A shocker for the bond markets: Withholding tax to apply on listed bonds, without grandfathering

Team Financial Services | finserv@vinodkothari.com

Section 193 of the Income Tax Act[1] provides for TDS payment in case of interest on securities. Currently listed debentures are exempt from TDS without any limit. The exemption comes way of clause (ix) of the proviso to sec. 193.

The said clause is now sought to be deleted. The deletion, if affirmed by the statute, will be effective from 1st April, 2023, thereby meaning that any interest paid by companies on listed bonds will now be subject to tax.

The amendment has a retroactive effect, as it applies even to bonds that may have already been issued. If the issuer and the investor have both entered into a securities transaction on the strength of the law then existing, and the bondholder suddenly comes under the purview of deduction of tax at source, this will be like acquiring a security with no safe harbor. It is notable that certainty of tax treatment for capital market transactions is an essential mainstay for the healthy growth of capital markets.

A frail retail market:

Source: SEBI data

The table below shows the issuances of corporate bonds through private placements and public issuance.

| Year | Public Issuance (Rs. in Cr.) | Private Placements (Rs. in Cr.) |

| 2015-16 | 33,811.92 | 458073.48 |

| 2016-17 | 29547.15 | 640715.51 |

| 2017-18 | 5172.56 | 599147.08 |

| 2018-19 | 36679.4 | 610317.61 |

| 2019-2020 | 15068.37 | 674702.88 |

| 2020-2021 | 10588.02 | 771839.98 |

| 2021-2022 | 11589.41 | 588036.94 |

| 2022-2023* | 6863.18 | 522089.99 |

Source: SEBI data

As evident from the above figures, the market for bond issuance in India is mostly a private placement market, where the investors are mostly institutional investors. Retail participation mostly happens in case of public issues of bonds, or maybe through secondary market activity in the debt segment of the stock exchanges.

For example, in FY22, the total private placement of bonds added to Rs 588037 crores, whereas 28 public offering issued only Rs 11589 crores. It is highly unlikely that retail investors would have participated in private placements, mostly done for qualified institutional investors.

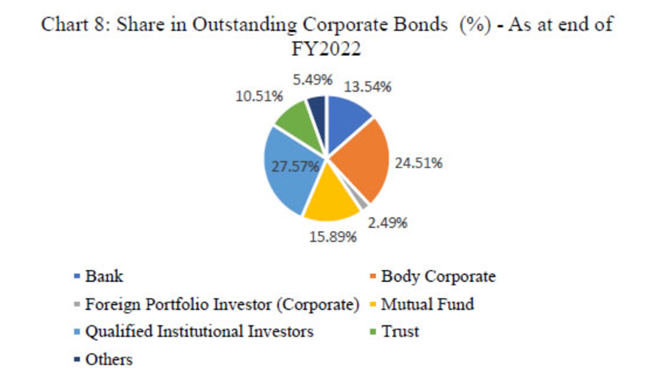

As per RBI in ‘Corporate Bond Markets in India – Challenges and prospects’[2], the investor base for corporate bonds is largely dominated by domestic institutions – insurance companies, banks and mutual funds. Retail participation in corporate bonds remains low as also depicted in the chart below:

Having a retail participation is a sign of maturity of the market, as it cushions the markets from volatility, runs, contagion effects etc. The risk of financial sector connectivity, which is the breeding ground for contagion, is much more in case of institutional buyers.

In any case, it should be clearly a part of the active government policy-making to encourage retail investors to invest in fixed income instruments. This is why investments in REITs were opened up to retail investors.

In light of this objective, it is disheartening to note that the withdrawal of the exemption is proposed in the Budget. If retail investors have to suffer withholding tax, subsequently to claim the same as set-offs, etc., they are forced to go through the complicated process tax filings.

Concerns difficult to understand:

As a matter of principle, withholding tax may be convenient but not the ideal way to collect taxes. Withholding taxes pass the burden of tax collection to the person responsible for paying the income in question. A fair tax assessment, and collection of tax based on what it the tax liability of the taxpayer, is the job of the fiscal authorities, and cannot be passed on to the persons responsible for making payments.

India has, however, continued to rely on withholding taxes.

The key idea in tax at source rather tax at the taxpayer can be a potential for tax evasion.

However, in case of listed bonds, that apprehension becomes baseless. If it is a subscription to a listed security or holding thereof, the investor has demat account, bank account, etc. The trail of the information including the income earned on the investment is easily available. In absence of a chance of tax evasion, it is not proper for the government to have moved for source-based tax.

However, this provision will further deter public participation in bond issuances by companies.

No grandfathering

The worst part of the change is that there is no grandfathering; therefore, withholding tax will start applying from the 1st of April, 2023. In other words, issuance already done before the effective date will also be affected by the new provision.

[1] https://incometaxindia.gov.in/pages/acts/income-tax-act.aspx

[2] https://rbidocs.rbi.org.in/rdocs/Speeches/PDFs/DGTRSCORPORATEBOND9F5A9CEECBDF49ACBACD1872A4C62A3D.PDF

Leave a Reply

Want to join the discussion?Feel free to contribute!