According to Section 2(31) of the Companies Act, 2013 ‘Deposit’ includes any receipt of money by way of deposit or loan or in any other form by a company, but does not include such categories of amount as may be prescribed in consultation with the Reserve Bank of India. The exclusions are cited in Rule 2 (1) (c) of Companies (Acceptance of Deposits) Rules, 2014 which are applicable to public and private companies.

Rule 2 (1) (c) (viii) of Deposit rules excludes amounts received from a person who, at the time of the receipt of the amount, was a director of the company or a relative of the director of the private company, provided that the person declares that the amount is his own fund and not borrowed. The private company is required to disclose the details of money so accepted in the Board’s report.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-05-06 16:53:472022-05-06 16:58:16Whether a private company can accept deposits from HUF?

The Report of the Company Law Committee – 2022 (“CLC Report”) has proposed various important amendments to the existing Companies Act, 2013 (“the Act”) and some in the Limited Liability Partnership Act, 2008 (“LLP Act”). The recommendations touch a wide array of elements under the Act – be it the association/ cooling period of directors, auditors, KMPs, etc. or corporate actions such as mergers, transfer of unclaimed monies to IEPF on account of buyback etc., de-clogging of NCLTs for restoration of company’s name after having been dissolved as defunct, setting up of specialized company law Benches of NCLT for dealing with matters of economic importance such as corporate restructuring, and specialized IBC cases or cases involving public interest. The recommendations also seek restoration of some meaningful provisions of the erstwhile CA 1956.While some suggestions pertain to ease of compliances and moving towards digitization with respect to certain compliances of a company, others pertain to building a robust corporate governance framework including alignment of the law with various provisions with SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“Listing Regulations”). This is the 3rd CLC Report in the series of recommending changes to the 2013 Act, several reforms in the Act had been suggested in past by the CLC Report 2016, Committee to Review Offences Under Act of 2018 and CLC Report 2019. A brief summary of the issues under hand and the recommendations along with proposed amendments have been provided for as an Annexure to the CLC Report itself, and therefore, we find it useful to discuss only some of the recommendations which require analysis. Applicability The Committee report, if accepted by the Government, will potentially lead to an Amendment Bill, and therefore, there will be an enactment by a law of the Parliament. Once passed, it is expected that several of the amendments will require extensive rule-making, as there are references in several provisions to “class or classes of companies”. Thus, while we get a broader view of the direction into which the law will move, but as they say, the devil lies in the detail. We will get to know the details, hopefully divine and not devilish, only when the Bill is available for review.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-04-15 14:45:482022-08-29 19:05:09CLC recommends major reforms in corporate laws for ease of doing business

Regulation of remuneration to managerial personnel (viz., directors, managing director, manager) (“managerial remuneration”) is an important aspect of corporate governance. Sections 197 of the Companies Act, 2013 (“Act”) read with Schedule V impose limits on managerial remuneration. Additionally, Section 197 (12) read with Rule 5 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 requires certain disclosure of managerial remuneration as a part of the board report, in particular, the ratio of remuneration of each director to the median remuneration of employees; percentage increase of remuneration of each director, CEO, CFO, CS or manager in a financial year; comparison of percentile increase in managerial remuneration with percentile increase in remuneration of employees other than managerial personnel etc.

Akin to India, laws globally also keep checks over managerial remuneration. Although laws in countries like the US, UK, Switzerland, etc. do not require approval from any government authorities, suitable control is ensured through shareholders, or appropriate disclosures. There have been corporate disputes around managerial remuneration in the UK where stockholders have challenged payments made to the CEO, having been paid large salaries and bonuses [Feuer v. Redstone][1]. The global practices of disclosing managerial remuneration to the shareholders has been discussed in the later part of this article.

The same has a potential of conflict of interests, since the matter relates to the direct pecuniary interest of the decision-makers of the company. In view of the same, while limits are provided in the Act itself, a partial control is being exercised on the matter through the requirement of shareholders’ approval (earlier, Central Government’s approval was required in case of payment of managerial remuneration in excess of the specified limits under Section 197, the same has now been omitted).

In this article, the authors attempt to demystify some questions revolving around the concept of managerial remuneration, as follows –

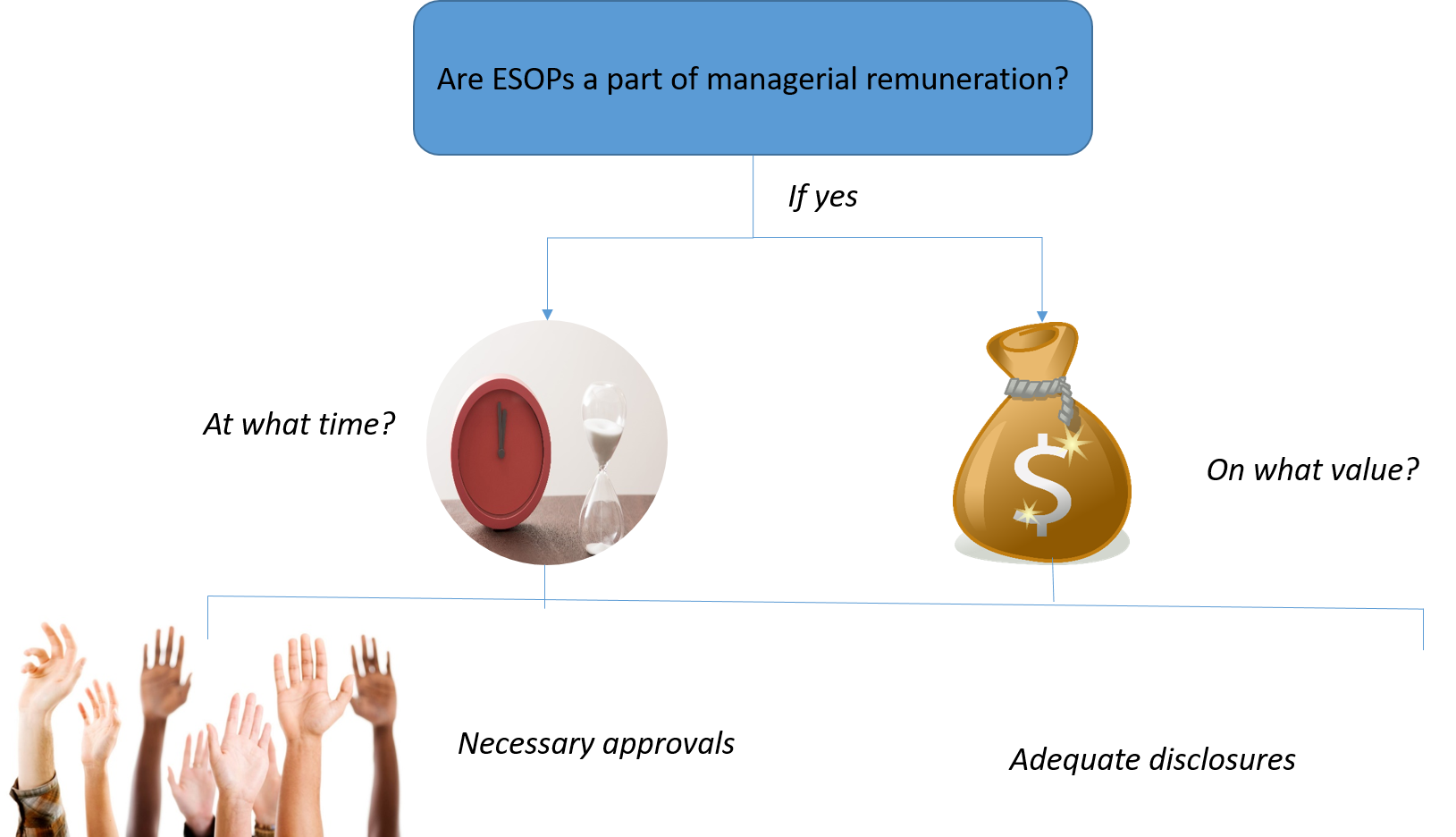

Whether ESOPs are considered a part of managerial remuneration?

If yes, at what point of time should the ESOPs be considered a part of remuneration for calculation of limits applicable to the payment of managerial remuneration?

Since the ESOPs do not involve any actual cash outflows from the company, what should be the value at which the ESOPs shall be considered a part of the remuneration?

In case the managerial remuneration of a managerial personnel exceeds the specified limits, as a consequence of including ESOPs as part of the remuneration, when and how should the company obtain the approval of the shareholders for the same?

While we focus on throwing light on the treatment of ESOPs as managerial remuneration from the viewpoint of the statutory limits and approval requirements in terms of the Act and the Listing Regulations[2],the taxation and accounting aspects of the ESOPs are also discussed briefly in this article.

Granting ESOPs to managerial personnel

There exists a nexus between compensation and motivation. The corporates appreciate this fact and have taken progressive steps to upheave the same. One move towards this is the Employee Stock Option Purchase or ESOPs. The ESOPs are based on the principle that an adequately compensated employee would work diligently and help in wealth creation for the stakeholders which in turn would help the Company to grow. ESOPs embrace this consensual approach. Stock Options or ESOPs as we call it, entitles the holder of the option with a right to convert such options into stock of the company at a future date.

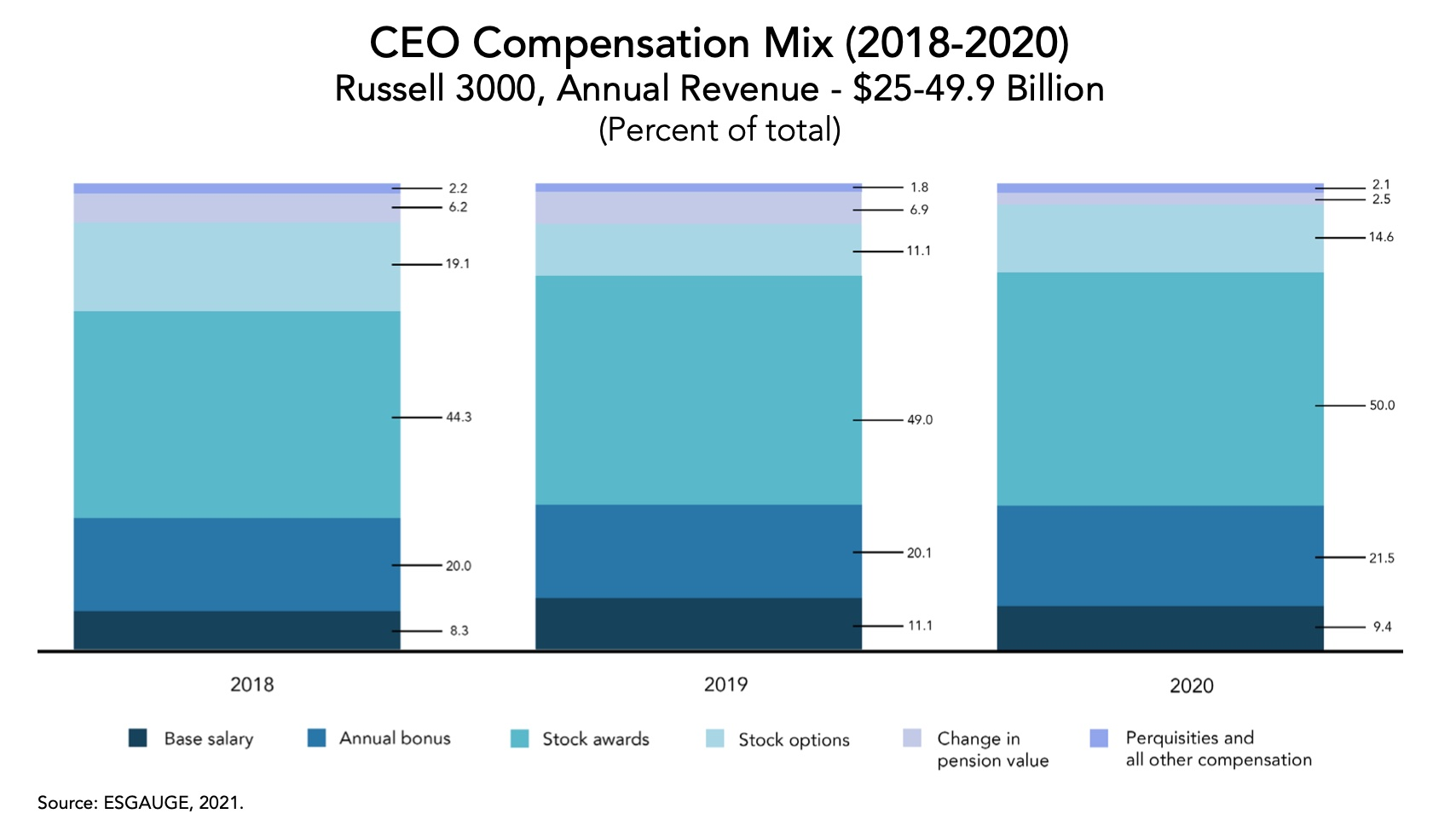

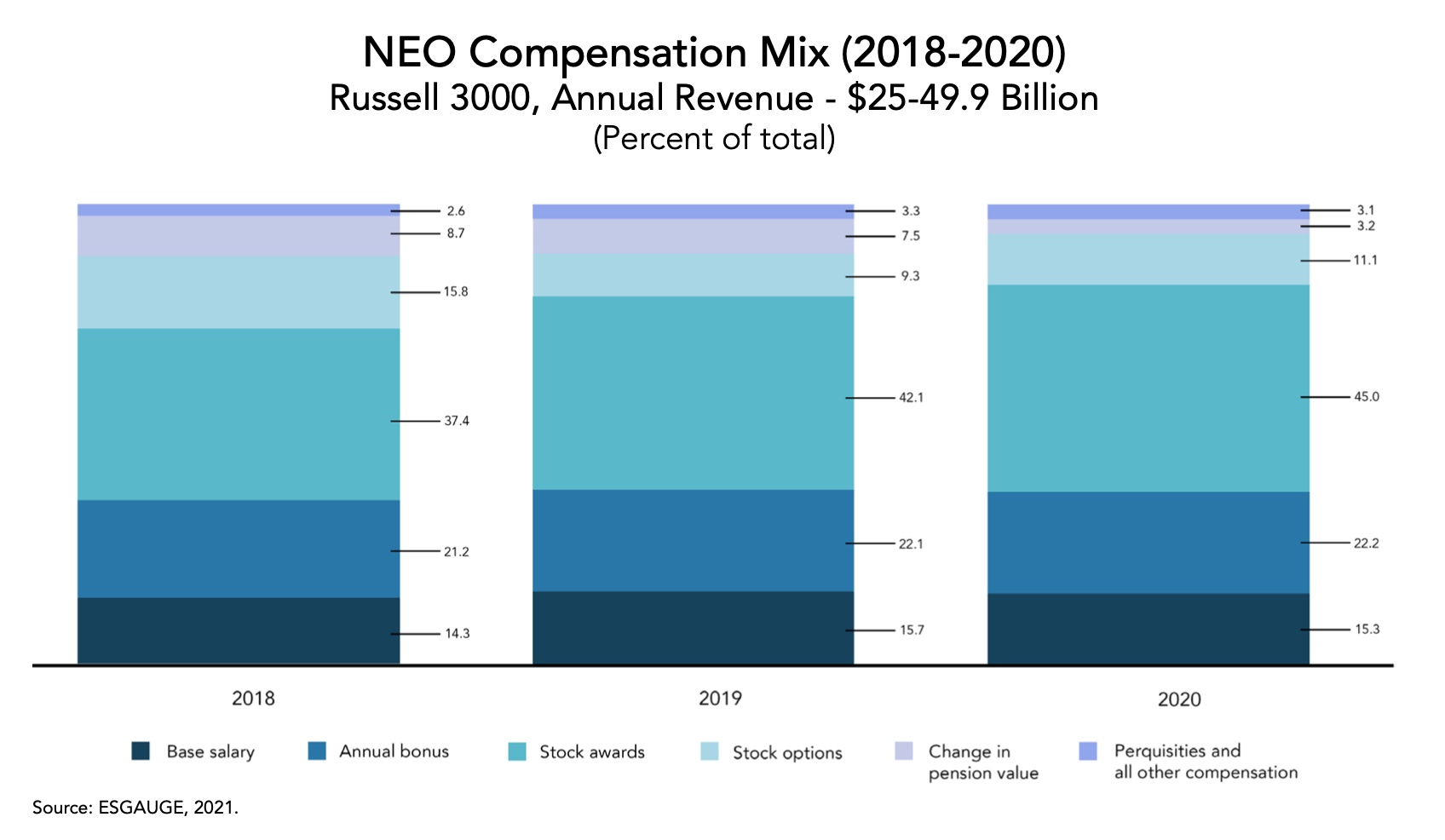

ESOPs are frequently used as a measure to reward employees, including directors and other key managerial personnel. Dylon Minor, in his CEOs with Lots of Stock Options Are More Likely to Break Laws, published by Harvard Law Review, states that “For many executives, the bulk of their compensation comes in the form of equity compensation, which includes both stock options and stock awards”. The figures show the proportion of stock options and stock awards along with other components of compensation paid to chief executive officers (CEO) and non-executive officers (NEO) of the top companies included under the Russell 3000 Index. In the year 2020, around 64.6% of CEO’s compensation consisted of stock options and stock awards, whereas, the same constituted about 56% of the compensation mix of the NEOs. In view of the significance of managerial remuneration in corporate governance of a company and the remarkable magnitude of stock options, it becomes crucial to identify its impact on the managerial remuneration, so as to ensure that proper approvals and disclosures are in place with respect to such stock options.

Treating ESOPs as managerial remuneration

Remuneration as defined under 2(78) of the Companies Act, 2013 means;

“any money or its equivalentgiven or passed to any person for services rendered by him and includes perquisites as defined under the Income-tax Act, 1961.”

Further, in terms of clause (vi) of Section 17(2) of the Income Tax Act, 1961 (“IT Act”), perquisites includes – (vi) the value of any specified security or sweat equity shares allotted or transferred, directly or indirectly, by the employer, or former employer, free of cost or at concessional rate to the assessee.

Explanation.—For the purposes of this sub-clause,—

(a) “specified security” means the securities as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956) and, where employees’ stock option has been granted under any plan or scheme therefore, includes the securities offered under such plan or scheme.

Further, Schedule V of the Act requires some disclosures to be made in the “corporate governance” part of the board’s report, relating to the managerial remuneration such as –

“(i) all elements of remuneration package such as salary, benefits, bonuses, stock options, pension, etc., of all the directors;

XX

(iv) stock option details, if any, and whether the same has been issued at a discount as well as the period over which accrued and over which is exercisable.”

Similar disclosures are required to be made in the “corporate governance” section of the Annual Report of a listed company, in terms of Schedule V of the Listing Regulations.

These disclosure requirements establish beyond doubt that the ESOPs are included under the managerial remuneration, and therefore, the provisions, as applicable to the other components of managerial remuneration, are applicable to ESOPs mutatis mutandis.

The above explains that ESOPs are certainly treated as part of remuneration. The rationale for the same is based on the concept of Cost to Company (“CTC”). One may question as to how the same can be treated as cost to the company, since there is no explicit payout by the company for ESOPs. Let us understand the same with the help of the table below –

Price at which ESOPs are granted

Cost to the company

Benefit to the employees

Market price on the date of grant

Intrinsic value – Nil Time value – difference between market price on the date of exercise and on the date of grant

The employee gets a right to obtain equity shares of the company at a later date, without paying the premium accrued on the time value of the equity shares. The employee has the right to the upside in the price of the shares, without getting exposed to the risk of downside movement in prices of the shares at the time of exercise

Market price on the date of exercise

Nil

Such options are as good as purchase of shares from the market directly. There is no motivation to the employees in getting such options and therefore, completely redundant and practically ruled out.

Any price lower than the market price on the date of grant

Intrinsic value – difference between market price on the date of grant and exercise price offered by the company Time value – difference between market price on the date of exercise and on the date of grant

The employee gets a right to obtain equity shares of the company at a later date, without paying the differential value between the actual market price on the date of exercise and the price at which the options have been exercised to the employee.

The company, by providing stock options that permit an employee to obtain equity shares of the company at a particular price, forgoes its claim to a higher value, which is no different from an expense. Given the fact that the options will be exercised only where the exercise price is lower than the prevailing fair value of the share, the exercise reduces the market capitalization of the company on the date of actual exercise of the option by the employee. Thereby, there is a loss in shareholder value, and hence, there is cost to the company.

In view of the arguments above, we have no doubt in holding that ESOPs are as much a cost to a company as any other pay-outs given to managerial personnel. Therefore, to the question “whether ESOPs may be considered a part of the managerial remuneration”, the answer is certainly in the affirmative.

That brings us to the question of “when” and “how much” of ESOPs are to be treated as managerial remuneration. We approach this question with prefatory remarks such as, the various stages of ESOP cycle, valuation of options, accounting and tax treatment of ESOPs, etc.

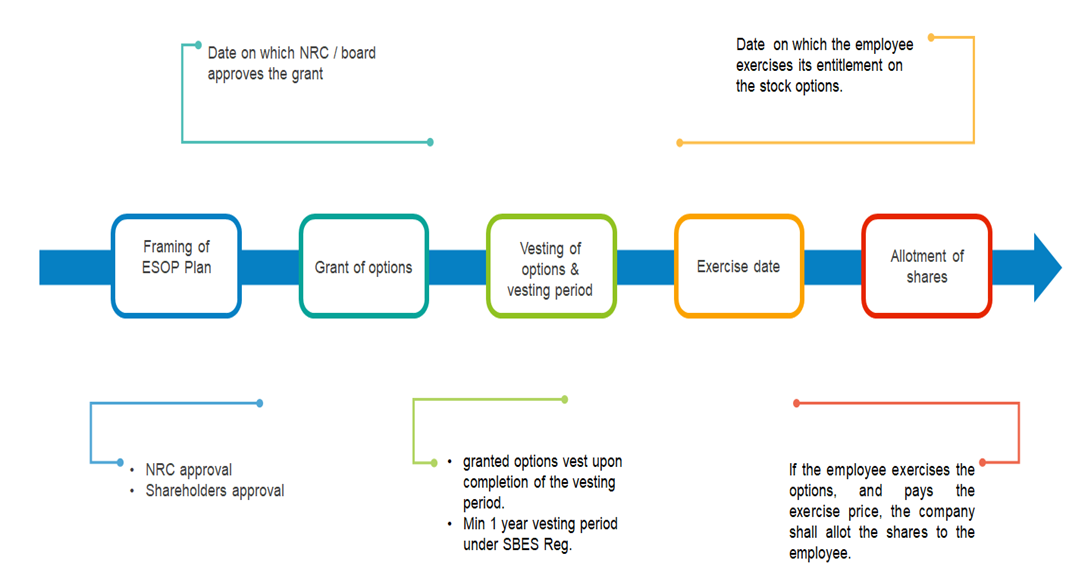

Stages of ESOP cycle

The whole cycle of ESOP passes through a series of stages as discussed below –

The different stages of the ESOP cycle results in varying practices in treating the same as part of managerial remuneration, which we will discuss in the later part of this article.

Valuation for ESOPs

Valuation for ESOPs can be done by following either of the two methods:

Intrinsic Value Method (IVM), or

Fair Value Method(FVM)

Valuation under IVM:

Intrinsic Value, in case of a listed company, is the amount by which the quoted market price of the underlying share exceeds the exercise price of an option or the value of the underlying share determined by an independent valuer in case of an unlisted company, exceeds the exercise price of an option.

For example, an option with an exercise price of INR 100 on an equity share whose current quoted market price is INR 125, has an intrinsic value of INR 25 per share on the date of its valuation.

Accordingly, if the market price of the underlying share at the grant date is the same as the exercise price, then the intrinsic value of the options is Nil.

Ind AS- 102 (“Standard”) also provides for valuation under IVM, in those exceptional cases where fair value of the equity instruments cannot be estimated reliably (Para 24). However, Income-tax law is concerned with intrinsic value only, since income tax law taxes the option as a perquisite only on the exercise date. Given the fact on the exercise date, the time value is always zero, whatever value the option has is its intrinsic value only.

Valuation under FVM:

In terms of Ind AS 102, in the books of the company, ESOPs are to be recognized at an estimated fair value of the options from the date of grant of options, spread over the vesting period (if any). Fair value of an ESOP is estimated using an option-pricing model like the Black-Scholes or binomial model on the date of grant. In the case of listed stocks, Black Scholes method is the most commonly used model. The model takes into consideration the exercise price of the option, life of the option, current price of underlying shares, risk-free interest rate, expected volatility of the share, expected dividend and the tenure at the end of which the options vest (Para B6 of Ind AS 102).

Recognising ESOPs as a part of Managerial Remuneration:

While we understand that ESOPs are to be treated as a part of managerial remuneration, the question is, at what stage, and with what valuation. There are possibly three approaches to the regulation of managerial remuneration:

Aligning the treatment with the taxability of perquisite

Aligning the treatment with debit in company’s books under accounting standards

If neither of these approaches give a satisfactory result, thinking of a midway between the two approaches above.

We discuss below why approach (a) and (b) both lead us to incoherent results as far as regulation of managerial remuneration is concerned.

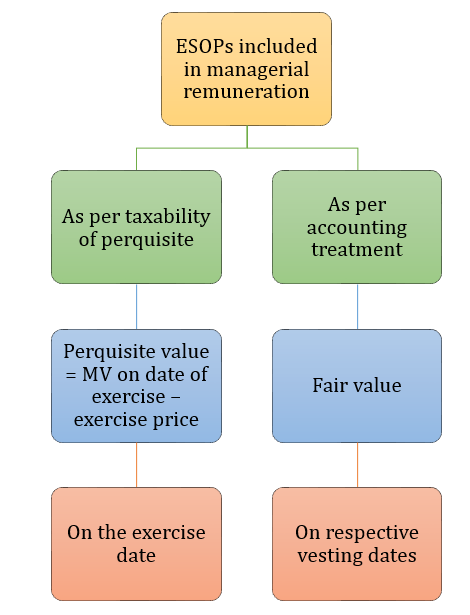

A. Recognition of ESOPs based on taxability of perquisite

The tax treatment of ESOPs needs to be examined from the point of view of the employer as well as the employee. In the hands of the employer/ company, the cost of the options entails a tax deduction, and the benefits are taxable in the hands of the employee as perquisites.

Since the definition of “remuneration” under section 2(78) of the Companies Act refers to perquisites as defined under Income-tax Act, the most obvious approach, which seems very tempting to accept, is that ESOPs become a part of remuneration when they become taxable, and based on how much value they become taxable. Thus, the timing of treating the ESOPs is the time of exercise, and the amount at which it is taken as remuneration is the difference between the fair value at the time of exercise, and the exercise price.

While for the purposes of the discussion contained herein, the taxability in the hands of the employee is relevant and deserves consideration, we have also included the tax deductibility of the ESOPs in the hands of the company, for a comprehensive understanding.

Tax deduction in the hands of the company

As far as the tax deductibility of the ESOP expense in the hands of the company is concerned, the same is deductible as debited in accordance with generally accepted accounting principles. As the cost of the ESOPs is an employee benefit expense, it is to be considered under the generic provisions under Section 37 (1) of the IT Act.

The Mumbai ITAT, in the matter of Unnikrishnan V S Vs. Income Tax Officer, International Taxation 4(3)(1), Mumbai [ITA Nos. 1200 and 1201/Mum/2018 ] has held that while the ESOPs are taxable at the time of exercise of the options by the employees, the benefits accrue from the date of grant of options itself and during the tenure of vesting period. The learned Tribunal stated that –

“The character of income may be inchoate at that stage but certainly what is being sought to be taxed now, on account of the specific provision under section 17(2)(vi), is a fruit of services rendered much earlier and the benefit, which has now become a taxable income, accrued to the assessee in 2007. All that section 17(2)(vi) decides is the timing of an income, but it does not dilute or negate the fact that the benefit, in which is being sought to be taxed, had arisen much earlier i.e. at the point of time when the ESOP rights were granted.” [Emphasis supplied]

Tax deduction in the hands of the employee

As mentioned above, ESOPs are identified as perquisites for the provisions of IT Act, and therefore, become a part of the remuneration on the exercise date at a value which is the exercise price as reduced from the Fair Market Value (FMV) of the underlying equity shares. FMV is calculated as per Rule 11UA of the Income Tax Rules, 1962. In the case of listed stocks, the listed price is the fair market value. Further, capital gains may arise at the time of sale of shares by the employee, being the difference between the FMV on exercise date, and the actual realization upon sale of shares.

Now let us take help of an example to understand the implications if ESOPs are taken as part of managerial remuneration from the taxation perspective as discussed above.

Company A grants 5,00,000 options to Mr. X, the Managing Director, with the following information:

Grant date

Vesting Date

Exercise date

Market value

100

150

200

Exercise price

50

50

50

Date

1st April, 2022

1st April, 2025

1st April, 2027

Value of the option

Fair value (as computed by option pricing model)

Say, 80

Say, 140

150

Time value (diff. Between fair value and intrinsic value)

30

40

0

Intrinsic value (market value – exercise price)

50

100

150

In the instant case, the perquisite value to be included in the remuneration will be Rs. (200-50), i.e. Rs. 150. The same, being exercised in April, 2027, shall form part of the remuneration of Mr X in the FY 2027-28 and therefore, the same has to be calculated as a percentage of the net profits for FY 2027-28, to identify whether the remuneration exceeds the limits given under Section 197 of the Act.

Therefore, going by the income-tax approach, the entire value of Rs. 150 will be treated as managerial remuneration at the time of exercise. One may note that there is a huge difference between the accounting treatment, accounting cost is Rs. 80, spread over the vesting period.

However, there are several issues with treating ESOPs based on taxability for the purpose of regulation of managerial remuneration.

Issues with recognition of managerial remuneration as per taxability approach

The ESOPs relate to a period of time over which the managerial personnel has rendered services to the company. Taxability, however, arises at a point of time.

There may be instances where the person to whom options were granted, being a managerial personnel, does not remain a managerial personnel or even in the payrolls of the company at the time of exercise of options.

This approach leads to a complete departure between the CTC as debited by the company, and its treatment as a part of managerial remuneration.

It has to be understood that the ESOPs are a cumulative payment for the services rendered over a period of years, and not solely related to the year of exercise. This is also substantiated by the ITAT in the matter of Unnikrishnan V S (supra). Recognising ESOPs as part of managerial remuneration as per its taxability in the hands of the recipient will lead to a situation where the ESOP, though pertaining to the services rendered for a cumulative set of financial years, only be considered for the calculation of managerial remuneration for a particular year. This approach therefore is inconsistent and does not seem reasonable.

B. Recognition of ESOPs based on the accounting treatment of ESOPs

Under the provisions of Ind AS- 102, ESOPs shall be recognised by the company in its books, on i.) the grant date (where options vest immediately) or ii.) during the vesting period (where there is a vesting period) at the fair value of the options.

This standard states that in case of equity settled options, the company shall recognise the services received by it from an employee on the date of grant of options to the employee, till the date of vesting. There is, accordingly, a debit to employee benefit expense, and credit to equity by way of creation of a reserve in this regard.

The relevant para(s) of the Standard has been produced herein below:

10 For equity-settled share-based payment transactions, the entity shall measure the goods or services received, and the corresponding increase in equity, directly, at the fair value of the goods or services received, unless that fair value cannot be estimated reliably. If the entity cannot estimate reliably the fair value of the goods or services received, the entity shall measure their value, and the corresponding increase in equity, indirectly, by reference to the fair value of the equity instruments granted.

11 To apply the requirements of paragraph 10 to transactions with employees and others providing similar services, the entity shall measure the fair value of the services received by reference to the fair value of the equity instruments granted, because typically it is not possible to estimate reliably the fair value of the services received, as explained in paragraph 12. The fair value of those equity instruments shall be measured at grant date.

The above case refers to recognising ESOPs as CTC on grant date. However, where there is a predetermined vesting period, the same shall be recognised during the vesting period and not on the grant date. [refer to para 14 and 15 of the Standard].

Comparison of i.) (immediate vesting) and ii.) ( vesting on satisfaction of vesting conditions and/or a vesting period)

Basis

i.) on grant date

ii.) during vesting period

Vesting period

In cases where options vest immediately upon granting

In cases where there is a vesting period viz. a specified period of service is required to be completed

Receipt of services

Presumption that services (as consideration of equity shares) has been received

Presumption that services will be received during vesting period

Let us take an example to understand the manner in which the value of the ESOPs under managerial remuneration will be recognised applying the logic of the accounting standards.

i.) Options granted on grant date with immediate vesting

Company A grants 5,00,000 options to Mr. X. Grant date – January 1, 2022.

In this case the 5,00,000 options shall vest with Mr. X on January 1, 2022 at fair value of the options. Let’s say the exercise price of the option is fixed at Rs. 50. The fair value of the options shall be recognised in the year of grant i.e. in FY 2021-22, and amounts to Rs. 120. The accounting entry shall be:

Recognition of services as an expense:

Director’s Remuneration a/c … Dr {less from P/L}

To Outstanding Options {increase in liability}

This will result in an increase in the managerial remuneration of Mr. X in the FY 2021-22 by Rs. (120-50)*5,00,000 = Rs. 3,50,00,000.

ii.) Options granted with a vesting schedule spread over 3 years

Company A grants 5,00,000 options to Mr. X. Grant date – January 1, 2022. The vesting period is fixed at 3 years from the date of grant. The exercise price of the options are Rs. 50. Fair value of the option as on the date of grant is Rs. 50, at the end of one year from the grant date – Rs. 80, at the end of second year – Rs. 100, at the end of third year – Rs. 120.

The vesting schedule is as under:

On completion of 12 months from the date of grant of options = 30%

On completion of 24 months from the date of grant of options = 30%

On completion of 36 months from the date of grant of options = 40%

In this case the same will be included in the managerial remuneration as under –

Rs. 80 * 30% of 5,00,000 = Rs. 1,20,00,000 – on December 31, 2022 – to be included in the managerial remuneration of FY 2022-23

Rs. 100 * 30% of 5,00,000 = Rs. 1,50,00,000 – on December 31, 2023 – to be included in the managerial remuneration of FY 2023-24

Rs. 120 * 40% of 5,00,000 = Rs. 2,40,00,000 – on December 31, 2024 – to be included in the managerial remuneration of FY 2024-25.

Issues with recognition of managerial remuneration as per accounting treatment

If the remuneration is treated based on the accounting treatment, there are some contentious issues:

Most importantly, the grant of the option is recognised as a cost over the vesting period, while it is not certain whether or not the option will be exercised. It is quite usual, either because of movement in prices of shares, or because of the employee not having been able to organize funding for the exercise price, that the option is never exercised. However, based on the grant of the option, the employee would have already been treated as having been remunerated, which again, would be illogical.

In cases where the options are granted at the fair value on the grant date, the intrinsic value of the option is zero on the grant date. Hence, the company has not suffered a CTC on the grant date. The option is vested over time, and exercised beyond vesting, and therefore, the option may acquire value over time. However, to say that this value is a cost to the company on the grant date itself, seems mismatched with the concept of remunerating an employee.

Most importantly, since the definition of managerial remuneration under sec. 2(78) of the CA, 2013 refers to the definition of perquisite for tax purposes, this treatment is going beyond the statutory definition. There are other cases where there is a divergence between the cost to company and the taxable value of the perquisite, and it has been a consistent practice to treat only the taxable value of the perquisite as a part of managerial remuneration. Examples may be rent free accommodation, employer’s contribution to provident fund, HRA, etc.

C. Recognition of ESOPs as part of the managerial remuneration – balancing between the accounting and taxability approach

Based on the above discussions, one can argue that both the cases are not entirely appropriate for considering ESOPs as CTC. In such a situation, a combination of (A) and (B) may be proposed to be opted by the companies for the recognition of ESOPs as managerial remuneration.

The proposed alternative seeks to treat ESOPs as managerial remuneration in the following manner –

It takes into account the actual taxable value of the ESOPs, but

instead of including the same in the remuneration of the financial year in which the same is exercised, the same is spread over the vesting period of the ESOPs, and

related back to the net profit of the financial years to which the vesting of options pertains.

The proposed alternative seems comparatively reasonable than the other options since though the employee derives benefits on or after the exercise date, the benefits actually accrue during the vesting period itself, since vesting is actually the condition to be satisfied in order to be eligible for the exercise of the options granted to the employee. Linking the same with the taxable value, instead of the accounting treatment, provides a realistic view of the remuneration actually given to the managerial personnel.

Manner of computation of managerial remuneration as per the aforesaid option

A company has in January 2022, offered to grant a maximum no. of 5,00,000 equity shares under its ESOP scheme to Mr X, MD of the Company. The vesting period is fixed at 3 years from the date of grant. The vesting schedule is as under:

On completion of 12 months from the date of grant of options = 30%

On completion of 24 months from the date of grant of options = 30%

On completion of 36 months from the date of grant of options = 40%

The exercise price of the share is Rs. 50 and fair value/ market value on the date of exercise is Rs. 200.

The above options shall form part of the managerial remuneration of Mr. X as follows:

30% of 5,00,000 i.e. 1,50,000 options shall vest in December 2022, another 1,50,000 shares vest in December 2023, and the remaining 200000 shares vest in December 2024.

There may be, say a period of another 2 years, from the last of the vesting schedules, for the exercise. Assume, therefore, that the employee exercises all the options, for 500000 shares, in December 2026.

The remuneration is, therefore, the perquisite value, being 500000* Rs.(200-50), i.e.Rs. 7,50,00,000 .

However, this remuneration is related back to the years 2022, 2023 and 2024, in the ratio of 30:30:40.

Advantages of such approach

Some of the advantages of this approach are:

Remunerating managerial personnel by way of ESOPs is an important component of managerial remuneration, and therefore, it doesn’t escape the process of shareholders’ approval.

By relating the recognition of the options as a part of remuneration only on actual exercise, any possibility of treating ESOPs as a part of remuneration, without the actual exercise, gets avoided.

Where the managerial personnel is not associated as such, at the time of exercise, this may seem like taking shareholders’ approval, in many cases, long after the actual debit in profit and loss a/c. However, in case of managerial remuneration, the debit to the profit and loss a/c and the approval by shareholders are quite often disconnected. In the era of Central Govt control on managerial remuneration, it was quite common that the approval was obtained several years after the provision in the profit and loss a/c, as discussed below.

Manner of obtaining shareholders’ approval?

Now a question arises as to what if the values calculated as above lead to breach of limits as per the net profits of corresponding financial year or as already sanctioned by shareholders. Therefore, if in any of the years, the managerial remuneration has exceeded the limits cast by sec. 197/Schedule V, the approval may be sought at any time before allotment of the shares. If, and to the extent, the shareholders do not approve the managerial remuneration, the shares cannot be allotted, beyond the shareholders’ approval.

Retrospective approval for managerial remuneration

In terms of section 197 of the Act, read with Schedule V, the shareholders’ approval is required to be taken where the remuneration payable to a managerial personnel exceeds the limits of net profits as provided for under the section or in the event of loss or inadequacy of profits for the year to which the same relates. Limits on managerial remuneration, by the very nature, are always calculated retrospectively, and therefore, a post facto approval for managerial remuneration is almost a regular feature.

Consider the following situation: The managing director is receiving remuneration, say Rs 25 lacs a month, on a monthly basis. Obviously, he takes this money home every month. It is only after the end of the year, when the financial statements have been drawn, that we know the profits for the year, and compute whether the amount paid over the year is within the limit of 5%, or within the approved limit as per shareholders’ resolution.

Assuming that we find that the profits are falling inadequate [if the remuneration paid is Rs 25 lacs *12 = Rs. 300 lacs, and the profits are less than Rs 60 crores, the limit of 5% will be breached], the company shall take the amount of remuneration paid in excess of the limits for approval by shareholders. If the shareholders do not approve such payment, the amount paid in excess shall be refundable by the managerial personnel, within a period of 2 years or such lesser time as may be allowed by the shareholders. Until such refund, the managerial personnel shall be deemed to be holding the money in trust for the company. [sec 197 (9)].

In our suggested methodology for ESOPs, in case the value of the option during the vesting period, along with other remuneration paid, is exceeding the limits, the approval shall be taken after exercise and before allotment of the shares. This is similar to the retrospective approval for excess remuneration, and fits into the structure of sec. 197 (9). That the allotment is subject to the shareholders’ approval, may be suitably incorporated in either the ESOP Plan itself, or at the time of approval of grant of such stock options by the board committee.

Disclosure of ESOPs as a part of managerial remuneration

Once we have arrived at the conclusion that ESOPs are considered as a part of the managerial remuneration, and given the values involved, it becomes important to give appropriate disclosures around the same. While there are specific requirements on disclosures of ESOPs as a part of managerial remuneration, under applicable laws as discussed above, it is important that companies go by the spirit and not only letter-compliance of law, and disclose information in such a manner so as to present a fair and conclusive view before the shareholders and other stakeholders.

Global practices on approval and disclosure of managerial remuneration

As discussed above, managerial remuneration is either regulated or disclosed in several other major jurisdictions too, requiring the companies to put managerial remuneration in the domain of shareholders, either for explicit approval, or at least for disclosure. Specific disclosure is also, in the manner of speaking, a regulatory requirement, as the shareholders may then put curbs by shareholders’ vote. The concept of “say on pay”, that is, the right of shareholders to have a mandatory non-binding vote on the compensation of their executives has been in existence since a long time, and legislation to this effect has been enacted in countries all around the world such as UK, US, India, Singapore, Netherlands,Switzerland, Belgium etc. Further, some countries are moving towards binding votes in place of advisory votes of shareholders. The International Scope of Say on Pay published by the European Corporate Governance Institute (ecgi) in September, 2013 defines Say on Pay as: “(1) a recurring, mandatory, (2) binding or advisory shareholders’ vote, (3) provided by law, that (4) directly or indirectly through the approval of the remuneration system, remuneration report or remuneration policy, (5) governs the individual or collective global remuneration package of the executive or managing directors of the corporation.”

USA:

Wide attention to managerial remuneration, mostly called “CEO compensation”, was drawn during the passage of the Dodd Frank law[3]. The Dodd Frank law brought the concept of “say on pay”, that is, shareholders have a say on the pay of the CEO. Consequently, amendments have been made to the Securities Exchange Act of 1934 (“SEC Act”) to enforce the concepts introduced by the Dodd Frank laws by way of regulatory enforcement. Section 14A of the SEC Act requires shareholders to approve the executive compensation by way of a separate resolution at least once in every 3 years, or such other frequency of lesser duration (i.e., 1 or 2 years) as may be approved by the shareholders once in every 6 years. However, the approvals are non-binding in nature. Section 14 of the SEC Act has also been amended to require disclosure of such “information that shows the relationship between executive compensation actually paid and the financial performance of the issuer, taking into account any change in the value of the shares of stock and dividends of the issuer and any distributions.” It also seeks disclosure in the annual meeting of shareholders as to whether any employee or director of the company is permitted to purchase financial instruments that are designed to hedge or offset any decrease in the market value of equity securities granted as part of compensation or held directly/ indirectly by the employee or director.

A substantial portion of a US executive’s compensation package typically consists of equity-based incentive awards. Title 26 of the United States Code provides the amended Internal Revenue Code of the US, a part of which deals with the meaning and taxability of ESOPs. Though originally defined in Section 4975(e)(7), it requires to qualify the conditions given under section 401(a) and various conditions of section 409. For tax purposes, the income in respect of stock options is recognised when the stock options are exercised by the option-holder. [4] However, there are special Incentive Stock Options (ISOs) as defined under section 422(b) in which case, no income is recognised at the time of transfer of shares to the employees pursuant to the exercise of the options, and no deduction is available to the employers. On the sale of shares, capital gains accrue as usual in either of the cases.

UK

In the UK Companies Act, 2006, the managerial payment under section 226A is defined as ‘any form of payment or other benefit made to or otherwise conferred on a person as consideration for the person holding, agreeing to hold or having held office as director of a company…’ This indicates that the remuneration to directors also includes stock options.

The remuneration to directors has to be paid as per the remuneration policy which is approved by the shareholders. The policy and the remuneration to be paid has to be recommended by the committee constituted for the said purpose. (Section 226B)

As per Section 412, the notes to financial statements must disclose the gains made by the directors on exercise of share options. Further, the Directors’ remuneration report has to be approved by the shareholders (Section 439). In addition to this, Article 9A of the Directive of the European Parliament and the Councillists down the matters to be disclosed in the remuneration report regarding each individual director’s remuneration which, inter alia, includes the number of shares and share options granted or offered, and the main conditions for the exercise of the rights including the exercise price and date and any change thereof.

Therefore, presently, in UK, there are two lines of control on director’s remuneration –

Approval of director’s remuneration policy by a binding vote of shareholders and any subsequent modifications thereto;

Approval of director’s remuneration report on an annual basis by way of an advisory vote of the shareholders

Various aspects of the Employee Share Plans in the UK along with the regulatory overview and taxation aspects may be accessed in the Q&A guide.

France

Article L225-44 to L225-47 of the French Commercial Code deals with director’s remuneration. As per the said articles, the directors shall receive an annual fixed remuneration fixed by the shareholders at the general meeting. Such an amount is distributed among the directors as determined by the Board. The directors may also receive exceptional remunerations for the missions conferred upon the directors. As per Article L225-177, the shareholders may authorize the board of directors or the executive board to grant stock options to the employees of the company. In terms of Article L225-185, the executive directors of the company may be granted stock options.

The remuneration to directors, including the stock options, is recommended by the compensation committee and decided by the board. Such remuneration is annually approved by the shareholders. (Para 26 of French Corporate Governance Code of listed corporations).

The Board is required to present the compensation of directors in respect of the closed financial year at the annual general meeting which includes stock options, performance shares and multi-annual variable compensation plans together with the performance criteria used to determine these compensation components. If the shareholders vote against the resolution, the Board is required to examine the reasons and expectations of shareholders and accordingly rule on the modifications to be made to the compensation due or paid or the future compensation policy.

Singapore

In terms of Section 169 of the Companies Act, 1967 of Singapore, a director cannot be paid any emoluments in respect of his office, unless the same is approved by the shareholders of the company. In the context of Singapore, the term “emoluments” has been given a wider meaning and includes “any fees, percentages and other payments made (including the money value of any allowances or perquisites) or consideration given, directly or indirectly, to the director…. in the director’s capacity as such or otherwise in connection with the affairs of that company…”. Such a wide definition of emoluments, includes, beyond doubt, the stock options granted to the directors.

Section 161 of the Singapore Act requires prior approval of shareholders for issue of any shares to the directors. In case of issue of shares as a part of the options granted to the directors, the approval is required to be taken at the time of granting of such options to the directors. Such options granted to any director and CEO of the company, if any, are required to be disclosed in the register of directors’ and CEO’s shareholding.

Sections 164A and 165 of the Singapore Act obligates a director to disclose when asked for by way of a notice by a specified percentage of shareholders (in number/ by value) and annually as when as there is some change in the particulars, the particulars of the emoluments received by him. Further, the Director’s Statement required to be annexed with the annual financial statements in terms of Section 201 read with the Twelfth Schedule requires the following disclosures pertaining to the options granted to the directors, as following –

2. Where any option has been granted by a company, other than a parent company for which consolidated financial statements are required, during the period covered by the financial statements to take up unissued shares of a company —

(a)the number and class of shares in respect of which the option has been granted;

(b)the date of expiration of the option;

(c)the basis upon which the option may be exercised; and

(d)whether the person to whom the option has been granted has any right to participate by virtue of the option in any share issue of any other company.

4. Where a parent company or any of its subsidiary corporations has at any time granted to a person an option to have shares issued to the person in the company or subsidiary corporation, the directors’ statement of the parent company must state the name of the corporation in respect of the shares in which the option was granted and the other particulars required under paragraphs 2, 5 and 6.

5. The particulars of shares issued during the period to which the statement relates by virtue of the exercise of options to take up unissued shares of the company, whether granted before or during that period.

6. The number and class of unissued shares of the company under option as at the end of the period to which the statement relates, the price, or method of fixing the price, of issue of those shares, the date of expiration of the option and the rights (if any) of the persons to whom the options have been granted to participate by virtue of the options in any share issue of any other company.

From the aforesaid, it seems that in Singapore, the managerial remuneration is governed to a great extent by way of initial approvals and continual disclosures.

Apart from the approval requirements, there are some restrictions on the number of shares that can be issued as a part of the ESOP plan. The number of shares issued to directors, chief executive officers, general managers, and officers of equivalent rank is restricted to 50 percent of the total number of available shares under the plan. The maximum entitlement of each participant is 25 percent of the total number of shares available in the ESOP.

A detailed regulatory overview of the current ESOP scenario can be referred to in the question-answer guide to the Singapore ESOP plans.

As discussed above, the emoluments to be paid to directors is required to be approved by the shareholders (in the Annual General Meeting, generally) before being paid to the directors. Director’s fees are taxable in the year in which the director becomes entitled to the fees, which is said to be the date on which the same is approved by the shareholders.

From the Inland Revenue Authority of Singapore’s guide to employment income, the gains on ESOP are taxable when the stock options are exercised, however, if the ESOP plan imposes a restriction on the sale of shares for a definite period, the same is exercisable once the restriction period ends. For ESOP plans with a vesting period, the gains become taxable as per the vesting schedule and are recognised on the date of vesting. Further, currently, a tax-deferment scheme is also effective – Qualified Employee Equity-based Remuneration Scheme (Qualified EEBR Scheme), which provides an option for the deferment of tax for a period of five years, subject to certain qualifying conditions for the same.

Concluding Remarks

The significance of managerial remuneration in ensuring an effective corporate governance has been recognised in almost all the major countries of the world, due to its potential of conflict of interest. However, presently, there is an anomaly in the presence of adequate controls over ESOPs, accounting for a major part of the managerial remuneration/ executive compensation in many companies, especially, the listed ones. While the total pool of options under an ESOP plan is approved by the shareholders, as also the managerial remuneration of the managerial personnel at the time of his appointment/ re-appointment, what generally does not come before the shareholders for approval is the exact number of share options granted to one person, and its effect on the net profits of the company at the time of exercise. Therefore, there is an evident gap that requires appropriate treatment. While disclosures with respect to ESOPs are required to be made in annual reports, companies generally disclose it in terms of the fair value of the options, and sometimes, also ignore the same in the computation of the managerial remuneration. A definite approach of treating ESOPs as part of managerial remuneration, stating the time and value at which the same is taken and the manner in which shareholders’ approval will be taken is the need of the time, so as to do away with the existing reflecting gaps.

[2] Reg 17(6)(e) requires shareholders’ approval by way of a special resolution for compensation payable to executive directors who are promoters or members of the promoter group if –

(i) the annual remuneration payable to such executive director exceeds rupees 5 crore or 2.5 per cent of the net profits of the listed entity, whichever is higher; or

(ii) where there is more than one such director, the aggregate annual remuneration to such directors exceeds 5 per cent of the net profits of the listed entity

[3] Subtitle E of the Dodd Frank Wall Street Reform and Consumer Protection Act is based on accountability and executive compensation. It requires the executive compensation to be approved by the shareholders of the company, as also, the same to be disclosed to the shareholders in terms of pay vs performance of the directors.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-04-14 17:22:112022-05-13 12:14:55ESOPs as part of managerial remuneration

Considering the key significance of auditors’ independence in ensuring the integrity of the statutory audit function, the Companies Act, 2013 (‘Act’) has prescribed several eligibility conditions, qualifications as well as disqualifications for their appointment. While there are several disqualifications under section 141, which includes indebtedness, provision of guarantee, conviction, etc. The existence of a “business relationship” between the auditor and auditee has also been stated as one of the prima facie disqualifying factors for a person to be appointed as an auditor in a company. It is significant to note that this disqualification was not there under the corresponding provisions of the Companies Act, 1956.

The relevant clause dealing with ‘business relationship’ is clause (e) of sub-section (3) of Section 141 of the Act. The clause (as reproduced below) has a wide coverage and includes all direct as well as indirect business relationships as under –

‘A person or a firm who, whether directly or indirectly, has business relationship with the company, or its subsidiary, or its holding or associate company or subsidiary of such holding company or associate company of such nature as may be prescribedshall not be eligible for appointment as an auditor of a company.’

Further, the meaning of the phrase ‘business relationship’ has been detailed out under sub-rule (4) of Rule 10 of the Companies (Audit and Auditors) Rules, 2014 (‘Rules’) which also carries certain carve-outs. In this article, we have tried to unbox the said carve-outs given for the existence of those business relationships which do and which do not lead to disqualifying the auditors from appointment.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-01-14 12:00:562022-01-14 12:00:56Auditors’ disqualification on account of business relationships: purport and scope

Companies are creatures of their shareholders. If the company is a private company, the business and wealth of the company is the property of its shareholders. Technically, shareholders own the shares of the company, and certainly, a shareholder may donate his shares out. There are several iconic examples of such demonstrations of charitable intent, such as Mark Zuckerberg giving away 99% of his holdings in Facebook and Bill Gates donating 95% of his wealth to their charitable foundation and ultimately utilizing the same for charitable purposes.

However, can the shareholders resolve that the business and assets of the company that they own be donated out? Conceptually, there should be no difference between emptying out the assets of the company to the same charitable cause to which shareholders would have considered donating the shares. There are various judicial precedents[1] to refer to when it comes to checking the admissibility of a shareholder to transfer his shares by way of gift. However, in case of donation of shares, the company would remain up and running, and the charity will become simply the owner of the shares. However, if the business or assets of the company are donated out, that amounts to a mode of winding up, because the charity will not obviously run the business. So, can such donation be used as a mode of emptying the company out, so as to spend all its substratum, and once the company that empties out itself, it may just become a dud company, good for a strike off action u/s 248 (2) of the Companies Act, 2013 (‘Act’).

Surely enough, it will be unusual for the Memorandum of Association (‘MoA’) of the company to have the power to donate all its assets out. Normally, MoA will have charity as one of the incidental powers, but incidental powers can only be used in furtherance of the business or in conjunction thereof. There is no question of using incidental powers to donate the business out itself. So, can a corporate entity take such a drastic action, as to donate out all assets? And if yes, what will be the modality of doing the same? Also, what happens to the donee?

We have started with the donee being a charity. By way of argument, if one could donate all assets out to a charity, one can do it even to another entity. However, there may be taxation implications in that case, also discussed in this article.

Permissibility for a corporate person to make gifts

A doubt may arise as to whether a company, being a corporate person, can make a gift. Before answering that question, let us first understand the legality of making gifts. As per Section 25 of the Indian Contract Act, 1972, a contract without consideration is void. The same is also contemplated through the latin maxim ex nudo pacto nor oritur action meaning ‘a contract without consideration is void’. Here the adequacy of the consideration is not necessary and only the presence of the same suffice the requirement for constituting a valid contract.

However, Section 25 provides certain exceptions under which a contract is valid even if the same is not backed by consideration, which are –

A written and registered document made on account of natural love and affection between the parties, i.e., a gift

Compensation for voluntary services given by the recipient in the past

Time barred debt

Explanation 1. —Nothing in this section shall affect the validity, as between the donor and donee, of any gift actually made.

Now given the fact that one can make gifts to the other, however, in the context of of a corporate person, the component of natural love and affection cannot be said to be present. The same was a question raised for determination before the ITAT – Mumbai bench in the matter of KDA Enterprises Pvt. Ltd., Mumbai vs Department Of Income Tax, ITA No.2662/M/2013, where both the donor as well as the donee were companies. In the matter of KDA Enterprises (supra), the AO was of the view that gifts can be given only by natural persons and therefore, a gift by a company is not tenable[2], against which, an appeal was preferred by the Company. However, the ITAT shifted the attention of the contended AO to the explanation u/s 25 of the Contract Act which states that the section does not have any effect on the validity of the gifts between donor and donee.

The AO, in the instant case, had further submitted that no gift deed has been executed, which is again, not a prerequisite for a valid gift. Here, one may refer to the definition of gift given under Section 122 of the Transfer of Property Act, 1822, which defines gift as –

“Gift is the transfer of certain existing moveable or immoveable property made voluntarily and without consideration, by one person, called the donor, to another, called the donee, and accepted by or on behalf of the donee.”

From the above definition, the three essential components of gift can be noted –

Transfer or delivery of property

Voluntary, i.e., with a donative intent

Acceptance by donee

The aforementioned components of a gift may be present in case of a company as a donee and therefore, the contention of the AO that the transfer is not a gift on the basis of either of the grounds does not survive merit consideration.

In view of the above, the ITAT in the matter of KDA Enterprises (supra), has allowed the admissibility of gift by a company to a company and held that –

“… the companies are competent to receive and make gifts. All the three requirements of a valid gift, viz. identity of the donor, capacity/source and the genuineness stands proved in the case of the assessee. All the donor companies and the assessee are authorized by their Memorandum and Articles of Association for giving and receiving gifts. Proper resolutions in the Board Meeting have been passed by all the four companies for making the gift to the assessee and assessee has also accepted the said gifts by way of adopting a resolution in the meeting of Board of Directors.” [Emphasis supplied]

In another similar case of D.P. World Pvt. Ltd. vs. DCIT, ITA No. 3627, which related to the gift of shares made by a company to another, the view was upheld that a company can make a gift. The relevant extract is reproduced below –

“It would not be out of place to mention that a combined reading of Sec. 82 of the Companies Act, Section 5 and Section 122 of the TPA suggest that a company can validly transfer the shares by way of gift, provided where Articles of Association of the donor company permits the same. In case of donor is a foreign company, the relevant corporate/commercial law of the jurisdiction where the donor is based needs to be considered. In the light of the above discussion, we have no hesitation to hold that a company can gift shares and such transaction may appear as ‘strange’ transaction but cannot be treated as “non – genuine” transaction.” [Emphasis supplied]

Power of shareholders regarding disposal of all assets of a company

While the Act does permit the disposal of assets of a significant value in the company after obtaining shareholders’ approval, however, the shareholders’ authority cannot extend beyond the MoA of the company. Where the disposal of assets has the effect of impacting the going concern status of the company, the same cannot be done without express authorization for the same in the MoA of the company. This is evident from the rulings cited above as well, since in each of the said rulings, the company(ies) had express authority for making/ receiving gifts/donations through its/their MoA.

Points for consideration in case of disposal of entire assets of a company as a gift/donation

The above discussions clearly entail that a company is competent enough to make and/or receive gifts and/or donations. Having said that, consider the case of a company which wants to dispose off all its assets by way of donations/ gifts. The following points are significant to be considered while making the gift / donation:

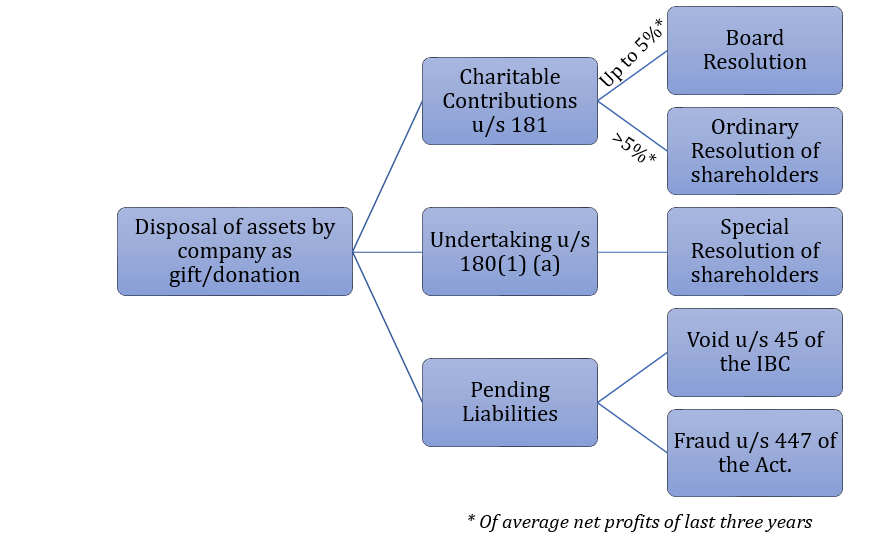

Board’s / shareholder’s power to make charitable contributions u/s 181 of the Companies Act (‘Act’)

The Act recognizes the power of directors to make contributions to bona fide charitable and other funds u/s 181 of the Act, subject to the shareholders’ approval if the same exceeds 5% of the preceding three years’ average net profits.

Disposal of undertaking u/s 180(1) (a) of the Act

Section 180(1)(a) of the Act restricts the powers of the board with respect to disposal of substantial undertaking(s) of a company. It requires shareholders’ consent by way of a special resolution in order to dispose of the whole or substantially the whole of undertakings of the company.

For the purposes of the said sub-section, undertaking would mean an undertaking in which the company’s investments exceed 20% of its net worth or which generates income equal to 20% or more of the total income of the company. ‘Substantial’ part of undertaking would mean 20% or more of the undertaking of the company.

Further, undertaking has not been defined under the Act and its meaning can be taken from the provisions of the Income Tax Act, 1961 (‘IT Act’). The explanation to Section 2(19AA) of the IT Act, defines undertaking as –

“undertaking shall include any part of an undertaking, or a unit or division of an undertaking or a business activity taken as a whole, but does not include individual assets or liabilities or any combination thereof not constituting a business activity.”

In a case where a company wishes to donate all its assets, it definitely calls for taking approval of the shareholders and in fact considering the disposal of the entire assets, the unanimous approval from the shareholders should rule out any defiance from a third party.

Disposal of assets without cleaning of liabilities may attract section 45 of the IBC and 447 of the Act

While there may be no bar on the disposal of all the assets of a company, thereby leading it to dissolution, the same can be done only after all the external liabilities have been paid. Where a company has disposed off all its assets for free, without settlement of the external liabilities, the same may amount as an undervalued transaction under Section 45 of the Insolvency and Bankruptcy Code, 2016 (‘IBC’), and may be rendered void and therefore, directed to be reversed.

Done with the intent to defraud the creditors, the same also attracts the provision of Section 447 of the Act and imposes mandatory imprisonment on the person guilty of such offence.

Impact of disposal of all assets of a company

The disposal of all the assets of the company leads to the loss of substratum of the company. In the matter of Mohan Lal & Anr vs Grain Chamber Ltd, 1968 SCR (2) 252, “Substratum of the Company is said to have disappeared when the object for which it was incorporated has substantially failed, or when it is impossible to carry on the business of the Company except at a loss, or the existing and possible assets are insufficient to meet the existing liabilities.” This, in turn, becomes a ‘just and equitable ground’ u/s 271 for winding up of the company.

“…. the company has ceased to carry on business, its substratum is gone, it has carried on ultra vires business and that the said business has been carried on by meddlers and that it will be just and equitable that the company should be wound up.”

However, as per Section 274(2) of the Act, a petition for winding up on the basis of just and equitable grounds can be dismissed by the Tribunal if it is of the opinion that a remedy other than winding up is available to the petitioners and seeking winding up of the company is unreasonable.

Tax implications on gifts/donations

Gifts and donations are not prohibited to be made by the companies, rather regulated and made taxable over and above the specified limits. The provisions of IT Act by way of certain clauses of Section 56, provides for taxability in case of transfer of shares without consideration, over and above a specified amount. Similarly, Section 80G of the IT Act also permits various donations and voluntary contributions.

No capital gains

Any transfer of a capital asset under a gift or to an irrevocable trust is an exempted transfer under section 47(iv) of the IT Act, and therefore, not taxable as capital gains. However, reference may be made of the ruling of Madras High Court in the matter of Principal Commissioner Of Income Tax vs M/S.Redington (India) Limited, T.C.A.Nos.590 & 591 of 2019, in which, on the facts of the case it was found that the transfer of shares, camouflaged in the nature of a gift made to its subsidiary, is actually an attempt of corporate restructuring and does not include the necessary elements of a gift (para 6).

The receipt/giving of such gifts/donations cannot be said to be related to the business of an assessee and therefore, cannot be made taxable as profits and gains of business or profession (refer cases above).

Chargeability as income from other sources

Section 56 of the IT Act admits taxability of certain gifts (both movable and immovable) without consideration beyond a specified limit. As per clause (x) of Section 56, gifts (cash/movable property/immovable property) is not taxable upto a certain threshold, being Rs. 50 lacs. Over and above the specified limit, gifts are taxable as ‘income from other sources’ except when the same qualifies as an exception under the proviso to the said clause. Here also, benefits can be availed by a trust or an organisation registered under Section 12A, 12AA or 12AB or u/s 10(23C) for charitable or religious purposes.

Concluding Remarks

Disposal of all assets of a company does not seem to be prohibited and can be sought as a good means of providing closure to the business, subject to the same being authorised through the charter documents and sanctioned through shareholders’ consent. However, the same should not be designed as a ‘tax avoidance’ exercise, since if the malicious intent becomes evident, it may attract payment of taxes along with fine and penalty and may even lead to prosecution based on the severity of the case.

[2] The sin qua non of a gift is that the transaction is without any consideration and out of natural love and affection, as held in various judicial pronouncements. Since company is an artificial judicial person, so there cannot be any natural love & affection by a company or between the companies. Hence, a transaction of gift cannot be said to be valid or legally tenable between companies or where one of the parties is a company.”

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-01-09 10:57:122022-01-17 19:44:20Can companies donate out all their assets?

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2022-01-04 15:19:472022-01-04 15:19:47FAQs on minority squeeze-out : Section 236 of the Companies Act, 2013

Majority always prevails in corporate democracy. The management of the company is based on the majority rule i.e all matters decided in a general meeting ensue from majority voting which may overlook interests of minority. The need to balance the rights of majority and minority members is well recognized in the Sec 241 of the Companies Act, 2013 (the “Act”) thereby providing protection against oppression and mismanagement for the members of a company. It enunciates the rights of minority to impinge the decisions of majority by applying before Tribunal.

Section 241(1) of the Act states that the complaint can be filed by aforesaid mentioned member(s) before Tribunal when:

(a) the affairs of the company have been or are being conducted in a manner prejudicial to public interest or in a manner prejudicial or oppressive to him or any other member or members or in a manner prejudicial to the interests of the company; or

(b) the material change, not being a change brought about by, or in the interests of, any creditors, including debenture holders or any class of shareholders of the company, has taken place in the management or control of the company, whether by an alteration in the Board of Directors, or manager, or in the ownership of the company’s shares, or if it has no share capital, in its membership, or in any other manner whatsoever, and that by reason of such change, it is likely that the affairs of the company will be conducted in a manner prejudicial to its interests or its members or any class of members.

However, for seeking relief in case of oppression and mismanagement, eligibility requirements as provided under Section 244(1) of the Act must be satisfied by minority member(s) unless otherwise waived off by the Tribunal on application made by member(s).

This article intends to exhibit the grounds considered by Tribunal while passing the order and in exercise of the authority for grant of waiver in applications.

Eligibility for filing applications under Section 241

Section 244(1) of the Act provides the eligibility criteria for filing an application before tribunal to seek relief in case of oppression and mismanagement.

However, as per various judicial precedents merely fulfilling the aforesaid criteria is not the only ground considered by Tribunal to pass an order in favor of the minority. The Tribunal may exercise its power to waive off all or any of the aforesaid mentioned eligibility requirement on justifiable grounds. Such power of exemption is specifically provided in the proviso to section 244 (1), which states,

“Provided that the Tribunal may, on an application made to it in this behalf, waive all or any of the requirements specified in clause (a) or clause (b) so as to enable the members to apply under section 241.”

Notably, the proviso does not hint at the possible ‘reasons’ which can be considered by the Tribunal to grant exemptions. However, section 399 of the predecessor Companies Act, 1956 empowered the Central Government to authorise any member or members of the company to apply to the Company Law Board under section 397 or 398, notwithstanding the minimum requirements. At this point, it would be pertinent to note that the Tribunal too, has to observe principles of natural justice as per Rule 14 of the NCLT, 2016.

Accordingly, few extracts from judicial pronouncements are illustrated herein discussing the grounds considered by Tribunal while passing the order.

Cases and circumstances where waiver has been granted

● Principle of Natural justice, serious injury

Essentially, natural justice requires that a person receives a fair and unbiased hearing before a decision is made that will negatively affect them. Courts have always emphasized on presence of “just and equitable” as the main intent while passing any order which acts as one of the grounds for the grant of waiver. Accordingly, the Tribunal may grant waiver, if in its opinion, it is just and equitable.

Same was established in Sri Krishna Tiles & Potteries v. The Company Law Board And Ors., where petitioner Arunachalam was the lone shareholder out of the members of the company and does not have support of the remaining 49 members. He held only 3015 equity shares which was obviously less than 10 per cent of the paid up share capital of the company. It was contended that no opportunity be granted to the petitioner to show to the Company Law Board that substantiates the waiver of locus standi.

Court held that It is not a protection, granted to the company because the company is after all constituted by its members. It is a bar on the members. In removal of that bar the members have a right of hearing and not the company. Normally, any citizen in a free democratic country has a right to go to court if his interests are adversely affected by the action of anyone. Such right cannot be denied to members of the company qua the working of their company. The statutory bar created can be removed if circumstances exist. This is in consonance with the principle that everyone has a right to approach the court for redress of his grievance. If 11 per cent shareholders can move an application under Section 397 or Section, 398 of the erstwhile Companies Act without the intervention of the Company Law Board or the Central Government then a lesser number should have a right to do so on being authorised without having to fight first a battle with the company before the Company Law Board and then in court.

Similarly, in Photocon Infotech Pvt. Ltd. v. Medici Holdings Ltd. , the Tribunal granted the waiver to the applicant which was subsequently aggrieved by Respondent that the applicant does not fulfil locs standi and filed appeal before NCLAT.

NCLAT upheld the decision of Tribunal and stated that it is open ended wide discretion of NCLT and all judicial powers and discretions are to be so exercised that it should not be arbitrary or whimsical. Interest of justice should always been the guiding factor.

● Substantial Interest in Company

Substantial interest is an exceptional circumstance meriting the grant of waiver. It can be substantial monetary investment or substantial long-standing relationship with the company forming a substantial emotional investment in the company.

The same can be well construed from Thomas George v. Malayalam Industries Ltd., where the locus standi was waived off High Court of Kerala. The applicant and his wife together held 8.84 per cent of the total issued share capital of the respondent company, and thus fell short of the requirement under Sec 244(1). However, the applicants were subscribers to the charter documents of the company and the husband was a managing director and responsible for setting up of the hotel that was being run by the first respondent-company.

The Kerala High Court held that despite not meeting the ten per cent requirement, the applicants’ well established relation with the company as promoter and key managerial personnel reflected their substantial interest in the company’s affairs. Accordingly the waiver was granted.

Similarly, referring to Cyrus Investments Pvt. Ltd. v. Tata Sons Ltd & Ors, the appellants had an interest to the extent of one-sixth of the overall value of the company. Failure to meet the criteria of 1/10th of the share capital was because of the inclusion of preference share capital in the share capital reducing the appellants issued share per centage from eighteen per cent to 2.71 per cent.

The NCLAT held the appellant’s substantial interest in the overall value of the company was exceptional and compelling enough to grant a waiver under Section 244 of the Act.

Also, in this case, there were forty-nine minority shareholders all having shareholding less than 2% individually. This meant that they could not form the required 10% unless they approached the Tribunal in groups of six or more. This showcased the dependence of minority shareholders on one another for their rights.

Tribunal admitted the waiver application observing that the members cannot always be expected to approach the Tribunal in groups where the minority shareholding was disintegrated to an extent that multiple shareholders would have to rely on one-another to fulfil the ten per cent requirement under Section 244(1).

● Dilution in Shareholding because of oppression

In Manoj Bathla v. Vishwanah Bathla, the shareholding of the respondent was dramatically reduced from twenty-five per cent to 0.33 per cent in the company. This was the subject-matter of the application under Section 241 as well as the plea for warrant of grant of waiver. The NCLT had already granted the waiver, but appealing to the NCLAT, the appellants argued that the respondent does not fulfil the criteria for a section 241 application or the waiver application , as his shareholding was virtually zero per cent, even disentitling him from the status of a member.

The NCLAT upholding the decision of the NCLT, observed that refusing the grant of waiver herein would be depriving the respondent from the relief sought against allegations of oppression manifesting from manipulation of shareholding, because of which the respondent’s interest in the company seemed prejudiced. Noting this, the NCLAT upheld the grant of waiver to enable the respondent to proceed under Sec 241.

Similarly, in Photocon Infotech Pvt. Ltd. v. Medici Holdings Ltd., the reason for application under section 241 was the attempt of the management in demerging key assets of the company in slump sale. However, the Tribunal observed that the shareholding of the aggrieved were also purposely diluted and left with a minute shareholding of 0.038 per cent and 6.62 per cent in order to prevent them from filing a case of oppression and mismanagement. This was done by increasing the number of members of the company by transferring fifteen shares to the employees.

It was held that this dilution of the aggrieved, preventing them from fulfilling the criterion under Section 244 is an exceptional circumstance and in the interest of justice, Hence, waiver was granted.

Similarly, in Farhat Sheikh v. Esemen Metalo Chemicals Pvt. Ltd., where the respondents have increased the issued and subscribed capital in Esemen by issue of further 5,000 equity shares which were allotted to applicant thereby reducing the petitioner’s holding from 16.25 per cent. to approximately 8 per cent. The increase in the capital has been made by the respondents only with the ulterior motive of diluting the shareholding of the petitioner and to take away her qualification under Section 399 of the Companies Act, 1956.

Court granted waiver as issue of shares by respondents was an ulterior motive to dilute the shareholding of petitioner thereby taking away her qualification.

Considering the significance of the minority in aforesaid cases, Tribunal granted waiver of locus standi specified in Section 244.

Cases and circumstances where waiver has not been granted

The object of prescribing a qualifying percentage of shares to file petitions is clearly to ensure that frivolous litigation is not indulged in by persons who have no real stake in the company. Hence, the said requirement is vital and can not be overlooked unless public interest is involved.

● In V.K. Mathur And Others v. K.C. Sharma And Ors, petition was originally filed under section 397 and 398 of the Companies Act, 1956. Later, some of those who moved to Central Government back out from giving a written consent to the original petition when made. Members applied to the Company Law Board for an authorisation in terms of section 399(4) of the Act to enable them to move an application under section 397 and 398 in the High Court. Company Law Board authorised “the applicants” to apply to the court under the above section in relation to the company.