SEBI notifies substantial amendments in Listing Regulations

Proposals approved in SEBI BM of March, 2021 made effective

Payal Agarwal | Executive ( corplaw@vinodkothari.com ) May 07, 2021

Introduction

SEBI, the capital market regulator of India, vide a gazette notification dated 06th May, 2021 notified Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Second Amendment) Regulations, 2021 [“the Amendment Regulations”] that were approved in SEBI’s Board Meeting held on March 25, 2021. Most of the amendments were already rolled out earlier as consultation papers in 2020. The amendments become effective from May 06, 2021.

This article discusses the major amendments carried out and the likely impact and actionable for the listed entities.

Brief of the amendments are as follows –

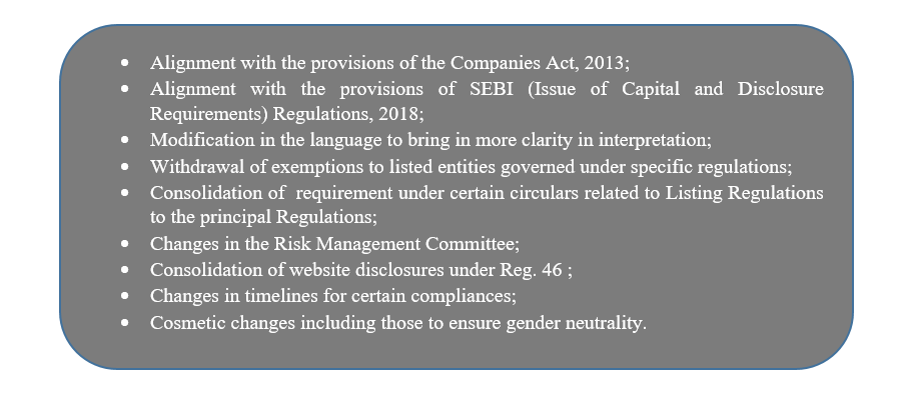

A gist of all the amendments under the Amendment Regulations have been captured in a snippet.

A gist of all the amendments under the Amendment Regulations have been captured in a snippet.

1. Applicability of the Listing Regulations

In terms of Regulation 3 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2013 (‘Listing Regulations’) the provisions of Listing Regulations are applicable to entities that list the designated securities on the stock exchange.

The Amendment Regulations clarify that the applicability of certain provisions of Listing Regulations based on market capitalisation will continue to apply even where the entities fall below the prescribed threshold.

While the market capitalisation may be derived for any day, the recognised stock exchanges viz. BSE Limited and National Stock Exchange of India Limited releases a list of listed entities based on market capitalisation periodically. However, the provisions under Listing Regulations become applicable based on market capitalisation as at the end of the immediate previous financial year.

The present amendment on the continuation of applicability of provisions even after the listed entity ceasing to be among the top 500, 1000, 2000 listed entities, as the case may be, seems inappropriate. The applicability of these provisions were originally introduced in view of the size of the listed entities that held major market cap. Indefinite applicability of the said provisions despite fall in the market capitalisation of the listed entity is more of a compliance burden. The provision should be amended by SEBI in line with the timeframe provided under Reg. 15 i.e. where a listed entity does not fall under the list of top 100, 500, 1000, 2000 for three consecutive financial years, the compliance requirement should cease to apply.

Therefore, a conjoint reading of both the provisions should be allowed to take a liberal interpretation in respect of the newly-inserted Regulation 3(2) as well, thereby relaxation of compliance requirements on completion of a look-back period of 3 consecutive financial years.

2. Risk Management Committee

Regulation 21 of Listing Regulations requires the listed entities to constitute a Risk Management Committee (RMC). A comparative study of the erstwhile and the amended provisions w.r.t RMC is given below –

| Topic | Erstwhile provisions | Amended provisions |

| Applicability of RMC | · On top 500 listed entities (Based on market capitalisation) | · On top 1000 listed entities based on market capitalisation |

| Composition | · Members of Board of Directors

· Senior executives of listed entity · 2/3rds IDs in case of SR Equity Shares |

· Minimum 3 members

· Majority being members of board of directors · Atleast 1 Independent Director (ID) · 2/3rds IDs in case of SR Equity Shares |

| Minimum no. of meetings | One | Two |

| Quorum | Not specified | · 2 or 1/3rds of total members of RMC, whichever is higher

· Including atleast 1 member of Board |

| Maximum gap between two meetings | Not specified | Not more than 180 days gap between two consecutive meetings |

| Roles and responsibilities | The board of directors were to define the role and responsibility and delegate monitoring and reviewing of the risk management plan and such other functions, including cyber security. | As provided under Part D of Schedule II, that inter alia includes:

· Formulating of risk management policy; · Oversee implementation of the same; · Monitor and evaluate risks basis appropriate methodology, processes and systems. · Appointment, removal and terms of remuneration of CRO. |

| Power to seek Information | No such power. The same was only available with Audit Committee under Reg. 18 (2) (c). | RMC has powers to seek information from any employee, obtain outside legal or other professional advice and secure attendance of outsiders with relevant expertise, if it considers necessary. |

The roles and responsibilities of the RMC has now been specified in the Regulations itself, which were once left at the discretion of Board. The formulation of Risk Management Policy has also been delegated to the RMC, with particular contents of the policy being specified under the Schedule.

An important role of the RMC, among others, include review of the appointment, removal and terms of remuneration of Chief Risk Officer (CRO). The appointment of CRO is not a mandatory requirement under Listing Regulations. CRO is required to be appointed for all banking companies, and non-banking financial companies (NBFCs) having asset size of Rs. 50 billions or more, being registered as an Investment and Credit company, Infrastructure Finance Companies, Micro Finance Institutions, Factors, or Infrastructure Debt Funds. Further, the Insurance Regulatory and Development Authority of India (IRDAI) Corporate Governance Guidelines requires the insurance companies to appoint CRO.

The role of RMC further provides for co-ordination with other committees where the roles overlap. It is seen that the risk management function is also laid upon the Audit Committee. Therefore, the roles of both the committees might be overlapping. In view of the same, some companies choose to constitute one joint committee combining the roles of both Audit Committee and RMC. From the provisions providing for co-ordination of activities, it may also be taken as a clear indication that the committees cannot be merged into one, but co-ordinate where the activities require so.

Actionables –

- Changes in the constitution of RMC / Constitution of RMC in case of first-time applicability;

- Modification of the Risk Management Policy as per the Amendment Regulations;

- Amending the existing charter of the Committee to align with the amendments.

While the Amendment Regulations are effective immediately, the changes cannot take place overnight. Therefore, it is advisable that the listed entities shall take the matter of constitution/ re-constitution of RMC in the ensuing Board Meeting. The modification of Risk Management Policy will be then taken up by the RMC and can be done within a reasonable period of time.

What should be this period? A probable answer to this should lie in the proviso to clause (a) of Reg. 15 that permits a timeline of six months from the applicability to comply with corporate governance requirements as stipulated under regulations 17 to 27, clauses (b) to (i) and (t) of sub-regulation (2) of regulation 46 and para C, D and E of Schedule V. However, that is applicable only in case of companies covered in Reg. 15 (2) (a). Therefore, the time available is till June 30, 2021 as thereafter, the companies will be required to confirm on RMC composition in the quarterly filings done under Reg. 27.

3. Overriding powers of LODR Regulations

Earlier, proviso to Regulation 15(2)(b) provided a clear stipulation of overriding effect of specific statute in case of conflicting provisions. The Amendment Regulations provides for deletion of the said proviso effective from September 1, 2021. No rationale seems to have been provided in the agenda[1] put up before SEBI at the board meeting for this major amendment.

Regulators viz. RBI, IRDA, PFRDA at times have specific corporate governance related compliances that are stricter and at times conflicting with the requirements of Listing Regulations. For eg. With respect to composition of Audit Committee for a public sector bank, RBI Circular of September, 1995 provides for following composition in case of public sector banks: (a) Executive Director of the Bank (Wholetime director in case of SBI) (b) two official directors (i.e. nominees of Government and RBI) and (c) Two non-official, non-executive directors (at least one of them should be a Chartered Accountant). Directors from staff will not be included in ACB. This is certainly conflicting with the composition provided in Reg. 18 of Listing Regulations.

Subsequent to September 1, 2021 these entities will be regarded as non-compliant of the provisions of Listing Regulations and may be subject to penalty in terms of SEBI Circular dated January, 2020.

4. Reclassification of promoters into public – related exemptions and procedural changes

Regulation 31A of the LODR Regulations specifies the conditions and approvals post which the promoters can be re-classified into public shareholders. SEBI had proposed changes to the same in a consultation paper dated 23rd November, 2020. The consultation paper was critically analysed in our article. Amendments have been made on similar lines in Regulation 31A.

5. Alignment with the provisions of the Companies Act, 2013

Certain amendments have been made to remove the gap between the provisions of LODR Regulations, with that of the Companies Act, 2013 as given below –

- Separate meeting of independent directors – The requirement of conducting a separate meeting of the independent directors without the presence of any other member of the Board of the company is required under both the Companies Act, 2013 as well as the LODR Regulations. However, whereas the Companies Act requires one meeting in a financial year, the LODR Regulations required one meeting in a year (calendar year). Therefore, the same has been substituted with a “financial year” so as to align the requirements of both the governing laws.

- Display of Annual Return on website – Section 92 read with allied rules requires the companies, having a website, to display its Annual Return on the website. New clause has been inserted under Regulation 46 of LODR Regulations that requires placing the Annual Return on the website of the company.

- Changes in requirements pertaining to placing of financial statements on website – The audited financial statements of each of the subsidiaries was required to be placed on the website prior to the Amendment Regulations. New provisos has been inserted under the same so as to avoid preparation of separate financial statements of the subsidiary company, where the requirements under the Companies Act, 2013 are met if the consolidated financial statements are placed instead of separate ones.

6. Mandatory website disclosures

Regulation 46 of the LODR Regulations provides the mandatory contents to be placed on the website of a listed entity. Most of the disclosures were already existing under respective regulations viz. Reg 30, 43A etc. However, the same has been consolidated under regulation 46. This will now enable stock exchanges to levy penalty in terms of SEBI circular dated 22nd January, 2020.

7. Analyst meet

The listed entity is required to disclose the schedule of analyst or institutional investor meet and the presentations made to them on its website under regulation 46 and on the website of the stock exchange under Schedule III. The Amendment Regulations have explained the term ‘meet’ to mean the group meetings and calls, whether digitally or by physical means. The Amendment Regulations will require the listed entity to upload the audio/ video recordings and the transcripts within the prescribed timeframe. The same is in line with SEBI’s Report on disclosures pertaining to analyst meets, investor meets and conference calls. However, the amendment does not cover disclosure of one-to-one investor/ analyst meet conducted with select investors recommended in the said Report.

8. Consolidation of various SEBI circulars

Certain circulars of SEBI lay down various requirements to be complied with in relation to the LODR Regulations. The Amendment Regulations have consolidated the requirements under the principal LODR Regulations.

- Requirement of Secretarial Compliance Report – While the requirement of Annual Secretarial Compliance report were applicable on the listed entities and its material subsidiaries since a few years back, the same has now been specifically provided under newly inserted sub-regulation (2) of Regulation 24A. Earlier, the practice came pursuant to a SEBI circular.

- Timeline for report of monitoring agency regarding deviation in use of proceeds – Pursuant to the requirements of Regulation 32 of the LODR Regulations, the monitoring agency is required to give a report on the utilisation of proceeds of issue on a quarterly basis. While timelines were not specified in the LODR Regulations, the report was required to be given within 45 days from the end of the quarter. This timeline was pursuant to the SEBI circular dated 24th December, 2019 . Now, with the Amendment regulations, the same is specified under regulation 32(6) of the LODR Regulations.

- Requirement of Business responsibility and sustainability report (BRSR)- SEBI had proposed a new format to replace the existing Business Responsibility Report. The proposal was finalised and the BRSR format has been made mandatorily applicable from FY 2022-23 onwards, vide SEBI circular dated April, 2021 . The same has also been consolidated under Regulation 34 of the LODR Regulations. A detailed discussion on BRSR is covered in our article.

Conclusion

The Amendment Regulations are very crucial and significant in nature. While on one hand, certain provisions are aligned with the Companies Act, 2013, whereas on the other hand, overriding powers have been given to LODR Regulations which will require the listed entities formed under special statute to comply with the LODR Regulations in entirety. Uniformity in timelines and relaxation in certain disclosure requirements will encourage ease of doing business, and the coverage of certain provisions extended to listed entities based on market capitalisation will have a remarkable impact on the corporate governance of listed entities.

[1] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/meetingfiles/apr-2021/1619067328922_1.pdf#page=18&zoom=page-width,-17,763

Our other materials on the relevant topic can be read here –

- https://vinodkothari.com/2021/06/presentation-on-lodr-amendments/

- https://vinodkothari.com/2020/09/companies-amendment-act-2020/

- https://vinodkothari.com/2019/07/sebi-amends-lodr-in-relation-to-equity-shares-with-superior-rights/

- https://vinodkothari.com/2019/02/overlap-in-reporting-of-secretarial-compliance/

- https://vinodkothari.com/2018/12/faqs-on-sebi-listing-obligations-and-disclosure-requirements-amendment-regulations-2018/

- https://vinodkothari.com/2016/01/sebi-faqs-on-listing-regulations-2015-brings-ambiguity-rather-than-clarity/

Sir, pls confirm is risk management committee once applicable on listed entity then its always applicable for example as on 31/03/22 company falls under top 1000 listed entity then in next year its falls under Top 2000 listed entity.

Roles and Responsibility of of Risk Management Committee has been given in Part C of Schedule II (not it part D of Schedule II), clause D has been omitted by the SEBI (LODR) (Amendment) Regulations, 2018 w.e.f. 01.04.2020

Sir, please note that the Role and Responsibility of RMC has been given in clause C of Part D of Schedule II of LODR Regulations.