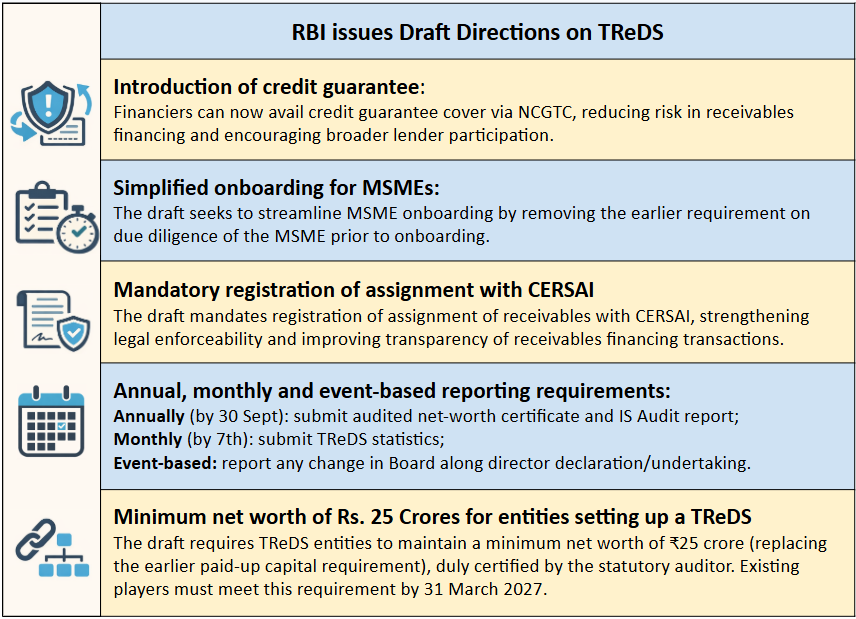

Financiers are now permitted to avail credit guarantee cover (via NCGTC) for exposures on TReDS. This is a significant step towards de-risking receivables financing and encouraging wider participation by lenders. Notably, RBI had already expanded the ecosystem in 2023 by permitting insurers as participants to provide credit insurance cover for such exposures.

🔹 Simplified onboarding for MSMEs:

In line with the Governor’s statement, the draft seeks to streamline MSME onboarding by removing the earlier requirement on due diligence of the MSME prior to onboarding.

🔹 Mandatory registration of assignment with CERSAI:

The draft mandates (earlier recommended) registration of assignment of receivables with CERSAI, strengthening legal enforceability and improving transparency of receivables financing transactions.

🔹Annual, monthly and event-based reporting requirements:

Annually (by 30 Sept): submit audited net-worth certificate and IS/Cyber Security Audit report. Monthly (by 7th): submit TReDS statistics. Event-based: report any change in Board along with director declaration/undertaking.

🔹Minimum net worth of Rs. 25 Crores for entities setting up a TReDS

The draft requires TReDS entities to maintain a minimum net worth of ₹25 crore (replacing the earlier paid-up capital requirement), duly certified by the statutory auditor. Existing players must meet this requirement by 31 March 2027.

Financing needs of MSMEs in India: Working capital constitutes a major part of SMEs’ funding requirements

There are considerable gaps in funding for SMEs: In India, the total addressable demand for external credit is estimated to be USD 173 billion[1] while the overall supply of finance from formal sources is estimated to be USD 441 trillion. The Expert Committee on Micro, Small and Medium Enterprises, constituted by Reserve Bank of India in December, 2018 has estimated the overall gap in India to be USD 238 – 298 billion[2].

Traditional sources of funding are working capital facilities with banks; however, given their unorganised nature, lack of formal financial statements, etc., many SMEs find it difficult to have formal lines of credit from banks.

The marketplace is trying alternative sources of working capital for SME. The avenues tried based on the different components of the working capital:

Accounts receivables

Inventory

Trade Receivables Discounting System (TREDS) Factoring/ supply chain financing

Credit period for accounts payable, funded by way of reverse factoring/ supply chain financing

Trade Receivables Discounting System (TReDS/TREDS)

TREDS is almost India’s own innovation, though it was inspired by Mexico’s NAFIN Cadenas Productivas Program. TREDS as a mechanism for discounting and unitisation of trade receivables was launched in 2014. Currently, there are 4 of them – RXIL, M3, InvoiceMart and C2FO Factoring Solutions Private Limited. The first one is the largest.

Limited number of funding participants. However, given that there are quite a limited number of funding participants in the TREDS ecosystem currently (as informed by some of the participants in the TREDS platform(s), only 5-6 banks are currently actively bidding), there is very little competitive bidding for invoices currently. The cost of funding, we were given to understand, is about 0.25% – 0.40% higher than bank finance, if the buyer happens to be a BBB rated entity.

Supply chain financing is growing, as present-day trade needs to move fast; working capital availability is key to achieving turnover with low spreads, to service the ultimate consumer affordably and efficiently. Supply chain finance is a key mode of financing for upstream procurements as well as downstream supplies by an entity with a good credit standing, say Anchor. Usually, the financing is done by setting a limit based on the Anchor’s credit standing, with a bank or NBFC. Both banks and NBFCs are active in the space. Financing may be done by discounting of supply bills, either accepted by the Anchor as due for payment, or drawn by the Anchor on the dealers/ customers of the Anchor.

Most supply chain financing programs work on first loss guarantee by the Anchor. For the downstream supplies, Anchor usually has to provide a first loss guarantee support, to the extent of 5% to 10% of the pool of receivables funded by a lender under the facility.

Factoring

Factoring law, intended to encourage factoring, has not lived to its purpose due to regulatory overtone. The Factoring Regulation Act was enacted to facilitate and encourage factoring; however, its regulatory stance has served to stifle factoring. Only a handful of NBFCs are currently registered as factors, while banks are not required to register[4]. As a result, the volume of factoring in India is trivial, as compared to global jurisdictions.

Potentialfor securitisation of SME receivables

Direct securitisation by SMEs is not feasible. There are 2 ways in which securitisation of MSME receivables can take place: securitisation of trade receivables by SME itself; and secondly, receivables are funded by intermediaries (banks, NBFCs), aggregated by intermediaries, and securitised by them.

Securitisation by SMEs directly is not feasible, as volumes are not sufficient. Plus, it requires direct access to investors, which is unviable. Hence, the discussion below focuses on securitisation of receivables funded by intermediaries.

Intermediated securitisation is the way the world does it. However, regulations in India have scuttled the possibility. Acquisition of receivables by intermediaries (either on their balance sheet, or in the balance sheets of trade finance conduits) is quite common world-over[5]. However, this activity has not picked up in India, for several reasons:

There is a bar on securitisation of revolving credit facilities in the RBI SSA Directions. Naturally, a trade receivable funding program has to be structured as a revolving facility, to allow the SME continued and assured access to working capital. Issuance of asset backed commercial paper is also barred under the same Directions.

Regulated financial lenders cannot do a securitisation transaction outside of SSA Directions. If unregulated entities (not regulated by the RBI, say, a conduit vehicle) does a securitisation outside of SSA Directions, no regulated lender can invest in such a transaction, as any investment so made will be a full charge against regulatory capital.

As a result, securitisation of trade receivables is currently a near impossibility under the regulatory regime.

Will trade receivables securitisation help?

Table below compares securitisation with TREDS, supply chain financing and securitisation:

TREDS

Supply Chain Financing

Securitisation

Consistent availability of funding

While the funding limits are established based on the rating and credit of the buyer, the funding happens on invoice-by-invoice basis. There is no assurance as to either availability or the cost of funding

As limits are assigned for each vendor/ dealer, there is an assured availability at a pre-agreed cost of funding

As limits are assigned for each vendor/ dealer, there is an assured availability at a pre-agreed cost of funding by the intermediary, who, in turn may take receivables to capital markets

Disintermediation

Involves financial intermediaries

Involves financial intermediaries

Involves intermediaries at the inception, but eventually, the intermediaries offload the receivables to capital market

Burden on banks’ balance sheets

Receivables are on the balance sheet of the lender

Receivables are on the balance sheet of the lender

Receivables are off the balance sheet for regulatory capital purposes

Pricing

While pricing is primarily done on the strength of the Anchor, at times, SME gets good pricing based on the liquidity in the banking system

Pricing is done based on the FLDG support provided by the Anchor; hence, priced based on achor’s credit rating

Availability of capital market access, coupled with credit enhancements may bring down the cost of funding

Policymakers need to enable alternative instruments, and leave the choice to the marketplace. The Table above makes a case for securitisation of trade receivables. Such securitisation does not conflict with TREDS; TREDS may continue as an option, leaving the choice to SMEs /lenders the benefit of choice.

Role of credit enhancements in trade receivables securitisation

The potential structure of securitisation of trade receivables, as it commonly works in global jurisdictions, is as follows:

Figure: Structure of Trade Receivable Securitisation

In essence, there are two levels of credit support – one, at the level of each SME (seller), which sells receivables to the Intermediary/conduit. This is typically by way of over-collateralisation or a first loss facility.

Having thus acquired credit enhanced receivables from the SMEs, the intermediary arranges a program-wide credit enhancement. This enhancement essentially becomes a mezzanine support.

The entire program works as a revolving facility, such that the SME sellers continue to sell receivables on an ongoing basis. On the other hand, the securised paper has a fixed maturity, subject to roll-over at the discretion of the paper holders. Hence, there needs to be liquidity support provided to the conduit, typically by a bank.

Providers of credit enhancement:

SIDBI, as credit enhancer for SME funding, may provide the program credit support.

SIDBI, in turn, may be counter-guaranteed by MDBs

Policy/regulatory changes required:

The bar on securitisation of revolving credit facilities, introduced looking at the experience during GFC, needs to be withdrawn. There is an inherent liquidity risk on the part of the intermediary that does securitisation (the risk that early amortisation triggers may cause the facility to wind down, while the committed funding still will have to be continued by the intermediary), but this may be addressed by appropriate capital charge. Note that there is no bar on revolving credit securitisation either in the EU Capital Directions, or in Basel Securitisation Framework.

Likewise, the bar on issuance of asset backed commercial paper needs to be removed. The provider of liquidity facility needs an appropriate capital charge for the maximum value of the facility.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2024-11-27 16:15:362024-11-27 16:20:09Securitisation of MSME receivables in India

The concept of Trade Receivables Discounting System (TReDS) was introduced by RBI to enable discounting of invoices of MSME sellers against large corporates, including government departments and public sector undertakings, through an auction mechanism to ensure prompt realisation of trade receivables at competitive market rates.

TReDS transactions fall under the umbrella of “factoring business.” Factoring is a financial practice where a company sells its trade receivables, or outstanding invoices, to a third party at a discount in exchange for immediate cash. TReDS platforms provide a digital infrastructure for facilitating such transactions, enabling efficient invoice discounting and promoting liquidity for MSMEs.(Our FAQs on TReDS and the India Factoring Report 2023 can be read here and here)

In a move to further strengthen the TReDS and promote smoother financial transactions, the RBI has announced significant enhancements to the TReDS guidelines. These enhancements are in line with the announcement made by RBI in the Statement on Developmental and Regulatory Policies dated February 8, 2023, to address certain challenges faced by financiers while bidding for low-rated buyers’ payables on TReDS platforms. (Our article on the same can be read here)

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Anita Baidhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngAnita Baid2023-06-13 12:45:312023-06-13 17:12:39Embracing a Wider Scope for TReDS

Receivables or debtors though from the face of it is considered as a positive thing for businesses, however when you lift the tag of positivity one can assess the true color of trade receivables. This essentially means that despite it being classified as an asset it may not be helping the business when required. For instance, ABC Ltd has 1 lakh recorded as debtors in its financials however these debtors are of no substantial use unless it is converted into liquid forms of funds. This in essence is the reason why TReDS was introduced, RBI vide Guidelines for the Trade Discounting System (TReDS) opined that the scheme for setting up and operating the institutional mechanism for facilitating the financing of trade receivables of MSMEs from Corporate and other buyers, including Government Departments and Public Sector Undertakings (PSUs), through multiple financiers is known as TReDS.