CSR – Accounting and taxation

Loading...

Loading...

Loading...

Loading...

Anita Baid | Vice President, Financial Services (anita@vinodkothari.com)

The Supreme Court of India (‘SC’ or ‘Court’) had given its judgement in the matter of Small Scale Industrial Manufacturers Association vs UOI & Ors. and other connected matters on March 23, 2021. The said order of SC put an end to an almost ten months-long legal scuffle that started with the plea for complete waiver of interest, but edged towards waiver of interest on interest, that is, compound interest, charged by lenders during Covid moratorium. From the miseries suffered by people due to the pandemic, to the economic strangulation of trade and activity – the unfinished battle with the pandemic continues. Nevertheless, the SC realised the economic limitation of any Government, even in a welfare state. The SC acknowledged that the economic and fiscal regulatory measures are fields where judges should encroach upon very warily as judges are not experts in these matters. What is best for the economy, and in what manner and to what extent the financial reliefs/ packages be formulated, offered and implemented is ultimately to be decided by the Government and RBI on the aid and advice of the experts.

Compound interest continues to elude judicial acceptance – there are several rulings against compound interest pertaining to arbitral awards, and a lot more for civil awards. In the present ruling as well, observations of the Apex court seem to be indicating that compound interest is penal in nature. This may be surprising to a person of finance, as in the financial world, compound interest is ubiquitous and unquestionable.

In the concluding part of the judgment while dismissing all the petitions, the Court lifted the interim relief granted earlier, pertaining to the NPA status of the borrowers. However, the last tranche of relief in the judgement came for the large borrowers that had loans outstanding/ sanctioned as on February 29, 2020 greater than Rs. 2 crores, and other borrowers who were not eligible to avail compound interest relief as per the Scheme for grant of ex-gratia payment of difference between compound interest and simple interest for six months to borrowers in specified loan accounts (1.3.2020 to 31.8.2020) dated October 23, 2020 (“Ex-Gratia Scheme”). The Court did not find any basis for the limit of Rs 2 crores while granting relief of interest-on-interest (under ex-gratia scheme) to the borrowers. Thus, the Court directed that there shall not be any charge of interest on interest/ penal interest for the period during moratorium for any borrower, irrespective of the quantum of loan, or the category of the borrowers. The lenders should give credit/ adjustment in the next instalment of the loan account or in case the account has been closed, return any amount already recovered, to the concerned borrowers.

Given that the timelines for filing claims under the ex-gratia scheme have expired, it was expected that the Government would be releasing extended/ updated operational guidelines in this regard for adjustment/ refund of the interest on interest charged by the lenders from the borrowers. Further, it seemed that the said directions of the Court would be applicable only to the loan accounts that were eligible and have availed moratorium under the COVID 19 package.

However, as a consequence of the aforesaid ruling, the Reserve Bank of India (‘RBI’) has issued a circular on April 7, 2021 (‘RBI Circular’) instructing the financial institutions to take steps for refund/ adjustment of the interest on interest. While the SC order clearly pertains to the Ex-Gratia Scheme of MoF, the RBI does not talk anywhere about the burden being passed to the GoI.

The RBI Circular is applicable on all lending institutions, that is to say, (a) Commercial Banks (including Small Finance Banks, Local Area Banks and Regional Rural Banks), (b) Primary (Urban) Co-operative Banks/State Co-operative Banks/ District Central, Co-operative Banks, (c) All All-India Financial Institutions, (d) Non-Banking Financial Companies (including Housing Finance Companies).

More than 20 writ petitions were filed with the Supreme Court and the relief sought by them can broadly be classified in four parts – waiver of compound interest/ interest on interest during the moratorium period; waiver of total interest during the moratorium period; extension of moratorium period; and that the economic packages/ reliefs should sector specific. Our write on the issue can be read here.

The contention of the petitioners was that even charging interest on interest/compound interest can be said to be in the form of penal interest. Further, it was argued that the penal interest can be charged only in case of wilful default. In view of the effect of pandemic due to Covid19 and even otherwise, there was a deferment of payment of loan during the moratorium period as per RBI circulars, hence, it cannot be said that there is any wilful default which warrants interest on interest/penal interest/compound interest. The appeal was that there should not be any interest on interest/penal interest/compound interest charged for and during the moratorium period.

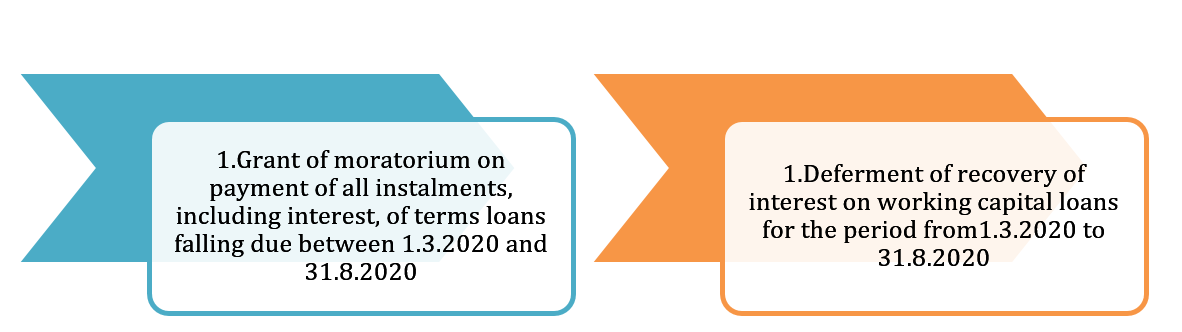

The Central Government and RBI had already provided the following reliefs to mitigate the burden of debt servicing brought about by disruptions on account of Covid19 pandemic:

The nature of moratorium was to provide a temporary standstill on payment of both, principal and interest thereby providing relief to the borrowers in two ways, namely, the account does not become NPA despite nonpayment of dues; and since there was no reporting to the Credit Information Companies, the moratorium did not adversely impact the credit history of the borrowers.

It is important to understand the concept of “moratorium”- the word “moratorium” is categorically defined by the RBI, while issuing various circulars. The relevant circulars of RBI show that “moratorium” was never intended to be “waiver of interest”, but “deferment of interest”. In other words, if a borrower takes the moratorium benefit, his liability to make payment of contractual interest (both normal interest and interest on interest) gets deferred for a period of three months and subsequently three months thereafter. After a very careful and major consideration of several fiscal and financial criteria, it’s inevitable effects and keeping the uncertainty of the existing situation in mind, the payment of interest and interest on interest was merely deferred and was never waived.

Further, it is to be noticed that while the standstill applicable to bank loans results in the bank not getting its funds back during the period of moratorium, the bank continues to incur cost on bank’s deposits and borrowings. Since a moratorium offers certain advantages to borrowers, there are costs associated with obtaining the benefit of a moratorium and placing the burden of the same on lenders might just shift the burden on the financial sector of the country. If the lenders were to bear this burden, it would necessarily wipe out a substantial and a major part of their net worth, rendering most of the banks unviable and raising a very serious question over their very survival. Even on the occurrence of other calamities like cyclone, earthquake, drought or flood, lenders do not waive interest but provide necessary relief packages to the borrowers. A waiver can only be granted by the Government out of the exchequer. It cannot come out of a system from banks, where credit is created out of the depositor’s funds alone. Any waiver will create a shortfall and a mismatch between the Bank’s assets and liabilities.

Considering the same, the Government had granted the relief of waiver of compound interest during the moratorium period, limited to the most vulnerable categories of borrowers, that is, MSME loans and personal loans up to Rs. 2 crores. Our write up on the same can be viewed here.

However, the SC felt that there is no justification to restrict the relief of not charging interest on interest with respect to the loans up to Rs. 2 crores only and that too restricted to certain categories. Accordingly, the SC had directed that directed that there shall not be any charge of interest on interest/compound interest/penal interest for the period during the moratorium and any amount already recovered under the same head, namely, interest on interest/penal interest/compound interest shall be refunded to the concerned borrowers and to be given credit/adjusted in the next instalment of the loan account.

The ruling however, did not clarify as to who shall bear the burden of the waiver of such interest on interest. Further, the RBI Circular seems to place the burden on the lenders and not wait for the Government to come up with a relief scheme or extend the existing ex-gratia scheme.

Coverage of Lenders

All lending institutions are covered under the ambit of the RBI Circular. The coverage includes all HFCs and NBFCs, irrespective of the asset size. Clearly, non-banking non-financial entities, or unincorporated bodies are not covered by the Circular.

Coverage of Borrowers

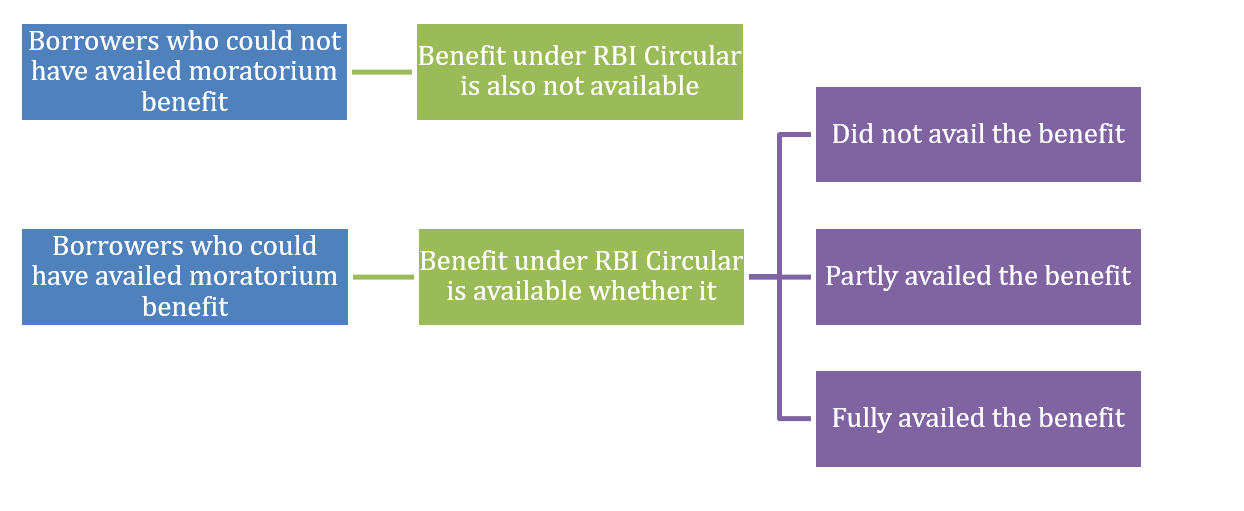

The borrowers eligible as per March 27 Circular (COVID-19 – Regulatory Package) were those who have availed term loans (including agricultural term loans, retail and crop loans) and working capital financing in the form of cash credit/ overdraft. Certain categories of borrowers were ineligible under the March 27 Circular such as those which were not standard assets as on 1st March 2020. Hence, loans already classified as NPA continued with further asset classification deterioration during the moratorium period in case of non-payment.

The question that arises is whether the benefit under the RBI Circular is limited to any particular type of facility? The benefit of the RBI Circular is to be provided to all borrowers, including those who had availed of working capital facilities during the moratorium period. Further, the benefit is irrespective of the amount sanctioned or outstanding and irrespective of whether moratorium had been fully or partially availed, or not availed. However, this should include only those loans that were originally eligible to claim the moratorium but did not claim it or claimed partially or fully.

Thus, all corporate borrowers, including NBFCs who may have borrowed from banks, are apparently eligible for the relief.

Another crucial aspect is whether the benefit is applicable to facilities which have been repaid, prepaid during the moratorium period? If so, upto what date? The benefit must be provided to all eligible loans existing at the time of moratorium but has been repaid as on date.

Coverage of facilities

Both term loans as well as working capital facilities are covered. Facilities which are not in the nature of loans do not seem to be covered. Further, facilities for which the Covid moratorium was not applicable also do not seem to be covered. Examples are: unfunded facilities, loans against shares, invoice financing, factoring, financial leases, etc. In addition, borrowing by way of capital market instruments such as bonds, debentures, CP, etc are not covered by the RBI Circular.

Questions will also arise as to whether lenders will be liable to provide the relief in case of those loans which are securitised, assigned under DA transactions or transacted under co-lending arrangement? We have covered these questions in our detailed FAQs on the moratorium 1.0 and 2.0.

Since the moratorium benefit was to be extended only to such installments that were falling due during the said moratorium period. Hence, only those borrowers were eligible for availing moratorium who were standard as on February 29, 2020 and whose installments fell due during the moratorium period. Accordingly, there can be the following situations:

Burden of interest on interest

The SC order was with reference to the Central Govt decision vide Ex-Gratia Scheme. Among other things, the petitioners had challenged that there was no basis for limiting the amount of eligible facilities to Rs 2 crores, or limiting the facility only to categories of borrowers specified in the Ex-Gratia Scheme. As per the GoI decision, the benefit was to be granted by lending institutions to the borrowers, and correspondingly, there was a provision for making a claim against SBI, acting as the banker for the GoI.

The SC order is an order upon the UoI. Neither were individual banks/NBFCs parties to the writ petition, nor does it seem logical that the order of the Court may require parties to refund or adjust interest which they charged as per their lending contracts. The UoI may be required to extend a benefit by way of Covid relief, but it does not seem logical that the burden may be imposed on each of the lending institutions, who, incidentally, did not even have the chance to take part in the proceedings before the apex court.

Hence, it seems that the impact of the SC order is only to extend the benefit of the Ex-Gratia Scheme to all borrowers, but the mechanics of the original circular, viz., lending institutions to file a counterclaim against the UoI through SBI, should apply here too.

Accounting disclosure for FY 20-21

The RBI Circular talks about a disclosure for the adjustment or refund to be reflected in the financial statements for FY 20-21.

In terms of accounting standards, the question whether the liability for refund or adjustment of the compound interest is a liability or a provision will be answered with reference to Ind AS 37 Provisions, Contingent Liabilities and Contingent Assets. Since the RBI Circular may be seen as creating a liability as on 31st March, 2021, the lending institution may simply adjust the differential amount [that is, compound interest – simple interest on the Base Amount] into the ongoing account of the customer. If such a liability has been booked, there is no question of any provision.

The computation of the differential amount will have to be done for each borrower. Hence, any form of macro computation does not seem feasible. Therefore, there will not be much of a difference between a provision and a liability.

Accounting for the refund in FY 20-21 by the borrowers

If the lending institution makes a provision, can the borrower book a receivable by crediting interest paid or provided? The answer seems affirmative.

Mechanism of extending the benefit

Methodology for calculation is to be provided by IBA. In this regard, representation has been made to the Government to bear the burden.

Base amount: If the mode of computation as provided in the RBI Circular is to be followed [IBA’s methodology will be awaited], then the computation will be based on the amount outstanding as on 1st March 2020.

Computation: On the Base amount, the differential amount will be CI- SI.

If the facility has been fully repaid during the moratorium period, the Differential Amount will run upto the date of the repayment.

Actionables

A board approved policy is to be put in place immediately. In this regard, the concern is whether the lenders can modify existing moratorium policy or adopt a new policy altogether? In our opinion, the existing policy itself may be amended to give effect to the RBI Circular or alternatively a new policy may be adopted.

Also, there is no timeline prescribed as to by when are these actionables required. However, since there are certain disclosure requirements in the financials for the FY 2020-21, the policy must be in place before the financials are approved by the Board of the respective lenders.

The lender may await the instructions to be issued by the Government and the methodology to be prescribed by IBA. Logically, the same method as was provided under the Ex-Gratia Scheme should be applicable. Accordingly, lenders may create provisions for the refund of the excess interest charged and whether corresponding receivable will be shown would depend on whether the same is granted by the Government.

The RBI moratorium notifications freezed the delinquency status of the loan accounts, which availed moratorium benefit under the scheme. It essentially meant that asset classification standstill was imposed for accounts where the benefit of moratorium was extended. A counter obligation on Credit Information Companies (CIC) was also imposed to ensure credit history of the borrowers is not impacted negatively, which are availing benefits under the scheme.

Various writ petitions were filed with the SC seeking an extended relief in terms of relaxation in reporting the NPA status to the credit bureaus. Hence, while hearing the petition of Gajendra Sharma Vs Union of India & Anr. and other writ petitions, the SC granted stay on NPA classification in its order dated September 03, 2020. The said order stated that:

“In view of the above, the accounts which were not declared NPA till 31.08.2020 shall not be declared NPA till further orders.”

The intent of granting such a stay was to provide interim relief to the borrowers who have been adversely affected by the pandemic, by not classifying and reporting their accounts as NA and thereby impacting their credit score.

In its latest judgment, the SC has directed that the interim relief granted earlier not to declare the accounts of respective borrowers as NPA stands vacated. We have also covered the same in our write up.

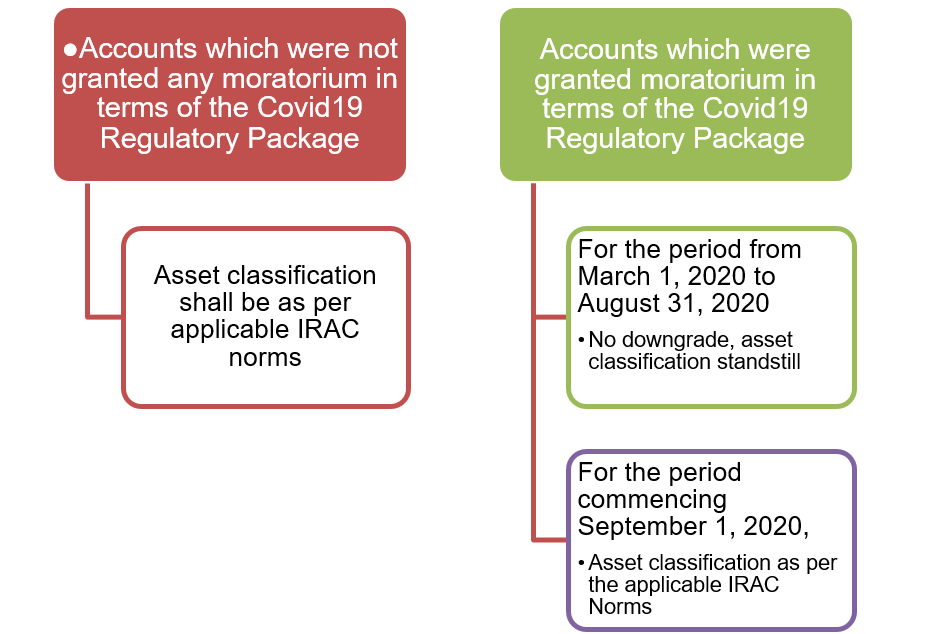

As a consequence of the SC order, the RBI Circular has clarified the asset classification as follows:

This would mean that after September 1, 2020 though there was a freeze on NPA classification, the same cannot be construed as a freeze on DPD counting. The DPD counting has to be in continuation from the due date of the EMI. The accounts classified as standard, but in default of more than 90 DPD may now be classified NPA, since the freeze on NPA classification is lifted by the SC and directed by the RBI as well.

-A LIMPID VIEW ON MINORITY PROTECTION RIGHTS UNDER INDIAN CORPORATE LAW

Sharon Pinto, Manager, corplaw@vinodkothari.com

The Ruling of the Supreme Court (SC) in this case has shed light on several important aspects related to majority versus the minority rule, oppression and mismanagement, role of Non-Executive Directors (NEDs), scope and powers of the Tribunal in providing relief to any matter under section 242 of the Companies Act, 2013.

This article critically discusses on the various aspects of principles of law emanating from the instant ruling.

Section 241 of the Companies Act, 2013 (‘Act, 2013’/ ‘Act’) provides that any member of a company who complains that:

(a) the affairs of the company have been or are being conducted in a manner prejudicial to public interest or oppressive to him or any other member or members or to the interests of the company; or

(b) the material change, not being a change brought about by, or in the interests of any class of shareholders of the company, has taken place in the management or control of the company, whether by an alteration in the Board of Directors, or manager, or in the ownership of the company’s shares, and that by reason of such change, it is likely that the affairs of the company will be conducted in a manner prejudicial to its interests or its members or any class of members, may apply to the Tribunal, provided such member has a right to apply under Section 244 of the Act.

Further, the Act under Section 244 specifies not less than one hundred members of the company or not less than one-tenth of the total number of its members, whichever is less, or any member or members holding not less than one tenth of the issued share capital of the company,

may make an application on the aforesaid grounds unless the said requirement is waived by the Tribunal on an application made by the applicant.

The Tribunal is empowered under the provision of Section 242 of the Act to make such order as it deems fit, on receipt of such an application, if it is of the opinion that:

a) the company’s affairs have been or are being conducted in a manner prejudicial or oppressive to any member or members or prejudicial to public interest or in a manner prejudicial to the interests of the company; and

(b) that to wind up the company would unfairly prejudice such member or members, but that otherwise the facts would justify the making of a winding-up order on the ground that it was just and equitable that the company should be wound up.

By delving into the legislative history of oppression and mismanagement, the SC stated that prejudice to public interest and prejudice to the interests of any member or members were not among the parameters prescribed in the 1913 Act, but under the 1956 Act, prejudice to public interest was included both under the provision relating to oppression and also under the provision relating to mismanagement. Prejudice to the interest of the company was included only in the provision relating to mismanagement. Later, the Act, saw the clubbing of oppression and mismanagement under the same provision and general grounds prescribed are conduct –

The Honorable Court also noted the shift between the conduct of company’s affairs in a prejudicial manner as mentioned above to have been ‘present and continuing’ under the 1913 Act and 1956 Act, whereas, ‘past, present and a continuous’ conduct of affairs of the company can be considered under the present form of statute, although acts of distant past are not to be considered.

As per the provisions stated under the current statute, existence of a dual criteria for invoking oppression and mismanagement is a pre-requisite. Along with the prejudicial conduct of company’s affairs as stated above, the circumstances should be such that they form just and equitable grounds for the winding up of the company, although such winding up may cause unfair prejudice against the members. Thus, the onus of proof for establishing the aforementioned dual criteria rests on the members proposing a case of oppression and mismanagement. If the Tribunal is of the opinion that acts of the company have given rise to such a situation that requires giving such relief as mentioned under section 241 for disposing the matter without winding up of the company.

This ruling has shed significant light on the scope of the powers of the Tribunal prescribed under the Act. The Apex Court stated that the rights of the appellate tribunal are curtailed to the matters put forth before the NCLT at the time of the original petition. Therefore, no fresh matters can be decided by the NCLAT as it is not the original court of dispute. Further, NCLT is the final court of fact. Thus, the facts of the case taken up, confirmed or set aside by the NCLT cannot be questioned at the NCLAT, unless the same pertains to the question of law or have been specifically appealed against.

Sub-section (1) of section 242 of the Act states “the Tribunal may, with a view to bringing to an end the matters complained of, make such order as it thinks fit”. Thus, Section 242 confers the Tribunal with the power to make an order directing several actions. However it has been established under this ruling that such powers of the Tribunal are bound by the reliefs enlisted under the provisions and it may make any supplementary orders which are necessary for putting an end to the matters complained of and giving effect to the order made under the provision. Therefore it is beyond the scope of the Tribunal, under the garb of this provision, to make orders which are specifically barred by law under any other Act in force, for instance reinstatement of a director. It is also established that a contract of personal services cannot be enforced by the Tribunal and at the most it stands as an employment dispute. Further, it is beyond the powers of the Tribunal to set aside an article, unless an amendment of such article has amounted to prejudice or oppressive conduct against the members or the company, as the members of the company enter the company having read and agreed the terms of contract and cannot later question the same.

Failed business decisions and the removal of a person from directorship cannot be projected as acts oppressive or prejudicial to the interests of the minorities. Even in cases where the Tribunal finds that the removal of a Director was not in accordance with law or was not justified on facts, the Tribunal cannot grant a relief under Section 242 unless the removal was oppressive or prejudicial. Thus it has to be established that such a removal has amounted to oppression and unfair prejudice to the interests of the minority shareholders or the company, irrespective of the legality of the removal.

Further, mere acts of removal of an executive chairperson or a director from the company cannot be considered to trigger the basis for just and equitable grounds for winding up of the company. The SC referred to the case of Hanuman Prasad Bagri & Ors. vs. Bagress Cereals Pvt; (2001) 4 SCC 420. Ltd. The removal of director which has not been made in accordance with law or is not justified by the facts and made with the intent to oppress or prejudice the interests of some members may provide for relief under section 242 of the Act.

The Apex Court further stated that in the given case, since the position of Executive Chairman is not recognized by law, the removal was not required to be executed at a general meeting. While the SC took this view, however, the attention of the SC was not drawn to the fact that whether a person is designated as such or not, on being an executive chairperson, it is a general practice to designate one of the directors as an executive chairperson as per the Articles of the company and therefore, attract compliance under Section 196 and Section 169 of the Act.

The law provides for certain items not expressly stated in the agenda, which is circulated prior to the board meeting to be taken up at the meeting itself with the consent of majority of the directors. Citing the judgment in the case of M.I. Builders Pvt. Limited vs. Radhey Shyam Sahu & Others, the stance of the SC remained unclear on whether any important items which necessitate deliberations and consultation of the directors can be tabled at the meeting as per the provision, it is an important question to ponder upon. The requirement of sending an adequate notice with the items to be discussed is an important requirement, so as to enable the directors to consider and plan their schedule as well as action to attend and participate in the meeting. Thus it may be detrimental to the company if an important agenda item is tabled at the meeting with no prior intimation given to the directors.

In order to invoke an order under the provision for oppression and mismanagement there is a necessity of just and equitable grounds amounting to winding up of the company. The SC established by various judgments that such grounds can be said to exist when there is a justifiable lack of confidence in the conduct and management of the company’s affairs. The concept of just and equitable grounds flows from the Law of Partnership and has its roots in probity, good faith and mutual confidence. However for imposing that the organization is in fact in the form of a quasi-partnership, the same has to be properly established in the pleadings. A company however small or domestic cannot per se, be considered a quasi-partnership and shall remain to be a company, the members of which have subscribed to the articles and agreed to conduct business together.

A better understanding of the grounds that would make a just and equitable cause for winding up of the company can be drawn from the case decided by the House of Lords in the matter of Lau V. Chu, where it was established that a situation of a functional deadlock where the members have lost faith in the ability of the management to conduct affairs of the company, leading to frustration in the shareholders in a manner that the company cannot operate tantamount to such a just and equitable cause, irrespective of whether the structure of the company is that of a quasi-partnership or not. On the other hand, in cases where a breakdown of faith between members is proposed as a ground purporting winding up, without the existence of a management deadlock, it is necessary to establish that there exists a quasi-partnership which is based on mutual faith among the partner as suggested earlier.

A person who willingly becomes a shareholder and thereby subscribes to the Articles of Association (AoA) and who was a willing and consenting party to the amendments carried out to those Articles, cannot later on challenge those Articles. The same would tantamount to requesting the Court to rewrite a contract to which he became a party with eyes wide open. Since the SC has not held the power of the company to pass a special resolution for enforcing transfer of shares of a member (expulsion clause) under the AoA to be illegal, there should not be any question on considering it to be illegal. It has been established that unless such clause has been inserted as an amendment in a manner prejudicial to the rights of certain members of the company, the same cannot be contested against. It should also be noted that it is beyond the powers of the Tribunal to restrict or set aside any articles of the company.

It was held that, affirmative voting rights for the nominees of institutions which hold majority of shares in companies have always been accepted and recognized globally. Therefore, an article empowering nominated directors with such rights was not ruled out by the court. This view was based on the fact that if an institution happens to be a shareholder, and a notice of a meeting either of the Board or of the General body is issued, pre-consultation is justified for the institution to have an idea about the stand to be taken by them in the forthcoming meeting. However, the same poses serious questions on the independence of the directors and disposal of independent judgement as is required under the provision of Section 166 of the Act. The view of the court in this matter is such that not all directors are required to be independent, as they may represent the interest of their nominators. Nevertheless, it is to be understood that such nominated directors have dual fiduciary duty towards the institution as well as towards the company and the same has to be balanced. Further in case of a clash between the two, the statute can be interpreted such that the company’s interest shall override the interest of the investor institute as enshrined under the duties of a director.

Our other related write-ups dealing with accustomed to act are as follows:

It is the duty of every director irrespective whether they are appointed as Independent Directors under Section 149 of the Act or as appointees of certain shareholders or institutions as per the provisions of Section 152, to uphold the interest of the company and all the stakeholders at large. The position of nominee directors of the company was established by referring the judgments given in Re: Neath Rugby Limited and Central Bank of Ecuador and others vs. Conticorp SA and others (Bahamas), However, as discussed before, it cannot be denied that the nominee directors have dual fiduciary duties – one of which is the shareholder which nominated them and the other, is the company on whose Board they are nominated. While balancing the two, they have to ascertain that the interests of the company at large are safe-guarded and thus the company’s interest would triumph over the interest of the nominator institute. The nominee directors are therefore required to ensure both public and private interest while disposing their functions as directors. However, carrying this dual responsibility, they cannot be considered devoid of having an independent opinion as the same would contradict the basic duties of a director irrespective of the manner of appointment of such a director and may result in a detrimental situation for the company.

Conclusion

The ruling has clarified various important questions of law as discussed above, although there exist certain areas not touched upon by the court which would require further interpretation and rulings. While the burden of proof lies on the members claiming a relief under the provisions of the oppression and mismanagement, the Tribunal is required to exercise utmost care as to fulfillment of the requirement as intended behind the provisions. The essence of the provision is the existence of malafide actions of the management and conduct of affairs of the company in an unfair and prejudicial manner, which when evidenced can be sought relief against without winding up the company. Further, directors and management of the company have the primary responsibility of protecting the rights of the company, while balancing between profit and probity and the same cannot be compromised.

-Megha Mittal & Ajay Kumar

The idea that directors owe a fiduciary duty towards the company has been deep instilled in the very being of the corporate world – not only in spirit, but also in law. Section 166 of the Companies Act, 2013 (‘Act’) provides that “a director shall act in good faith in order to promote the objects of the company for the benefit of its members as a whole, and in the best interests of the company, its employees, the shareholders, the community and for the protection of environment.” While section 166 of the Companies Act, 2013 sets out the duties of a director towards the company and its stakeholders in general, one must note that a company also has certain specific set of stakeholders, say lenders, whose interests must also be taken care of – enter “Nominee Directors.”

Nominee directors are usually appointed by financial institutions or investors, generally referred to as nominators, on the board of the borrower company for the purpose of representing and safeguarding their interest thereof. However, regardless of its appointment by a specific stakeholder, a Nominee Director is not relieved of his general duties as a director of the company inter-alia duties under section 166 of the Act. This dual role of a Nominee Director has given way to years of debate with respect to a Nominee Director’s actions affecting the company vis-à-vis its nominator.

While much has been deliberated on this state of pseudo-conflict, the conundrum has now come to rest as the Hon’ble Supreme Court, in its landmark judgement in Tata Consultancy Services Limited v. Cyrus Investments Private Limited & Ors. clarified that while a nominee director is entitled to take care of the interests of the nominator, he is duty bound to act in the best interests of the company and not fetter his discretion.[1]

In this article, we shall throw light on the role and nature of Nominee Directors, and discuss their rights, duties and actions in case of conflict, in light of the Apex Court’s order in Tata Consultancy vs. Cyrus Investments (supra).