Securitisation of stressed loans: Opportunities and structures

Comments on RBI’s Discussion Paper on Securitisation of Stressed Assets Framework (SSAF) dated January 25, 2023

Timothy Lopes, Manager | Vinod Kothari Consultants Pvt. Ltd.

Background

At present, in India, there exists a framework for securitisation of standard assets only. in September, 2021 the RBI issued the ‘Master Direction – Reserve Bank of India (Securitisation of Standard Assets) Directions, 2021’ (‘SSA Directions’)[1], which deals with standard asset securitisation. Under the SSA Directions, the definition of standard assets does not include non-performing loans, i.e., only those assets with a delinquency up to 89 days, would qualify for securitisation under the SSA directions.

For assets that turn non-performing, i.e., 89+ days-past-due (‘DPD’), including those that retain the classification as the borrower has not been able to clear all his past arrears, the same can, at present, be sold under the Master Direction – Reserve Bank of India (Transfer of Loan Exposures) Directions, 2021 (‘TLE Directions’)[2], which has a framework for sale of stressed assets (which includes non-performing assets). Technically, there is a process of “securitisation” of non-performing loans (‘NPLs’), by issuing “security receipts” (‘SRs’) against the same; however, the framework for issue and investing in SRs is quite different, and is normally not captured as a part of securitisation in the industry parlance[3].

Assets sold through the TLE route require a complete arm’s length sale, without any credit support from the seller and there is typically no tranching. This results in substantial haircuts on these stressed loan pools. Further, most of the NPLs that face a problem in the current scenario are retail loans or re-performing loans (see discussion on re-performing loans later). These retail pools are not normally sold under the ARC route since ARCs lack the capability in this specific asset class and are more suited towards wholesale transactions.

NPL issue compounded by 12th Nov., 2021 circular:

On 12th November, 2021, RBI issued a circular dealing with ‘Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances – Clarifications’[4], which changed the norms for upgradation of Non-Performing Assets (‘NPAs’) to standard assets. The new norms stated that “loan accounts classified as NPAs may be upgraded as ‘standard’ asset only if entire arrears of interest and principal are paid by the borrower.”

Owing to this change, the norms for upgrading an NPA account to standard has become more stringent. Due to this, NPA numbers have shot up and are likely to shoot up further. With sale of these NPAs under TLE resulting in a substantial hair cut and ARCs lacking capability for retail NPAs, there arises a need for a framework that deals with securitisation of NPAs.

Pursuant to the Statement on Developmental and Regulatory Policies dated September 30, 2022[5], it had been decided to introduce a framework for securitisation of stressed assets, in addition to the ARC route, similar to the framework for securitisation of standard assets.

In light of this, the RBI has issued a Discussion Paper on Securitisation of Stressed Assets Framework (‘SSAF’) dated 25th January, 2023, inviting comments on the same by February 28, 2023, (‘RBI discussion paper’ / ‘discussion paper’)[6].

This article gives a global flavour to securitisation of non-performing loans, also addresses the major questions posed by the discussion paper on SSAF.

Global scenario

According to the European Central Banks Financial Stability Review (November, 2022)[7], Banks’ NPL ratios have dropped in the first half of 2022, driven mainly by securitisations and asset disposals.

The table below shows the decline trend of NPL ratios, which would mean that securitisation and asset sale volumes of NPLs have gone up, since it is the main driver for the declining trend.

Source: ECB Financial Stability Review (November, 2022)

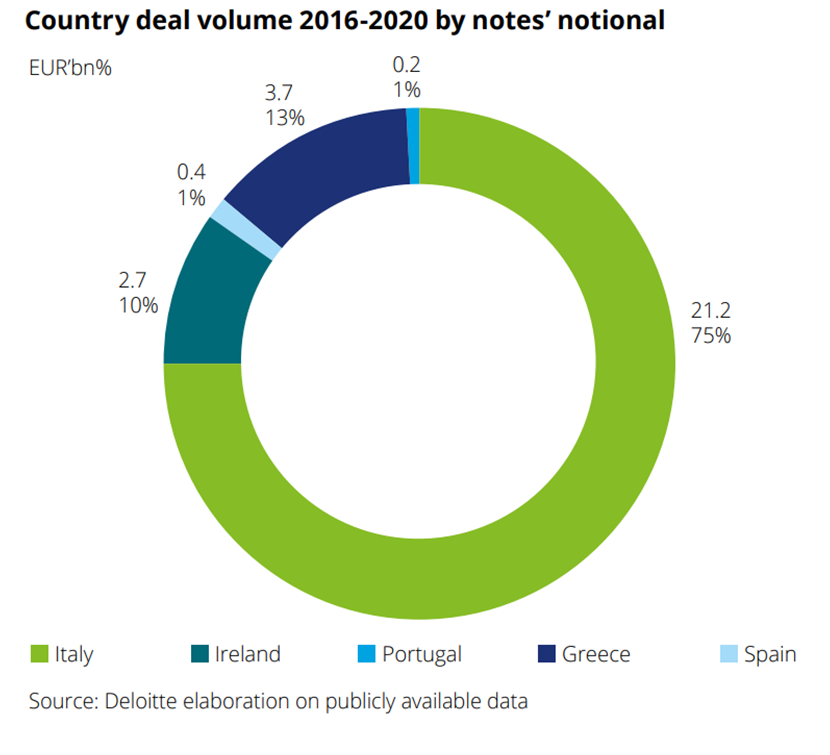

Further, a report by Deloitte on ‘NPL securitisation and related government guarantee schemes in Europe’ (October, 2020) states that “Since 2016, there have been total transactions of EUR 88.8bn by gross book value (GBV) and EUR 28.2bn by notional value, with over 75% of the deals based in Italy, followed by Greece, Ireland, Portugal, and Spain. Around 75% have included an element of government guarantee.”

The data below shows the country-deal volume from 2016-2020.

Types of NPL securitisation globally[8] –

The US market involves mostly agency securitisations, which recognise the concept of ‘Re-performing Loans’, which are securitised into Mortgage Backed Securities (MBS). When loans are securitised, they are placed in an MBS trust guaranteed by the Agency. The guarantee ensures that the Agency will supplement amounts received by the trust to permit timely payment of principal and interest to the MBS investor[9].

Italy introduced the Garanzia Cartolarizzazione Sofferenze (GACS) scheme[10] in 2016, which involves bundling NPLs to be securitised into a special purpose vehicle with tranches of varying seniority. The scheme comes with a government guarantee. The government guarantees only the senior tranches of securitization transactions, after the tranche receives a BBB rating.

In Greece, the “Hercules Asset Protection Scheme” (HAPS) scheme was introduced in 2019 and according to a report by the ECB titled “An empirical study of securitisations of non-performing loans” (May, 2022)[11], the scheme “is largely based on the GACS scheme, albeit with some differences, as requirements tend to be less strict (e.g. no investment grade rating requirement for the senior tranche)”.

Global regulations on securitisation do not prohibit securitisation of standard or substandard assets, leaving it for the originators and investors to take their own view on the extent of non-performing loans in the pool. Hence, there may be pools of all standards assets, all substandard or RPL assets, or mixtures of the two.

However, over the last 2-3 years, most of the global regulators, led by Basel Committee on Banking Supervision[12], have brought specific capital requirements for pools which are overwhelmingly composed of NPLs. In the UK, the Prudential Regulatory Authority issued a policy statement PS 24/21[13], implementing the Basel standards on securitisation of NPLs.

Discussion paper questions and responses

Should SSAF be limited to NPAs?

One of the questions of the RBI discussion paper (reproduced below) relates to whether the SSAF should be limited only to NPAs or should include standard assets too?

“Discussion Question 1: Should Securitisation of Stressed Assets Framework be limited only to NPAs, or should it include standard assets too, up to a certain threshold?”

In our view, it need not be limited to NPAs only. Barring Simple, Transparent and Comparable (STC) securitisation (where NPAs are explicitly excluded), this is best left to the decision of the market forces.

Type of assets eligible under SSAF

Another question relates to the type of assets that should be securitised under the SSAF. This is reproduced below –

Discussion Question 2: Which type of assets should be eligible for Securitisation of Stressed Assets?

Wholesale transactions are normally done through the ARC route. Thus, under the SSAF, only retail transactions should be permitted, since ARCs lack the capability for retail loans. Certain loans come under the category of ‘Re-performing loans’, that is, they are categorised as NPA and have started performing again, but have not returned to standard status, since the borrower has not cleared all his dues.

The regulations do not recognise this concept of re-performing loans. However, most retail loans are of this nature. Though regulatorily these loans are non-performing, in essence, they are performing.

Hence, the regulatory framework may either limit the exposure of a single nonperforming loan to the pool size – say 10% or so, or, since single asset securitisations are permitted in case of standard assets, the choice of retail versus corporate loans may be left to the market. The possibility of regulatory arbitrage and evergreening needs to be adequately provided for.

Should there be MRR requirements?

Discussion Question 3: Whether form and quantum of Minimum Retention Ratio (MRR) is required to be prescribed regulatorily for SSAF?

The SSAF is intended to deal with securitisation of NPAs. In order for assets to turn into NPAs, they would have had to be on the books for a certain period. Assets securitised under the SSAF would have been held for a certain period on the books of the originator.

The idea of Minimum Risk Retention (‘MRR’) is for the originator to have a continuing stake in the pool and avoid a originate-to-sell model, which would result in sub-par originating/underwriting standards. However, in case of NPAs, the originator has already shown a continuing stake in the pool and the intent now is to remove such assets from the book, because they have turned non-performing after having retained a continuing stake.

Accordingly, imposing MRR requirements seems unnecessary for these loans. However, European Regulations[14] have prescribed a 5% MRR, in case of NPLs.

Resolution Manager under SSAF

The discussion paper talks about a “resolution manager” which would be “of paramount importance because of their involvement with resolution/recovery exercise of the underlying exposures and reporting requirements to financial regulators”.

However, in most cases, the originator would continue to act as a servicer and there may be no need to appoint a resolution manager. There is no question that the originator will be completely out of the structure.

Introducing the requirement of a resolution manager as a regulatory imposition, thus, seems unnecessary, keeping in view the fact that the originator would continue to service the transaction in most cases and in case there is a need for such a resolution manager, the market could develop the same. If the parties decide to engage the services of a “specialised servicer”, or resolution manager as the RBI calls it, the parties may choose to have such services. However, the regulations stipulating an independent servicer may not be required.

Accordingly, having a separate “resolution manager” requirement is neither advisable nor necessary. If needed, market forces could develop the same.

Capital Requirement

The discussion paper proposes a capital regime based on External Ratings Based Approach (‘ERBA’), subject to minimum non-refundable purchase price discount (‘NRPPD’) of 50% and Risk Weight (‘RW’) floor of 100%.

As given in the RBI discussion paper, “NRPPD is the difference between the outstanding balance of the exposures in the underlying pool and the aggregate consideration at which securitisation notes on these underlying exposures are sold to third party investors.”

The Basel norms prescribe that where the NRPPD is equal to or higher than 50%, regulated entities may apply a 100% RW to the senior tranche of the NPA securitisation. Accordingly, the RBI has proposed a minimum NRPPD of 50% in order to qualify for the SSAF framework.

However, a lower NRPPD should not be completely ruled out. A lower NRPPD should also be permitted under the SSAF and a higher RW may be prescribed for NPA pools with a NRPPD lower than 50%.

However, in the UK, the PRA decided to keep the NRPPD at 50% itself[15].

Due Diligence requirements

Due diligence is always conducted by the investors itself. As mentioned earlier, the need for a resolution manager is unnecessary and not advisable, so there is no question of due diligence being undertaken by the resolution manager. The framework under the SSA directions for due diligence on part of the investors would suffice.

Should credit enhancement be permitted?

The discussion paper lays down the following questions with respect to credit enhancement –

“Discussion Question 12: Which of the following options may be considered for permitting credit enhancement:

a) Credit Enhancements may be permitted for all tranches; the capital requirement will be based on external credit rating framework for all REs extending Credit Enhancement (CE)

b) Credit Enhancement may only be permitted for senior tranches. In either of the options, originator cannot provide CE

c) Credit Enhancements are not allowed.

Further, regarding reset of credit enhancement, is there any specific aspect which should be considered while following a regime similar to the CE reset regime prescribed for SSA?”

Credit enhancement is an integral part of a structured finance transaction. The intent of credit enhancement is to support the structure and protect the senior tranches in the structure up to a certain extent. Accordingly, credit enhancement should be allowed in NPL securitisation as well.

Conclusion

The discussion paper certainly comes as a welcome move, given the fact that securitisation of NPLs would introduce a new market for these assets, especially retail and re-performing loans.

Considering the fact that NPAs on the books of banks and NBFCs may shoot up after the RBI circular dated November 12, 2021, these guidelines, when implemented, would serve to act as an additional option available to financial institutions when dealing with such non-performing assets.

However, certain critical questions raised by the discussion paper would have to be tackled appropriately by the RBI before implementation of final guidelines, in order for NPL securitisation to be a success in India.

[1] https://rbidocs.rbi.org.in/rdocs/notification/PDFs/85MDSTANDARDASSETSBE149B86CD3A4B368A5D24471DAD2300.PDF

[2] https://rbidocs.rbi.org.in/rdocs/notification/PDFs/86MDLOANEXPOSURESC6B1DFB428C349D885619396317F04DE.PDF

[3] SARFAESI Act – https://legislative.gov.in/sites/default/files/A2002-54.pdf

Master Circular – Asset Reconstruction Companies – https://www.rbi.org.in/scripts/BS_ViewMasterCirculars.aspx?Id=12267&Mode=0

[4] https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=12194&Mode=0

[5] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=54466

[6] https://www.rbi.org.in/Scripts/PublicationsView.aspx?id=21728

[7] https://www.ecb.europa.eu/pub/pdf/fsr/ecb.fsr202211~6383d08c21.en.pdf

[8] More details on NPL securitisation and the global scenario can be viewed in our presentation here – https://vinodkothari.com/2022/04/securitisation-of-non-performing-loans/

[9] See – https://capitalmarkets.fanniemae.com/media/20951/display

[10] https://www.dt.mef.gov.it/it/attivita_istituzionali/interventi_finanziari/gacs/

[11] https://www.ecb.europa.eu/pub/pdf/scpops/ecb.op292~092b778aa8.en.pdf

[12] https://www.bis.org/basel_framework/chapter/CRE/45.htm?inforce=20230101&published=20201126

[13] https://www.bankofengland.co.uk/-/media/boe/files/prudential-regulation/policy-statement/2021/october/ps2421.pdf?la=en&hash=50C443589C01E2CAD2A85CFF12F09C00A433DF8D

[14] See – https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32021R0557&from=EN

[15] Refer to – https://www.bankofengland.co.uk/-/media/boe/files/prudential-regulation/policy-statement/2021/october/ps2421.pdf?la=en&hash=50C443589C01E2CAD2A85CFF12F09C00A433DF8D

Leave a Reply

Want to join the discussion?Feel free to contribute!