CIV-ilizing Co-investments: SEBI’s new framework for Co-investments under AIF Regulations

Payal Agarwal, Partner and Simrat Singh, Senior Executive | Finserv@vinodkothari.com

Background

Within an AIF structure, funds are committed by the investors and the AIF in turn, through its Investment Manager, makes investments in investee entities in line with the fund’s strategy. Situations may arise where an investee company of the AIF may require additional capital, that the Investment Manager may not be willing to provide out of the fund’s corpus possibly due to multiple reasons such as over-exposure, non-alignment with funding strategy, capital constraints etc.

In such cases, the Manager may encourage investors to commit further funds directly into the investee. This gives rise to what is known as ‘co-investment’ – an investment by limited partners (LPs or investors) in a specific investee alongside, but distinct from, the flagship fund. Globally, these are also called ‘Sidecar’ funds or ‘parallel’ funds.1

Benefits of co-investments

Investors benefit from co-investments primarily in terms of cost efficiency, in the following ways:

- No or lower management fees and a reduced rate of carried interest.2

- Reducing/ removing operational and administrative expenses such as in due diligence process & deal sourcing

- Where management and incentive fees are directly charged on co-investments, they are usually capped and lower than when investing directly into the PE Fund.3

- Not only are headline rates4 typically lower, but management fees are often charged on invested rather than committed capital, reducing fee drag and mitigating the J-Curve.5

For Managers co-investment offers the following advantages:

- Provide access to expanded capital;

- Enables it to pursue larger transactions without over extending the main fund

A Preqin study6 found that 80% of LPs reported better performance from equity co-investments than traditional fund structures.

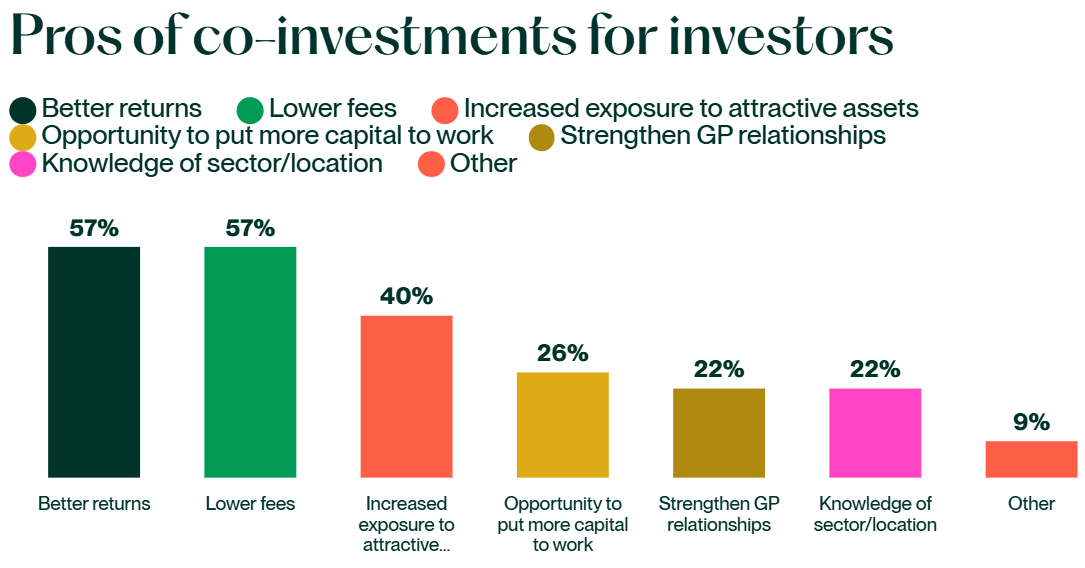

Fig 2: Investor’s perceived benefits of co-investment

Source:A&0 Shearman

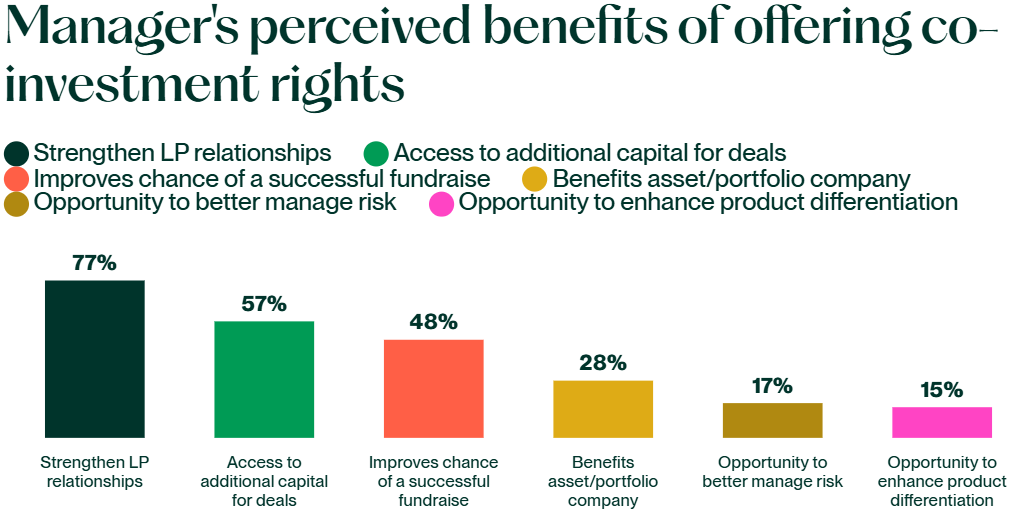

Fig 2: Manager’s perceived benefits of offering co-investments.

Source: A&0 Shearman

Regulating Co-investments by AIFs in India

Co-investments by AIF investors in the investees of AIF were primarily offered in accordance with the SEBI (Portfolio Managers) Regulations, 2020 (“PM Regulations”). In 2021, PM Regulations were amended to regulate AIF Managers offering co-investments by acting as a portfolio manager of the investors (see need for regulating the co-investment structure below). The AIF Regulations, in turn, required the investment manager to be registered under PM Regulations, for providing co-investment related services.

Keeping in view the rising demand for co-investments, SEBI, based on a recent Consultation Paper issued on 9th May 2025, has amended the AIF Regulations, vide notification dated 9th September, 2025 and issued a circular in September 2025 introducing a dedicated framework for co-investments within the AIF regime itself. Note that the recently introduced framework is in addition to and does not completely replace the co-investment framework through PM as provided in the PM Regulations.

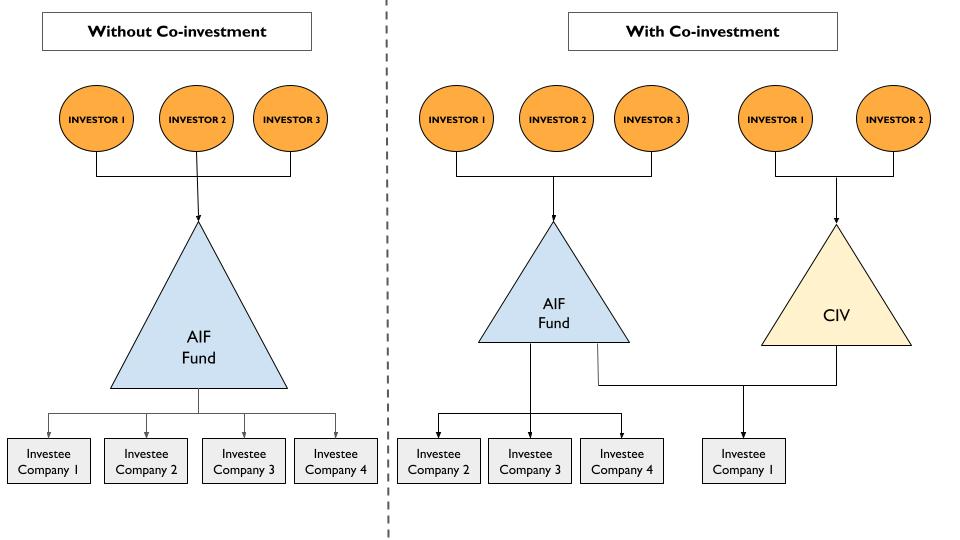

The newly introduced framework refers to co-investments as an affiliate scheme within the main scheme of the fund, in the form of a Co-investment Vehicle Scheme (CIV) and does not require a separate registration by the Investment Manager in the form of Portfolio Manager under PM Regulations.

Interestingly, in May 2025, IFSCA also issued a Circular specifying operational aspects for co-investments by venture capital funds and restricted schemes operating in the IFSC. In this article, we discuss the new framework vis-a-vis the existing PMS route.

Need for regulating co-investments

- Conflicts of interest

- Especially around the timing of exit. Main fund vs. co-investors may have different preferences.

- Voting rights alignment

- Misalignment can fragment decision-making.

- Risk concentration for investors

- Exposure to a single company rather than a diversified portfolio.

- Disclosure and transparency obligations for managers

- Other fund investors need clarity on why the deal was structured as a co-investment.

- Questions may arise on whether the main fund had sufficient capacity to invest.

- Risk of concerns about preferential treatment of select investors.

- Operational issues:

- Warehousing: main fund may initially acquire the investment until co-investment vehicle is ready; requires proper compensation to the fund for interim costs.

- Expense allocation: management costs must be fairly shared between the fund and the co-investment vehicle.

Co-investment through PMS Route – the existing framework

Under the PMS Route, the AIF Manager intending to offer co-investment opportunities to its investors shall first register itself as a ‘Co-investment Portfolio Manager’ (see reg. 2(1)(fa) of PM Regulations) post which it can invest the funds of investors subject to the following conditions:

- 100% of AUM shall be invested in unlisted securities [see reg. 24(4B)];

- Only a manager of a Cat I & II AIF is allowed to offer co-investment;

- The terms of co-investment in an investee company by a co-investor, shall not be more favourable than the terms of investment of the AIF [see proviso to reg. 22(2)]:

- Terms relating to exit of co-investors shall be identical to that of exit of AIF [see proviso to reg. 22(2)];

- Early termination/withdrawal of funds by co-investor shall not be allowed. [see reg. 24(2)(a)]

The AIF Manager, registered as a Co-investment Portfolio Manager, is subject to all the compliances as required under the PM Regulations, read with the circulars issued thereunder, except the following:

- The minimum investment limit of Rs. 50 Lac per investor in case of PMS will not apply [see reg. 23(2)];

- Min. net worth criteria of Rs. 5 Crore shall not apply to such a PM [see reg. 11(e)];

- Appointment of a custodian is not required. (see reg. 26)

- Roles and responsibilities of the compliance officer can be discharged by the principal officer of the Manager. [see reg. 34(1)]

| Particulars | Discretionary | Non-discretionary | Co-investment |

| No. of clients | 1,92,548 | 6,733 | 609 |

| AUM (Rs. Crores) | 33,05,958 | 3,18,685 | 4,674 |

Table 1: No. of co-investment clients and their total AUM as on 31.07.2025.

As per Table 1, it is evident that co-investment under the PMS Regulations has not taken off yet. One of the major reasons is the additional registration & compliance burden associated with this route.

Co-investment through CIV : the recently approved framework

A formal regulatory framework for co-investment has been introduced in the AIF Regulations vide SEBI (Alternative Investment Funds) (Second Amendment) Regulations, 2025. The Amendment Regulations define “co-investment” as:

“Co-investment” means investment made by a Manager or Sponsor or investor of a Category I or II Alternative Investment Fund in unlisted securities of investee companies where such a Category I or Category II Alternative Investment Fund makes investment;”

The framework is restricted to “unlisted securities” only, for the following reasons:

- There is a greater information symmetry in case of unlisted securities;

- In case of investment in listed securities, it is difficult to establish whether an investor’s decision to invest is driven by the fund manager’s advice or based on the investor’s own independent assessment;

- Co-investments are typically undertaken in unlisted entities.

Reg 2(1)(fa) defines co-investment scheme as:

“Co-investment scheme” means a scheme of a Category I or Category II Alternative Investment Fund, which facilitates co-investment to investors of a particular scheme of an Alternative Investment Fund, in unlisted securities of an investee company where the scheme of the Alternative Investment Fund is making investment or has invested;”

The conditions for co-investment through the AIF route is prescribed through the newly inserted Reg 17A to the AIF Regulations read with the Circular dated September 09, 2025. Additionally, the Circular also refers to the implementation standards, if any, formulated by SFA with regard to offering of the co-investment schemes by the AIFs. Since the CIV operates as an affiliate AIF, in order to make it operationally feasible, a CIV has been granted the following exemptions under the AIF Regulations [See reg. 17A(10) of AIF Regulations]:

- No minimum corpus of ₹20 Cr.

- No continuing sponsor/manager interest (2.5%/₹5 Cr).

- Exempt from Placement Memorandum contents, filing modalities, tenure requirement.

- Exempt from 25% single-investee company concentration limit

Investment via PMS vs Investment via CIV of an AIF

Post the AIF Amendment, investors have a choice for investing either through the PMS Route or through the CIV route under AIF Regulations. A comparison between the 2 routes is listed below:

| Aspects | Investing through CIV | Investing through PMS |

|---|---|---|

| Regulatory framework | SEBI (Alternative Investment Funds) Regulations, 2012 | SEBI (Portfolio Managers) Regulations, 2020 |

| Limit on investment by each investor | Upto 3 times of investment made by such investor in the investee company through AIF. | No limit |

| Registration requirement for Manager | No separate registration required | Co-investment Portfolio Manager license mandatory. |

| Kind of securities | only in unlisted securities | only in unlisted securities |

| Mode of investment | Through and in the name of the CIV scheme | Directly in the securities of the investee company. |

| Co-terminus exit | Timing of exit of CIV = Timing of exit of AIF Scheme from such investee company. | Co-terminus exit |

| Eligibility of investor | Only Accredited Investors | Any investor |

| No regulatory bypass | CIV cannot: – Give indirect exposure to such investees where direct exposure is not permitted to the investors; – Create situations needing additional disclosures; – Channel funds where investors are otherwise restricted. | Considered as direct investment by the investor. |

| Ineligibility of investors | Defaulting, excused, or excluded investors of AIF cannot participate in CIV. | No such exclusion. This seems like a regulatory loophole. |

| Operational burden | CIV aggregates co-investors’ exposure; hence, only the Scheme appears on the capital table; Unified voting and simplification of compliance requirements for investees as well | Multiple co-investors appear directly on the investee company’s cap table. Closing times may be different, and operationally difficult for investors and investees to exercise voting rights and ensure compliances at each investor’s level. |

| Scope for co-investment | Managers can extend co-investment services to investors of any AIF managed by them (Sponsor may be same or different) | A Co-investment Portfolio Manager can serve only his own AIF’s investors, and others only if managed by him with the same sponsor |

| Ring-fencing of funds and investments | Separate bank & demat accounts for each CIV | Bank & demat account of investor |

| Leverage restrictions | CIV cannot undertake any leverage. | The PM cannot undertake leverage and invest. |

| Taxation | Tax pass through granted to Cat I & II AIFs make the investors directly liable to tax except on business income of the AIF | Capital gain and DDT payable by investor directly |

| Filing a shelf PM | Managers are required to file a separate Shelf PM for each CIV Scheme. | No such requirement |

Conclusion

Much of the future trajectory of co-investments in India will depend on how both investors and managers weigh the relative merits of the PMS and CIV routes. While the PMS framework comes with higher compliance costs and additional registration requirements, the absence of a maximum cap on investments by the co-investors may still serve as a motivational factor for continued usage of the same. By contrast, the CIV framework seeks to simplify execution and preserve alignment with the parent AIF, although the 3 times’ cap on the co-investor’s share may be a hindrance for investors, thus making the CIV structure less attractive. Recently RBI had also issued Directions for regulated entities investing in AIFs with a view to curb evergreening and excessing investing in AIF structures (see our article on the same). The AIF Manager shall be cognizant of these restrictions in order to ensure there is no bypass through CIV.

Large institutional investors, sovereign funds and pension funds are likely to be the early adopters of CIV structures, given their scale, accredited investor status, and preference for alignment with fund managers. High-net-worth individuals (HNIs) and family offices, on the other hand, may still prefer the PMS route owing to its flexibility and direct exposure. Over time, the regulatory tweaking of these frameworks, if any and the appetite of investors for concentrated exposure will determine how the Indian co-investment landscape unfolds.

- Financing Business Innovation: World Bank ↩︎

- Goldman Sachs: The Case for Co-investments, Strategic Investment Funds: World Bank ↩︎

- Structuring Co-investments in Private Equity: American Bar Association ↩︎

- In private equity, the headline rate (e.g., 2% management fee, 20% carry) is what’s stated in the PPM, but the effective rate investors actually pay is usually lower. This depends on factors like fees on committed vs. invested capital, negotiated discounts or preferential terms, and lifecycle adjustments such as fee step-downs post-investment period. ↩︎

- The J Curve represents the tendency of private equity funds to post negative returns in the initial years and then post increasing returns in later years when the investments mature. The negative returns at the onset of investments may result from investment costs, management fees, an investment portfolio that is yet to mature, and underperforming portfolios that are written off in their early days: Corporate Finance Institute ↩︎

- Private Equity Co-Investment Outlook: Preqin ↩︎

See our other resources on AIFs:

- FAQs on specific due diligence of investors & investments of AIFs

- RBI bars lenders’ investments in AIFs investing in their borrowers

- Capital subject to ‘caps’: RBI relaxes norms for investment by REs in AIFs, subject to threshold limits

- Can CICs invest in AIFs? A Regulatory Paradox

- Trust, but verify: AIFs cannot be used as regulatory arbitrage

- 2020 – Year of change for AIFs

- AIF ail SEBI: Cannot be used for regulatory breach

- PPT on financial and capital markets