NFRA’s Call for a Two-Way Communication: A New Requirement or a Gentle Reminder?

Tagging auditors and TCWG to make amends

– Team Corplaw | corplaw@vinodkothari.com

Introduction

NFRA moved the needle, and it is to be seen if the ocean starts boiling.! A 7th Jan 2026 circular from NFRA, addressed to listed entities and their auditors, seemed like an attention-drawer to standards of auditing which are already there, and yet, the auditing fraternity is holding meetings with boards and senior management of listed entities, to comply with what was always a compliance requirement. Does the 7th Jan circular bring up any new boxes to be ticked, any new procedures to be laid or responsibilities to be reiterated? As we detail out in this article, there may be need for action on several fronts on the part of listed entities – identification of nodal persons, listing developments that need to be communicated, constituting team for responding to the findings of the auditors in course of their audit other than those that sit in the audit report, formation of sub-groups of TCWG, etc.

Admittedly, the NFRA Circular arises from NFRA’s observations, that either the requirements of standards of audit [mainly, SA 260 and SA 265] are either not complied with, or taken lightly. . In view of the principles of law,, as well as the various audit reporting requirements, the National Financial Reporting Authority (‘NFRA’), released a circular January 07, 2026 on ‘Effective Communication Between Statutory Auditors and Those Charged with Governance, Including Audit Committees’ (‘Circular’). The said Circular highlights the existing requirement under the Companies Act, 2013 (‘Act’) as well as the Standards of Auditing for both theStatutory Auditors (‘Auditors’) and Those Charged with Governance (‘TCWG’), including the Audit Committee of having a robust framework of allowing communication on various integral financial and audit related aspects.

In this brief note, we have tried to analyse the Circular to understand its need, the legal framework, and list down actionables for the Companies.

NFRA’s overarching power to deal with violations

The provisions of section 132(4) of the Act provides overarching powers to NFRA being an independent regulator, in respect of matters relating to accounting and auditing, of prescribed classes of entities broadly described as “Public Interest Entities’ (PIE). Being a non-obstante clause, it becomes explicit that the powers vested with NFRA being in the nature of that as powers with a civil court under the Code of Civil Procedure, 1908, supersedes any other legal stance.

The powers ranges in the following manner:

- Powers similar to those vested with a civil court under the Code of Civil Procedure

- discovery and production of books of account and other documents, at such place and at such time as may be specified by NFRA;

- summoning and enforcing the attendance of persons and examining them on oath;

- inspection of any books, registers and other documents of any person referred to in aforesaid clause at any place;

- issuing commissions for examination of witnesses or documents;

- Where professional or other misconduct is proved, have the power to make order for—

- imposing penalty of—

- not less than one lakh rupees, but which may extend to five times of the fees received, in case of individuals; and

- not less than five lakh rupees, but which may extend to ten times of the fees received, in case of firms;

- Debarring the member or the firm from—

- being appointed as an auditor or internal auditor or undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate; or

- performing any valuation as provided under section 247,

for a minimum period of six months or such higher period not exceeding ten years as may be determined

International perspective

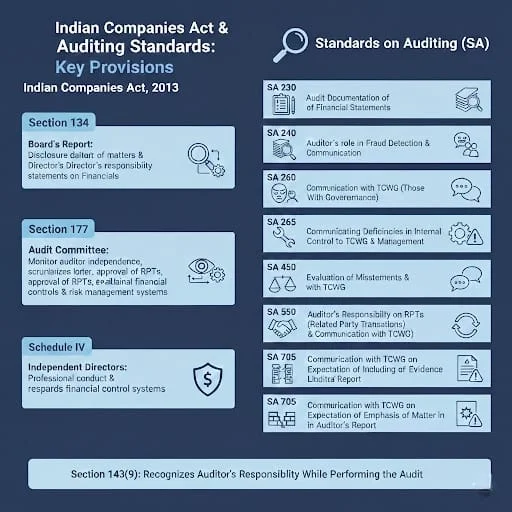

SA 260 (revised) in India is largely modeled on ISA 260, issued by the IAASB, and is replicated in most of the significant countries, albeit with relevant domestic amendments . Australian Auditing Standards ASA 260 requires having effective two-way communication with the TCWG. Even in United States SA 380 – communication with the audit committee casts the responsibility on the auditor to communicate certain matters to those who have responsibility for oversight of the financial reporting process. Further in the UK, ISA (UK) 260 on the same lines recognises the requirement of the communication during the audit by the TCWG. Singaporean authorities also issued the SSA 260, which requires communication deals with communication of TCWG during the course of Audit by the auditors.

NFRA’s Observations – Gaps under the existing practices

As discussed above, the existing need for following an effective two-way communication is based on NFRA’s observations some of which included:

- Entity’s governance structure has either not been evaluated or been done incorrectly leading to incorrect identification of TCWG.

- The communication process with TCWG was incomplete and not properly documented.

- Another major gap in the above process was failure to record the purpose and objective of two-way communication and simply relying on the audit engagement letter.

- Failure to communicate significant matters, including the planned scope and timing of the audit, materiality, key audit matters and significant risks (such as going concern issues, valuation deficiencies and unusual transactions outside the normal course of business

- Communication with the TCWG is not made in the following respects:

- Significant unusual transactions such as supplier and land advances and circuitous dealings with promoter or group‑controlled entities outside the normal course of business.

- Instances of non-compliance that could affect an entity’s licenses to operate were not communicated.

- Deficiencies in the RPT policy and concerns over related party transactions, including significant increases and questions as to whether they were in the ordinary course of business, or whether they were at arm’s length.

- Weaknesses or the absence of internal controls including serious deficiencies in credit policies and the failure of the Risk Management Committee to meet over multiple years.

Some of the Orders given by NFRA can also be referred here below:

| Case title | Issue | Order |

|---|---|---|

| Vikas Proppant and Granite Limited [5th July, 2024] | Among other violation of SAs, auditors failed to determine TCWG and there is no documentation of communication | Penalty of 2 Lakh on Engagement partner(EP) and 3 lakh on audit firm. EP was debarred from being appointed as auditor or internal auditor for a period of two years |

| Sanwaria Consumer Limited[9th September, 2024] | Among other violations, failed to determine TCWG and communicate the responsibilities of auditor, overview of planned scope, timing of audit and deficiencies in internal control and failed to maintain documentation of the same. | Penalty on CA of Rs. 5 lakh and also debarred for a period of one year from being appointed as the auditor or internal auditor and also undertaking audit in respect of financial statements or other activities. |

| M/S Sundaresha & Associates[18th August, 2023] | Among other violations failed to determine TCWG and also failed to communicate with TCWG about the responsibilities of the auditor; overview of planned scope; timing of the audit; and deficiencies in Internal Control, failure to report about siphoning of funds, etc. | Penalty of Rs 1 Crore upon audit firm. A firm is debarred for a period of four years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate. Imposed penalty of 5 lakh upon EP and also debarred for a period of 5 years from being appointed as auditor or internal auditor. |

| CMI Limited26th April, 2024] | Among other violations, failed to determine TCWG, communicate with TCWG about the responsibilities of the auditor, overview of planned scope, timing of the audit and deficiencies in Internal Control and to maintain audit documentations of such activities. | Penalty on firm 50 lakh. Partner penalised for Rs. 10 lakh and also debarred for 2 years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate. |

| Vikas WSP Limited[23rd April, 2024] | Among other violations, failed to have proper documentation of communication with TCWG. | Penalty of Rs. 5 Lakh on firm |

Who can be identified as TCWG?

The first step towards having an effective two-way communication is to know whom to address the communication to. While auditors are known to the auditee, it is imperative for the purposes of having an effective dialogue to know who are the ones falling under TCWG. As per SA 260 revised, TCWG is defined to mean and contain the following elements in case of companies:

- The person(s) with the responsibility

- For overseeing the strategic direction of the entity and obligations related to the accountability of the entity

- Overseeing of the financial reporting process

- May include management personnel, for example, executive members of a governance board of a private or public sector entity, or an owner-manager.

As per the aforesaid definition, persons who have the responsibility over the strategic decisions and are accountable in relation to the affairs of the entity and also oversee the financial reporting process should be considered as a part of the TCWG. Which means can only the Audit Committee be identified as such? Should it also be extended to the entire Board? Or Can certain concerned officials also be part of the TCWG?

As pointed out by NFRA, while several companies have only been identifying their audit committee as TCWG, the language of SA 260 as discussed above, makes it clear that given the overall sense of having the two-way communication in place, the board as a whole should be identified as TCWG. Having said that, even in cases where the Board has delegated this responsibility to the Audit Committee, there needs to be proper scope and flexibility to escalate serious concerns even to the Board as a whole.

Actionables For Companies

Pursuant to the said Circular read along with the provisions of the SAs and CA, 2013 and relevant rules, Companies have to ensure certain actionable in respect of the audit for ensuring there is effective communication. The actionables are mentioned below.

- Proper identification of TCWG: Whether the entire board or only the Audit Committee is required to be identified as TCWG and the same is communicated to the Auditor.

- Ensure a two way communication process with the auditors.

- Communication shall be in writing and properly documented

- Frame policies and processes to implement these requirements in letter and spirit.

- Form of communication:

- In writing

- For oral communication to be documented to include date , time, details of persons involved

- Written communication between auditors and TCWG shall form part of audit work papers and part of the agenda and minutes of the Board or AC meeting held subsequently.

- Presentations in bullet form alone, or communication by emails with a caveat of ‘no comments from the other party is construed as acceptance’, is unacceptable.

- Remarks or comments from TCWG or vice versa should be given on the subject matter raised.

- During the course of communication with the statutory auditor following things must be kept in mind:

- Written communication between auditors and TCWG shall form part of audit work papers and part of the agenda and minutes of the Board or AC meeting held subsequently.

- Presentations in bullet form alone, or communication by emails with a caveat of ‘no comments from the other party is construed as acceptance’ is an unacceptable form of communication.

- Remarks or comments from TCWG or vice versa should be given on the subject matter raised.

- Meetings with Auditors

- TCWG to meet with Auditors at least twice a year

- Once before the commencement of the audit

- Well in advance before the approval of financial statements by TCWG.

- Where auditors request a meeting with TCWG:

- TCWG shall accede, or

- Communicate reasons in writing for declining the request

- Especially in cases where they have reason to believe the existence of fraud or

- Significant weaknesses in internal controls

Preparation of a documented framework

For the purpose of communication with auditors a documented framework needs to be framed. This framework may include the following:

- Objective and purpose of two communications.

- Identification of nodal persons for ensuring an effective two way communication.

- Matters to be communicated by TCWG relevant to the audit

- Summary of key SAs requiring communication of specific matters with TCWG by the Auditors

- Policy and Process of updating or escalating the matters to TCWG about the discussion and communication between

- Nodal officers of TCWG and Auditors

- Subgroups of TCWG and Auditors

- Expected Agenda matters for the meetings.

- Policy and process of documenting and communicating the views/ instructions/ actions of TCWG on the significant matters communicated by the Auditors.

- All significant communications shall be in writing and formally acknowledged by both the Auditor and TCWG, either in the form of minutes of the meeting or letters.

Actionable for the Auditors

In addition to the actionables for the companies to ensure effective communication, the Circular also highlights responsibilities for the auditors. In the course of audit, if the auditor comes across any discrepancies or any significant matter which requires the attention of the TCWG, it must be communicated with the TCWG timely and appropriately.

However, certain specific responsibilities/actionables has also been specifically prescribed which are mentioned below:

- Meet with TCWG in person or virtually at least twice a year as per below mentioned timeline:

- Once before the commencement of the audit.

- Well in advance before approval of financial statements by TCWG.

- Auditor must ensure certain specific points must be communicated with TCWG:

- Significant difficulties encountered during the audit.

- Significant transactions or events where management felt difficulties identifying appropriate accounting policies and standards and the auditor’s view on the same.

- Significant and material weakness in internal financial controls.

- Compliance with the Independence and Code of Ethics

- Audit Strategy and Audit Planning.

- Auditor while doing the audit must communicate the following specifically:

- Deficiencies in related party transaction policy and issues relating to related party transactions.

- Significant unusual transactions such as circuitous dealing with promoter or group related entities

- Instances of non-compliance must be communicated.

- Discuss with the auditor at the start of the financial year:

- Planned scope and timing of audit

- Expectation of two way communication

Matters to be communicated to TCWG

Please refer to A9−A36 of SA 260(revised) as issued in May 2016, dealing with the matters to be discussed with and communicated between the Auditors and TCWG. These matters include the following:

- The Auditor’s Responsibilities in Relation to the Financial Statement Audit

- Planned Scope and Timing of the Audit

- Significant Findings from the Audit

- Auditor Independence

- Significant Qualitative Aspects of Accounting Practices

- Significant Difficulties Encountered during the Audit

- Significant Matters Discussed, or Subject to Correspondence with Management

- Circumstances that Affect the Form and Content of the Auditor’s Report

- Other Significant Matters Relevant to the Financial Reporting Process

- Supplementary Matters

In addition to the matters as listed in the SA 260(revised), reference shall be made to para 5.6 of the said NFRA Circular, which further lists items that must invariably form part of the agenda matters for interactions between the Auditors and TCWG.

Role of the Company Secretary in implementing the Circular

Generally, there is a confusion whether company secretaries should be designated as the TCWG. Reading the definition of TCWG provided in para 10(a) of SA 260 the persons who have the responsibility of overseeing the strategic direction or financial reporting process and are accountable in relating to the affairs of the entity are designated as the TCWG. In this context the members of the board or subgroup of the board are designated as the TCWG and which again shall be aligned with the auditors.

Given the intent of requirement for facilitating two-way communication as well as the scope of the said requirements, it is understood that the instant circular deals with finance and audit controls. Further, referring to the definition of TCWG in para 10(a) SA 260 (Revised), the following is included:

“The person(s) or organization(s) (e.g., a corporate trustee) with responsibility for overseeing the strategic direction of the entity and obligations related to the accountability of the entity. This includes overseeing the financial reporting process. For some entities, those charged with governance may include management personnel, for example, executive members of a governance board of a private or public sector entity, or an owner-manager.

XXX”

The above definition makes it clear that TCWG primarily includes the members of the Board or of a sub-group thereof. At the most, given the coverage of ensuring and overseeing financial controls, heads of the finance and audit function may also be considered to be part of TCWG.

Concluding Remarks – What is two-way?

SA 260 and the Circular lay great stress on documentation. Documentation is not the essence of audit; however, documentation is the only way to audit the effectiveness of the audit. Audit documentation is the principal record of auditing procedures applied, evidence obtained, and conclusions reached by the auditor in the engagement.

Auditing is not a mere bunch of auditors’ observations; in order to arrive at the conclusions, the auditor must have had a series of discussions with the auditee. Key audit matters are discussed typically with the audit committee; these matters arise from observations and management discussions. Many draft matters are settled in the course of discussions – the fact that a matter was resolved on the basis of explanations provided should all find its place in documentation.

Additionally, two-way communication also involved the auditee communicating significant developments – strategic changes, internal findings on fraud or error, noticed incidents of breach of internal control, etc. The expectation that these matters will be expeditiously communicated by the TCWG to the auditor is a part of the communication framework referred to in para 5.3 of the Circular.

NFRA’s nudge is quite significant, as it has caused most auditors to engage in discussions with the TCWG to move towards effective communication. The only hope is that the impression of compliance does not overtake the spirit of effective audit itself.

Read More:

Growing relevance of Audit Committee and IDs

Lending to your own: RBI Amendment Directions on Loans to Related Parties

Thank you for your response.

Please note that in the above article under the section role of the company secretary in implementing the circular, it is mentioned that

“the above definition makes it clear that TCWG primarily includes the members of the Board or of a sub-group thereof. At the most, given the coverage of ensuring and overseeing financial controls, heads of the finance and audit function may also be considered to be part of TCWG.”

However, in the above response it is mentioned that KMP not being member of the Board cannot form part of TCWG.

Request you to kindly guide on the same.

Please note that given the context of identification of TCWG for companies, it should either be the entire Board or its sub-committee of the board which should be identified as such and also aligned with the auditors of the Company. Further, the article is also updated to reflect this understanding. You may also refer to our FAQs [https://vinodkothari.com/wp-content/uploads/2026/03/FAQs-on-NFRA-1.pdf] where we have dealt with this question.

1. Can any other officer of the Company such as CFO form part of TCWG (i.e. sub committee of Board identified as TCWG)

2. Can you also please highlight what is the concept of Nodal Officer and whether he can any senior management person who can act as Nodal Officer or he can only be a Director?

NFRA, vide its Circular dated January 07, 2026, has clarified that the Board of Directors shall be regarded as TCWG. It is further clarified that TCWG may also comprise a subset of the Board, such as the Audit Committee or certain members of the Board.

Accordingly, it is evident that only members of the Board of Directors can constitute TCWG, and therefore, Key Managerial Personnel such as the Chief Financial Officer (CFO), not being a member of the Board, cannot form part of TCWG.

The appointment of Nodal officer for communication is a direct recommendation from the NFRA circular which is aimed at strengthening the bridge between auditors and TCWG. To maintain two-way communication NFRA has recommended identifying nodal officer for communication. As per the NFRA Circular, nodal officer for this purpose may include IDs as well as Non-IDs. Accordingly, while nodal officers for the purpose of the NFRA Circular can only be board members, however, in our view, members from finance team may assist the nodal officer for coordination purposes with the team of Statutory Auditor for the purpose of enabling two-way communication.