Chains of control: Change of control approval keeps NBFCs perplexed, often non-compliant

– Vinod Kothari (vinod@vinodkothari.com)

Paragraph 42 of the Master Direction – Reserve Bank of India Non-Banking Financial Company – Scale Based Regulation) Directions, 2023 (‘SBR Directions’), mandates obtaining prior approval from the RBI for any change in shareholding of 26% or more or any change in management amounting to 30% or more. Before we get into details of the requirement, it is important to start with two observations.

First, this regulation, requiring RBI’s approval for change of control, shareholding or management, applies to all NBFCs, large or small. Given the expanse of the definition, exacerbated by the lack of clarity, this regulation is a constant pain for most NBFCs, particularly the smaller ones.

The second point – the regulation is worded quite vaguely. As the discussion below will reveal, what is change in shareholding of 26% does not come clearly from the language at all. When the language is unclear, the subjects are exposed to erring on the safer side of the law, and end up doing superfluous compliances.

Language may not be clear, but the intent or object of the regulations is clear; one would wish the interpretation of the provision does justice to the intent.

NBFCs must seek the prior permission/ approval from the RBI before strategic changes such as takeovers, acquisition of major shareholding, or significant management changes from the viewpoint of entry of new persons on board. What is the intent of seeking this approval: the RBI granted registration to an NBFC after examination of its control, shareholding and management. The RBI had to satisfy itself that the persons behind the NBFC are “fit and proper”. In a manner of speaking, the RBI is handing the keys of an access to the financial system – therefore, it wanted to be fully sure of who the person taking the keys are.

It is a person acquiring control, coming into management, or building up a significant shareholding, who needs to be tested from the viewpoint of “fit and proper”. There is no question of the person, who is admittedly already in control, from earning that qualification. Also, there is no question of the person walking out of control or transferring out significant shareholding to need approval.

Regulatory carve outs

There are two exceptions, viz., if shares are bought back with court (now NCLT) approval, or, in case of change of management, if directors are re-elected on retirement by rotation. But even with exceptions, NBFCs still need to inform the regulator about any changes in their directors or management.

Note that the carve-out in case of buybacks is only for such buybacks as are coming for NCLT approval, which would mean reduction of capital u/s 66 of Companies Act 2013. As regards buybacks done with board or shareholders’ approval, in view of the limit of 10%/25% of the equity shares, usually a single buyback should not cause a change of control, but it may so happen that one significant shareholder stays back, and other takes a buyback and exits, causing the former’s shareholding to gain majority or significant shareholding (as discussed below). In such a case, exceptions from RBI approval will not be available.

And the other carve-out of reappointment of directors is not a change in management at all. If, at a general meeting, the existing director(s) is rotated out, and a new director comes in place, there is surely no exception in that case.

Three situations requiring approval

There are three situations requiring approval of the RBI; all of these have to be seen in light of the purpose of getting the supervisor’s sign off by way of a “fit and proper” person check. The three situations are:

- Takeover or acquisition of control

This is required to be read in light of the definition of “control” in SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (‘SAST regulations’) [by virtue of reg 5.1.5]. There is an inclusive definition of “control” in SAST Regulations, which is far from giving any bright-line test of when control is said to have been acquired[1]. There is no definition of “takeover” in the SAST Regulations, even though the title of the Regulations is “substantial acquisition of shares” and “takeovers”. A view might be that “substantial acquisition of shares” is a case of takeover. In that case too, there are two different situations covered by SAST Regulations – first time acquisition of 25% or more of the equity shares [Reg 3 (1), or a creeping acquisition of 5% or more in a financial year, by a person already holding 25% or more [Reg 3 (2)].

Acquisition of control is covered separately by Reg 4. The question, in the context of NBFCs is, whether “takeovers” and “change of control” are to be read as two separate situations, and if yes, what will be the meaning of “takeover”? Can it be said that every “substantial acquisition of shares” is a takeover, and if so, whether only the first-time acquisition or the creeping acquisition as well? First of all, there is no reason to include creeping acquisition here, as the relevance of the same is limited to equity listed companies. In fact, the way creeping acquisition is defined in SAST Regulations, there may actually be no change in shareholding at all, and still an acquirer may have hit the creeping acquisition limit.

Acquisition of “control”, though subjective, has been interpreted in several leading SC and SAT rulings. The definition of “control” in sec. 2 (27) of the Act and Reg. 2 (1) (e) of SAST Regulations is an inclusive one: it does not define control, but extends the meaning of the term to include management control or the right to appoint majority directors. The more common mode of control is voting control. The expression “control” has been subject matter of several leading rulings such as Arcelormittal India Private V. Satish Kumar Gupta, in which the Supreme Court defined the expression “control” in 2 parts; de jure control or the right to appoint a majority of the directors of a company; and de facto control or the power of a person or persons acting in concert, directly or indirectly, in any manner, can positively influence management or policy decisions. In Shubhkam Ventures V. SEBI, the meaning of control was extensively discussed by the SAT, it was held that the test is to see who is in the driving seat, the question would be whether he controls the steering, the gears and the brakes. If the answer to this question is affirmative, then alone would he be in control of the company. In other words, the question to be asked in each case would be whether he is the driving force behind the company and whether he is the one providing motion to the organization. If yes, he is in control but not otherwise.

Note that control may be direct or indirect. Indirect control typically arises when the controlling person controls an intermediate entity or entities, which in turn have a control over the target entity.

- Any change in shareholding resulting in acquisition/transfer of 26% shareholding

This clause may have a lot of interpretational difficulties. First question – is 26% the magnitude of change in shareholding, or is the threshold which cannot be crossed? For example, if a shareholder was holding 25% shares in the NBFC, and now proposes to acquire another 1%, is this subject to regulatory approval? The answer should be clearly yes, because the shareholder will now be having what is regarded by the regulation as significant shareholding. On the contrary, if the person is already holding 26%, he is a significant shareholder already, either by virtue of having such shareholding at the time of formation of the NBFC, or based on the acquisition approved by the RBI. So, what will be the next level that will require regulatory approval? Logically, it seems that the person has already been approved to come as a significant shareholder, and therefore, an increase in shareholding should not require any intervention. In other words, the regulatory approval is required for the first time acquisition and not for the creeping acquisition. It may, however, be argued that if the creeping acquisition makes the equity holding cross 50%, then it amounts to acquisition of control, and that falls under the first clause.

In short, regulatory approval is required for first time acquisition of 26% equity stake or higher, or 50% or higher.

There are many other points that arise in connection with the change in shareholding.

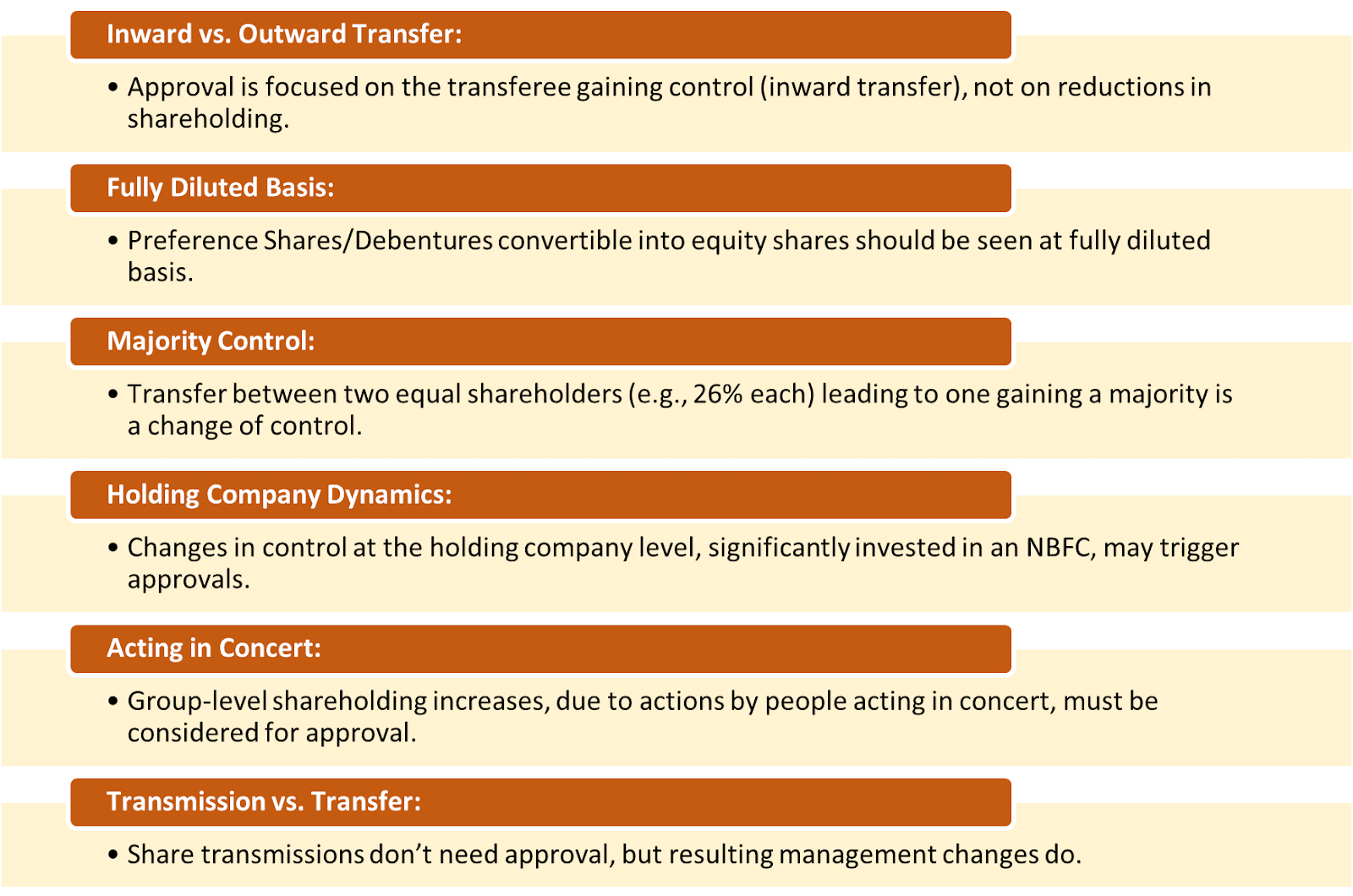

First, is the transfer in shareholding here inward transfer, or can it mean outward transfer as well? Every transfer has a transferor and a transferee, but it is logical to assume the context of the regulation requires the supervisor to approve the transferee. It is the transferee who is coming in control. This is also evident from the word of the proviso to reg 42.1.1 (ii), which is obviously an exception to the main clause, and uses the words “prior approval would not be required in case of any shareholding going beyond 26 percent”. It implies that the concern of the regulator can only be for shareholding going beyond 26% and not reduction of the level of shareholding. The same intent also becomes evident from use of the word “progressive increases over time”. Note that there is inclusivity in the regulation – evident from words like “including”. Further, someone may extract a meaning from the language “transfer” – saying even a transfer out is also a transfer. This is precisely the point we made earlier – that this provision, worded loosely and applied universally, gives a lot of scope for an ambitious regulator to ask for approvals where approvals may not have any relevance.

Secondly, the expression is transfer of “shareholding” – should it include preference shares and convertible debt instruments as well? On the face of it, a preference shareholder or debenture holder does not have control over the entity. If the shares or debentures are either compulsorily or optionally convertible, then the threshold of 26% should be computed by taking the post-dilution equity base. Also, sometimes, preference shares may come with terms which give the preference holders some degree of control. For example, several decisions may be made subject to preference holders’ okay. Or the preference shares may be participating preference shares. In these cases, excluding preference shares altogether may not be proper.

Third, if there are two shareholders, both holding 26% each, and now, one transfers the holding to the other, this may be a case of change of control, as the acquirer now will have 52% holding.

Fourth, when it comes to acquisition of control or significant shareholding, one must take a substantive view, and should not be hamstrung by literal interpretation. For example, if entity A is the NBFC, and entity B is the holding company whose business or assets, almost entirely, constitutes the holding of shares in the NBFC, then, one should apply the change of control at the holding company level as well. Note that even as per SAST Regulations, if a holding vehicle is, to the extent of 80% or above, invested in the target company, acquisition of stake in the holding vehicle will be taken as direct acquisition of stake in the target entity.

Fifth, if some shareholders are acting in concert, or are deemed to be acting in concert, the increase in shareholding should be seen at a group level. Whether certain persons are acting in concert is left to facts or the surrounding situations.

Sixth, transfers of shares may require approval, but if the vesting of shares happens due to a transmission, there is no question of approval for the acquisition. However, if this leads to a change in management, the same shall require approval.

Change in Control:

- Change in management

This clause is admittedly the most vague clause, and may result into situations which have no correlation with a change in control, yet coming for regulatory approval. The actual language says: “Any change in the management …which would result in change in more than 30 percent of the directors”. This should really mean a change in management or directorships, which is connected with or arising out of a change of control. If control changes or shifts, usually management also shifts. However, there may be a change in board positions irrespective of any change in control or real change of management at all. Appointment and removal of independent directors are not considered for this purpose. However, nominee directors have not been excluded. Therefore, any appointment or removal of nominee directors will require prior approval if such appointment breaches the limit of 30%.

In reality, the language rules the meaning, and the interpretation is that if there is a change in directorships to the extent of 30% or more, excluding independent directors, the same will require a change of control process, even though there is not even a slightest change in control.

Here again, one may use literal interpretation and argue that “change in directorships” may include directors going out, or coming in. However, in the context, there can never be an intent to control the exit of directors. Exit may happen purely for involuntary or personal reasons – death, resignation, incapacity, etc. The supervisor is to be concerned with the directors who come in, who have to earn the label of being “fit and proper”.

In case of entities with smaller boards, say having 2 or 3 board members, change of even one director may cause change of 30% or more, though there is no real change of management or management control.

Another point to discuss here is, like in case of shareholding, does the change in directorships include progressive changes too? For example, if a company’s board consists of 6 directors, and one is rotated out or replaced in year 1, and the other one, say, after a year or two, without any concerted action, have we reached a change in directorships of 30% or more? In case of shareholding, progressive increases are specifically included; not so in case of change of directorships.

In the author’s view, the provisions of Reg 42 cannot be stretched to imply that every appointment of a director in an NBFC requires RBI’s approval – if such was the intent, the intent could have been spelt out. Neither is there a reason for such micro regulation, since the focus has to be on change of control. However, as a practical expedient, NBFCs are encouraged to intimate the periodic changes in board positions to the RBI by way of an intimation. Therefore, the regulator has an intimation of the changes that take place over time. If the changes in board positions are part of the same intent or design, and are merely phased over time, the same will usually also be associated with a change in shareholding. In any case, if even independent of a shareholding change, if the changes in management happening over time are mutually connected and a part of the attempt to gain management of the NBFC, the same will require regulatory approval. Given the subjectivity involved, NBFCs may want to play safe and place the facts before the RBI for its guidance.

Intra-group transfers

The meaning of “intra- group” transfers is the shareholding which is spread across members of a group. A group should mean here entities either have common control, or common significant influence, or those where persons have been disclosed as acting in concert for holding shares in the NBFC. The following is a question from the RBI’s FAQs relating to intra-group transfers. It is difficult to get the meaning of the response. Once again, the 26% is not the total magnitude of change, but crossing the threshold. Therefore, in the answer below, 26% cannot be read as the total shifting of shares within the group. The group is already above 26%, and now, there is movement of shares within the group. Is the regulator trying to say once the group is holding 26%, any realignment of shares within the group will require approval? Also, in most cases, the shifting of intra-group shareholding does not happen within a closed group. For example, if there are 4 entities of a group holding shares, one of the members of the group may transfer shares to a 5th entity. The lack of any basis for the response is evident from the approach – apply to us by way of a letter, and then we will let you know whether approval is needed or not. It is sad that a regulator/supervisor sits to decide whether the matter comes within the regulatory ambit.

Here is an excerpt from the RBI FAQs:

26. Whether acquisition/ transfer of shareholding of 26 per cent or more of the paid up equity capital of an NBFC within the same group i.e. intra group transfers require prior approval of the Bank?

Yes, prior approval would be required in all cases of acquisition/ transfer of shareholding of 26 per cent or more of the paid up equity capital of an NBFC. In case of intra-group transfers, NBFCs shall submit an application, on the company letter head, for obtaining prior approval of the Bank. Based on the application of the NBFC, it would be decided, on a case to case basis, whether the NBFC requires to submit the documents as prescribed at para 3 of DNBR (PD) CC.No. 065/03.10.001/2015-16 dated July 9, 2015 for processing the application of the company. In cases where approval is granted without the documents, the NBFC would be required to submit the same after the process of transfer is complete.

Corporate Restructuring

Corporate restructuring in the NBFC sector involves reorganizing the company’s structure, operations, or finances to improve efficiency, address financial distress, or comply with regulatory requirements. This process can include mergers, demergers, amalgamations, and such other changes in corporate structure.

Given that corporate restructuring is a strategic decision for the structure and existence of the NBFC, it becomes important to evaluate the need for regulatory approvals in this regard. The intent of the regulator, as discussed above, is to require the prior approval in case of substantial acquisitions and change in shareholding beyond the threshold of 26%, with the intent to acquire ‘control’. Hence, in case the corporate restructuring leads to such a change in control or shareholding, with or without the change in management, the same must be done with the consent of the RBI.

For instance, if ABC Ltd. is the holding company of an NBFC and the NBFC intends to merge with the holding company. There is no change in control as such pursuant to such merger. However, as per RBI FAQ No. 84, this shall require the prior approval from RBI.

Another instance could be that ABC Ltd (being non-NBFC) intends to merge with an NBFC. As per RBI FAQ No. 85, where a non-NBFC mergers with an NBFC, prior written approval of the RBI would be required if such a merger satisfies any one or both the conditions viz.,

- any change in the shareholding of the NBFC consequent on the merger which would result in a change in shareholding pattern of 26 per cent or more of the paid-up equity capital of the NBFC.

- any change in the management of the NBFC which would result in change in more than 30 per cent of the directors, excluding independent directors.

Even if an NBFC intends to amalgamate with another NBFC, as per FAQ No. 86, the NBFC being amalgamated will require prior written approval of the RBI.

It may be noted that the prior written approval of the RBI must be obtained before approaching any Court or Tribunal for seeking orders for merger/ amalgamation in all such cases which would ordinarily fall under the scenarios discussed above.

[1] Read our detailed analysis on the topic here- https://vinodkothari.com/2017/09/sebi-aborts-brightening-of-fine-lines-of-control/ (last accessed in November, 2024)

[2] Refer to our article on- https://indiacorplaw.in/2016/03/choosing-between-blurred-line-and.html

[3] Read Our FAQs on Change in Management and Control : https://vinodkothari.com/2016/06/faqs-on-change-in-control-or-management-of-an-nbfc/

Leave a Reply

Want to join the discussion?Feel free to contribute!