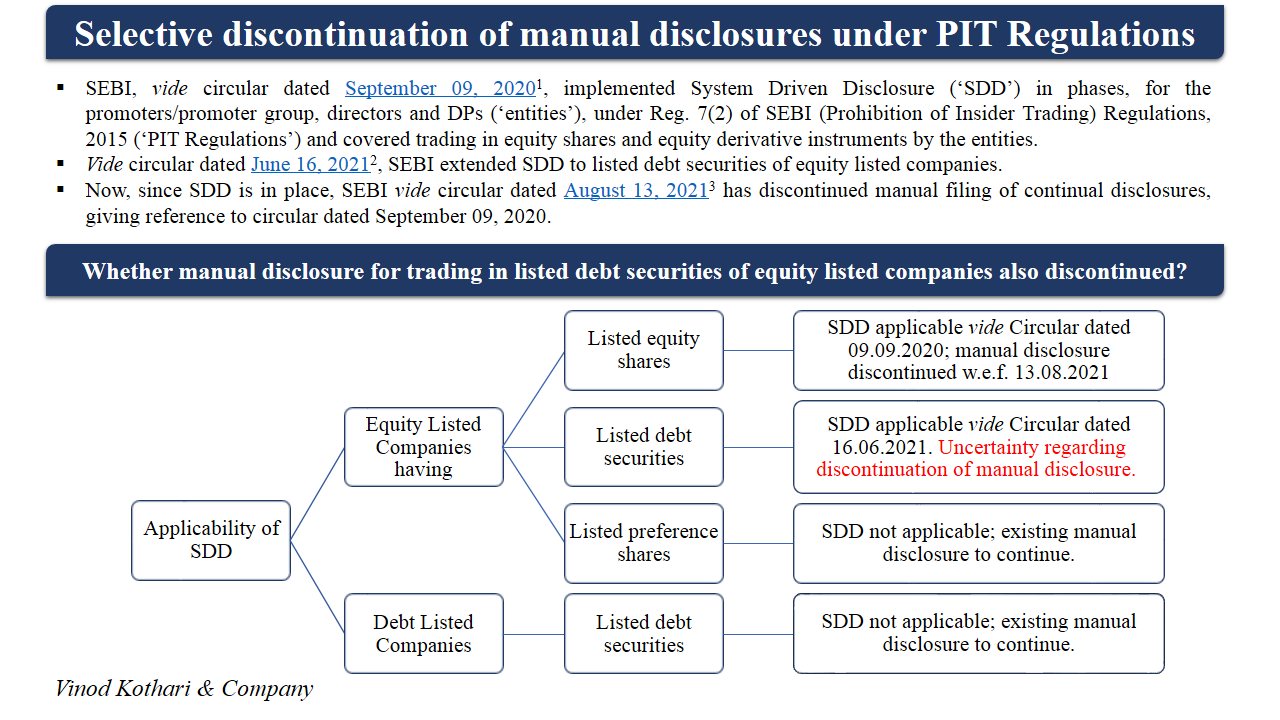

FAQs on Structured Digital Database

Loading…

Loading…

Our other materials on the topic:

Loading…

Our other materials on the topic:

By CS Aisha Begum Ansari (aisha@vinodkothari.com)

When you go silent, you may be doing a soul searching, as for example, in meditational techniques. However, in case of listed entities, silent period is a period just before declaration of financial results, to ensure that there is no accidental leakage of confidential information. Silent period is different from “trading window closure” that most corporate professionals in India are familiar with. However, this article discusses the relevance of silent period, as a subset of the trading window closure, and its relevance to listed entities in India. While exploring the topic, the author also makes a study of the global laws around silent period.

Insider trading is a ‘white collar’ crime that seeks to exploit the unpublished, non-democratic information (that is, what is not available in public domain) to the advantage of a select few, and to the disadvantage of the market in general. Since, it is a fraud upon the market in general, it has always been a significant topic for the securities market regulators around the globe. In India, Securities and Exchange Board of India (‘SEBI’) has framed the regulatory framework to curb the insider trading called as SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’).

The material inside information is generally accessed by the top executives and employees of the company. To avoid the exploitation of such information, the company prohibits them from trading in its securities while having access to such information. The preventive framework of insider trading does not just end by prohibiting the employees from trading; it also needs to ensure that such material inside information is not leaked outside the organization. There are many ways used by the insiders to leak such information such as sharing the same on social media, sharing of information during analyst or institutional investor meets, etc.

Silent period is different from trading window closure. Silent period is when the company’s top executives, say that CEO, CFO etc. will refrain from doing public communications altogether. The intent is to ensure that there is no interaction with investors or public at large, so as to avoid unintended slippage of information. Currently, SEBI regulations do not require companies to mandatorily observe a silent period; therefore, companies may choose to adopt this practice by way of their Code of Fair Disclosure.

A silent period (also known as quiet period) is a stipulated time during which a company’s senior management and investor relation officers do not interact with the institutional investors, analysts and the media. The purpose of the silent period is to preserve the objectivity and avoid the appearance of the company providing insider information to select investors. During the silent period, the company does not make any announcements that can cause a normal investor to change their position on the company’s securities.

Trading window closure period (also known as blackout period or closed period) refers to the period during which the employees of the company who have access to material inside information are prohibited from trading in the securities of the company. In some of the developed countries, the securities market regulators give a freehand to the companies to decide the period during which the trading window shall be closed. In India, the PIT Regulations provide that the companies shall close the trading window from the end of the closure of the financial period for which results are to be announced till 48 hours after the disclosure of financial results to the stock exchanges. For any other material inside information, SEBI has given the responsibility to the compliance officers of the companies to close the trading window when the employees can reasonably be expected to have possession of inside information.

Silent period differs from the trading window closure in such a way that trading window closure prohibits the employees to trade in the securities of the company while having access to material inside information and silent period prohibits or restricts the company’s spokespersons to interact with the institutional investors or analysts. The purpose of trading window closure is to prohibit trading on the basis of inside information and the purpose of silent period is to prohibit communication of inside information illegitimately.

The PIT Regulations or any other regulatory framework in India do not provide for the requirements of silent period. So, the duration of silent period differs from company to company. Some companies specify the silent period as 20-30 days before the declaration of financial results till the date of disclosure and some companies align the silent period with the trading window closure period. The following table gives the synopsis of the practice followed by the Indian listed entities regarding silent period:

| Name of the Company | Practice followed |

| Mahindra & Mahindra Limited | Silent period commences from 20 days before the declaration of financial results till the date of disclosure of results |

| Tata Consultancy Services Limited | Quiet period starts 20 days before the declaration of financial results till the date of disclosure of results |

| HCL Technologies Limited | Silent period is same as trading window closure period |

| Asian Paints Limited | Silent period is observed between the end of the period and the publishing of the stock exchange release for that period |

| Wipro Limited | Quiet period commences from 16th day of the last month of the quarter and ends with 48 hours after earnings release. |

| Infosys Limited | Silent period is observed between the 16th day prior to the last day of the financial period for which results are required to be announced till the earnings release day. |

Thus, it can be concluded that the silent period is smaller than the trading window closure period.

Analysts/ investors meets can be a medium of leak of material inside information, therefore, the companies avoid interaction with them during trading window closure period. So, does it mean that companies completely abstain from interacting with the analysts and investors? While the answer may differ from company to company and the policies adopted by them for communication with analysts and investors. Some companies completely refrain from the analysts/ investors meets while some companies interact with them and discuss the past and historical information which is already available in public domain and general future prospects of the company, dodging the specific questions relating to the material inside information.

While the regulations framed by SEBI are silent about the silent period, the Guidelines for Investor Relations for Listed Central Public Sector Enterprises issued by the Department of Disinvestment, Ministry of Finance, Government of India, provides for the duration of silent period and obligations of the public sector enterprises in this regard. The Guidelines advise that the silent period should commence 15 days prior to the date of Board meeting in which financial results are considered and end 24 hours after the financial results are made public. The Guidelines requires the companies to abstain from meeting the analysts and investors and not communicate with them unless such communication would relate to the factual clarifications of previously disclosed information.

| Country | Trading window closure period | Silent period | Analyst meet during silent period |

| United States of America (USA)[2] | USA laws do not provide any specific timeline for trading window closure period. Thus, the companies are free to determine it | There are two types of silent period prevalent in USA:

1. When the company makes an Initial Public Offering (‘IPO’) – the Securities Exchange Commission (‘SEC’) mandates such companies to maintain a silent period from the date of registration with SEC which lasts till 40 days after the securities begin to trade on the stock exchanges. Such silent period is heavily regulated by the SEC. 2. During finalization of quarterly results – the silent period is not clearly defined by SEC. |

During the silent period, the interaction with the analysts and investors is reduced. The companies either go completely silent or they speak about only past and historical information. |

| United Kingdom (UK)[3] | Unlike USA, the UK laws prescribe the trading window closure period. Article 19.11 of Market Abuse Regulations specifies the period of trading window closure starting from 30 calendar days before the announcement of an interim financial report or a year-end report till the second trading day after announcement of financial report. | UK laws do not comment anything about the silent period. Thus, the companies determine the silent period as per their own discretion.

|

Since UK laws do not provide for silent period, the companies, as per their discretion, avoid interactions with the analysts and investors during such period.

|

| Canada[4] | Para 6.10 of National Policy on Disclosure Standards (‘Policy’) discusses about blackout period. It states that the company’s insider trading policy should specify the period which may mirror the quiet period. | Para 6.9 of the Policy talks about quiet period. While the Policy does not prescribe the duration of quiet period, it states that the period should run between the end of the quarter and the release of a quarterly earnings announcement. | The Policy states that the company need not completely stop communicating with the analysts and investors during the quiet period, but the communication should be limited to responding to inquiries concerning publicly available or non-material information. |

After discussing the practices followed by the Indian listed companies and the regulatory framework of other developed countries, it can be concluded that the concept of silent period is not something new, though unregulated. Some companies align the silent period with the trading window closure period while some provide for lesser duration for silent period. Some companies completely abstain from interacting with the analysts and the institutional investors during the silent period whereas some prefer discussing the generally available information only.

[1]https://www.dipam.gov.in/dipam/downloadFile?fileUrl=resources/pdf/capital-market-regulation/IR_Guidelines_website.doc

[2] https://www.irmagazine.com/reporting/six-commonly-asked-questions-and-answers-about-quiet-periods

[3] https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014R0596&from=EN

[4] http://ccmr-ocrmc.ca/wp-content/uploads/51-201_np_en.pdf

Other relevant materials of interest can be read here –

http://vinodkothari.com/2021/07/step-by-step-guide-for-disclosure-for-analysts-investors-meet/

http://vinodkothari.com/2021/05/sebi_defines_investors_meet/

CS Vinita Nair, Senior Partner | Vinod Kothari & Company

July 23, 2020

Link to gazette notification: http://egazette.nic.in/WriteReadData/2020/220574.pdf

Effective date: July 17, 2020

SEBI in the Board meeting held on June 25, 2020 (‘SEBI BM’) discussed amendments in PIT Regulations on Structured Digital Database, continual disclosures and amendments in the Code of Conduct (CoC).

This article discusses the position prior to amendment, relevant discussion at SEBI BM and actionable post amendment.

Prior to the amendment

Reg 3(5) of the regulations provided maintenance of SDD-1 with names of persons with whom UPSI was shared and PAN/ any other identifier of the person (where PAN was not available). SDD was required to be maintained with adequate internal controls and checks such as time stamping and audit trails to ensure non-tampering of the database.

The regulation indicated that just the listed entity is required to maintain the same. However, SEBI clarified in the guidance note, pursuant to an insertion made on July 5, 2019, that the requirement to maintain SDD-1 was applicable to listed companies, and intermediaries and fiduciaries who handle UPSI of a listed company in the course of business operations.

Discussion in SEBI BM

As per the agenda of the SEBI BM It was proposed to specify following in relation to SDD:

Post amendment

Prior to the amendment

Continual disclosures under Reg 7 (2) (b) was required to be made by the promoters, member of promoter group and designated persons to the stock exchanges within two trading days of receipt of the disclosure or becoming aware of such information. System driven disclosure was implemented vide SEBI Circular dated May 28, 2018 only for The CEO and upto two levels below CEO of a company and all directors. The database was submitted to the depositories along with PAN of the individuals.

Discussion in SEBI BM

Investigation of delay or non-compliance due to manual submissions takes up considerable time and effort and clogs the system. In order to eliminate it was proposed to automate the process of filing such disclosures by way of SDD-2 thereby enabling timely and fair disclosure without intervention of entities involved. SEBI will be issued detailed circular on the same to the market participants.

Post amendment

Reg 7 (2) (c) inserted to provide enabling power for issue of format and manner of submitting SDD-2.

Prior to the amendment

Trading window restriction was not applicable on transactions specified in proviso to Reg 4 (1), in respect of pledge for a bonafide purpose and transactions undertaken in accordance with respective SEBI Regulations such as acquisition by conversion of warrants or debentures, subscribing to rights issue, further public issue, preferential allotment or tendering of shares in a buy-back offer, open offer, delisting offer.

Discussion in SEBI BM

Offer for sale was not included in the said list despite SEBI having laid detailed procedure for the same.

Post amendment

Enabling clause inserted to include the transactions which are undertaken through such other mechanism as may be specified by the Board from time to time. SEBI vide Circular dated July 23, 2020 provided that trading window restriction shall not apply in case of rights entitlement and Offer for Sale.

Prior to the amendment

Only profits from contra trade were disgorged and credited to Investor Protection and Education Fund (IPEF) administered by SEBI. The listed entity had the option to take disciplinary action including by way of recovery, clawback.

Discussion in SEBI BM

The listed entity could take action against person violating the CoC by way of disciplinary actions viz. wage cut, collecting of certain amount etc. There was no uniform approach w.r.t. utilization of amounts levied by the listed entities/ intermediaries/ fiduciaries for other violations of CoC viz. trades during window closure, trade without pre-clearance etc.

Also, a clawback is generally a contractual agreement between the employee and the employer in which the employee agrees to return previously paid or vested remuneration to the employer under certain circumstances. However, every employment agreement may not have a “clawback” clause or provision. Whereas, disgorgement as an equitable remedy, aimed at depriving the wrongdoer of his ill-gotten gains. It was suggested to substitute ‘clawback’ with ‘disgorgement’.

Post amendment

Any amount collected for violation of CoC shall also be remitted to SEBI for credit to the IPEF. The word ‘clawback’ has been deleted in Schedule B and Schedule C. SEBI vide Circular dated July 23, 2020 has provided that such amounts shall be credited to the IPEF through the online mode or by way of a demand draft (DD) in favour of the Board (i.e. SEBI – IPEF) payable at Mumbai. The bank account details of SEBI – IPEF for online transfer is given below:

Prior to the amendment

Violation of PIT Regulations was required to be informed to SEBI. SEBI vide Circular dated July 19, 2019 prescribed format for standardized reporting of violations under CoC.

Discussion in SEBI BM

The intimations received from listed companies/ intermediaries/fiduciaries were maintained in non IT based environment. To ensure that such intimations were captured electronically in an IT based environment to create a data repository, which could be used for conducting examination of cases or for any other data analysis, in future, it was recommended to file intimations with the stock exchanges.

Post amendment

The violations will be required to be reported to the stock exchanges in the form and manner as may be prescribed by SEBI. SEBI vide Circular dated July 23, 2020 prescribed the format in supersession of July, 2019 circular.

Whether the intimations filed with the stock exchanges will be publicly available, is not clear.

The format is broadly similar to that prescribed in July, 2019, however, has following modifications:

|

Particulars |

July, 2020 Circular | July, 2019 Circular |

Remarks |

| Details of DP | Whether the DP is promoter or belongs to promoter group | Whether the DP is promoter /promoter group/ holding CXO level position (e.g. CEO, CFO, CTO etc). | The details highlighted is anyways provided under Designation of DP and Functional role of DP. This seemed repetition. |

| Details of transaction | No of shares traded and value (Rs.) (Date- wise) | No of shares traded (which includes pledge) and value (Rs.) (Date- wise). | The legislative note under definition of ‘trading’ in the Regulations clarify that trade includes pledge. |

| Details of violations | Details of violations observed under Code of Conduct. | Details of violations observed under SEBI (PIT) Regulations, 2015. | Reference aligned with Para 12 of Schedule B of the Regulations. |

| Amount collected for CoC violation | · Mode of transfer to IPEF (Online/ DD)

· Details of the transfer. |

No such field. | It seems that the amount is to be first transferred and thereafter, reporting is to be done as payment details is required to be furnished. |

SDD-1

Maintenance of SDD-1 to be ensured with details of persons sharing the UPSI. SDD to be preserved for minimum 8 years from completion of relevant transactions. Internal control manual/ SOP, if any, will be required to be updated to capture the amendment.

SDD-1 may be maintained by Compliance Officer or may be maintained by various functional heads who are in possession of UPSI and share the same for legitimate purpose. The Compliance Officer should have access to the same as that is required for deciding of pre-clearance for the trades by DPs.

SDD-2

Reporting continual disclosure in SDD-2 after the format is prescribed by SEBI. In case SEBI decides to implement SDD-2 in the manner it implemented in 2018, the listed entity will be required to furnish name and PAN details of promoter, member of promoter group and all designated persons to the depository.

CoC

The CoC will be required to be amended to capture the amendments by removing reference of clawback provision and specifying to deposit amounts collected for violation to IPEF.

Violation of the regulations and of CoC to be reported to the stock exchange instead of SEBI by listed entity/ intermediary/ fiduciary in the format provided by SEBI vide circulated dated July 23, 2020.