FAQs on Type-I NBFC Registration Exemption

– Anita Baid, Dayita Kanodia & Chirag Agarwal | finserv@vinodkothari.com

Loading…

Loading…

– Anita Baid, Dayita Kanodia & Chirag Agarwal | finserv@vinodkothari.com

Loading…

– Team Finserv | finserv@vinodkothari.com

Existing companies may apply within 6 months of 1st July; new companies may avoid registration on satisfying Type 1 and asset size conditions

The RBI’s relief to exempt pure investment companies from exemption from regulation, is now in final shape. We have earlier commented on the draft Amendment Directions. The final amendments in Directions, notified on 29th April, 2026, accept some of the public feedback. However, the condition that the NBFC seeking exemption should not have any debt on the liability, nor any debt on the asset side, even if from/to group entities, remains.

The exemption window opens on 1st July, based on asset size, no customer interface, no public funds and some other conditions (discussed below). The window remains till 31st Dec., 2026; however, even in future, it will be open for NBFCs to opt to exit from registration.

Read more →

The RBI’s proposed relief to exempt pure investment companies from exemption from regulation is not a cakewalk but a hurdle race. It is not an exemption that comes in auto mode; you need to earn the right to be exempt. Some of the important pre-conditions that the RBI has proposed are:

| Type of NBFC | Options Available |

| NBFCs holding Type I Registration as on April 1, 2026 | Option 1: Apply for deregistration Option 2: Continue to remain as Type I NBFC |

| Entities that fulfil the conditions for Unregistered Type I NBFC, after April 1, 2026 | Option 1: Satisfy the conditions under 66A and remain unregistered [see box on Conditions Subsequent] Option 2: Apply for registration as Type I NBFC |

| NBFCs not having a customer interface and public funds and having an asset size below ₹1000 crores, but not registered as Type I | Option 1: Apply for deregistration Option 2: Apply for registration as Type I NBFC to avail regulatory exemptionOption 3: Maintain status quo |

| NBFCs not having a customer interface and public funds and having asset size above ₹1000 crores, but not registered as Type I | Option 1: Apply for registration as NBFC Type I Option 2: Apply for registration as NBFC Type II, in case of changes in business model |

Several NBFCs that have been registered with the RBI before the concept of Type 1 was introduced in 2016 may not have the CoR as a Type 1 NBFC in spite of the fact that as on date they don’t have access to public funds nor any customer interface. Such an NBFC with an asset size less than ₹1000 crores will still have an option to apply for deregistration, subject to the satisfaction of the conditions prescribed. However, such NBFCs in case they decide to maintain the status quo will not be eligible for the regulatory exemption available to Type 1 NBFCs.

If an entity carries investment activity with owned funds, within a limit of ₹1000 crores, does it need RBI registration? The answer seems to be – no. Such a company obviously does not have to go through the rigour of seeking registration first, and then qualifying for an exemption.

The company in question still has to satisfy the exemption conditions; and the auditor will need to give an exception report. The meaning of exception report is that if there is a breach of any of the conditions of exemption, or there is any breach of any other provisions of the law, the auditor shall be required to make an exception report.

Notably, CARO Order also requires auditors to comment on adherence to RBI regulations, which, in future, will include these conditions too.

Is the requirement of asset size being within ₹1000 crores based on stand-alone financial statements, or will the assets of companies within the group be aggregated, as is done for the purpose of determination of the middle layer status of companies?

It seems that the aggregation requirement is not there for the Type 1 exemption.

The basis for this is FAQ 13, which states as follows:

Q13. As per regulations of the Reserve Bank, total assets of all the NBFCs in a Group are consolidated to determine the classification of NBFCs in the Middle 11 Layer. What shall be the treatment given to ‘Type I NBFCs’ and ‘Unregistered Type I companies’ in this regard?

Ans: For aggregation purposes, the asset size of ‘Type I NBFCs’ shall be considered but asset size of ‘Unregistered Type I NBFCs’ shall not be considered. It is emphasized that ‘Type I NBFCs’ shall always be classified in Base Layer regardless of such aggregation.

Are the exemption conditions, that there is no access to public funds and no customer interface, merely a statement of intent, or must also be borne out by the conduct in any of the past 3 financial years? Looking at the definition in para 6 (14A), which reads “Not accepting public funds and not intending to accept public funds”, and likewise, “Not having customer interface and not intending to have customer interface”, it appears that the exemption conditions are both a statement of fact as well as intent. If one is negated by the fact, a mere statement of intent may not help.

However, assume there are isolated instances of intra-group loans taken or intra-group loans given. The transactions are not indicating a “business model”, at least the ones on the asset side. Are we saying that the breach of the conditions of “no public funds” and “no customer interface”, at any time during the last 3 years, will disentitle the exemption?

We do NOT think so. There are two reasons to say this:

In our view, since the deregistration application has to be made within September 30, 2026, the audited financials for FY 25-26 must have been prepared. Hence, the last three financial years that would be considered are FY 23-24, 24-25 and 25-26.

It is usually hard to get a relief from a regulator, as relief is seen as a prize that you earn. If the idea was based on the premise that what does not matter for the financial system, and is still being regulated, is a burden both for the regulator and for the regulated, there would have been a more welcoming approach to exemption. Specifically:

Team Finserv | finserv@vinodkothari.com

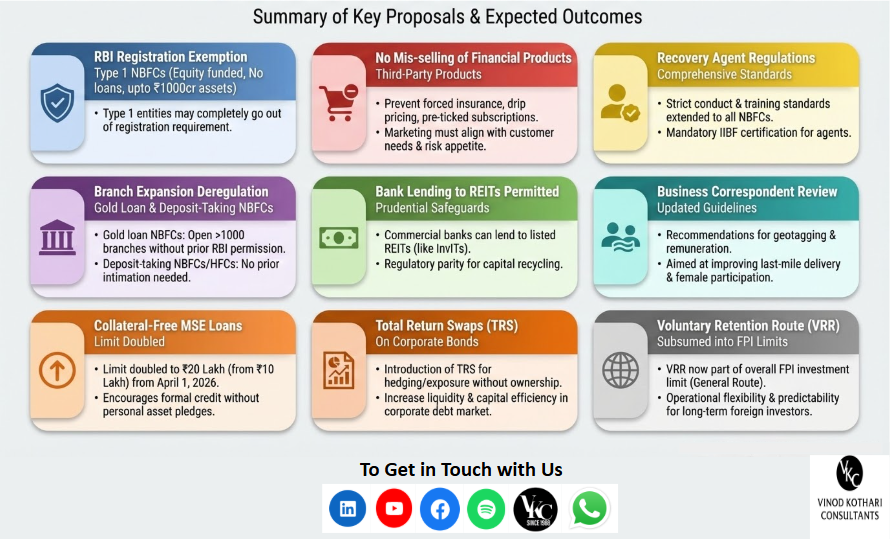

The Budget 2026 may not have brought any significant regulatory amendments or reliefs for the financial sector entities, however, the regulator has proposed a box full of surprises for the regulated entities. The Statement on Developmental and Regulatory Policies dated February 6, 2026 has proposed various significant changes. The measures span a wide spectrum, from exempting Type 1 NBFCs (with no public funds and no customer interface) from registration, to stricter norms on sale of third-party products, a harmonised recovery agent framework, permission for bank lending to REITs and an increase of collateral-free loan limits for MSMEs, among others. While the detailed guidelines for each of the proposals are yet to be issued, we provide a quick snapshot and implications of these proposals.

After several years of regulatory supervision over investment companies and small size NBFCs, the RBI has proposed to exempt NBFCs having no public funds and customer interface, with asset size not exceeding ₹1000 crore, from the requirement of registration. This will bring such NBFCs, which are commonly referred to as Type 1 NBFCs, outside the purview of RBI supervision, compliance and reporting requirements.

Earlier, access to public funds and customer interface were factors for applicability of several regulations, but not for complete exemption.

What is Customer Interface[1]

Para 6(4) of under the RBI (NBFCs – Registration, Exemptions and Framework for Scale Based Regulation) Directions, 2025 (“RBI Master Directions”) defines customer interface as “interaction between the NBFC and its customers while carrying on its business”

In essence, customer interface exists where an NBFC directly deals with customers in the course of its business, such as sourcing borrowers, communicating loan terms, collecting repayments, or addressing grievances. The concept focuses on direct dealing/direct public engagement between the NBFC and its customers in the conduct of its business.

Entities engaged in capital market transactions such as trading in shares, investments etc are not seen as having customer interface.

As to whether lending intragroup results in customer interface, the question is contentious – see our article here. .

Currently, NBFCs that do not have any customer interface are exempt from the fair lending practice norms, KYC norms, CIC reporting requirements are such other customer centric compliances.

What is “Public Funds”

Public funds is defined under RBI Master Directions as “includes funds raised either directly or indirectly through public deposits, inter-corporate deposits, bank finance and all funds received from outside sources such as funds raised by issue of Commercial Papers, debentures etc. but excludes funds raised by issue of instruments compulsorily convertible into equity shares within a period not exceeding five years from the date of issue.”

The expression public funds is much wider than public deposits; public deposits are only one part of it. Public funds broadly mean all funds raised by an NBFC from sources other than its own or self-funds. The definition is inclusive and covers multiple forms of debt funding, while also leaving room for other similar sources. Importantly, public funds are to be understood in contrast with self-funds, such as equity capital, which represent ownership and not fundraising. Funds raised from group entities are generally not regarded as public funds; however, if a group entity merely acts as a conduit for funds raised from the outside sources, such funds will still carry the character of public funds due to the direct and clear nexus with the public source.

The use of public funds is a key trigger for prudential regulation, as the RBI seeks to ensure safety and stability where public money is involved. In the absence of access to public funds, NBFCs are exempted from complying with prudential regulations, liquidity risk management framework and LCR norms.

Why Customer Interface and Public Funds Are Important

The RBI uses customer interface and public funds as risk filters to determine the extent of regulatory oversight required for an NBFC. Entities that neither deal with external customers nor raise public funds are considered to pose minimal consumer and systemic risk.

In line with this risk-based approach, the RBI has proposed to exempt NBFCs with no customer interface and no public funds, and with asset size not exceeding ₹1,000 crore, from the requirement of registration.

Banks and NBFCs routinely distribute third-party products alongside extending their core financial services. Such distribution is undertaken both through physical branches and through digital lending applications and platforms. It has, however, been frequently observed that certain banks and NBFCs take undue advantage of borrowers by using deceptive practices and dark patterns to sell third party products.

Dark patterns are tricky user interfaces “that benefit an online service by leading users into making decisions they might not otherwise make. Some dark patterns deceive users while others covertly manipulate or coerce them into choices that are not in their best interests[2]. Hence, there comes a need to regulate the same. The Central Consumer Protection Authority (“CCPA”), issued the Guidelines for Prevention and Regulation of Dark Patterns, 2023 to regulate such practices.

Digital lenders themselves may quite often be employing practices such as:

Accordingly, there is a felt need to ensure that third party products and services that are being sold at the bank counters or lending platforms are suitable to customer needs and are commensurate with the risk appetite of individual clients. It has therefore been decided to issue comprehensive instructions to REs on advertising, marketing and sales of financial products and services. The draft instructions in this regard shall be issued shortly for public consultation.

RBI has, from time to time, reminded lenders that they shall remain fully responsible for activities outsourced by them and, accordingly, are accountable for the conduct of their service providers, including recovery agents. In particular, the regulator has emphasised that lenders must ensure that neither they nor their agents engage in any form of intimidation or harassment, whether verbal or physical, during debt recovery.

While detailed guidelines governing the conduct of recovery agents are prescribed for HFCs, similar comprehensive guidelines are currently not specifically extended to NBFCs. RBI has now proposed that it will harmonise all the extant conduct-related instructions on engagement of recovery agents and other aspects related to the recovery of loans for all regulated entities.

An important requirement for recovery agents was with respect to the training of recovery agents. The recovery agents engaged by HFCs are required to undergo the training as prescribed by Indian Institute of Banking and Finance (IIBF) and obtain the certificate from the institute. If such training and certification requirements for recovery agents are extended to NBFCs, it will increase compliance and operational costs due to training expenses, certification fees, and time invested in upskilling agents. NBFCs may also need to strengthen their internal processes for onboarding, monitoring, and periodic re-certification of recovery agents. However, while this may raise short-term costs, it is likely to improve the quality of recoveries, reduce customer complaints and conduct risk, and strengthen long-term operational discipline.

As per the RBI Branch Authorisation Directions, NBFC-ICCs engaged in the business of lending against gold collateral are required to obtain prior approval of the RBI to open branches exceeding 1,000. Further, deposit-taking NBFCs and HFCs are required to inform the RBI and NHB, respectively, before opening any branch.

RBI has proposed to dispense with the requirement of prior approval or intimation for opening branches by such NBFCs. The change is likely to reduce hurdles in opening new branches for gold loan NBFCs, allowing them to expand more quickly and grow their operations.

| Type of NBFC | Erstwhile Requirement | Proposed Requirement |

| Deposit Taking NBFCs | Prior Intimation for the opening of branches | No need for prior intimation |

| HFCs | Prior Intimation to NHB before opening any branch | No need for prior intimation |

| NBFC-ICC (involved in gold lending) | Prior approval is required for branches exceeding 1000 | No need for prior approval |

The draft amendment directions have been issued here.

Banks were originally not permitted to lend to either InvITs or REITs, as these vehicles were created to refinance banks’ exposures in completed projects using market-based investor funds. While bank lending to InvITs was later allowed, subject to a prudential framework prescribed by the RBI. Banks must have a Board-approved policy governing InvIT exposures, covering appraisal, sanctioning, internal limits, and monitoring.

Prior to lending, banks are required to assess critical parameters including sufficiency of cash flows at the InvIT level, ensure that the combined leverage of the InvIT and its underlying SPVs remains within approved limits, and continuously monitor SPV performance, as the InvIT’s repayment capacity depends on these SPVs; banks must also consider the legal aspects of lending to trust structures, particularly enforcement of security. Lending is permitted only where none of the underlying SPVs with existing bank loans is facing financial difficulty, and any bank finance used by InvITs to acquire equity in other entities must comply with existing RBI restrictions.Lending to REITs, however, continued to be prohibited.

Regulatory Cap on Bank Investment in REITs/InvITs:

In view of the strong regulatory, disclosure, and governance framework applicable to listed REITs, it is now proposed to permit commercial banks to lend to REITs, subject to appropriate prudential safeguards. At the same time, the existing lending framework for InvITs will be harmonised with the safeguards proposed for REITs to ensure consistency and parity across both structures.

The proposal allows banks to lend to REITs within a well-defined risk framework, ensuring financial stability is not compromised. The proposal brings regulatory consistency between REITs and InvITs, creating a more uniform and predictable regime. At the same time, it enables efficient recycling of capital from completed real estate and infrastructure projects, supporting new lending without adding significant systemic risk.

A Business Correspondent (‘BC’) acts as an extension of a bank itself, to provide banking related services in areas which do not have access to such services. The intent of the BC model is financial inclusion, in order to connect everyone to the banking system. The scope includes among other things, creating awareness about savings and other products and education and advice on managing money and debt counselling, processing and submission of applications to banks, etc.

The activities to be undertaken by the BCs would be within the normal course of the bank’s banking business, but conducted through the BCs at places other than the bank premises/ATMs. Thus, the scope would not just be limited to marketing, sourcing and distribution of financial products, rather, it would be extended to provide banking services to the customers from the place of business of the BC.

Business Correspondents have been functioning as critical enablers of last mile access to financial services, particularly in respect of underserved, rural, and remote locations. Presently, BCs are regulated through RBI (Commercial Banks – Branch Authorisation) Directions, 2025. The Directions outline the eligibility criteria, due diligence requirements, oversight and monitoring, scope of activities, etc for engaging a Business Correspondent by banks.

RBI had set up a committee, consisting of officials from RBI , Department of Financial Service, Indian Banking Association and NABARD, to comprehensively examine their operations and make suitable recommendations for enhancing their efficiency. Discussions were held on action points of the previous meeting, Geotagging of BCs, Development of BC portal, Penalties imposed by banks on CBCs, Caution Money required from CBCs, BC Remuneration, participation of women in BC workforce etc.

Based on the Committee’s recommendations, the related regulatory guidelines are being reviewed, and the draft amendment directions will be issued shortly.

In 2010, following the RBI Working Group’s report (released March 6, 2010) on the Credit Guarantee Scheme (CGS) under CGTMSE, RBI mandated banks via circular in May 2010 to provide collateral-free business loans up to Rs. 10 lakh to Micro and Small Enterprises (MSEs).

A collateral-free business loan is an unsecured loan for business needs, requiring no pledge of assets like house, car, or property as mortgage until repayment backed by CGTMSE guarantee cover.

| MSEs are defined under the MSMED Act, 2006 and require mandatory Udyam Registration for eligibility, bank loans, priority sector benefits, and CGTMSE coverage—along with no blacklisting, viable project, and engagement in approved manufacturing/service/retail activities. Classifications: Micro enterprise (investment in plant/machinery ≤ Rs. 2.5 crore; turnover ≤ Rs. 10 crore); Small enterprise (investment ≤ Rs. 25 crore; turnover ≤ Rs. 100 crore); and Medium enterprise (investment ≤ Rs. 125 crore; turnover ≤ Rs. 500 crore). Banks must enforce this at branches, linking CGS/CGTMSE usage to staff evaluations for strict compliance. This remains the existing statutory requirement for MSE lending. |

RBI has decided to raise the collateral-free loan limit for MSEs from Rs. 10 lakh to Rs. 20 lakh, applicable to loans sanctioned or renewed on or after April 1, 2026, aiming to improve formal credit access, entrepreneurial activity, and last-mile delivery for collateral-scarce MSEs.

This policy shift represents a watershed moment for India’s grassroots economy, effectively doubling the financial runway for the nation’s most resilient entrepreneurs. By aligning with the PMMY ceiling, the policy ensures that a business’s potential rather than a proprietor’s personal property dictates its growth. This extra funding allows small businesses to move beyond daily expenses and finally invest in better machinery or technology to compete. Furthermore, it opens doors for women and young owners who may not own property to get formal bank support based purely on their performance. Ultimately, this change encourages more businesses to register officially, clearing the path for millions of small units to scale up and create more jobs without the fear of losing personal assets.

A Total Return Swap (TRS) is a derivative contract where a protection buyer exchanges the variable total return of an asset for a fixed return, shielding them from volatility. In this setup, the protection buyers swap the “total return” from the asset pool, with a return computed at a fixed spread on a base rate, say LIBOR. Protection sellers in a TRS guarantee a prefixed spread to protection buyers, who in turn, agree to pass on the actual collections and actual variations in prices on the credit asset to protection sellers. Essentially, the protection seller gains market exposure without a large upfront investment, while the protection buyer hedges their risk. Since protection sellers receive the total return from the asset, protection sellers also have the benefit of upside, if any, from the reference asset.

In India, the corporate bond market has historically lacked deep liquidity. To solve this, the Union Budget 2026 and the RBI have proposed introducing TRS specifically for corporate bonds and credit indices.

This development is a strategic shift toward “capital-efficient” investing. For business professionals, this means institutional investors can now gain exposure to corporate debt or hedge their existing bond portfolios without locking up massive amounts of capital on their balance sheets. By allowing the market to trade the “risk” and “returns” of bonds separately from the bonds themselves, the RBI aims to boost liquidity and make it easier for companies across various credit ratings to raise funds. Ultimately, this reform bridges a critical gap in India’s financial ecosystem, transforming the corporate bond market into a more active, transparent, and globally competitive space.

The draft amendment directions have been issued here.

Voluntary retention route for investment bonds and G-secs has been merged and made a part of the limit assigned for regular investments by FPIs; as a result, FPIs that commit to keep funds for at least 3 years may escape the minimum residual maturity requirement and the limits on investment in a bond issue by a single FPI. This introduces significant flexibility for those FPIs that are sure of staying invested in India for a long term, avoiding opportunism while granting them significant flexibility.

According to the Master Direction – Reserve Bank of India (Non-resident Investment in Debt Instruments) Directions, 2025, there are 5 channels of investments in debt instruments by non-resident investors. Under the VRR Route, FPIs are granted various operational exemptions, easing the investment process. VRR was introduced to encourage long term FPI investment in Indian debt markets by offering a dedicated investment channel with greater flexibility.

Given the strong utilisation of the VRR limits and to improve predictability and ease of doing business, the RBI has now decided to subsume VRR investments within the overall FPI investment limits under the General Route, while also providing additional operational flexibilities to FPIs investing through the VRR.

The detailed mechanism governing such limits has been notified here.

[1] Refer to our detailed write up on this topic- https://vinodkothari.com/2025/09/all-in-the-group-and-still-a a-customer/