Getting ready to implement BRSR from FY 2022-23 (Part-I)

- Team Vinod Kothari & Company, Corporate Law Division (corplaw@vinodkothari.com)

Business Responsibility & Sustainability Reporting (‘BRSR’), which was voluntary as a part of the regulatory provisions for the top 1000 listed entities (by market capitalization) for FY 2021 – 22, is now all set to become mandatory from FY 2022–23 onwards. BRSR is intended to serve as a single focal point for all non-financial disclosures relating to the company that will enable the stakeholders to understand the approach of the company on different issues such as sustainability, responsible business conduct, manner of dealing with stakeholders, etc. With only a few weeks left for the onset of FY 22-23, it is time for companies to get into immediate action, as there is evidently a lot of work to be done.

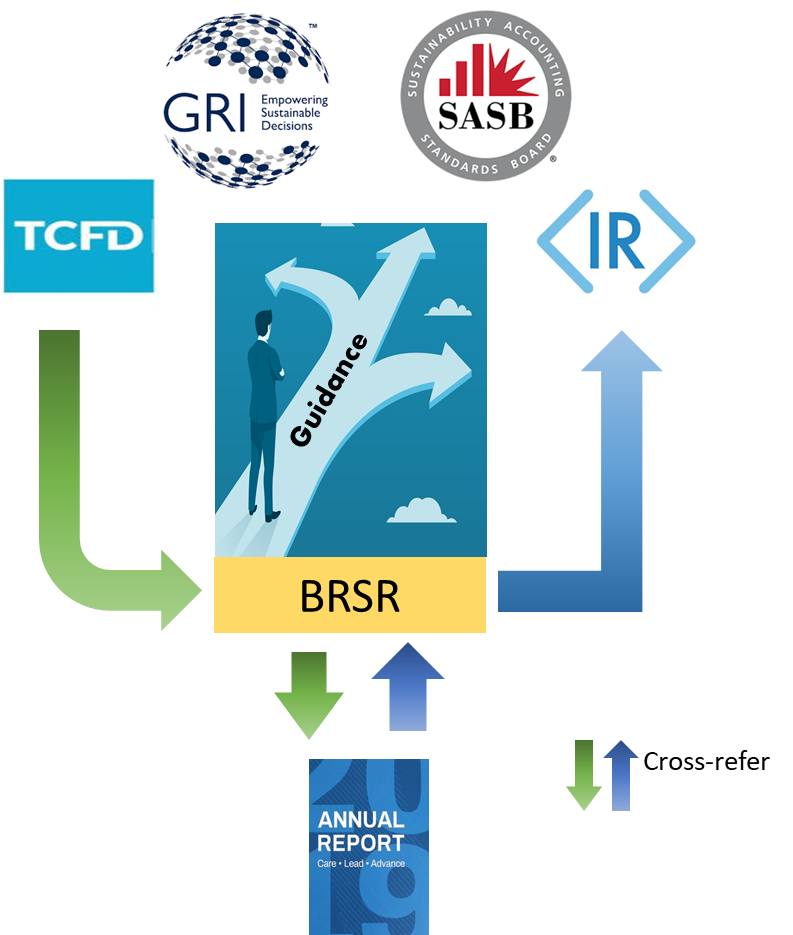

Based on the nine principles of National Guidelines on Responsible Business Conduct (‘NGRBCs’), BRSR in the real sense is actually an expanded and improved version to the existing BRR format. Our article on the additional cartload of details in BRSR as compared to BRR had given a firsthand of the additionalities involved in moving to BRSR. Although based on the same principles, BRSR is much more comprehensive as compared to its former counterpart. . Further, it is notable that as one of the universally accepted sustainability standards, Global Reporting Initiative Standards (‘GRI Standards’) can be closely referred for the enhanced requirements under BRSR and therefore, serve as a guidance for reporting under BRSR.

Having understood that the set-up of the overall framework for the reporting requirements under BRSR is likely to be a challenge to the corporates, this article has been prepared to aid in understanding the additional requirements as well as adopt an appropriate approach for preparing the same. This write up contains an inclusive guidance from the GRI Standards as well as several actionables. We have another comprehensive article dealing with the MCA recommendations on making BRR a fully loaded electronic form.

Interoperability of reporting and sector specific issues:

There are some entities which may have adopted various international sustainability reporting standards such as GRI, SASB, Integrated Reporting etc. To avoid repetition of information, SEBI vide its Guidance note has clarified that the reporting entities may provide a cross-referencing of the disclosures made by it based on the internationally accepted framework while making the relevant disclosures under the BRSR format. Also, for that matter if the required information has been disclosed in the annual report, cross reference to the same can also be provided.

Further, there might be disclosures under the BRSR format which are irrelevant for companies operating under specific sectors. In order to address such issues, it has been clarified by SEBI that the format of BRSR is generic and hence it is absolutely possible that some of the disclosures provided in the BRSR format may not be relevant to an entity belonging to a particular sector. In such a case, the entity may mention that the disclosure is not applicable along-with reasons for the same.

Guiding through the principle-wise disclosures

BRSR is a notable extension of BRR which provides not just for quantitative but also qualitative disclosures. The disclosure requirements under BRSR and its format is expected to bring in more standardization which in turn will help in effective comparability across companies.

Further, the disclosures provided under BRSR bear a close resemblance to the GRI standards and hence, the guidance for reporting under various criteria provided in the BRSR format can be taken from the relevant GRI standards as and when required.

The principle-wise guidance from GRI and additional actionable involved under BRSR are discussed below:

Principle 1: Business conduct to be ethical, transparent and accountable

Owing to heightened scrutiny from investors regarding corporate governance practices in an organization, it is imperative that business houses conduct their operations in a transparent manner and redress grievances of stakeholders, if any. The first principle under the BRSR reporting regime is based on the above premise and requires companies to report on such practices.

| Actionable involved under BRSR |

| Training and awareness programmes 1. Conducting training and awareness programmes for directors/KMPs/employees/workers ( ‘Participants’) ● Reviewing the manner for imparting training to each category of the Participant. ● Identification of codes and policies to be framed or updated for training purposes. Penalties and Fines 2. Providing details of fines / penalties /punishment/ award/ compounding fees/ settlement amount paid in proceedings by the entity or by directors / KMPs in the financial year. 3. Providing details of appeal/ revision preferred in cases where monetary or non-monetary action has been appealed ● Identification of laws under which the fine/ penalty/ awarded/ compounding fees etc. are to be considered under point (2) ● Fixation of thumb rule for ascertaining the specific cases under the above which requires reporting in terms of being material under Regulation 30 of the Listing Regulations. Framework for Anti-Bribery Cases (‘ABC’) 4. Forming an anti-corruption/anti-bribery policy. The disclosure on the anti-corruption or anti-bribery policy may include the following: ● Set -up or review of the risk assessment procedures and internal controls ■ Mechanism to deal with complaints on bribery / corruption ■ Coverage of trainings on anti-corruption issues ● Providing details of number of Directors/KMPs/employees/workers against whom disciplinary action was taken by any law enforcement agency for the charges of bribery/ corruption. ■ Bifurcation of the roles and responsibility of the officers of the company in case of identification and dealing with ABC Conflicts of Interest 5. Providing details of number of complaints received in relation to issues of Conflict of Interest of the Directors/KMPs ● Identifying the level of conflict of interest that requires reporting ● Defining conflict of interest at each reportable level 6. Providing details of any corrective action taken or underway on issues related to fines / penalties / action taken by regulators/ law enforcement agencies/ judicial institutions, on cases of corruption and conflicts of interest Value Chain Partners (‘VCPs’) 7. Conducting awareness programmes for value chain partners (‘VCPs’) with respect to any of the nine principles. ● Identifying and defining VCPs ● Framing policies and framework for efficient communication with them 8. Defining the processes undertaken for managing conflict of interest involving Board members. |

| Taking guidance from GRI in implementation |

| 1. Description of reporting entity’s values, principles, standards, and norms of behaviour. 2. Training on identified ethics to new and existing governance body, workers and business partners 3. Responsibility of executive-level positions and highest level of governance body. 4. Use of internal and external mechanisms for seeking advice on ethical behaviour and reporting concerns on adverse behaviour. (i) Availability and accessibility of the mechanisms and independence of same 5. Presence of a non-retaliation policy towards unethical behaviour and corruption. 6. Identifying incidents of corruption – meaning and impact. 7. Procedure and criteria of risk-assessment for corruption and significant risks identified. 8. Business operations that have been assessed for risk of corruption. 9. Extent and stage of training and communication on anti-corruption. 10. Collective action taken to combat corruption like proactive collaboration with peers, governments and the wider public sector, trade unions and civil society organizations. 11. Designing board structure and employee-incentives in a manner to avoid adverse instances of conflict of interest. |

Principle 2: Goods and services to be safe and sustainable

Owing to an increase in demand from consumers for sustainable and safe products, it has become important for companies to incorporate such sustainability practices while designing and manufacturing their products. Principle 2 on BRSR mandates certain disclosure requirements from companies with an aim of ensuring that they are responsive to such requirements.

| Actionables involved under BRSR |

| R&D for improvement of product-related impact on the environment 1. Apportioning a percentage of the R&D budget and capital expenditure investments towards improving the environmental and social impacts of the company’s products. ● Categorizing the products of the company with respect to the probable impact to the society and the environment ● Formulate a policy for measuring and mitigating the negative impact of the company’s products, if any, on the environment and the society at large. ● Fixation of the budget for R&D including the extent, manner, and other modalities for conducting such R&D (including capex). Sustainable sourcing of inputs and reclamation of products 2. Sustainable sourcing of inputs for production. ● Identifying the sustainable sourcing of inputs ● Segregate the products obtained sustainably and otherwise for the purpose of reporting. 3. Processes undertaken for reclaiming products for reusing, recycling and disposing at the end of life. ● Identification of the products that require reclamation exercise by the Company ● Devising the framework for reclaiming products and its management. ● Quantity of reclaimed products that has been reused, recycled and safely disposed of. ● Bifurcate the products reclaimed into different pre-formed categories for ease of reporting. ● Quantity of the products/ packaging material that has been reclaimed as percentage of products sold. EPR[1] 4. Submission of waste collection plan to the Pollution Control Board if Extended Producer Responsibility (‘EPR”) is applicable to the company. ● Identify whether EPR is applicable to the reporting entity. ● Formulation of waste collection plan. Life Cycle Assessment (‘LCA’) 5. Conducting LCA. ● Decide the product line as well as level upto which LCA shall be conducted. 6. Social or environmental concerns arising from the production/ disposal of the products. ● Actions to be taken to address the concerns based on the outcome of assessment conducted in (5). 7. Disclosure of the use of recycled input material used to the total material used in production. ● Setting up the procedures for collecting data from each factory outlet on the quantum of recycled inputs used |

| Taking guidance from GRI in implementation |

| 1. While compiling the information to be reported, the entity shall use the total weight or volume of materials. 2. Exclusion of rejects and recalls of products while compiling information to be disclosed. 3. The processes used to collect and monitor waste-related data. 4. Recycling or reusing of products may be separately disclosed. 5. Recycling of input materials for manufacturing primary products. |

Principle 3: Well-being of employees and employees of value chains

It is a well-recognized fact that employees are a vital part of any business organization. In line with this, the BRSR framework also covers disclosing the welfare and well-being of the employees and VCPs via Principle 3.

| Actionable under BRSR |

| Well-being of employees and workers 1. Measures taken for the well-being of employees and workers. ● Identifying the policies to be framed (Such policies can include health/medical/accident insurance, maternity/paternity benefits, day care facilities etc.) Providing details of retirement benefits provided to employees/workers for the current and the previous financial year. ● Identify the applicable laws on the entity for providing retirement benefits. Plant and office assessment 2. Ensuring that the premises/offices of the entity are accessible to differently abled employees and workers ● Identify the steps to be taken for making the premise of the entity accessible to differently abled workers and employees. This may include wheelchair ramps, signage braille etc. 4. Forming an equal opportunity policy as per Right of Persons with Disabilities Act, 2016. 5. Providing details of Return to work and Retention rates of permanent employees and workers that took parental leave. 6. Forming a mechanism to receive and redress grievances for permanent and other employees and permanent and other workers. 7. Providing details of membership of employees and worker in association(s) or Unions recognised by the company 8. Providing training to employees and workers on health & safety measures and skill upgradation. 9. Conducting performance and career development reviews of employees and workers. ● Deciding the frequency of such reviews. 10. Implementing a health and safety management system ● Laying down processes to be undertaken for identifying work-related hazards and assessing risks on a routine basis. ● Laying down processes for reporting work related hazards for workers. ● Providing access to non-occupational medical and healthcare services to employees and workers 11. Providing details of safety related incidents that occurred in the current as well as previous financial year. 12. Implementing measures to ensure a safe and healthy workplace 13. Providing details of complaints made by employees and workers on working conditions and health & safety. ● Appointment of person/ committee (‘authority’) for looking into the complaints received. ● Action taken by the authority on the complaints received. 14. Conducting assessments on whether the plants and offices of the company and reporting on the following metrics: ● Health and safety practices ● Working conditions ● Appoint the person who is to conduct the assessment (it can be carried out by the company/statutory authority/third party). 15. Providing details of any corrective action taken or underway to address safety-related incidents. 16. Extending life insurance or compensatory package in the event of death of employees or workers. 17. Providing details of the number of employees / workers having suffered high consequence work related injury / ill-health / fatalities, who have been rehabilitated and placed in suitable employment or whose family members have been placed in suitable employment. 18. Providing transition assistance programs to facilitate continued employability and the management of career endings resulting from retirement or termination of employment. ● Formulation of the program based on the requirements of the reporting entity. ● Decide the frequency of such programs. Well-being of VCPs 19. Implementing measures to ensure that statutory dues have been deducted and deposited by the value chain partners. 20. Conducting assessment of value chain partners with respect to the following : ● Health and safety practices ● Working conditions 21. Providing details of any corrective actions taken or underway to address significant risks / concerns arising from assessments of health and safety practices and working conditions of value chain partners. |

| Taking guidance from GRI in implementation |

| 1. Performance and career development review based on criteria known to the employees and superiors. 2. Grievance Mechanisms can be industry, multi-stakeholder or other collaborative initiatives. 3. Describing type of occupational health and safety professionals responsible for the management system. 4. Defining worker and benefit for the purpose of this principle 5. Formula to calculate return rate and retention rate 6. Contents of Transition assistance programs provided to support employees who are retiring or who have been terminated 7. Definition of value chain 8. Definition of high consequence work related injury |

Principle 4: Responsiveness to Stakeholders’ interests

The stakeholder group of a company is diverse and large. Each stakeholder has a different expectation from the company. It is important for companies to take the interests of all stakeholders into consideration while simultaneously pursuing its business objectives of growth and development. Principle 4 of BRSR asks companies to report about their stakeholders and the engagement practices with such stakeholders.

| Actionable under BRSR |

| Identifying stakeholders, key stakeholders and marginalized stakeholders 1. Process for identification of key stakeholders. ● Stakeholders include investors, shareholders, employees and workers (and their families), customers, communities, value chain members and other business partners, regulators, civil society actors, and media. ● Basis of determining the stakeholders of the entity. ● Based on the total number of stakeholders identified, categorize it into the groups to identify with whom to engage and not to engage. ● Understanding the level of and extent of engagement required with each category of stakeholder. 2. Listing of the stakeholders identified as key stakeholders. ● Identify whether the stakeholder is identified as a vulnerable/marginalized group. ● Establishing the channels for communication with stakeholders. 3. Providing the processes for consultation between stakeholders and the Board on economic, environmental and social topics. ● Formulation of process for providing feedback obtained to the Board. 4. Laying down the framework for incorporating the inputs obtained in (3) in formulation of policies. ● Identify the arrangements necessary for addressing the concerns. 5. Identify the arrangements necessary for addressing the concerns of vulnerable/ marginalized stakeholders. |

| Taking guidance from GRI in implementation |

| 1. Definition of stakeholders 2. Principles for effective stakeholder consultation ● Aligning with international standards ● Collective bargaining, ● Genuine consultation involves proper dialogue between parties ● Affected parties to understand the impact of change. 3. Definition of vulnerable/marginalized groups |

Principle 5: Promotion of Human Rights

It is quite common for companies to indulge in abusive practices, leading to exploitation of workers. While it is seemingly difficult for even the strictest of regulations to put a complete end to such abusive practices, the regulators’ approach has been that of requiring companies to report on the practices adopted by them to curb such violations and the remedy provided to employees who report such instances of human rights issues at the workplace. The new BRSR framework aims to mandate certain additional disclosures to ensure that companies respect and properly report on their human rights practices.

| Actionable under BRSR |

| Training and awareness on human rights issue 1. Providing training to employees/workers on human rights issues and policies of the company 2. Providing details of minimum wages paid to employees and workers. ● Computation of the minimum wages to be paid as per the provisions of Labour Code. 3. Providing details of salary/remuneration/wages paid to directors/KMPs/employees/workers ● Computation of median salary/remuneration/wage paid for the purpose of reporting. 4.Constituting a focal point (Individual/ Committee) responsible for addressing human rights impacts or issues caused or contributed to by the entity in conducting its business. Internal mechanism to combat human rights concerns 5. Implementing an internal mechanism to redress grievances related to human rights issues. ● Identifying the relevant laws under which the human rights concern can be raised ● Taking preventive actions under respective departments 6. Providing details on the number of complaints made by employees/workers during the year and pending resolution as at the end of the year for the current financial year and the previous financial year wrt the following issues: ● Sexual Harassment ● Discrimination at workplace ● Child Labour ● Forced Labour/Involuntary Labour ● Wages ● Other human rights related issues 7. Implementing mechanisms to prevent adverse consequences to the complainant in discrimination and harassment cases. ● Familiarization of the workforce on the protective policies available in the company to protect them against harassment and discrimination 8. Incorporating human rights requirements as part of the business agreements/contracts 9. Providing details on the % of plants and offices of the company that were assessed for : ● Child labour ● Forced/involuntary labour ● Sexual harassment ● Discrimination at workplace ● Wages ● Others 10. Providing details of any corrective actions taken or underway to address significant risks / concerns arising from the assessments at point 9 above 11. Providing details of a business process being modified / introduced as a result of addressing human rights grievances/complaints. 12. Conducting human rights due diligence ● Identifying the scope and coverage of such due diligence 13. Ensuring that the office/premises of the company are accessible to differently abled visitors ● Identifying the requirements for such visitors as given in the Rights of Persons with Disabilities Act, 2016 14. Conducting assessment of VCPs on the following issues: ● Sexual Harassment ● Discrimination at workplace ● Child Labour ● Forced Labour/Involuntary Labour ● Wages ● Others 15. Providing details of any corrective actions taken or underway to address significant risks / concerns arising from the assessments at point 14 above. |

| Taking guidance from GRI in implementation |

| 1. Reporting entities should also provide additional information about its values, principles, standards, and norms of behavior. 2. Total hours during the reporting period devoted to training on human rights policies. 3. Training of employees for making them aware of human rights. 4. Employees of third- party organisations who have also been included in calculation of the total employees trained during the reporting period. 5. Total contracts that include human rights clauses. 6. Operations of the entity that has undergone human rights impact assessment. 7. Suppliers assessed for social impacts. 8. Social impacts identified in the supply chain. |

Principle 6: Protection and restoration of environment

Considering the ever growing concerns around issues such as climate change and sustainable use of resources, it has become imperative for companies to factor in such concerns in the way they operate and plan for the future. Principle 6 aims to ensure that companies are transparent about their sustainability practices and make adequate disclosures on their usage of the shared natural resources.

| Actionable under BRSR |

| Energy consumption data 1. Computing total energy consumption and total energy intensity of the company in the current financial year and the previous financial year ● Identifying the sites for energy consumption ● Reviewing the green energy scheme beneficiaries 2. Identifying whether the company has any sites/facilities identified as designated consumers under the Perform, Achieve & Trade (PAT) Scheme of the Govt. of India. Details of water, air, liquid and hazardous waste discharge 3. Providing details of water usage and treatment 4. Implementing a mechanism for zero liquid discharge 5. Providing details of air emissions (other than GHG emissions) and greenhouse gas emissions of the company for the current financial year and the previous financial year 6. Implementing a project related to reducing greenhouse gas emissions 7. Implementing waste management practices in the company. It shall cover dealing with the following types of waste : ● Plastic waste ● E-waste ● Bio-medical waste ● Construction and demolition waste ● Battery waste ● Radioactive waste ● Other Hazardous waste ● Other Non-hazardous waste generated 8. Implementing a strategy to reduce usage of hazardous and toxic chemicals in the company’s products and processes and the practices adopted to manage such wastes. 9. Obtaining environmental approvals/clearances if the company has operations/offices in/around ecologically sensitive areas ● Ecologically sensitive areas include national parks, wildlife sanctuaries, biosphere reserves, wetlands, biodiversity hotspots, forests, coastal regulation zones etc. 10. Conducting environmental impact assessment of projects undertaken by the company based on applicable laws in the current financial year ● The assessment may be conducted by an independent external agency ● The results of such assessment shall be communicated in public domain. 11. Ensuring compliance with the applicable environmental law/regulations/guidelines in India ● The company shall identify all the environmental law/regulations/guidelines the provisions of which are applicable on the company ● Provide details of non-compliance and the fines/penalties/action taken by regulatory authorities such as pollution control boards or by courts 12. Forming a business continuity and disaster management plan 13. Assessing any significant adverse impact that was caused to the environment which arose from the value chain of the company ● The company shall form mitigation or adaptation measures to minimize such adverse impact |

| Taking guidance from GRI in implementation |

| 1. Report management approach for computing emissions 2. Methodologies adopted to report different emissions under this principle 3. While computing the information required under this principle, the reporting organization should, if subject to different standards and methodologies, describe the approach to selecting them. |

Climate change has been an area of increasing concern and for obvious reasons, dealing with the same is a responsibility of the corporates as well, as dealt with in our article Corporate Responsibility towards Climate Change.

Principle 7: Engagement with public and regulatory policy making

Large companies, owing to their multinational presence have the potential to impact and influence regulatory policy, which eventually results in defining the growth trajectory of the economy. Hence, they should ensure that they exercise their responsibility in a transparent manner keeping in mind the interests of the larger economy.

| Actionable under BRSR |

| 1. Affiliations with trade and industry chambers/ associations. ● Identifying the chambers/ associations for associating based on the sector in which the entity operates. 2. Corrective actions taken or underway on issues relating to anti-competitive conduct based on adverse orders from regulators. ● Pre-deciding the appropriate frequency for review of the actions taken. ● Appoint the person to be responsible for review. 3. Public policy positions advocated by the entity. |

| Taking guidance from GRI in implementation |

| 1. Include memberships at the organizational level in associations 2. Anti-competitive behavior – actions that can result in collusion with potential competitors, with the purpose of limiting the effects of market competition, such as – ● fixing prices or coordinating bids; ● creating market or output restrictions; ● imposing geographic quotas; ● allocating customers, suppliers, geographic areas, or product lines. |

Principle 8: Inclusive growth and equitable development

Owing to the prevalent inequalities & imbalances in the society, it is a moral obligation of all individuals and corporations to contribute towards building a more equitable and prosperous nation. Companies are also required to disclose their practices towards accomplishing such an objective, thus enabling the stakeholders to identify whether such an organization fulfills its social responsibility or not.

| Actionable under BRSR |

| Social Impact Assessments (SIA) 1. Ascertaining the applicability of SIA of projects undertaken by the reporting entity. ● Deciding the frequency of assessment to be conducted during the reporting period. ● Evaluation of the outcome of the assessment for taking up corrective actions if required. Rehabilitation and Resettlement (R&R) exercise 2. Projects of the reporting entity taken up for R&R . ● Understand the meaning the of R&R and its relevance with respect to the company ● Pre-deciding the basis based upon which it shall be taken up for R&R. 3. Redressal of the grievances of the local community. ● Defining the local community. 4. Input materials directly sourced from the MSME/ small producers. ● Identify the materials to be procured from MSMEs and small producers. 5. Actions taken to mitigate the negative impacts identified in the SIA. ● Fixation of the steps to be undertaken for identifying the impacts as negative or positive. CSR Projects and its impact 6. CSR projects undertaken in the aspirational districts identified by the government bodies. 7. Formulation of Preferential procurement policy. ● Bifurcation of the procurement made from marginalized /vulnerable groups and other suppliers. 8. Benefits derived from intellectual property based on traditional knowledge. ● Identify the intellectual properties of the reporting entity that is based on traditional knowledge. 9. Providing details of corrective actions taken in any adverse order relating to intellectual property involving traditional knowledge. 10. Identify the beneficiaries of the CSR projects carried out by the company. |

| Taking guidance from GRI in implementation |

| 1. Social Impact Assessment (SIA) projects undertaken during the reporting period. 2. Public disclosure of results of the assessment. 3. Formulation of local community grievance processes. 4. Formulation of effective stakeholders’ engagement plans. 5. Reporting of negative impacts on communities because of business conduct by the reporting entity. 6. Senior management personnel hired from the local community. |

Principle 9: Engagement with consumers

Over the years, businesses have gravitated towards becoming completely consumer centric, thus leading to consumers deciding the success or failure of the organization. Hence, it is essential that consumers make safe and informed choices while procuring goods and services. Principle 9 is intended to ensure that companies provide relevant information to consumers and redress their grievances, if any, thus improving the overall consumer experience.

| Actionable under BRSR |

| Significance of consumer complaints and feedback 1. Implementing mechanisms to receive and respond to consumer complaints and feedbacks Informing the consumer on the probable environmental impact. 2. Providing details on turnover of products and/ services as a percentage of turnover from all products/service that carry information about: ● Environmental and social parameters relevant to the product ● Safe and responsible usage ● Recycling and/or safe disposal 3. Providing details of number of consumer complaints received during the year and pending resolution as at the end of the year for the current financial year and the previous financial year wrt the following : ● Data privacy ● Advertising ● Cyber-security ● Delivery of essential services ● Restrictive Trade Practices ● Unfair Trade Practices ● Others 4. Product recalled on account of safety issues ● Provide a bifurcation between voluntary recalls and forced recalls. 5. Forming a framework/ policy on cyber security and risks related to data privacy. ● Defining cyber security and understanding its probable impact on the company ● Identifying the cyber related risk to the data privacy 6. Providing details of any corrective actions taken or underway on issues relating to advertising, and delivery of essential services; cyber security and data privacy of customers; re-occurrence of instances of product recalls; penalty / action taken by regulatory authorities on safety of products / services. 7. Providing information on products and services of the company on different channels/platforms 8. Informing and educating consumers about safe and responsible usage of products and/or services. 9. Devising mechanisms to inform consumers of any risk of disruption/discontinuation of essential services. 10. Displaying product information on the product over and above what is mandated as per local laws. 11. Carrying out surveys with regard to consumer satisfaction relating to the major products /services of the entity. 12. Details of data breaches. ● Identify the impact of such breaches. ● Identify the information involved. |

| Taking guidance from GRI in implementation |

| 1. Products and services for which health and safety impacts are assessed for improvement. 2. Non-compliances relating to health and safety impacts of products and services. 3. Complaints received concerning the breach of consumer privacy. 4. Measures taken to ensure security of personal data of the consumers collected by the entity. |

Conclusion

While it is important for businesses to remain financially sound and report on the financials in a transparent and effective manner, it is equally important for them to be cautious about the way their operations affect the environment and the society at large; and factor in sustainability practices in their day to day business operations. Looking at the vast contents of the BRSR format, companies are expected to initiate the actions at the earliest so that they are in a position to appropriately report on the same at the end of FY 2022-2023. As discussed in this article, while the GRI Standards are one of the guiding factors to interpret and report, there are several other international reporting standards which serve the same purpose.

BRSR is a crucial step taken in this direction as it will make the companies focus to a great extent on the reporting of such sustainability practices in a bid to ensure that companies fulfill their obligations towards the surroundings in which they operate and there is a more inclusive and sustainable economic growth.

While we discuss the “what to do” part of implementing BRSR in this article, the “how to do” part of the same has been dealt with in the Part II of this article.

[1] Uniform Framework for EPR under Plastic Waste Management Rules

EPR under e-waste management rules

Our resource center on Business Responsibility and Sustainable Reporting can be accessed here –

Hi,

I was going through your blog on BRSR Report. I had a doubt regarding the same.

Since it is mentioned that a company either files a consolidated or a standalone BRSR report, is it up to the company to decide how they want to file it, or are there some criteria they need?

E.g., while going through the BRSR report of a company, they mentioned 32 subsidiaries, associates, and joint ventures. Still, they have issued a standalone report, whereas another company has mentioned only three subsidiaries and holdings but has reported a consolidated report.

Can you please give clarity on this? It will help a lot.

As per the format prescribed by SEBI, the company may decide its reporting boundary in relation to BRSR reporting, i.e., whether to report the same on a standalone basis (i.e. only for the entity) or on a consolidated basis (i.e. listed entity along with its group companies whose accounts are consolidated). There are no specified criteria for the same.

Dear Mr Vinod,

Any idea about how many Indian companies have reported BRSR voluntarily for FY 2021-22 ?

With Regards,

Manish