SEBI proposals to ease overheated SME IPO market

SEBI proposes amendments in ICDR and LODR Regulations owing to recent concerns around SME listing

– Sakshi Patil, Executive and Sourish Kundu, Executive| corplaw@vinodkothari.com

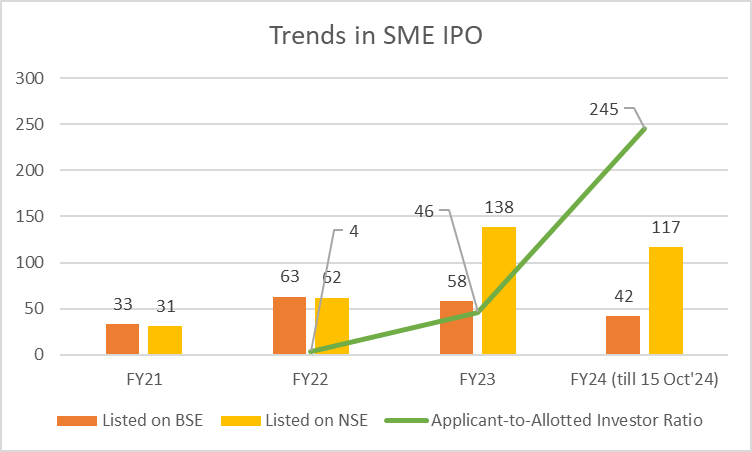

SME IPOs are constantly increasing at an evergrowing rate, with 31 companies listed on SME in FY 21-22 to a total of 138 companies listed in FY 23-24, and 117 companies already listed on SME as of the current FY (till 15th October, 2024) on NSE alone. Not only the number of SME IPOs, the investor participation in such IPOs has also increased substantially, with the applicant to allotted investor ratio from 4X in FY 22 to 46X in FY23 and 245X in FY24. A data on the SME listings during the current and previous FY suggests that, while majority of listed SMEs have booked listing gains, approx 20-30% of such entities have subsequently witnessed a price drop (39 out of 224 companies listed on NSE, 26 out of 91 companies listed on BSE1).

The recent surge in SME IPOs over the last few years, including substantial investor participation in such IPOs, coupled with the recent regulatory concerns w.r.t. diversion of issue proceeds, funding to shell companies, misinflation of revenues etc. has required a re-look into the existing regulatory universe under which SMEs are listed and operate post listing. In August 2024, an advisory was also issued by SEBI regarding investment in the securities of entities listed on SMEs. NSE rolled out stricter eligibility criteria effective September 1, 2024. Greater emphasis on positive cashflow pre listing (w.e.f. Sept 1), capping of 90% over issue price during special pre-open session for SME IPO (w.e.f. July 4) signal the emphasis for investor protection. Following the same, a Consultation Paper has been issued by SEBI, proposing amendments to the provisions of ICDR and LODR Regulations, with a view to strengthen the pre and post-listing requirements for SMEs. Key proposals include restricting the access of SME Exchange to informed investors, and ensuring such IPOs serve the original purpose of making finance available to SMEs for their business growth, and not for funding the promoters’ requirements.

A brief of the 27 proposals, as against the existing requirements and our comments are presented below:

| Particulars | Existing requirement | Proposal under CP | Rationale and Our Comments |

|---|---|---|---|

| Stricter eligibility conditions for SME IPO | |||

| Ineligibility conditions for IPO (Proposal 8) | Currently based on PromotersDirectors Selling shareholders in some cases. | To be extended to promoter group as well. | SME companies are closely held by promoter and promoter groups. Hence, any action against the promoter group may also have a significant bearing on the issuer. |

| Additional eligibility requirements for SME IPO(Proposal 9A & 9B) | Firm/ LLP converted into company can apply for IPO without any cooling period – track record requirements are considered on a combined basis. | Co. which has been converted from LLP or partnership firm, shall be in existence for at least 2 yrs, with restated financial statements post conversion drawn in accordance with Schedule III of CA, 2013.Cooling off of 2 years in case of change of promoter, or introduction of new promoter acquiring 50% or more shareholding prior to filing of DRHP. | Helps in bringing a clearer picture of financial position post conversion. Cooling period in case of change in promoter is to bring steadiness in IPO.Track record should be based on the effective management of new promoter(s) and not past promoter(s). |

| Operating profits (EBIDTA)(Proposal 11) | Positive. | Rs. 3 cr for at least 2 out of 3 immediately preceding FYs. | To ensure financial viability of the company. Our Comments: NSE additionally mandates positive Free cash flow to Equity (FCFE) for at least 2 out of 3 financial years preceding the application. |

| Conversion of Pre-IPO outstanding convertible securities before IPO(Proposal 20) | Conversion not mandatory | Conversion mandatory | In line with the requirement for Main Board IPO. Provides clarity to investors on the company’s capital structure before they invest. |

| Structure of IPO and allotment | |||

| Minimum issue size(Proposal 10) | Not specified | Rs. 10 cr | To ensure companies with significant growth potential access the market.Loans and alternative funding sources typically cater to smaller amounts.Is aligned with BSE’s and NSE’s requirement for Main Board listing. |

| Offer for sale(Proposal 4A & 4B) | No restriction | Dual limits proposedOFS restricted upto 20% of issue size and for selling shareholders, OFS shall not exceed 20% of pre-issue shareholding on a fully diluted basis. | To prevent use of SME listing for dilution of promoter stake. |

| Face value(Proposal 12) | Not Specified | Rs. 10/- per share for existing issued capital and proposed new shares to be issued. | To enable better comparison amongst various issuers. |

| Minimum application size (Proposal 1) | Rs. 1 lakh | Rs. 2 lakh with existing minimum allocation of 35% (book-build issue)/ 50% (fixed price issue) to RIIs, ORRs. 4 lakh (resulting in deletion of RII category for minimum allocation requirements). | Limit participation of retail investors (bidding for upto Rs. 2 lakhs) to protect interest of smaller retail investors;Attract investors with risk taking appetite; Enhance the overall credibility of the SME segment. |

| Minimum no. of allottees (Proposal 3) | 50 | 200 | To ensure sizeable no. of investors Provide liquidity |

| Allotment methodology for Non – institutional investors (NII) category (Proposal 2) | Proportional allotment for NIIs | Draw of lots for minimum bid lot to NIIs divided into 2 categories: ⅓ rd of allocation for application size upto 10L⅔ rd of allocation for application size exceeding 10L | Align allocation methodology with Main Board IPO; Proportional allotment may encourage over-leveraging, over statement of interest and thus at times encourage mispricing. |

| Objects of issue & utilisation of proceeds | |||

| Raising funds for General corporate purpose (GCP) and unidentified acquisition (Proposal 7A & 7B) | GCP < – 25% of issue sizeGCP + unidentified acquisition < – should not exceed 35% of issue size | GCP restricted to lower of 10% of issue size or Rs. 10 cr;Prohibition on raising funds for unidentified acquisition | To reduce the risk of misuse of issue proceeds |

| Repayment of loan of promoter/ promoter group as an object of issue(Proposal 14) | No express prohibition. | Not allowed | To ensure that funds raised through IPO are used for business growth, not for repayment of promoters’ liabilities |

| Funding for working capital (Proposal 15) | No specific requirement | Mandatory statutory auditor certificate on a half-yearly basis for use of working capital funds raised exceeding Rs. 5 Crore, with disclosure of the same in financial statements. | Ensures that working capital funds are appropriately used Our Comments: The requirement of statutory auditor’s certificate is proposed to be made mandatory for all SME IPOs where a monitoring agency is not required to be appointed (see below). A specific mandate for working capital monitoring may not serve any additional purpose. |

| Monitoring of issue proceeds (Proposal 5A, 5B & 5C) | Monitoring agency mandatory if issue size >100 cr | Monitoring agency mandatory if: Issue size >20 cr ORObject of issue includes:funding subsidiary, repay loans/ borrowing of the subsidiary investment in JV/ subsidiaryacquisition In other cases, utilization certificate from statutory auditor on half-yearly basisPlace before AC and board Submit to stock exchange | Reduce risk of misuse or diversionBring more transparency for investors and accountability for issuer Our Comments: Presently, Reg 32(5) of LODR requires statutory auditors to certify the statement w.r.t. Utilisation of funds on an annual basis. The proposal will additionally require the same to be done on a half-yearly basis, in cases where a monitoring agency is not required to be appointed. |

| Disclosure of sources in case of requirement of having firm arrangement of finance for a project(Proposal 16) | No such requirement | Sanction letter to be disclosed in draft offer document and offer document where partial funding is by bank/NBFCs. | Additional diligence and disclosure for investors w.r.t. project appraisal by financial institutions. |

| Exit opportunity for dissenting shareholders in case of change in objects(Proposal 23) | No specific provision | Post-listing exit opportunity for dissenting shareholders in case of changes in the objects or terms, in line with Main Board provisions | Protects the interests of dissenting shareholders, ensuring they have an exit option in case of significant changes post-listing. |

| Promoter contribution and lock-in requirements | |||

| Lock-in of promoter holding(Proposal 6A & 6B) | Minimum Promoter Contribution (MPC) – 3 yrs Excess holding – 1 yr | MPC – 5 yrsExcess – Lock in on 50% to be released after 1 yr and;For remaining 50% to be released after 2 yrs. | To ensure that entire holding is not diluted post the lock in periodTo ensure promoter continues to have skin in game till company is on SME Exchange |

| Securities ineligible for MPC(Proposal 24) | No clarification w.r.t. adjustment of price for corporate action | Price per share for determining MPC eligibility should be adjusted for corporate actions (e.g., bonus, stock split) | Clarifies the pricing mechanism and ensures fairness in determining MPC eligibility, preventing manipulation through corporate actions. |

| Other additional disclosures | |||

| Disclosure of senior level management(Proposal 17) | KMP and SMP details are required to be disclosed in offer document | Disclosure of senior-level employees (e.g., head of sales, plant head, etc.), with their experiencesAdditional disclosure on ESIC/EPF detailsSite visit by merchant banker to form part of DD report and included in material inspection documents in offer document. | Better disclosure w.r.t. Employee strength of the company |

| Merchant banker fees(Proposal 18) | No requirement to disclose issue related fees | Merchant banker fees, by any name, to be disclosed in RHP | Increased transparency – presently such costs exceeds 30-40% of issue size, defeating the primary purpose of fundraising |

| Public comments on DRHP (Proposal 19) | No requirement. | At least 21 days’ for public comments; Disclose on website of SEs and lead managers;Public announcement in 3 newspapers – English, Hindi and regional. | Allows the public to provide feedback during draft offer document stage instead of opening of offer |

| Due diligence certificate by merchant banker(Proposal 21) | Required at the time of submission of offer document to SEs. | Mandatory submission to SE at the time of filing draft offer document. | Ensures that the due diligence process is completed and certified before the public sees the draft offer document. |

| Migration to Main Board | |||

| Migration from SME to Main Board(Proposal 13) | Post-issue face value of capital > Rs. 25 crores pursuant to fresh issue. | Where listed SME is not eligible to migrate, fund raising to be still permitted beyond Rs. 25 crores, subject to compliance with corporate governance norms and disclosure requirements under LODR. | Ensures that company can remain listed on SME platform having post issue face value more than 25cr with light touch of regulations applicable to them related to LODR |

| Corporate Governance Requirements | |||

| Related Party Transactions(Proposal 25) | Exempt from Reg 23 pursuant to Reg 15(2)(b). Compliance as per Companies Act applicable: Meaning of RP [as per section 2(76)]Approval of AC (for all RPTs)Approval of Board (for specified transactions if not in ordinary course or arm’s length)Approval of shareholders (for material RPTs requiring board approval as above) | Reg 23 to be made applicable to SME listed entities.De minimis exemption continues for smaller listed entities [Reg 15(2)(a)]Material RPTs based on turnover thresholds (10% of annual consolidated turnover)Absolute limits of Rs. 1000 crores not applicable. | Enhanced requirements to mitigate risk of circular transactions and abusive RPTs |

| Quarterly corporate governance report [Reg 27](Proposal 26) | Not applicable | Quarterly disclosure w.r.t. composition and meetings of the board and its committees to the stock exchange(s) | Harmonize disclosure requirements for SME and Main Board entitiesEnhancing transparency on functioning of board and committee Our comments: The CP mentions about disclosure of board and committees, however, it is not clear as to whether the other disclosures as are applicable to Main Board entities under the corporate governance report, is also proposed to be extended to SMEs |

| Periodic filings to stock exchanges(Proposal 27) | Half yearly filing of:: Shareholding pattern [Reg 31], Statement of deviation(s) or variation(s) [Reg 32],Financial Results [Reg 33] | To be made on a quarterly basis, at par with Main Board listed entities. | Reflects the financial health and fund utilization by companies; Aligned with requirements applicable to the Main Board. |

Our related resources:

- NSE tightens eligibility criteria for SME listing on NSE Emerge

- BSE and NSE SME Exchange Platforms: Big Opportunities for Small Companies and growing India

- The basics of bringing an IPO

- Based on market data as on 15th October, 2024. Taken from SEBI CP

↩︎