FAQs on compensation of Key Managerial Personnel and Senior Management under the Scale Based Regulatory Framework

Financial Services Division | (finserv@vinodkothari.com)

RBI had introduced the Scale Based Regulatory Framework: A Revised Regulatory Framework for NBFCs vide a circular dated October 22, 2021. Para 3.2.3 (h) of the circular dealt with ‘Compensation Guidelines’ which required that NBFCs shall put in place a Board approved compensation policy in order to address issues arising out of excessive risk taking caused by misaligned compensation packages.

In terms of the aforementioned para, the RBI subsequently issued a circular on April 29, 2022 detailing the ‘Guidelines on Compensation of Key Managerial Personnel (KMP) and Senior Management in NBFCs’.

With these FAQs, we aim to address some of the key questions that may arise out of the guidelines and provide an understanding of the same.

1. Applicability

1.1. What is the basic intent of RBI for issuing the Compensation Guidelines for NBFCs?

Response: As per the SBR framework and the text of the notification, the purpose appears to be – (i) to address issues arising out of excessive risk taking caused by misaligned compensation packages and (ii) to ensure that there is no conflict of interest.

Here, by misaligned compensation, the RBI seems to be pointing to scenarios where there is an imbalance between fixed pay structures and variable pay structures in a manner which may lead to excess risk taking by the key management and senior management personnel. Excess risk taking (that is, beyond the appetite of the entity) may lead to hyper-aggressive decision making and consequent severe losses.

One may note that there is a similar notification for banks to address concerns pertaining to Compensation of Whole Time Directors/ Chief Executive Officers/ Material Risk Takers and Control Function staff. The provisions of these Compensation Guidelines are a tilt towards the provisions of the compensation guidelines for the banks.

1.2. What is the connection between risk-taking and variable pay? Does the fixed & variable pay compensation have any relation with long-term and short-term performance of the entity?

Response: Variable pay is connected with the performance of the entity during the current year, or ensuing year(s). Presumption is that if senior management is entitled to substantial variable pay, there will be a motivation to focus on near-term and short-term performance, compromising long-term interests. For instance, there may be an overdrive towards selling loan pools, and thereby accelerating gains-on-sale, even though it might compromise long term asset quality.

For the same reason, variable pay promotes risk-taking. Riskier products, or risk-taking on the liability side (say, using short term funding to reduce cost of capital) may have short-term dividends, but may result in severe risks in the long-term.

The investigations into the Global Financial Crisis also showed that the bonus-laden compensation structure of banks was partly responsible for the run up to the crisis.

1.3. Controls on managerial remuneration exist in the Companies Act as well. Why would the RBI interfere in this domain?

Response: Companies Act (CA) controls are, first of all, limited to only “managerial personnel” which includes directors, managing director and manager (as defined in the Act). The Compensation Guidelines are for senior management as a whole, and therefore, much larger in scope.

More importantly, the intent of the CA is shareholder say on managerial remuneration by way of a so-called say-in-pay rules. However, the intent of these Guidelines is from the viewpoint of boardroom sensitisation, structured approach to compensation policies, and fixing accountability for compensation structures. These Guidelines have a different approach altogether. Further, the Guidelines are in addition to the law, and not in derogation or substitution. Therefore, the CA and the Guidelines both apply.

1.4. Do the Compensation Guidelines apply to all layers of NBFCs? Are there any exemptions?

Response: Yes. The Compensation Guidelines are not applicable to the following class of NBFCs:

- NBFC-Base Layer;

- Government owned NBFCs.

Apart from the above exceptions, it would apply to all TL, UL, and ML NBFCs.

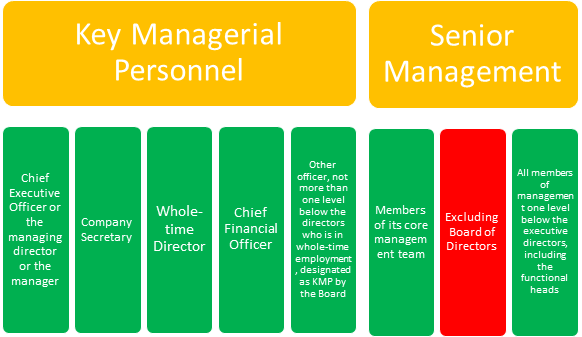

1.5. Who are KMPs and SMPs as mentioned in the Compensation Guidelines?

Response: The Compensation Guidelines are applicable to KMPs and senior management personnel. Both these expressions are to be interpreted in terms of the respective definitions provided under the Companies Act, 2013:

1.6. Do the principles regarding compensation provided in these Guidelines apply to the following:

a) Whole-time directors

b) Non-executive directors

c) Head of Departments

d) Company Secretary

e) CFO/CEO/MD

Response: As discussed hereinabove, the Compensation Guidelines are applicable only to specified class of employees i.e Key Managerial Personnel (KMP) and senior management. Accordingly, the applicability of the following personnel is discussed below. However, risk taking and remuneration /compensation policy are company-wide objectives and therefore, the boardroom of a company may apply the same principles across the organisation.

| S.no | Designation | Applicability |

| 1 | Whole-time directors | A whole time director is a KMP and accordingly, compensation paid to the same shall be covered under the Compensation Guidelines. |

| 2 | Non-executive directors | Non-executive directors are not KMP or senior management accordingly, compensation paid to the same shall not be covered under the Compensation Guidelines. However, Companies Act principles on managerial remuneration will be applicable here. |

| 3 | Head of Departments | Personnel appointed as Head of Department is classified as Senior Management. Accordingly, compensation paid to such personnel shall be covered under the Compensation Guidelines. |

| 4 | Company Secretary | A Company Secretary is classified as a KMP. Accordingly, compensation paid to the Company Secretary shall be covered under the Compensation Guidelines. |

| 5 | CEO/CFO/MD | A CFO/CEO/MD is classified as a KMP. Accordingly, compensation paid to the CEO/CFO/MD shall be covered under the Compensation Guidelines. |

| 6 | CXO | As the designation itself implies, the officer is the chief of a particular function. Appropriately, such remuneration should be included under the Guidelines. |

1.7. Given that the Compensation Guidelines are effective from April 1, 2023, are there any immediate actionables for the NBFCs?

Response: Every Applicable NBFC is required to put in place a board approved compensation policy in line with the Compensation Guidelines notified by the RBI.

The provisions of Compensation Guidelines are effective from April 1, 2023. However, the interim period should be seen as a period allowed for preparations. Applicable NBFCs should ideally start aligning their practices in accordance with the provisions of these Guidelines. For instance –

NBFCs which do not have a compatible compensation structure should start planning to align themselves with the Guidelines. Any appointments made in the interim period should consider the provisions of these Compensation Guidelines, even though the Guidelines are only mandatory from April 1, 2023. The same is important in our view, as this would make the NBFCs ready to transition and allow breathing space to NBFCs once the guidelines become mandatory.

NBFCs which do not have an NRC would now be required to have an NRC with the required constitution (see our comments below)

1.8. Will the NBFC need to review the appointment and existing compensation structures of KMP and senior management to ensure that they are in line with these Guidelines when they become applicable from 1st April 2023?

Response: No. Since the Compensation Guidelines are not applicable with retrospective effect, the existing contracts may not be reviewed. The Compensation Guidelines do not seem to give an indication otherwise.

However, in case the director/KMP is getting re-appointed or the compensation is payable after applicability of these Compensation Guidelines, the same should be reviewed so as to ensure adherence to in the Compensation Guidelines. Accordingly, necessary changes may be carried out in the existing compensation structure as well, so that from April, 2023, they are not offending the principles of the Guidelines.

1.9. Given these Guidelines become applicable from 1st April 2023, if the NBFC has to appoint any KMP or senior manager or modify any compensation package, in the interim, does it have to comply with these Guidelines?

Response: As discussed above, the Compensation Guidelines are effective from 1st April 2023; however, the Applicable NBFCs should follow the principles enunciated herein with immediate effect.

Our rationale for the same is as follows:, in essence, the period from notification of the SBR and effective date of the SBR framework is a transitional phase. Herein the NBFCs are being allowed to gradually move their systems towards the new framework and align the existing practices with the notified framework. Stating this, it is important that Applicable NBFCs should be guided by the principles enunciated under the SBR framework in all the activities undertaken even during the transition phase.

1.10. Will there be an impact on the compensation agreed or paid by the NBFC during the FY 2022-23, i.e., before the applicability date?

Response: In our view, the applicability of Compensation Guidelines can be discussed as follows

- Compensation agreed and paid prior to the effective date of the Compensation Guidelines: There shall be no effect on such compensation paid.

- Compensation agreed prior to the effective date but paid after the effective date: Ideally, compensation paid post the effective date should be paid as per the Compensation Guidelines. Any compensation declared prior to the effective date, but paid after the effective date, should be aligned with the Compensation Guidelines. However, there does not seem to be any explicit clarity on this aspect under the notification; hence, one may expect some sort of clarification from RBI.

- Compensation agreed and paid after the effective date: The same should be in accordance with the Compensation Guidelines.

1.11. In case a KMP has been appointed in December 2021 for a period of 5 years, will the Guidelines have an impact on the compensation to be paid after April 1, 2023?

Response: As seen hereinabove, in our view, in case the compensation is agreed to prior to the effective date, but has been paid after the effective date, the compensation should be in accordance with the Compensation Guidelines. Thus, in case a KMP has been appointed in December 2021, compensation can be as per the pre-agreed arrangement till the Compensation Guidelines come into effect. However, post the effective date, the compensation has to be mandatorily in accordance with the Compensation Guidelines.

Further, keeping the applicability date as the beginning of FY 2023, the Applicable NBFCs are being given the time to transition from the erstwhile regulations to the new regulations. Thus, the Applicable NBFCs should strive to align their existing compensation packages with the Compensation Guidelines during the transitional phase.

2. Nomination and Remuneration Committee (NRC)

2.1. What will be the constitution of the NRC in case the NBFC is not required to constitute the committee under the provisions of Companies Act, 2013?

Response: The Compensation Guidelines indicates that the NRC shall have the constitution, powers, functions and duties as laid down in section 178 of the Companies Act, 2013. In this context, the Companies Act requires every NRC to consist of at least three non-executive directors, out of which not less than one-half should be independent directors.

Further, Section 149(4) of the Companies Act, 2013 prescribes that every listed public company shall have at least one-third of the total number of directors as independent directors and the Central Government may prescribe the minimum number of independent directors in case of any class or classes of public companies.

As per the aforesaid provisions, the NRC must have non-executive directors (including independent directors). However, private companies and unlisted public companies are not required to mandatorily appoint either non-executive directors or independent directors on its board. In this case, a situation may arise wherein a company is required to appoint non-executive and independent directors even though the provisions of section 178 are not directly applicable to such a company.

In our view, the NBFC Master Directions no-where require that the ‘composition’ of AC has to be in accordance with sec. 177 of the Cos. Act, though ‘powers, functions, and duties’ are to remain the same [see, explanation II of para 70(1)]. In fact, the Master Directions state that the AC shall comprise of 3 ‘members’ of BoD.

What is envisaged in the Master Directions is that, the AC which has been constituted by a company in terms of sec. 177, shall suffice for the purpose of para 70(1). Hence, where there is no AC as per sec. 177, the composition need not be governed by the provisions of the Companies Act, but by the Master Directions.

2.2. Is there a change required in the constitution of the NRC of an existing NBFC-SI?

Response: While under the existing NBFC Master Directions, there is no specific stipulation as to ‘constitution’ of NRC as per section 178 of the Companies Act; the Compensation Guidelines do specifically require that ‘constitution’ of the NRC should be as per Section 178 of the Companies Act, 2013.

Hence, Applicable NBFCs which did not have the constitution of NRC as per Companies Act may need to realign the same.

2.3. Is there a change required in the constitution of the Audit Committee of an existing NBFC-SI?

Response: The existing provisions of the NBFC Master Directions nowhere require that the ‘composition’ of the Audit Committee has to be in accordance with section 177 of the Companies Act, though ‘powers, functions, and duties’ are to remain the same [refer, explanation II of para 70(1)]. In fact, the NBFC Master Directions state that the Audit Committee shall comprise 3 ‘members’ of the Board of Directors.

What is envisaged in the NBFC Master Directions is that, the Audit Committee which has been constituted by a company in terms of section 177, shall suffice for the purpose of para 70(1). Hence, where there is no Audit Committee as per section 177, the composition need not be governed by the provisions of the Companies Act, but by the NBFC Master Directions.

2.4. Will the Applicable NBFC be required to appoint an independent director(s) for the purposes of constituting the NRC even if it is a private company?

Response: As discussed above, given the explicit stipulation that the constitution of NRC shall be as per section 178 of the Companies Act, 2013, it becomes important to examine the provisions of CA, 2013. Section 178, explicitly applicable to public listed company, requires the NRC to have non-executive and independent directors. The question, therefore, focuses on whether a private company, being a Middle Layer NBFC, needs to have an independent director to sit on the NRC and the Audit Committee.

There are two potential views, and it is important to understand the underlying philosophy of both.

The first view is that private companies are “private”. They have a privately pooled capital, and given that, the boards of private companies are not required by CA to have independent directors at all. This is consistent with the fabric of the company. The whole basis of “privacy” of a private company will be frustrated if there are independent persons on its board. The RBI refers to the CA – both in case of NRC as well as AC. Reference to CA cannot lead to an extension beyond the CA itself. If the CA with corporate governance requirements at its heart does not require private companies to have IDs, the RBI cannot extend that requirement, particularly because the RBI’s Guidelines are on compensation, and not on the fabric of corporate governance. Further, the RBI has clearly preserved the provisions of the law – it, thereofere, cannot subvert or make a dent in those provisions. While the RBI was making a reference to the provisions of the CA, it was not distinguishing between public and private companies, and therefore, the idea is to allow a play to the provisions of the CA.

The second view is as follows:

The provisions under Companies Act are motivated by corporate governance concerns, which vary in intensity as per the constitution of a company. A listed public company or even a public company having large borrowings, etc. is treated differently from a private limited company; reason being obvious, that a private limited company is not dealing with public money or public funds; such a company operates in a closed environment; and as such, stricter corporate governance measures (like an independent director sitting on the the board) are not necessary.

However, the context in which these Compensation Guidelines have been issued is different. The SBR framework takes into account the systemic concerns associated with different NBFCs and thus classifies them into different layers. The Compensation Guidelines are applicable to Middle Layer (NBFCs having asset size of Rs. 1000 crore and above), Upper Layer (NBFCs identified by the RBI and top 10 NBFCs as per asset size) and Top Layer (NBFCs identified as such by the RBI) NBFCs, which, given their asset sizes, are expected to operate at huge volumes and carry a great magnitude of risks. Such NBFCs may have access to public funds (by way of bank borrowings, debenture issuance etc.), wherein large lenders or public would have exposures and consequent high systemic risks. Hence, looking at the constitution (that is whether the NBFC is a private limited or public limited) becomes less important, and looking at the size, activity, and function becomes more important. Therefore, it appears that RBI has now chosen to impose stricter corporate governance norms on such NBFCs. Further:

- The Compensation Guidelines are applicable to only Applicable NFBCs, which fall in the Middle Layer or Upper Layer or Top Layer. This means that only NBFCs having a significant size and systemic importance are required to have the said committee.

- The exemptions from appointment of independent directors were provided to private companies and unlisted public companies, after duly considering their magnitude. Since they operated on a small scale, the mandatory stipulation seemed to be an unnecessary burden.

- Considering the significant importance of NBFC with an asset size of more than 1000 crores, the NBFC should appoint independent directors in the NRC to ensure independence in functioning of the committee.

- Such large NBFCs are likely to have high leverage on their balance sheet, as owned funds may not be an adequate source for their funding operations. Considering that many lenders have exposure to such large NBFCs and there is a very high systemic risk involved, appointment of independent directors would ensure unbiased operations of the NBFC.

Thus, it may not be right to conclude that Applicable NBFCs registered as private companies and unlisted public companies can do away with the mandatory composition prescriptions merely due to the constitutional form of their entity. Looking at the intent and idea of SBR framework, the applicable NBFCs may be required to appoint independent directors irrespective of the form of their constitution.

The scale based regulation emanates from the idea that NBFCs having high risk should be effectively monitored. Thus, the Guidelines should be followed in spirit to effectively mitigate the risks arising in the course of the NBFC’s functioning.

Both the views above have their own merits. On balance, whenever a law refers to another law, it intends to effectively blend the provisions of that law with the scheme of its own. RBI making reference to the composition of the NRC and AC is intending to apply the same principles as in the CA for entities covered by the RBI. If an NRC or AC, if voluntarily constituted by a private company, will not be required to have independent directors as per the CA, it may not be illogical to say that that requirement cannot be an additionality imposed by the RBI Guidelines, as the RBI guidelines do not provide any particular constitution of such committees at all.

2.5. An applicable NBFC is voluntarily complying with the NRC constitution as per section 178 and has required NEDs and IDs on its board. Will it need to reconstitute the NRC as on 1st April, 2023?

Response: The same should not be required. A mere noting that the present NRC shall continue to be the NRC for the purpose of Compensation Guidelines should be sufficient.

2.6. Can the compensation policy be approved by a committee to which the Board has delegated such powers?

Response: The Compensation Guidelines provides that the NRC, inter alia, shall also have the mandate to oversee the framing, review and implementation of compensation policy of the company which should have the approval of the board.

The para suggests that the policy should be mandatorily approved by the board of the Applicable NBFC. The NRC should frame, review and implement the policy. It is only after the approval of the board that the policy would be adopted and implemented. The reason seems obvious, that the compensation policy is of great significance as it governs a potentially high risk area. Thus, the policy approval function has to be mandatorily approved by the board, and cannot be delegated.

2.7. What should be the contents of the compensation policy?

Response: The compensation policy shall have the following particulars:

- Constitution of NRC; scope and applicability in terms of who all does it apply, from when, etc.

- Broad philosophy of the entity about senior management compensation – the objective of attracting and retaining talent, providing reasonable incentives to performance, etc. Reference to HR policy and the interlinkage between this policy and HR policy

- Governance structure – distribution of powers between the Board, NRC and the HR department

- Prudent risk taking principles

- Principles for determining the ratio of fixed/ variable pay in the total compensation of the KMP and members of senior management;

- The principles for determining the proportion of fixed and variable compensation shall be in accordance with the Compensation Guidelines;

- Section 178 of the Companies Act, 2013 also stipulates that the remuneration policy of a company should have a balance between fixed and incentive pay.

- Material risk takers, non risk takers etc

- Performance management systems, key performance indicators

- Malus/ clawback provisions

- Provision against guaranteed bonus, permission for joining bonus

- Variable pay in different scenarios – death, incapacity, termination of employment, disciplinary action, etc

2.8. NRC has to work in close coordination with RMC. What does that mean?

Response: The main motivation behind the Compensation Guidelines is effective mitigation of risks. Risk identification and mitigation across the organisation broadly comes in the domain of RMC. Thus, in order to better mitigate risk, the Compensation Guidelines suggest that the NRC should work in ‘close coordination’ with the RMC.

Extent of variable pay itself is a risk factor, and therefore, the Risk Committee may have a role in the same. Therefore, the broad principles of risk taking, risk takers, and the asset side risks, KPIs etc may have to be aligned with the Risk Committee. The compensation itself is the domain of the NRC.

2.9. Once the NRC is constituted, will it have to review the “fit and proper” status of the NBFC’s existing directors as well?

Response: Under the current framework envisaged in Master Directions, NRCs of all NBFC-SIs are required to assess the “fit and proper” status of the proposed/existing directors on an ongoing basis. The said NBFCs are required to submit a quarterly certificate to the RBI stating that the fit and proper criteria has been followed in selection of directors. Further, a declaration is required to be obtained from the directors, which also contains undertakings w.r.t ascertainment of fit and proper criteria of the directors. Thus, the current guidelines also require assessment of fit and proper criteria.

The same provision has been reiterated in the current Compensation Guidelines as well. Thus, the Applicable NBFCs shall be required to review the “fit and proper” status of the existing directors as well.

2.10. What are the situations where the NRC may assume that there exists a conflict of interest when it comes to the appointment of senior management?

Response: For determining in what situations “conflict of interest” may arise, we have to first assess the meaning of the expression. . Here, conflict of interest means a situation where the interest of the appointee is against or is prejudicial to the interest of the company.

Applicable NBFCs, under the Compensation Guidelines are required to ensure that there is no conflict of interest in the appointment of directors, KMP and senior management, and any time thereafter. For assessing the same, the NRC should take a holistic view of the interest of the directors and other senior management on an ongoing basis and carefully assess the situations where there is a suspected conflict of interest with the directors/KMPs. For instance, the appointee can be a relative of an existing director or KMP in the company. Here, the NRC is required to assess if the appointee possesses requisite qualifications for the position, or he is being appointed merely by virtue of his connections in the company. In case the appointee does not possess the requisite qualifications, his appointment may be detrimental to the interest of the company.

Conflict of interest may also arise due to directorship or shareholding in other companies. For instance, the proposed appointee may be a director/shareholder of a competitor or a group entity.

3. Principles for Compensation

3.1. Is it necessary for all KMPs and senior management to have a variable pay element (with due reference to para 2.3.4 of these Guidelines)?

Response: The Compensation Guidelines requires to address issues arising out of excessive risk taking caused by misaligned compensation packages. As such, the Compensation Guidelines specify that a “reasonable portion” of the remuneration may be given in the form of variable pay. Is this a prescription for having a variable pay component, or caution against larger part of the pay coming in form of variable pay?

In our view, it is clearly the latter. Variable pay, or the performance bonuses, as mentioned above, came under sharp critique in the enquirities into the GFC. While paying senior executives without any linkage with performance may create sloth, promote inefficiency and callousness, at the same time, linking senior executive compensation with performance promotes risk taking. Hence, the stance of the Guidelines is neither to recommend fixed pay, nor to recommend variable pay, but to align variable compensation structures with proper risk management. It is the risk linking, and risk controls, which is the theme of the regulations.

Variable pay is not the device to control risks; instead, variable in many senses is the source of risks. At senior level, it is difficult to think of a compensation structure unconcerned with performance. Hence, variable pay is strongly recommended. However, it should come with due risk management, and considerations which may factor the risks too.

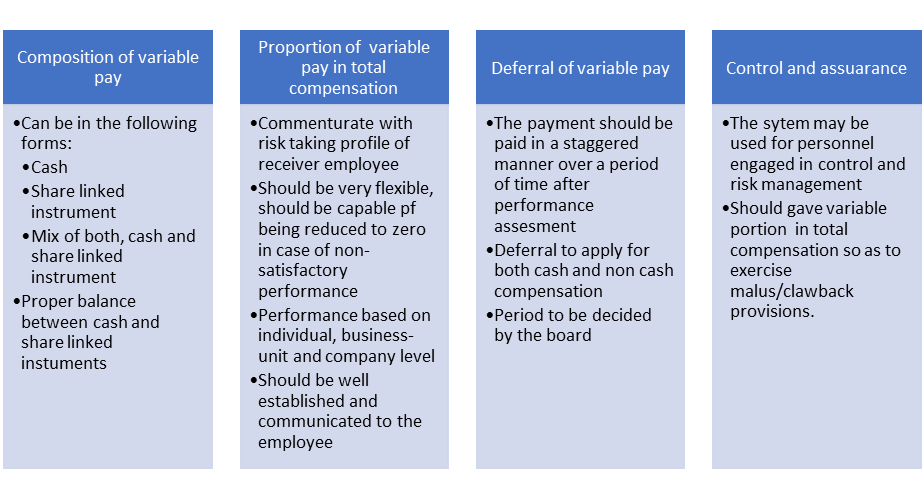

Para 2.3.2 states that the proportion of variable pay in total compensation needs to be commensurate with the role and prudent risk taking profile of KMPs/ senior management. At higher levels of responsibility, the proportion of variable pay needs to be higher. There should be proper balance between the cash and share-linked instruments in the variable pay in case the variable pay contains share linked instruments. The variable pay should be truly and effectively variable and can be reduced to zero based on performance at an individual, business-unit and company-wide level. In order to do so, performance measures and their relation to remuneration packages should be clearly defined at the beginning of the performance measurement period to ensure that the employees perceive the incentive mechanism. .

Hence, while explicitly the Guidelines do not either recommend or bar variable components; however, looking at the contents of this Para, it appears that variable component should form part of the component structure, after risk-related considerations.

3.2. Are there any compensation principles that should be applied for determining the proportion of variable pay for the different KMP roles?

Response: Para 2.3 of the Compensation Guidelines lays down the principles on the basis of which the variable pay component should be based on. The same is as follows:

Further, Para 2.3.2 stipulates that to effectively mitigate the risk, the component of variable pay in the total compensation should be increased with the level of the designation in the hierarchy.

3.3. How will the composition of variable pay structure be determined?

Response: The mix of cash, equity and other forms of compensation must be consistent with risk alignment. The mix will vary depending on the employee’s position and role. The NBFC should be able to explain the rationale for its mix.

3.4. What all may come under ‘share-linked instruments’?

Response: For the purpose of determining what constitutes ‘share-linked instruments’, reference has to be drawn to Securities and Exchange Board of India (Share Based Employee Benefits) Regulations, 2014. Accordingly, the following shall be classified as ‘share-linked instruments’ for the purpose of Compensation Guidelines:

- employee stock option schemes;

- employee stock purchase schemes;

- stock appreciation rights schemes;

- general employee benefits schemes; and

- retirement benefit schemes.

3.5. In case of ESOPs, what would happen to the following, in case such ESOP schemes are not completely aligned with the Compensation Guidelines:

- ESOP scheme approved, no vesting has taken place

- ESOP vesting has taken place, no exercise has been made

- ESOPs have been exercised

Response: The scenarios shall be dealt with in the following manner:

| S. No | Scenario | Response |

| 1 | ESOP scheme approved, no vesting has taken place | In such a case, the NRC has an option to withdraw the ESOP scheme. In case the NRC has the discretion to withdraw the ESOP (as per the provisions of the ESOP Scheme), the committee should specify the reasons for withdrawing the same. |

| 2 | ESOP vesting has taken place, no exercise has been made | Once vested, ESOP may be taken back in case the employee is proved to be involved in an act of fraud or misrepresentation. Further, the same is also dependent on the ESOP plan of the company. Upon any negative event listed in the ESOP plan, the company may withdraw the ESOP granted to any employee, with prior approval of NRC. In case the NRC has the discretion to withdraw the ESOP (as per the provisions of the ESOP Scheme), the committee should specify the reasons for withdrawing the same. |

| 3 | ESOPs have been exercised | In case the option has already been exercised, the company does not have an option to withdraw the exercised ESOP, since the ownership has already passed to the employee. |

3.6. Will the compensation policy of the NBFC need to ensure that positions higher in the organisational hierarchy should have a higher proportion of variable pay than those below?

Response: Yes. As discussed above, variable pay acts as a tool to control the risks arising out of misaligned compensation packages. Para 2.3.2 of the Compensation Guidelines provides that at higher levels of responsibility, the proportion of variable pay needs to be higher. This is because of the fact that the risk-taking ability as well as responsibility increases as one moves up in the organisational hierarchy. Thus, to adequately compensate for the risk-taking at the top of the hierarchy, variable portion in the total compensation should be increased commensurately. Also, as mentioned earlier, this would also enable implementation of malus/clawback provisions.

3.7. Does the variable pay of senior management necessarily have to be associated with performance at all three levels – individual, business and company?

Response: Yes. The performance is to be assessed at all the three levels. Practically looking, performance assessment at the individual level indicates growth in an individual. Performance at the business and company level indicates the individual’s contribution in the growth of the business and company. Thus, to have a holistic view of his growth, it is important to analyse performance of the individual at all the three levels.

3.8. Can the variable pay component be more than the fixed pay?

The Compensation Guidelines do not clearly specify the proportion of fixed and variable compensation in the total compensation. Thus, the proportion of the same is clearly subjective and depends upon the decision of the NRC taken in accordance with the dynamics of the company and the industry standards. However, in this regard, the Compensation Guidelines indicate that at higher levels of responsibility, the proportion of variable pay needs to be higher. Accordingly, while determining the ratio of fixed and variable pay in the total compensation at higher levels in the organisation, the NRC should keep the variable component higher than the fixed component. The same is done with a view to effectively compensate for the higher risk at higher levels in the company.

3.9. Can the deferral period for variable pay be decided by the NRC or any other committee authorised by the Board?

Response: No. Para 2.3.3 of the Compensation Guidelines stipulates that the deferral period may be decided by the board of the company. Thus, the same cannot be delegated. The reason behind the stipulation being that the decision for deferral is of utmost importance as it leads to reduction of immediate payment of compensation to the personnel, to which he is entitled to at that particular point of time. Thus, such a decision should be taken by the highest level of authority.

3.10. How are compensation payouts to be structured in line with the time horizon of risks (reference, para 2.3.3of the Compensation Guidelines)?

Response: Any risk assumed has a time horizon, that is, there is an estimated time period over which the results/outcome of the risk assumed is realised in which the risk may or may not materialise. There are certain cases where outcome is realised in a short time span, while there are some where outcome is realised only in the long-run.

Variable compensation payments should be structured accordingly. Payments should not be finalised over short periods where risks are realised over long periods. There must be adequate mechanism to avoid or defer payouts for income that cannot be realised or whose likelihood of realisation remains uncertain at the time of payout. The malus/clawback provisions may capture this.

3.11. Should the compensation policy of compliance and control function roles be necessarily delinked from the performance of the business areas they oversee?

Response: Employees that are engaged in the financial and risk control areas or as a part of compliance function must be independent, have appropriate authority, and be compensated in a manner that is independent of the business areas they oversee and commensurate with their key role in the NBFC. Effective independence and appropriate authority of such staff is necessary to preserve the integrity of financial and risk management’s influence on incentive compensation. Hence, the compensation should be delinked from the business performance.

4. Guaranteed Bonus

4.1. Will a clause with respect to”thirteenth month salary” i.e. an additional month’s salary that is paid if the senior manager remains with the company for the entire fiscal, in the compensation package be considered as a guaranteed bonus?

Response: Yes. Guaranteed bonus is a compensation to an employee, which is not linked to performance of the employee. Hence, such a loyalty bonus cannot be a part of the compensation package. However, pursuant to Para 3 of the Compensation Guidelines, joining/sign-on bonus can be payable upon new hiring of employees, which will neither be considered part of fixed pay nor of variable pay.

5. Malus and Clawback

5.1. What is malus/clawback?

Response: Clawback means an arrangement wherein the employee returns the previously paid incentives. Malus refers to an arrangement wherein the employee is not allotted/granted the compensation to which he is entitled to. Unlike clawback clauses, malus clause does not permit reversal of compensation already paid to the employee.

5.2. Under what scenarios, malus/clawback can be applied? Are these provisions mandatory or voluntary?

Response: Yes. Para 4 of the Compensation Guidelines provides for provision of clawback clauses in the compensation arrangement with the employee. Though the language of the text suggests that provision of such clauses is voluntary in nature, looking at the essence of the Compensation Guidelines, clawback clauses should ideally be provided for in the compensation arrangement.

The Compensation Guidelines have specified certain principles to be followed while invoking the clawback clause:

- The clause may be invoked due to the negative performance of the NBFC or due to misconduct of the employee.

- The NBFC should identify a set of circumstances under which the clause will be invoked.

- The NBFC should identify time periods during which such deferral may be invoked.

- Such a period should mandatorily be equal to at least the retention period.

Provisions of the same have been inserted to ensure that non-performing employees do not get rewarded. Further, the clawback provisions ensure that time-based risks are adequately factored in. This makes the compensation arrangement entirely performance based.

However, it may be noted that specific laws like SEBI regulations of Share-based Employee Benefits provide that the ESOPs may lapse due to a negative financial performance, hence, the ESOP Scheme must also be aligned with the Compensation Policy.

[1] NBFCs other than NBFC-BL and NBFCs owned by the Government (‘Applicable NBFCs)

Our other resources on the topic may be viewed here: https://vinodkothari.com/sbr/

Leave a Reply

Want to join the discussion?Feel free to contribute!