Making Corporate Governance IPO-ready

By Harsh Juneja | Executive ( corplaw@vinodkothari.com)

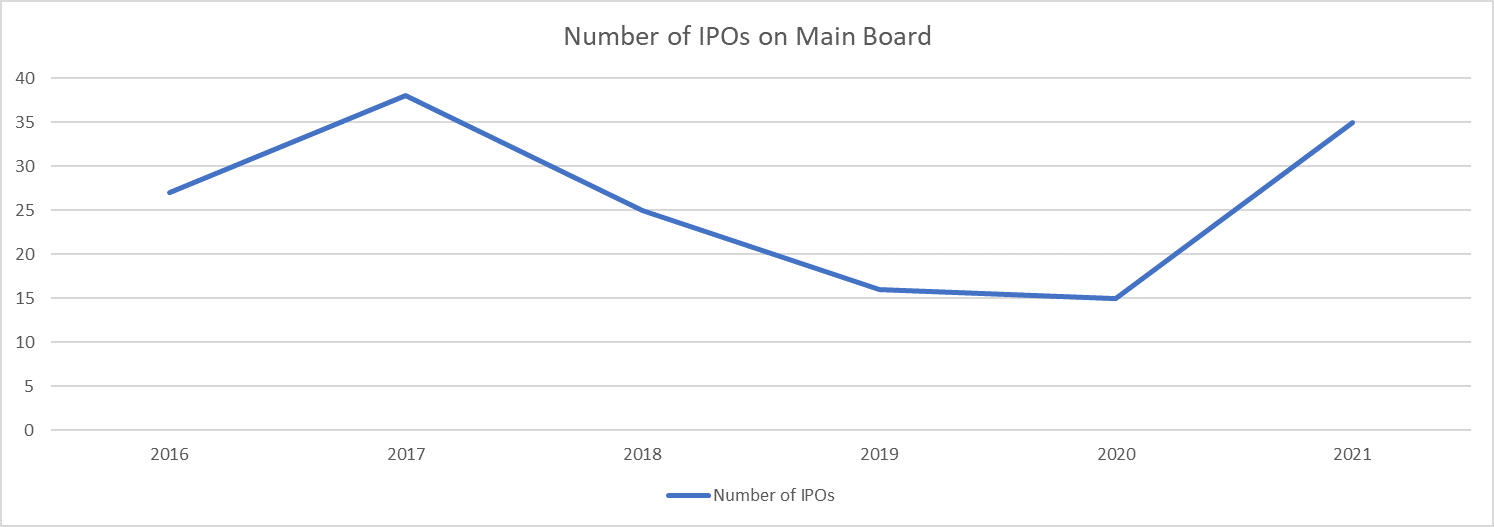

IPO Market Heating up

After facing economic crisis owing to the Covid-19 pandemic in March, 2020, a thunderstorm of IPOs strikes India’s Primary Markets. Since July 2020, a total of 48 Initial Public Offers (IPOs) have been issued which includes companies like Burger King, Zomato and Indigo Paints. Draft Red Herring Prospectus (DHRP) has also been filed by various unicorns like One 97 Communication (Paytm), Policy Bazaar Insurance and Nykaa for stepping their toes in the Indian Primary Market.

The above table indicates that even though the economy was not at its best pace in 2020, but still the number of IPOs had increased. Moreover, for 2021, even though the year has not completed yet, but the number of IPOs goes on increasing.

Post Pandemic Recovery

At the time of complete nationwide lockdown, stock market had hit rock bottom. But every cloud has a silver lining. Foreign Direct Investments (FDI) into country rose 15% on year-to-year to $39.9 billion (₹29,400 crore), according to a [1]report by CARE Ratings. Due to surge in foreign investments in the Indian market, it started healing itself. During these hard times, ‘Route Mobile Limited’ came up with an IPO which was a blockbuster in the capital market, as it was listed with a premium of 102.28%. Since then, capital market has been very receptive towards investments. This reception has made people more optimistic towards investment in primary markets.

Preparation in this IPO wave

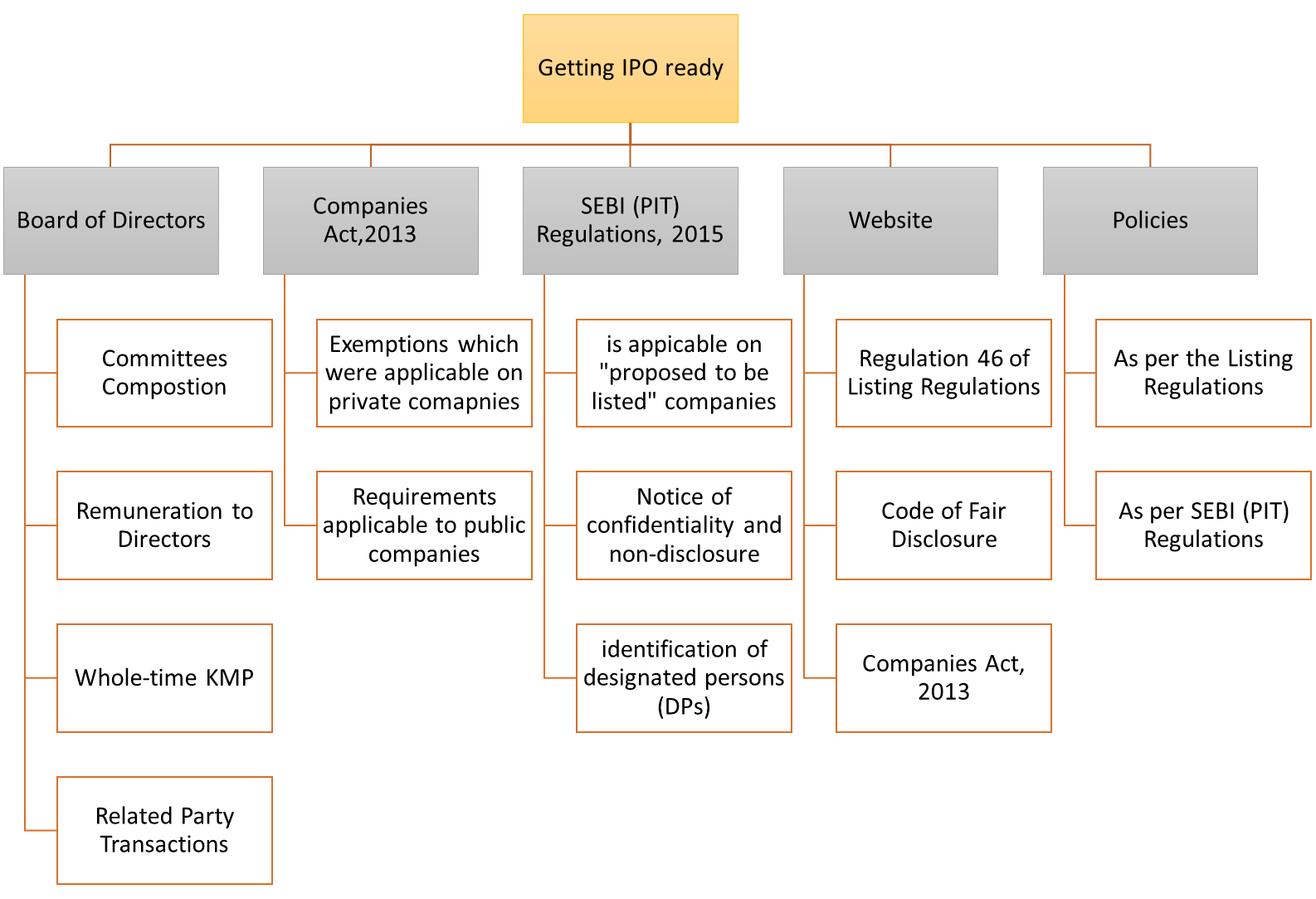

As we have discussed above, the people feel optimistic towards the Market, many companies which want to raise funds want to just swim along this wave. Companies feel that this is the best time to raise funds through stock market since they will be able to draw maximum premium for their shares. Potential companies need to ensure that mere compliance of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (‘SEBI (ICDR) Regulations’), is not sufficient as pursuant to listing, a plethora of compliances fall on the back of a company. Schedule VI of the SEBI (ICDR) Regulations, which deals with disclosures to be given in the Abridged Prospectus also requires a company to disclose that it has complied with the Corporate Governance provisions as specified under the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘the Listing Regulations’). Prospective issuers are also required to disclose the details of its committees along with a list of their members and detailed ‘Terms of References’ of such committees. These companies need to be prepared with compliances of the aforesaid provisions, along with some other compliances, beforehand to ensure that transitioning from an unlisted to listed company goes smoothly.

A snap shot of compliances one is required to be adhere to as a part of prepping up for an IPO can be seen below:

Board of Directors

Starting from the composition of the Board to the remuneration of the managerial personnel and requirement of Whole-time Key Managerial Person to review of all existing and probable related party transactions, all of these needs a reconsideration from the transition from a closely held company to a listed company.

Composition

The Board shall comprise of at least one woman director. At least 50% of total directors shall be non-executive directors (NEDs). The requirement of appointment of independent directors (IDs) shall also be adhered to as per the Listing Regulations.

Committees

· Audit Committee

Audit Committee shall have at least 3 members out of which at least 2/3rd members shall be IDs. The Chairperson of this Committee shall also be an ID and CS of the Company shall be the Secretary of the Committee.

· Nomination and Remuneration Committee (NRC)

NRC shall have at least 3 directors. Only NEDs can become members of NRC. At least 2/3rd members of NRC shall be IDs. The Chairperson of NRC shall be an ID only and chairperson of the Company, whether ED or NED, may become a member of NRC but shall not chair such committee.

· Stakeholders Relationship Committee (SRC)

SRC shall constitute of at least 3 directors, with at least one being an ID. The Chairperson of SRC shall be a NED.

-

Risk Management Committee (RMC)

As of now, requirement of constitution of RMC is applicable only on top 1000 listed companies. RMC shall consist of at least 3 members, majority of which shall member of the Board, with at least one being an ID.

Related Party Transactions

The ambit of related party shall be widened as it is not limited only to section 2(76) of the Companies Act, 2013 (‘the Act’), but also includes related parties as per Ind AS-24. All related party transactions shall be approved by only those members of the Audit Committee, who are IDs. All ‘material related party transactions’, as defined under Regulation 23 of the Listing Regulations, shall require approval of the shareholders and no related party shall vote to approve such resolution.

Whole-time Key Managerial Personnel (‘KMP’)

Pursuant to section 203 of the Act, read with Rule 8 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014, every listed company shall ensure it shall have the following Whole-time KMP:

- Managing Director, or Chief Executive Officer or Manager and in their absence, a Whole-time Director;

- Company secretary; and

- Chief Financial Officer.

Managerial Remuneration

Pursuant to listing, section 197 of the Act shall become applicable on a company. Therefore, it must ensure that the remuneration to managerial personnel is as per the limits prescribed under this section, before coming with an IPO. The Company is also required to pass a special resolution in case-

- Remuneration payable to a NED exceeds 50% of the total remuneration payable to all NEDs; and

- Remuneration payable to EDs who are promoters or a part of promoter group, which is exceeding the limits prescribed under Regulation 17(6)(e) of the Listing Regulations.

Provisions of Companies Act, 2013 applicable on listed entities

A company which is closely held is entitled to certain exemptions under the Act. However, pursuant to listing, the veil of all these exemptions gets lifted in the following manner:

- Pursuant to [2]MCA Notification dated June 05, 2015, private companies are exempt from compliances with various provisions of the Act like section 160, 162 and 180 etc. But due to listing, all these exempted provisions become applicable; and

- Various provisions like section 152(6) and 196 of the Act, which are only applicable on public companies, shall also become applicable on a private company post-listing. Therefore, the Company should ensure that provisions of these sections are complied with before an IPO.

SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘the PIT Regulations’)

The PIT Regulations, 2015 defines ‘proposed to be listed’ company as an unlisted company, whose securities are getting listed pursuant to filing of offer documents or other documents or pursuant to any merger or amalgamation. Prevention of Insider Trading in a company becomes inevitable in case its securities get listed. Therefore, the PIT Regulations also requires a company, even if it is proposed to be listed, to comply with its provisions. There are also few compliances which a company should be prepared with before coming up with an IPO:

- The Board should formulate and publish on its official website, a code of practices and procedures for fair disclosure of unpublished price sensitive information that it would follow in order to adhere to each of the principles set out in Schedule A to the PIT Regulations. A policy for determination of ‘legitimate purposes’ shall also form a part of this Code;

- Any person in receipt of UPSI pursuant to a “legitimate purpose” shall be considered an “insider” and due notice shall be given to such persons to maintain confidentiality of such unpublished price sensitive information in compliance with these regulations; and

- Before listing, the Company should identify its ‘designated persons’ who shall be governed by the Company’s Code of Conduct on Insider Trading.

Website

Companies Act, 2013 does not mandate a company to create a website. However, pursuant to listing, Regulation 46 of the Listing Regulations gets triggered which mandates it to maintain a functional website and upload various information on it as mentioned under Regulation 46(2). We discussed above about the Code of Fair Disclosure which companies are required to make under the PIT Regulations. This Code is also required to be disseminated on the website of the Company. Companies Act, 2013, requires following information to be disclosed on the website of a company, in case it maintains, –

- Details of business

- Invitation of Deposits

- Closure of books

- Statement for unpaid Dividend Account

- Corporate Social Responsibility

- Consolidated Financial Statements

- Terms and conditions of appointment of IDs

- Notice of candidature for directorship

- Notice of resignation from directorship

- NRC Policy

Policies

The Listing Regulations and PIT Regulations require a listed company to prepare various policies. As launching an IPO is itself a cumbersome process and requires a lot of other compliances to be fulfilled a prospective issuer should prepare these policies beforehand. The following policies required to be made are: –

Conclusion

As we have discussed, there are many companies which have been raising funds through IPOs this year and mere compliance of checklist of ICDR Regulations is not sufficient for a company from transition from an unlisted to a listed company. Potential issuers must bear in mind that pursuant to listing, the money of retail individual investors also vests with a company and thus requires good corporate governance practices.

[1] https://www.careratings.com/upload/NewsFiles/SplAnalysis/FDI%20Update%20-%20H1%20FY21.pdf

[2] https://www.mca.gov.in/Ministry/pdf/Exemptions_to_private_companies_05062015.pdf

You may also refer to our video on Appraising post-IPO governance requirements – https://www.youtube.com/watch?v=CXh3tiISxxY

Consolidation of SEBI regulations on non-convertible securities

SEBI measure may ease out issuance of debt securities

- Team Corplaw (corplaw@vinodkothari.com)

Introduction –

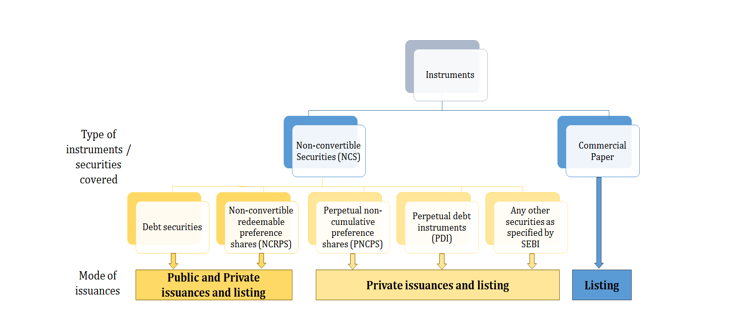

By a 9th August, 2021 Notification, SEBI has consolidated the regulatory framework pertaining to issue of non-convertible debentures (‘NCDs’), non-convertible preference shares (‘NCPS’), perpetual debt securities (‘PDIs’), and listed commercial paper. Along with the consolidation exercise, SEBI has also tried to iron out some of the difficulties being faced in respect of debt issuance by companies. Accordingly, the new SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (‘NCS Regulations’), notified on 9th August, 2021, have the effect of merging (and consequently, repealing) the SEBI (Issue & Listing of Debt Securities) Regulations, 2008 (‘ILDS Regulations’) and SEBI (Issue & Listing of Non-Convertible Redeemable Preference Shares) Regulations, 2013 (‘NCRPS Regulations’)

The NCS regulations have been introduced in line with the Draft Consultation Paper[1] (‘Consultation Paper’) issued by SEBI on the subject on 19th May, 2021.

In this article, we discuss and highlight the important changes incorporated in the NCS Regulations as compared to the ILDS Regulations and NCRPS Regulations.

Effective date and prospective applicability

The regulations shall be effective on the 7th day from the date of their publication in the Official Gazette i.e. 16th August, 2021.

As to whether NCS Regulations are applicable on issuances done before the effective date, it is evident from a reading of regulation 4(2) that NCS Regulations are to be satisfied by the issuer as on the date of filing draft offer document/offer document with SEBI, stock exchanges and RoC. This indicates that securities which are already floating in the market pursuant to issuances done before 16th August, 2021, NCS Regulations should not make a difference. Hence, the new regulations shall be applicable only to new issuances or new listing applications made on or after August 16, 2021.

The view is further substantiated by the fact that –

- There is no grandfathering clause in the NCS Regulations, and

- The provisions pertaining to ‘repeal and savings’ provide for continuation of “right, privilege, obligation or liability acquired, accrued or incurred under the repealed regulations” as if the repealed regulations have never been repealed – see discussion later.

Rationale behind the fused regulations–

Debentures, specifically non-convertible debentures, are purely debt instruments. However, NCRPS are hybrid instruments combining characteristics of both debt and equity thereby being ‘quasi-debt instruments’. Due to this reason, the NCRPS regulations were mostly modelled based on the ILDS regulations providing similar provisions on eligibility conditions, disclosure requirements, etc. Therefore, merging the two regulations would only be reasonable. The move to merge both these regulations may not be a complete solution to the regulatory chaos, but is definitely in the direction to combat multiplicity of laws. Further, the NCS Regulations also aim to –

- Harmonise provisions of the Companies Act, Rules made thereunder and SEBI Regulations

- Align various circulars, guidelines issued by SEBI

- Identify policy changes in line with the present market practices for ease of doing business

- Merge all the existing circulars into a single operational circular

Repeal of existing regulations –

The NCS regulations shall repeal the existing ILDS Regulations and NCRPS Regulations from the effective date. Reference to any provision under these regulations shall be deemed to make reference to corresponding provisions in the NCS regulations.

Applicability of the NCS Regulations-

The following have been covered by the NCS Regulations:

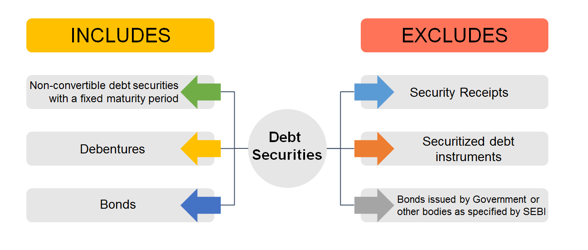

Definition of Debt securities –

Listing of Commercial Paper

Another important point to note is that the NCS Regulations only deal with listing of CP and issuance thereof shall not be covered. The NCS Regulations have adopted the earlier SEBI Circular on Listing of CPs with respect to provisions on the said subject. The caveats relating to eligibility, mode of issuance, etc. shall still be governed by the provisions of RBI read with FIMMDA operational guidelines.

Only additional caveats arising from the NCS regulation for the issuer is that they shall be required to register on SCORES Platform. In case the entity has its NCDs or NCRPs listed they are already required to register on SCORES Platform in terms of SEBI (Listing Obligation and Disclosure Requirements) Regulations, 201 (‘LODR Regulations’).

Issuers covered under the NCS regulations

Point at which conditions are to be satisfied

There are several conditions in the NCS Regulations which the issuer needs to fulfil as on the date of filing draft offer documents/offer documents – see, regulation 4(2). For instance, as on the date of filing of draft offer document or offer document, neither the issuer its promoters, promoter group or directors should be debarred from accessing the securities market or dealing in securities by SEBI, none of the promoters or whole-time directors of the issuer shall be promoter or whole-time director of another company which is a wilful defaulter. Therefore, if this condition is, say, breached after the securities are listed, the issuer shall not be seen as in breach of the regulations.

While most of the requirements have been retained from the erstwhile regulations, the NCS regulations also additionally prohibit any issuer from making an issue if as on the date of filing of the draft offer letter, if any of its promoters or whole-time directors are a promoter or whole-time director of another company which is a wilful defaulter.

Whether LLPs can issue debentures?

Key highlight of the definition of “issuer” under the NCS Regulations is inclusion of the term “body corporate”. The erstwhile definition of “issuer” under the ILDS Regulations did not include body corporates. Several rulings have established that an LLP is, in fact, a body corporate. Accordingly, this exclusion raised a question on the permissibility of listed debt issuances by an LLP. It was always, therefore, deemed that LLPs could only issue unlisted debt securities while listed debt securities by LLPs was not permitted by the ILDS Regulations. The said inclusion of “body corporate” in the definition of “issuer” will, therefore, enable LLPs to issue listed debt securities as well as NCRPS, thereby making way for further raising of funds.

However, the same shall be subject to any conditions in the LLP Act, 2008. The Company Law Committee Report[2] for decriminalization of LLP Act also discussed on raising of funds through issuance of secured non-convertible debentures to bodies corporate or trusts regulated by SEBI or RBI with certain fetters and suggested inclusion of new section in the LLP Act, 2008 for the same.

Highlights

1) Appointment of Debenture Trustee for all issues of debt security

The ILDS Regulations provided for appointment of a Debenture Trustee (’DT’) for public issuance of debt securities. While there was no explicit requirement for the appointment of debenture trustee for private placement of debt securities in the ILDS Regulations, in terms of Companies Act, 2013 (‘CA, 2013’) and SEBI Circular dated November 03, 2020, security was required to be created in the favour of a DT. Accordingly, there was no clarity as to the appointment of debenture trustee in case of issuance of unsecured NCDs through private placement. The NCS regulations now provide for mandatory appointment of DTs in case of all issuances of debt securities (Regulation 8 of the NCS Regulations).

Our Comments –

The same is a welcome change as it provides the required clarity on appointment of DTs. Considering the increasing relevance and importance of DTs in case of debt issuances, appointment of DTs in case of all debt securities becomes all the more important.

2) Widened applicability of EBP platform

The EBP platform is presently applicable to private placements of debentures amounting to Rs. 200 crores and above in a financial year. SEBI, in its Consultation Paper, proposed to reduce such limit to Rs.100 crores or above and making EBP mandatory for issues breaching the said limit. The same was proposed considering the benefits of the EBP platform and need for further increased participation from issuers and investors.

The said change did not reflect either in the draft or the final regulations. The revision in the limits may be made in the EBP Circular by SEBI.

Our Comments –

The concept of the EBP was introduced by SEBI with a view to make participation in the privately-placed bond market more inclusive. Electronic bidding platforms are there in several other markets – however, in most cases, these are private bidding engines, and are optional.

The private placement market in India is completely bespoke in nature, and issuances are almost completely OTC negotiations. In order to remove the veil of opacity, and allow a larger base of investors to participate, the EBP mechanism was introduced.

However, various market participants are averse to the EBP platform. Lengthy procedures delay the process for issuers which may not be suitable for a sensitive debt market. Different EBP platforms have different procedures thereby causing confusion. Most issuers still continue to negotiate on OTC basis and place the offer on EBP or make use of regulatory arbitrage methods such as market-linked debentures (‘MLDs’).

Therefore, increasing the scope of applicability of EBP may not be conducive to the Indian bond market. SEBI may consider making the EBP optional rather than mandatory. Where the issuer desires a wider audience for its proposed issue, the issuer may put the offer on the bidding platform. However, where an OTC deal is done, the issuer should be allowed to go ahead with the private placement straightaway. A potential investor wanting to invest therein will still have the chance to participate in the secondary market.

3) Private Placement Requirements

The NCS Regulations [regulation 44(2)] clarify the ambiguity regarding issuance of debt securities on private placement basis by a company in existence for less than three years. The requirement to provide annual reports for previous three years while making an application for listing presumed the requirement for a company to be in existence for at least three years to list its privately placed debentures. However, the proviso to regulation 44(2) resolves the above by specifying that ‘provided that issuers desirous of issuing debt securities on private placement basis who are in existence for less than three years may provide Annual Reports pertaining to the years of existence.

4) Exercise of Call or Put Option (Right to recall or redeem prior to maturity date)

The erstwhile provisions for issuance of non-convertible debt securities, provided framework for right to recall (i.e. Call Option) and right of redemption (i.e. Put Option) prior to maturity, in case of public issue of NCDs. In case of private placement of NCDs, the same was entirely guided by the terms of issue.

However, the NCS regulations have now stipulated that provisions relating to call and put option shall equally apply in case of public issuances as well as private placement.

This seems to take away the flexibility that issuers enjoyed in certain cases for issuers of privately placed debentures for example, where an interest rate in case of delay on part of the issuer could be avoided or kept at a minimal rate, the same will be charged at 15% interest rate.

It may be noted here that there is an apparent change in the language – while regulation 15 of NCS Regulations uses “shall”, regulation 17A of ILDS Regulations used “may”. However, this change in language does not change the law – it is still a ‘right’ in the hands of the issuer to “recall” the securities using a “call option” or “provide a right” to investors to “redeem” the securities using a “put option”. As it is a matter of right to the issuer, the right can still be exercised (or not exercised) by suitably providing for the same in the terms of issue.

Also, regulation 15 itself specifies that the issuer shall have a right to provide such right of redemption of debt securities prior to the maturity date (put option) to all the investors or only to retail investors.

The NCS Regulations do not state the time period for payment of interest, which was specified as 15 days from the day from which such right could be exercised under the erstwhile provisions.

Our Comments –

Since the Call and Put Option are exercised in accordance with the terms of issue and detailed disclosure made in this regard in the offer document, the issuers of privately placed debt securities issued prior to the NCS Regulations can provide these options after the expiry of one year from date of issue and only if it was disclosed in the offer document.

Further, it must be noted that the ‘call option’ feature would be relevant for debt securities as well as NCPS; however, ‘put’ option feature will only be relevant for debt securities. This is because a ‘put option’ enables the investor to exercise a ‘right’ to sell the securities to the issuer. Redemption of preference shares can either be done out of profits of the company or out of fresh issue of shares, as per Section 55 (2) (a) of Companies Act. In case the put option is exercised, the company will be under obligation to redeem and this may result in violation of section 55 in case the issuer is not able to redeem in the prescribed manner. Hence, while clause (a) of regulation 15(1) applies to all non-convertible securities (debt + NCPS), clause (b) applies only to debt securities.

5) Exemption from restriction of use of proceeds

Issuers of non-convertible securities are prohibited from using proceeds from issuances of such securities for providing loans to or acquisition of shares of entities under their promoter group or group companies. The erstwhile laws failed to distinguish between a financial entity and non-financial entity as regards to the nature of business. Therefore, the said restriction was applicable in case of all listed entities alike.

The NCS regulations provide the much needed relaxation from the said clenching restriction in case of a Non-Banking Finance Company (‘NBFC’), Housing Finance Company (‘HFC’) and a Public Financial Institution.

Our Comments –

The intent behind the restriction was to discourage using public money for funding group entities. However, providing loans or acquiring securities aren’t peculiar transactions in case of NBFCs and HFCs since they are ordinarily in such business.

6) Validity of shelf prospectus:

In case of Public Issue of debt securities:

The ILDS Regulations provide that not more than four issuances can be made under a single shelf prospectus while there is no such restriction under the Companies Act. To enable issuers to raise funds quickly without filing a separate prospectus each time, this restriction has been removed from NCS Regulations.

In case of private placement of debt securities:

The time validity of shelf prospectus in case of private placement of debt securities has been increased from 180 days to 1 year.

Our Comments –

This is a welcome move, as this will eliminate hassles for frequent issuers to file shelf prospectus multiple times.

7) Criteria of eligible issuer

Under the NCS Regulations, the condition that the issuer shall not be debarred from accessing the securities market or dealing in securities has been extended to promoter group entity as well. Further, certain additional conditions such as the promoter or WTD shall not be a promoter or WTD of a company which is a wilful defaulter, no promoters or directors shall be fugitive economic offenders or no fines or penalties are pending at the time of filing of offer document have been inserted.

Our Comments –

Associating payment of fines and penalties with listing might not be a feasible idea; as there might be situations where the issuer may have raised disputes/concerns on liability to pay such fines/penalties.

8) Additional Disclosures for NBFCs

In case the issuer is an NBFC/HFC additional disclosures on asset liability management are required to be provided pertaining to the latest audited financials. The same was not required under the ILDS Regulations. The disclosures also include details of contingent liabilities specifying the nature and amount of such liabilities.

9) Companies existing for less than 3 years – Annual report submission provision

As per the NCS Regulations in case an issuer who has been in existence for less than 3 years is desirous of issuing debt securities, annual reports pertaining to years of existence have been permitted to be provided.

10) Creation of Recovery Expense Fund – Whether applicable in case of NCPS?

Under the NCPs regulations requirement of maintenance is included under the general conditions applicable in case of public issuance of debt securities and NCPs and private placement of NCS. However, due regard must be given to SEBI circular dated October 22, 2020[3] which provides the manner and mode for creation and maintenance of recovery expense fund, specifically restricts the requirement only in case of issue of debt securities. Moreover, it may be noted that preference shares can be redeemed only out of profits and out of proceeds of new issuances (as provided for under section 55) and are thus, inherently different from debt securities. Hence, this requirement of recovery expense fund should not apply in case of NCPS.

11) Minimum subscription in case of public issue of Debt Securities

The ILDS Regulations gave the option to the issuer to identify the minimum subscription, however the NCS Regulations has straight away set a bar of 75% of the base issue size. This might take away the flexibility from the issuers.

The requirement of minimum subscription is however not applicable in the case of issuance of tax free bonds as specified by the Central Board of Direct Taxes.

12) Creation of Security

As per the ILDS Regulations, in case of secured debentures, the assets offered as collateral are required to be unencumbered provided that if the same are already charged to secure a debt, relevant permission to create a pari passu or a second charge will be taken from the existing chargeholders. This requirement was applicable to the total security cover in case of a debt issuance i.e. even in case of over-collaterisation.

However, the NCS regulations have eased out the said stipulation providing that the same shall apply on assets to the extent of 100% security cover. Thus, assets over and above the 100% security cover may be encumbered and the same may be provided as security without obtaining relevant permissions from the existing chargeholders.

For instance, if an issue of debentures is secured to the extent of 125% of the issue size – earlier the assets securing the entire 125% charge were required to be unencumbered, now only assets constituting 100% charge of the issue will be required to be unencumbered.

13) Due Diligence

The requirement of undertaking due diligence in case of public issue of NCDs was already there in the ILDS Regulations Additionally, SEBI vide its circular dated November 03, 2020, also required DTs to undertake due diligence w.r.t creation of security, irrespective of the debentures being issued publicly or on a private placement basis. The NCS Regulations now provide for due diligence in case of private placement as well, before filing of the offer document.

Overall, it seems that the Regulations are on a positive note. The discussion above is a quick compilation of the important points which come out of the NCS Regulations. We shall be continuously updating the list above on the basis of further observations.

You may also refer to our following articles on related subjects-

- Presentation on Corporate Bonds and Debentures

https://vinodkothari.com/2021/03/presentation-corporate-bonds-debentures/

- SEBI’s stringent norms for secured debentures

https://vinodkothari.com/2020/11/sebis-stringent-norms-for-secured-debentures/

- Market-Linked Debentures – Real or Illusory?

https://vinodkothari.com/2021/01/market-linked-debentures-real-or-illusory/

- FAQs on Commercial Paper

https://vinodkothari.com/2019/11/faqs-on-commercial-paper/

Our our Book on Law and Practice Relating to Corporate Bonds and Debentures, authored by Ms. Vinita Nair Dedhia, Senior Partner and Mr. Abhirup Ghosh, Partner can be ordered though the below link:

Our presentation on the structuring of debt securities can be viewed here – https://vinodkothari.com/2021/09/structuring-of-debt-instruments/

[1] https://www.sebi.gov.in/reports-and-statistics/reports/may-2021/consultation-paper-review-and-merger-of-sebi-issue-and-listing-of-debt-securities-regulations-2008-and-sebi-issue-and-listing-of-non-convertible-redeemable-preference-shares-regulations-2013-i-_50192.html

[2] https://www.mca.gov.in/Ministry/pdf/Report%20of%20the%20Company%20Law%20Committee%20on%20Decriminalization%20of%20The%20Limited%20Liability%20Partnership%20Act,%202008.pdf

[3] https://www.sebi.gov.in/legal/circulars/oct-2020/contribution-by-issuers-of-listed-or-proposed-to-be-listed-debt-securities-towards-creation-of-recovery-expense-fund-_47939.html

Classification out of promoter category under Listing Regulations

Anushka Vohra, Deputy Manager corplaw@vinodkothari.com

In common jargon, promoters are the persons who conceive the idea of incorporating a company and are associated with the company since its inception. In legal parlance, the concept of promoter has been kept open-ended. The definition has been captured under various legislations and has been made inclusive.

The status of a promoter might seem to be dignified and magnificent when looked from a wild blue yonder. However, as the saying, ‘uneasy lies the head, that wears the crown.’; likewise the status of being a promoter brings with itself shedload of liabilities and obligations. It is pertinent to note that once a promoter, always a promoter unless reclassified. Considering the several disclosures that an entity falling under the ambit of promoter / promoter group is required to provide, it is likely for a dormant promoter / promoter group to want to re-classify themselves.

Regulation 31A of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 provides the modus operandi with respect to re-classification of promoter / promoter group shareholding to public category.

There are several aspects to this re-classification. For example, what if the entity intending to re-classify intends to continue to be a shareholder, what if it’s a Trust, is there any exception for married daughters, estranged relations etc.

In this write-up, we have tried capturing the stance of stock exchange / SEBI for matters which have already been preferred for re-classification.

Message for Readers:We have endeavoured to cover all cases of re-classification occurred between the advent of Regulation 31 A in 2015 till August 05, 2021 but the same cannot be verified. We shall be further updating our list, based on applications made to the stock exchange(s). We shall also be coming with a consolidated write-up covering the intricacies of Regulation 31A and a detailed analysis on what motivates Promoter’s to reclassify them as public. |

1.Applications allowed

| Sr.No | Date of approval | Name of the listed entity | Outgoing promoter/ promoter group [name] | Whether promoter / promoter group (PG) | Promoter type (whether director or otherwise) | Shareholding at the time of re-classification (%) | Rationale given in the application for re-classification |

| 1. | June 24, 2021 | Fortis Malar Hospitals Limited[1] | Malvinder Mohan Singh | Promoter | Individual | NIL | Pursuant to SEBI order[2] |

| Shivi Holdings (P) Limited | |||||||

| RHC Finance Private Limited | |||||||

| Todays Holdings Private Limited | |||||||

| Oscar Investments Limited | |||||||

| Malav Holdings Private Limited | |||||||

| RHC Holdings Private Limited | |||||||

| Fortis Healthcare Holdings Private Limited | |||||||

| 2. | May 27, 2021 | Arvind Limited | AML Employee’s Welfare Trust[3] | Trust | 2.44 | No control | |

| 3. | April 06, 2021 | ISMT Limited[4] | Tara Jain[5]

|

Promoter | Individual | 0.97 | The members belong to Ashok Kumar Jain group, the later Promoter Director. After the demise of Mr. Ashok Kumar Jain, none of the family members have been appointed on the Board and do not exercise any control. |

| Ashok Kumar Jain (HUF) | PG

|

HUF | 1.73 | ||||

| Aayushi Jain | Individual | 0.03 | |||||

| Akshay Jain | Individual | 0.01 | |||||

| Tulika Estate & Holdings Limited | Company | 0.37 | |||||

| 4. | April 05, 2021 | Healthcare Global Enterprises[6] | Ramesh S Bilimagga | Promoter | Individual

|

0.21 | No control

|

| Ganesh Nayak

|

Promoter | 0.22 | |||||

| Venkatesh Sudha | PG | 0.02 | |||||

| Pradeep Nayak

|

PG | 0.02 | |||||

| Adarsh Ramesh

|

PG | NIL | |||||

| Gopi Chand Mammillapalli

|

Promoter | 1.44 | |||||

| Gopinath K S

|

Promoter

|

0.32 | |||||

| Prakash Nayak

|

PG | 0.05 | |||||

| Srinivas K Gopinath | PG | NIL | |||||

| 5. | April 01, 2021 | VXL Instruments Limited[7] | M V Nagaraj | Promoter | Individual | 2.39 | 1. Leading life and occupation independently;

2. Not connected with any activity of the Company. |

| 6. | March 31, 2021 | Aarti Industries Limited[8] | Dilip Dedhai and Nimesh Dedhai | None specified | Individuals | 0.04 | No control |

| Bhavesh Mehta

|

Individual | 0.04 | |||||

| Bhavesh Mehta and Alka Mehta | Individuals | 0.10 | |||||

| 7. | January 28, 2021 | Nippon Life India Asset Management Limited[9] | Reliance Capital Limited | Promoter | Company | 0.93 | Pursuant to Share Purchase Agreement (‘SPA’) |

| 8. | January 08, 2021 | Mafatlal Industries Limited[10] | Vishad Padmanabh Mafatlal Public Charitable Trust | Promoter | Shareholder- Trust | 0.17 | No control. |

| 9. | December 24, 2020 | Jyoti Limited[11] | Chirayu Ramanbhai Amin | PG | Individual | NIL | Not engaged in day to day affairs |

| Mayank Nitubhai Amin | |||||||

| 10. | December 24, 2020 | Teamlease Services Limited[12] | Dhana Management Consultancy LLP | PG | LLP | 4.99 | Not engaged in day to day affairs |

| Anupama Gupta | Promoter | Individual | 0.02 | ||||

| 11. | December 15, 2020 | Mindtree Limited[13] | Krishnakumar Natarajan & family | Promoter & PG | Individuals

|

5.00 | This re-classification was sought pursuant to takeover of Mindtree by L&T. L&T acquired 60 %

|

| Rostow Ravanan & family | 0.67 | ||||||

| N S Parthasarathy & family | 1.43 | ||||||

| Subroto Bagchi & family | 4.77 | ||||||

| LSO Investment Private Limited[14] | Promoter

|

Foreign Company | 1.16 | ||||

| Kamran Ozair

|

Individual

|

NIL | |||||

| Scott Staples

|

NIL | ||||||

| 12. | December 09, 2020 | Birlasoft Limited[15] | Shashishekhar Pandit | None specified

|

Individual

|

NIL

|

No control. |

| Nirmala Pandit

|

|||||||

| Chinmay Pandit

|

|||||||

| Kishor Patil

|

|||||||

| Shrikrishna Patwardhan | |||||||

| Ajay Bhagwat | |||||||

| Ashwini Bhagwat jointly held with Mr. Ajay Bhagwat | |||||||

| Sachin Tikekar | |||||||

| Anupama Patil | |||||||

| Proficient Finstock LLP | LLP | ||||||

| K and P Management Services Pvt. Ltd. | Company | ||||||

| Hemlata Shende | Individual | ||||||

| 13. | November 26, 2020 | Ruchi Soya Industries Limited[16] | The entire PG was replaced by new set of Promoters | – | – | 0.14 | This was pursuant to approval of Resolution Plan under Corporate Insolvency Resolution Process of Ruchi Soya Industries Limited (“the Corporate Debtor”). |

| 14.

|

November 23, 2020 | DFM Foods Limited[17] | Mohit Jain | None specified. | Individual | NIL

|

Entire stake was sold to AI Global Investments (Cyprus) PCC Limited. |

| Surekha Jain | |||||||

| Rohan Jain | |||||||

| Rashad Jain | |||||||

| The Delhi Flour Mills Company Limited | Company | ||||||

| 15. | November 19, 2020 | Aplab Limited[18] | Zee Entertainment Enterprises Limited | Promoter | Company | 9.50 | Pursuant to termination of shareholder’s agreement |

| 16. | October 07, 2020 | Igarashi Motors India Limited[19] | Mukund P | Promoter | Individual | NIL | 1. Divested his stake on August 28, 2019 in favor of Igarashi Electric Works Ltd, Japan and Agile Electric Sub Assembly Private Limited;

2. Ceased to be MD from October 01, 2019. |

| MAPE Securities Private Limited | Company | No control. | |||||

| 17. | July 29, 2020 | Tourism Finance Corporation of India Limited[20] (TFCIL) | Red Kite Capital Private Limited (RCPL) | None specified | Company | 0.17 | Sale of entire stake[21] |

| 18. | July 13, 2020 | Andhra Paper Limited[22] | International Paper Investments Luxembourg s.a.r.l. | None specified | Foreign Company | NIL

|

1. NIL shareholding;

2. No special rights. |

| IP International Holdings Inc | |||||||

| 19. | June 25, 2020 | Welspun Group[23] | Intech Metals S.A. | PG | Body Corporte | 1.54 | 1. Not connected with any activity of the Company;

2. No control over the affairs of the Company. |

| 20. | June 24, 2020 | XT Global Infotech Limited[24] | Velchala Premchand Krishna Rao | PG

|

Individual | 0.80 | Leading life and occupation independently |

| V. Radhabai | 0.00 | Expired on December 25, 2015

|

|||||

| 21. | June 12, 2020 | Yes Bank[25] | Madhu Kapur

|

Promoter

|

Individual | 1.12 | Pursuant to RBI direction. |

| Rana Kapur

|

NIL | ||||||

| Yes Capital (India) Private Limited | Company

|

NIL | |||||

| Mags Finvest Private Limited | 0.30 | ||||||

| Morgan Credits Private Limited | NIL | ||||||

| 22. | February 26, 2020 | Ajmera Realty and Infra India Limited[26] | Fahrenheit fun and games Private Limited | None specified. | Company | 7.05 | 1. Not involved in the management;

2. No control over the affairs of the Company. |

| 23. | February 20, 2020 | Essel Propack Limited[27] | Ashok Kumar Goel, Trustee of Ashok Goel Trust | None specified | Trustee | 7.67 | Pursuant to Share Purchase Agreement (“SPA”) |

| Goel Ashok Kumar | Individual | 0.27 | |||||

| Kavita Goel | 0.01 | ||||||

| Vyoman Tradelink India Private Limited | Company | 0.06 | |||||

| Pan India Paryatan Private Limited | 0.02 | ||||||

| Nandkishore | Individual | NIL | |||||

| 24. | January 31, 2020 | Innovassynth Investments Limited[28] | Futura Polyesters Limited | None specified | Company | NIL | Do not want to be associated with the Company. |

| 25. | January 29, 2020 | Sudarshan Chemical Industries Limited[29] | Rohit Kishor Rathi | None specified | Individual | 6.72 | No control over the affairs of the Company. |

| Kishor Laxminarayan Rathi | 1.10 | ||||||

| Aruna Kishor Rathi | 1.10 | ||||||

| Laxminarayan Finance Private Limited | Company | 1.01 | |||||

| 26. | October 14, 2019 | Astra Microwave Products Limited[30] | K Murali Mohan | None specified. | Individual | 0.95 | No control. |

| ASSR Reddy | 0.34 | ||||||

| Lakshmi Reddy Chittepu | 0.23 | ||||||

| Padmavathi Chfttepu | 0.19 | ||||||

| Shumlreddy Lakshmi | 0.13 | ||||||

| Chandrasekara Reddy G | 0.06 | ||||||

| Subrarnanyam J | 0.03 | ||||||

| Venkatamma Chittepu | 0.00 | ||||||

| G Thulasi Devi | 0.00 | ||||||

| Narapu Reddy CV | 0.00 | ||||||

| T.Sitarama Reddy | 1.00 | ||||||

| 27. | March 25, 2019 | Refex Industries Limited[31] | T. Jagdish | None specified | Individual | 0.0478 | No control. |

| Seema Jain | 0.5436 | ||||||

| 28.

. |

September 19, 2019 | Redington (India) Limited[32] | Harrow Investment Holding Limited | Promoter | Company | NIL | Disinvested entire stake in the Company in 2017 |

| 29. | November 21, 2018 | India Gelatine & Chemicals Limited[33] | Manorama N. Mirani | None specified | Individual | 0.17 | No substantial shareholding |

| Sunil P. Mirani | 1.11 | ||||||

| Arjun S. Mirani | 0.01 | ||||||

| Aditi P. Mirani | 0.05 | ||||||

| Madhav N. Mirani | 0.97 | ||||||

| Kishorsinh R. Mirani | NIL | ||||||

| Manish K. Mirani | NIL | ||||||

| Nayankumar C. Mirani | NIL | ||||||

| Rahul C. Mirani | NIL | ||||||

| Jash N. Mirani | NIL | ||||||

| Nimisha M. Mirani | NIL | ||||||

| Hina N. Mirani | NIL | ||||||

| Tanmay N. Mirani | NIL | ||||||

| Purnima K. Mirani | NIL | ||||||

| 30. | October 19, 2018 | Sonata Software Limited[34] | Bela M Dalal

|

None specified | Individual | 0.21 | The aforesaid members have gradually reduced their shareholding over the past few years and current shareholding along with PACs is not more than 5% |

| Mukund Dharamdas Dalal | 0.99 | ||||||

| Daltreya Investment & Finance Private Ltd | 0.10 | ||||||

| Bhupati Investments and Finance Pvt Ltd | 1.49 | ||||||

| Shyam Bhupatirai Ghia | 0.00 | ||||||

| 31. | September 28, 2018 | Eicher Motors Limited[35] | Arjun Joshi | None specified | Individual | 0.37 | 1. Shares were acquired pursuant to transmission during 2017-18;

2. Prior to inheritance they did not fall into Promoter & Promoter Group category;

3. None of them is an immediate relative of any other Promoter. |

| Nihar Joshi | 0.37 | ||||||

| Shonar Joshi | 0.37 | ||||||

| 32. | September 21, 2018 | Electrosteel Steels Limited[36] | Electrosteel Castings Limited | Promoter | Company | 45.23 | Pursuant to approval of Resolution Plan under IBC, Electrosteel Steels Limited was acquired by Vedanta Star Limited. |

| 33. | October 09, 2017 | Century Textiles and Industries Limited[37] | Ravi Makharia | None specified | Individual | 0.001 | Ramavatar Makhari was an Executive Director (ED) of Pilani Investment and Industries Corporation Limited, which is the Promoter of Century Textiles and Industries Limited. Therefore, he had also shown the shareholding of his immediate relatives under Promoter Group category.

Further, Ramavatar Makharia ceased to be the ED w.e.f. September 23, 2016. And hence re-classification was sought. |

| Lakshmi Devi Makharia | 0.0032 | ||||||

| Ramavatar Makharia | 0.0031 | ||||||

| 34. | October 05, 2018 | Kalpataru Power Transmission Limited[38] | Mohammed Kanga | PG | Individual | NIL | No control over the affairs of the Company. |

| Ishrat Imtiaz Kanga | |||||||

| Imran Imtiaz Kanga | |||||||

| Ismat Imtiaz Kanga | |||||||

| 35. | March 20, 2017 | Adani Ports and Special Economic Zone Limited[39] | Rakesh Namanlal Shah | Not specified | Individual | 0.06 | No control. |

| Pritiben Rakeshlal Shah | 0.02 | ||||||

| Bhavik Bharatbhai Shah | 0.00 | ||||||

| Surekha Bhavikbhai Shah | 0.00 | ||||||

| Vinod Sanghavi | 0.00 |

2.Applications rejected

| Sr.No | Date of approval | Name of the listed entity | Proposed outgoing promoter/ promoter group [name] | Whether promoter / promoter group (PG) | Promoter type (whether director or otherwise) (eg say if trust) | Shareholding at the time of re-classification (%) | Reason cited by the stock exchange, if any |

| 1. | March 18, 2020 | ABM Knowledgeware Limited[40] | Baburao Bhikunaik Rane | Promoter Group

|

Individual- immediate relative of Promoter KMP

|

0.02 | The Promoter seeking re-classification are holding more than 10% of the voting rights in ABM Knowledgeware Limited.

|

| Sunita Baburao Rane | 0.01 | ||||||

| Sharada Bhushan Rane | 0.01 |

3. Applications ongoing

| Sr.No | Date of making application | Name of the listed entity | Proposed outgoing promoter/ promoter group [name] | Whether promoter / promoter group (PG) | Promoter type (whether director or otherwise) (eg say if trust) | Shareholding at the time of re-classification (%) | Rationale given in the application for re-classification

|

| 1. | August 05, 2021 | Axis Bank Limited[41] | United India Insurance Company Limited | Promoter | Company | 0.03 | 1. Insignificant shareholding;

2. No representative on the board;

3. Have no control over the affairs of the Bank. |

| National Insurance Company Limited | 0.02 | ||||||

| New India Assurance Company Limited | 0.67 | ||||||

| General Insurance Corporation of India | 1.01 | ||||||

| 2. | July 12, 2021 | Lux Industries Limited[42] | Neha Poddar | PG | Individual- Immediate relative of Promoter | 0.17 | 1. Their name is included in PG by virtue of they being immediate relative of the Promoter.

2. They are financially independent and in no way are related to the business carried out by the Company. |

| Shilpa Agarwal Samriya | 0.17 | ||||||

| 3. | July 09, 2021 | JK Cement Limited[43] | Kavita Y Singhania | Promoter | Individual | 5.01 | On demise of her husband |

| 4. | June 29, 2021 | The Sandur Maganese & Iron Ores Limited[44] | Nazim Sheikh | PG

|

Managing Director | 0.10 | Resignation |

| U R Acharya | Director(Commercial) | 0.02 | |||||

| K Raman | CFO | 0.01 | |||||

| 5. | June 18, 2021 | Arvind Limited[45] | Samvegbhai Arvindbhai Lalbhai | None specified | Individual | NIL | No control |

| Anamikaben Samvegbhai Lalbhai | |||||||

| Saumya Samvegbhai Lalbhai | |||||||

| Snehalben Samvegbhai Lalbhai | |||||||

| Badlani Manini Rajiv | 0.00 | ||||||

| Arvind Farms Private Limited | Company | NIL | |||||

| Adore Investments Private Limited | |||||||

| Amardeep Holdings Private Limited | |||||||

| Samvegbhai Arvindbhai HUF | HUF | ||||||

| 6. | April 26, 2021 | Jindal Photo Limited[46] | Aakriti Ankit Aggarwal | None specified | Individual | NIL | No control over the affairs of the Company. |

| Aakriti Trust | Trust | ||||||

| 7. | April 12, 2021 | Strides Pharma Science Limited[47] | SeQuent Scientific Limited | PG | Immediate relative of Promoter KMP | NIL | Pursuant to SPA, the shares held by Stride were sold to an LLP. |

| 8. | April 10, 2021 | Sequent Scientific Limited[48] | Agnus Capital LLP | None specified | LLP | NIL | Pursuant to SPA |

| 9. | April 08, 2021 | Solara Active Pharma Sciences Limited[49] | SeQuent Scientific Limited | None specified | Company | 1.54 | Pursuant to SPA |

| 10. | May 25, 2021 | Shree Cement Limited[50] | Padma Devi Maheshwari | PG | Individual | 0.0017 | Neither the individual nor the person related to individual, holds more than 1% of the total voting rights. |

| 11. | March 09, 2021 | Shreyas Shipping and Logistics Limited[51] | Mahesh Sivaswamy | Promoter | Individual | NIL | 1. The Promoters had disposed off their entire stake during the period July 2018 to September 2018 by way of gift to other promoters;

2. No control over the affairs of the Company. |

| Mala Mahesh Iyer | |||||||

| Murli Mahesh | |||||||

| Mithila Mahesh | |||||||

| 12. | January 22, 2021 | Gati Limited[52] | Mahendra Kumar Agarwal | None specified | Individual | 1.29 | Erstwhile founder and MD of the Company, now has no control |

| TCI Finance Limited | Company | 0.82 | No control. | ||||

| Mahendra Investment Advisors Private Limited | 0.12 | ||||||

| Mahendra Kumar Agarwal & Sons HUF | HUF | 0.45 | |||||

| Bunny Investments & Finance Private Limited | Company | 0.22 | |||||

| Jubilee Commercial & Trading Private Limited | 0.12 | ||||||

| 13. | January 06, 2021 | Integrated Capital Services Limited[53] | Ambarish Chatterjee | Promoter | Individual | 0.07 | 1. They were the shareholders of Deora Associates Private Limited which merged with Integrated Capital Services Limited w.e.f. September 26, 2018. Pursuant to the merger, the shareholders of Deora Associates Private Limited became shareholders of Integrated Capital Services Limited.

2. They became Promoters by virtue of the merger and have no control over the affairs. |

| Jai Rani Deora | 1.15 | ||||||

| Arun Deora[54] | 1.12 | ||||||

| Rajeev Kumar Deora[55] | 6.74 | ||||||

| Brijender Bhushan Deora[56] | 0.982 |

Note:

- The percentage of shareholding, wherever shown as 0.00% would mean that shares are held but since the amount of shares held is negligible vis-à-vis the total paid-up share capital, the percentage is 0.00;

- NIL shareholding means no shares are held in the Company.

Reference to our other articles on similar topic:

- https://vinodkothari.com/2020/12/sebi-proposes-liberal-provisions-for-promoter-reclassification/

- https://vinodkothari.com/2021/06/sebi-revisits-the-concept-of-promoter/

[1] https://www.bseindia.com/xml-data/corpfiling/AttachHis/1224bd10-df95-458f-a82a-a9f7229d36bb.pdf

[2] https://www.sebi.gov.in/sebi_data/attachdocs/mar-2019/1553000134426.pdf

[3] https://www.bseindia.com/xml-data/corpfiling/AttachHis/fdcba980-f25c-4483-a710-d451cfb08a08.pdf

[4] https://www.bseindia.com/xml-data/corpfiling/AttachHis/16958972-8291-4026-a7df-1ef880e5a231.pdf

[5] Wife of Late Mr. Ashok Kumar Jain, former Promoter of the Company.

[6] https://hcgel.com/wp-content/uploads/2021/04/SE-intimation-Promoter-reclassification-06-April-2021.pdf

[7] https://www.bseindia.com/xml-data/corpfiling/AttachHis/0e9eb184-b8e9-4958-b20d-2ef8b216340c.pdf

[8] https://www.aarti-industries.com/Upload/PDF/approval-of-reclassification.pdf

[9] https://www.bseindia.com/xml-data/corpfiling/AttachHis/0e924e6e-2018-40a5-afa2-9882e984ddfb.pdf

[10] https://www.bseindia.com/xml-data/corpfiling/AttachHis/fe5eeda8-626a-49d3-a21e-4923e8a84636.pdf

[11] https://www.bseindia.com/xml-data/corpfiling/AttachHis/02390e16-475f-4941-99f3-d3a922888112.pdf

[12] https://www.bseindia.com/xml-data/corpfiling/AttachHis/491066f3-a579-4ea1-a72d-4e6ce8564643.pdf

[13] https://www.mindtree.com/sites/default/files/2020-12/235IntimationonReclassificationapplicationsapproval.pdf

[15] https://www.birlasoft.com/sites/default/files/resources/downloads/investors/intimation-of-the-approval-of-the-stock-exchanges-for-reclassification-of-promoters.pdf

[16] http://www.ruchisoya.com/stock_exchange/Approvals_form_BSE___NSE_for_Promoters_classification__1_.pdf

[17] http://www.dfmfoods.com/download/investors/Intimation-of-Approval-of-Stock_Exchanges-for-Reclassification-of-Outgoing-Promoters.pdf

[18] https://www.bseindia.com/xml-data/corpfiling/AttachHis/66abdb7d-4257-478f-9dc8-ee38315844b1.pdf

[19] https://www.bseindia.com/xml-data/corpfiling/AttachHis/ff9326d6-c22d-4a06-9dc3-dc2f628dee76.pdf

[20] https://www.tfciltd.com/public/investor/160224589357-TFCIReclassApproval290720.pdf

[22] https://www.andhrapaper.com/uploads/investors/1626162587ApprovalsfromSEforreclassificationofPromoters.pdf

[23] https://www.bseindia.com/xml-data/corpfiling/AttachHis/ece3265f-9040-4b46-b2a2-33afd5890b8f.pdf

[24] https://www.valueresearchonline.com/downloads/stock-announcement/D57DFE0F-AEFD-40AD-89DC-64B185E5F8AD/

[25] https://www.yesbank.in/pdf/promoter_reclassification_stock_exchange_approval_pdf

[26] https://www.bseindia.com/xml-data/corpfiling/AttachHis/56b8219e-d087-4739-bda1-5397a359e058.pdf

[27] https://www.bseindia.com/xml-data/corpfiling/AttachHis/3cfdd742-3061-44cc-a3c6-e332c41bb130.pdf

[28] https://www.bseindia.com/xml-data/corpfiling/AttachHis/7307deb5-0f51-48d0-9b4a-f546c525d863.pdf

[29] https://www.sudarshan.com/perch/resources/sudarshan-approval-to-application-for-promoters-reclassification-klr-group.pdf

[30] https://www.bseindia.com/xml-data/corpfiling/AttachHis/e40baa8a-828d-41fe-b4f3-7af24e64c7b9.pdf

[31] https://www.bseindia.com/xml-data/corpfiling/AttachHis/abac5973-e866-4a5d-8cf8-68f462ded13e.pdf

[32] https://redingtongroup.com/wp-content/uploads/2019/09/HarrowReclassificationapproval.pdf

[33] http://www.indiagelatine.com/financial/Reclassification%20approval%20by%20BSE_21.11.pdf

[34] https://www.bseindia.com/xml-data/corpfiling/CorpAttachment/2018/10/d9b5e05c-3085-4155-b315-4edcdc0fd1c1.pdf

[35] https://www.bseindia.com/xml-data/corpfiling/CorpAttachment/2018/9/876a9088-9393-4e2e-9b5d-d09ddd3f8ca4.pdf

[36] https://www.eslsteel.com/investor-relations/pdf/lodr-26sep18a.pdf

[37] https://www.centurytextind.com/assets/pdf/news-and-events/reclassification-under-regulation-sebi.pdf

[38] https://www.bseindia.com/xml-data/corpfiling/CorpAttachment/2018/10/da115de5-ff37-420f-8975-e3bd10d73753.PDF

[39] https://www.adaniports.com/-/media/Project/Ports/Investor/corporate-governance/Corporate-Announcement/other-intimation/11420032017Update-on-reclassification-for-promoter-group.pdf?la=en

[40] https://www.valueresearchonline.com/downloads/stock-announcement/416C36C1-0DA3-4A5A-BDE8-BB60AEA1FD05/

[41]https://www.axisbank.com/docs/default-source/corporate-announcements/material-events-disclosed-under-sebi-(listing-obligations-and-disclosure-requirements)-regulations-2015/2020-2021/submission-of-application-for-promoter-reclassification-05-08-2021.pdf

[42] https://www.bseindia.com/xml-data/corpfiling/AttachHis/f32e9326-71bb-4bbe-940a-1e2dda2c5ed5.pdf

[43] https://www.bseindia.com/xml-data/corpfiling/AttachLive/43f432f7-a179-4fc3-8c45-fe02834f6e06.pdf

[44] https://www.sandurgroup.com/doc/21-06-29-Ltr2Bse-Intimation-under-Reg-30-and-31A-BM-reclassification-from-Promoter-to-Public.pdf

[45] https://www.moneycontrol.com/livefeed_pdf/Jun2021/ff77f16f-f738-4da1-80ed-8f09b8144312.pdf

[46] https://www.bseindia.com/xml-data/corpfiling/AttachHis/fb767238-c630-4908-bb6a-220c9e8abec8.pdf

[47] https://www.bseindia.com/xml-data/corpfiling/AttachHis/234a75e4-8668-4cc0-be1b-54de843a9447.pdf

[48] https://www.bseindia.com/xml-data/corpfiling/AttachHis/3259619c-6041-4ebf-aa06-eda0173eb68f.pdf

[49] https://www.bseindia.com/xml-data/corpfiling/AttachHis/295e848a-1943-48d5-ba67-3fa699d2e5b6.pdf

[50] https://www.bseindia.com/xml-data/corpfiling/AttachHis/3148e1be-41fe-44ac-971d-e65f36221854.pdf

[51] https://www.bseindia.com/xml-data/corpfiling/AttachHis/ecae4e2e-77cc-4b1b-bb2f-5485af0af388.pdf

[52] https://www.bseindia.com/xml-data/corpfiling/AttachHis/f67f33ba-8c77-4458-b0ae-6160022abdc1.pdf

[53] https://www.bseindia.com/xml-data/corpfiling/AttachHis/bbda8d1c-e076-4fe4-9a3b-b91da3707016.pdf

[54] Held office as a NED from July 25, 2007 and resigned on October 12, 2018.

[55] NRI and permanently settled in Australia, not connected directly / indirectly.

[56] Held office as a NED and Chairman from July 25, 2007 and resigned from office on June 19, 2020.

CG’s Power to Relax MPS Requirements

– An Unbridled Power?

Pammy Jaiswal, Partner and Sachin Sharma, Executive (corplaw@vinodkothari.com)

Background

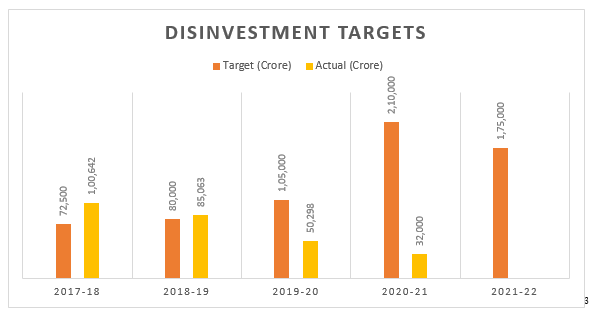

The government has been undertaking disinvestment exercise in PSUs since 1991[1] with an intent to overcome various shortcomings including lack of proper management as well as over capitalisation[2]. This exercise has been considered effective to reduce the fiscal burden and raise money to meet public needs and at the same time. Through disinvestment, proceeds are channelized in various ways to strengthen the Indian economy. Since disinvestment gives out a larger share of PSU ownership in the hands of the private sector as well as larger section of the public, it sets the groundwork for India’s firm capital market.

The targets of disinvestment are set in every Union Budget, however the actual level of disinvestment varies from the targets set every year; and while there are various methods of disinvestment like Offer for Sale (OFS), Strategic Sale, IPO, FPO etc., however Offer for Sale (OFS) of shares are extensively used by the Government.

Driven by the intention to involve the private sector and global investors to bring in efficiency and provide much needed cash to help revive the economy hit sharply by the Covid-19 pandemic, the new Public Sector Enterprise (“PSE”) Policy has been unveiled. The new PSE Policy provides a clear roadmap for disinvestment in all non-strategic and strategic sectors and provides that the bare minimum CPSEs will be held on to, and the rest will be privatised. This policy marks a huge shift in the government attitude towards privatisation of state-owned companies.

At this juncture, it is important to note that in addition to the reasons and/ or motivation for disinvestment mentioned above, another reason would be compliance/ alignment with the MPS requirements under Securities Contracts (Regulation) Rules, 1957(“SCR Rules”). Regulation 19A of “SCR Rules”), requires that a listed entity must have at least 25% public shareholding[4] so as to prevent concentration of shares in few hands and enable wider participation of public. Minimum Public Shareholding (MPS) requirement was introduced in the year 2010[5] for listed public sector companies, every listed PSU were required to comply with 10% MPS requirement within timeframe of 3 years.

Extended timelines to comply with MPS for listed PSUs

With the increase in threshold from 10% to 25% in August, 2014, these companies were given 3 years to comply with the 25% MPS requirement, which later got increased to 4 years in July, 2017.

Considering the fact that PSUs were facing difficulty in diluting their shareholdings and they could not comply with the said requirement with given timeframe, the Central Government (CG) allowed fresh timeline of 2 years in August, 2018 i.e. till August 2, 2020. Later, considering the unfavourable market conditions due to Covid-19 outbreak across the world, the Ministry of Finance vide its notification dated July 31, 2020 again extended the time period by 1 year i.e. till August 2, 2021.

Further, SEBI vide its circulars dated November 30, 2015 and February 22, 2018 had prescribed the manner for achieving MPS to comply with the said requirements.

In order to address the cases of non-compliance with MPS norms, structured fine for every day of non-compliance has been prescribed by SEBI vide its circular dated October 10, 2017. Other penalties include freezing of promoter shareholding and compulsory delisting.

Now, Ministry of Finance(MoF) vide notification dated 30th July, 2021 has inserted new sub-rule i.e. sub-rule 6 in Rule 19A in the SCR Rules which has empowered the CG to exempt any listed public sector company in the public interest from complying with any or all of the provisions of this Rule, that is aimed at increasing MPS to 25%.

Probable impact of relaxation

- Optimum Price Discovery

As observed from the foregoing paragraphs, it is clear that the Government has been setting the blue print to privatise the PSUs as a part of its PSE Policy every year. However, looking at the current market situation, where the real price discovery is highly affected due to the COVID era, it seems that the current time may not be smooth and effective for the Government to go on a disinvestment spree.

Accordingly, to pave a concrete path for the achieving the desired intent through disinvestment, the power has now been permanently reserved by the Central Government to relax the MPS requirements in case of listed PSUs. The said power can be instrumental in getting optimum price discovery as well as adequate value for their existing investments held in the strategic and non-strategic sectors.

- Unbridled power to offset a level playing field

Maintenance of a minimum public float helps to attract Indian as well foreign investors. Further, more importantly, while the norms for MPS is for any listed company, the power to relax the MPS requirements have been brought for listed PSUs only. Moreover, the amendment brought this time, unlike the previous amendments, is unbridled. Complying with the MPS requirements is one of the most fundamental requirements that SEBI has laid down so as to help in strengthening the capital market in the long run. However, granting the power to the Central Government to relax the same does not allow a level playing field to all the listed entities.

Conclusion

In the last fiscal, the government has sold its stake via seven offer for sale (OFS) transactions and also tendered shares in buyback offerings by a similar number of CPSEs which includes selling its 15% stake in Rail Vikas Nigam Ltd (PSU) through an Offer for Sale (OFS), reducing the its stake in that PSU to 75.68%. Also PSUs such as Mazagon Dock Shipbuilders Limited and Indian Railway Finance Corporation Limited came out with Initial Public Offerings (IPO).

Further, in last week of July this year, CG has also opened the offer for sale (OFS) for its 8% stake in Housing and Urban Development Corporation (HUDCO) Limited. LIC’s IPO is also in pipeline for the current fiscal. The privatisation of PSUs such as Air India, BPCL, Pawan Hans, BEML, NINL and Shipping Corp has also been planned to be done in the current fiscal[6].

According to the PSUs shareholding data provided by bsepsu.com, there are a total of 68 listed CPSEs in India out of which 24 of them have less than 25% public shareholding as on July 31, 2021.

As discussed above, while the CG has been empowered to relax the MPS requirement and the said list of exempted PSUs may be rolled out soon, however, being an absolute power that has been given, SEBI has given an upper hand to the CG to waive off an essential condition for listed PSUs.

[1] http://www.bsepsu.com/historical-disinvestment.asp

[2] http://www.bsepsu.com/importance-disinvestment.asp

[3] https://www.indiabudget.gov.in/doc/Budget_Speech.pdf

[4] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/jun-2021/1624346958513.pdf#page=1&zoom=page-width,-16,792

[5] https://egazette.nic.in/WriteReadData/2010/E_440_2011_011.pdf

[6] http://www.bsepsu.com/bsepsu_Articles.asp

Read our other articles on the topic here –

FAQs on recent amendments under the Listing Regulations

Loading…

Loading…

Other write-ups on the subject matter:

1.Recent amendments relating to independent directors

2.SEBI notifies substantial amendments in Listing Regulations

3.New year brings stricter norms for appointment of IDs

4. LODR changes on Independent Directors – Things to do before 1st Jan., 2022