Indian Valuation Standards: Standardizing the rules of valuation in India

Refer to valuation approaches here- https://vinodkothari.com/2020/09/valuation-approaches-and-methods/

GST on assignment of receivables: Wrong path to the right destination

Team Vinod Kothari Consultants P. Ltd

There has been a lot of uncertainty on the issue of exigibility of direct assignments and securitisation transactions to goods and services tax (GST). While on one hand, there have been opinions that assignments of secured debts may be taxable being covered by the circuitous definition of “actionable claims”, there are other views holding such assignments of debts (secured or unsecured) to be non-taxable since an obligation to pay money is nothing but money, and hence, not “goods” under the GST law[1]. The uncertainty was costing the market heavily[2].

In order to put diverging views to rest, the GST Council came out with a set of Frequently Asked Questions on Financial Services Sector[3], trying to clarify the position of some arguable issues pertaining to transactions undertaken in the financial sector. These FAQs include three separate (and interestingly, mutually unclear) questions on – (a) assignment or sale of secured or secured debts [Q.40], (b) whether assignment of secured debts constitutes a transaction in money [Q.41], and (c) securitisation transactions undertaken by banks [Q.65].

The end-result arising out of these questions is that there will be no GST on securitisation transactions. However, the GST Council has relied on some very intriguing arguments to come to this conclusion – seemingly lost between the meaning of “derivatives”, “securities”, and “actionable claims”. If one does not care about why we reached here, the conclusion is most welcome. However, the FAQs also reflect the serious lack of understanding of financial instruments with the Council, which may potentially create issues in the long run.

In this note[4] we intend to discuss the outcome of the FAQs, but before that let us first understand what the situation of the issue was before this clarification.

Situation before the clarification

- GST is chargeable on supply of goods or services or both. Goods have been defined in section 2(52) of the CGST Act in the following manner:

“(52) “goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply;”

Services have been defined in section 2(102) of the CGST Act oin in the following manner:

““services” means anything other than goods, money and securities but includes activities relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged;”

Money, is therefore, excludible from the scope of “goods” as well as “services”.

Section 7 details the scope of the expression “supply”. According to the section, “supply” includes “all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business.” However, activities as specified in Schedule III of the said Act shall not be considered as “supply”.

It may be noted here that “Actionable claims, other than lottery, betting and gambling” are enlisted in entry 6 of Schedule III of the said Act; therefore are not exigible to GST.

- There is no doubt that a “receivable” is a movable property. “Receivable” denotes something which one is entitled to receive. Receivable is therefore, a mirror image for “debt”. If a sum of money is receivable for A, the same sum of money must be a debt for B. A debt is an obligation to pay, a receivable is the corresponding right to receive.

Coming to the definition of “money”, it has been defined under section 2(75) as follows –

““money” means the Indian legal tender or any foreign currency, cheque, promissory note, bill of exchange, letter of credit, draft, pay order, traveller cheque, money order, postal or electronic remittance or any other instrument recognised by the Reserve Bank of India when used as a consideration to settle an obligation or exchange with Indian legal tender of another denomination but shall not include any currency that is held for its numismatic value.”

The definition above enlists all such instruments which have a “value-in-exchange”, so as to represent money. A debt also represents a sum of money and the form in which it can be paid can be any of these forms as enlisted above.

So, in effect, a receivable is also a sum of “money”. As such, receivables shall not be considered as “goods” or “services” for the purpose of GST law.

- As mentioned earlier, “actionable claims” have been included in the definition of “goods” under the CGST Act, however, any transfer (i.e. supply) of actionable claim is explicitly excluded from being treated as a supply of either goods or services for the purpose of levy of GST.

Section 2(1) of the CGST Act defines “actionable claim” so as to assign it the same meaning as in section 3 of the Transfer of Property Act, 1882, which in turn, defines “actionable claim” as –

“actionable claim” means a claim to any debt, other than a debt secured by mortgage of immovable property or by hypothecation or pledge of movable property, or to any beneficial interest in movable property not in the possession, either actual or constructive, of the claimant, which the civil courts recognise as affording grounds for relief, whether such debt or beneficial interest be existent, accruing, conditional or contingent;”

It may be noted that the inclusion of “actionable claim” is still subject to the exclusion of “money” from the definition of “goods”. The definition of actionable claim travels beyond “claim to a debt” and covers “claim to any beneficial interest in movable property”. Therefore, an actionable claim is definitely more than a “receivable”. Hence, if the actionable claim represents property that is money, it can be held that such form of the actionable claim shall be excluded from the ambit of “goods”.

There were views in the industry which, on the basis of the definition above, distinguish between — (a) a debt secured by mortgage of immovable property, and a debt secured by hypothecation/pledge of movable property on one hand (which are excluded from the definition of actionable claim); and (b) an unsecured debt on the other hand. However, others opined that a debt, whether secured or unsecured, is after all a “debt”, i.e. a property in money; and thus can never be classified as “goods”. Therefore, the entire exercise of making a distinction between secured and unsecured debt may not be relevant at all.

In case it is argued that a receivable which is secured (i.e. a secured debt) shall come within the definition of “goods”, it must be noted that a security granted against a debt is merely a back-up, a collateral against default in repayment of debt.

- In one of the background materials on GST published by the Institute of Chartered Accountants of India[5], it has been emphasised that a transaction where a person merely slips into the shoes of another person, the same cannot be termed as supply. As such, unrestricted expansion of the expression “supply” should not be encouraged:

“. . . supply is not a boundless word of uncertain meaning. The inclusive part of the opening words in this clause may be understood to include everything that supply is generally understood to be PLUS the ones that are enlisted. It must be admitted that the general understanding of the world supply is but an amalgam of these 8 forms of supply. Any attempt at expanding this list of 8 forms of supply must be attempted with great caution. Attempting to find other forms of supply has not yielded results however, transactions that do not want to supply have been discovered. Transactions of assignment where one person steps into the shoes of another appears to slip away from the scope of supply as well as transactions where goods are destroyed without a transfer of any kind taking place.”

Also, as already stated, where the object is neither goods nor services, there is no question of being a supply thereof.

- Therefore, there was one school of thought which treated as assignment of secured receivables as a supply under the GST regime and another school of thought promoted a view which was contrary to the other one. To clarify the position, representations were made by some of the leading bankers and the Indian Securitisation Foundation.

Situation after the clarification

- The GST Council has discussed the issue of assignment and securitisation of receivables through different question, extracts have been reproduced below:

- Whether assignment or sale of secured or unsecured debts is liable to GST?

Section 2(52) of the CGST Act, 2017 defines ‘goods’ to mean every kind of movable property other than money and securities but includes actionable claim. Schedule III of the CGST Act, 2017 lists activities or transactions which shall be treated neither as a supply of goods nor a supply of services and actionable claims other than lottery, betting and gambling are included in the said Schedule. Thus, only actionable claims in respect of lottery, betting and gambling would be taxable under GST. Further, where sale, transfer or assignment of debts falls within the purview of actionable claims, the same would not be subject to GST.

Further, any charges collected in the course of transfer or assignment of a debt would be chargeable to GST, being in the nature of consideration for supply of services.

- Would sale, purchase, acquisition or assignment of a secured debt constitute a transaction in money?

Sale, purchase, acquisition or assignment of a secured debt does not constitute a transaction in money; it is in the nature of a derivative and hence a security.

- What is the leviability of GST on securitization transactions undertaken by banks?

Securitized assets are in the nature of securities and hence not liable to GST. However, if some service charges or service fees or documentation fees or broking charges or such like fees or charges are charged, the same would be a consideration for provision of services related to securitization and chargeable to GST.

- The fallacy starts with two sequential and separate questions: one dealing with securitisation and the other on assignment transactions. There was absolutely no need for incorporating separate questions for the two, since all securitisation transactions involve an assignment of debt.

- Next, the department in Question 40 has clarified that the assignment of actionable claims, other than lottery, betting and gambling forms a part of the list of exclusion under Schedule III of the CGST Act, therefore, are not subject to GST. This was apparent from the reading of law, therefore, there is nothing new in this.

However, the second part of the answer needs further discussion. The second part of the answer states that – any charges collected in the course of transfer or assignment of a debt would be chargeable to GST, being in the nature of consideration for supply of services.

There are multiple charges or fees associated in an assignment or securitisation transaction – such as servicing fees or excess spread. While it is very clear that the GST will be chargeable on servicing fees charged by the servicer, there is still a confusion on whether GST will be charged on the excess spread or not. Typically, transactions are devised to give residuary sweep to the originator after servicing the PTCs. Therefore, there could be a challenge that sweep right is also a component of servicing fees or consideration for acting as a servicing agent. The meaning of consideration[6] under the CGST Act is consideration in any form and the nomenclature supports the intent of the transaction.

Since, the originator gets the excess spread, question may arise, if excess spread is in the nature of interest. This indicates the need for proper structuring of transactions, to ensure that either the sweep right is structured as a security, or the same is structured as a right to interest. One commonly followed international structure is credit-enhancing IO strip. The IO strip has not been tried in Indian transactions, and recommendably this structure may alleviate concerns about GST being applied on the excess spread.

- Till now, whatever has been discussed was more or less settled before the clarification, question 41 settles the dispute on the contentious question of whether GST will be charged on assigned of secured debt. The answer to question 41 has compared sale, purchase, acquisition or assignment of secured debt with a derivative. The answer has rejected the view, held by the authors, that any right to a payment in money is money itself. The GST Council holds the view that the receivables are in the nature of derivatives, the transaction qualifies to be a security and therefore, exempt from the purview of supply of goods or supply of services.

While the intent of the GST Council is coming out very clear, but this view is lacking supporting logic. Neither the question discusses why assignments of secured receivables are not transactions in money, nor does it state why it is being treated as derivative.

Our humble submission in this regard is that assignment of secured receivables may not be treated as derivatives. The meaning of the term “derivatives” have been drawn from section 2(ac) of the Securities Contracts (Regulation) Act, 1956, which includes the following –

(A) a security derived from a debt instrument, share, loan, whether secured or unsecured, risk instrument or contract for differences or any other form of security;

(B) a contract which derives its value from the prices, or index of prices, of underlying securities.

In the present case, assignment of receivables do not represent any security nor does it derive its value from anything else. The receivables themselves have an inherent value, which get assigned, the fact that it is backed a collateral security does not make any difference as the value of the receivables also factor the value of the underlying.

Even though the logic is not coming out clear, the intent of the Council is coming out clearly and the efforts made by the Council to clear out the ambiguities is really commendable.

[1] Refer: GST on Securitisation Transactions, by Nidhi Bothra, and Sikha Bansal, at https://vinodkothari.com/blog/gst-on-securitisation-transactions-2/; pg. last visited on 06.06.2018

[2] At the recently concluded Seventh Securitisation Summit on 25th May, 2018, one leading originator confirmed that his company had kept transactions on hold in view of the GST uncertainty. It was widely believed that the dip in volumes in FY 2017-18 was primarily due to GST uncertainty.

[3] http://www.cbic.gov.in/resources//htdocs-cbec/gst/FAQs_on_Financial_Services_Sector.pdf

[4] Portions of this note have been adopted from the article – GST on Securitisation Transactions, by Nidhi Bothra and Sikha Bansal.

[5] http://idtc-icai.s3.amazonaws.com/download/pdf18/Volume-I(BGM-idtc).pdf; pg. last visited on 19.05.2018

[6] (31) “consideration” in relation to the supply of goods or services or both includes––

(a) any payment made or to be made, whether in money or otherwise, in respect of, in response to, or for the inducement of, the supply of goods or services or both, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government;

(b) the monetary value of any act or forbearance, in respect of, in response to, or for the inducement of, the supply of goods or services or both, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government:

Provided that a deposit given in respect of the supply of goods or services or both shall not be considered as payment made for such supply unless the supplier applies such deposit as consideration for the said supply;

Fair Market Value – as per Company Law perspective

By Nikita Snehil | nikita@vinodkothari.com

The term ‘Fair market value’ has been used hundreds of times in the Income Tax Act, 1961, however, the same has also been given due weightage under the Companies Act, 2013. The present Article intends to explain the meaning of the term ‘Fair Market Value’, its significance and its relevance as per Companies Act, 2013.

Meaning of Fair Market Value

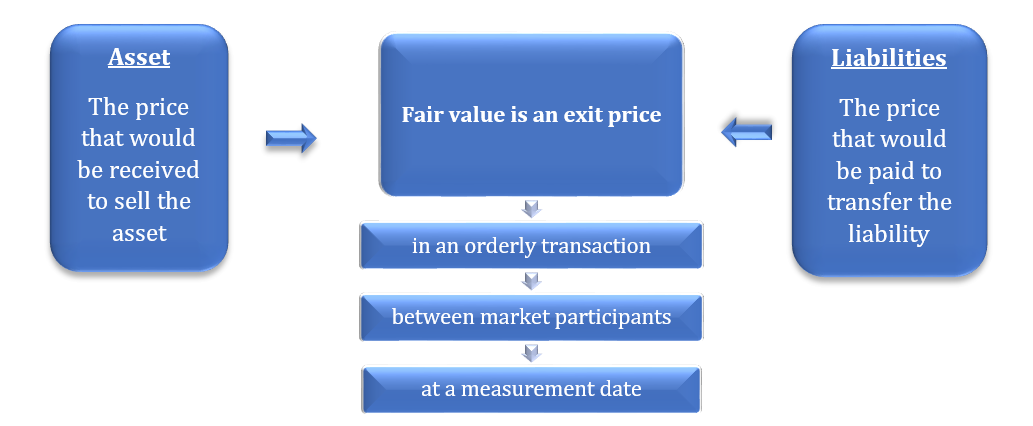

In general parlance, Fair market value is the price agreed between a buyer and a seller for a specific asset. Both parties should be aware of the asset’s condition and willing to participate in the transaction with no force or conditions.

However, the term has been defined in para 9 the Ind AS 113[1], which states the following:

“Ind AS defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

Therefore, the definition can be illustrated in the following way:

The concept of Fair Market Value has become all pervasive particularly after the introduction of International Financial Reporting Standards because there is greater stress on fair value today than in the past.

Provisions of the Companies Act, 2013 referring to fair valuation

The provisions of the Companies Act, 2013 (‘Act’) talks about the requirement of valuation in many cases, the following table shows the sections of the Act requiring valuations:

| Section no. | Valuation purpose |

Requirements in brief

|

| 54 | Issuance of Sweat Equity Shares | The sweat equity shares to be issued shall be valued at a price determined by a registered valuer as the fair price giving justification for such valuation.

|

| 62(1) (c) | Preferential Offer | When a company proposes to issue new shares, the price of such shares should be determined by the valuation report of a Registered Valuer.

|

| 192(2) | Non-cash transaction involving directors | Where there is a sale or purchase of any asset involving a company and its directors (or its

holding, subsidiary or associate company) or a person connected with the director for consideration other than cash, the value of the assets has to be calculated by a Registered Valuer.

|

| 230 & 232 | Compromises, Arrangements and Amalgamations | In case of compromise or arrangement between members or with creditors or any class of them, a valuation report in respect of shares, property or assets, tangible and intangible, movable and immovable of the company is required by a Registered Valuer.

|

| 236 | Purchase of minority share holding | Where an acquirer or person acting in concert with the acquirer acquires 90% or more of the equity capital in a company, then they can offer to the minority shareholder or the minority shareholder can offer to the acquirer, to acquire the minority shareholding at a valuation determined by the Registered Valuer.

|

| 281 & 305 | Winding up of a company | In case of winding up, the valuation of assets of the company prepared by the Registered Valuer is required.

|

Who can be valuer?

Though the Act does not specify anything regarding the eligibility of the registered valuers, the Companies (Share Capital and Debenture) Rules, 2014 provides the following:

For the purposes of these rules, it is hereby clarified that, till a registered valuer is appointed in accordance with the provisions of the Act, the valuation report shall be made by an independent merchant banker who is registered with the Securities and Exchange Board of India or an independent Chartered Accountant in practice having a minimum experience of ten years.

Thereafter, MCA had notified the provisions governing valuation by registered valuers [section 247 of the Act and the Companies (Registered Valuers and Valuation) Rules, 2017 (‘Rules’), both to come into effect from 18 October, 2017.

Valuation by Registered Valuers

As per the notified section 247(1), where a valuation is required to be made in respect of any property, stocks, shares, debentures, securities or goodwill or any other assets or net worth of a company or its liabilities under the provision of this Act, it shall be valued by a person having such qualifications and experience and registered as a valuer in such manner, on such terms and conditions as may be prescribed and appointed by the audit committee or in its absence by the Board of Directors of that company.

Proposal of MCA to have registered valuers

The definition of ‘Valuer’ in the said Rules, provides the following:

“valuer” means a person registered with the authority in accordance with these rules and the term “registered valuer” shall be construed accordingly.

Therefore, the valuer will have to obtain the Certificate of Registration after complying the qualification and eligibility criteria as specified in the Rules, in order to do the valuation.

Eligibility of Registered Valuers

As per Rule 3 of the said Rules, the following person shall be eligible to be a registered valuer if he-

- Is a valuer member of a registered valuers organisation;

Explanation.- For the purposes of this clause, “a valuer member” is a member of a registered valuers organisation who possesses the requisite educational qualifications and experience for being registered as a valuer;

- Is recommended by the registered valuers organisation of which he is a valuer member for registration as a valuer;

- Has passed the valuation examination under rule 5 within three years preceding the date of making an application for registration under rule 6

- Possesses the qualifications and experience as specified in rule 4;

- Is not a minor;

- Has not been declared to be of unsound mind;

- Is not an undischarged bankrupt, or has not applied to be adjudicated as a bankrupt;

- Is a person resident in India; .

Explanation.- For the purposes of these rules ‘person resident in India’ shall have the same meaning as defined in clause (v) of section 2 of the Foreign Exchange Management Act, 1999 (42 of 1999) as far as it is applicable to an individual;

- Has not been convicted by any competent court for an offence punishable with imprisonment for a term exceeding six months or for an offence involving moral turpitude, and a period of five years has not elapsed from the date of expiry of the sentence:

Provided that if a person has been convicted of any offence and sentenced in respect thereof to imprisonment for a period of seven years or more, he shall not be eligible to be registered;

- Has not been levied a penalty under section 271J of Income-tax Act, 1961 (43 of 1961) and time limit for filing appeal before Commissioner of Income-tax (Appeals) or Income-tax Appellate Tribunal, as the case may be has expired, or such penalty has been confirmed by Income-tax Appellate Tribunal, and five years have not elapsed after levy of such penalty; and

- Is a fit and proper person:

Further, with respect to a partnership entity or company, the following shall not be eligible to be a registered valuer if-

- It has been set up for objects other than for rendering professional or financial services, including valuation services and that in the case of a company, it is not a subsidiary, joint venture or associate of another company or body corporate;

- It is undergoing an insolvency resolution or is an undischarged bankrupt;

- All the partners or directors, as the case may be, are not ineligible under clauses (c), (d), (e), (g), (h), (i), (j) and (k) as mentioned above;

- Three or all the partners or directors, whichever is lower, of the partnership entity or company, as the case may be, are not registered valuers; or

- None of its partners or directors, as the case may be, is a registered valuer for the asset class, for the valuation of which it seeks to be a registered valuer.

Applicability of the Rules

As per the transitional provisions specified in the Rules read with the MCA’s Notification[1] on extending the transitional period:

“Any person who may be rendering valuation services under the Act, on the date of commencement of these rules, may continue to render valuation services without a certificate of registration under these rules upto 30th September, 2018:

Provided that if a company has appointed any valuer before such date and the valuation or any part of it has not been completed before 30th September, 2018, the valuer shall complete such valuation or such part within three months thereafter.”

Therefore, the persons intending to act as the registered valuers must obtain the Certificate of Registration within September 30, 2018, as per the requirements of the Rules.

Issuance of Valuation Standards by ICAI

Recognising the need to have the consistent, uniform and transparent valuation policies and harmonise the diverse practices in use in India, the Council of the Institute of Chartered Accountants of India at its 375th meeting has issued the Valuation Standards vide the Press Release[2] dated May 25, 2018, mandating the compliance with the Standards for the Chartered Accountants providing valuation reports under various provisions of the Companies Act.

The Standards include the framework for the preparation of valuation report, valuation bases, approaches and methods, scope of work, analyses and evaluations, documentation and reporting, intangible assets and financial instruments, among several other aspects.

Therefore, recognizing the importance of valuation, the Rules introduced by MCA and the standards introduced by ICAI will provide a benchmark to the professionals to ensure uniformity in approach and quality of valuation output.

[1] http://mca.gov.in/Ministry/pdf/INDAS113.pdf

[2] http://www.mca.gov.in/Ministry/pdf/CompaniesRules2018_12022018.pdf

[3] https://www.icai.org/new_post.html?post_id=14799&c_id=238

Borrowing Cost from Company Law’s perspective

By Abhirup Ghosh, abhirup@vinodkothari.com

& Nikita Snehil, nikita@vinodkothari.com

Proper flow of funds within an organisation can be termed as the lifeline of the organization. In the course of the operation, each and every organization stands in need of money over and above their capital. Therefore, in order to meet the financial needs, they are bound to depend on external sources for funding. The source of funds would typically depend on the purpose and duration for which the fund is required.

Say for instance, if the Company requires funds for making a capital expenditure it would go for long term finance like term loans or external commercial borrowings. However, if the company requires funding to meet its working capital needs, it would go for short term financing sources like working capital loans or overdraft facility from banks.

Apart from the tenure or purpose of fund raising there is one more factor which also affects the choice of funding source and that is the borrowing cost. Eventually, over the years, this factor has become the most important of all.

Companies try various kind of fund raising techniques to achieve the lowest borrowing cost and in this regard it is very important to take note of the regulatory aspects of raising funds. In this article we intend we will discuss the various legal and regulatory issues relating to the issuance of the securities or fund raising and borrowing costs.

Meaning of borrowing cost

Before we delve into further details, let us first understand what constitutes to be borrowing cost. In general, Borrowing Cost means the interest and other costs incurred by an organization in relation to the borrowing of funds. However, the same has also been defined in Accounting Standard 16 in the following manner:

‘3.1 Borrowing costs are interest and other costs incurred by an enterprise in connection with the borrowing of funds.’

xxx

4. Borrowing costs may include:

(a) interest and commitment charges on bank borrowings and other short-term and long-term borrowings;

(b) amortisation of discounts or premiums relating to borrowings;

(c) amortisation of ancillary costs incurred in connection with the arrangement of borrowings;

(d) finance charges in respect of assets acquired under finance leases or under other similar arrangements; and

(e) exchange differences arising from foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs’.

To sum up, Borrowing Costs are the expenses incurred by the organization in borrowing the funds.

Modes of Borrowings

Next, with respect to modes of borrowing, the modes of funding can be distinguished majorly between long term borrowing and short term borrowing.

A. Modes of Short Term Borrowings and the cost involved in raising the same:

1. Temporary loans like loans repayable on demand, cash credit facilities and overdraft arrangements

A loan is repayable on demand when:

(a) there is no time for repayment specified (and hence, the obligation to repay on demand is implied by law); or

(b) the parties actually express the obligation to repay on demand or request (i.e., the same is an express term).

Therefore, a loan with no repayment terms, or loan agreement with no repayment date, is a loan repayable on demand. The borrowing company is required to pay the loan along with the interest amount determined by the lender. Example of a demand loan can be the overdraft facilities provided by the Banks.

An overdraft is an arrangement by which a company is allowed to draw more than what is to the credit of its account at the bank. The charges for overdraft facility has to be paid by the company to the Bank, when such facility is utilised.

Cash credit is an arrangement by which a company borrows from its bankers up to a certain limit against a bond of credit by one or more securities or some other security. The company is charged interest on the amount actually utilized and not on the limit sanctioned.

2. Commercial Papers (CPs)

Commercial Papers are unsecured money market instrument which can be issued either in the form of a promissory note or in a dematerialised form through any of the depositories approved by and registered with SEBI. Further, commercial papers are instruments issued by the company, so as to fulfil the short-term fund requirement and have easy liquidity in the market with less compliance burden.

However, before issuing commercial paper, the eligible issuers must obtain the credit rating for the issuance of commercial paper from any one of the SEBI registered Credit Rating Agencies.

Raising finance through issuance of these would not qualify to be deposits for the purpose of Companies Act as the term deposits exclude any money received by issuing money market instruments.

3. Working capital loans

A working capital loan is a loan that has the purpose of financing the everyday operations of a company. Working capital loans are not used to buy long-term assets or investments and are instead used to finance the day to day expenses such as to buy inventory, cover payroll, wages, etc. The lender charges interest for lending the working capital loans.

4. Issuance of NCDs with less than one year maturity

Companies having a tangible net worth as per the latest audited balance sheet, of not less than Rs.4 crore can issue Non-Convertible Debentures (NCDs) of maturity less than one year. The eligible corporate intending to issue NCDs is required to obtain credit rating for issuance of the NCDs from one of the rating agencies specified by RBI and the companies are even required to ensure at the time of issuance of NCDs that the rating so obtained is current and has not fallen due for review. Therefore, raising such funds shall require fulfilment of eligibility criteria and expenses for credit rating.

Like commercial papers, these are also money market instruments. Therefore, raising of finance through issuance of NCDs would not be treated as money market instrument for the purpose of Companies Act.

5. Letter of Credit

A Letter of Credit (L/C) is a letter from a bank guaranteeing that a buyer’s payment to a seller will be received on time and for the correct amount. Here the banks act as disinterested third parties and they release funds only after certain conditions are met. Banks issue letters of credit when a company applies for the same and has the assets or credit to get approved.

6. Trade Credit

A trade credit is an agreement or understanding between agents engaged in business with each other, it allows the exchange of goods and services without any immediate exchange of money. When the seller of goods or service allows the buyer to pay for the goods or service at a later date, the seller is said to extend credit to the buyer. This is a type of instrument where no cost is involved. Sometime, the payment terms may also offer discount as an incentive for early payment.

B. Modes of Long Term Borrowings and the cost involved in raising the same:

1. Loan from Bankers

Long-term loans are a type of business financing in which the maturity date of the loan extends past a year and can even last for as long as 20 years (e.g. commercial property loans). This is used mainly to finance long-term projects such as business expansion, franchising, purchase of property, plant, and equipment and other fixed assets. Companies may also avail loan from Bankers on the basis of their credibility. The company has to pay interest on the full amount of the loan sanctioned by the bank, irrespective of the amount utilised by the company. The longer the tenure extends, the more amount of interest money has to be paid in total.

2. Issuance of Debentures

A debenture is a securitised loan and is backed by a certificate. It is the most important method of obtaining loan for a longer period by the companies. On the basis of coupon, the debentures can be classified into two categories – coupon bearing [These debentures are issued at face value and the specified rate of interest is earned by the holders of these securities] and zero coupon [These debentures are issued at a discounted price and redeemed at par; and these do not carry any coupon rate.]. Generally, the following types of debentures are issued by the companies:

(a) Compulsorily Convertible debentures (CCDs): These debentures are mandatorily converted into equity shares of the company, as per the terms specified at the time of issue or on the expiry of specified period.

(b) Non-convertible Debentures (NCDs): These debentures do not carry the option of conversion into equity shares and are therefore, redeemed on the expiry of certain specified period. Most commonly, entities issued NCDs for meeting their long term capex requirements.

NCDs issued to corporates or listed or fully secured do not qualify to be deposits for the purpose of Companies Act.

(c) Optionally convertible debentures (OCDs): The investor has an option to convert into shares at the pre-determined price and time.

3. Inter-Corporate Deposits

An Inter-Corporate Deposit (ICD) is an unsecured borrowing by corporates from other corporate entities registered under the Companies Act, 2013 (or the erstwhile Companies Act, 1956). Corporates having surplus funds lend to another corporate in need of funds.

Inter-corporate deposits are exempt from the definition of deposits under Companies Act. Therefore, this is a very widely used mode of finance.

However, the companies shall also consider applicability of the restrictions under section 185 (dealing with loan to directors etc.) and section 186 (dealing with loans and investments by companies) of the Act, 2013 on the lending as well as the borrowing companies.

4. External Commercial Borrowings (ECBs)

ECB is basically debt availed by Indian companies in foreign currency, from a non-resident lender, in accordance with the ECB Framework, issued by the Ministry of Finance. There are no restrictions on the use of such loans, except the items mentioned in the negative list in relation to the end use mentioned by BRI in the ECB framework. Once the RBI and Ministry of Finance approves a loan and its terms, no limitations are placed on interest and principal payments. However, entities are required to report to the RBI through its designated banker every time an interest payment is made.

RBI vide RBI/2017-18/169 A.P. (DIR Series) Circular No.25[1] dated April 27, 2018 has further liberalised certain norms of the framework. The erstwhile provision had prescribed separate all-in-cost ceilings for different tracks in ECBs which were linked to the maturity period. Now, a uniform all-in-cost ceiling of 450 basis points over the benchmark rate is stipulated irrespective of the maturity period of ECB. Further, the ECB Liability to Equity Ratio for ECB raised from direct foreign equity holder under automatic route has been enhanced to 7:1 (as against 4:1 earlier). Therefore, by liberalising the framework, the Government has broaden the scope of fund raising for the companies.

Further, earlier, proceeds of ECBS could be used only for the purpose of meeting capital expenditures, but vide the aforesaid change, the end use restriction has been liberalised and the ECBs can now be used for the purpose of working capital requirements as well.

Compliance for borrowings by a company under the Companies Act, 2013

The borrowing powers of a company is mentioned in section 179(3) and 180(1)(c) of the Companies Act 2013.

Section 179 (3) (d): The powers to borrow money can only be exercised by the Directors at a duly convened meeting of the board, to borrow moneys. However, the power to borrow money may be delegated by the Board by passing a resolution for such delegation at a duly convened Board Meeting, to any committee of directors, the managing director, the manager or any other principal officer of the company or in the case of a branch office of the company, the principal officer of the branch office.

Section 180 (1) (c): The provisions of this section prohibits the Board of Directors of a company from borrowing a sum which together with the moneys already borrowed by the company, exceeds the aggregate of its paid-up share capital and free reserves, apart from the temporary loans obtained by the company’s bankers in the ordinary course of business unless the company has received the prior approval of the shareholders of the company, through a special resolution in general meeting.

Therefore, the Board may continue borrowing within the limits approved by the shareholders, however, in order to borrow beyond the above-mentioned limit, the Board of Directors will have to obtain prior approval of the shareholders.

Meaning of the term ‘Temporary Loans’ in section 180(1)(C)

As per the explanation provided in section 180(1)(C), the expression “temporary loans”

means loans repayable on demand or within six months from the date of the loan such as short-term, cash credit arrangements, the discounting of bills and the issue of other short-term loans of a seasonal character, but does not include loans raised for the purpose of financial expenditure of a capital nature.

Borrowings by private companies

Private companies are exempted from the entire provisions of section 180 of Act, 2013 vide MCA Notification[2] dated June 5, 2015.

Borrowings by banking companies:

As per the proviso provided in section 180(1)(C), the acceptance of deposits of money from the public, repayable on demand or otherwise, and withdrawable by cheque, draft, order or otherwise, in the ordinary course of its business by a banking company, shall not be deemed to be borrowing of monies by the banking company.

Ultra Vires Borrowings

As per the provision of section 180 (5), where a company borrows in excess of its borrowing limits as approved by the shareholders, then such borrowing in excess of the limit shall not be valid or effectual unless the lender proves that he advances the loan in good faith without knowledge that the limit imposed by the law has been exceeded.

Conclusion

The above mentioned various modes of borrowings provide the various option of fund raising by the companies. The various options of borrowing further depends on the need of the companies and the nature of borrowings. The most relevant part is the basic idea is to identify and explore the avenues to reduce the borrowing costs for companies. Identifying low cost avenues is a joint responsibility of the treasury department and the compliance team, while the treasury team should opt to explore new avenues, the compliance team should see if the same fits into the existing regulatory framework.

[1] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11267&Mode=0

[2] http://www.mca.gov.in/Ministry/pdf/Exemptions_to_private_companies_05062015.pdf

Sudden prohibition for CA Valuers

By Yutika Lohia, (yutika@vinodkothari.com) (finserv@vinodkothari.com)

Introduction

The income tax laws of our country have witnessed a lot vicissitudes over the years. Responding to the changing reforms as well as practices, the law makers have always tried to pace up with the dynamic economy. Chartered Accountants, in India, are widely accepted as tax professionals and in that capacity they play a very important role in the comprehending the income tax laws for the commoners. But a recent change by the IT Department would certainly not please the CA fraternity in the country. Read more →