Social stock exchange for enterprises: a road not taken, or a road not found?

Payal Agarwal, Senior Manager | payal@vinodkothari.com

Social Stock Exchange (SSE) that emerged as a concept in India for the first time in the Budget Speech of FY 2019-20, has become a reality with the creation of a necessary regulatory ecosystem around the same during 2022. More about the regulatory ecosystem of SSEs can be read at Social stock exchanges: philanthropy on the bourses. Following the same, the two recognised stock exchanges of India having nation-wide trading terminals, viz., the NSE and BSE, have been granted recognition as SSEs in India. With this, an implementation mechanism has been provided for the “social enterprises” to get itself registered and listed on the SSEs.

As per the NSE’s list of registered NGOs, a total of 18 not-for-profit organizations (NPOs) have been registered till date (data accessed on 4th September, 2023). The BSE’s website also contains a list of around 19 NPOs registered with its SSE segment. Fundraising through SSE is not a mandatory requirement for NPO; however, to facilitate fund raising by NPOs, a proposal has been rolled out to relax certain requirements applicable to NPOs registered with SSEs. A brief of the proposals may be accessed at Flexibility-centric recommendations proposed for SSE framework. While a traction is observed in NPOs getting registered with SSEs as a “social enterprise”, the other group of social enterprises, the for-profit entities (FPEs) have been seemingly neglected.

Recognition to FPEs as “social enterprise” on SSEs

Chapter X-A of the ICDR Regulations deals with SSE and also applies to an FPE seeking to be identified as a “social enterprise”. While the regulations enable an FPE to be identified as a “social enterprise”, the relevant machinery to be identified as such has not been provided by the SSEs so far. As for fundraising, the FPEs have access to the capital markets through conventional sources, viz., the main board, SME exchange or debt segment; however, they are still not provided access to the “social enterprise” identifier.

Further, there might be FPEs which may as well not require access to the capital markets for fundraising, but only recognition of being a “social enterprise”, as is presently permitted for the NPOs. There does not seem to be a clear guidance yet on whether such brand building exercise is possible on SSEs for FPEs not raising any funds through the capital markets.

Meaning of “social enterprise”

In the context of SSEs, the ICDR Regulations define “social enterprise” as an NPO or a FPE that meets the eligibility criteria specified in Chapter X-A of the ICDR Regulations. An entity, whether an NPO or an FPE, is required to establish the primacy of its social intent in order to be eligible for identification as a “social enterprise”.

Three cumulative conditions have been provided for through which the primacy of one’s social intent can be established:

- The entity shall be engaged in one or more of the eligible activities specified in clause (a) of sub-regulation (2) of regulation 292E of ICDR Regulations.

- The entity shall target underserved or less privileged population segments or regions recording lower performance in the development priorities of central or state governments.

- The entity shall demonstrate that 67% of its eligible activities are being provided to targeted population by establishing one or more of the following three conditions:

- at least 67% of the immediately preceding 3-year average of revenues is earned from providing eligible activities to members of the target population; or

- at least 67% of the immediately preceding 3-year average of expenditure has been incurred for providing eligible activities to members of the target population; or

- members of the target population to whom the eligible activities have been provided constitute at least 67% of the immediately preceding 3-year average of the total customer base and/or total number of beneficiaries.

Where these conditions are fulfilled by an FPE, the same is very well eligible to be identified as a “social enterprise”.

In general parlance, a “social enterprise” does not eliminate the “profit-earning motive” of an entity altogether, it only requires primacy of a “social objective”. The OECD defines social enterprise as “any private activity conducted in the public interest, organised with an entrepreneurial strategy, whose main purpose is not the maximisation of profit but the attainment of certain economic and social goals, and which has the capacity for bringing innovative solutions to the problems of social exclusion and unemployment.”

The European Union defines SE as: “an operator in the social economy whose main objective is to have a social impact rather than make a profit for their owners or shareholders. It operates by providing goods and services for the market in an entrepreneurial and innovative fashion and uses its profits primarily to achieve social objectives. It is managed in an open and responsible manner and, in particular, involves employees, consumers and stakeholders affected by its commercial activities.”

Benefits of FPEs as “social enterprise”

Since the term “profits” are linked to FPEs, there may be a general notion as to how the same can qualify as a “social enterprise”. A social enterprise is not necessarily a charitable organisation, and one needs to understand that the “profit objective” does not take away the “social” benefits associated with one’s activities.

Citing from The Forprofit Social Enterprise Is The Impact Model Of The Future reported in Forbes, “profitability and positive social impact are not mutually exclusive. It is, in fact, possible to build a successful company and do good.”

If one has to list down the benefits of having an FPE as a “social enterprise”, the most important of them may be the sustainability of social benefits that come with an FPE. Unlike NPOs that depend on donations and charity for arranging funds towards meeting their social targets/ objectives, an FPE works on a self-sustainability model, wherein the social enterprise earns profits alongside creation of social impact, and plough back those profits, or a part thereof, in further generation of social impact. The FPEs also have access to the “impact investors” who are not merely philanthropists, but provide finance with an expectation of a measurable social return, alongside financial returns.

Having access to a diverse range of financial products helps an FPE in scaling up and expanding their activities, as well as investments for research and innovation.

Popularity of “social enterprises” in the form of FPEs

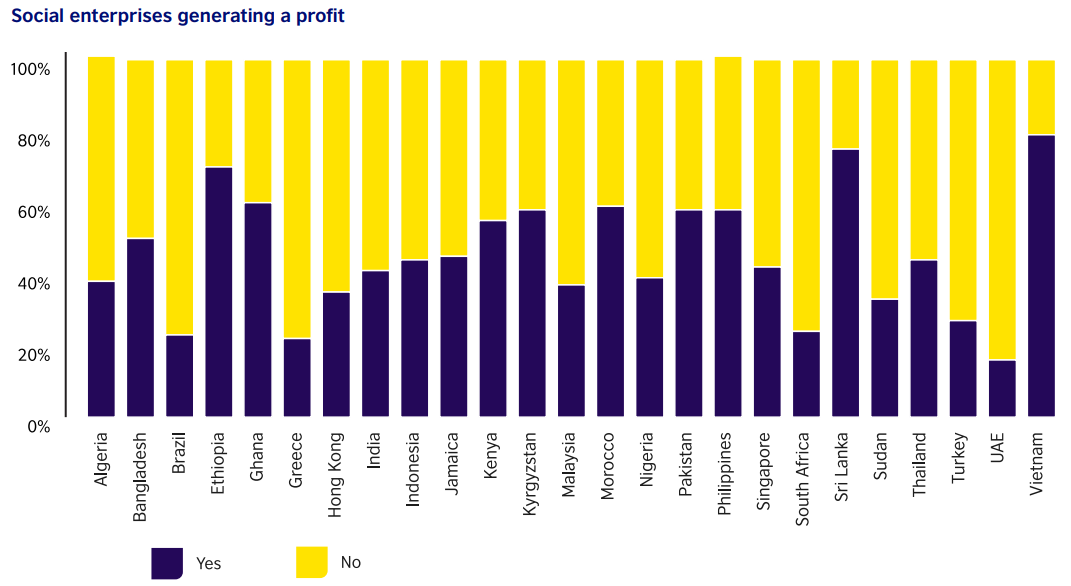

A 2022 report by the British Council and Social Enterprise UK titled More in common: The global state of social enterprise reflects the position of social enterprises across 27 countries across the globe. As regards the legal form of social enterprise, the Report suggests that more than half of the social enterprises in UAE, Singapore, Vietnam, Thailand including India are incorporated in the form of private companies. A Study of Emerging Patterns of Social Enterprises, published in March, 2022 by the Pune International Centre suggests that a tilt towards the popularity of private company structure may be on account of the flexibility to use the profits or surplus.

Each of the countries covered under the research reported varying proportions of profit-generating social enterprises. While some of these enterprises direct a major part of their profits towards the business growth and development activities, a few of them also reported distribution of a significant proportion of the profits with their shareholders or in the form of rewards to staff and beneficiaries.

Concluding Remarks

While the meaning of “social enterprise” may vary across jurisdictions, the driving idea remains the “primacy of a social intent”. There is no denying the fact that FPEs may very well be recognised as social enterprises, and there are benefits associated with such classification. Profit generation and social impact creation are not conflicting, but complementing each other. Stakeholders are widely moving towards a “values-based” rather than merely “value-based” approach, and hence, an FPE focussing on social impact will ultimately benefit it in long term value creation for its stakeholders. Similarly, larger the profits available with an FPE, more funding pool becomes available for investment in social projects, thereby, multiplying the social impact.

In such a scenario, FPEs do need to be provided access to the SSEs, if not for fundraising, for the recognition of the “social objectives” of such entities. While there is no data to substantiate the same, the FPEs are likely to opt for registration on SSEs, given entry is provided to them on the SSEs.

Leave a Reply

Want to join the discussion?Feel free to contribute!