Multi-lender LSPs – Compliance & Considerations

– Aditya Iyer, Manager (Legal) (finserv@vinodkothari.com)

- The illusion of choice – a consumer’s woe

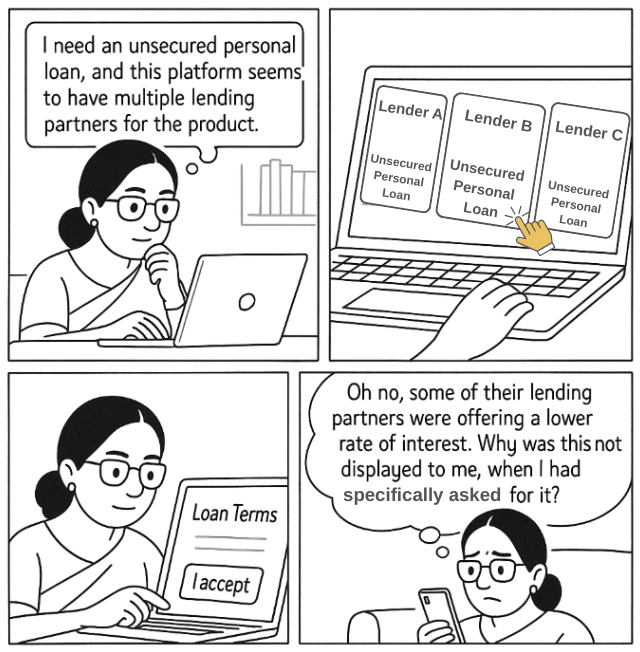

Consider this: you’re out shopping on a Saturday afternoon for a perfect pair of jeans. You stop by a store that retails multiple brands and boasts the best variety. With a salesperson to guide you, you make your pick after careful diligence and comparison, and finally check out. Hours later, however, you discover that certain brands were selling better trousers at a lower price point, in the very same store, but these were deliberately obscured from your vision. Now, you feel duped, hurt and confused.

It’s still the same product. However, what has changed is your ability to make an informed choice. What’s worse, indeed, is that you were made to believe that you had an informed choice.

A sincere consumer, shopping for trousers from a multi-brand store.

- Multi-lender LSPs (MLLs)

Drawing parallels from the above, in the lending space, a similar tale unfolds. There is an emerging class of platforms that operate as Multi-lender LSPs (MLLs). These MLLs undertake the sourcing function for multiple lenders against a given product. For instance, Partner ‘A’ may act as a sourcing agent via its platform for unsecured personal loans offered by Lenders X, Y, and Z.

In this case, the consumer may be onboarded onto the platform and be under the impression that they are making an informed choice, and receiving an impartial display of all options for the given loan product. If this is indeed the case, then there is no issue. However, it is possible that due to factors including (a) certain Lender-LSP Arrangements, and (b) differences in the commission received from various lenders, the loan product of a particular lender may be pushed to the borrower. The borrower may also be influenced towards making a particular selection through the use of deceptive design practices designed to subvert their decision-making process (Dark Patterns – for more, see our resource here).

Here, the lack of choice and transparency, and insufficient disclosure in the sourcing process would be an unfair lending practice. And unlike a simple pair of trousers, here the consumer’s hard-earned money and personal finances are at stake.

A similar tale unfolds on a multi-lender platform.

- Requirements for REs under the Digital Lending Directions, 2025

- Para 6 of the DL Directions

In order to protect the borrower and their right to choose, the RBI vide the Digital Lending Directions, 2025 (‘DL Directions’) has prescribed additional requirements upon REs contracting with such MLLs (refer to our article on the DL Directions here).

These requirements under Para 6 of the DL Directions are applicable upon “RE-LSP arrangements involving multiple lenders”, and pertain to:

- The borrower being provided a digital view of all the loan offers which meet the borrower’s requirements.

- A view of the unmatched lenders as well.

- The digital view would have to include the KFS, APR, and penal charges if any of all the lenders, to display terms in a comparable manner.

- The content displayed should be unbiased and objective, free from the influence of any dark patterns or deceptive design practices designed to favour a given product.

The RBI’s annual report for FY 2024-2025 also reveals that the rationale behind these additions was to mitigate risks arising out of LSPs that display the loan offers in a discretionary way, and “which seldom display all available loan offers to the borrower for making an informed choice”. These requirements were, of course, first published via the Draft Guidelines on ‘Digital Lending – Transparency in Aggregation of Loan Products for Multiple Lenders’ (our team’s views on the same may be found here).

- Multi-lender LSP v. LSP working for multiple lenders – Is there a difference?

Although this may not be immediately apparent from the language, the “RE-LSP arrangements involving multiple lenders” being contemplated here (in our view) are not RE-LSP arrangements where a single LSP is contracting with multiple REs, each for a separate product, but rather the MLLs described above.

For example, consider a scenario where the LSP works with Lender ‘A’ for vehicle loans, Lender ‘B’ for personal loans, Lender ‘C’ for gold loans and so on. Would this then be considered a Multi-lender LSP requiring compliance under Para 6 of the DL Directions? In our view, no.

Here, because each borrower has only a single lender for a particular product, there is no question of their ability to choose being prejudiced, or there being a need to draw a comparison between the terms offered by multiple lenders. Hence, the requirements under Para 6 of the DL Directions would not be applicable upon REs contracting with such LSPs.

Such requirements would only become relevant in the case where the LSP is undertaking sourcing for multiple lenders against a particular product. In such a case, because the borrower is under the impression that they have a choice, it becomes crucial to protect the borrower’s ability to make that choice (in an informed, transparent, and non-discriminatory manner).

- Consumer Protection Act, 2019

Additionally, with reference to the above scenario, under Section 2(9) of the Consumer Protection Act, the following (amongst others) have been recognised as consumer rights (upon violation of which the consumer can seek redressal):

- Right to be informed: “the right to be informed about the quality, quantity, potency, purity, standard and price of goods, products or services, as the case may be, so as to protect the consumer against unfair trade practices”

- Access to competitive prices: “the right to be assured, wherever possible, access to a variety of goods, products or services at competitive prices”.

In our view, with respect to MLLs, this may be interpreted to mean that the borrower has a right to be informed of the comparable options and to receive an impartial, unbiased, and competitive display of the terms to enable their decision-making.

Finally, it is to be noted that such MLLs, would also qualify as “E-Commerce Entities” under the Consumer Protection (E-Commerce) Rules, and the said rules inter alia cast a duty upon such entities to ensure that they do not adopt any unfair trade practice, whether in course of business on its platform, or otherwise [Rule (4)(2)]. Under the E-commerce Rules, a “marketplace e-commerce entity” is an e-commerce entity providing an information technology platform to facilitate transactions between buyers and sellers. Marketplace e-commerce entities are required to ensure that:

- All the details about the sellers necessary to help the buyer make an informed decision at the pre-purchase stage are “displayed prominently in an appropriate place on its platform”

To the extent MLLs would meet this definition, they would also need to ensure the same.