APPLICATION UNDER SARFAESI- A Liberal Approach by the Supreme Court

By Richa Saraf, (legal@vinodkothari.com) Read more →

By Richa Saraf, (legal@vinodkothari.com) Read more →

By Richa Saraf, (legal@vinodkothari.com)

By Parul Bansal, (corplaw@vinodkothari.com)

With the development of the economic conditions of the country, various investors including the retail investors are stepping into the securities market with the intention to earn higher return on their investments which has lead to large portion of their income being invested in shares, bonds or securities of listed companies. At this juncture, return on their investment is proportionate to the growth of listed companies. Therefore, their destiny in the stock market lies at the mercy of management and promoters of listed companies.

Stock Exchange Board of India (“SEBI”) with an endeavor to prevent the investors from the monopoly of the listed companies and to debar/prevent the undesirable/illegal transactions has enacted Securities Contract (Regulation) Act, 1956 (“SCRA, 1956”) and Securities Contract (Regulation) Rules, 1957 (“Rules, 1957”) thereof.

Listed Companies are those companies of which shares are listed on the stock exchange and certain percentage of such shareholding is available for the public to trade in with transparency and liquidity. If large portion of the shareholding of listed companies remain blocked in the hands of the promoters, subsidiary or associate company then the intent of listing such securities is breached and becomes redundant. The promoters will be at liberty to manipulate the price and the market tricking will be easy. This will also reduce the floating capacity of the securities of the company due to less liquidity. Ministry of Finance vide press release dated June 4, 2010 has also stated that:

“A dispersed shareholding structure is essential for the sustenance of a continuous market for listed securities to provide liquidity to the investors and to discover fair prices. Further the larger the number of shareholders, the less is the scope for price manipulation.”

To prevent such abuse, sub-rule 19 of the Rules, 1957 specifies the conditions for initial and continuous listing of a company.

As per regulation 19(2)(b) of the Rules, 1957, any company proposing to list its securities shall maintain MPS as mentioned below based upon the post issued share capital of the company:

| Post issued share capital at offer price | MPS (minimum) | |

| 1 | Less than or equal to INR 600 crores | 25% of each class or kind of equity shares or

debenture convertible into equity shares issued by the company |

| 2 | More than INR 600 to INR 4000 crores | Such % of each class or kind of equity shares or debentures convertible into equity shares issued by the company equivalent to the value

of four hundred crore rupees |

| 3 | More than INR 4000 crores | 10% of each class or kind of equity shares or debentures convertible into equity shares issued by the company |

| In case of 2 and 3, company shall attain MPS equal to 25% within 3 years from the date of listing its securities | ||

SEBI has, vide circular dated March 10, 2017, laid down criteria for Schemes of Arrangement by Listed Entities and relaxation under Rule 19 (7) of the Securities Contracts (Regulation) Rules, 1957 (SCRR). Further, to align with the rules of Rule, 1957, amendments were carried out therein through circular dated September 21, 2017.

Pursuant to aforesaid circulars, any listed issuer may for the purpose of arrangement submit a draft scheme of arrangement under sub-rule 19 of Rules, 1957 for seeking relaxation from the applicability of strict provisions of sub-rule 19(2) of Rules, 1957, for listing of its equity shares on a recognized Stock Exchange without making an initial public offer, on satisfying the conditions as mentioned in para III of Annexure I thereof. In terms of such conditions at least 25% of the post-scheme paid up share capital of the transferee entity shall comprise of shares allotted to the public shareholders in the transferor entity. However, on fulfillment of following condition, requirement to attain such MPS may be waived off:

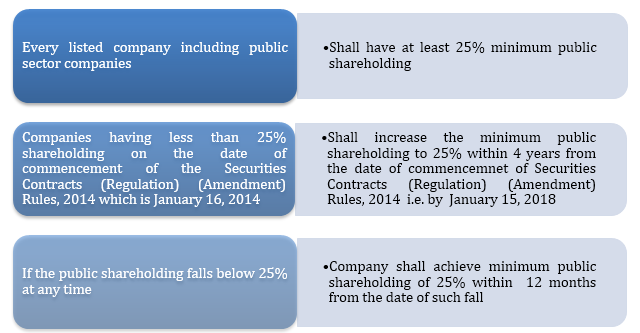

Pursuant to sub-rule 19A of the Rules, 1957 every listed company including the Public Sector Company shall maintain MPS of 25% of the total shareholding of the Company. Initially, limit for the Public Sector Companies was fixed at 10% but later on the same was also increased from 10% to 25% to provide equal footing to listed companies and PSUs.

Pursuant to proviso of sub-rule 19A of Rules, 1957, every listed company which is not meeting the minimum public shareholding specified under sub-rule 19 of the Rules, 1957 shall in accordance with the provision of sub-rule 19A accomplish the same within the stipulated time period which is 4 year from the date of commencement of SCRA Amendment Rules, 2014 i.e. by January 15, 2018. Earlier the time specified was upto January 15, 2017 and listed companies failing to comply with the same has faced severe consequences in past. Albeit, strict steps have been taken by SEBI against such companies, public shareholding of such companies was still below the requirement. Therefore, SEBI has, once again vide circular on July 03, 2017, extended the time limit for achieving the minimum public shareholding by one year i.e. January 15, 2018.

This extension of time yet again by SEBI is a clear indication of the its accommodative and perceptive regulatory approach and takes cognizance of the need for a reasonable timeframe within which non-compliant companies may take remedial action with respect to public holding requirements. SEBI has not only increased the time limit for bringing the public shareholding within specified limits but has also amended various Regulations and Acts thereof for achieving the requirement of minimum public shareholding.

SEBI has vide circular dated December 16, 2010 and August 29, 2012 specified the methods for complying with the minimum public shareholdings such as issuance of shares to public through prospectus, offer of shares held by promoters to public, right issues/ bonus issue to public shareholders with promoters or promoter group shareholders forgoing their entitlement, etc.

Subsequently, another circular was issued by SEBI on February 08, 2012 through which listed companies were allowed to achieve minimum public shareholding through institutional placement programme. Along with the aforesaid, SEBI has also specified that listed companies desirous of achieving the minimum public shareholding may approach SEBI with the appropriate details and the same will be entertained by it on the basis of merits.

Despite aforementioned efforts of the SEBI to facilitate achieving minimum shareholding, various companies have not complied with the same. As a result SEBI has taken stern actions like freezing of voting rights, delisting of securities, exclusion of scrips from F&O segments etc.

SEBI has once again vide circular dated October 10, 2017[1], in order to bring uniformity of approach in enforcement of MPS norms and to ensure compliance with same, laid down following procedure:

Provided that where it is observed that the listed entity has adopted a method for complying with MPS requirements which is not prescribed by SEBI under clauses (2)(i) to (vi) under SEBI circular[1] dated November 30, 2015 and approval for the same has not been obtained from SEBI under clause 2 (vii) of the said circular, the recognized stock exchanges shall refer such cases to SEBI.

Upon intimation of compliance and on being satisfied, RSE shall remove the aforementioned restriction levied on the listed entities, its promoter, promoter group and directors.

Aforementioned actions taken by SEBI are without prejudice to its power to take action under the securities laws for violation of the MPS requirements.

Colombo Stock Exchange

Pursuant to rule 7.13 of the listing rules[2] of the Colombo Stock Exchange, every company listed on the main Board shall maintain a minimum public shareholding as stipulated therein. Previously, such listed companies were required to comply with this requirement of minimum public shareholding by December 31, 2016. However, likewise SEBI, Stock Exchange Commission in consultation with Colambo Sock Exchange has extended the timeline to June 30, 2017 for the listed companies not complying with the requirement of minimum public shareholding.[3]

Europeon Union (Euronext)

Pursuant to the regulations of Euronext Amsterdam[4], minimum public shareholding maintained by the companies shall be 25% of the issued shares of the company. Unlike, SEBI, Colambo Stock Exchange, Euronext considers the free float/liquidity available for the security of the company. In case a large number of shares of the company are available to public, ensuring enough liquidity for the such shares, irrespective of the percentage, minimum public shareholding may go below 25% subject to the condition that minimum public shareholding shall never be lower than 5% and the free float shall always represent at least EUR 5 million (based on the offering price).

[1] http://www.bseindia.com/downloads/whtsnew/file/Manner%20of%20achieving%20MPS%20301115.pdf

[2] https://cdn.cse.lk/pdf/Section-7.pdf

[3] https://cdn.cse.lk/cmt/upload_cse_report_file/directives_24_18-11-2016.pdf

[4] https://uk.practicallaw.thomsonreuters.com/9-572-8048?transitionType=Default&contextData=(sc.Default)&firstPage=true&bhcp=1

By Richa Saraf, (legal@vinodkothari.com)

The Hon’ble National Company Law Appellate Tribunal (NCLAT) has held that ‘Power of Attorney’ holders are not authorized to present Insolvency Application under Section 7, 9 and 10 of the Insolvency and Bankruptcy Code, 2016 (IBC). It is only authorized representatives, duly authorized by Board Resolution, who are authorized to present the same. The same is based on a simple rationale that company being juristic person only acts through its Board of Directors, who can exercise all powers which company is entitled to and they may vide resolution authorize any person to present application. Further, officers authorized by Board cannot give Power of Attorney to any other person. Below, we discuss the ruling. Read more →

By CS Vinita Nair, (corplaw@vinodkothari.com)

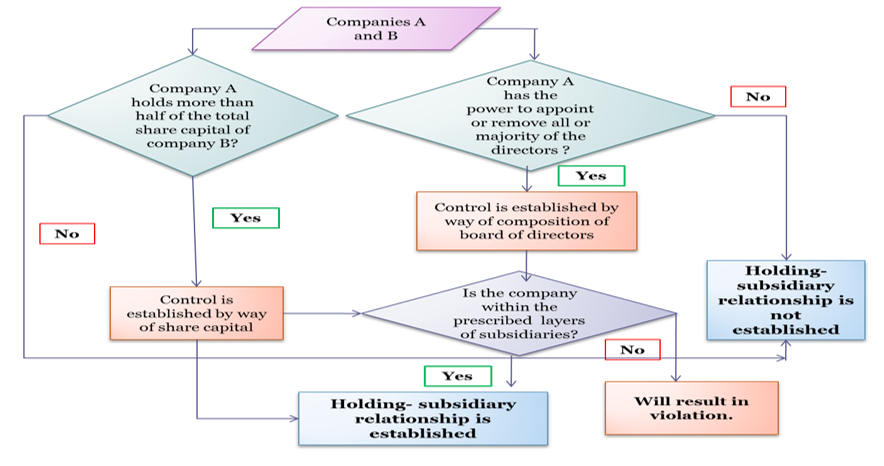

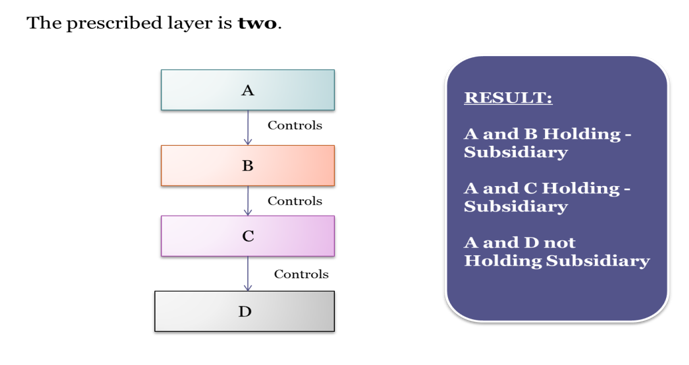

MCA has issued a notification notifying the Companies (Restriction on Number of Layers) Rules, 2017[1], imposing a limit of two layers of subsidiaries which shall be effective from September 20, 2017[2]. Earlier, MCA vide public notice dated 1 June 28, 2017[3] had conveyed its intent of issuing a notification proposing amendments to the Companies (Specification of Definitions Details) Rules, 2014 containing the restriction on layers of subsidiaries beyond prescribed number and had invited suggestions on the draft notification. This write up initially discusses the conditions imposed and thereafter analyses the permitted combinations.

Proviso to Section 2 (87) along with explanation (d) was proposed to be omitted in Companies (Amendment) Bill, 2016. However, in view of reports of misuse of multiple layers of companies, where companies create shell companies for diversion of funds or money laundering, MCA has decided to retain the provisions and commence the aforesaid proviso and explanation. Further, MCA had no intent to exempt private companies from the requirement as well. Companies (Amendment) Bill, 2017 as passed by Lok Sabha omitted the amendment proposed in Proviso to Section 2 (87).

Figure 5 of Taxmann’s Your Queries on Companies Act, 2013

Rule 2(2) of Companies (Restriction on number of layers) Rules, 2017 shall not apply to following classes of companies, namely:-

(a) a banking company;

(b) a non-banking financial company as defined in the Reserve Bank of India Act, 1934 (2 of 1934) which is registered with the Reserve Bank of India and considered as systemically important non-banking financial company by the Reserve Bank of India; (Nothing specified in relation to housing finance companies/ NBFC CICs).

(c) an insurance company being a company which carries on the business of insurance in accordance with provisions of Insurance Act, 1938 and Insurance Regulatory Development Authority Act, 1999;

(d) a Government company referred to in clause (45) of section 2 of the Act.

Exemptions in cases of Housing Finance Companies, Core Investment Companies as well as Non-Operative Financial Holding Company, Companies that become subsidiary entities pursuant to lenders acquiring majority of shareholding in the borrowing entity as a measure to deal with stressed assets in accordance with the guidelines issued by the Reserve Bank of India from time to time are missed out in the Rules notified.

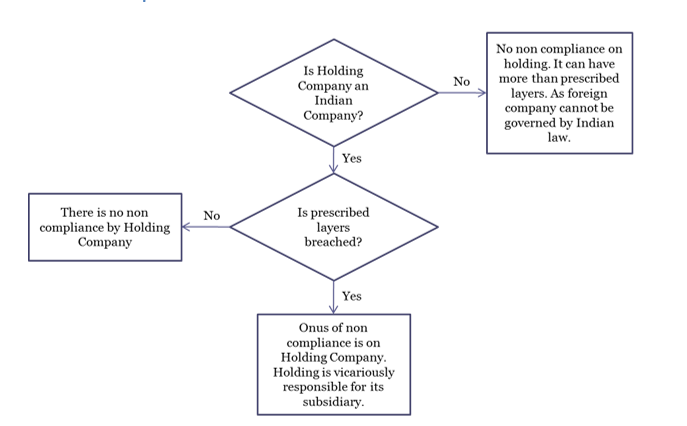

First proviso to Rule 2 of the Rules provides exemption to a Company from acquiring a company incorporated in a country outside India with subsidiaries beyond two layers as per the laws of such country.

The exemption in case of acquiring of subsidiaries incorporated outside India should be extended equally to subsidiaries freshly incorporated outside India. There need not be a distinction in acquisition and incorporation of subsidiary outside India. Either a company may acquire a subsidiary outside India which in turn has several layers of downstream investment or it may float a subsidiary outside India which will keep on further incorporating or acquiring subsidiaries outside India.

It cannot be interpreted that a Company incorporating subsidiaries outside India will have to adhere to the restriction of layers even if the same is permitted as per law of that country.

One layer which consists of one or more wholly owned subsidiary or subsidiaries shall not be taken into account while computing the number of layers. The proposed Rule provided the explanation to the effect that one layer which is represented by a wholly owned subsidiary shall not be taken into account.

‘Layer’ cannot mean ‘Layers’ based on interpretation that singular includes plural. Therefore, it should not be read as any layer represented by a wholly owned subsidiary. The whole purpose will get defeated if companies are allowed to incorporate layers of wholly owned subsidiaries without any restriction.

It is very pertinent to ponder whether the wholly owned subsidiaries can be at layer not immediately following the layer of holding company.

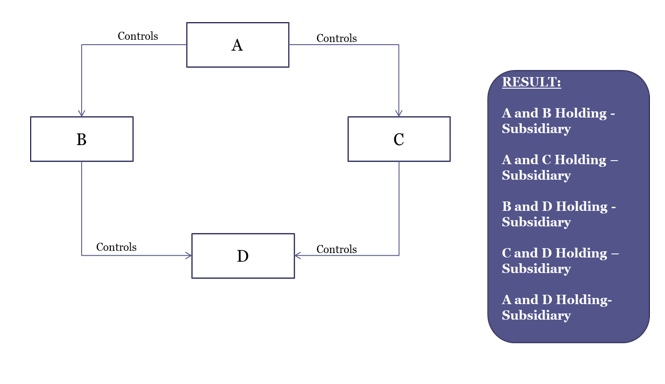

Example 1: Company ‘A Ltd’ has a subsidiary ‘B Ltd’ which in turn has a subsidiary ‘C Ltd’. ‘C Ltd’ forms a wholly owned subsidiary ‘D Ltd’. How can Company ‘A Ltd’ avail the exemption for the layer represented by ‘D Ltd’ which is not wholly owned subsidiary of ‘A ltd’.

Example 2: Company ‘A Ltd’ has wholly owned subsidiaries ‘B Ltd’ and ‘C Ltd’. Both of these wholly owned subsidiaries hold shares in ‘D Ltd’ in the ratio of 60% and 40% respectively. Thereafter, ‘D Ltd’ forms a subsidiary ‘E Ltd’. In this case, the layer represented by ‘B Ltd’ and ‘C Ltd’ shall not be considered.

Therefore, the layer of wholly owned subsidiary has to reflect in the first layer and not thereafter in order to avail the exemption.

Similar restriction on number of layers of investment companies has already been in force under Section 186 (1). The provisions of this rule shall not be in derogation of the proviso to sub-section (1) of section 186 of the Act.

The holding companies, other than exempted companies, that breach the conditions of layers of subsidiaries as on the date of commencement of provision are prohibited from incorporating additional layer of subsidiaries.

Such holding companies shall file return in Form CRL-1 with the Registrar within a period of 150 days from the date of publication of these rules in Official Gazette. The form requires specifying layer number of the subsidiary and percentage of shares held by holding company.

The Rules further provide that, such Company shall not, in case one or more layers are reduced by it subsequent to the commencement of these rules, have the number of layers beyond the number of layers it has after such reduction or maximum layers allowed in sub-rule (1), whichever is more.

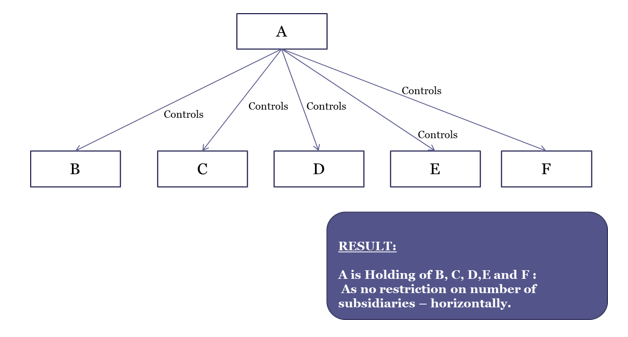

All the below mentioned structures are permitted and well in compliance

Figure 9 of Taxmann’s Your Queries on Companies Act, 2013

Figure 9 of Taxmann’s Your Queries on Companies Act, 2013

Case 1:

Figure 8 of Taxmann’s Your Queries on Companies Act, 2013

In the aforesaid structure, if we consider on as is basis, there exists more than 2 layers of subsidiaries. Therefore, an existing company cannot go beyond ‘D’. Once the provisions are enforced, an existing holding company A will not be able to float ‘D’ unless any exemptions/ relaxations become applicable.

Case 2 – ‘B’ is a wholly owned subsidiary of ‘A’:

In that case, the structure is permissible.

Case 3 –’C’/ ‘D’[1] is a wholly owned subsidiary of ‘A’:

In that case, the structure is not permissible for reasons stated above.

Case 4 – ‘B’/’C’ is a subsidiary incorporated outside India:

Currently, the wording of draft rule prescribes ‘acquired’ subsidiaries to be exempted. However, there is no reason to infer that the benefit cannot be extended to subsidiaries incorporated outside India if the laws of host country permit the same.

Case 5 – ‘B” is a subsidiary acquired outside India while ‘C’ and ‘D’ and subsidiaries of ‘B’ incorporated in India

So ‘A’, ‘C’ and “D’ are companies incorporated in India while ‘B’ is a subsidiary outside India. The exemption cannot be extended to ‘C’ and ‘D’ merely because it’s immediately holding company is a subsidiary acquired outside India. Therefore, the limit is likely to be breached unless ‘B’ or ‘C’ or ‘D’ is a wholly owned subsidiary.

Case 6 – ‘A’/‘B’/’C’ fall under exempted companies:

In that case, the restriction shall not apply.

Case 7 – ‘B’/’C’/ ‘D’ is an LLP:

The expression ‘company’ includes body corporate. Therefore, an existing company cannot go beyond ‘D’. Once the provisions are enforced, an existing holding company A will not be able to float ‘D’ unless any exemptions/ relaxations become applicable.

[1] Either of ‘C’ or ‘D’

Figure 7 of Taxmann’s Your Queries on Companies Act, 2013

If any company contravenes any provision of these rules the company and every officer of the company who is in default shall be punishable with fine which may extend to ten thousand rupees and where the contravention is a continuing one, with a further fine which may extend to one thousand rupees for every day after the first during which such contravention continues.

[1] http://egazette.nic.in/WriteReadData/2017/179104.pdf

[2] http://egazette.nic.in/WriteReadData/2017/179105.pdf

[3] http://www.mca.gov.in/Ministry/pdf/Notice_29062017.pdf

[4] Either of ‘B’ or ‘C’ or ‘D’

By Mayank Agarwal & Anita Baid (finserv@vinodkothari.com)

Peer to Peer lending (P2P Lending) is a virtual marketplace which connects borrowers and lenders online by providing quick funds to borrowers and high returns to lenders. The borrower can raise fund by borrowing from a single lender or a group of lenders. The accelerated growth in P2P Lending platforms was recognized for the first time by the Reserve Bank of India (RBI) in its First Bi-monthly Monetary Policy Statement, 2016-17[1]. Read more →

By Nidhi Bothra, (nidhi@vinodkothari.com)

In March, 2016 a committee was constituted under the Chairmanship of Mr. Ajay Tyagi to draft and submit a bill on resolution of financial firms. In September, 2016, the Committee submitted its report and bill which was titled as “The Financial Resolution and Deposit Insurance Bill, 2016”[1] (Bill 2016). The objective of the Bill, 2016 was to provide for a framework for safeguarding the stability and viability of financial services providers and to protect the interest of the depositors, as the name of the bill also suggests[2].

The Financial Resolution and Deposit Insurance Bill, 2017[3] (Bill, 2017) is formulated to provide resolution to certain categories of financial service providers in distress; the deposit insurance to consumers of certain categories of financial services; designation of systemically important financial institutions; and establishment of a Resolution Corporation for protection of consumers of specified service providers and of public funds for ensuring the stability and resilience of the financial system and for matters connected therewith or incidental thereto.

The proposed legislation together with the Insolvency and Bankruptcy Code, 2016 is expected to provide a comprehensive resolution mechanism for the economy.

The existing draft of the Bill, 2017 has been referred to a Joint Parliamentary Committee of both the Houses, under the Chairpersonship of Shri Bhupender Yadav, for examination and presenting a Report to the Parliament.

The Bill is divided into several chapters, which deal with establishment of a Resolution Corporation, its powers, management and functioning which is broadly to function along with the appropriate regulator[4] of financial services provider, classification of persons as systematically important financial institutions, deposit insurance, restoration and resolution plan, method of resolution, liquidation etc.

The brief highlights of the Bill[5], 2017 are as follows:

The classification of a specified service provider into any of the categories of risk to viability except the category of critical risk to viability under section 45, shall be kept confidential by the appropriate regulator, the Corporation and by all relevant parties.

6. Categorisation of specified service providers under risk to viability categories —

7. Restoration and Resolution Plan — Any specified service provider, classified in the category of material or imminent risk to viability shall submit a restoration plan to the appropriate regulator and a resolution plan to the Corporation within ninety days of such classification. Every restoration plan will prescribe for the details of restoring category to low moderate and resolution plan on who resolution will be achieved.

Where a systemically important financial institution is classified in the category of low or moderate risk to viability, it shall submit the information required under this subsection assuming that it is classified in the category of material or imminent risk to viability.

Where the Resolution Corporation determines that liquidation is the most appropriate method for the resolution of a specified service provider, notwithstanding anything in any other law for the time being in force relating to liquidation and winding up, the Corporation shall make an application to the Tribunal for an order of liquidation in respect of such specified service provider.

The detailed actions as prescribed under the Bill for various categories of risks is tabulated in Annexure I to this note.

The Bill, 2016 aimed at including all NBFCs its foray. Bill, 2017 only intends to cover such NBFCs and other entities in the group, if such NBFC is classified on high risks to viability categories. This was an important and a necessary change from the Bill, 2016.

All the NBFCs, big and small will be continued to be monitored by the appropriate regulators, however, matters will get escalated only if they are on the risks to viability meter. Similar would be the case with other financial services providers as well.

Some key issues that the Bill, 2017 does not address or overlook are as follows:

For both categories of risks to viability, there can be strong intervention of the authorities in running of the business itself. One may find it difficult to find the distinction between the two categories of the risks to viability as the action taken by the authorities and from the specified service providers seems to be almost similar.

In case an entity is categorised as critical risk to viability, the turnaround of the resolution plan is to be carried out within one year, else the Resolution Corporation may require the liquidation of the entity. The entities, in determination here have an element of systemic risks and therefore liquidation of such entities can have daunting consequences on the economy. The provision for triggering liquidation should be well defined or determined in consultation with the Central Government.

4. Rule-making – The devil, as they say, lies in the details. A lot of actions to be taken in each of the risks categorisation will come by way of rule-making. This will determine the effectiveness of the resolution plans and restoration plans prescribed in the Bill, 2017.

5. Existing resolution mechanisms – The appropriate regulators have introduced several policy initiatives and resolution guidance and schemes for restructuring of stressed assets, special restructuring norms, strategic restructuring norms, corporate debt restructuring wherein the entities were required to submit resolution/ restructuring/ restoration plans within certain timeframes. The experience with these guidelines have indicated the failure of these guidelines and schemes to provide for a resolution plan within the dedicated time frame and also restoring the position of the entities.Therefore, appropriate learnings from those guidelines should also be reflected in the Bill,2017.

| SL no. | Category of risk to viability (Section 36) | Categorised by ** | Immediate action to be taken by the specified service provider | Continued Action required by the specified service provider | Action taken by appropriate regulator and/ or corporation |

| 1 | Low | Appropriate Regulator | No Action taken, regular monitoring of the activities of the entity may be conducted.

Where a SIFI is classified in the category of low or moderate risk to viability, it shall submit the information required under section 39 (2) assuming that it is classified in the category of material or imminent risk to viability. |

||

| 2 | Moderate | Appropriate Regulator | No Action taken, regular monitoring of the activities of the entity may be conducted.

Where a SIFI is classified in the category of low or moderate risk to viability, it shall submit the information required under section 39 (2) assuming that it is classified in the category of material or imminent risk to viability. |

||

| 3 | Material | Resolution Corporation or Appropriate Regulator | Submit a restoration plan[12] to the appropriate regulator and a resolution plan[13] to the resolution corporation within 90 days of such classification.

A copy of the restoration plan and resolution plan to be submitted to the resolution corporation and appropriate regulator respectively, within 15 days of the first submission, thereof. Every systemically important financial institution shall submit a restoration plan to the appropriate regulator and a resolution plan to the Corporation within ninety days of its designation under section 25. |

Every restoration plan or resolution plan shall be revised annually and the appropriate regulator and the Corporation shall be informed of such revised restoration plan, within seven days of the revision.

Every material change shall be immediately informed to the appropriate regulator and the Corporation. |

Additional inspection may be carried out to monitor the risk to viability.

Appropriate regulator may prevent entity from taking certain business decisions including declaration of dividend, establishing new business or acquiring new clients, undertaking related party transactions, increasing liabilities etc. Appropriate regulator may require the entity to increase capital, sell assets etc. |

| 4 | Imminent | Resolution Corporation or Appropriate Regulator

Or If the specified service provider has not submitted the restoration plan or resolution plan within prescribed time frame. |

Submit a restoration plan to the appropriate regulator and a resolution plan to the resolution corporation within 90 days of such classification.

A copy of the restoration plan and resolution plan to be submitted to the resolution corporation and appropriate regulator respectively, within 15 days of the first submission, thereof. Every systemically important financial institution shall submit a restoration plan to the appropriate regulator and a resolution plan to the Corporation within ninety days of its designation under section 25. |

Every restoration plan or resolution plan shall be revised annually and the appropriate regulator and the Corporation shall be informed of such revised restoration plan, within seven days of the revision.

Every material change shall be immediately informed to the appropriate regulator and the Corporation. |

The resolution corporation may appoint an officer to inspect the functioning of the entity and act as an observer.

The corporation may prevent the entity from accepting funds, declaring dividend, acquiring new businesses or new clients, undertake related party transactions etc. The corporation may require the entity to infuse new capital or sell identified assets etc.

A specified service provider classified in the category of imminent risk to viability shall, if it is not a SIFI, submit a resolution plan to the Corporation within 90 days.

|

| 5 | Critical | Resolution Corporation or Appropriate Regulator – effective from the date of publication in official gazette | N.A. | N.A. | Corporation shall be deemed to be the administrator[14] and may take the following actions:

a. resolve the issue through a scheme or merger or amalgamation or bail-in instrument. b. Transfer whole or part of assets/ liabilities to another person c. Create a bridge service provider d. Cause liquidation of the entity e. No legal action or proceeding including arbitration shall commence or continue until conclusion of resolution. f. No repayment or acceptance of deposit shall be made or liabilities incurred. g. temporarily prohibit (not exceeding 2 business days) by an order in writing, the exercise of such termination rights of any party to such specified contract with the relevant specified service provider or its associate company or subsidiary License granted to the entity by the appropriate regulator may be withdrawn or modified.

|

[1] http://dea.gov.in/sites/default/files/FRDI%20Bill-27092016_1.pdf

[2] See our article titled – Financial Resolution and Deposit Insurance Bill: Implications for NBFCs, by Vinod Kothari and Niddhi Parmar, here https://vinodkothari.com/blog/financial-resolution-and-deposit-insurance-bill-implications-for-nbfcs-by-niddhi-parmar/

[3] http://164.100.47.4/BillsTexts/LSBillTexts/Asintroduced/165_2017_LS_Eng.pdf

[4] Appropriate Regulator is defined in First Schedule to the Bill, 2017 to include a) RBI, b) IRDA, c) SEBI, d) Pension Fund Regulatory Development Authority or any other regulator as notified by the Central Government.

[5] http://164.100.47.4/BillsTexts/LSBillTexts/Asintroduced/165_2017_LS_Eng.pdf

[6] Financial services provider categorised as specified service providers and SIFIs fall within the purview of the Resolution Corporation. The detailed mechanism of monitoring is discussed further in the highlights.

[7] A specified service provider is a person as defined in Second Schedule to Bill, 2017 and includes

[8] As defined in Section 2 (19) of the Bill, 2017 — means any banking institution, that has obtained deposit insurance under sub-section (3) of section 33. Section 33 (3) states that every banking institution that has been granted a banking license by the appropriate regulator shall be deemed to be categorised as insured service provider for obtaining deposit insurance under the Act.

[9] Insured service provider is a banking institution that has obtained deposit insurance

[10] To qualify as an SIFI, the Central Government will consider the size, complexity of the financial service provider, the nature and volume of transactions undertaken, interconnectedness with other financial service providers and nature of services offered and possibility of substitution such business.

[11] The categorisation are based on assessment of the following parameters:

(a) adequacy of capital, assets and liability; (b) asset quality; (c) capability of management; (d) earnings sufficiency; (e) leverage ratio; (f) liquidity of the specified service provider; (g) sensitivity of the specified service provider to adverse market conditions; (h) compliance with applicable laws; (i) risk of failure of a holding company of a specified service provider or a connected body corporate in India or abroad; and (j) any other attributes as the Corporation deems necessary

[12] A restoration plan as per the provisions of Section 39, will contain details of assets and liabilities of the entity, including contingent liabilities, steps to be taken by the entity to move to moderate classification at least, time frame within which such restoration plan will be executed and other information relevant for the appropriate regulator to assess the plan.

[13] A resolution plan, as per the provisions of Section 40, will contain details of assets and liabilities of the entity, identification of critical functions of the specified service provider, access to financial market infrastructure services, either directly or indirectly, strategy plans on exiting the resolution process and any other relevant information.

[14] The resolution plan must be completed within one year from the date of classification into critical risk to viability. Where the plan is completed within one year and the Corporation deems necessary, it shall require liquidation of the entity.