Posts

Supreme Court’s Judgment in Bhushan Power and Steel Ltd.: a wake up call for the Resolution Professionals and Committee of Creditors

Team Resolution | resolution@vinodkothari.com

The Supreme Court judgement in the matter of Kalyani Transco v. Bhushan Power and Steel Ltd., set aside the resolution plan for Bhushan Power and Steel Ltd., and directed liquidation, after almost 6 years the resolution plan was approved by National Company Law Tribunal, citing significant gaps in the conduct of corporate insolvency resolution processes – for instance, lapses in meeting statutory timelines, deficiencies in eligibility verification under section 29A, irregularities in plan implementation, judicial overreach by National Company Law Appellate Tribunal, among others.

In this write up, we have made an attempt to discuss significant points of law as discussed by SC in this ruling and also provide our humble comments on the same. Needless to say, many of the concerns highlighted by the SC in this judgment would act as a binding code of conduct for all resolution professionals, CoCs, and even judicial institutions.

Read more →Presentation on IBBI’s Discussion Paper on ‘Streamlining Processes under the Code: Reforms for Enhanced Efficiency and Outcomes’

– Team Resolution | resolution@vinodkothari.com

See more:

Discussion on IBBI Discussion Paper dated 4th February, 2025

Importance of Filing Timely Claims in IBC: A Guide for Government Departments

– Neha Malu, Deputy Associate | resolution@vinodkothari.com

Introduction

In the landscape of corporate insolvency, the timely submission of claims by creditors is of paramount importance. The Insolvency and Bankruptcy Code, 2016 (“IBC”) provides a structured process for dealing with corporate debtors in distress. This article highlights the necessity of adhering to prescribed timelines for claim submission and underscores the repercussions of delays, drawing on pertinent judicial rulings. Additionally, it offers a comprehensive overview for government departments on the process of filing claims under the IBC.

Now, in case of IBC, there are two stages-

- Corporate insolvency resolution process (CIRP) stage, and

- Liquidation stage.

Upon initiation of CIRP, an interim resolution professional is appointed who makes a public announcement in Form A within 3 days of his appointment. The respective creditors of the concerned corporate debtor are required to file their claims within the timeline specified herein below. However, it is to be noted that if the CIRP of the concerned corporate debtor fails, the creditors are also required to submit their claims once again in the liquidation process.

Read more →CIRP (Second Amendment Regulations), 2023 – A snapshot

– Team Resolution | resolution@vinodkothari.com

The Insolvency and Bankruptcy Board of India (IBBI), has, vide notification dated 18th September, 2023 introduced the IBBI (Insolvency Resolution Process for Corporate Persons) (Second Amendment) Regulations, 2023 (‘CIRP Amendment Regulations’/ ‘Amendment Regulations’) effective from 18th September, 2023, so as to further streamline the insolvency resolution process.

The amendments (discussed below) provide some relaxation to the stakeholders thereby extending the timeline for submitting claims. Further, an attempt has also been made to provide assistance to NCLT Benches for dealing with applications u/s 7 or 9 for admission/rejection of claim. However, the obligation of the Resolution professionals (RPs) have also been increased as the amendment now requires the RPs to not just take handover of the assets of the Corporate Debtor (CD) but also verify asset by asset list of the CD, tally the same with the financials of the CD, and to report the same while making application u/s 19(2), if not found in conformity with the assets shown in the financials of the CD. Also, for condonation of delay of claims filed by the stakeholders, the amendment now requires the RP to file application before AA.

Read more →

Comments on proposed changes to the Corporate Insolvency Resolution and Liquidation Framework under Insolvency and Bankruptcy Code, 2016

– Team Resolution (resolve@vinodkothari.com)

On 23rd December, 2021, the Ministry of Corporate Affairs has issued proposed changes to the Corporate Insolvency Resolution and Liquidation Framework under Insolvency and Bankruptcy Code, 2016[1] and has solicited comments on the same.

While we discuss the proposed amendments in details below, a bird’s eye view of the proposed amendments gives an indication towards a more creditor-friendly approach, wherein the creditors have been bestowed with extended powers such as right to initiate insolvency proceedings, as well as have become less burdened with the the proposed amendment of only producing IU records at the time of application. At the same time, the roles and responsibilities of the RPs/liquidators seem to have been further widened by making RPs and liquidators also responsible for investigation of avoidance proceedings.

Other ancillary amendments like commencement of look-back back period, timeliness in approval of resolutions plans follow the trend of making the resolution process free of loopholes as and when they are identified.

Below we discuss the proposed amendments in detail –

Resolution Plans – A Non returning visa to the resolution land

Anushka Vohra | Deputy Manager (corplaw@vinodkothari.com)

On September 13, 2021, in the matter of Ebix Singapore Private Limited v. Committee of Creditors of Educomp Solutions Limited[1], the Apex Court ruled that a Resolution Plan, once submitted with the Adjudicating Authority (“AA”) for approval, cannot be subsequently withdrawn at the behest of the Resolution Applicant. While this question of withdrawal of resolution plans has been around for quite some time, especially due to the COVID disruption, the Hon’ble Supreme Court has now given the final word of law.

An Insolvency Resolution Process sans Claims – A Defunct Process?

- Devika Agrawal, Executive (resolution@vinodkothari.com )

Introduction

Under the provisions of Insolvency and Bankruptcy Code, 2016 (IBC), the determining criteria for insolvency is a definite default, rather than financial sickness or ‘inability to pay’ . While the latter is certainly suggestive of a larger state of insolvency, where the company may be unable to pay its outstanding debts, the former does not necessitate the same. Hence, the likelihood of an application for initiation of CIRP on the basis of an isolated event of default/ non-payment, sans a financial stress in the company, cannot be ruled out.

Owing to such uncertainty, it may so happen that an application, initiated on the basis of such an isolated event of default, is admitted before the adjudicating authority without any other cases of defaults by the company. Naturally, there would be no claims to file except that of the applicant. If it were to happen, it forces one to ponder as to how CIRP will proceed, and if at all there is something to resolve.

CIRP without claims?

As per the Code, CIRP commences after an application has been admitted by the AA. Once an application is admitted by the AA, an Interim Resolution Professional is appointed, who is responsible for invitation and collation of claims, and subsequent constitution of the committee of creditors (‘CoC’). All decisions with respect to the corporate debtor’s business are thereafter taken with the approval of CoC, including approval of Resolution Plan or passing of a resolution for liquidation of the Corporate Debtor. Hence, it can be said that the CoC, constituted on the basis of the claims, drives the CD through the process till revival/ liquidation, as the case may be.

However, in a rather odd situation, when no claims are received after the initiation of CIRP, how will the IRP constitute CoC? In essence, when no claims are received by the Interim Resolution Professional (‘IRP’) after the initiation of CIRP, the questions that would arise are (aside, the broader question as to whether there was at all a need for resolution, will remain) – how is the CIRP likely to proceed, how will IRP constitute CoC, and most importantly, what is it for which the IRP should invite resolution plans? Does non-receipt of any claims by the creditors prove that the Corporate Debtor is, in fact, not a defaulter?

Books of the corporate debtor/public announcement

At the first instance, the books of the corporate debtor will assist in determining whether at all the CD has liabilities (financial/operational, otherwise). It may be the case that the CD does not have any liability at all (besides that pertaining to the creditor who filed the application). In such a case, attempts can be made by the CD and the Creditor to arrive at an agreement among themselves, instead of proceeding with CIRP and having the CD jammed in a situation of Moratorium.

However, there may be cases where the books acknowledge liabilities but there are no claimants. This might pose practical difficulties for the IRP because if no claims are received, the constitution of CoC would become impossible which in turn would lead to the CIRP coming to a complete halt. Occurrence of such a situation might necessitate the following actions to be taken by the IRP-

- sending of individual mails, requesting claims, to the Financial creditors so that, at least, a CoC can be constituted.

- ensure that the public announcement, inviting claims of creditors, are made in accordance with the manner laid down in the CIRP Regulations and in newspapers with wide reach.

- if, in case, no claims are received despite of efforts being made by the IRP, a final attempt should be made by the IRP by way of re-issuance of public announcement

Say, even after these efforts, no one shows up. There is a stage set, but there are no creditors to run the show. In such cases, what can the IRP do? We can explore the following alternatives.

Section 12A of Insolvency and Bankruptcy Code, 2016

Prior to section 12A of the Code, the withdrawal of an admitted insolvency resolution process was not expressly provided for. However, in view of reasons like a post-admission settlement or restructuring, the need to allow such withdrawal was realised – Section 12A of the Code enables withdrawal of the applications filed under Section 7, 9 or 10 of IBC, post its admission, if the committee of creditors (CoC) approves of such withdrawal by a voting share of at least ninety percent.

The very fact that section 12A mandates the approval of CoC as a precondition for withdrawal, there is no occasion to apply the said provisions before the constitution of CoC. A deeper reading of section 12A further indicates that the application for withdrawal must be filed by the very applicant who initiated the process. The reason is simple, the cause initiated by one cannot be withdrawn merely by virtue of a majority of others. Thus, the fact that withdrawal can be done only at the behest of the original applicant and with the consent of at least 90% CoC members maintains the much required trade off.

However, in the given state of affairs, the devil lies in the fact that no claims have been received so as to constitute the CoC. Further, to assume that the applicant who, at the first place, initiated the application, and thereafter chose to remain missing in action would initiate the withdrawal process, seems rather bizarre.

Even if one were to assume the possibility of withdrawal application by such a creditor, would the very filing be construed as a mere pressure tactic for recovery of claims? If yes, the same would attract penal provisions under the Code, and as such the Applicant would be liable for the consequences.

Knocking the Doors of NCLT

From the above discussion, we understand that a situation as such would indeed put the IRP/ RP in a pickle. Another probable way out could be an application being filed by the IRP/ RP under section 60 (5) of the Code thereby praying for annulling the process or directing the original applicant to file an application under section 12A.

Further, in Swiss Ribbons (P) Ltd. v. Union of India (Supra)[1], the Hon’ble Supreme Court made it clear that “at any stage where the committee of creditors is not yet constituted, a party can approach the NCLT directly, which Tribunal may, in exercise of its inherent powers under Rule 11 of the NCLT Rules, 2016, allow or disallow an application for withdrawal or settlement…….”

Thus, on the strength of the aforesaid order and the power and jurisdiction in section 60 (5), the IRP/ RP may take necessary steps before the Hon’ble Bench.

Such entanglement would leave the IPR/ RP in the middle of the sea, so to say that he can neither continue the CIRP in absence of the CoC, nor proceed for withdrawal as per section 12A.

Corporate Debtor – a Defaulter or no

Another line of thought that arises in the given facts could be whether the Corporate Debtor can be construed as a ‘defaulter’. In the given case, since no claims are received after the initiation of CIRP, can it be assumed that the Corporate Debtor has not defaulted in the payment of dues of any other creditor except for that of the applicant. Based on this assumption, can it be said that the CD is not a defaulter?

The above straight jacket assumption would not hold good as it is important to note that another probable situation that could arise is that the default of other creditors is apparent from the books of accounts of the Corporate Debtor. In such cases, if no claims are received by the IRP, the IRP may, in furtherance to the mandatory public announcement, send a mail to the banks/ financial creditors, inviting claims from them so that at least the CoC can be constituted and the CIRP can proceed.

While the above situation is a rather odd one, it would indeed be an interesting situation to understand the possible course of action that the IPs could resort to, and the role of the Adjudicating Authorities in such cases.

Revising minimum public holding requirements for large issuers and companies under CIRP

Securities Contract (Regulations) Amendment Rules, 2021 notified

Payal Agarwal, Executive ( corplaw@vinodkothari.com )

Background

SEBI had released a consultation paper on 20th November, 2020 order to review the requirements of minimum public offer for large issuers. The Consultation Paper proposed to reduce the requirements of minimum public offer for large issuers while also reducing the time period to meet the minimum public shareholding requirement (“MPS”). Further, SEBI had released another consultation paper on 19th August, 2020 for review of minimum public shareholding requirements for companies undergoing CIRP under IBC, wherein the Consultation Paper suggested three different modes of recalibrating the requirement for MPS upon approval of resolution plan.

Consequently, the Ministry of Finance has notified the Securities Contract (Regulations) Amendments Rules, 2021 (“the Amended Rules”) on 18th June, 2021 to amend Rule 19 and 19A of the Securities Contract (Regulations) Rules, 1957 (“the Rules”) giving effect to the above-mentioned proposals.

Reduction in minimum public shareholding requirement for large issuers

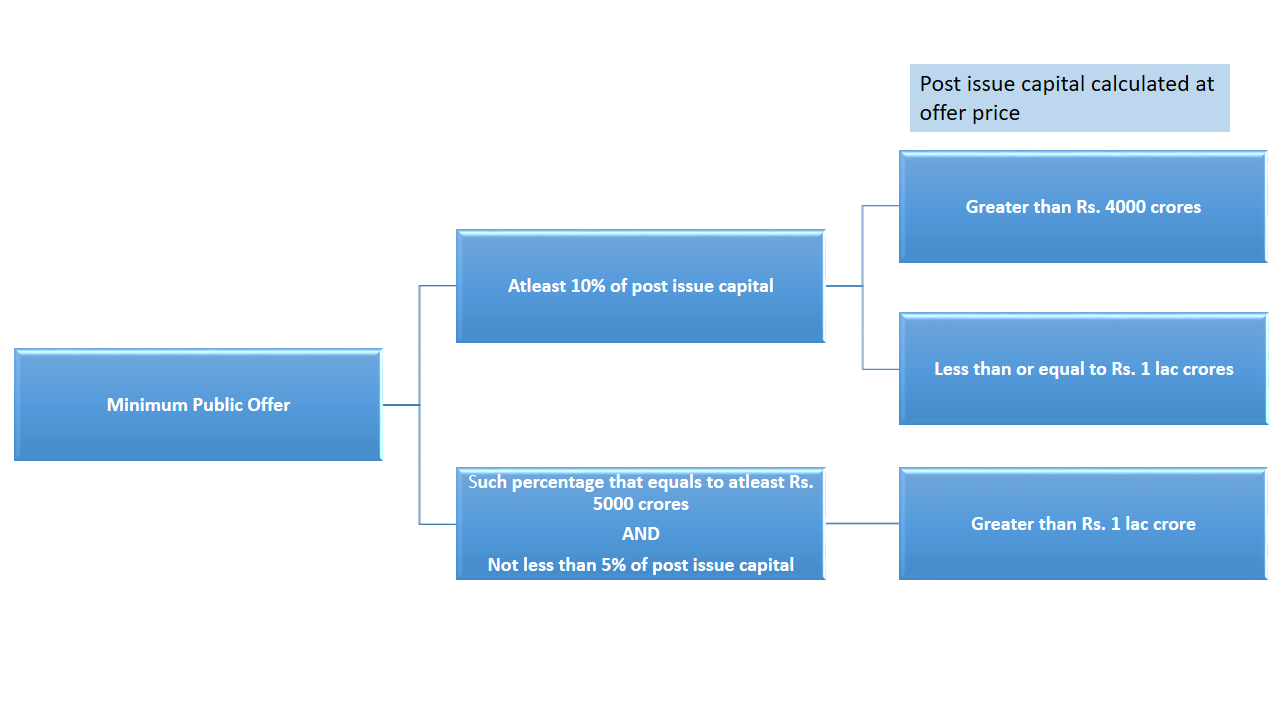

Who are large issuers?

Large issuers are issuers with post issue market capitalisation (‘MCap’) equal to or above Rs. 4000 crores. Currently all issuers with an MCap of Rs. 4000 crores are required to dilute 10% of an IPO to public shareholding. Large issuers have now been bifurcated into large issuers (MCap of Rs. 4000 crores and above) and very large issuers (MCap of Rs. 1 lakh crores).

New minimum public offer requirements for large issuers as per the Amended Rules

The post issue MCAP requirement for large and very large issuers has now been amended as below –

Accordingly, a flat rate of 10% has been set for large issuers while an incremental rate has been set for very large issuers with a post issue MCap of Rs. 1 lakh crores and above. For issuers below these thresholds, the existing requirements continue.

Accordingly, a flat rate of 10% has been set for large issuers while an incremental rate has been set for very large issuers with a post issue MCap of Rs. 1 lakh crores and above. For issuers below these thresholds, the existing requirements continue.

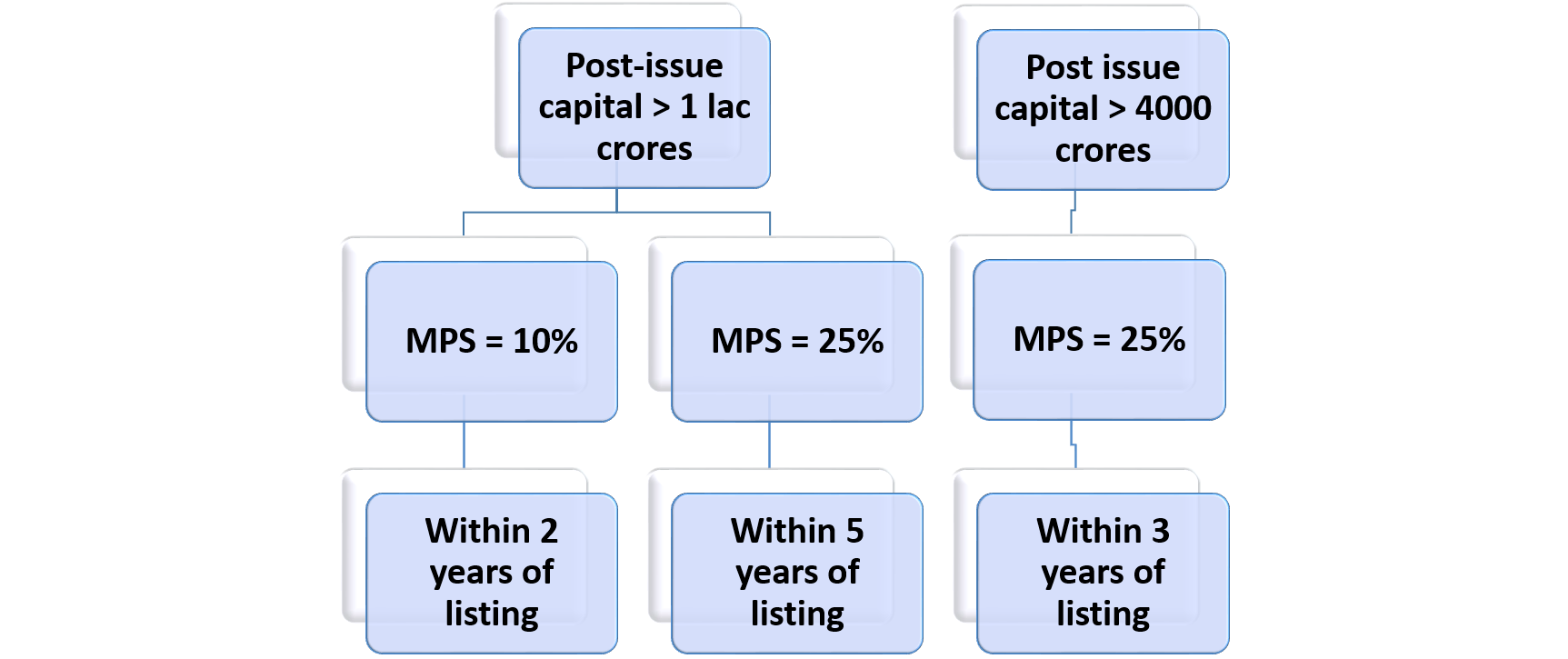

New MPS requirement

Currently, companies are required to meet the MPS within 3 years from the date of listing. However, in case of large issuers, the MPS is to be met as follows –

Rationale as proposed in the Consultation Paper

The reduction in the minimum public offer requirements for large issuers was proposed due to the following reasons –

- The compliance of such minimum public shareholding requirements is cumbersome for the large issuers.

- The large issuers already have investments from strategic investors who are classified as “public shareholders” post listing. Therefore, the requirement of minimum public offer results in unnecessary dilution of control of promoters thereby imposing constraints on issuers.

Minimum public shareholding requirement for companies under Resolution Plan

Further, amendments have been made in Rule 19A of the Rules, with respect to the minimum public shareholding requirements for a company under CIRP under Insolvency and Bankruptcy Code, 2016 (‘IBC’).The Amended Rules provide a strict-er timeline for post-CIRP companies to comply with the MPS requirements upon implementation of resolution plans

Change in the requirements as per the Amended Rules are as follows –

| Particulars | Requirement before amendment | Requirement as per Amended Rules |

| Public shareholding falls below 25% | Bring to 25% within 3 years of such fall | No change |

| Public shareholding falls below 10% | Bring to 10% within maximum 18 months of such fall | Bring to 10% within maximum 12 months from such fall |

| Minimum public shareholding to be maintained | No such requirement | Shall not fall below 5% |

Rationale as proposed in the Consultation Paper

The relaxations with respect to the strict enforcement of Rule 19 of the Rules have been given in order to ensure revival of a Corporate Debtor pursuant to a resolution plan. However, while the same seems to be in favour of Corporate Debtors, specifying no MPS requirement may result in cases where the public shareholding will become extremely low, leading to less float, thereby hampering the market integrity and price discovery in secondary market.

The Consultation Paper suggested three different alternatives out of which the second one has been preferred since the MPS of 5% being a lower threshold will incentivise the companies to stay listed post-CIRP whereas higher thresholds may cause total delisting

The said requirement shall have significant ramifications for resolution applicants who otherwise are more focused on operational aspects over regulatory requirements. While resolution plans relaxes several requirements like an open offer under SAST regulations, it is significant to note that requirements w.r.t. MPS were never completely waived off. The present step of giving more stringent timelines is introduced with the objective of protecting the investors’ interest and shielding them from the possible loss of value due to delayed MPS adherence. The loss of value can be on account of delisting of such corporate debtors under CIRP, whereas the shareholders may recover potential value from the shares of such corporate debtor if it continues to remain listed post implementation of resolution plan.