that SEBI in its interpretative letter had stated that the company would not be required to take shareholders’ approval, subject to compliance with the provisions of reg. 31A of LODR regulations. Reg, 31A of LODR regulations provide for shareholders’ approval, hence it was not very clear whether exemption from obtaining shareholders’ approval was granted or not.

At present reg. 31A (3) (b) (i) of LODR regulations provide that promoter/ persons belonging to promoter group seeking re-classification should not together hold more than 10% of the total voting rights in the listed entity.

The Consultation Paper proposes to increase the threshold of 10% to 15%, to enable those promoters who have shareholding of less than 15% but are no longer involved in the day-to-day control of the listed entity to opt-out from being classified as promoters, without having to reduce their share-holding.

At present reg. 31A of LODR Regulations is silent on the time period within which the listed entity must place the reclassification request received from the promoter/ persons belonging to promoter group before the board, consequently as per SEBI’s data, in certain cases reclassification requests from promoter/ persons belonging to promoter group have not been placed before the Board, thereby ceasing the process in its initial phase.

To prevent this and streamline the process of reclassification, SEBI has proposed insertion of a time limit of one month receiving the reclassification request, within which the listed entity must place the same before its board of directors.

As mentioned above, reg. 31A (3) (a) (ii) provides that the time gap between the meeting of the board at which the proposal for reclassification was accepted and the meeting of the shareholders, seeking approval for the same should be at least 3 months. The rationale behind the same was to give adequate time to the shareholders for considering the request of the promoter.

However, time gap 3 months resulted in an increase in the total time taken in the process. In order to increase both cost and time efficiency, the Consultation Paper proposes to reduce the minimum time gap from 3 months to 1 month.

At present reg. 31A (9) provides exemption from the provisions of reg. 31A (3), (4) and (8)(a), (b) of LODR regulations in cases where re-classification of promoter/ persons belonging to promoter group is as per the resolution plan approved under s. 31 of the IBC, subject to the condition that the promoter seeking re-classification do not remain in control of the listed entity.

It is proposed to extend the said exemption to re-classification pursuant to an order/ direction of the Government/ regulator and/or as a consequence of operation of law since the re-classification is a natural consequence of the order/direction of the Government/ regulator.

It is proposed to extend the exemption from procedure for re-classification to cases where the re-classification is pursuant to an open offer made in accordance with the provisions of SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 2011 (‘SAST regulations’), subject to the satisfaction of following conditions:

The rationale behind the exemption being that in cases where intent of reclassification has already been mentioned in the Letter of Offer, the requirement of promoter making an application is a mere procedural formality since the fact of re-classification is already present in the public domain.

Exemption from the procedure for re-classification, is also proposed to be granted in cases where, pursuant to an open offer, a listed entity intends to re-classify erstwhile promoter/ persons belonging to promoter group but the promoter/ persons belonging to promoter group are not traceable or are not co-operative, but the same can be done after the fulfillment of the following conditions:

Reg. 31 of LODR Regulations mandates that all entities falling under promoter/ promoter group are to be disclosed separately in the shareholding pattern.

As a matter of practice, several companies do not disclose names of persons in promoter/ promoter group who do not hold any shares.

It is to be noted that pursuant to the SEBI (Listing Obligations and Disclosures Requirements) (Sixth Amendment) Regulations, 2018[4] SEBI had, by virtue of by insertion of reg. 31(4) required that all entities falling under promoter and promoter group be disclosed separately in the shareholding pattern of listed entities appearing on the website of the stock exchanges in accordance with the formats specified by the SEBI . However, since the provisions of the Regulations still did not explicitly require entities to disclose the entire list of promoter/ promoter group irrespective of their shareholding, companies continued the practice of disclosing only those promoter/ promoter group entities that held shares in the company. A detailed write-up on this insertion in Reg 31(4) can be read here.

To fill this gap, it has been proposed that all entities falling under promoter and promoter group be disclosed separately even if they do not hold shares in entity. Further it is proposed that listed entities obtain a declaration on a quarterly basis, from their promoters on the entities/ persons that form part of the ‘promoter group’.

Disclosures of all entities falling under promoter/ promoter group irrespective of the fact whether they hold shares in the listed entity hold all the more importance in light of the recent SEBI circular on Automation of Continual Disclosures under reg. 7(2) of SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT regulations’). In order to facilitate System Driven Disclosures (‘SDD’)[5] pursuant to the said circular, the listed entities are required to disclose to the designated depository the PAN number/ Demat account number (for PAN exempt entities) of all Promoters and promoter group so that the system can capture any trade in securities made by such entities.

Exemptions provided in the consultation paper in cases of open offer and order/ direction of Government/ regulator lead to reduction in compliance burden on the listed entity, further the proposed amendments w.r.t reduction in time gap between the board meeting and general meeting and the setting of time limit for placing the application before the board will lead to streamlining the entire process and bring efficiency in the same.

The clarification w.r.t to disclosure of names of promoter group entities holding ‘Nil’ shareholding and obtaining quarterly declarations from promoter may add to the compliance burden of listed entities at once, but in our view, should be effective in the long run.

Specific comments/suggestions on the Consultation Paper can be made to SEBI on or before December 24, 2020.

[1] For full text of the consultation paper see:

[2] For full text of the informal guidance see:

https://www.sebi.gov.in/sebi_data/commondocs/Alembic-sebiletter_p.pdf

[3] For full text of the informal guidance see:

https://www.sebi.gov.in/sebi_data/commondocs/oct-2017/gujaratsebi_p.pdf

[4] See: https://www.sebi.gov.in/legal/regulations/nov-2018/securities-and-exchange-board-of-india-listing-obligations-and-disclosure-requirements-sixth-amendment-regulations-2018_41051.html

[5] Circular no. SEBI/HO/ISD/ISD/CIR/P/2020/168 dated September 09, 2020 available at:

https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/sep-2020/1599654391917.pdf#page=1&zoom=page-width,-16,559

-Effectiveness however doubtful!

Abhishek Saraf | Vinod Kothari and Company

SEBI observed that under the current remote e-voting framework, the participation of the public non institutional shareholders/ retail shareholders (shareholders) is at negligible level. One of the reasons behind such low participation may be due to reluctance of the shareholders to register with multiple e-voting service providers (ESPs) which provide the e-voting facility to the listed entities. Shareholders may be finding it a tedious task to register with multiple ESPs for casting their vote and maintain multiple user IDs and passwords for the said purpose.

In view of the same and with the intent to increase the optimum utilization of the remote e-voting process by shareholders, SEBI came out with consultative paper[1] on 5th March 2020 to review the e-voting mechanism as provided by various ESPs.

Based on the public comments on consultative paper, SEBI vide its circular[2] dated 09th December 2020 decided to enable the facility of a singly log in credential for the purpose of e-voting for all demat account holders.

This article covers the circular along with our analysis on the probable impact which SEBI intends to achieve by way of easing and at the same time securing the remote-e-voting process for shareholders.

The existing mechanism requires shareholders to register themselves with ESPs and have a separate login credential for each ESP to be able to cast their vote on resolutions proposed to be passed at the general meetings. The same can be explained better with the help of the following example:

Suppose a shareholder Mr. S holds shares in 3 companies and these companies appoint different ESPs for providing remote e-voting facility to vote on the resolutions proposed to be passed at their respective general meeting.

Now the shareholder shall register himself with all the 3 ESPs and have a separate login credential for each ESP to be able to cast his vote. Under the given situation, the shareholder may find it tedious and therefore, skip the whole process itself. The notice calling the general meeting contains the instruction for logging in the portal of the Depository in the following manner:

With an intent to address the issue of negligible voting by the shareholders, SEBI has introduced a mechanism to make e-voting process more secure, convenient and simple for shareholders under which the shareholder will be allowed to cast their vote directly through their demat accounts/ Depositories/ Depositories Participants without having to go through the hassle of registering with various ESPs and maintaining a list of multiple user IDs and passwords. In the process, only a single login credential will be enough for the shareholders to participate in remote e-voting and register their vote in respect of any item.

The existing process as envisaged above will be replaced with a single doorstep which will be accessed by a single login credential under which the shareholder shall be allowed to vote without any further authentication by ESPs.

By taking the help of the above example, the new facility can be explained in the following manner-

Under the new facility, Mr. S does will not have to maintain login credentials for all the 3 ESPs but only have to register with the Depository either directly or through his demat accounts with Depsoitory Participants to have access to all the ESPs through a single log in without additional authentication with ESPs. This has been explained in detail below.

The facility shall be implemented in 2 phases.

Under Phase -1:

SEBI has instructed to implement the process as provided in Phase-1 within 6 months of the date of the circular (i.e. within 9th June 2021).

Shareholders with demat accounts have been provided the option to either directly register with Depositories to access the e-voting page of various ESPs through websites of the Depositories or accessing various ESP portals directly from their demat accounts, through the facility provided by the depository without any further authentication by ESPs, for participation in the e-voting process.

Under Phase-2:

SEBI has instructed to implement Phase 2 within 12 months from the completion of the process in Phase 1.

Under the 2nd phase, it has been proposed to further enhance the convenience and security of the system with the help of One Time Password (OTP) verification mechanism wherein the shareholders will be allowed to login through registered mobile number or E-mail based OTP verification as an alternate in place of logging through username and password for cases where shareholders have directly registered with the Depository

Further for logging in through demat account with the DPs, a second factor authentication using mobile or e-mail based OTP shall also be introduced after logging in.

While the SEBI circular requires implementation in two phases, the consultative paper was different on the following fronts:-

Depositories

ESPs

This framework for one stop log-in has only been made mandatory in respect of public non-institutional shareholders/ retail shareholders and the existing process may continue for all physical shareholders and shareholders other than individuals viz. institutions/ corporate shareholders. Further, SEBI’s perception on the current shareholder participation is based on its public consultation and is probably because, the shareholders are not taking the trouble of registering themselves with the various ESPs.

The step taken by SEBI towards a more democratic participation of the shareholders may be effective in the long run. However, its current effectiveness seems to be doubtful unless the shareholders for whom the same has been made, find it useful and be ready to implement the same.

Our other relevant resources on similar topic can be read here –

[1] https://www.sebi.gov.in/reports-and-statistics/reports/mar-2020/consultative-paper-on-e-voting-facility-provided-by-listed-entities_46213.html

Shaifali Sharma | Vinod Kothari and Company

Analyst and investor meets are one of the many ways of communicating and sharing information. Conducting periodical meetings, conferences, one-to-one meetings or con-calls with analysts or investors who wish to know more about the company, its historic performance, financial details, future prospects, etc. is a common practice for the listed entities. The most common amongst these meetings are the earning calls which is called immediately following the release of the quarterly or annual financial results. Whereas, one-to-one meets or conference calls with selective investors/ analysts are also conducted in the normal course of business of the companies.

With the intent to rule out any information asymmetry in the market, the schedule, presentations or any information material used during such analyst or institutional investor meetings are required to be disclosed by companies to stock exchange(s) and also hosted on the company’s website as required under the SEBI (Listing Obligations and Disclosure Requirements), Regulations, 2015 (‘Listing Regulations’).

Moreover, the SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’) requires fair disclosure of material events and therefore, provides principles for fair disclosure which includes

The governing Regulations are discussed in this article.

However, looking at the practice of most of the listed companies, it has been observed that such disclosures are simply box ticking exercise where disclosure of mere PowerPoint slides of presentation are given instead of what is discussed in the meeting to give an example.

The concerns relating to disclosures in respect of analyst meets/ institutional investors meet/ conference calls were discussed by Primary Market Advisory Committee (‘PMAC’) constituted by SEBI in July, 2020 which then formulated a Sub-Group to recommend specific disclosure requirements to strengthen analyst/ investor meets. In this regard, a ‘Report on disclosures pertaining to analyst meets, investor meets and conference calls[1]’ (‘Report’) has been issued on November 20, 2020 seeking public comments on or before December 21, 2020. The Sub-Group has recommended to make the disclosure requirements optional for the initial one year and mandatory thereafter for all the listed companies. This article attempts to analyse the recommendations and their probable impact on the current regime under the Listing Regulations and PIT Regulations.

Further, on perusing the Report it has been observed that it explicitly distinguishes between scheduled meeting with the analysts and investors and unscheduled one-to-one calls with them. This article discusses the intention behind such distinction recognised by SEBI itself.

Listing Regulations

Regulation 46(2)(o) of the Listing Regulations requires the listed entity to disseminate the schedule of analyst or institutional investor meet and presentations made by the listed entity to analysts or institutional investors simultaneously with submitting the same to the stock exchange. The aforesaid Regulation is reproduced below:

“46(2) The listed entity shall disseminate the following information under a separate section on its website:

xxx

(o) schedule of analyst or institutional investor meet and presentations made by the listed entity to analysts or institutional investors simultaneously with submission to stock exchange;”

Further, Part A(A)(15) of Schedule III of the Listing Regulations read with SEBI circular[2] dated September 09, 2015, requires the listed entity to disclose the schedule of analyst or institutional investor meet and presentations on financial results made to such analysts or institutional investors without any application of the guidelines for materiality as specified u/r 30(4) of the Listing Regulations.

Furthermore, Part C(8)(e) of Schedule V of the Listing Regulations requires the listed entity to disclose the presentations made to the institutional investors or analysts in the section on the Corporate Governance of the Annual Report under the head ‘Means of Communication’.

Apart from above requirements, principles governing disclosures and obligations of listed entity shall be simultaneously conformed viz. to provide adequate and timely information to recognised stock exchange(s) and investors, provide adequate and timely information to shareholders, to ensure timely and accurate disclosure on all material matters including the financial situation, performance, ownership, and governance of the listed entity, etc.

PIT Regulations

Pursuant to Regulation 8 of PIT Regulations, every listed company is required to formulate a Code of Fair Disclosure and Conduct for fair and timely disclosure of UPSI in compliance with the principles set out in Schedule A to the PIT Regulations. The principles of fair disclosure w.r.t analyst meet is as follows

| Country Name | Disclosure Requirement

|

| USA |

|

| UK |

|

| Singapore |

|

| Canada |

|

Information Asymmetry

As discussed above, the Listing Regulations require the listed entities to disclose the schedules and presentations for analyst or institutional investor meetings on its website and to the stock exchange(s) with 24 hours of the event taking place. However, except for few top companies, majority of the listed companies treat this as a mere formality. They disclose only the occurrence of analyst/ investor meets and circumvent disclosure of significant details of the said event.

As per the Report, it has been observed that the reports shared by the listed entities have information that does not have its source from quarterly results or investor presentation and thereby lead to selective sharing of information. Therefore, it is seen that there exists information asymmetry due to following the Regulations in letter and not in spirit.

Selective disclosure and Risk of divulging UPSI

Selective disclosure occurs when a company releases UPSI about the company to an individual or selective group of persons (e.g., analysts or institutional investors) before disclosing the information to the general public. It creates an adverse impact on market integrity similar to that of insider trading. Selective disclosure lead to asymmetry information.

For example, analyst/ investors during a one-to-one meet are provided with such price sensitive information which may not be disclosed in presentation or the financial results and is not available in public domain.

Therefore, issues concerning selective sharing of information, disclosure of incomplete information, inconsistency in the disclosures made by different listed companies have made it essential for SEBI to review the current regulatory requirements and further strengthen the disclosure regime.

Conflicting views of Kotak Committee on Investor/ Analyst meets

The Committee on Corporate Governance constituted under the Chairmanship of Mr. Uday Kotak Committee (‘Kotak Committee’) by SEBI issued its ‘Report on Corporate Governance[8]’ in October, 2017 wherein it took a contrary view and stated that disclosure of schedule of investor/ analyst meetings does not serve any practical purpose and therefore may not be required. Relevant extract provided below:

“The Committee was of the view that the disclosure of schedules of analyst/institutional investor meetings does not serve any practical purpose, and there have been instances of its misuse. Hence, the Committee recommended that the disclosure of schedules of analyst/institutional investor meetings may not be required. To clarify, the information to be shared at such meetings has to be strictly in compliance with the SEBI PIT Regulations.”

On the other hand, the present Report has considered institutional investors meet or conference call with analysts/ shareholders as a material event and emphasis has been placed on strengthening the disclosure framework. It is significant to note that while the Kotak Committee was of the view that putting up the schedule for investors meeting have the potential of being misused, the Sub-Group constituted by the PMAC holds a completely contrary view and has not recommended to do away with the said practice.

New disclosure requirements pertaining to post-earnings conference calls/quarterly calls

Listed companies generally organise analyst / investor meetings or conference calls after the release of quarterly financial results. To curb any information asymmetry among different class of stakeholders, the following recommendations are proposed:

The idea is to immediately disclose any UPSI shared at such conference calls. Some of the top listed companies like Tata Steel[9], Reliance Industries[10], Infosys[11], Pricol Ltd[12], Power Finance Corporation Ltd[13], have already adopted the above practices and upload the audio/video recordings, transcripts of analysts / investor conference calls on their respective websites. The recommendations will now require the other listed companies to put in place an effective disclosure mechanism in this regard.

Discretion of companies to limit attendees of conference calls

Unlike in US, Indian listed companies generally restrict the conference calls to their respective analysts / investors only to avoid any unnecessary disruption of call, presence of competitors, etc.

However, genuine institutional investor or analyst may get excluded from participating in the meeting and thus, Sub-Group suggested that companies should make the provision of inclusion of certain individuals based on their request and on verification of their credentials.

Accordingly, Sub-Group has recommended to leave the discretion with the listed companies for deciding the participants for such meetings.

One-to-one meetings – Selective or effective disclosures?

Listed companies in their course of business are often seen conducting one-to-one meetings/ con-calls with investors / analysts (‘private meets’). Such private discussions are more risky due to the following:

Even if a company wishes to make public the proceeding of such meeting/ call, the investor may not agree to share private call records in public domain.

However, by disclosing one-to-one affairs, chances of information asymmetry will reduce. Also, other investors, particularly the minority investors, who are generally not a part of such meets may be benefitted from effective price discovery. Besides investors, regulatory authorities and stock exchanges will also be able to track such meets for any future references.

In view of the above, Sub-Group has made following recommendations:

Unlike in case of post-earning calls, it seems recording and disclosure of private meets is not required. It is always better to look before you leap, hence companies must consider recording such private meets (written or audio) and making it public to avert possibility of selective disclosure and leak of material information.

Further, in addition to the affirmation by official of company involved, a confirmation from the concerned party (investor/ analyst) shall also be obtained confirming that no material public information was shared with the concerned analyst during such meeting, and that the information shared in the meeting was only clarification of facts/information already available in public domain.

After the recommendations of Kotak Committee in the year 2017 to discard the requirements of disclosing the schedule of analyst / institutional investor, a new approach of SEBI to enhance transparency and strength disclosure framework of analyst/ investor meets is evident from the recommendations of the Sub-Group.

An effective disclosure mechanism will be required to be put in place by companies for adequate and timely disclosures. A measure of ‘silent or quiet period’ may be adopted where companies for a specified period (generally prior to release of financial results) refrain from interaction with the analyst/ investor/ media in order to avoid inadvertent disclosures of UPSI on selective basis. To conclude, the recommendations seems to promote a culture of corporate governance encouraging companies to follow the compliance in spirit of law.

Other reading materials on the similar topic:

Our Youtube Channel: https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

[1] https://www.sebi.gov.in/reports-and-statistics/reports/nov-2020/report-on-disclosures-pertaining-to-analyst-meets-investor-meets-and-conference-calls_48208.html

[2] https://www.sebi.gov.in/legal/circulars/sep-2015/continuous-disclosure-requirements-for-listed-entities-regulation-30-of-securities-and-exchange-board-of-india-listing-obligations-and-disclosure-requirements-regulations-2015_30634.html

[3] https://www.sec.gov/rules/final/33-7881.htm

[4] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32014R0596

[5] http://rulebook.sgx.com/rulebook/703-0

[6] http://rulebook.sgx.com/rulebook/appendix-71-corporate-disclosure-policy

[7]https://webfiles.thecse.com/resource/CSE%20Policy%205%20%E2%80%93%20Timely%20Disclosure,%20Trading%20Halts%20and%20Posting%20Requirements.pdf

[8] https://www.sebi.gov.in/reports/reports/oct-2017/report-of-the-committee-on-corporate-governance_36177.html

[9] https://www.tatasteel.com/investors/financial-performance/analyst-call-recording/

[10] https://www.ril.com/InvestorRelations/FinancialReporting.aspx

[11] https://www.infosys.com/investors/news-events/analyst-meet/2020/india/main.html

[12] https://www.pricol.com/investor-call-transcripts.aspx

[13] https://www.pfcindia.com/Home/VS/109

-CS Henil Shah & CS Burhanuddin Dohadwala

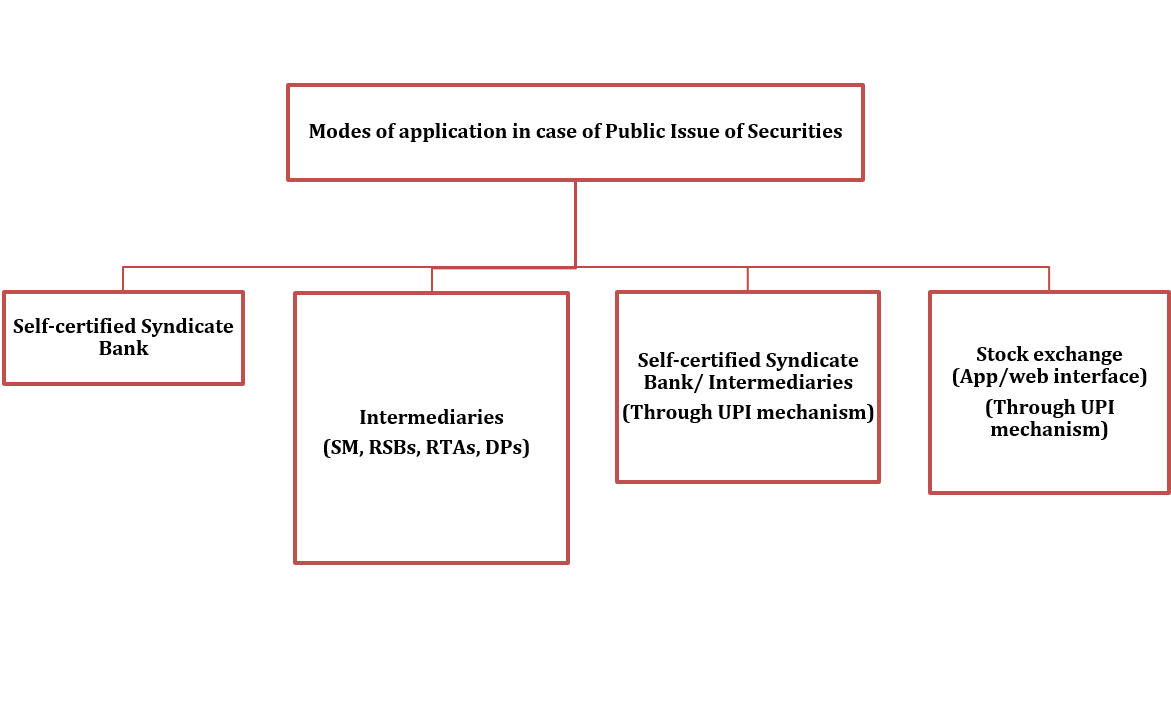

In order to streamline the process in case of public issue of debt securities and to add an addition to the current Application Supported by Blocked Amount (‘ASBA’) facility. Securities and Exchange Board of India (‘SEBI’) vide its circular dated November 23, 2020[1] (‘November 23 Circular’) has introduction Unified Payments Interface (‘UPI’) mechanism for the process of public issues of securities under:

The said circular shall be effective to a public issue of securities for the aforesaid captioned regulations which opens on or after January 01, 2021 (‘effective date’). Earlier, SEBI Circular dated July 27, 2012[2] (‘Erstwhile Circular’) provided the system for making application to public issue of debt securities. The Erstwhile Circular will stand repealed from the effective date. However, SEBI Circular dated October 29, 2013[3] w.r.t allotment of debt securities shall continue to remain in force.

Earlier in November, 2018[4] SEBI had introduced use of UPI as a payment mechanism with ASBA, to streamline the process of public issue of equity shares and convertibles and implemented the same in 3 phases.

The article below covers the role required to be done by the issuer in case of public issue of debt securities.

UPI[5] is an instant payment system developed by the National Payments Corporation of India (‘NPCI’), an RBI regulated entity. UPI is built over the IMPS (‘Immediate Payment Service’) infrastructure and allows you to instantly transfer money between any two parties’ bank accounts.

The facility to block funds through UPI mechanism whether applying through intermediaries (viz syndicate members, registered stock brokers, register and transfer agent and depository participants) or directly via Stock Exchange (‘SE’) app/ interface is set for upto and amount of Rs. 2 lakhs, which is the maximum limit approved by NPCI for capital markets vide its circular dated March 03, 2020[6].

Sponsor Bank as a term was introduced under the SEBI circular dated November 01, 2018 meaning a self-certified syndicate bank appointed by issuer to conduit/act as a channel with SE and NCPI to facilitate mandate collect requests and/or payment instructions of retail investors.

| November 23 Circular | Erstwhile Circular | Remarks |

| Direct application through SE app/web-interface along with amount blocked via UPI mechanism. | Direct application over the SE interface with online payment facility; | Online payment facility stands replaced with UPI mechanism. However, it is not clear as to how the application to be submitted where amount to be invested is above 2 lac rupees. |

| Application through intermediaries along with details of his/her bank accounts for blocking funds | Application through lead manager/syndicate member/sub-syndicate members/ trading members of SE using ASBA facility | No change |

| Application through SCSBs with ASBA. | Applications through banks using ASBA facility; | No change |

| Application through SCSBs/intermediaries along with his/her bank account linked UPI ID for the purpose of blocking of funds, if the application value is Rs.2 lac or less. |

– |

New insertion. |

|

– |

Application through lead manager/syndicate member/sub-syndicate members/ trading members of SE without use of ASBA facility | This was discontinued for all public issue of debt securities made on or after October 01, 2018 vide SEBI Circular dated August 16, 2018[7]. |

|

– |

Application through lead manager/syndicate member/sub-syndicate members/ trading members of SE for applicants who intended to hold debt securities in physical form. | No reference made in the present circular |

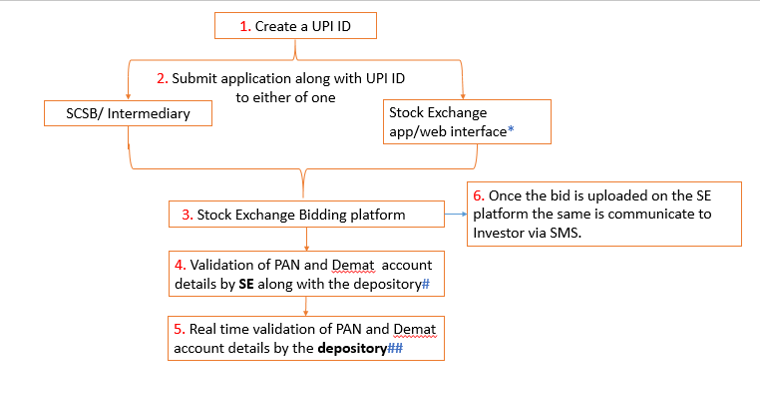

Process of the applying utilizing UPI mechanism is produced in a diagrammatic form as below:

Process of the applying utilizing UPI mechanism is produced in a diagrammatic form as below:

* Application made on SE App/web interface shall automatically get updated on SE biding platform

# Upon bid being entered under the bidding platform SE shall undertake validation process of PAN and Demat account along with Depository.

## In case of any discrepancies the same are reported by depositories to SE which in turn relays the same to intermediaries for corrections.

Apart from appointing a sponsor bank by the issuer the roles of issuer remain same as those already required under the SEBI circular dated July 27, 2012 i.e.:

Only the aforesaid roles are aligned with newly introduced with UPI Mechanism.

SEBI vide its circular dated November 10, 2015 had, in order to stream line the process of public issue of equity shares and convertibles issued a circular to reduce the timeline for issue from 12 working days to 6 working days and same was introduced for public issue of debt securities, NCRPS and SDI vide circular dated August 16, 2018[8]. The same has been re-iterated/repeated under the November 23 Circular. Indicative timelines for various activities are re-produced under Annexure-A.

Conclusion

Public issue application using UPI is a step towards digitizing the offline processes involved in the application process by moving the same online. UPI mechanism in public issue process shall essentially bring in comfort, ease of use and reduce the listing time for public issues.

Annexure A:

Indicative timelines for various activities

| Sr. No. | Particulars | Due Date (working day) |

| 1. | Issue Closes | T (Issue closing date) |

| 2. |

|

T+1 |

| 3. |

|

T+2 |

| 4. |

|

T+3 |

| 5. |

|

T+4 |

| 6. |

|

T+5 |

| 7. | Trading commences; | T+6 |

Our other materials on the topic can be read here –

[1] https://www.sebi.gov.in/legal/circulars/aug-2018/streamlining-the-process-of-public-issue-under-the-sebi-issue-and-listing-of-debt-securities-regulations-2008-sebi-issue-and-listing-of-non-convertible-redeemable-preference-shares-regulations-_40004.html

[2]https://www.sebi.gov.in/legal/circulars/jul-2012/system-for-making-application-to-public-issue-of-debt-securities_23166.html

[3]https://www.sebi.gov.in/legal/circulars/oct-2013/issues-pertaining-to-primary-issuance-of-debt-securities-amendment-to-simplified-debt-listing-agreement_25622.html

[4] https://www.sebi.gov.in/sebi_data/attachdocs/nov-2018/1541067380564.pdf

[5] https://www.sebi.gov.in/sebi_data/commondocs/mar-2019/useofunifiedpaymentinterfacefaq_p.pdf

[6] https://www.npci.org.in/PDF/npci/upi/circular/2020/UPI%20OC%2082%20-%20Implementation%20of%20Rs%20%202%20Lakh%20limit%20per%20transaction%20for%20specific%20categories%20in%20UPI.pdf

[7] https://www.sebi.gov.in/legal/circulars/aug-2018/streamlining-the-process-of-public-issue-under-the-sebi-issue-and-listing-of-debt-securities-regulations-2008-sebi-issue-and-listing-of-non-convertible-redeemable-preference-shares-regulations-_40004.html

[8]https://www.sebi.gov.in/legal/circulars/nov-2020/introduction-of-unified-payments-interface-upi-mechanism-and-application-through-online-interface-and-streamlining-the-process-of-public-issues-of-securities-under-sebi-issue-and-listing-of-debt-_48235.html

Timothy Lopes – Senior Executive CS Harshil Matalia – Assistant Manager

The year 2020 – ‘Year of pandemic’, rather we can say the year of astonishing events for everyone over the globe. Without any doubt, this year has also been a roller coaster ride for Alternative Investment Funds (‘AIFs’) with several changes in the regulatory framework governing AIFs in India.

Recent Regulatory Changes for AIFs

In continuation to the stream of changes, Securities Exchange Board of India (‘SEBI’), in its board meeting dated September 29, 2020, has approved certain amendments to the SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’). The said amendments have been notified by the SEBI vide notification dated October 19, 2020. The following article throws some light on SEBI (AIFs) Amendment Regulations, 2020 (‘Amendment Regulations’) and tries to analyse its impact on AIFs.

Regulation 4 of AIF Regulations prescribes eligibility criteria for obtaining registration as AIF with SEBI. Prior to the amendment, Regulation 4(g), provided as follows:

“4 (g) the key investment team of the Manager of Alternative Investment Fund has adequate experience, with at least one key personnel having not less than five years experience in advising or managing pools of capital or in fund or asset or wealth or portfolio management or in the business of buying, selling and dealing of securities or other financial assets and has relevant professional qualification;”

The amended provision to 4 (g) extends the meaning of relevant professional qualification, the effect of which seems to add more qualitative criteria to the management team of the AIF, to be evaluated at the time of grant of certification. The newly amended section 4(g) of the AIF Regulations reads as follow:

“(g) The key investment team of the Manager of Alternative Investment Fund has –

Provided that the requirements of experience and professional qualification as specified in regulation 4(g)(i) and 4(g)(ii) may also be fulfilled by the same key personnel.”

It is apparent from the prima facie comparison of language that the key investment team of the Manager may have one key person with five years of experience (quantitative) as well as a personnel holding professional qualification (qualitative) from institutions recognised under the regulation. Further, clarity has been appended in form of proviso to the section that quantitative and qualitative requirements could be met by either one person, or it could be achieved collectively by more than one person in the fund.

With this elaboration, SEBI has harmonized the qualification requirements as that with the requirement specified for other intermediaries such as Investment Advisers, Research Analysts etc. in their respective regulations. Detailed prescription on degrees and qualifications for AIF registration by SEBI is a conferring move and is expected to aid as a clear pre-requisite on expectations of SEBI from prospective applications for registration of the fund.

Regulation 20 of AIF Regulations specifies general obligations of AIFs. Erstwhile, the responsibility of making investment decisions was upon the manager of AIFs. It has been noticed by the SEBI from the disclosures made in draft Private Placement Memorandums (‘PPMs’) filed by AIFs for launch of new schemes, that generally Managers prefer to constitute an Investment Committee to be involved in the process of taking investment decisions for the AIF. However, there was no corresponding obligation in the AIF Regulations explicitly recognizing the ‘Investment Committee’ to take investment decisions for AIFs. Such Investment Committees may comprise of internal or external members such as employees/directors/partners of the Manager, nominees of the Sponsor, employees of Group Companies of the Sponsor/ Manager, domain experts, investors or their nominees etc.

These amendments are based on the recommendations to SEBI to recognize the practice followed by AIFs to delegate decision making to the Investment Committee.[1] The rationale behind amendments to AIF Regulations is based on the following merits as proposed in the recommendations::

Thus, the insertion was made, giving the option to the Manager to constitute an investment committee subject to the following conditions laid down in the newly inserted sub-regulation, i.e. Regulation 20(6) of the AIF Regulations given below –

The constitution of investment committee is a global standard practice followed by the Funds. However, funds structure in India might be altered with the new defining role of investment committee under the AIF Regulations. The investment committee generally comprises of nominees of large investors in the fund and at times other external independent professional bodies that act as a consenting body towards prospective deals of the fund. The amendment will alter the role of investors holding positions at investment committee as the new defining role might deter them from taking underlying obligations. From the funds perspective seeking external independent professionals might get costly as there is an obligation introduced by way of this amendment regulation. Further, it casts an onus on the investment committee to be involved in day to day functioning of the fund, which used to be otherwise (where members were usually involved in mere finalising the deals). Lateral entry of the members to investment committee post placement of memorandum with the consent of investors is aimed at greater transparency in funds functioning.

As per Clause 4 of Schedule VIII of FEMA (Non-Debt Instrument) Rules, 2019 (‘NDI Rules’) any investment made by an Investment Vehicle into an Indian entity shall be reckoned as indirect foreign investment for the investee Indian entity if the Sponsor or the Manager or the Investment Manager –

(i) is not owned and not controlled by resident Indian citizens or;

(ii) is owned or controlled by persons resident outside India.

Therefore, in order to determine whether the investment made by AIFs in Indian entity is indirect foreign investment, it is essential to identify the nature of the Manager/Sponsor/investment manager, whether he is owned or controlled by a resident Indian citizen or person resident outside India.

RBI in its reply to SEBI’s query on downstream investment had clarified that since investment decisions of an AIF are taken by its Manager or Sponsor, the downstream investment guidelines for AIFs were focused on ownership and control of Manager or Sponsor. Thus, if the Manager or Sponsor is owned or controlled by a non-resident Indian citizen or by person resident outside India then investment made by such AIF shall be considered as indirect foreign investment.

Whether an investment decision made by the Investment Committee of AIF consisting of external members who are not Indian resident citizens would amount to indirect foreign investment?

In light of the above provisions of the NDI Rules and with the introduction of the concept of an “Investment Committee”, SEBI has sought clarification from the Government and RBI vide its letter dated September 07, 2020[2].

With the enhancement in eligibility criteria, SEBI has ensured that the investment management team of the AIF would have relevant expertise and required skill sets.

Further, giving recognition to the concept of an investment committee will cast an obligation on investment committee fiduciary like obligations towards all the investors in the fund. . However, there exists certain ambiguity under the NDI Rules, for applications wherein external members of investment committee who are not ‘resident Indian citizens’, which is currently on hold and pending receipt of clarification.

[1] https://www.sebi.gov.in/sebi_data/meetingfiles/oct-2020/1602830063415_1.pdf

[2] https://www.sebi.gov.in/sebiweb/about/AboutAction.do?doBoardMeeting=yes

‘Technical’ contravention subject to minimum compoundable amount, format for public disclosure of compounding orders revised.

– CS Burhanuddin Dohadwala | corplaw@vindkothari.com

Introduction

Compounding refers to the process of voluntarily admitting the contravention, pleading guilty and seeking redressal. It provides comfort to any person who contravenes any provisions of FEMA, 1999 [except section 3(a) of the Act] by minimizing transaction costs. Reserve Bank of India (‘RBI’) is empowered to compound any contraventions as defined under section 13 of FEMA, 1999 (‘the Act’) except the contravention under section 3(a) of the Act in the manner provided under Foreign Exchange (Compounding Proceedings) Rules, 2000. Provisions relating to compounding is updated in the RBI Master Direction-Compounding of Contraventions under FEMA, 1999[1].

Following are few advantages of compounding of offences:

Present Circular

Pursuant to the supersession of FEM (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2017[2] (‘TISPRO”)and issuance of FEM (Non-Debt Instrument) Rules, 2019[3] [‘NDI Rules] and FEM (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019[4] [‘MPR Regulations’], RBI has updated the reference of the erstwhile regulations in line with the NDI Rules and MPR Regulations vide RBI Circular No.06 dated November 17, 2020[5] (‘Nov 2020 Circular’).

Additionally, the Nov 2020 Circular does away with the classification of a contravention as ‘technical’, as discussed later in the article.

Lastly, the Nov 2020 Circular modifies the format in which the compounding orders will be published on RBI’s website.

Compounding of contraventions relating to foreign investment

The power to compound contraventions under TISPRO delegated to the Regional Offices/ Sub Offices of the RBI has been aligned with corresponding provisions under NDI Rules and MPR Regulation as under:

| Compounding of contraventions under NDI Rules | |||

| Rule No. | Deals with | Corresponding regulation under TISPRO | Brief Description of Contravention |

| Rule 2(k) read with Rule 5 | Permission for making investment by a person resident outside India; | Regulation 5 | Issue of ineligible instruments |

| Rule 21 | Pricing guidelines; | Paragraph 5 of Schedule I | Violation of pricing guidelines for issue of shares. |

| Paragraph 3 (b) of Schedule I | Sectoral Caps; | Paragraph 2 or 3 of Schedule I | Issue of shares without approval of RBI or Government respectively, wherever required. |

| Rule 4 | Restriction on receiving investment; | Regulation 4 | Receiving investment in India from non-resident or taking on record transfer of shares by investee company. |

| Rule 9(4) | Transfer by way of gift to PROI by PRII of equity instruments or units of an Indian company on a non- repatriation basis with the prior approval of the Reserve Bank. | Regulation 10(5) | Gift of capital instruments by a person resident in India to a person resident outside India without seeking prior approval of the Reserve Bank of India. |

| Rule 13(3) | Transfer by way of gift to PROI by NRI or OCI of equity instruments or units of an Indian company on a non- repatriation basis with the prior approval of the Reserve Bank. | ||

| Compounding of contraventions under MPR Regulations | |||

| Regulation No. | Deals With | Corresponding regulation under TISPRO | Brief Description of Contravention |

| Regulation 3.1(I)(A) | Inward remittance from abroad through banking channels; | Regulation 13.1(1) | Delay in reporting inward remittance received for issue of shares. |

| Regulation 4(1) | Form Foreign Currency-Gross Provisional Return (FC-GPR); | Regulation 13.1(2) | Delay in filing form FC (GPR) after issue of shares. |

| Regulation 4(2) | Annual Return on Foreign Liabilities and Assets (FLA); | Regulation 13.1(3) | Delay in filing the Annual Return on Foreign Liabilities and Assets (FLA). |

| Regulation 4(3) | Form Foreign Currency-Transfer of Shares (FC-TRS); | Regulation 13.1(4) | Delay in submission of form FC-TRS on transfer of shares from Resident to Non-Resident or from Non-resident to Resident. |

| Regulation 4(6) | Form LLP (I); | Regulations 13.1(7) and 13.1(8) | Delay in reporting receipt of amount of consideration for capital contribution and acquisition of profit shares by Limited Liability Partnerships (LLPs)/ delay in reporting disinvestment / transfer of capital contribution or profit share between a resident and a non-resident (or vice-versa) in case of LLPs. |

| Regulation 4(7) | Form LLP (II); | ||

| Regulation 4(11) | Downstream Investment | Regulation 13.1(11) | Delay in reporting the downstream investment made by an Indian entity or an investment vehicle in another Indian entity (which is considered as indirect foreign investment for the investee Indian entity in terms of these regulations), to Secretariat for Industrial Assistance, DIPP. |

Technical contraventions to be compounded with minimal compounding amount

As per RBI’s FAQs[1] whenever a contravention is identified by RBI or brought to its notice by the entity involved in contravention by way of a reference other than through the prescribed application for compounding, the Bank will continue to decide (i) whether a contravention is technical and/or minor in nature and, as such, can be dealt with by way of an administrative/ cautionary advice; (ii) whether it is material and, hence, is required to be compounded for which the necessary compounding procedure has to be followed or (iii) whether the issues involved are sensitive / serious in nature and, therefore, need to be referred to the Directorate of Enforcement (DOE). However, once a compounding application is filed by the concerned entity suo moto, admitting the contravention, the same will not be considered as ‘technical’ or ‘minor’ in nature and the compounding process shall be initiated in terms of section 15 (1) of Foreign Exchange Management Act, 1999 read with Rule 9 of Foreign Exchange (Compounding Proceedings) Rules, 2000.

Nov 2020 Circular provides for regularizing such ‘technical’ contraventions by imposing minimal compounding amount as per the compounding matrix[1] and discontinuing the practice of giving administrative/ cautionary advice.

Public disclosure of compounding order

Compounding order by RBI can be accessed at the RBI website-FEMA tab-compounding orders[1]. In partial modification of earlier instructions issued dated May 26, 2016[2] it has been decided that in respect of the Compounding Orders passed on or after March 01, 2020 a summary information, instead of the compounding orders, shall be published on the Bank’s website in the following format:

| Sr. No. | Name of the Applicant | Details of contraventions (provisions of the Act/Regulation/Rules compounded)

(Newly inserted) |

Date of compounding order

(Newly inserted) |

Amount imposed for compounding of contraventions | Download order

(Deleted) |

It seems that the compounding order will not be available for download.

Conclusion:

The delegation of power is done for enhanced customer service and operational convenience. Revised format of disclosure of compounding orders will be more reader friendly. Delay in filing of forms under MPR Regulations on FIRMS portal is subject to payment of Late Submission Fees (LSF) as per Regulation 5. The payment of LSF is an additional option for regularising reporting delays without undergoing the compounding procedure.

Abbreviations used above:

FIRMS: Foreign Investment Reporting & Management System.

| Our other articles/channel can be accessed below:

1. Compounding of Contraventions under FEMA, 1999- RBI delegates further power to Regional Offices:

2. Other articles on FEMA, ODI & ECB may be access below: https://vinodkothari.com/category/corporate-laws/

3. You Tube Channel: |

[1] https://www.rbi.org.in/scripts/Compoundingorders.aspx

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10424&Mode=0

[1] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10424&Mode=0

[1] https://m.rbi.org.in/Scripts/FAQView.aspx?Id=80 (Q. 12)

[1] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=10190

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11253&Mode=0

[3] http://egazette.nic.in/WriteReadData/2019/213332.pdf

[4] https://www.rbi.org.in/Scripts/BS_FemaNotifications.aspx?Id=11723

[5]https://rbidocs.rbi.org.in/rdocs/notification/PDFs/APDIRS62545AA7432734B31BD5B59601E49AA6C.PDF