A matter of scale in securitisation

Qasim Saif, Vice President and Yuvraj Kundargi, Executive | finserv@vinodkothari.com

Background

The previous financial year witnessed Indian banks entering the securitisation market as originators, marking a positive step towards large-volume transactions. Their participation also raised expectations that non-lending institutions could increasingly come in as investors in such instruments.

Midway through this year, the Reliance group announced a landmark transaction, raising funds through securitisation of loan receivables of its group entities. These loans are proposed to be repaid from the receivables from usage of digital telecommunication infrastructure by Reliance group companies.

Issuances were made by three trusts: Radhakrishna Securitisation Trust, Shivshakti Securitisation Trust, and Siddhivinayak Securitisation Trust with maturities of approximately three, four and five years respectively, and carrying an average coupon of 7.75%.

This transaction represents the largest securitisation issuance in India to date. It is marked by a unique structure where the transaction is not supported by credit enhancements from the originator. Instead, the obligors’ rating, supported by a guarantee from Reliance Industries Ltd., enabled the securities to achieve a AAA rating.

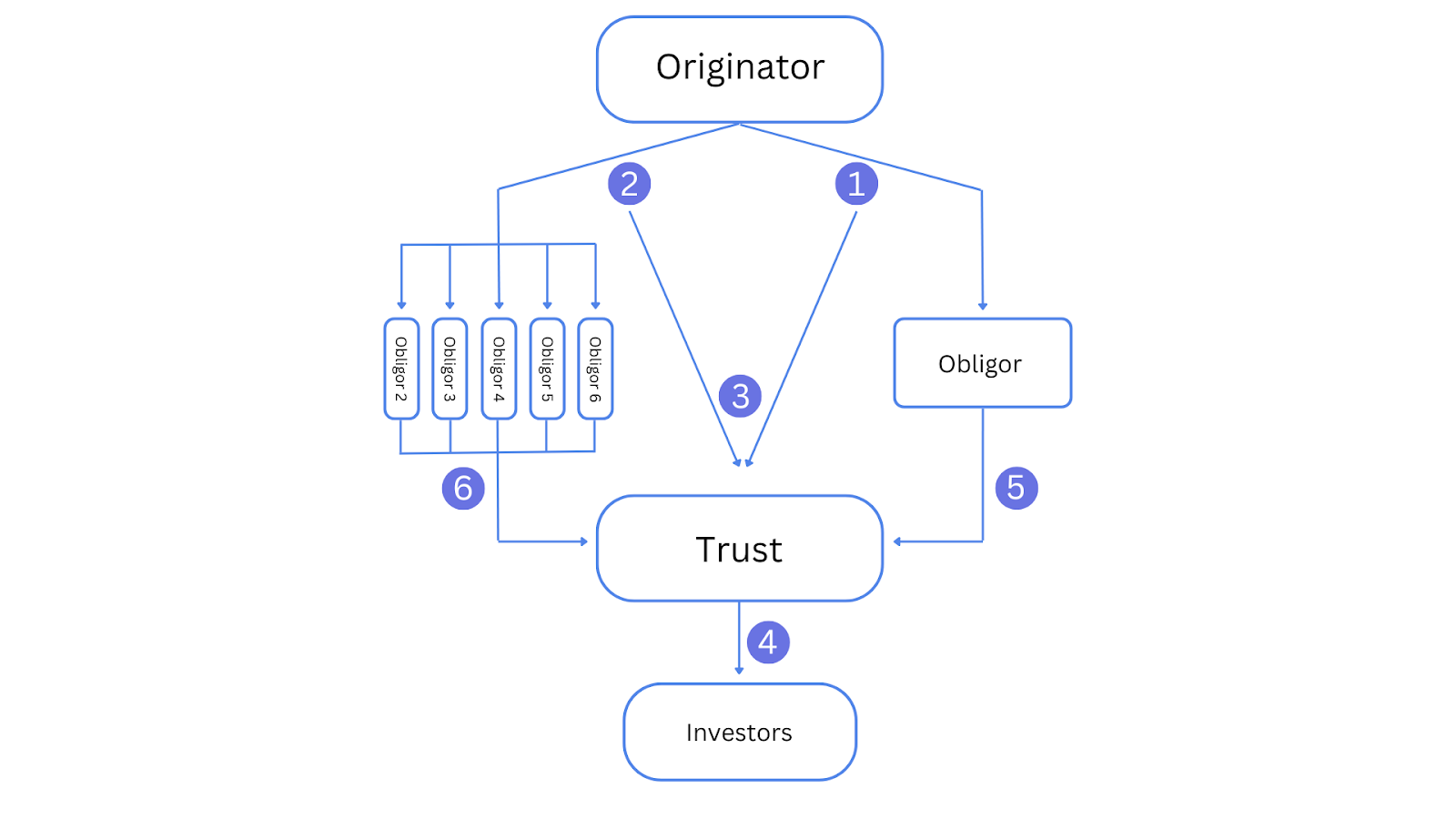

This article discusses the structure of the transaction, its elements, and the flow of funds.

Read more: A matter of scale in securitisationUnderstanding the Structure

1. Loan by Originator

The originators, Sikka Ports & Terminals Limited (SPTL) and Jamnagar Utilities & Power Private Limited (JUPL), provided a long-tenure loan to the obligor, Digital Fibre Infrastructure Trust (DFIT).

However, the maturity of the loan’s principal extends far beyond the tenure of the pass-through certificates (PTCs) issued under the securitisation structure. Out of a total sanction amount of ₹33131 crore, ₹25000 crore was lent out by the originators for a period of 30 years. An additional loan amounting to ₹8131 crore was also extended, but is not being securitised in this transaction.

2. Put Option with Originator

Parallely, the originator entered into a put option agreement with five Reliance group entities, namely, Reliance Industries Holding Pvt. Ltd., Srichakra Commercials LLP, Karuna Commercials LLP, Devarshi Commercials LLP, and Tattvam Enterprises LLP. The put option gave the originator the right to sell the loan receivables to these entities. Since the maturity of the underlying loan is significantly longer than the tenure of PTCs, the trustee would exercise the put option with the group entities and proceeds from sale of the loan receivables would be used for principal repayment.

Section 19A of the SDI Regulations, which specifies the conditions governing securitisation, mandates that no obligor shall have more than 25% in the asset pool at the time of securitisation. This serves to reduce credit concentration by specifying a minimum number of obligors. Entering into an option agreement with five separate entities fulfills these diversification requirements, ensuring compliance with the SDI regulations.

3. Assignment of Receivables to the Securitisation Trust

The originator assigned the loan receivables, along with the receivables under the put option agreement, to the securitisation trusts. Three trusts were involved in this deal: Siddhivinayak, Shivshakti, and Radhakrishna. SPTL assigned its loans to the first two trusts, while JUPL assigned its loan to Radhakrishna. Reliance Industries Holding Pvt. Ltd., one of the option counterparties, is not a part of the structure of the first trust; Siddhivinayak only has four option counterparties.

(all values in ₹ crore)

| Structure of the deal | |||

| Trusts | Siddhivinayak | Shivshakti | Radhakrishna |

| Value of Receivables | 6780.34 | 6943.36 | 4461.71 |

| Assignor of Receivables | STPL | JUPL | JUPL |

| Value of PTCs | 8000.00 | 8000.00 | 5000.00 |

| Value of Options | 1615.93 | 1339.92 | 870.24 |

| Number of Option Counterparties | 4 | 5 | 5 |

| Principal Repayment from Options | 6463.72 | 6699.62 | 4351.22 |

| Principal Repayment from DFIT | 1536.28 | 1300.38 | 648.78 |

| Yield on PTCs | 7.80% | 7.73% | 7.66% |

| Tenure of PTCs in years | 5 | 4 | 3 |

4. Issuance of Securitised Notes

The trusts issued securitised notes to investors, backed by loan receivables. These notes, or pass-through certificates (PTCs), have varying tenures of five, four, and three years respectively. They also have different yields, as the table above highlights. The notes were rated by two independent agencies, Crisil and Care Edge, and all three issuances were given a AAA rating.

5. Investor Participation

Roughly three-fourths of the issuance has been subscribed by the country’s leading asset managers, including Aditya Birla Sun Life AMC, HDFC AMC, ICICI Prudential AMC, Nippon Life India AMC, and SBI Funds Management Ltd.

6. Servicing of Securitised Notes

- Interest payments: Serviced from the interest on the underlying loan by DFIT .

- Principal repayments: Since the maturity of the underlying loan is significantly longer than the PTCs, the trustee would exercise the put option with the group entities. The proceeds from the sale of the loan under this option were then used to repay the principal to the securitised noteholders.

Read our other articles: