Archive for month: July, 2020

Intricacies of the Draft Framework on Sale of Loans

-Kanakprabha Jethani (kanak@vinodkothari.com)

Background

The draft framework for ‘Sale of Loan Exposures’[1] (‘Draft’) issued by the Reserve Bank of India (RBI) recently provides a detailed framework for sale of all kinds of loan exposures viz. standard, stressed and NPLs. The RBI invited comments and suggestions from the stakeholders on the Draft and has raised a few specific questions for discussion in the Draft.

Presently, there are two separate guidelines, one for sale of standard assets (Direct Assignment guidelines) and one for sale of stressed assets and NPLs (Master Circular on Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances[2])

While we have already prepared a comparative[3] and a detailed analysis[4] for sale of standard loans, we hereby provide an analysis of guidelines relating to sale of stressed assets and NPLs.

Understanding the Existing Framework

The existing framework for sale of loan exposures is posed in bits and pieces. The framework may broadly be understood in the following manner:

| For sale of standard loans (this includes assets falling between 0-90 DPD) | Guidelines on Transactions Involving Transfer of Assets through Direct Assignment (DA) of Cash Flows and the Underlying Securities- Provided in the Master Directions for NBFCs[5] |

| For Sale of stressed loans (this includes NPAs, SMA-2 and standard assets under consortium, 75% of which has been classified as NPA by other lenders and 75% of lenders by value agree to the sale to ARCs) | · Para 6 of Master Circular – Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances

· Notification issued by the RBI on Prudential Framework for Resolution of Stressed Assets[6] · Notification issued by the RBI on Guidelines on Sale of Stressed Assets by Banks[7] |

| For Sale of NPLs (this includes assets falling in the 90+DPD bucket) | · Para 7 of Master Circular – Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances

· Notification issued by the RBI on Guidelines on Sale of Stressed Assets by Banks |

What does the Draft behold?

The Draft proposes a consolidated framework to govern sale of loan exposures and is a combination of certain existing guidelines and some newly introduced ones. Let us delve into key changes introduced in the Draft one by one.

Applicability

Seller

While the existing guidelines were specifically applicable to NBFCs, banks and other financial institutions, the applicability of the Draft is extended to SFBs and All India Financial Institutions (AIFIs) such as NABARD, NHB, SIDBI, EXIM Bank etc.

Purchaser

The existing guidelines were applicable to sale of loans by a financial entity to another. However, this did not prohibit sale of loans to non-financial entities. The only difference was that the rights under SARFAESI and other laws were impacted.

The Draft guidelines specifically state that the sale of sale of loans may be made by the entities mentioned above as sellers to any regulated entity, which is allowed by its statutory or regulatory framework to buy such loans.

Hence, any sale of loans, to entities whose regulatory/statutory framework does not allow such purchase, cannot be done. Further, sale of loan to entities whose regulatory/statutory framework allows such purchase, irrespective of whether such entity is a financial entity or not, shall be governed by the provisions of the Draft.

Nature of Assets

The Draft directions contain separate provisions for sale of standard assets, sale of stressed assets to ARCs and sale of NPAs. Under the existing framework, an asset was said to be standard, till it is classified as NPA i.e. after 90 DPD. The Draft defines stressed assets to include NPAs as well as SMA accounts. Thus, any 0+ DPD account becomes a stressed asset. Due to this, the provisions relating to sale of standard assets, which are broadly in line with the guidelines on DA, shall not apply on assets falling between 1 to 90 DPD.

Since the classification of the asset is strictly based on the number of days past due, it may raise various practical difficulties. For example, if the due date for repayment of a loan installment is January 1, 2020 and there is a grace period of 10 days. The loan is classified as SMA-0 on February 1, 2020 (irrespective of the fact that it is not even 30 days past the grace period) and now, the sale of such loan shall be as per the guidelines for sale of stressed assets.

Recourse against the Transferor/Originator

Under the existing guidelines, the sale to ARCs was allowed on a ‘with’ or ‘without’ recourse basis and sale of NPAs to parties other than ARCs was allowed on a non-recourse basis only. The Draft clearly states that any sale of loans shall be on a ‘without recourse’ basis only. While there will be no impact on sale of standard assets and sale NPAs to parties other than ARCs, the transactions of sale of stressed assets to ARCs shall certainly be affected.

Treatment of loans given for on-lending

The Draft contains specific provisions with respect to the loans that were granted by the originator for on-lending. Para 51 of the Draft states that “Lenders may also purchase stressed assets from other lenders even if such assets had been created out of funds lent by the transferee to the transferor subject to all the conditions specified in these directions.”

Let us take an example to understand this:

A is an NBFC, which has given out a loan amounting to Rs. 100 @ 5% p.a. to B, which is another NBFC. Now B, gives out loans of Rs. 20 each @ 7% p.a. to 5 individuals.

Now, A can purchase these 5 loans from B, when they become stressed i.e. 0+ DPD. Here, it is clearly visible that the risk undertaken by B has no risk at all. The funds for lending have been provided by A. B keeps the assets in its books only till they are standard. As soon as assets turn SMA-0, B will remove them from its books sell them off to A. Additionally, till the time assets were standard, B earned a spread of 2%.

Manner of Transfer

The Draft defines transfer as- “transfer” means a transfer of economic interest in loan exposures in the manner prescribed in these directions, and includes loan participations and transactions in which the loan exposure remains on the books of the transferor even after the said transaction.

Para 9 contradicts the definition, requiring a legal separation of the asset from the books of the transferor. Tis issue has been discussed at length in our write-up titled “Originated to transfer- new RBI regime on loan sales permits risk transfers.[8]”

The Draft further specifies that the sale/transfer of loans may be done by way of assignment or novation. Presently, most of such transactions are effected through assignment only. The loan agreement usually contains a clause whereby the borrowers gives consent to the lender to sell the loan to a third party. In case such a clause is not there in the loan agreement, the sale of loan would require consent of all the parties to the agreement, including the borrower. In this case, the transfer of loans will have to be effected through novation of the agreement.

The Draft simply clarifies that transfer may be done through either of the modes. We do not see any practical implication as such.

Asset Classification

The asset classification criteria has been divided into 2 categories:

- If the transferee has existing exposure to the same borrower: The asset classification shall be the same as that of the existing exposure in books of the transferee

- If the transferee does not have an existing exposure to the same borrower: The asset acquired shall be classified as standard and thereafter the classification shall be determined based on the record of recovery

If the existing exposure is not standard in the books, the asset classification of the acquired asset shall also be as per the existing exposure. This seems to be derived from the asset classification practices followed earlier to determine stress in the assets i.e. if the borrower is defaulting in one of the exposures, it is likely to delay/default in repayment of other exposures as well.

However, this shall increase the provisioning requirements for the transferee and thus, may be a demotivating factor for sale of stressed assets.

MHP requirements

The Draft extends MHP requirements to ARCs as well. The business of ARCs includes frequent selling and buying of loans and portfolios. Putting a holding requirement of 12 months may slow down the business.

On the other hand, this may ensure that ARCs put better recovery efforts, before selling the loans to other entities.

Reporting Requirements

The existing guidelines did not lay the responsibility of reporting to CIC on any of the parties. Thus, the same was determines by the agreement between the parties. Usually, in case of sale to ARCs, the reporting is done by the ARCs and in case of sale to banks/FIs, the reporting is done by the originator only (since originator usually acts as a servicer).

The Draft specifically lays the responsibility of reporting on the transferee. Reasonably, the servicer of the loans has entire information of the servicing of the loan, repayment patterns etc. and thus, is the most suitable party to do the reporting. Let us examine a few cases with regard to reporting:

| Transferee | Servicer | Reporting Obligation on | Remarks |

| ARC | ARC | ARC | Since the ARC is servicing the loan, it shall be able to properly report the details to CICs |

| Bank/FI | Originator | Bank/FI | The Bank/FI will have to obtain the servicing details from the originator and then report the same to CICs |

| Bank/FI | Bank/FI | Bank/FI | Since the bank/FI is servicing the loan, it shall be able to properly report the details to CICs |

Hence, the reporting obligation may be placed on the servicer or may be kept open for the parties to decide.

Realisation

The existing guidelines relating to sale of NPAs required the transferor to work out the NPV of the estimated cash flows associated with the realisable value of the assets net of the cost of realisation. At least 10% of the estimated cash flows should be realized in the first year and at least 5% in each half year thereafter, subject to full recovery within three years.

The above requirement is not there in the Draft, the reason for which is unknown.

The Draft provides that in case of sale to ARCs, if the ARC is not able to redeem the SRs/PTCs by the end of resolution period (obviously due to inadequate servicing of the loans) the liability against the same should be written off as loss.

Takeover of standard assets

The Draft allows all the regulated entities, other than the transferor, to take over the assets from ARCs, once they turn standard on successful implementation of resolution plan. Earlier only ARCs were allowed to buy assets from other ARCs. This is a welcome move as it will enable other financial entities to buy assets from ARCs.

Conclusion

The Draft has come with some interesting proposals and the RBI is yet to receive comments on the same from the industry. The representations from the industry and the response of the RBI on the same will formulate the new regime for securitisation.

Our other write-ups may be referred here:

http://vinodkothari.com/2020/06/presentation-on-draft-directions-on-sale-of-loans/

http://vinodkothari.com/2020/06/new-regime-for-securitisation-and-sale-of-financial-assets/

[1] https://www.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=957

[2] https://www.rbi.org.in/Scripts/BS_ViewMasCirculardetails.aspx?id=9908#7

[3] http://vinodkothari.com/2020/06/originated-to-transfer-new-rbi-regime-on-loan-sales-permits-risk-transfers/

[4] http://vinodkothari.com/2020/06/comparison-on-draft-framework-for-sale-of-loans-with-existing-guidelines-and-task-force-recommendations/

[5]https://rbidocs.rbi.org.in/rdocs/notification/PDFs/45MD01092016B52D6E12D49F411DB63F67F2344A4E09.PDF

[6] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11580&Mode=0

[7] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10588&Mode=0

[8] http://vinodkothari.com/2020/06/originated-to-transfer-new-rbi-regime-on-loan-sales-permits-risk-transfers/

Udyam Registration Process

Watch our Youtube video explaining the entire Udyam Registration process here: https://youtu.be/dqm64_oTbnQ

Read our other resources on related topics here –

Recent Trends in Crypto-Industry: India & Abroad

-Megha Mittal

“Opportunity amidst tragedy” would likely be the most suitable phrase to summarise the journey of cryptos during the Global Pandemic- with disruption taking a toll on people and economies, and physical proximities massively restrictred, cryptos have outshone traditional assets, by virtue of its inherent features- easy liquidity, access and digitalisation.

Further, as countries around the globe attempt to stimulate their economies by opening floodgates of liquid funds, the ‘digital natives’ have and are expected to increasingly venture into adventure-some investments- think, cryptos. And while such adventurous investing may be short-lived, the results may infact have a long-lasting impact- it is this expected impact that has sets the ‘bull’ stage for cryptos in times to come.

In this brief note, we cover the recent highlights and developments in the crypto-industry, also discussing developments in the relatively new concepts of stablecoins, crypto-lending.

Udyam Portal: The pristine MSME Registration Process

-Qasim Saif (finserv@vinodkothari.com)

The Indian government has been taking a number of measures to tackle the disruptions caused by the pandemic, giving special focus on small businesses. The small and medium size businesses form the backbone of any economy, specially developing economies like India, hence, the Micro, Small and Medium Enterprises (MSME) are seen as a key player in promoting momentum in economy once movement restrictions and social distancing norms are lifted. In order to stimulate the post-Covid economic scenarios, it is crucial to focus on the growth and development of the MSME sector.

The definition of MSME comes from section 7 of the Micro, Small and Medium Enterprises Development Act, 2006 (‘Act’) . Based on the proposal of the Finance Minister, he Ministry of Micro, Small and Medium Enterprises on 1st June 2020 via notification, amended the definition of MSME in order to increase the scope and hence bringing larger number of firms within the ambit of MSME. As per the revised definition, the classification is based on the investment and turnover of the entity.

The latest definition of MSME as per the notification is as follows-

| Revised Classification applicable w.e.f 1st July 2020 | |||

| Composite Criteria: Investment in Plant & Machinery/equipment and Annual Turnover | |||

| Classification | Micro | Small | Medium |

| Manufacturing Enterprises and Enterprises rendering Services | Investment in Plant and Machinery or Equipment: Not more than Rs.1 crore and Annual Turnover; not more than Rs. 5 crores |

Investment in Plant and Machinery or Equipment: Not more than Rs.10 crore and Annual Turnover; not more than Rs. 50 crores |

Investment in Plant and Machinery or Equipment: Not more than Rs.50 crore and Annual Turnover; not more than Rs. 250 crores |

The aforesaid definition removes the bifurcation of investment limits for Manufacturing and Service industry which were previously existent. Hence, it is expected that large number of service providers would be covered as they tend to have lesser investment in plant and machinery or equipment and turnover as compared to Manufacturing entity with similar profits.

As the changes in classification are to be applicable from 1st July 2020, the Ministry of Micro, Small and Medium Enterprises have come up with a Notification dated 26-06-2020 which provide for a novel method of registration for MSME (‘Udyam Registration’).

The said notification provides for process for registration of MSME which shall become applicable from 1st July 2020, the requirement of Udyam Registration shall also be applicable on existing MSME’s.

Pursuant to the amendment in the definition of MSME and the introduction of procedure for filing the memorandum under the Udyam Registration, it seems that registration as an MSME shall be a necessity and accordingly be considered as a pre-requisite for availing benefit under the various schemes introduced by the Ministry.

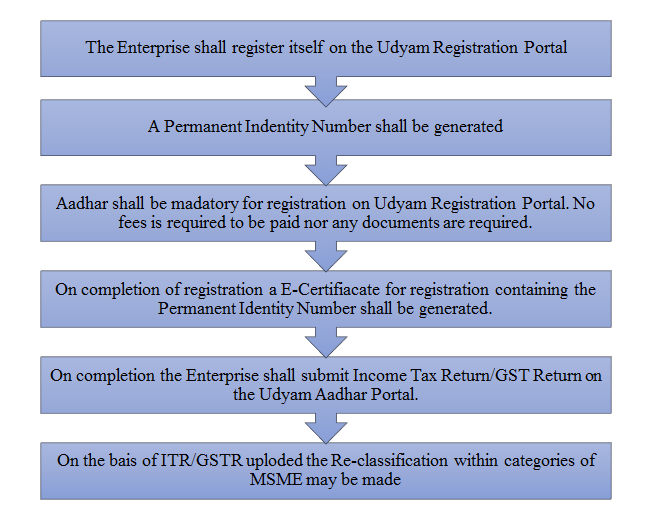

The Process of Registration

Registration on the basis of self-declaration

As per the Udyam Registration requirement it is evident that Udyam Registration can be done on the basis of filing a self-declaration. The relevant extract of the notification states as follows-

“Any person who intends to establish a micro, small or medium enterprise may file Udyam Registration online in the Udyam Registration portal, based on self-declaration with no requirement to upload documents, papers, certificates or proof.”

On review of the registration process on the Udyam Registration portal, it is been observed that the list of major activities contains a specific head for trading activities, land transport as well as an option for selecting ‘Others’. Thus, it may be concluded that trading, transportation and such other activities are included under activities of a service enterprise and shall be required to be registered as an MSME on the Udyam Registration portal.

Requirement of Aadhar

The Aadhaar of following persons shall be required for registration as an MSME.

| Type of Entity | Aadhar of |

| Proprietorship Firm | Proprietor |

| Partnership Firm | Managing Partner |

| HUF | Karta |

| Company / LLP / Co-operatives / Trust / Organisations* | Authorised Signatory |

*PAN and GSTIN of enterprise shall also be required

Non-Availability of Aadhar

In case the person does not have Aadhar, he/she can approach MSME-Development Institutes or District Industries Centres (Single Window Systems) with his Aadhaar enrolment identity slip or copy of Aadhaar enrolment request or bank photo pass book or voter identity card or passport or driving licence and the Single Window Systems will facilitate the process including getting an Aadhaar number and thereafter in the further process of Udyam Registration

Calculation of Investment in Plant, Machinery and Equipment, and Annual Turnover

In order to determine whether the enterprise falls within the limits of MSME and under which category Calculation of amount for Investment in Plant, Machinery and Equipment, and Annual Turnover is required to be calculated.

Plant, Machinery and Equipment.

The Plant, Machinery and Equipment shall have same meaning as under Income Tax Rules, 1962 hence not include land, building and furniture and fittings. Further it shall not include items mentioned in Explanation 1 to Section 7(1) of MSME Act 2006 shall be excluded.

All units with Goods and Services Tax Identification Number (GSTIN) listed against the same Permanent Account Number (PAN) shall be collectively treated as one enterprise and investment figures for all of such entities shall be seen together and only the aggregate values will be considered for deciding the category as micro, small or medium enterprise.

The calculation of investment in plant and machinery or equipment will be linked to the Income Tax Return (ITR) of the previous years. In case of a new enterprise, where no prior ITR is available, the investment will be based on self-declaration of the promoter of the enterprise and such relaxation shall end after the 31st March of the financial year in which it files its first ITR.

However, it shall be noted that in case of new enterprise without any ITR, where calculation is made on self-declaration basis, the purchase (invoice) value of a plant and machinery or equipment, whether purchased first hand or second hand, shall be taken into account excluding Goods and Services Tax (GST).

Turnover

On the similar grounds as investment the turnover shall also be calculated on collective basis for all units with Goods and Services Tax Identification Number (GSTIN) listed against the same Permanent Account Number (PAN) and all such units shall be treated as one enterprise and turnover figures for all of such entities shall be seen together and only the aggregate values will be considered for deciding the category as micro, small or medium enterprise.

Further it shall be noted that the Exports of goods or services or both, shall be excluded while calculating the turnover of any enterprise.

Information as regards turnover and exports turnover for an enterprise shall be linked to the Income Tax Act or the Central Goods and Services Act and the GSTIN. The figures of enterprise which do not have PAN will be considered on self-declaration basis for a period up to 31st March, 2021 and thereafter, PAN and GSTIN shall be mandatory.

Registration by existing MSMEs

In case of existing MSMEs, the registration shall be valid till March 2021. They are required to register themselves under the Udyam Registration portal before the expiry of their registration under Udyog Aadhaar or EM-II.

Updation of information

The registration as an MSME may be obtained based on a self-declaration by the applicant, without submitting any other documents, certificates or proofs of investment in plant and machinery or equipment or turnover. However, once the URM is granted, the MSME is required to update details on the portal, including details of the ITR and the GST Return for the previous financial year and such other additional information as may be required, on self-declaration basis.

Failure to update the relevant information within the period specified [to be specified] in the online Udyam Registration portal will render the enterprise liable for suspension of its status.

Changes in classification

On the basis of information furnished and updated from time to time as well as information from Government sources including ITR/GSTR the classification of enterprise may be changed to a lower to higher category (graduation) or from higher to lower category (reverse-graduation).

In case of graduation an enterprise will maintain its prevailing status till expiry of one year from the close of the year of registration. In case of reverse-graduation of an enterprise, the enterprise will continue in its present category till the closure of the financial year and it will be given the benefit of the changed status only with effect from 1st April of the financial year following the year in which change happened.

Accordingly, it can be inferred that the limits of investment and turnover shall be reckoned on the basis of the ITR and GST returns filed for the previous financial year.

Grievance redressal

The Champions Control Rooms functioning in various institutions and offices of the MSME-Development Institutes along with District Industries Centres in their respective districts shall act as Single Window Systems for facilitating the registration process and further handholding the micro, small and medium enterprises in all possible manner.

In case of any discrepancy or complaint, the General Manager of the District Industries Centre shall undertake an enquiry for verification of the details of Udyam Registration and thereafter forward the matter to the Director or Commissioner or Industry Secretary concerned of the State Government who after giving an opportunity to present its case and based on the findings, may amend the details or recommend to the Ministry of MSME’s, Government of India, for cancellation of the Udyam Registration Certificate.

Further it shall be noted that, if provision for registration under MSME Act, 2006, is violated Section 27 of the Act, provides for a fine which may extend upto one thousand rupees for first conviction and a fine ranging from one thousand to ten thousand rupees for second and subsequent conviction.

Conclusion

The new process provides an easy, quick and simple method for registration that will be linked to information submitted under Income Tax and GST, hence being user friendly as well as keeping a check on reliability of information. The move is intending to promote ease of doing business in lieu of the introduction of Atmanirbhar Bharat scheme.

This process and amended definition would help more MSME to take benefit of government schemes for MSME hence providing them an elevated pedestal to provide a push to kick-start economy after the covid restrictions are lifted.

Our other relevant articles may be referred here:

Partitioning of advisory services from distribution activities

– Harshil Matalia (finserv@vinodkothari.com)

Updated as on July 04, 2020

The Securities and Exchange Board of India (SEBI) had notified SEBI (Investment Advisers) Regulations, 2013 (IA Regulations)[1] in 2013, to regulate activities of Investment Adviser (IA). IA is a person who provides investment advices with respect to financial and investment products to its clients for a consideration. Regulation 3 (1) of the IA Regulations mandates every person which acts as an IA or holds itself out as an IA to register itself unless the person is exempted from registration under regulation 4 of IA Regulations.

A series of consultation papers were issued in 2016, 2017 and 2018, which was followed by another consultation paper[2] proposing amendments in the IA regulations released by SEBI on January 15, 2020. Subsequently, SEBI in its meeting held on February 17, 2020[3] approved the proposals on regulatory changes based on comments received on consultation paper. On July 03, 2020, SEBI has amended IA regulations by introducing SEBI (IA)(Amendment) Regulations, 2020[4] (Amendment Regulations) which shall come into force on September 30, 2020. The main objective to bring such regulatory amendments is to protect the interest of investors and prioritize investors’ interest over the interest of IA.

This write-up provides a brief note on amendments brought by SEBI and its implications on the sector.

Segregation of Advisory & Distribution Activities

As per regulation 15(5) of the IA Regulations, there is an obligation on IA to disclose all conflicts of interest that arises while serving its clients. There is a possibility that IA would advise to invest in products which shall fetch maximum commission or products that may be risky and less sellable in the market. To overcome such a situation, IA must disclose potential conflict of interest to the client.

An IA may be engaged in activities other than investment advisory and hence it is necessary to ensure an arms-length relationship between its activities as an IA and other activities as prescribed under regulation 15(3). Individuals registered as IAs are not allowed to provide distribution or execution services under amended IA Regulations. However, corporate entities registered as IAs can offer execution or distribution services provided that the investment advisory services are offered through separate identifiable division or department.

Further as per recent amendments in Regulation 22 of IA Regulations, “family of IA” shall not provide distribution services to the same client advised by IA. SEBI has inserted a definition of ‘Family of IA’ which shall include individual IA, spouse, children and parents. SEBI has also prescribed the requirement for non-individual IAs to have client level segregation at a group level which means that client can either take advisory or distribution services from the IA and the same client cannot avail any other service, as the case may be, by the same IA or its group entities. Group for this purpose shall mean:

- For Company- an entity which is a holding, subsidiary, fellow subsidiary, associate or an investing company or venturer of the company as per the provisions of Companies Act, 2013 or;

- In any other case- an entity which has controlling interest or which is subject to controlling interest of a non-individual investment adviser.

Implementation of Advice (Execution)

IAs also offer implementation services to its clients i.e. execution of advice provided to the client by charging some reasonable consideration. Thus, the client finds ‘all in one shop’ by availing such services. It has been suggested that IA should clearly declare to the client that it will not seek any power of attorney or authorisations from its clients for auto implementation of investment advice. However, SEBI in Amendment Regulations emphasis that whether to avail implementation services would be sole choice of client and the IA cannot force its client to avail implementation services. Further, IA shall provide implementation services to its advisory clients only through direct schemes/products in the securities market. IA or group or family of IA shall not charge directly or indirectly any consideration including commission or referral fees for providing implementation services. SEBI has also mandated IAs to provide declaration that no consideration shall be received by IA for implementation of advice or execution services. The said declaration has been inserted under item 5 of the First schedule of IA Regulations.

Terms and Conditions of Investment Advisory Services

As per regulation 19, an IA shall maintain copy of agreement with the client, if any, along with other records specified under the said regulation. Since the requirement of advisory agreement is not mandatory under the erstwhile IA Regulations, most of the clients always remain unaware about the terms and conditions of the advisory services that they are going to obtain from IAs.

SEBI has been receiving numerous investor complaints against IAs that they charge exorbitant advisory fees, promising false returns, non-disclosure of detailed fees structure etc. In absence of written agreement between adviser and client, client may not be able to prove his claim.

Therefore, SEBI has mandated an execution of agreement between IA and client which shall specify key terms and conditions, as may be prescribed by SEBI, regarding investment advisory services and this would in turn facilitate transparency.

Advisory Fees

As per the Code of Conduct for IAs prescribed under third schedule of IA Regulations, IAs shall charge fair and reasonable fees to the clients in lieu of providing advisory services. There have been several complaints received by SEBI regarding unreasonable fees being charged by IAs. To restrain such instances and unfair practices, SEBI has inserted Regulation 15A regarding advisory fees that can be charged by IAs to its clients.

The discussion paper has provided two modes of charging fees to clients. IAs can either charge fees by opting Assets under Advice (AUA) mechanism or they can charge fixed fees. SEBI inserted the definition of AUA in Regulation 2(aa) of IA Regulations which shall mean aggregate net asset value of securities and investment products for which IA has rendered investment advice irrespective of whether the implementation services are provided by investment adviser or concluded by the client directly or through other service providers. Under AUA mechanism, fees shall be charged on the basis of underlying assets under advice subject to maximum 2.5 percent of AUA per annum per family across all schemes/ products/ services provided. On other hand, as per fixed fees terms, IA can charge maximum Rs. 75,000 p.a. per family across all schemes/ products/ services provided. The option of choosing mode for charging fees is available with IA, however, change of mode can be effected only after 12 months of on boarding/last change of mode.

In practice, it would be difficult to implement maximum ceiling limit proposed by SEBI. There are certain portfolios that contain high risk products which requires effective skills and essential time to provide any investment advice. In such cases, maximum ceiling would be discouraging for IAs to charge a particular fees to compensate for their efforts. Therefore, in Board memorandum, SEBI has proposed to reconsider and enhance fixed fees from Rs. 75,000 to Rs. 1,25,000 p.a. per ‘family of client’ and fees under AUA mechanism shall be 2.5 percent of AUA per annum per ‘family of client’ across all schemes/ products/ services offered by IA. SEBI inserted a definition of ‘Family of client’ which constitutes individual, dependent spouse, dependent children and dependent parents. IAs would also be required to mention detailed fees structure along with adequate calculations under terms and conditions of advisory agreement. The above-mentioned proposed fees structure is not yet finalised; and is expected to be specified by the SEBI at the earliest. Also, SEBI is expected to bring more clarity that whether IA can charge fees using different fees structure to different categories of customers.

Eligibility Criteria for IAs

The eligibility criteria for IA includes qualification and net worth requirement. Under the erstwhile IA Regulations, regulation 7 and 8 deals with the qualification and net worth requirements respectively. IAs or a principal officer of non-individual IAs shall have minimum qualification as prescribed under the regulation 7.

SEBI has amended the qualification and net worth requirement. SEBI has introduced the definition of “persons associated with investment advice” and “principal officer” in Amendment Regulations. All client facing persons such as sale staff, service relationship managers, client relationship managers, etc. shall be deemed to be persons associated with investment advice, whereas principal officer shall mean managing director/managing partner, designated director etc. who is responsible for overall business operations of non-individual IAs. In terms of the erstwhile IA Regulations, IA shall have either professional qualification/post-graduation or graduation along with five year experience of advisory as mentioned in regulation 7(1). However, as per recent amendments, an individual IA and principal officer in case of non-individual IA shall be required to meet both the criteria that is to have professional qualification/post-graduation along with 5 years experience at all times. The requirement of certification on financial planning (NISM) remains unchanged.

In terms of the erstwhile IA Regulations, IAs which are body corporate shall have a net worth of not less than twenty-five lakh rupees and for IAs who are individuals or partnership firms shall have net tangible assets of value not less than rupees one lakh. However, SEBI has increased minimum net worth criteria to rupees fifty lakhs and rupees five lakhs for non-individual and individual IAs respectively. However, all persons associated with investment advice shall comply with the qualification requirements with minimum two years of experience. The existing IAs shall comply with new eligibility norms within 3 years from the date of commencement of Amendment Regulations. The summary of erstwhile eligibility criteria along with recent amendments is given below:

|

For Individual IAs |

|||

|

Requirement |

Erstwhile |

Amended |

Persons associated with Investment Advice including representatives |

|

Education |

Professional qualification/post-graduation | Professional qualification/post-graduation with 5 years of experience | Professional qualification/post-graduation with 2 years of experience |

| Graduation with 5 years of experience | |||

|

Certification |

NISM | NISM | NISM |

|

Net Worth |

Rs. 1 lakh | Rs. 5 lakhs |

Not applicable |

|

For Non-individual IAs |

|||

|

Requirement |

Erstwhile for representatives |

Amended for principal officer |

Persons associated with Investment Advice including representatives |

|

Education |

Professional qualification/post-graduation | Professional qualification/post-graduation with 5 years of experience | Professional qualification/post-graduation with 2 years of experience |

| Graduation with 5 years of experience | |||

|

Certification |

NISM | NISM | NISM |

|

Net Worth |

Rs. 25 lakhs | Rs. 50 lakhs |

Not applicable |

Use of Nomenclature

In order to obviate misunderstanding and confusion amongst investors regarding the roles and responsibilities of distributors including mutual fund distributors who refer to themselves as ‘independent financial adviser’ or ‘wealth adviser’, it is relevant that the nomenclature should not mislead the investors. Therefore, SEBI has inserted Regulation 3(3) which specifies that any person other than IA registered with SEBI, dealing in distribution of securities shall not use the nomenclature “Independent Financial Adviser (IFA) or Wealth Adviser or any other similar name.

Conversion of Individual IAs to Non-individual IAs

SEBI has inserted additional criteria under regulation 13 which directs individual IA to apply for registration as non-individual IA, in case number of clients of such individual IA exceeds 150 in total.

Conclusion

With these amendments, SEBI took efforts to make robust regulation for investment advisers. Some of the changes would definitely pick up the slacks, however, SEBI should reassess the proposal for ceiling limit on advisory fees and bring more clarity.

[1]https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/jun-2020/1591597643206.pdf#page=1&zoom=page-width,-15,842

[2]https://www.sebi.gov.in/reports-and-statistics/reports/jan-2020/consultation-paper-on-review-of-regulatory-framework-for-investment-advisers-ia-_45685.html

[3] https://www.sebi.gov.in/media/press-releases/feb-2020/sebi-board-meeting_46013.html

[4] http://egazette.nic.in/WriteReadData/2020/220363.pdf and https://www.sebi.gov.in/media/press-releases/jul-2020/sebi-notifies-amendments-to-sebi-investment-advisers-regulations-2013_47006.html