Archive for month: June, 2026

Financial Intermediation: The Future Will Test What the Past Has Taught

Pearls of Wisdom from Dr Frank Fabozzi

Read the trascript from the Mahattva session with Dr. Frank Fabozzi. See the full video on our YouTube channel here.

Vinod Kothari

Good day, everyone, and today our guest is Dr. Frank Fabozzi. If you are in finance, I don’t need to introduce who Dr. Fabozzi is, because anyone who has studied finance would have gone through some of his books. If you are in the financial world, you would probably go through some of the institutions where he started. If you are in one of the leading financial players, you would have probably heard or benefited from his lectures or writings. Author of over 150 books. Over the last 60 years of teaching and writing history, Dr. Fabozzi is a leading, pioneering name in the world of finance, and today it’s sheer good luck that we have him. He has taught in leading institutions in the world, including the MIT, including City University of New York, including Yale University, plenty of academic institutions all over the world he has taught Dr. Fabozzi, it’s our indeed a great pleasure that despite your extremely busy schedule, you could find time to address us and our participants today. Dr. Fabozzi.

Dr Frank Fabozzi

Thank you for that kind introduction, I appreciate it.

Vinod Kothari

Okay. Dr. Fabozzi, the first that I have for you is quite generic, and I’m trying to talk or get some sense from you about financial intermediation in general. Now, you are a veteran, and you’ve seen the financial intermediaries evolve over the last, roughly about 60 years, and you’re, I mean, interacted and written with a lot of scholars all over this time. Could you tell us what are the key trends that you were able to identify, and going forward, how do you see these trends emerging? Dr Fabozzi.

Dr Frank Fabozzi

Well. I’ve been around, as you mentioned, in this market for 50 or 60 years, and, you know, if we’re talking about how financial intermediation or financial markets have changed over that period, I mean. I’ll give you some general information about it, but it’s very interesting. It’s hard to appreciate how the market has changed until you actually were involved in that market and saw how those innovations were important. But if we were looking at, like, thinking about several long-term trends that stand out over the last 50 to 60 years, I can think of, like, 3 themes that would help me think about how capital markets have changed. The first one is what we call the transformation from what is called “originate and hold” to “originate and distribute”. We’ll talk about that. Second, the impact of technology and data, and that’s often overlooked. And the growing inter-connectedness of the financial system.

So let me just take them one at a time.

First is, if we’ve seen a shift from bank-centered finance toward market-centered finance. So we know historically what a bank would have done. They’ve gathered deposits, they made loans, they largely held those loans on their balance sheet until maturity. Today, capital markets perform many functions that were once dominated by banks. For example, developments such as securitization, which you and I know very well, given a book on that area, syndicated lending, private credit. even ETFs and derivatives. They’ve expanded the role of markets in allocating capital, and managing risk. So the broader significance is really not what a lot of people think: the creation of new products. But it is a change in how financial intermediation is organized. The financial system has moved from, as I mentioned before, the originate and hold model, towards originate and distribute model, where origination, funding, risk-bearing, servicing, and distributions, can be performed by different specialized participants.

The second trend, I believe, is that information technology has fundamentally changed the economics of financial intermediation. Traditionally, banks possessed significant informational advantages because they knew their customers, and they knew their local markets better than anyone else. Credit decisions then, often relied on personal relationships, local knowledge, and accumulated experience. Today, we know there is a vast amount of financial, operational, and behavioral data that can be collated, analyzed, and transmitted almost instantly. Information that was once difficult to obtain and largely confined to local institutions has become far more accessible. As a result, this competitive advantage increasingly comes from the data, analytics, and technology, rather than proximity alone, or factors like understanding local markets. This has, if we think of the implications, lowered the information barriers, increased the competition, and enabled new entrants.

Vinod Kothari

New entrants, such as?

Dr Frank Fabozzi

FinTech companies, and firms that lend to private entities, and private credit in general. These all compete in an area that was once dominated by traditional banks.

And the third trend I see is regulation has played an important role in shaping the evolution of financial intermediation. You know, historically, after every major financial crisis, regulators get wiser.. They make sure that their regulated entities tighten up on their credit. improved liquidity, and they develop risk management requirements. So these reforms generally made the banking system safer and more resilient; but what they’ve also done is they’ve altered the economics of certain activities that go on in the financial markets. So as a result, some lending and risk-taking activities migrated to other parts of the financial system as a result. And the risk that disappears, that’s the important thing, we always think about, you know, these innovations as better handling of risk. But it’s the handling of risk, not risk disappearing. What we see is risk is now redistributed among the key participants in the financial market.

So, one of the enduring lessons of financial history is that regulation often brings changes where risk resides, who bears that risk, rather than eliminating the risk itself. So, looking ahead, here’s what I expect. Financial intermediation is going to become increasingly interconnected. The traditional boundaries between banks, asset management firms, technology firms, even the exchanges and data providers, are already becoming less distinct, and that trend is going to continue.

And at the same time, some of the things are unlikely to change, and this is important to emphasize. Finance is ultimately built on trust. Institutions can adopt new technology, business models, delivery channels, but still, they must earn the confidence of customers, investors, and markets. Those are the tools that’ll continue to continually evolve, but the core functions of finance: allocating capital, providing liquidity, managing risk – they fundamentally remain the same.

Vinod Kothari

Sir, thank you very much for the perspective, and you talked about three key trends which you say have changed the shape of financial intermediation over the years. You talked about, number one, the originate- to-distribute the model having taken over the originate- to-hold the model. And then you talked about the role of data technology. And then you talked about the increasing interconnectedness in the financial system. Extremely important, sir.

My second question flows from what you just mentioned; It’s actually an offshoot of what you just elaborated, and therefore comes naturally. You talked about the role of financial intermediaries from changing from the aggregated model: originating to hold, to continue to fund it, and continue to keep it, and to manage the risk of the lending transaction. And you’re saying that this is now getting kind of broken into several subcomponents. Now, does it mean the so-called concept of universal banking, where one bank does it all, is gradually giving way to more itemized or atomized functions, with each intermediary focusing on core competencies? There are some who do underwriting, some who do processing, there are some who do data keeping, there are some who do recoveries or risk management, and there are some who do funding. Do you see, therefore, that universal banking is going to be a thing of the past?

Dr Frank Fabozzi

Well I don’t know if it’s going to be a thing of the past. I do think the traditional concept of universal banks is under increasing pressure, although I don’t believe that they’ll disappear, and let me just explain why. Historically, if we think about it, universal banks offered all of the functions that you mentioned, [and it’s a little difficult for me to hear you, if you could put it a little louder, but I think I got what you said.] But, you know, you know, all of those things you mentioned, there were clear advantages to do that in one structure, because what can a bank do? A bank could share information internally, develop customer relationships, which could spill over to multiple products. and large balance sheets provided stability and funding capability. Now, let’s look at what has changed. Okay, first, technology dramatically lowered the cost of specialization. All those little things the banks did, today, different firms can excel at, for example, acquiring customers, credit assessment, payments, custody, investment management, servicing, data analytics. And they can all be done now by specialized firms. As a result, many activities that were bundled together in a universal bank can now be performed more efficiently by specialized providers. However, I don’t think that the coordinating function has disappeared. Financial services ultimately, and I’m coming back to this concept of depends on trust, accountability, and relationship management. Someone still needs to understand the customer, aggregate information across multiple activities, manage risk holistically, and provide a seamless experience. Those responsibilities become even more important as the underlying financial system becomes more fragmented, more participants. For that reason, I see universal banks evolving. Rather than disappearing. Their role’s likely to shift from being vertically integrated manufacturers of every financial product to becoming platforms that coordinate a network of specialized providers, and by platform, just to be clear, I mean an organization that brings together and coordinates multiple providers and customers through a common interface, rather than producing every service itself. The customer may continue to interact with a single institution, but what goes behind the scenes is : There are multiple firms that may be contributing different components to the overall service. For example, a wealth management client may receive investment advice through a brand, we see this bank brand platform, while portfolio management is provided by an asset management that could be a subsidiary to the bank. Securities are held by custodians. Trades are executed through external market makers and exchange. Risk analytics are supplied by specialized technology firms, and the underlying infrastructure operates on a third-party cloud computing platform. And similarly, if we look at the mortgage customer, they may deal exclusively with a bank, even though who all are actually involved ? Credit scoring by another entity. Property valuation. Nowadays we have these drive-by inspections in the United States. But you have specialized people who do that. You have fraud detection, documentation verification, then you have loan services. All provided by separate specialized providers. So, in this environment, the competitive advantage of universal banks will increasingly rely on their ability to integrate and oversee the specialized services. Well, from the customer’s perspective, they don’t see this. They just see one entity.

So, this evolution creates both opportunities and challenges. Specialization can improve efficiency. innovation and customer choice. At the same time, it makes risks harder to identify, because exposures are distributed across a network of institutions rather than concentrated on the balance sheet of just one entity. So understanding how these connections interact will become increasingly important, not only for market participants, but, really regulators also.

So I don’t think the concluding response here is whether universal banks will survive. The more important message is they adapt. My expectation is that the most successful institutions will be those that combine the trust, the balance sheet strength, and relationships of traditional banking with the flexibility of platform based business models. So in that sense, the universal banking of the future may look less like a financial conglomerate and more like an orchestrator of a financial ecosystem.

Vinod Kothari

Extremely wonderful comment, sir.

So, my next flows from the point that you mentioned some time back. Where you were talking about the evolution of the regulations focusing on risk management. And, given that, you also mentioned that, there is an increasing risk-based regulation by the financial regulators across the world. Now, we also see that there is a development which is very clearly visible, and for this, concerns have been expressed by the Financial Stability Board as well. The development of unregulated or less regulated financial intermediaries, which are not banks. For example, talk about private credit funds. Now, roughly about $1.5 to $2 trillion are sitting with private credit funds, which are non-banking financial intermediaries. They are not banks. They’re doing functions which are similar to banks. And at the same time, there is obviously no prudential regulation applicable to them. Do you see any concern in this development where non-banking financial bodies, such as private credit funds, accumulate a substantial extent of wealth. They do a function which is quite close to the traditional banks, and yet not be subjected to the banking regulations.

Dr Frank Fabozzi

We’re talking about the rise of non-financial intermediaries, NDFIs, and actually, I think it’s one of the most significant developments in modern finance. These entities include asset managers, private credit funds, hedge funds, money market funds, insurance companies, and other entities that perform important intermediation functions without operating as traditional banks, as you pointed out. But to me, their growth is just a natural evolution of the financial systems. They’ve expanded access to capital, they’ve created alternative funding channels. They’ve brought specialized expertise to different market segments, and they’ve increased competition. So, in many cases, they’ve helped make financial markets broader and more efficient. To me, the key is not whether they’re good or they’re bad. They’re now an essential part of the financial system. The more important, I think, is whether we fully understand the risks that they create, and how those risks interact with the broader financial system.

So, if I were to focus on three areas, the first would be leverage. It can be more difficult to identify and measure risk of leverage in parts of the non-banking system. In banks. Leverage is generally visible. We could look at the balance sheet, and report to regulators, and they’re subject to extensive regulatory oversight. Now, when we talk about non-bank institutions. Leverage may arise through taking it away. They can securitise. You have derivatives, you have repo financing, you have borrowing arrangements, or you have other structures, but they’re not as transparent as the risks that we see as we can identify in banks. So as a result, risk can build gradually and remain largely unnoticed on these non-bank institutions. Until market conditions deteriorate.

The second is liquidity risk, and that remains a significant concern. Some investment vehicles offer frequent liquidity while holding assets that may be difficult to sell and value, during periods of market distress. Under normal conditions, that mismatch may not be apparent. During periods of uncertainty, however, it can create pressure for asset sales, and I think, create market instability.

And third, the financial system has become interconnected, as I’ve emphasized, everything across the board. If I didn’t mention clearinghouses, we have that same thing. They’re all linked through funding arrangements, collateral relationships, all having shared risk exposure. As a result, risks that originated in one sector can rapidly spread to others. Financial shocks rarely remain confined to the institutions where they first appeared. And this is particularly concerning really in private markets.

We talk about private credit and private equity, and those are the two major areas in alternative investments that we’re concerned with. And they’re key, also, to the role of development of startup companies. I don’t view NBFIs as a source of weakness, nor do I view them as a substitute for traditional banking. They become permanent and important components of the financial ecosystem. The challenge for regulators, in my opinion, and not only regulators, but investors, is to focus less on where risks are located, and more on how leverage, liquidity pressures, and this interconnectedness can interact across the system. So, in the future, financial stability will depend not only on the resilience of individual institutions, but also on our ability to understand the networks that connect them.

Vinod Kothari

That’s an extremely important observation, and you mentioned, the three significant risks of private credit, or private equity for that matter, are leverage, liquidity, and interconnectedness. Would you also take opacity as one of the significant risks? Opacity because they are not governed by any specific reporting requirements, and they are not governed by any specific valuation requirements as well?

Dr Frank Fabozzi

Yes, I agree, yeah.

Vinod Kothari

So, that brings me to the fifth question relating to artificial intelligence, and the entire world today is talking about artificial intelligence. So far as financial intermediaries are concerned, it’s quite obvious that most of them are currently relying on AI, and I’m sure you would agree that going forward, they rely more on use of AI, either for decision making, and obviously for managing their business. Now, one of the risks which is quite commonly pointed out when you rely on artificial intelligence is that human thinking could be different. Every human mind can think differently, but artificial intelligence, ultimately, the way it’s structured, it might probably lead to or give the same answer in given situations. So hundreds of thousands of people thinking alike, or thinking exactly the same because all of them are relying on the AI tool, might result in a homogenized action. And therefore, there might probably be more volatility in the system because of reliance on AI. Is that a risk that you perceive, or do you see any other risk in the increasing dependence of the financial world on financial technology, including artificial intelligence? Sir.

Dr Frank Fabozzi

Well, it’s the first time someone asked me about AI, mostly when people say, well, I lost my job due to AI? But, that’s a different answer, and for this one, and I’ll have a different answer. I think the concern that you mentioned is very real, although perhaps not for the reasons that some people often assume. Most discussions about AI and finance focus on whether AI can make better predictions, improve efficiency, reduce costs. or process information faster than humans can. And those are important, but let’s look at it from a financial stability perspective. I think the more important issue is whether AI changes what you just mentioned, the diversity of decision-making within the financial system. Financial markets function best when the market when participants hold different views.

Every time someone says, oh, great minds think alike, I would say, no, great minds should think differently. Every transaction , think about this, every transaction that we see going on in the marketplace reflects some disagreement about value, risk, or future outcomes. Historically, that diversity emerged because of different investors, institutions, investment committees brought different experiences, incentives, and judgments to the decision-making. So, the concern to me is that widespread adoption of AI can unintentionally reduce that diversity. If a large number of institutions rely on similar models, data sources and training methods, and they may begin to reach conclusions at roughly the same time, the same conclusions, at the same time. In normal markets. That may improve efficiency. During periods of stress, however, it can amplify market movements, because many participants are reaching, or they’re reacting in the same direction simultaneously, based on what AI provides. So, in many ways, this is not an entirely new phenomenon. If we look at financial history, it contains numerous examples of institutions relying on similar risk models, credit ratings, or forecasting frameworks. So, one lesson from a past crisis is that a system can become fragile when too many participants make decisions based on the same assumptions. Even if each individual institution appears to be prudent when viewed in isolation.

If we go back and we tear apart the global financial crisis, we could see the assumptions that were made. Just a simple example. You know, people generating their models assuming, their risk models assuming, a normal distribution.

We’ve now learned a lot more about probability distributions of outcomes, particularly extreme events, but people did that only after the crisis.

So at the same time, I don’t believe that the solution is to reject AI. Not that you could really reject it; that’s an impossibility. But the real challenge to me is governance. I didn’t spend a lot of time talking about governance. Now with AI and a few other events, I see that as becoming increasingly important. Because as AI becomes more deeply embedded in financial institutions, it’s essential that the responsibility for a decision remains with human professionals. Models can provide insights, recommendations, but accountability cannot be delegated to a computer programmer. You can’t get it from algorithms. So, decisions that affect clients. portfolios and institutions, they require human oversight, something I think we’re not seeing. Not only human oversights, judgment, and the ability to consider factors that may not be captured by the data. The goal should be Judgment enhanced by AI rather than judgment by AI.

By the way, look at the World Cup, since I imagine you have a global audience here. There’s a human that’s coaching that team. They have all the data and all the statistics. If you ever looked at the accumulation of information, statistics, on every moment. On a court, you know, whether it’s a basketball court, a soccer field, or a base they have all the statistics they want. We still have a human coach managing those teams, or coaching those teams.

So, in fact, I think the greatest risk is not that AI makes mistakes, because we all make mistakes. The greater risk is that large institutions begin making the same mistake at the same time, because they’re relying on similar models and similar recommendations. A single bad decision: no problem. That’s manageable. But thousands of institutions making the same bad decision simultaneously has systemic consequences.

So I think, to wrap it up, I think about AI in terms of financial stability. The key is not simply whether a model is accurate. The more important question is whether widespread adoption of that model makes the financial system, to use the term you said earlier, more homogeneous. Efficiency is valuable, but resilience often comes from diversity.

Vinod Kothari

Fantastic comments. I think it’s extremely wonderful to hear your thoughts on this, that ultimately it’s human decision, human governance, which can mitigate the risk of the homogenized behavior that might result from reliance on artificial intelligence. Extremely valid comment.

Sir, I cannot resist the temptation but to ask you about this book that we wrote immediately after the global financial crisis. [Shows Introduction to Securitization, by Dr Fabozzi and Vinod Kothari] It’s your book Introduction to Securitization. So, where do we stand today? What do you think about securitization and credit derivatives? Are these the products which were designed for good times? But now that we have volatile markets, are these products still going to be relevant? What’s your futuristic thinking on these instruments?

Dr Frank Fabozzi

It’s very funny. You know as well as I, at that time, securitization was considered a gimmick and all that. As soon as the global financial crisis hit, though, the major agencies in the U.S. kept writing to emphasize the importance of securitization. If we think of it, there’s certainly periods when investors become more willing to take risks in search of higher returns. During those periods, you know, financial innovation often accelerates. Products become more complex, market participants sometimes focus more on yield than on the risk required to achieve the return. So financial history contains many of these examples, and, you know, we talk about securitization and credit derivatives. They’re such examples.

You know, it’s very difficult to see how the scenario changed. I’m 79. I’ll give you an example: When I tell you about securitization, how important it is, it is so difficult for most of the people listening to understand that. Let me put it in perspective. And this is no exaggeration at all. In 1972 or 73, prior to securitization I went to get a mortgage loan for a house. I went to my local savings and loan association, I walked in there, and I said, I’d like to get a house. I need money to buy this particular house, and I gave them the address. They said to me, first thing is, oh, do you have an account here? And I would say, yes, I did. Because I knew they were going to ask that.

Then they said to me, okay, you want to buy the old Phillips property? I know him, he’s a great guy, I used to golf with him on weekends, and we’d have dinners together, I know his kids, and all that. He knew all about the house. He said, oh, a couple of months ago, they just added an enhancement to their basement and all that. So he [banker] knew everything about the house. He knew everything about the seller. He didn’t know that much about me, because I just moved into the area. Now, what happened then? He said, I can evaluate your credit. He did. He said, we approve you for the loan. I said, great, when can I close? He said to me, you can close when other people who we’ve made loans to pay off their loans! Now, I couldn’t believe that I couldn’t get a loan until other people paid off their loans or defaulted.

So what happened? There were parts of the country where banks had a lot of money. There were other parts of the country, and I was in the other one. Parts of a country where money was very tight.

In comes securitization. And then, at the same time, there was the savings and loan crisis. Banks had 30-year mortgages on their books. During a period of rising interest rates, these banks were technically underwater, but the government kept them alive. And I mean, these institutions were savings and loan institutions.

So what then happened? Someone came up with a bright idea and said, Why keep the mortgage loans on the books? A bank doesn’t want to hold a loan for 30 years, because they’re worried about interest rates fluctuating up and down. When rates fluctuate up and down, a bank’s margin, will either decrease, or increase, and become negative, as it did during the savings and loan crisis1. So they developed securitization. What they did, they said, is take these illiquid loans. And pull them together, And then create securities based on these loans, that are backed by these loans.

And all of a sudden, you now created a capital market for these instruments alone, these mortgage-backed securities. And that helped resolve the savings and loan crisis, and make mortgages readily available. Nowadays, you want a mortgage? And you don’t have that much time. You have gone to fill up your gas tank. May not be the gas tank of a small car, but if you have a big truck, by the time you fill up that truck with gas, they will give you a mortgage.

So, to me, even though securitization sounds like a horrible thing, you could see in the context that I described why it was very important.

Credit derivatives did the same thing. Credit derivatives, and by the way, securitization, have gone beyond mortgages. We have student loans. You can even get municipalities doing securitization, their traffic tickets, everything, nowadays. And in fact, you may be an athlete in a certain sport. You can securitize your future royalties. Almost all the major entertainers, particularly musicians and other artists, securitized their future earnings.

So both credit derivatives and securitization, they were both developed to address legitimate economic needs. And they make economic sense. What they’re doing is separating the origination of risk from the ownership of risk. And that improves efficiency, expands access to capital, and enhances, certainly, risk management. When corporations do it, this securitization is a risk management tool for them. So, the difficulty arises when market participants begin to confuse risk transfer with risk elimination. Moving risk from one institution to another doesn’t make the risk disappear. It simply changes who bears it. So, that’s my view on the two. I don’t see them as being gimmickry at all.

Vinod Kothari

Thank you very much, sir. It’s an extremely pertinent comment. Your thoughts are extremely important for the market participants. And your time today, I know, is extremely precious, so thank you very much for giving your time today, and wish you health and happiness, sir. Thank you very much.

Dr Frank Fabozzi

Thank you, thank you for the opportunity.

- Readers may note US mortgages are typically fixed rate mortgages. ↩︎

TReDS Master Directions issued by RBI

- Harshita Malik | finserv@vinodkothari.com

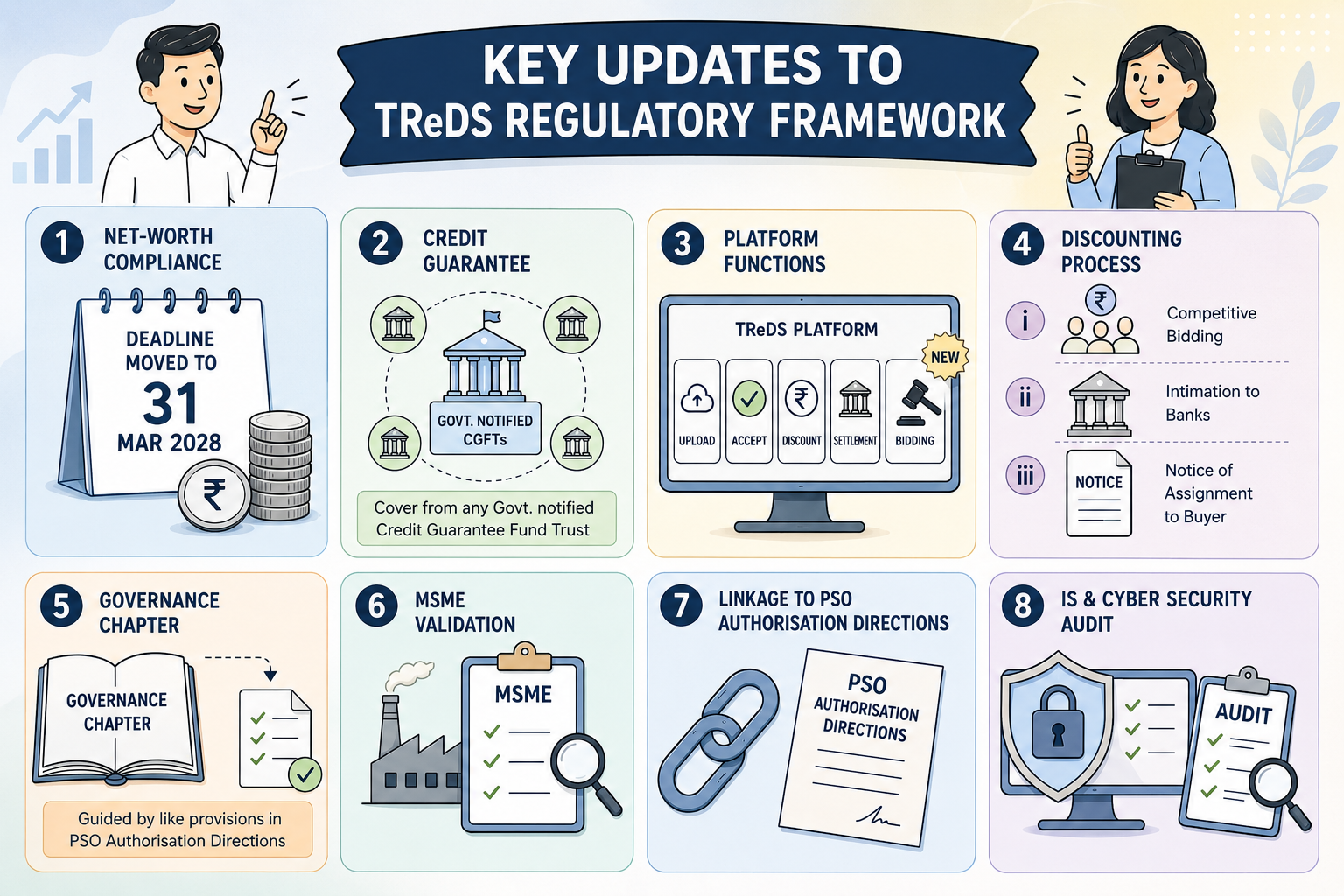

RBI has issued the Reserve Bank of India (Trade Receivables Discounting System) Directions, 2026 (‘Final Directions’), replacing the draft Trade Receivables Discounting System (TReDS) directions (‘Draft Directions’) published earlier (read our article on the draft here). The Final Directions make a number of substantive changes from the Draft Directions and consolidate several operational and supervisory requirements by cross-referencing the Master Directions on Authorisation to operate a Payment System (‘PSO Authorisation Directions’).

Highlights:

- Net-worth compliance: Prescribed minimum limit of ₹25 crore, deadline being 31st March 2028 for existing entities;

- Credit Guarantee: Financiers may now avail credit guarantee cover from any credit guarantee fund trust notified by the Government of India (earlier draft limited cover to NCGTC);

- Platform Functions: ‘Bidding’ added as a formally recognised core platform function alongside uploading, accepting, discounting and settlement;

- Discounting Process: Three operational obligations for discounting:

(i) transparent multi-financier competitive bidding; (this is similar to multi-lending platform in case of digital lending)

(ii) intimation to the working capital/CC account banks of the buyer and seller; and

(iii) formal service of a notice of assignment to the buyer in favour of the financier;

- Governance Chapter: Deletion of the standalone governance/fit-and-proper chapter proposed in the draft; presumably now guided by the like provisions in the PSO Authorisation Directions;

- MSME Validation: Platforms must implement validation mechanisms to ensure that sellers uploading invoices or bills of exchange are bona fide MSMEs; While the draft recommended a simplified process for onboarding of MSMEs, the Final Directions requires a validation mechanism to ensure that seller is MSME;

- Linkage to PSO Authorisation Directions: Several application and authorisation procedures are cross-referenced to the PSO Authorisation Directions;

- IS & Cyber Security Audit: IS audit and cyber security audit requirements have been aligned with RBI guidance referenced in DPSS.CO.OD.No.1325/06.11.001/2019-20 dated January 10, 2020 (scope and coverage to follow that letter).

Background:

TReDS is a technology-enabled platform for financing trade receivables through multiple financiers. The Draft Directions issued earlier set out proposed regulatory, governance and operational requirements. The Final Directions refine those proposals, streamline supervisory overlaps by cross-referencing existing PSO Authorisation Directions, and add operational safeguards to strengthen transparency and MSME protection.

Discounting Process:

The platform shall facilitate the discounting of factoring units by way of receiving bids from multiple financiers in a transparent manner, resulting in flow of funds to the sellers, providing intimation to banks holding working capital / cash credit accounts of buyer and seller, serving of notice of assignment to buyer in favour of financier, with final payment being made by the buyer to the financier on due date. Since financing a transaction on TReDS will result in assignment of receivables in favour of the financier, the platform shall file the said assignment with the central registry (CERSAI), as provided under Registration of Assignment of Receivables (Reserve Bank) Regulations, 2022 dated January 14, 2022 (as amended from time to time).

Changes at a Glance:

| Basis | Erstwhile Guidelines/Circulars | Draft Directions | Final Directions |

|---|---|---|---|

| Definition of TReDS | Scheme for setting up and operating the institutional mechanism for facilitating the financing of trade receivables of MSMEs from corporate and other buyers, including Government Departments and Public Sector Undertakings (PSUs), through multiple financiers | A system for facilitating financing of trade receivables. It is a technology platform on a digital or electronic network for facilitating factoring of trade receivables through multiple financiers | A technology platform on a digital or electronic network for facilitating factoring of trade receivables through multiple financiers. Although the definition has changed from the erstwhile guidelines, the substance remains the same. |

| Application Mechanism | Application format same as for any non-bank entity to seek authorisation under the PSS Act | PRAVAAH portal, Form A of Appendix 1 of these directions | Subsumed into the consolidated PSO Authorisation Master Direction. Application through the PRAVAAH portal. |

| Capital Requirement | ₹25 crore paid-up equity capital | ₹25 crore Net Worth | ₹25 crore Net Worth |

| Governance / Fit-and-Proper | Specified fit and proper criteria for entities and their promoter/promoter group- sound credentials and integrity, financial soundness and track record of at least 5 years in running the business | Specified fit and proper criteria for directors- fairness and integrity, conviction, insolvency debarment, unsound mind, financially unsound | No such requirement prescribed under the Final Directions, since such aspects are covered under the PSO Authorisation Directions |

| Net-worth Compliance Deadline | Paid-up equity capital to be maintained from the inception itself | 31st March 2027- for existing entities authorised to operate TReDS | 31st March 2028- for existing entities authorised to operate TReDS |

| Participants on TReDS Platform | Seller, Buyer, Financier, and Insurance Companies | Sellers, Buyers, Financiers, Insurance Companies, NCGTC | Sellers, Buyers, Financiers, Insurance Companies, Credit Guarantee Fund Trust notified by Government of India (not restricted to NCGTC) |

| Platform Activities | Uploading, accepting, discounting, bidding, trading and settlement | Uploading, accepting, discounting and settlement of factoring units | Uploading, accepting, bidding, discounting and settlement of factoring units |

| MSME Eligibility Verification | Required as part of the KYC process | Validation mechanisms required to be put in place to ensure that the seller uploading invoices/bills of exchange is an MSME | Validation mechanisms to ensure that the seller is an MSME, and funds due to the seller are credited in the seller’s bank account only. |

| Discounting Process | Facilitate the discounting of the factoring units by the financiers resulting in flow of funds to the MSME with final payment of the factoring unit being made by the buyer to the financier on due date. | Facilitate the discounting of factoring units by the financiers, resulting in flow of funds to the sellers, with final payment of the factoring unit being made by the buyer to the financier on due date | 2 new operational obligations added: (i) intimation to working capital/CC account banks of buyer and seller; (ii) formal serving of notice of assignment to buyer in favour of the financier |

| Credit Guarantee | Credit insurance available, no mention of credit guarantee | Only through NCGTC | Can be provided by any credit guarantee fund trust set up by Government of India |

| IS Audit& Cyber Security Audit | No such mandatory requirement | Conducted by CERT-In empanelled auditors | Scope and coverage shall be as per the RBI’s Letter DPSS.CO.OD.No.1325/06.11.001/2019-20 dated January 10, 2020 |

| Reporting Requirements | No such requirement. | Annually (by 30 Sept): submit audited net-worth certificate and IS/Cyber Security Audit report. Monthly (by 7th): submit TReDS statistics. (Format: Appendix 1)Event-based: report any change in Board along with director declaration/undertaking. (Format: Appendix 2) | Remains unchanged from the draft. |

| Settlement Process | TReDS will generate the payment obligations of all financiers in respect of all factoring units financed on a given date, on T+2 basis. | TReDS to ensure efficient and seamless settlement of transactions amongst the participants | Remains unchanged from the draft |

| KYC | KYC of both the buyer and the MSME seller is required | KYC of the buyer is required. Validation mechanism that the seller is an MSME to be put in place. | Remains unchanged from the draft |

Closing Remarks

The Final Directions strengthen operational transparency, broaden access to government-backed credit guarantees, and place explicit obligations on platforms to verify MSME eligibility and formalise discounting workflows. By folding several requirements into the PSO Authorisation Directions, the RBI has aimed to streamline authorisation and oversight while emphasising operational controls that protect MSMEs and financiers.

Avoid Turning Your Referral Partner into a DSA/LSP

Simrat Singh | Finserv@vinodkothari.com

RBI regulatory framework for banks and NBFCs recognise entities such as LSPs and DSAs, but do not define the term “referral partner”. Consequently, several lenders engage referral partners under agreements that merely replicate the DSA arrangement with a change in the nomenclature but without altering its substance. This is a risky approach. Courts have held that the existence of an agency relationship depends on the rights created between the parties, not on the title of the agreement. Therefore, if a referral partner agreement authorises the intermediary to represent the lender or perform functions ordinarily discharged by a DSA or outsourced agent, the intermediary may be regarded as a DSA irrespective of its contractual designation. Accordingly, while drafting a referral partner agreement, equal attention must be paid not just to the scope of what can be done but also what the agreement does not permit. To understand the difference between a LSP, Referral partner and DSA, may refer to our resource Referral or Representation? The Fine Line Between LSP, DSA and Referral Partner.

Set out below are contractual provisions that should be avoided in an agreement with a referral partner.

- Do not confer authority to make commitments: Such authority is inconsistent with a mere referral arrangement and indicates an agency relationship. The agreement should not permit the referral partner to:

- assure loan sanction;

- quote specific interest rates since that is a function of borrower risk and lender’s credit evaluation and interest rate model;

- commit timelines for approval or disbursement; or

- make any representation which is binding on the lender

- Do not permit the referral partner to hold itself out as representing the lender: A referral partner should not portray itself as the lender’s representative or create the impression that it is authorised to act on the lender’s behalf. Accordingly, the agreement should prohibit the intermediary from describing itself as the lender’s agent or representative, using the lender’s name or branding in a manner that suggests an affiliation beyond a referral arrangement, or making any statement or representation that could lead customers to believe that it has authority to act for or bind the lender.

- Do not permit collection or processing of loan applications and loan repayments: These functions form part of customer acquisition, onboarding and servicing, which are characteristics of DSAs or LSPs. A referral partner should not collect or verify KYC documents and/or scrutinise applications and collect customer information/documents in any manner. Further, activities such as identity verification, obtaining customer consents, conducting due diligence or facilitating KYC should remain with the lender or its authorised service providers. A referral partner should not participate in the lending process beyond introducing the customer.

- Keep performance obligations limited to referrals: The referral partner should not be evaluated based on portfolio quality; recovery performance; or loan servicing metrics. Performance obligations should relate only to successfully introducing prospective customers.

- No compensation linked to lending functions or loan performance: A success-based referral fee, by itself, does not create an agency relationship. However, the consideration should not be linked to underwriting, servicing, collections, portfolio performance, recoveries or any other lending function. The agreement should make it clear that the referral fee is payable solely for successful referrals and not for performing any activity connected with the lending process.

- Do not authorise communication of lending decisions/negotiation: All customer communications should originate directly from the lender. The referral partner should not communicate sanction or rejection of applications; loan terms; deficiencies in documentation; repayment schedules; or disbursement confirmation. Further, negotiation on behalf of the lender is a strong indicator of representation/agency. The agreement should not authorise the intermediary to negotiate pricing; tenure; collateral requirements; repayment schedules; or restructuring terms.

- Do not assign post-disbursement responsibilities: Its role should ordinarily cease once the customer has been introduced. The referral partner should not undertake collections; recovery; repayment follow-ups; customer grievance handling; restructuring assistance; or foreclosure processing.

- Avoid clauses indicating exclusive representation: Clauses requiring the intermediary to exclusively promote the lender’s products or act as its sales representative reinforce the impression that the intermediary is representing the lender rather than merely referring customers.

- Avoid excessive operational control: Compliance obligations may be imposed, but they should not amount to day-to-day supervision. Operational control is a recognised indicator of agency. Accordingly, the agreement should avoid prescribing detailed supervision clauses or detailed operational instructions unrelated to regulatory compliance.

- Include non-agency provisions: The agreement should expressly provide that:

- the referral partner is an independent contractor;

- the relationship between the parties is on a principal-to-principal basis;

- it has no authority to represent or bind the lender;

- the referral partner shall not collect, process, or handle customer documents, KYC records, or sensitive customer information;

- all lending decisions are taken exclusively by the lender;

- Avoid agency terminology: Last but not the least, expressions such as authorised representative; sales representative; marketing representative; branch; agent; or authorised person should be avoided throughout the agreement because the language used often reflects the intended legal relationship.

SEBI’s New Advertisement Code: Dil Khol Ke Advertise Kar?

– Prerna Roy | corplaw@vinodkothari.com

Advertisement of products and services is one of the key requirements of any business, including for capital markets intermediaries such as Stock Brokers, OBPPs, Research Analysts, Mutual Funds and Asset Management Companies etc. If a business does not advertise, prospective customers may never become aware of its products and services. At the same time, given the complexity of the products and services offered by these market participants, and the risks it exposes the retail customers to, these advertisement and marketing materials are regulated by SEBI. In this context, these SEBI-regulated entities are presently being governed by separate advertisement frameworks, resulting in a fragmented regulatory framework and differing compliance requirements. Further, strict compliance requirements attract in the form of prior approval requirements for all communications issued by these entities currently.

With the objective of promoting ease of doing business, regulatory consistency, consolidation of frameworks while continuing to focus on investor protection, SEBI has issued a consultation paper on the Common Advertisement Code for Specified SEBI-Regulated Entities. Through the proposed Code, SEBI seeks to ease the process of advertising by SEBI-regulated intermediaries by removing prior approval requirements and introducing a common framework, while continuing to maintain accountability, transparency and investor protection.

Read more: SEBI’s New Advertisement Code: Dil Khol Ke Advertise Kar?Key Proposals

- Permitting Celebrity endorsements

Presently, the regulatory framework generally prohibits celebrity endorsements by SEBI-regulated entities, except in case of MFs and AMCs, where the same is permitted at the industry level, subject to prior approval from SEBI (Para 11.9.5 of the SEBI Master Circular for Mutual Funds).

The proposed Code seeks to permit celebrity endorsements for all specified SEBI-regulated entities, subject to prior approval from SEBI or the relevant supervisory body. Such approval would be required for celebrity endorsements at the brand/entity level.

The Code identifies the following supervisory bodies for this purpose:

- Stock Exchanges – Stock Brokers, including Online Bond Platform Providers;

- Depositories – Depository Participants;

- Investment Advisers Administration and Supervisory Body (IAASB) – Investment Advisers;

- Research Analysts Administration and Supervisory Body (RAASB) – Research Analysts;

- Association of Mutual Funds in India (AMFI) – Mutual Funds and Asset Management Companies; and

- Association of Portfolio Managers in India (APMI) – Portfolio Managers.

- Clarifying the scope of Advertisement

Presently, there is no distinction between advertisements containing promotional content and general financial literacy content. As a result, even financial literacy content is required to comply with the regulatory framework governing advertisements.

The proposed Code seeks to distinguish between advertisements and non-advertisement communications by providing an illustrative list of communications that would not constitute advertisements. These include, inter alia, reports shared with existing clients, product/service information, regulatory communications, responses to client queries, basic factual information about the regulated entity, and non-promotional product demonstrations.

Thus, no approval/ reporting requirements would apply to communications that are purely educational or investor-awareness oriented and do not contain any promotional content relating to the products or services of a regulated entity, as such communications fall outside the scope of the proposed Code.

- Replacing Prior approval requirements by post advertisement reporting

Presently, the regulatory framework requires regulated entities to obtain prior approval from SEBI or the relevant supervisory body before issuing any advertisement. The proposed Code seeks to replace this requirement with a post-advertisement reporting framework, under which advertisements must be reported promptly and, in any event, no later than 24 hours from their issuance to SEBI/ relevant supervisory body.

- Permitting Rankings and rating in advertisements

Presently, there is a complete prohibition on the use of ratings or rankings in advertisements depicting performance.

The proposed Code seeks to permit specified regulated entities to use ratings/rankings in advertisements, provided such ratings/rankings are assigned by a Past Risk and Return Verification Agency (PaRRVA).

Notably, any entity recognised as a PaRRVA shall, in consultation with SEBI and industry bodies, develop a methodology for rating/ranking specified regulated entities. Such ratings/rankings must disclose their methodology, clarify that they are only one factor for investor consideration, and be based on a study or survey covering all relevant market participants to ensure objectivity and comparability.

- Prohibition on usage of dark patterns

Presently, none of the existing frameworks expressly prohibit the use of dark patterns, such as false urgency, subscription traps, or forced actions.

The proposed Code seeks to expressly prohibit the use of dark patterns specified in Annexure I to the Guidelines for Prevention and Regulation of Dark Patterns, 2023, issued by the Central Consumer Protection Authority.

Recent amendments issued by the RBI also focus on prohibiting use of dark patterns and mis-selling by RBI regulated entities such as banks and NBFCs. Read our article on the same here

- Abbreviated Disclosures for Short-Format Messaging allowed

Presently, mandatory disclosure requirements apply to all forms of advertisements. These disclosures, including disclaimers thereto, are lengthy in nature and take up a lot of space. The proposed Code seeks to relax this requirement for short-format communications such as SMS and push notifications. Where space constraints do not permit inclusion of the prescribed details and disclaimers, a hyperlink to such information on the regulated entity’s official website may be provided. The website, in turn, shall contain the detailed disclosures as required (refer Para 7(4) of the proposed Code).

Conclusion

This is a significant move by SEBI and is expected to promote ease of doing business while addressing the multiplicity of regulatory frameworks that often leave regulated entities wondering, “kya karen kya na karen, yeh kaisi mushkil haye.” By introducing a common and harmonised advertisement framework, SEBI seeks to bring greater clarity, consistency and regulatory certainty. Overall, the Consultation Paper is a welcome step in the present-day scenario.

NBFC-UL Classification Approach Revised by RBI

- Harshita Malik | finserv@vinodkothari.com

Background

RBI, vide its Press Release dated April 10, 2026, had issued draft Amendment Directions (read our article on the draft here) proposing changes to the methodology for identification of NBFC-Upper Layer (NBFC-UL) and the inclusion of Government-owned NBFCs in the Upper Layer. Following the consultation period, the RBI has finalised these proposals vide its Press Release dated June 24, 2026, effective immediately. The amendment package comprises four directions:

- SBR 2nd Amendment Directions: revises the UL identification framework under the Scale Based Regulation architecture;

- CRM 3rd Amendment Directions: extends concentration norms to Govt.-owned NBFCs and introduces the State Government guarantee provision;

- Governance Amendment Directions: exempts Govt.-owned NBFC-ULs from mandatory listing and pre-listing disclosures; and

- Financial Statements 2nd Amendment Directions: aligns the financial statements framework with the revised UL classification.

Revised Norms of Classification and Compliance

- Annual Classification/Identification Process:

RBI will continue to conduct an annual identification exercise for classifying NBFCs in the Upper Layer. Compliance obligations attach from the date the RBI notifies the NBFC-UL list, not from the date an entity crosses the asset threshold independently. - Revised Criteria for UL-Classification:

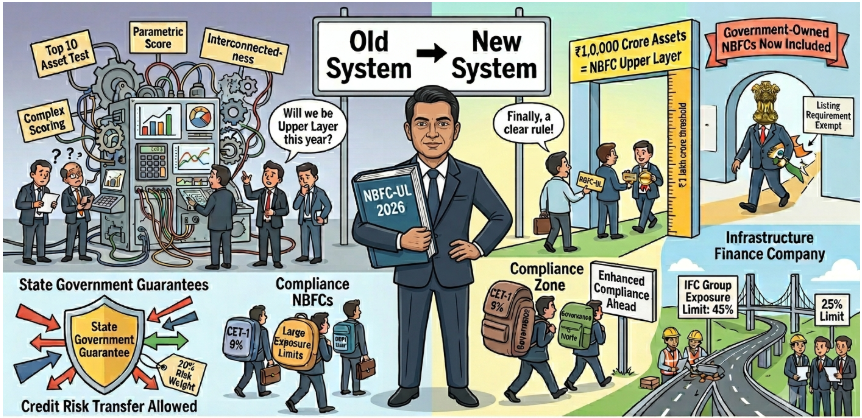

The current two-step approach (top ten by asset size and parametric scoring) will be replaced by a simple, absolute asset size criterion.

| An NBFC with standalone audited assets of ₹1,00,000 crore or more (as per the latest audited balance sheet) shall be classified in the Upper Layer. |

Key features of the revised criterion are:

- Standalone basis: asset size test applies to the standalone balance sheet of the NBFC, not consolidated group assets.

- Periodic review: ₹1,00,000 crore threshold will be reviewed every 3 years, more stringent than the 5-year cycle proposed in the draft, ensuring the threshold remains calibrated to market evolution.

- Bright-line simplicity: subjective scoring element is eliminated entirely, reducing regulatory uncertainty for entities near the boundary.

- Category-agnostic: UL list may include NBFC-ICCs, HFCs, CICs, deposit-taking NBFCs, and Government NBFCs; the type of NBFC is not a pre-condition.

- Inclusion of Government-owned NBFCs:

Eligible Government-owned NBFCs that breach the ₹1,00,000 crore threshold will now be included in the NBFC-UL list for the first time. Previously, these entities were placed only in the Base or Middle Layer. However, Government-owned NBFC-ULs are exempt from two obligations:- Mandatory listing within three years of notification (proviso to Para 43 of the Governance Directions); and

- Pre-listing disclosures (proviso to Para 23 of the Financial Statements Directions).

All other Upper Layer norms, including CET-1 capital, leverage, large exposures, governance, and provisioning requirements, apply in full.

- No exemption to Government Owned NBFCs from Concentration Norms:

Government-owned NBFCs will henceforth be subject to the concentration norms applicable to their respective layer. The earlier blanket exemption has been withdrawn. The transition is handled as follows:- Existing exposures that currently breach prudential limits are grandfathered and may continue until maturity, but no fresh exposure to such obligors is permitted.

- Additional exposure beyond prudential limits is permissible only if fully covered by eligible credit risk transfer instruments, resulting in zero net incremental exposure for Middle Layer and Upper Layer NBFCs.

- Provision for Credit Risk Transfer:

All NBFC-ULs may now use State Government guarantees to offset credit exposures without any portfolio-level cap. The regulatory treatment of the exposure so transferred is:- The exposure is recognised on the State Government (rather than the borrower);

- The exposure is exempt from prudential exposure limits; and

- 20% risk weight applies for capital computation purposes.

- Higher permissible exposure limit on connected counterparties for IFCs in Upper Layer:

NBFC-Infrastructure Finance Companies (‘NBFC-IFCs’) benefit from a specific carve-out: while the general rule caps exposure to a group of connected counterparties at 25% of the eligible capital base, NBFC-IFCs in the Upper Layer are permitted to go up to 45% of the eligible capital base (a 20 percentage-point premium) under the proviso to Para 35 of the Concentration Risk Management Directions. This reflects the inherently concentrated and long-tenor nature of infrastructure financing. - NBFCs in the Banking Group to comply with existing provisions:

NBFCs that are part of a banking group do not follow the SBR layer-based identification process for UL compliance. Instead, they shall continue to adhere to the applicable provisions for Upper Layer NBFCs, as per the RBI (Commercial Banks – Undertaking of Financial Services) Directions, 2025, for NBFCs under the banking group and carrying out lending activities. Our article on compliances to be followed by such NBFCs in the banking group can be seen here.

Regulatory Implications for Newly Classified NBFCs-UL

Classification as an NBFC-UL triggers a comprehensive set of enhanced regulatory requirements. Entities crossing the ₹1,00,000 crore threshold for the first time should anticipate the following:

| Compliance Area | Requirement for NBFC-UL | Trigger/Notes |

| CET-1 Capital | Minimum 9% of Risk-Weighted Assets | Binding where growth is aggressive |

| Leverage Ratio | Maintained alongside CRAR; special attention for derivative-heavy entities | Currently less acute as most NBFCs in India are not active in derivatives |

| Large Exposures Framework | Single-party cap: 20% of Tier 1 capital; Group cap: 25% (NBFC-IFC: 45%) | Economic-interdependence test determines group risk |

| Standard Asset Provisioning | Differential provisioning by asset class | Higher than ML/BL requirements |

| Mandatory Listing | Within 3 years of notification as UL | Exempt for Govt.-owned NBFC-ULs |

| Governance | Enhanced governance- board composition and listing requirements | Applicable under Chapter-V of the Governance Directions 2025 |

Closing Remarks

The shift from a hybrid scoring methodology to a single asset-size threshold is a significant moment in India’s NBFC regulatory architecture. The old framework, elegant in theory but notoriously opaque in application, left entities in a state of perpetual uncertainty about whether their exposure profile, liability structure, or interconnectedness would tip them over the UL line in any given year. The replacement with a bright-line rule removes that ambiguity.

That clarity, however, comes with a structural trade-off: the parametric approach was designed to capture systemic importance beyond sheer size: interconnectedness, leverage complexity, and liability fragility. A purely asset-based threshold is a blunter instrument. An NBFC with ₹1,05,000 crore in assets but a conservative, government-securities-heavy balance sheet will face the same UL compliance burden as one of equal size with complex wholesale funding and concentrated sector exposures.

The inclusion of Government-owned NBFCs is the more substantive policy shift. Large public-sector financial institutions, several of which have historically operated outside the SBR scrutiny framework, will now be subject to CET-1 discipline, large exposure limits, and differential provisioning. The listing exemption softens the reputational-governance dimension but does not dilute the prudential obligations.

The three-year review cycle (tightened from the draft’s five years) signals that the RBI is alive to the possibility that India’s NBFC sector may grow in ways that make ₹1,00,000 crore a less meaningful threshold over time. Market participants should treat this as a dynamic floor, not a permanent bright line.

Finally, the State Government guarantee provision, extending a zero-cap credit risk transfer tool to all NBFC-ULs, is a quiet but important liquidity-facilitation measure, especially relevant for NBFCs with significant exposure to state-owned utilities and infrastructure projects.

Ease of doing business to enhancing oversight: Proposed reforms by IRDAI in the Corporate Agent Regulations

– Khewan Sonchhatra, Executive | corplaw@vinodkothari.com

Several amendments were introduced to the Insurance Act, 1938, the Life Insurance Corporation Act, 1956, and the Insurance Regulatory and Development Authority Act, 1999 through the Sabki Bima Sabki Suraksha Act, 2025. These amendments primarily aim to liberalise foreign investment norms, reduce capital requirements, strengthen regulatory oversight of market participants, and enhance measures for the protection of policyholders’ interests[1].

Now, IRDAI has issued a consultation paper proposing amendments to the regulations governing insurance intermediaries. The CP aims at several objectives including simplifying regulatory requirements, promoting ease of doing business, strengthening accountability and transparency, and enhance policyholder protection.

Key proposals are:

1. Shift from recurring renewals to perpetual registration framework

The following amendments call for substitution of the current framework involving a 3-year renewal exercise by a perpetual registration framework involving payment of an annual fee:

| Regulation | Existing Provision | Proposed Amendment |

| Regulation 10 – Validity of Registration | A Certificate of Registration was valid for a period of three years and required renewal before expiry | Registration will remain valid indefinitely, subject to payment of annual fees and unless surrendered, suspended or cancelled by the Authority. |

| Regulation 11 – Procedure for Issuance of Fresh Certificate to Existing Corporate Agents | Regulation 11 dealt with the renewal of registration by Corporate Agents upon expiry of the three-year registration period. Renewal applications were required to be filed before expiry along with the prescribed renewal fee. | The entire regulation is substituted. Existing Corporate Agents will now apply for a fresh certificate of registration before expiry of their current certificate and pay the applicable annual fee. Once granted, the fresh certificate will operate under the perpetual registration regime.It means that all the existing corporate agents have to compulsorily apply for fresh registration to get covered under the new perpetual regime.

VKCo comment: Given that existing corporate agents are validly registered, there may not be a need for a provision requiring fresh registration. A simple transitional provision requiring payment of annual fee once the renewal period is over, would have sufficed. |

| Regulation 12 – Registration not granted | The regulation contained references to refusal of registration as well as refusal of renewal of registration. | References to “renewal” and “renew” are omitted |

| Regulation 13 – Effect of Refusal | The regulation referred to refusal of registration as well as refusal of renewal of registration. | The words “of a renewal thereof” are omitted. |

| Regulation 4(3) Application fee | Rs. 10000 at the time of application and Rs. 25000 upon communication of grant of registration by the authorityand Rs. 25000 for renewal of Registration. | Rs. 10000 at the time of applicationand further payment of annual fee on a yearly basis as per Schedule VI. |

2. Simplification of Regulatory Processes and Reduction of Compliance Burden

| Regulation 7(3)(c),(d), (e) Formalities relating to specified persons of corporate agents | Every Specified Person engaged by a Corporate Agent was required to obtain an IRDAI-issued certificate, valid for 3 years, before soliciting and procuring insurance business. The regulations also prescribed the process for issuance, transfer (switching between Corporate Agents) and migration of such certificates. | Clauses (c), (d) and (e) are proposed to be omitted.

These requirements are proposed to be omitted. |

| Regulation 22(5) – Certificate Number Requirement | Corporate Agents shall disclose details of Specified Persons along with their IRDAI-issued certificate numbers while reporting office and personnel details to the Authority. | The words “along with their certificate number issued by the Authority” are omitted.

The amendment removes the requirement to furnish the certificate numbers of Specified Persons to IRDAI, thereby simplifying reporting obligations and reducing procedural compliance |

3. Strengthening accountability and oversight of Specified Personnel, Point of Sales Personnel and Authorised Verifier

| Regulation 14(v) – Number of Specified Persons[2] | The Corporate Agent was required to solicit and procure a reasonable number of insurance policies commensurate with its resources and the number of Specified Persons employed by it. The requirement was assessed at the entity level | Each branch office must employ Specified Persons commensurate with the volume of business handled by that branch, including members enrolled under group policies. Further, every branch must have at least one Specified Person. |

| Regulation 14(vi) – Policy-wise Tagging of Sales Personnel | The existing Regulation requires the Corporate Agent to maintain records in the format specified by IRDAI containing policy-wise and specified person-wise details, wherein every policy solicited by the Corporate Agent is tagged to the concerned Specified Person. The Corporate Agent is also required to provide access to such records to IRDAI. | Changes:● Expansion of coverage from only specified person to specified person or POSPs[3].

● Mandatory capture of Aadhar/Pan details of the salesperson. ● Record the salesperson details in the policy document ● Traceability of the individual responsible for the sale |

| Regulation 14(x) – Periodic Training Requirement (INSERTION) | Specified Persons were required to undergo prescribed training before being permitted to solicit insurance business. However, there was no mandatory recurring training requirement after registration. | The Principal Officer and Specified Persons must complete at least 25 hours of theoretical and practical training from an approved institution every three years. |

| Regulation 14(xi) – Power to Impose Business Restrictions(INSERTION) | The regulations did not expressly empower IRDAI to impose business-specific conditions, restrictions or limits after grant of registration. | IRDAI may, in the interest of policyholders and orderly growth of insurance business, impose conditions, restrictions or limits on the business of a Corporate Agent either at the time of registration or subsequently. |

| Regulation 19(1) – Professional Indemnity Insurance | A newly registered Corporate Agent could be granted up to 12 months from the date of registration to obtain and submit the professional indemnity insurance[4] policy. | Every Corporate Agent shall have the professional indemnity insurance policy from its inception. |

| Regulation 25(4) – Qualification of Authorised Verifiers (INSERTION) | The regulations prescribed requirements relating to Authorised Verifiers but did not specifically provide a separate provision requiring a pre-recruitment test and practical training in the manner now proposed | A new sub-regulation is inserted requiring Authorised Verifiers to:● Pass a pre-recruitment examination conducted by an examination body nominated by IRDAI; and

● Complete practical training from an IRDAI-approved training institution |

4. Enhanced disclosure and transparency requirements

| Regulation 17 – Nomenclature of Corporate Agents and Associations | The regulations did not mandate the use of the words “Insurance” or “Assurance” in the name of Corporate Agents or their association. | Where the principal business of the entity is insurance intermediation as a Corporate Agent, the name must contain the word “Insurance” or “Assurance”. Similar requirements are introduced for associations of Corporate Agents. |

| Regulation 26(2) – Threshold for Enhanced Reporting | The corporate agent shall be responsible for all the acts and omissions of its principal officer, specified persons and other employees including violation of code of conduct specified under these regulations and liable to a penalty which may extend to one crore rupees under the provisions of Sec. 102 or the Ac | The threshold is increased from ₹1 crore to ₹10 crore. |

| Regulation 31(2) – Disclosure of Insurance Intermediation Revenue | Corporate Agents whose principal business was other than insurance intermediation were required to maintain segment-wise reporting capturing revenues from insurance intermediation and other income received from insurers. | Corporate Agents are now required to disclose revenues from insurance intermediation and other income/receipts from insurers through a separate schedule forming part of their financial statements and submit audited financial statements along with the auditor’s report to IRDAI by 30 September every year. |

| Regulation 31(4) – Disclosure by Large Corporate Agents (INSERTION) | The regulations did not specifically require Corporate Agents to disclose commission earned, related party transactions, profits or dividend repatriation based on a commission threshold. | A Corporate Agent earning more than ₹10 crore commission in a financial year must annually disclose:● Commission earned;

● Related Party Transactions (RPTs); ● Profits; and ● Dividend repatriated. These disclosures must be submitted to IRDAI and also published on the Corporate Agent’s website. VKCo comment: No particular format of the aforesaid disclosures has been provided. |

| Schedule AA – Undertaking for Foreign-Owned Corporate Agents | Required the insurance intermediary to:● Obtain prior IRDAI approval for dividend repatriation;

● Restrict payments to related parties to 10% of total expenses; ● Maintain specified Indian-residency requirements for leadership, directors and KMPs; and ● Bring in technological and managerial expertise. |

Requires the insurance intermediary to:● Submit quarterly details of related party transactions (RPTs) and annual audited financial statements to IRDAI;

● Place such disclosures on its website; and ● Ensure all RPTs are supported by proper agreements, approvals and documentation and comply with applicable laws |

5. Introduction of a proportionate annual fee and regulatory supervision framework

| Regulation 4(3) Application fee | Rs. 10000 at the time of application and Rs. 25000 upon communication of grant of registration by the authorityand Rs. 25000 for renewal of Registration. | Rs. 10000 at the time of application and further payment of annual fee as specified within 15 days of the of communication of grant of registration |

| Schedule V Clause III – Suspension or Cancellation without Notice (INSERTION) | The regulations permitted suspension or cancellation of registration in specified circumstances such as fraud, misconduct or other regulatory violations. However, there was no specific provision for suspension solely on account of non-payment of annual fees because the framework was based on registration and renewal. | A new provision is inserted under which registration shall be suspended without notice if the Corporate Agent fails to pay the annual fee within the prescribed timeline. The Corporate Agent may seek revocation of suspension by paying the annual fee together with an additional penalty of 10% within three months from the date of suspension. |

| Schedule VI – Introduction of Annual Fee Framework(INSERTION) | Corporate Agents were required to pay registration fees and renewal fees at prescribed intervals under the existing three-year registration framework. | A completely new annual fee regime is introduced. Every Corporate Agent must pay an annual fee equal to the higher of:● ₹10,000; or

● 1/25th of 1% (0.04%) of commission and other receipts received from insurers during the preceding financial year. Late payment attracts penalties and continued non-payment may result in suspension or cancellation of registration. |

[1] https://vinodkothari.com/2025/12/major-amendments-in-insurance-act-2025/

[2] Specified Person means an employee of a Corporate Agent who is responsible for soliciting and procuring insurance business on behalf of a corporate agent and shall have fulfilled the requirements of qualification, training and passing of examination as specified in these regulations. A Specified Person is the employee or representative of a Corporate Agent who actually sells insurance policies to customers

[3] Point of Sales Person (POSP) means an individual who has the prescribed qualifications, has completed the required training and examination, and is authorized to solicit and market only those insurance products specified by IRDAI. As defined in reg 14(vi)

[4] Professional Indemnity Insurance (PII) is an insurance policy that protects an intermediary against financial losses arising from errors, omissions, negligence, misrepresentation or professional mistakes committed while rendering professional services.

RBI’s Draft Model Risk Management Guidelines, 2026; What NBFCs using AI/ML Need to Know

RBI has published a draft “Guidance on Regulatory Principles for Model Risk Management, 2026” for public consultation and it’s the first time AI/ML models used in credit underwriting, customer interaction and other business processes get a dedicated regulatory lens, applicable across the full spectrum of REs, including NBFC-BL, ML, UL and TL.

Here’s what stood out for NBFCs deploying AI/ML:

𝟏. 𝐈𝐭’𝐬 𝐧𝐨𝐭 𝐣𝐮𝐬𝐭 𝐚𝐛𝐨𝐮𝐭 “𝐀𝐈” — 𝐬𝐜𝐨𝐩𝐞 𝐢𝐬 𝐰𝐢𝐝𝐞 A “model” now covers any system — including spreadsheet-based tools — that takes inputs, applies processing logic, and produces outputs materially affecting decisions, irrespective of whether the RE itself labels it a “model.” A loan pricing calculator that drives lending rates qualifies. Many NBFCs may discover they’re running more “models” than they thought.

𝟐. 𝐀𝐜𝐜𝐨𝐮𝐧𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐬𝐭𝐚𝐲𝐬 𝐰𝐢𝐭𝐡 𝐭𝐡𝐞 𝐍𝐁𝐅𝐂 — 𝐞𝐯𝐞𝐧 𝐟𝐨𝐫 𝐭𝐡𝐢𝐫𝐝-𝐩𝐚𝐫𝐭𝐲/𝐯𝐞𝐧𝐝𝐨𝐫 𝐀𝐈 Many NBFCs lean on fintech/vendor-provided AI for underwriting or collections scoring. The draft makes clear: outsourcing the model doesn’t outsource the risk. Independent validation by the RE is mandatory regardless of any certification the vendor provides, plus enhanced RMCB oversight irrespective of risk tier, and contractual rights to technical documentation and audit access.

𝟑. 𝐄𝐱𝐩𝐥𝐚𝐢𝐧𝐚𝐛𝐢𝐥𝐢𝐭𝐲 𝐟𝐨𝐫 𝐦𝐚𝐭𝐞𝐫𝐢𝐚𝐥 𝐝𝐞𝐜𝐢𝐬𝐢𝐨𝐧𝐬 Credit underwriting models fall squarely in “material decision-making” territory — meaning higher explainability thresholds apply. If a model (e.g., a black-box ML scorecard) can’t fully explain itself, NBFCs must compensate with enhanced validation, output verification, frequent monitoring and usage restrictions.

𝟒. 𝐁𝐢𝐚𝐬 𝐚𝐧𝐝 𝐟𝐚𝐢𝐫𝐧𝐞𝐬𝐬 𝐭𝐞𝐬𝐭𝐢𝐧𝐠 𝐛𝐞𝐜𝐨𝐦𝐞𝐬 𝐞𝐱𝐩𝐥𝐢𝐜𝐢𝐭 NBFCs must proactively identify risks of discriminatory outputs — especially unfair treatment of customer groups in credit decisions — run fairness assessments, and recalibrate or redesign where needed.

𝟓. 𝐂𝐡𝐚𝐭𝐛𝐨𝐭𝐬, 𝐯𝐨𝐢𝐜𝐞 𝐛𝐨𝐭𝐬 & 𝐠𝐞𝐧𝐀𝐈 𝐜𝐮𝐬𝐭𝐨𝐦𝐞𝐫 𝐢𝐧𝐭𝐞𝐫𝐟𝐚𝐜𝐞𝐬 𝐠𝐞𝐭 𝐬𝐩𝐞𝐜𝐢𝐟𝐢𝐜 𝐠𝐮𝐚𝐫𝐝𝐫𝐚𝐢𝐥𝐬 For any AI model interfacing with customers, NBFCs must:

- Disclose to customers that they’re interacting with an AI/ML system, with its limitations;

- Provide an option to switch to a human when requested;

- Guard against hallucinations via system-level controls (critical for generative AI);

- Build in protections against prompt injection, adversarial inputs and anomalous usage;

- Run structured “red-teaming” / challenge testing on such models

𝟔. 𝐇𝐮𝐦𝐚𝐧 𝐨𝐯𝐞𝐫𝐬𝐢𝐠𝐡𝐭 𝐢𝐬 𝐧𝐨𝐧-𝐧𝐞𝐠𝐨𝐭𝐢𝐚𝐛𝐥𝐞 Human-in-the-loop/on-the-loop arrangements, kill-switch/override mechanisms, and periodic human review of AI-driven decisions are mandated — with explicit attention to “automation bias” and decision fatigue among reviewing staff.

𝟕. 𝐆𝐨𝐯𝐞𝐫𝐧𝐚𝐧𝐜𝐞 𝐧𝐞𝐞𝐝𝐬 𝐭𝐨 𝐠𝐨 𝐭𝐨 𝐁𝐨𝐚𝐫𝐝 𝐥𝐞𝐯𝐞𝐥 A Board-approved Model Risk Management Framework covering AI/ML models is mandatory, with high-risk models requiring Risk Management Committee of the Board (RMCB) approval, risk-based tiering, a living model inventory, and decommissioned models retained for 10+ years.

𝐓𝐡𝐞 𝐭𝐚𝐤𝐞𝐚𝐰𝐚𝐲 𝐟𝐨𝐫 𝐍𝐁𝐅𝐂𝐬: this is currently in draft/consultation stage and will eventually replace Chapter 3 (Credit Risk Models) of RBI’s 2002 Guidance Note on Credit Risk Management. NBFCs using AI/ML for credit underwriting, collections, or customer-facing chat/voice interfaces should start mapping their existing models against this framework now — inventory, validation independence, explainability thresholds, and human oversight will likely demand real governance uplift, not just policy paperwork.

FAQs on Advertising, Marketing and Sale of Financial Products and Services, agency and referral activities: Commercial Banks

– Team Finserv | finserv@vinodkothari.com

In order to regulate mis-selling concerns for both products/ services of regulated entities and third-parties by a regulated entity, amendments have been issued ‘Advertising, Marketing and Sale of Financial Products and Services by Regulated Entities’, via two sets of amendment directions for Commercial Banks:

- Reserve Bank of India (Commercial Banks – Responsible Business Conduct) Second Amendment Directions, 2026 (‘RBC Amendment Directions’)

- Reserve Bank of India (Commercial Banks – Undertaking of Financial Services) Third Amendment Directions, 2026 (‘UFS Amendment Directions’)

See our other resources on the subject:

- Detailed write up on the Amendment Directions here.

- Youtube video here.

- FAQs on Advertising, Marketing and Sale of Financial Products and Services, and agency activities: NBFCs here.

- The Brochure for a half day workshop on June 26, 2025 (Physical-Bengaluru) where we will be discussing the Amendment Directions in detail can be accessed through here.

Policy Updates from SEBI: June Meeting Highlights

– Abhishek Namdev, Assistant Manager and Srihari G.S., Executive | corplaw@vinodkothari.com