Funding through crowdfunding platform: whether qualifies to be CSR?

-Platforms different from implementing agency

-Pammy Jaiswal, Partner and Sachin Sharma, Executive (corplaw@vinodkothari.com)

Crowdfunding Platforms

Crowdfunding platforms are digital platforms which solicit funds for various ventures. They pave way for easy accessibility to a vast network of people through social media. Individuals, charities or companies can create a campaign for specific causes for contribution from anyone, either a corporate, or an association, or an individual. Two broad classes of crowdfunding platforms are: investment-based, which consists of stocks, royalties, and loans, where the funders are investors in a campaign and can obtain monetary benefits. The other is donation-based, where funders do not expect monetary compensation. They fund a campaign because they support its cause. For understanding the concept on crowdfunding in detail, kindly refer to our article here.

Crowd sourcing has become an important aspect for carrying out CSR activities[1]. Around 27% of the crowdfunding campaigns are initiated to cover medical expenses. Several crowdfunding platforms are running parallelly across India as well as the world. Some of the Indian crowdfunding platforms include Impactguru, Milaap, Ketto, etc. As the world is under the grip of COVID- 19, these platforms are playing their remarkable role in sourcing funds for COVID-19 relief through several campaigns. Till now, Ketto has raised ₹324.60cr for its COVID relief campaigns whereas Milaap has raised ₹182.47Cr and Impact Guru has raised ₹61.46cr for their COVID relief campaigns. Further, crowdfunding platforms are not only popular in India but also across the world. Several global platforms are also working to raise funds for various projects/ campaigns. Global Giving collection in its Coronavirus Relief Fund has moved to $13,363,987.

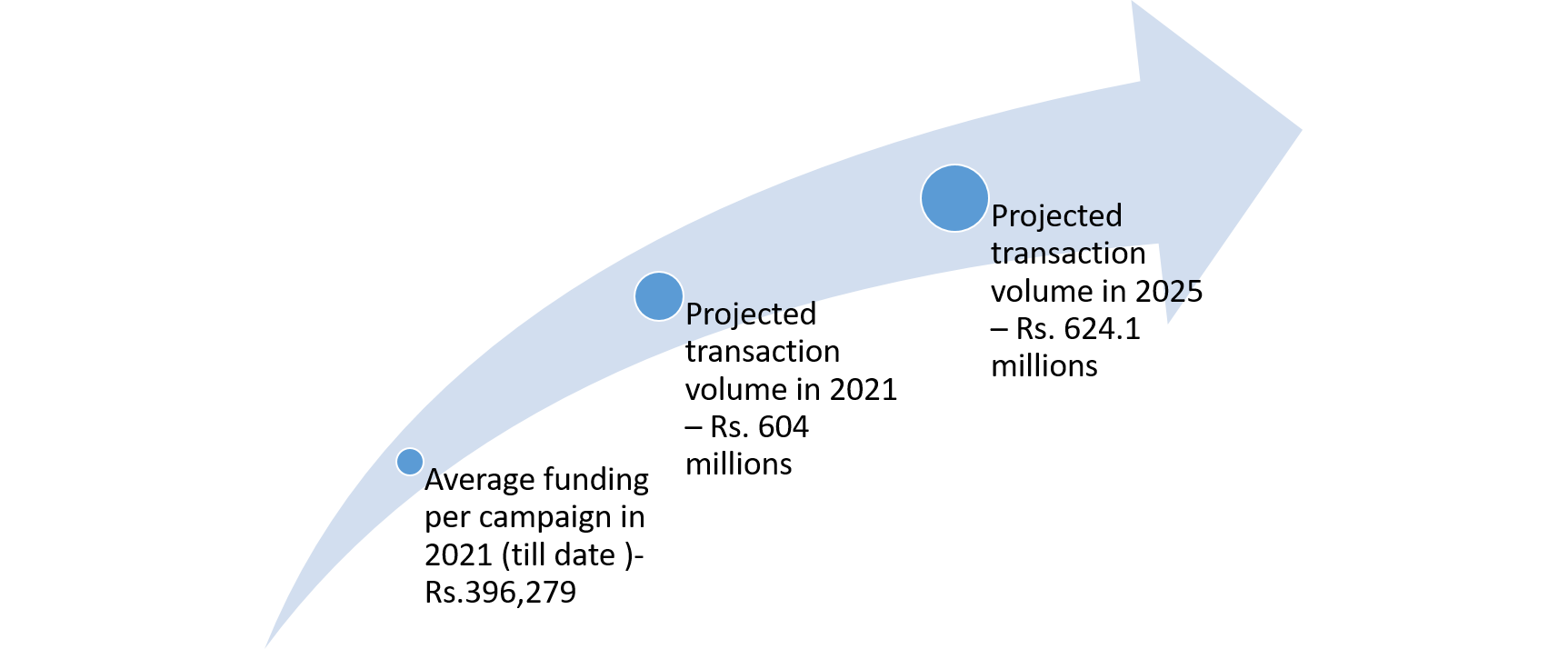

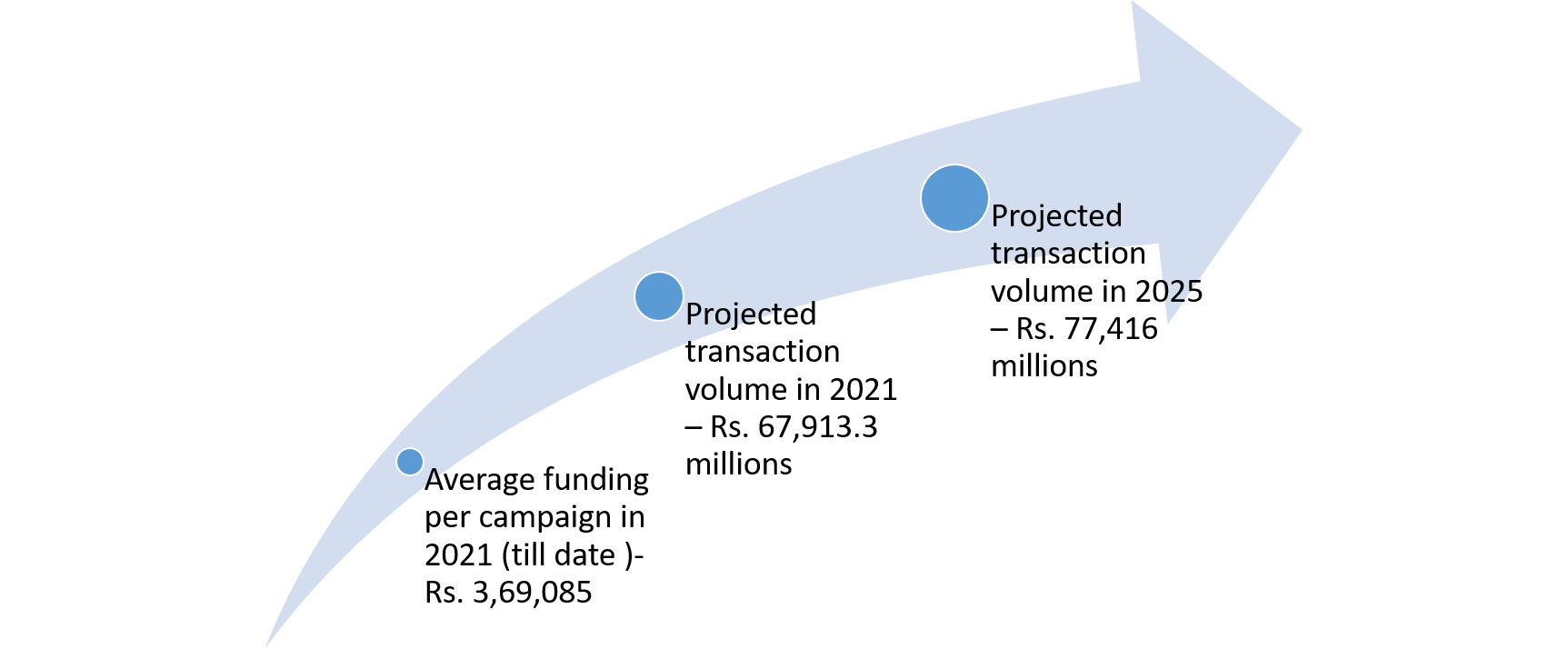

Growth in transactions of crowdfunding platforms

The crowdfunding platforms have attained greater visibility and importance in India as well as globally as per the statistics[2] given below-

The first figure corresponds to the Indian position and the second figure pertains to global statistics.

What is an ‘Implementing Agency’ (IA)

The term IA has not been defined under the CSR provisions (section 135 of the Companies Act, 2013 as well as the rules made thereunder), however, the report on CSR activities uses the term IA for carrying out CSR indirectly.

IA, as the name suggests is an implementation tool for the entity to carry out its CSR activities. As per Rule-4(1) of the Companies (Corporate Social Responsibility Policy) Rules, 2014, section 8 companies, registered public trusts, and registered societies (collectively, called ‘entities’) can be referred to as IAs. The nature or activities of an IA can be distinguished from that of a beneficiary through a very thin line. Our article containing the detailed discussion on the same can be read here.

While carrying out CSR activities through an IA, there are several things that a company needs to consider after the amendment under the CSR provisions have been notified on 22nd January, 2021. They include:

- IA which includes a section 8 company, public charitable trusts, or a society either formed by the company or otherwise needs to be registered under section 12A and 80G of the IT Act;

- All IAs, are required to register themselves with MCA by filing e-form CSR-1; and

- IAs which include a section 8 company, public charitable trusts, or a society not formed by the company require a track record of three years in carrying out similar CSR projects.

Crowdfunding platform working as a connecting point

Crowdfunding Platforms simply acts as connecting point between CSR contributors and CSR opportunities. It neither gets into implementation nor acts as agent for implementation, it acts merely as a connection point.

Deprived of the crowd sourcing mechanism, each company would have to look for its own sources for their CSR activity which will be a very inefficient way for carrying out CSR. India is a vast country and therefore huge number of CSR opportunities are present where each company would like to carry out its CSR obligations strategically so as to fulfil their CSR objectives. Crowdfunding platforms have filled up the information asymmetry and plays a role of an information bridge similar to what media does. Since it does not go into the implementation role at all, there is nothing wrong in routing/ using such platforms for carrying out CSR activities.

How is a crowdfunding platform different from being an IA?

An IA is regarded to work as an extended arm of the company in carrying out CSR activities. The whole purpose of involving an IA is to relieve the company from using its time to identify reliable projects and programs wherein the funds may be used or allocated. Another reason to involve an IA for carrying out CSR is that the company may not have the requisite expertise and experience to shortlist the authentic activities or entities where the money can be spent.

Having said that, on the other hand, a crowdfunding platform does not work as an extended arm of the company, rather, it is a voluntary body which acts a connecting point between the IA/ beneficiary and the company. It does not have the liberty to allocate the money in the project of its own choice, rather, the fund giver chooses the exact project or IA where it wants the money to be used.

Further, to be eligible to carry out CSR activities as an IA, registration with the MCA and under IT Act (except for govt entities and those set up under an Act of Parliament or State Legislature) is necessary while crowdfunding platforms may be relieved from such mandatory requirement considering its role as a connecting point between the fund raiser and the fund giver. Therefore, crowdfunding platforms cannot be regarded as IA.

The third point of difference between the two is when a CSR activity is routed through the IA, monitoring and utilisation report is required to be supplied by such IA to the Company. Whereas, when funds are contributed through crowdfunding platform, the ultimate beneficiary or IA which takes the funding, is liable to provide a utilisation report to the fund giver.

Features of the crowdfunding platform which distinguishes it from an IA

As discussed above, a crowdfunding platform acts as a medium to connect the contributor and the contribute. If it also relevant to understand the extent these crowdfunding platforms differ from an IA.

We have gone through the websites of several crowdfunding platforms and have presented a tabular presentation of areas where they are different from becoming an IA.

| Basis | Ketto[1] | ImpactGuru[2] | Milaap[3] | Role of IAs |

| Accountability | It shall not in any manner be responsible or held accountable for any transaction between the Users. | No obligation to become involved in disputes between any Users, or between Users and any third party arising in connection with the use of the Site | Assume no responsibility to verify whether the Donations are used in accordance with any applicable laws, and such responsibility rests solely with the Champion or Charity, as applicable | Accountable to the companies donating the funds. |

| Utilisation of funds | It is merely an intermediary and does not interfere in the transaction between Donors / Contributors and Campaigner | Not responsible in any way whatsoever towards the end utilization of funds | Facilitates the Donation transaction between Champions and Donors, but is not a party to any agreement between a Champion and a Donor, or between any user and a Charity. | It decides the areas and entities where funds are to be allocated |

| Obligations or liabilities wrt funds collected | Does not hold any right, title or interest over the funds or rewards or have any obligations or liabilities in respect of such providing the same to the Donor / Contributor | Does not take any responsibility for making sure that the project for which the funds are raised through its Site is completed and made available to the Funders | No control over the conduct of, or any information provided by a Champion or a Charity, and Milaap hereby disclaims all liability in this regard | Liable if the same remains unspent or not spent within the permitted activities. Utilisation reports have to be shared signifying the utilisation of funds for permitted activities |

| Liability for correctness of information on the platform | Not liable | Not liable | Not liable | Liable |

| Responsibility for success/ outcome of the project | Not liable | Not liable | Not Liable | Liable |

| Verification whether funds are used as per applicable laws or fund-raising purpose | Responsibility on the Campaigner | Responsibility on the Campaigner | Responsibility on the Campaigner | Responsibility on the IA |

Safeguards/ points of consideration in funding through the platform

- Funds are going to the beneficiary directly:

The fund is put directly from the crowdfunding platform to the beneficiary’s account and no third party is involved here. In this, it becomes a case of direct CSR activity. Utilisation report is required.

- Funds are going to another IA (registered):

Where the funds raised by crowdfunding platform goes to an entity registered as an IA with MCA, monitoring as well as utilization report will be required

- Funds are going to another IA (registered) which itself carries out CSR activities:

Where the fund raiser is a registered IA, however, carries out the CSR activities itself, it will be a case of direct CSR and not through an IA.

Conclusion

Crowdfunding platforms are emerging as promising sources for business houses to fulfil their CSR goals. These platforms should be expected and at the same time be bound by the mandatory registration provisions with the MCA since their role is not be act as an IA but a mere platform where fund raisers and fund givers can meet.

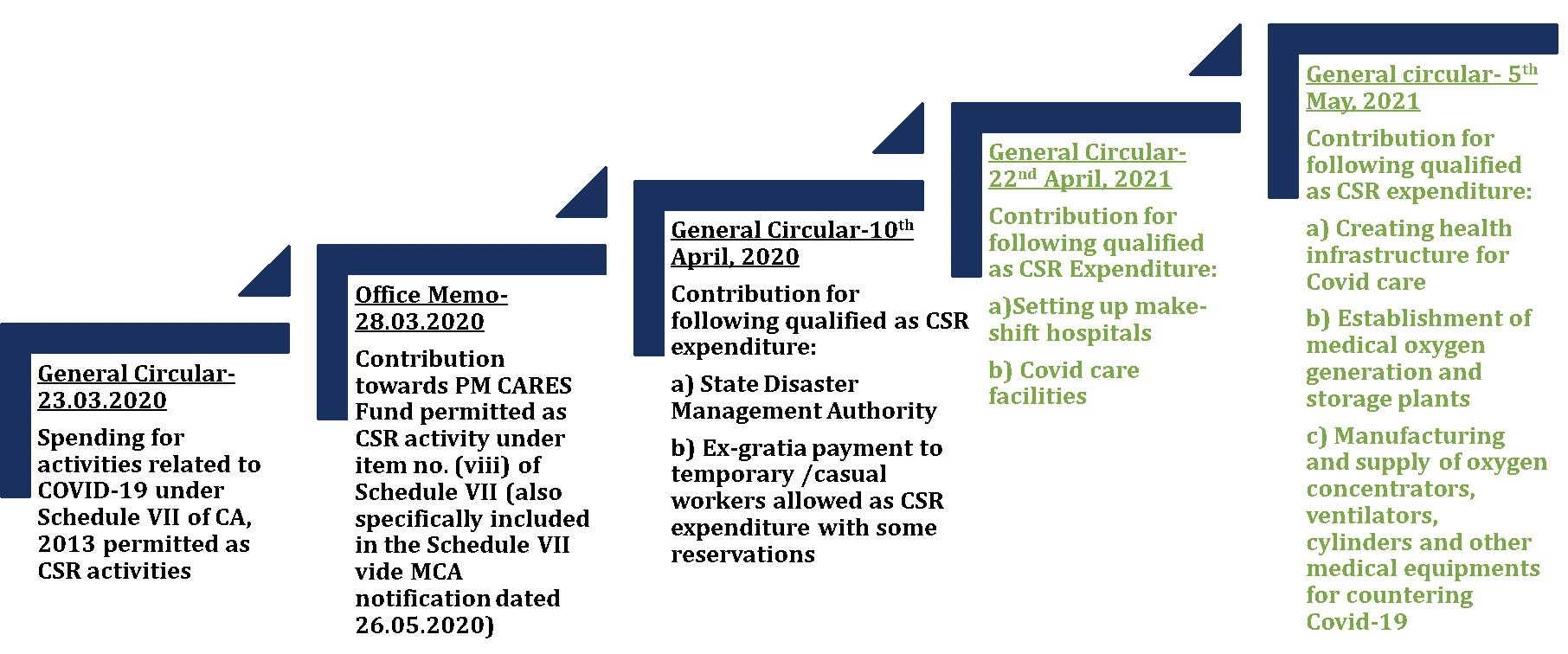

Ministry of Corporate Affairs (MCA) vide several circulars have brought several relaxations and broad based the activities under Schedule VII in relation to COVID-19 and health care.

Looking at the ongoing era of the pandemic, it has become very common for several digital platforms to come forward and act as source of link between the agencies/ beneficiaries and the corporates for several activities which are also covered under Schedule VII of the Companies Act, 2013.

Our other resources on CSR can be read here

[2] https://www.statista.com/outlook/dmo/fintech/alternative-financing/crowdfunding/worldwide?currency=INR

[1] https://www.ketto.org/terms-of-use.php

[2] https://www.impactguru.com/terms-of-use

Leave a Reply

Want to join the discussion?Feel free to contribute!