Regulator’s move to repair the NBFC sector

-Mridula Tripathi

The evolving impact on people’s health has casted a threat on their livelihoods, the businesses in which they work, the wider economy, and therefore the financial system. The outbreak of this pandemic is nothing like the crisis faced by the economies in the year 2007-08 and imperils the stability of the financial system. The market conditions have forced traders to take aggressive steps exposing the system to great volatility thereby resulting in crashing asset values. Combating the pandemic and safeguarding the economy, the financial sectors across the globe have witnessed numerous reforms to hammer the aftermaths of the global crisis. Read more →

Guidance on money laundering and terrorist financing risk assessment

-Financial Services Division (finserv@vinodkothari.com)

Background

The Reserve Bank of India (RBI) introduced an amendment[1] to Master Direction – Know Your Customer (KYC) Direction, 2016 (‘KYC Directions’)[2] requiring Regulated Entities (REs) to carry out money laundering (ML) and terrorist financing (TF) risk assessment exercises periodically. This requirement shall be applicable with immediate effect and the first assessment has to be carried out by June 30, 2020.

Carrying out ML and TF risk assessment is a very subjective matter and there is no thumb rule to be followed for the same. There is no uniformity on procedures of risk assessment, however, they may be guided by a set of broad principles. The following write-up intends to explore guidance principles enumerated by international bodies and suggest principles to be followed by financial institutions in India, specifically NBFCs, for carrying out risk assessment exercise.

Origin of the concept

The concept of ML and TF risk assessment arises from the recommendations of Financial Action Task Force (FATF). FATF has also provided detailed guidance on TF Risk Assessment[3]. Due to the inter-linkage between ML and TF, the guidelines also serve the purpose of guiding ML risk assessment. TF risk is defined as-

“A TF risk can be seen as a function of three factors: threat, vulnerability and consequence. It involves the risk that funds or other assets intended for a terrorist or terrorist organisation are being raised, moved, stored or used in or through a jurisdiction, in the form of legitimate or illegitimate funds or other assets.”

Global practices for ML/TF risk assessment

Based on FATF recommendations, many jurisdictions have prepared and published risk assessment procedures. India is yet to come up with the same.

For example, the National risk assessment of money laundering and terrorist financing[4] is the guidance published by the UK government. It provides sector specific guidance for risk assessment. The sector specific guidance is further granulated keeping in view the specific threats to certain parts of the sector.

The guidance provided by the Republic of Serbia[5] is a generalised one providing broad guidance to all sectors for risk assessment.

In Germany, financial institutions are classified on the basis of potential risk of ML/TF identified by them (considering the factors such as location, scope of business, product structure, customers’ profile and distribution structure) and the intensity of supervision by regulator is based on such risk categorisation.

Risk assessment process by NBFC

The risk assessment of a financial sector entity such as an NBFC, need not be complex, but should be commensurate with the nature and size of its business. For smaller or less complex NBFCs where the customers fall into similar categories and/or where the range of products and services are very limited, a simple risk assessment might suffice. Conversely, where the loan products and services are more complex, where there are multiple subsidiaries or branches offering a wide variety of products, and/or their customer base is more diverse, a more sophisticated risk assessment process will be required.

Based on the guiding principles provided by the FATF and specific guidance issued by FATF for banking and financial sector[6], the process of risk assessment by NBFCs may be divided into following stages:

Stage 1: Collection of information

The risk assessment shall begin with collecting of information on a wide range of variables including information on the general criminal environment, TF and terrorism threats, TF vulnerabilities of specific sectors and products, and the jurisdiction’s general AML capacity

The information may be collected externally or internally. In India, Directorate of Enforcement is the body which deals with ML and TF matters and has collection of information and list of terrorists. Further, the information may also be obtained from Central Bureau of Investigation.

Stage 2: Threat identification

Based on the information collected, jurisdiction and sector specific threats should be identified. Threat identification should be based on the risks identified on the national level, however, shall not be limited to the same. It should also be commensurate to the size and nature of business of the entity.

For individual NBFCs, it should take into account the level of inherent risk including the nature and complexity of their loan products and services, their size, business model, corporate governance arrangements, financial and accounting information, delivery channels, customer profiles, geographic location and countries of operation. The NBFC should also look at the controls in place, including the quality of the risk management policy, the functioning of the internal oversight functions etc.

Stage 3: Assessment of ML/TF vulnerabilities

This stage involves determination of the how the identified threats will impact the entity. The information obtained should be analysed in order to assess the probability of risks occurring. Based on the assessment, ML/TF risks should be classified as low, medium and high impact risks.

While assessing the risks, following factors should be considered:

- The nature, scale, diversity and complexity of their business;

- Target markets;

- The number of customers already identified as high risk;

- The jurisdictions the entity is exposed to, either through its own activities or the activities of customers, especially jurisdictions with relatively higher levels of corruption or organised crime, and/or deficient AML/CFT controls and listed by RBI or FATF;

- The distribution channels, including the extent to which the entity deals directly with the customer or relies third parties to conduct CDD;

- The internal audit and regulatory findings;

- The volume and size of its transaction.

The NBFCs should complement this information with information obtained from relevant internal and external sources, such as operational/business heads and lists issued by inter-governmental international organisations, national governments and regulators.

The risk assessment should be approved by senior management and form the basis for the development of policies and procedures to mitigate ML/TF risk, reflecting the risk appetite of the NBFC and stating the risk level deemed acceptable. It should be reviewed and updated on a regular basis. Policies, procedures, measures and controls to mitigate the ML/TF risks should be consistent with the risk assessment.

Stage 4: Analysis of ML/TF threats and vulnerabilities

Once potential TF threats and vulnerabilities are identified, the next step is to consider how these interact to form risks. This could include a consideration of how identified domestic or foreign TF threats may take advantage of identified vulnerabilities. The analysis should also include assessment of likely consequences.

Stage 5: Risk Mitigation

Post the analysis of threats and vulnerabilities, the NBFC must develop and implement policies and procedures to mitigate the ML/TF risks they have identified through their individual risk assessment. Customer due diligence (CDD) processes should be designed to understand who their customers are by requiring them to gather information on what they do and why they require financial services. The initial stages of the CDD process should be designed to help NBFCs to assess the ML/TF risk associated with a proposed business relationship, determine the level of CDD to be applied and deter persons from establishing a business relationship to conduct illicit activity.

Focus on CDD procedure

While entering into a relationship with the customer, carrying out Customer Due Diligence (CDD) is the initial step. It is during the CDD process that the identity of a customer is verified and risk based assessment of the customer is done. While assessing credit risks, financial entities should also assess ML/TF risks. The CDD procedures and policies should suitably include checkpoints with respect to ML and TF.

The risk classification of the customer, as discussed above, should also be done based on the CDD carried out. The CDD procedure, apart from verifying the identity of the customer, should also go a few steps further to understand the nature of business or activity of the customer. Measures should be taken to prevent the misuse of legal persons for money laundering or terrorist financing.

In case of medium or high risk customers, or unusual transactions, the entities should also carry out transaction due diligence to identify source and application of funds, beneficiary of the transaction, purpose etc.

NBFCs should document and state clearly the criteria and parameters used for customer segmentation and for the allocation of a risk level for each of the clusters of customers. Criteria applied to decide the frequency and intensity of the monitoring of different customer segments should also be transparent. Further, the NBFC must maintain records on transactions and information obtained through the CDD measures. The CDD information and the transaction records should be made available to competent authorities upon appropriate authority.

Some examples of enhanced and simplified due diligence measures are as follows:

Enhanced Due Diligence (EDD)

- obtaining additional identifying information from a wider variety or more robust sources and using the information to inform the individual customer risk assessment

- carrying out additional searches (e.g., verifiable adverse media searches) to inform the individual customer risk assessment

- commissioning an intelligence report on the customer or beneficial owner to understand better the risk that the customer or beneficial owner may be involved in criminal activity

- verifying the source of funds or wealth involved in the business relationship to be satisfied that they do not constitute the proceeds from crime

- seeking additional information from the customer about the purpose and intended nature of the business relationship

Simplified Due Diligence (SDD)

- obtaining less information (e.g., not requiring information on the address or the occupation of the potential client), and/or seeking less robust verification, of the customer’s identity and the purpose and intended nature of the business relationship

- postponing the verification of the customer’s identity

Ongoing CDD and Monitoring

Ongoing monitoring means the scrutiny of transactions to determine whether the transactions are consistent with the NBFC’s knowledge of the customer and the nature and purpose of the loan product and the business relationship.

Monitoring also involves identifying changes to the customer profile (for example, their behaviour, use of products and the amount of money involved), and keeping it up to date, which may require the application of new, or additional, CDD measures. Monitoring transactions is an essential component in identifying transactions that are potentially suspicious. Monitoring should be carried out on a continuous basis or triggered by specific transactions. It could also be used to compare a customer’s activity with that of a peer group. Further, the extent and depth of monitoring must be adjusted in line with the NBFC’s risk assessment and individual customer risk profiles

Reporting

The NBFCs should have the ability to flag unusual movement of funds or transactions for further analysis. Further, it should have appropriate case management systems so that such funds or transactions are scrutinised in a timely manner and a determination made as to whether the funds or transaction are suspicious. Funds or transactions that are suspicious should be reported promptly to the FIU and in the manner specified by the authorities. There must be adequate processes to escalate suspicions and, ultimately, report to the FI.

Internal Controls

Adequate internal controls are a prerequisite for the effective implementation of policies and processes to mitigate ML/TF risk. Internal controls include appropriate governance arrangements where responsibility for AML/CFT is clearly allocated and there are controls to test the overall effectiveness of the NBFC’s policies and processes to identify, assess and monitor risk. It is important that responsibility for the consistency and effectiveness of AML/CFT controls be clearly allocated to an individual of sufficient seniority within the NBFC to signal the importance of ML/TF risk management and compliance, and that ML/TF issues are brought to senior management’s attention.

Recruitment and Training

NBFCs should check that personnel they employ have integrity and are adequately skilled and possess the knowledge and expertise necessary to carry out their function, in particular where staff are responsible for implementing AML/CFT controls. The senior management who is responsible for implementation of a risk-based approach should understand the degree of discretion an NBFC has in assessing and mitigating its ML/TF risks. In particular, it must be ensured that the employees and staff have been trained to assess the quality of a NBFC’s ML/TF risk assessments and to consider the adequacy, proportionality and effectiveness of the NBFC’s AML policies, procedures and internal controls in light of this risk assessment. Adequate training would allow them to form sound judgments about the adequacy and proportionality of the AML controls.

Stage 6: Follow-up and maintaining up-to-date risk assessment

Once assessed, the impact of the risk shall be recorded and measures to mitigate the same should be provided for. The information that forms basis of the risk assessment process should be timely updated and the entire risk assessment procedure should be carried out in case of major change in the information.

The compliance officer of the NBFC should have the necessary independence, authority, seniority, resources and expertise to carry out these functions effectively, including the ability to access all relevant internal information. Additionally, there should be an independent audit function carried out to test the AML/CFT programme with a view to establishing the effectiveness of the overall AML/CFT policies and processes and the quality of NBFC’s risk management across its operations, departments, branches and subsidiaries, both domestically and, where relevant, abroad.

[1] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11873&Mode=0

[2] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11566

[3] https://www.fatf-gafi.org/media/fatf/documents/reports/Terrorist-Financing-Risk-Assessment-Guidance.pdf

[4] https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/655198/National_risk_assessment_of_money_laundering_and_terrorist_financing_2017_pdf_web.pdf

[5] https://www.nbs.rs/internet/english/55/55_7/55_7_4/procena_rizika_spn_e.pdf

[6] http://www.fatf-gafi.org/media/fatf/documents/reports/Risk-Based-Approach-Banking-Sector.pdf

Our other write-ups on NBFCs may be viewed here: http://vinodkothari.com/nbfcs/

Write-rps relating to KYC and Anti-money laundering may also be referred:

Would the doses of TLTRO really nurse the financial sector?

-Kanakprabha Jethani | Executive

Vinod Kothari Consultants P. Ltd

Background

In response to the liquidity crisis caused by the covid-19 pandemic, the Reserve Bank of India (RBI) through a Press Release Dated April 03, 2020[1] announced its third Targeted Long Term Repo Operation (TLTRO). This issue is a part of a plan of the RBI to inject funds of Rs. 1 lakh crores in the Indian economy. Under the said plan, two tranches of LTROs of Rs. 25 thousand crores each have already been undertaken in the months of February[2] and March[3] respectively. This move is expected to restore liquidity in the financial market, that too at relatively cheaper rates.

The following write-up intends to provide an understanding of what TLTRO is, how it is supposed to enhance liquidity and provide relief, who can derive benefits out of it and what will be its impact. This article further views TLTROs from NBFCs’ glasses to see if they, being financial institutions, which more outreach than banks, avail benefit from this operation.

Meaning

LTRO is basically a tool to provide funds to banks. The funds can be obtained for a tenure ranging from 1 year to 3 years, at an interest rate equal to one day repo. Government securities with matching or higher tenure, would serve as a collateral. Usually, the interest rate of one day repo is lower than that of other short term loans. Thus, banks can avail cheaper finance from the RBI.

Banks will have to invest the amount borrowed under TLTROs in fresh acquisition of securities from primary or secondary market (Specified Securities) and the same shall not be used with respect to existing investments of the bank.

In the current LTRO, the RBI has directed that atleast 50% of the funds availed by the bank have to be invested in investment grade corporate bonds, commercial papers and debentures in the secondary market and not more than 50% in the primary market.

Why were the existing measures not enough?

Ever since the IL&FS crisis broke the liquidity supply chain in the economy, the RBI has been consistently putting efforts to bring back the liquidity in the financial system. For almost a year, the RBI kept cutting the repo rate, hoping the cut in repo rates increases banks’ lending power and at the same time reduces the interest rate charged by them from the customers. Despite huge cuts in repo rates, the desired results were not visible because the cut in repo rates enhanced banks’ coincide power by a nominal amount only.

Another reason for failure of repo rate cuts, as a strategy to reduce lending rates, was that repo rate is one of the factors determining the lending rate. However, it is not all. Reduction in repo rates did affect the lending rate, but the effect was overpowered by other factors (such as increased cost of funds from third party sources) and thus, the banks’ lending rates did not reduce actually.

Further, various facilities have been introduced by the RBI to enhance liquidity in the system through Liquidity Adjustment Facility (LAF) which includes repo agreements, reverse repo agreements, Marginal Standing Facility (MSF), term repos etc.

- Under LAF, banks can either avail funds (through a repurchase agreement, overnight or term repos) or extend loans to the RBI (through reverse repo agreements). Other than providing funds in the time of need, it also allows the banks to safe-keep excess funds with the RBI for short term and earn interest on the same.

- Under MSF (which is a new window under LAF), banks are allowed to draw overnight funds from the RBI against collateral in the form of government securities. The rate is usually 100 bps above the repo rate. The amount of borrowing is limited to 1% of Net demand and Term Liabilities (NDTL).

- In case of term repos, funds can be availed for 1 to 13 days, at a variable rate, which is usually higher than the repo rate. Further, the funds that can be withdrawn under such facility shall be limited to 0.75% of NDTL of the bank.

Although these measures do introduce liquidity to the financial system, they do not provide banks with ‘durable liquidity’ to provide a seamless asset-liability match, based on maturity. On the other hand, having funds in hand for a year to 3 years definitely is a measure to make the maturity based assets and liabilities agree. Thus, giving banks the confidence to lend further to the market.

Bits and pieces to be taken care of

The TLTRO transactions shall be undertaken in line with the operating guidelines issued by the RBI through a circular on Long Term Repo Operations (LTROs)[4]. A few points to be taken care of are as follows:

- The RBI conducts auctions (through e-Kuber platform) for extending such facility. Banks have to bid for obtaining funds from such facility. The minimum bid is to be of Rs. 1 crore and the allotment shall be in multiples of Rs. 1 crore.

- The investment in Specified Securities is to be mandatorily made within 30 days of availment of funds. In case the bank fails to deploy funds availed under TLTRO within 30 days, an incremental interest of repo rate plus 200 basis points shall be chargeable, in addition to normal interest, for the period the funds remain un-deployed.

- The banks will have to maintain the amount of specified securities in its Hold-to-Maturity (HTM) portfolio till the maturity of TLTRO i.e. such securities cannot be sold by banks until the term of TLTRO expires. Further, in case bank intends to hold the Specified Securities after the term of TLTRO expires, the same shall be allowed to be held in banks’ HTM portfolio.

Impact

The TLTRO operation of the RBI is expected to bring about a relief to the financial sector. The LTRO auctions conducted recently received bids amounting to several times the auction amount. Thus, a clear case of extreme demand for funds by banks can be seen. Although, the recent auctions are yet to reap their fruits, the major benefits that may arise from this operation are as follows:

- The liquidity in the banking system will get increased. Resultantly, the banks’ lending power would increase. Thus, injecting liquidity into the entire economy.

- Since, the marginal cost of funds of the banks will be based on one-day repo transactions’ rate, the same shall be lower as compared to other funding options of similar maturity. A reduced cost of funds for the banks will compel banks to lend at lower rates. Thus, making the short-term lending cheaper.

The picture from NBFCs’ glasses

Barely out of the IL&FS storm, the shadow bankers had not even adjusted their sails and were hit by another crisis caused by the covid-19 disruption. While the RBI is introducing measures for these lenders to cope with the crisis such as moratorium on repayment instalments[5], stay on asset reclassification based on the moratorium provided etc. The liquidity concerns of NBFCs remain untouched by these measures.

Word has it, the TLTRO is expected to restore liquidity in the financial system. Only banks can bid under LTRO auctions and avail funds from the RBI. This being said, let us look at how an NBFC would fetch liquidity from this.

Banks would use the funds availed under TLTRO transactions to invest in Specified Securities of various entities. Let us assume a bank avails funds of Rs. 1 crore under LTRO. Out of the funds availed, the bank decides to invest 50% in Specified Securities of companies in non-financial sector and 50% in entities in financial sector. Assuming that the entire 50% portion is invested in Specified Securities of 20 NBFCs equally. Each NBFC gets 2.5% of the funding availed by the Bank.

In the primary market

For the purchase of Specified Securities through primary market, the question of prime importance is whether it is feasible for an NBFC to come up with a fresh issue in the current scenario of lockdown. It is not feasible for an NBFC to plan an issue, obtain a credit rating, and get done with all other formalities within a period of 30 days. Thus, the option of fresh issue would generally be ruled out. Primary issues in pipeline may get banks as their investors. However, existence of such issues in pipeline are very low at present.

If an NBFC decides to go for private placement and gets it done within a span of say around a week, it can succeed in getting fresh liquidity for its operations. However, looking at the bigger picture, the restriction of investing only in investment grade securities bars the banks from investing in NBFCs which have lower rating i.e. usually the smaller NBFCs (more in number though). So the benefit of the scheme gets limited to a small number of NBFCs only. Thus, the motive of making liquidity reach the masses gets squashed.

In the secondary market

Above was just a hypothetical example to demonstrate that only a fraction of funds given out under LTRO would actually be used to bring back liquidity to the stagnant NBFC sector. It is important to note here that the liquidity is being brought back through purchase of securities from the secondary market, which does not result in introduction of any additional money to the NBFCs for their operations.

The liquidity enhancement in secondary market would also be limited to Specified Securities of investment grade. Thus, as already discussed, only the bigger size NBFCs would get the benefit of liquidity restoration.

Conclusion

The TLTRO is a measure introduced by the RBI to enhance liquidity in the system. Although it provides banks with liquidity, the restrictions on the use of availed funds bar the banks to further pass on the liquidity benefit. As for NBFCs, the benefit is limited to making the securities of the NBFCs liquid and the introduction of fresh liquidity to the NBFC is likely to be minimal.

Further, the benefit is also likely to be limited to bigger NBFCs, destroying the motive of making liquidity reach to the masses. A few enhancements to the existing LTRO scheme, such as directing the banks to ensure that the investment is not concentrated in a few destinations or prescribing concentration norms might result in expanding liquidity reach to some extent and would create a chain of supply of funds that would reach the masses through the outreach of such financial institutions.

News Update:

The RBI Governor in his statement on April 17, 2020[6], addressed the problem of narrow outreach of liquidity injected through TLTRO and announced that the upcoming TLTRO (TLTRO 2.0) would come with a specification that the proceeds are to be invested in investment grade bonds, commercial paper, and non-convertible debentures of NBFCs only, with at least 50 per cent of the total amount availed going to small and mid-sized NBFCs and MFIs. This is likely to ensure that a major portion of the investments go to the small and mid-sized NBFCs, thus expanding the liquidity outreach.

[1] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=49628

[2] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=49360

[3] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=49583

[4] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=49360

[5] Our detailed FAQs on moratorium on loans due to Covid-19 disruption may be referred here: http://vinodkothari.com/2020/03/moratorium-on-loans-due-to-covid-19-disruption/

[6] https://rbidocs.rbi.org.in/rdocs/Content/PDFs/GOVERNORSTATEMENTF22E618703AE48A4B2F6EC4A8003F88D.PDF

Our write-up on stay on asset classification due to covid-19 may be referred here: http://vinodkothari.com/2020/04/the-great-lockdown-standstill-on-asset-classification/

Our other write-ups on NBFCs may be referred here: http://vinodkothari.com/nbfcs/

Moratorium on loans due to Covid-19 disruption

Team Financial Services, Vinod Kothari Consultants P Ltd.

This version dated 14th April, 2020. We shall continue to develop this further based on the text of notification and the clarifications, if any, issued by the RBI.

We are also gratefully obliged to see that the page has received attention and comments from several borrowers. We submit, humbly, that the page is primarily for guidance of lenders.]

To address the stress in the financial sector caused by COVID-19, several measures have been taken by the RBI as a part of its Seventh Bi-monthly Policy[1]. Further, the RBI has come up with a Notification titled COVID 19 package[2]. These measures are intended to mitigate the burden on debt-servicing caused due to disruptions on account of COVID-19 pandemic. These measures include moratorium on term loans, deferring interest payments on working capital and easing of working capital financing. We have tried to provide our analysis of the measures taken by RBI in form of the following FAQs.

Further, in this regard the Ministry of Finance has also issued FAQs on RBI’s scheme for a 3-month moratorium on loan repayment.

Legal/contractual nature of the Moratorium

1. Has the RBI granted a compulsory moratorium?

No, the lending institutions have been permitted to allow a moratorium of three months. This is a relaxation offered by RBI to the lending institutions. Neither is it a guidance by the RBI to the lenders, nor is it a leeway granted by the RBI to the borrowers to delay or defer the repayment of the loans. Hence, the moratorium will actually have to be granted by the lending institution to the borrowers. The RBI has simply permitted the lenders to grant such moratorium.

2. Who are the lending institutions covered by the moratorium requirement?

All commercial banks (including regional rural banks, small finance banks and local area banks), co-operative banks, all-India Financial Institutions, and NBFCs (including housing finance companies and micro-finance institutions) have been permitted to allow the moratorium relaxation to its borrowers.

3A. Is this the first time such a moratorium or relaxation has been granted by the RBI?

During the demonetisation phase in November 2016, a 60 day relaxation was offered to small borrowers accounts for recognition of an asset as sub-standard. Our detailed analysis on the same can be viewed here- http://vinodkothari.com/wp-content/uploads/2017/03/Interpreting_the_2_months_relaxation_for_asset_classification.pdf

3B. Has there been similar relaxation provided by other jurisdictions across the globe?

India is not the only country to grant a moratorium during this time of crisis. Several other countries have granted a moratorium in varying terms. A table showing the details of moratoriums granted globally may be read here http://vinodkothari.com/2020/04/the-great-lockdown-standstill-on-asset-classification/

4. What is meant by moratorium on term loan?

Moratorium is a sort of granting of a ’holiday’- it is a repayment holiday where the borrower is granted an option to not pay during the moratorium period. It is a restructuring of the terms of the loan with the mutual consent of the lender and the borrower. The consent of the lender will be in the form the lender’s circular or notice – see below. The consent of the borrower may be obtained by a “deemed consent unless declined” option.

For example, in case the instalment falls due on April 01, 2020, and the lender has granted a moratorium of 3 months from a specific date, say April 1, 2020, then the revised due date for repayment shall be July 1, 2020.

Scope and implementation of the moratorium

5. From what date can the moratorium be granted?

The lenders are permitted to grant a moratorium of three months on payment of all instalments falling due between March 1, 2020 and May 31, 2020. The intention is to shift the repayment dates by three months. Therefore, the moratorium should start from the due date, falling immediately after 1st March, 2020, against which the payment has not been made by the borrower.

For example, if an instalment was due on 15th March, 2020, but has remained unpaid so far, the lender can impose the moratorium from 15th March, 2020 and in that case, revised due date shall be 15th June, 2020

6. Will the moratorium be applicable in case of new loans sanctioned after March 1, 2020 during the lockdown period?

Technically, new loans sanctioned after March 1, 2020 are not covered under the press release since it mentioned about loans outstanding as on March 1, 2020. However, based on the RBI circular it can be inferred that the Lending Institution may at its own discretion extend the benefit to such borrowers in case the loan instalments of such new loans are falling due between March 1, 2020 and May 31, 2020.

7. Is the moratorium on principal or interest or both?

The repayment schedule and all subsequent due dates, as also the tenor for loans may be shifted by three months (or the period of moratorium granted by the lending institution). Instalments will include payments falling due from March 1, 2020 to May 31, 2020 in the form of-

(i) principal and/or interest components;

(ii) bullet repayments;

(iii) Equated Monthly instalments;

(iv) credit card dues.

8A. What shall be the moratorium period?

Lending Institutions may use their discretion to allow a moratorium of upto three months. It is not necessary to provide a compulsory moratorium of three months- it can be less than three months as well. Practically, we envisage that all lenders shall grant a moratorium to all borrowers across board for 3 months.

However, a moratorium beyond three months shall be considered as restructuring of loan.

8B. Can NBFCs grant extensions for loans where the last EMI falls due after May 31st?

The Covid-19 Regulatory Package issued by RBI has allowed the grant of moratorium to only those instalments that are falling due between March 1, 2020 and May 31, 2020. However, considering the disruption caused across the globe, the Company may consider extension of the EMI dates for installments falling due after May 31, 2020.

The reason for granting such relaxation is not related to any specific borrower’s financial difficulty because of any economic or legal reasons. The reason for such relaxation would be the disruption caused across an entire class of borrower and not any individual borrower. Hence, this would not be considered as restructuring and will not require any asset classification downgrade.

9. Reading the language of the RBI Notification strictly, it says: “lending institutions” are permitted to grant a moratorium of three months on payment of all instalments1 falling due between March 1, 2020 and May 31, 2020. [Para 2]. The notification nowhere refers to the payments which had already fallen due before March 1. Therefore, will those payments continue to age during the moratorium period? For example, will something which is 30 DPD will become 120 DPD?

As per the contents of the letter dated March 31, 2020 written by RBI to IBA, any amount which was overdue on 29th Feb, 2020, there is no moratorium with respect to those amounts, and therefore, the existing IRAC norms will continue to apply. The RBI contends that there was no disruption in February, and therefore, one cannot bring disruption as the basis for not paying what had fallen due before March 1.

However, in our view, such an interpretation will be completely counter-intuitive. The whole intent behind the moratorium is the disruption in the system due to an externality. If the borrower had an instalment which was 30 days past due on 1st March, it cannot be contended that he will have difficulty in paying his current dues but will have no difficulty in paying what had already become due. But for the systemic disruption, it could well have been that the borrower would have cleared all his dues.

The meaning of the moratorium is that payments do not fall due during the period of the moratorium – whether current or past. Therefore, the moratorium period cannot result into ageing of the past dues. Of course, if the past dues are an overdue rate, the overdue rate may continue. But for the purpose of counting DPD, the moratorium period will have to be excluded.

Taking any other interpretation will frustrate the very purpose of the moratorium. By rules of appropriation, whatever the borrower pays between March 1 and May 31 would have first gone towards clearing his overdues. Hence, a moratorium on the current dues should apply to the existing dues as well.

There has been a ruling of the Delhi High court in Anantraj Limited vs Yes Bank order dated 6th April, 2020 in response to a writ petition, where the court has also stated that there will be no transformation of a standard account into an NPA, since before an account becomes an NPA, it has to pass through SMA 1 and SMA 2, and as per RBI’s own admission, there will be no downgradation of the status due to the moratorium. In essence, the Delhi High court seems to be holding the same view as expressed by us above. Our analysis of the judgement can be read here- http://vinodkothari.com/2020/04/moratorium-on-asset-classification-of-past-due-accounts/

10. How will the moratorium impact the existing loan tenure?

In case a moratorium is granted, the RBI circular states that the repayment schedule for such loans as also the residual tenure, will be shifted across by three months after the moratorium period.

However, in certain cases of long tenure loans (say, home loans), the additional burden on the borrower due to the accrued interest (and interest on such interest) would cause the amount to swell so much that paying the accumulated interest in one go may not be feasible. This may require the lender to convert the accrued interest also into instalments. Converting such accrued interest into manageable instalments is the lender’s prudential call, and should not be taken as a case of restructuring, since the total tenure is going beyond 3 months over the original term.

11. Will the interest accrue during the moratorium period?

Yes, the moratorium is a ‘payment holiday’ however, the interest will definitely accrue. The accrual will not stop.

12. Will there be delayed payment charges for the missing instalments during the moratorium period?

Overdue interest is charged in case of default in payment. However, during the moratorium, the payment itself is contractually stopped. If there is no payment due, there is no question of a default. Therefore, there will be no overdue interest or delayed payment charges to be levied.

13. Which all loans shall be considered eligible for the relaxation?

All term loans outstanding as on March 1, 2020 are eligible to claim the relaxation. Also, there may be a deferment of interest in case of working capital facilities sanctioned in the form of cash credit/overdraft and outstanding as on March 1, 2020.

14. Is the moratorium applicable to the following:

(a) Personal loans

The moratorium is applicable to all term loans and working capital facilities (refer para 5 and 6 of the Statement on Developmental and Regulatory Policies). Therefore, the lender may extend the benefit of the moratorium or deferment of interest to lending facilities in the nature of term loans as well as revolving lines of credit, a.k.a. working capital facilities, as the case may be.

(b) Overdraft facilities

Overdraft facilities allow the account-holder to withdraw more money than what is held in the account. It is a kind of short-term loan facility, which the account-holder shall be required to repay within a specified period of time or at once, depending on the terms of arrangement with the bank. Thus, in case repayment is to be made within a specified tenure , the same qualifies to be term-loan and moratorium shall be applicable on EMIs of such overdraft facility.

(c) An unsecured personal loan extended by a lender through prepaid cards for making payments at partner merchant PoS

Such unsecured personal loans may be repayable in the form of EMIs or a bullet repayment. As discussed above, if repayment is made over a period of time, moratorium is applicable. In case of bullet repayments as well, moratorium may be granted.

(d) Invoice financing

Invoice financing can be of 2 types- (a) Factoring and (b) Asset-based invoice financing.

In case of factoring, the factor purchases the receivables of an entity and pays the amount of receivables reduced by a certain percentage (factoring fee) to the entity. Thereafter, the factor is responsible to recover the money from the debtor of such entity. There is no moratorium in case of commercial invoices.

Another device commonly used is invoice financing i.e. asset-based invoice financing, which allows a vendor to avail a credit facility against the security of receivables. Since the underlying here is the commercial receivable, for which there is no moratorium, the same is not covered by the moratorium as being discussed.

(e) Payday loans

Payday loans are unsecured personal credit facilities obtained by salaried individuals against their upcoming pay-cheques. The amount of such facilities is usually limited to a certain part of the borrower’s upcoming salary.

In case of such loans, the repayment term, though very short, is pre-determined and is payable from out of the salary of the individual. As there is no deferral of salary payments, we are of the view that there is no case of disruption here.

(f) Loan against turnover

These loans are extended by the lenders on the basis of expected turnover of a merchant, mostly on e-commerce websites. The intent is to finance the day-to-day business needs of the borrower in order to attain the expected turnover. Thus, such loans are essentially working capital loans. As already discussed, moratorium may be allowed on working capital loans.

(g) Long-term loans

These kinds of loans have a pre-specified term, which is usually greater than 3 years. Needless, to say, being term loans, moratorium shall be allowed on such loans. Such loans are usually secured and may cover the following kinds of loans:

- Housing loans

- Equipment finance loans

- Personal loans

- Two-wheeler loans

- Auto-finance loans

(h) Gold loans

The applicability of the Notification to gold loans is quite interesting. Most gold loans have a bullet repayment term. In addition, some gold loans induce a customer to make payment of interest on a regular basis, and offer a concessional rate of interest should the customer pay interest on a regular basis. The following situations may explain the applicability of the Notification to gold loans:

- If the bullet repayment is due during the Moratorium period, the loan will be eligible for the moratorium, and the borrower may make the bullet repayment at the end of the moratorium period.

- If the bullet repayment is due after the Moratorium period, the moratorium has no impact on the loan. There is no question of any extension of the loan term, as there were no payments due during the disruption period.

- If there is interest payment during the moratorium period, and the customer has opted for the same, the customer will get holiday from the interest payment during the moratorium period, and the customer will still be eligible for the lower rate of interest.

15. How will the moratorium be effective in case of working capital facilities?

The working capital facilities have been allowed a deferment of three months on payment of interest in respect of all such facilities outstanding as on March 1, 2020. The accumulated interest for the period will be paid after the expiry of the deferment period.

16. Is it possible for the Lender to not provide a moratorium?

Technically, certainly yes. However, borrowers may take advantage of the Ministry of Law circular that the COVID disruption is a case of “force majeure” and FMC does not result in a contractual breach. Hence, lenders will be virtually forced into granting the same.

17. Is the lending institution required to grant the moratorium to all categories of borrowers?

Since the grant of the moratorium is completely discretionary, the lending institution may grant different moratoriums to different classes of borrowers based on the degree of disruption on a particular category of borrowers. However, the grant of the moratorium to different classes of borrowers should be making an intelligible distinction, and should not be discriminatory.

18. Can the lender revise the interest rate while granting extension under the moratorium?

The intent of the moratorium is to ensure relaxation to the borrower due to the disruption caused. However, increase in interest rate is not a relief granted and hence should not be practised as such.

19. Can the moratorium period be different for different loans of the same type? For example, a lender grants a moratorium of 3 months for all loans which are 60-89 DPD, and a moratorium of 2 months for all loans which are 30 -59 DPD as on the effective date.

The moratorium is essentially granted to help the borrowers to tide over a liquidity crisis caused by the corona disruption. In the above example, the scheme seems to be to get over a potential NPA characterisation, which could not be the intent of the relaxation.

20. Will the grant of different moratorium periods be regarded as discrimination by the NBFC?

An NBFC may assess where the disruption is likely to adversely impact the repayment capacity of the borrower and take a call based on such assessment. For example in case of farm sector borrowers and daily wage earners, the disruption will be maximum. However, a salaried employee may not be facing any impact on their repayment capacity.

21. Can a borrower prevail upon a lending institution to grant the moratorium, in case the same has not been granted the lending institution?

The grant of the moratorium is a contractual matter between the lender and the borrower. There is no regulatory intervention in that contract.

22. Can the borrower pay in between the moratorium period?

It is a relief granted to the borrower due to disruption caused by the sudden lockdown. However, the option lies with the borrower to either repay the loan during this moratorium as per the actual due dates or avail the benefit of the moratorium.

23. Will such payment be considered as prepayment?

This will not be considered as prepayment and there will not be any prepayment penalty on the same.

24. Is the moratorium applicable to financial lease transactions?

Financial leases are akin to loan transactions and have rental payouts similar to EMIs in case of a term loan. Hence, lessors under a financial lease may confer the benefit of the moratorium under the RBI circular.

25. Is the moratorium applicable to operating lease transactions?

Operating leases are not considered as financial transactions and hence, they shall not be covered under the RBI circular for granting moratorium. However, lessors may, in their wisdom, grant the benefit of moratorium. Note that the NPA treatment in case of operating leases is not the same as in case of loans.

Refer to our various articles on leasing here.

26. A loan was in default already as on 1st March, 2020. The lender has various security interests – say a mortgage, or a pledge. Will the lender be precluded from exercising security interest during the holiday period?

The moratorium is only for what instalments/payments were due from 1st March 2020 upto the period of moratorium conferred by the lender (so, 31st May, in case of a 3 month moratorium). The same does not affect payment obligations that have already fallen due before 1st March. Hence, if there was a default, and there were remedies available to the lender as on 1st March already, the same will not be affected.

However, note that for using the powers under the SARFAESI Act, the facility has to be characterised as non-performing. Unless the facility was already a non-performing loan, the intervening holiday will defer the NPA categorisation. In that case, the use of SARFAESI powers will be deferred until NPA categorisation happens.

Modus operandi for giving effect to the moratorium

27. What are the actionables required to be taken by the lending institution to grant the moratorium?

The RBI Notification dated 27th March, 2020, para 8 mentions about a board-approved policy. Accordingly, the lending institution may put in place a policy. The Policy should provide maximum facility to the concerned authority centre in the hierarchy of decision-making so that everything does not become rigid. For instance, the extent of moratorium to be granted, the types of asset classes where the moratorium is to be granted, etc., may be left to the relevant asset managers.

Further, the instructions in the notification must be properly communicated to the staff to ensure its implementation.

You may refer to the list of actionables here.

28. The RBI has mentioned about a Board-approved policy. Obviously, under the present scenario, calling of any Board-meeting is not possible. Hence, how does one implement the moratorium?

Please refer to our article here as to how to use technology for calling board meetings.

29. In case the lender intends to extend a moratorium, will it require consent of the borrower and confirmation on the revised repayment schedule?

Based on the policy adopted by the lending institution, the moratorium may be extended to all borrowers or only those who approach the lender in this regard. However, the revised terms must be communicated to the borrower and the acceptance must be recorded.

An option may be provided to the borrower for opting the moratorium. In case the borrower fails to respond or remains silent, it may be considered as deemed confirmation on the moratorium. In case of acceptance by the borrower to opt for moratorium, including deemed acceptance, the revised terms shall be shared which should be accepted by the borrower- either electronically or such other means as per the respective lending practice. Further, the PDC or NACH should not be presented for encashment as per the existing terms.

However, in case the borrower has not opted for the moratorium by his action or otherwise has expressly denied the option, the PDC and NACH shall be encashed as per the existing terms and necessary action can be initiated by the lender in case of dishonour.

30. Is the lender required to obtain fresh PDCs and NACH debit mandates from the borrowers?

An option may be provided to the borrower for opting the moratorium. In case the borrower fails to respond or remains silent, it may be considered as deemed confirmation on the moratorium. In such a case the PDC or NACH should not be presented for encashment as per the existing terms.

However, in case the borrower has not opted for the moratorium by his action or otherwise has expressly denied the option, the PDC and NACH shall be encashed as per the existing terms and necessary action can be initiated by the lender in case of dishonour.

31. In case the payment has been made by a borrower for the installment due for the month of March 2020, does the lender need to refund the same?

The payments already received may not be considered for the purpose of passing the moratorium relaxation. The lenders have their discretion, but appropriately, these payments may either be regarded as payment of principal as on 1st March, 2020, duly discounted for the time lag between 1st March and the actual repayment date, or the payment already made by the borrower may just be excluded from the moratorium. For example, if the payments fell due on 7th March, and by 15th March, 80% of the payments have already been made, the same may just be excluded from the holiday, thereby granting holiday only for the payments due on 15th April and 15th May.

NPA classification and restructuring

32. What will be the impact on the NPA classification on the following loans:

- Standard as on March 1, 2020

- NPA as on March 1, 2020

- Showing signs of distress as on March 1, 2020

In case of standard loan, the moratorium period will not be considered for computing default and hence, it will not result in asset classification downgrade. Our views in this regard have been discussed elaborately above.

As per the FAQs issued by the MoF, it is clear that the benefit of moratorium is available to all such accounts, which are standard assets as on 1st March 2020. Hence, loans already classified as NPA shall continue with further asset classification deterioration during the moratorium period in case of non-payment.

In case of assets showing signs of distress as on March 1, 2020, the moratorium may still be extended since they are classified as standard asset. Further, the asset classification of account which has been classified as SMA should not further be classified as a NPA in case the installment is not paid during the moratorium period and the classification as SMA should be maintained. [Refer our detailed response in Q9 above]

33. Effectively, are we saying the grant of the moratorium is also a stoppage of NPA classification?

The RBI contends that there was no disruption in February, and therefore, one cannot bring disruption as the basis for not paying what had fallen due before March 1. The benefit of the moratorium is not applicable for the amounts which were already past due before March 01, 2020..

34. Is grant of moratorium a type of restructuring of loans?

The moratorium/deferment is being provided specifically to enable the borrowers to tide over the economic fallout from COVID-19. Hence, the same will not be treated as change in terms and conditions of loan agreements due to financial difficulty of the borrowers.

35. What will be the impact on the loan tenure and the EMI due to the moratorium?

Effectively, it would amount to extension of tenure. For example, if a term loan was granted for a period of 36 months on 1st Jan 2020, and the lender grants a 3 months’ moratorium, the tenure effectively stands extended by 3 months – so it becomes 39 months how.

Since there is an accrual of interest during the period of moratorium, the lender will have to either increase the EMIs (that means, recompute the EMI on the accreted amount of outstanding principal for the remaining number of months), or change the last EMI so as to compensate for the accrual of interest during the period of the moratorium. Since changing of EMIs have practical difficulties (PDCs, standing instructions, etc.), it seems that the latter approach will be mostly used.

36. How will the deferment of interest in the case of working capital facilities impact the asset classification?

Recalculating the drawing power by reducing margins and/or by reassessing the working capital cycle for the borrowers will not result in asset classification downgrade.

The asset classification of term loans which are granted relief shall be determined on the basis of revised due dates and the revised repayment schedule.

37. Will the delayed payment by the borrower due to the moratorium have an impact on its CIBIL score?

The moratorium on term loans, the deferring of interest payments on working capital and the easing of working capital financing will not qualify as a default for the purposes of supervisory reporting and reporting to credit information companies (CICs) by the lending institutions. Hence, there will be no adverse impact on the credit history of the beneficiaries.

Impact of moratorium on corporate borrowers

37A. What will be the impact of the moratorium on the corporate borrowers? If the corporate borrower is having a secured loan with the bank, and due to the moratorium, the tenure gets extended, is it a case of modification requiring “modification of charge” within the meaning of the Companies Act?

Answer should be in the negative, for the following reasons:

- 79 provides for “modification in the terms or conditions or the extent or operation of any charge”. There is no modification in the terms of the charge, or the extent or operation of the charge. The charge is on the same property; the exposure amount also does not change by the very fact of the moratorium.

- The modification is not a result of a unique transaction between the lender and the borrower, which needs to be publicly intimated. The moratorium is the result of an external event, which the public at large is expected to be aware of.

- The moratorium is not a case of restructuring of the debt that requires any kind of regulatory reporting by the borrower. The moratorium is the result of a force majeure event.

Taking the view that the resulting extension of tenure is a case of moratorium will make thousands of borrowers file modification, which is both perfunctory and unnecessary.

37B. Under Part A of Schedule III of LODR Regulations, a corporate debt restructuring is to be deemed to be a material event requiring reporting to the stock exchanges. Is the moratorium-related restructuring a case of corporate debt restructuring?

Answer should be negative once again. This restructuring is not a result of a credit event. It is result of a force majeure.

Impact of the Moratorium on accounting under IndAS 109

38. Where there are no repayments during the moratorium period, is it proper to say that the loan will be taken to have “defaulted” or there will be credit deterioration, for the purposes of ECL computation?

The provisions of para 5.5.12 of the IndAS 109 are quite clear on this. If there has been a modification of the contractual terms of a loan, then, in order to see whether there has been a significant increase in credit risk, the entity shall compare the credit risk before the modification, and the credit risk after the modification. Sure enough, the restructuring under the disruption scenario is not indicative of any increase in the probability of default.

39. There are presumptions in para B 5.5.19 and 20 about “past due” leading to rebuttable presumption about credit deterioration. What impact does the moratorium have on the same?

The very meaning of “past due” is something which is not paid when due. The moratorium amends the payment schedule. What is not due cannot be past due.

40. Will the effective interest rate (EIR) for the loan be recomputed on account of the modification of tenure?

The whole idea of the modification is to compute the interest for the deferment of EMIs due to moratorium, and to compensate the lender fully for the same. The IRR for the loan after restructuring should, in principle, be the same as that before restructuring. Hence, there should be no impact on the EIR.

41. What will be the impact of the moratorium for accounting for income during the holiday period?

As the EIR remains constant, there will be recognition of income for the entire Holiday period. For example, for the month of March, 2020, interest will be accrued. The carrying value of the asset (POS) will stand increased to the extent of such interest recognised. In essence, the P/L will not be impacted.

42. If the moratorium is a case of “modification of the financial asset”, is there a case for computing modification gain/loss?

As the EIR remains constant, the question of any modification gain or loss does not arise.

43. Does the “modification of the financial asset”call for impairment testing?

The contractual modification is not the result of a credit event. Hence, the question of any impairment for this reason does not arise.

Impact in case of securitisation transactions

44. There may be securitisation transactions where there are investors who have acquired the PTCs. The servicing is with the originator. Can the originator, as the servicer, grant the benefit of the moratorium? Any consent/concurrence of the trustees will be required? PTC holders’ sanction is required?

Servicer is simply a servicer – that is, someone who enforces the terms of the existing contracts, collects cashflows and remits the same to the investors. Servicer does not have any right to confer any relaxation of terms to the borrowers or restructure the facility.

While the moratorium may not amount to restructuring but there is certainly an active grant of a discretionary benefit to the borrowers. In our view, the servicer by himself does not have that right. The right may be exercised only with appropriate sanction as provided in the deed of assignment/trust deed – either the consent of the trustees, or investor’ consent.

45. Irrespective of whether the moratorium is granted with the requisite consent or not, there may be some missing instalments or substantial shortfall in collections in the months of April, May and June. Is the trustee bound to use the credit enhancements (excess spread, over-collateralisation, cash collateral or subordination) to recover these amounts?

As we have mentioned above, the grant of the moratorium by the servicer will have to require investor concurrence or trustee consent (if the trustee is so empowered under the trust deed/servicing agreement). Assuming that the investors have given the requisite consent (say, with 75% consent), the investors’ consent may also contain a clause that during the period of the moratorium, the investors’ payouts will be deemed “paid-in-kind” or reinvested, such that the expected payments for the remaining months are commensurately increased.

This will be a fair solution. Technically, one may argue that the credit enhancements may be exploited to meet the deficiency in the payments, but utilisation of credit enhancements will only reduce the size of the support, and may cause the rating of the transaction to suffer. Therefore, investors’ consent may be the right solution.

Impact in case of direct assignment transactions

46. There may be direct assignment transactions where there is an assignee with 90% share, and the assignor has a 10% retained interest. Can the assignor/originator, also having the servicer role, grant the benefit of the moratorium? Any consent/concurrence of the assignee will be required?

In our view, the 10% retained interest holder cannot grant the benefit without the concurrence of the 90% interest holder.

47. What will be the impact of the moratorium on the assignee?

Once again, as in case of securitisation transactions, if the grant of the moratorium takes place with assignee consent, the assignee may agree to give the benefit to the borrowers. In that case, the assignee does not have to treat the loans as NPAs merely because of non-payment during the period of the moratorium.

Impact in case of co-lending transactions

48. In case of a co-lending arrangement, can the co-lenders grant differential benefit of the moratorium?

Since the grant of moratorium is discretionary, the co-lenders may intend to grant different moratorium periods to the same borrower. However, that could lead to several complications with respect to servicing, asset classification etc. Hence, it is recommended that all the parties to the co-lending arrangement should be in sync.

[1] https://rbidocs.rbi.org.in/rdocs/PressRelease/PDFs/PR21302E204AFFBB614305B56DD6B843A520DB.PDF

[2] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11835&Mode=0

Our other write-ups relating to covid-19 disruption can be read here- http://vinodkothari.com/covid-19-incorporated-responses/

Other write-ups on NBFCs can be read here- http://vinodkothari.com/nbfcs/

Moving to contactless lending, in a contact-less world

-Kanakprabha Jethani (kanak@vinodkothari.com)

Background

With the COVID-19 disruption taking a toll on the world, almost two billion people – close to a third of the world’s population being restricted to their homes, businesses being locked-down and work-from home becoming a need of the hour; “contactless” business is what the world is looking forward to. The new business jargon “contactless” means that the entire transaction is being done digitally, without requiring any of the parties to the transaction interact physically. While it is not possible to completely digitise all business sectors, however, complete digitisation of certain financial services is well achievable.

With continuous innovations being brought up, financial market has already witnessed a shift from transactions involving huge amount of paper-work to paperless transactions. The next steps are headed towards contactless transactions.

The following write-up intends to provide an introduction to how financial market got digitised, what were the by-products of digitisation, impact of digitisation on financial markets, specifically FinTech lending segment and the way forward.

Journey of digitisation

Digitisation is preparing financial market for the future, where every transaction will be contactless. Financial entities and service providers have already taken steps to facilitate the entire transaction without any physical intervention. Needless to say, the benefits of digitisation to the financial market are evident in the form of cost-efficiency, time-saving, expanded outreach and innovation to name a few.

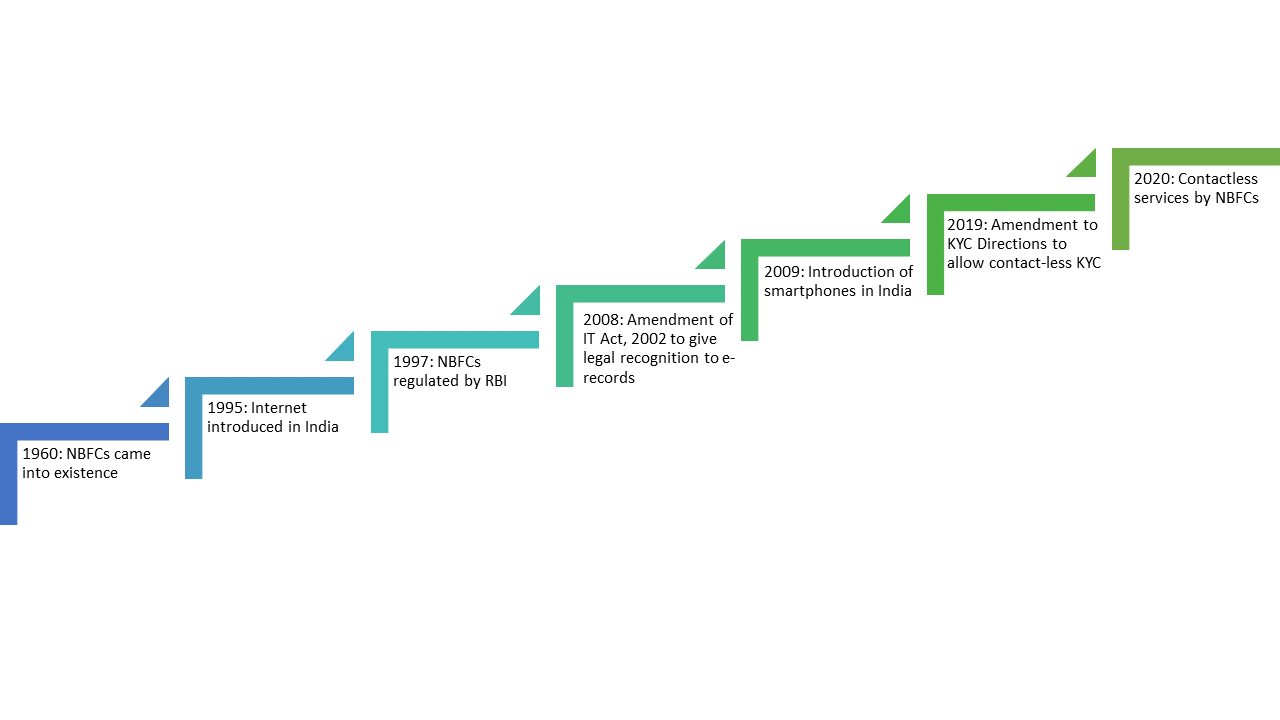

Before delving into how financial entities are turning contactless, let us understand the past and present of the financial entities. The process of digitisation leads to conversion of anything and everything into information i.e. digital signals. The entire process has been a long journey, having its roots way back in 1995, when the Internet was first operated in India followed by the first use of the mobile phones in 2002 and then in 2009 the first smartphones came into being used. It is each of these stages that has evolved into this all-pervasive concept called digitisation.

Milestones in process of digitisation

The process of digitization has seen various phases. The financial market, specifically, the NBFCs have gone through various phases before completely guzzling down digitization. The journey of NBFCs from over the table executions to providing completely contactless services has been shown in the figure below:

From physical to paperless to contactless: the basic difference

Before analysing the impact of digitisation on the financial market, it is important to understand the concept of ‘paperless’ and ‘contactless’ transactions. In layman terms, paperless transactions are those which do not involve execution of any physical documents but physical interaction of the parties for purposes such as identity verification is required. The documents are executed online via electronic or digital signature or through by way of click wrap agreements.

In case of contactless transactions, the documents are executed online and identity verification is also carried out through processes such as video based identification and verification. There is no physical interaction between parties involved in the transaction.

The following table analyses the impact of digitisation on financial transactions by demarcating the steps in a lending process through physical, paperless and contactless modes:

| Stages | Physical process | Paperless process | Contactless process |

| Sourcing the customer | The officer of NBFC interacts with prospective applicants | The website, app or platform (‘Platform’) reaches out to the public to attract customers or the AI based system may target just the prospective customers | Same as paperless process |

| Understanding needs of the customer | The authorised representative speaks to the prospects to understand their financial needs | The Platform provides the prospects with information relating to various products or the AI system may track and identify the needs | Same as paperless process |

| Suggesting a financial product | Based on the needs the officer suggests a suitable product | Based on the analysis of customer data, the system suggests suitable product | Same as paperless process |

| Customer on-boarding | Customer on-boarding is done upon issue of sanction letter | The basic details of customer are obtained for on-boarding on the Platform | Same as paperless process |

| Customer identification | The customer details and documents are identified by the officer during initial meetings | Customer Identification is done by matching the details provided by customer with the physical copy of documents | Digital processes such as Video KYC are used carry out customer identification |

| Customer due-diligence | Background check of customer is done based on the available information and that obtained from the customer and credit information bureaus | Information from Credit Information Agencies, social profiles of customer, tracking of communications and other AI methods etc. are used to carry out due diligence | Same as paperless process |

| Customer acceptance | On signing of formal agreement | By clicking acceptance buttons such as ‘I agree’ on the Platform or execution through digital/electronic signature | Same as paperless process |

| Extending the loan | The loan amount is deposited in the customer’s bank account | The loan amount is credited to the wallet, bank account or prepaid cards etc., as the case may be | Same as paperless process |

| Servicing the loan | The authorised representatives ensures that the loan is serviced | Recovery efforts are made through nudges on Platform. Physical interaction is the last resort | Same as paperless process. However, physical interaction for recovery may not be desirable. |

| Customer data maintenance | After the relationship is ended, physical files are maintained | Cloud-based information systems are the common practice | Same as paperless process |

The manifold repercussions

The outcome of digitisation of the financial markets in India, was a land of opportunities for those operating in financial market, it has also wiped off those who couldn’t keep pace with technological growth. Survival, in financial market, is driven by the ability to cope with rapid technological advancements. The impact of digitisation on financial market, specifically lending related services, can be analysed in the following phases:

Payments coming to online platforms

With mobile density in India reaching to 88.90% in 2019[1], the adoption of digital payments have accelerated in India, showing a rapid growth at a CAGR of 42% in value of digital payments. The value of digital payments to GDP rose to 862% in the FY 2018-19.

Simultaneously, of the total payments made up to Nov 2018, in India, the value of cash payments stood at a mere 19%. The shift from cash payments to digital payments has opened new avenues for financial service providers.

Need for service providers

With everything coming online, and the demand for digital money rising, the need for service providers has also taken birth. Services for transitioning to digital business models and then for operating them are a basic need for FinTech entities and thus, there is a need for various kinds of service providers at different stages.

Deliberate and automatic generation of demand

When payments system came online, financial service providers looked for newer ways of expanding their business. But the market was already operating in its own comfortable state. To disrupt this market and bring in something new, the FinTech service providers introduced the idea of easy credit to the market. When the market got attracted to this idea, digital lending products were introduced. With time, add-ons such as backing by guarantee, indemnity, FLDG etc. were also introduced to these products.

Consequent to digital commercialization, the need for payment service providers also generated automatically and thus, leading to the demand for digital payment products.

Opportunities for service providers

With digitization of non-banking financial activities, many players have found a place for themselves in financial markets and around. While the NBFCs went digital, the advent of digitization also became the entry gate to other service providers such as:

Platform service providers:

In order to enable NBFCs to provide financial services digitally, platform service providers floated digital platforms wherein all the functions relating to a financial transaction, ranging from sourcing of the customer, obtaining KYC information, collating credit information to servicing of the customer etc.

Software as a Service (SaaS) providers:

Such service providers operate on a business model that offers software solutions over the internet, charging their customers based on the usage of the software. Many of the FinTech based NBFCs have turned to such software providers for operating their business on digital platforms. Such service providers also provide specific software for credit score analysis, loan process automation and fraud detection etc.

Payment service providers:

For facilitating transactions in digital mode, it is important that the flow of money is also digitized. Due to this, the demand for payment services such as payments through cards, UPI, e-cash, wallets, digital cash etc. has risen. This demand has created a new segment of service providers in the financial sector.

NBFCs usually enter into partnerships with platform service providers or purchase software from SaaS providers to digitize their business.

Heads-up from the regulator

The recent years have witnessed unimaginable developments in the FinTech sector. Innovations introduced in the recent times have given birth to newer models of business in India. The ability to undertake paperless and contactless transactions has urged NBFCs to achieve Pan India presence. The government has been keen in bringing about a digital revolution in the country and has been coming up with incentives in forms of various schemes for those who shift their business to digital platforms. Regulators have constantly been involved in recognising digital terminology and concepts legally.

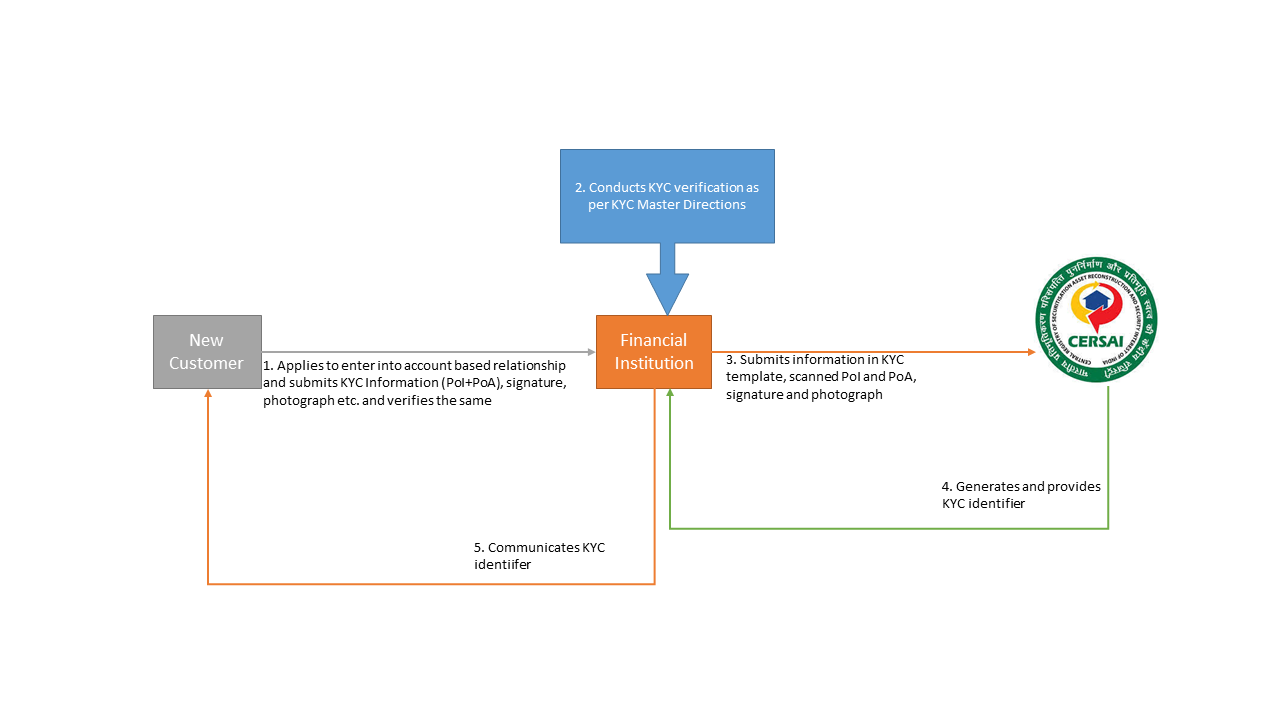

In Indian context, innovation has moved forward hand-in-hand with regulation[2]. The Reserve Bank of India, being the regulator of financial market, has been a key enabler of the digital revolution. The RBI, in its endeavor to support digital transactions has introduced many reforms, the key pillars amongst which are – e-KYC (Know Your Customer), e-Signature, Unified Payment Interface (UPI), Electronic NACH facility and Central KYC Registry.

The regulators have also introduced the concept of Regulatory Sandbox[3] to provide innovative business models an opportunity to operate in real market situations without complying with the regulatory norms in order to establish viability of their innovation.

While these initiatives and providing legal recognition to electronic documents did bring in an era of paperless[4] financial transactions, the banking and non-banking segment of the market still involved physical interaction of the parties to a transaction for the purpose of identity verification. Even the digital KYC process specified by the regulator was also a physical process in disguise[5].

In January 2020, the RBI gave recognition to video KYC, transforming the paperless transactions to complete contactless space[6].

Further, the RBI is also considering a separate regime for regulation of FinTech entities, which would be based on risk-based regulation, ranging from “Disclosure” to “Light-Touch Regulation & Supervision” to a “Tight Regulation and Full-Fledged Supervision”.[7]

Way forward

2019 has seen major revolutions in the FinTech space. Automation of lending process, Video KYC, voice based verification for payments, identity verification using biometrics, social profiling (as a factor of credit check) etc. have been innovations that has entirely transformed the way NBFCs work.

With technological developments becoming a regular thing, the FinTech space is yet to see the best of its innovations. A few innovations that may bring a roundabout change in the FinTech space are in-line and will soon be operable. Some of these are:

- AI-Driven Predictive Financing, which has the ability to find target customers, keep track on their activities and identify the accurate time for offering the product to the customer.

- Enabling recognition of Indian languages in the voice recognition feature of verification.

- Introduction of blockchain based KYC, making KYC data available on a permission based-decentralised platform. This would be a more secure version of data repository with end-to-end encryption of KYC information.

- Introduction of Chatbots and Robo-advisors for interacting with customers, advising suitable financial products, on-boarding, servicing etc. Robots with vernacular capabilities to deal with rural and semi-urban India would also be a reality soon.

Conclusion

Digital business models have received whole-hearted acceptance from the financial market. Digitisation has also opened gates for different service providers to aid the financial market entities. Technology companies are engaged in constantly developing better tools to support such businesses and at the same time the regulators are providing legal recognition to technology and making contactless transactions an all-round success. This is just the foundation and the financial market is yet to see oodles of innovation.

[1] https://www.rbi.org.in/Scripts/PublicationsView.aspx?id=19417

[2] https://www.bis.org/publ/bppdf/bispap106.htm

[3] Our write on Regulatory Sandboxes can be referred here- http://vinodkothari.com/2019/04/safe-in-sandbox-india-provides-cocoon-to-fintech-start-ups/

[4] Paperless here means paperless digital financial transactions

[5] Our write-up on digital KYC process may be read here- http://vinodkothari.com/2019/08/introduction-of-digital-kyc/

[6]Our write-up on amendments to KYC Directions may be read here: http://vinodkothari.com/2020/01/kyc-goes-live-rbi-promotes-seamless-real-time-secured-audiovisual-interaction-with-customers/

[7] https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/WGFR68AA1890D7334D8F8F72CC2399A27F4A.PDF

Bridging the gap between Ind AS 109 and the regulatory framework for NBFCs

-Abhirup Ghosh