Archive for month: May, 2021

Social Stock Exchanges – Enabling funding for social enterprises the regulated way

By Sharon Pinto & Sachin Sharma, Corplaw division, Vinod Kothari & Company (corplaw@vinodkothari.com)

Background

The inception of the idea of Social Stock Exchanges (SSEs) in India can be traced to the mention of the formation of an SSE under the regulatory purview of Securities and Exchange Board of India (SEBI) for listing and raising of capital by social enterprises and voluntary organisations, in the 2019-20 Budget Speech of the Finance Minister. Consequently, SEBI constituted a working group on SSEs under the Chairmanship of Shri Ishaat Hussain on September 19, 2019[1]. The report of the Working Group (WG) set forth the framework on SSEs, shed light on the concept of social enterprises as well as the nature of instruments that can be raised under such framework and uniform reporting procedures. For further deliberations and refining of the process, SEBI set up a Technical Group (TG) under the Chairmanship of Dr. Harsh Kumar Bhanwala (Ex-Chairman, NABARD) on September 21, 2020[2]. The report, made public on May 6, 2021[3], of the TG entails qualifying criteria as well as the exhaustive ecosystem in which such an SSE would function.

In this article we have analysed the framework set forth by the reports of the committees with the globally established practices.

Concept of SSEs

As per the report of the WG dated June 1, 2020[4], SSE is not only a place where securities or other funding structures are “listed” but also a set of procedures that act as a filter, selecting-in only those entities that are creating measurable social impact and reporting such impact. Further the SSE shall be a separate segment under the existing stock exchanges. Thus, an SSE provides the infrastructure for listing and disclosure of information of listed social enterprises.

Such a framework has been implemented in various countries and an analysis of the same can be set forth as follows:

A. United Kingdom

- The Social Stock Exchange (SSX) was formed in June 2013 on the recommendation of the report of Social Investment Taskforce. The exchange does not yet facilitate share trading, but instead serves as a directory of companies that have passed a ‘social impact test’. It thus provides a detailed database of companies which have social businesses. It facilitates as a research service for potential social impact investors.

- Further, companies that are trading publically in the main board stock exchange, may list their securities on SSX, thus only for-profit companies can list on the SSX[5] It works with the support of the London Stock Exchange and is a standalone body not regulated by any official entity.

- Social and environment impact is the core aim of SSX. To satisfy the same, companies are required to submit a Social Impact Report for review by the independent Admissions Panel composed of 11 finance and impact investing experts.

- The disclosure framework comprises adherence to UK Corporate Governance Guidelines and Filing Annual Social Impact Reports determine the continuation of listing in SSX.

B. Canada

- Social Venture Connection (SVX)[6] was launched in 2013. Like SSX, SVX is not an actual trading platform but it is a private investment platform built to connect impact ventures, funds, and investors. It is open only for institutional investors[7].

- The platform facilitates listing of for-profit business, NPO, or cooperatives categorized as, Social Impact Issuers and Environment Impact Issuers. These entities are required to be incorporated in Ontario for at least 2 years and have audited financial statements available.

- For listing, a for-profit business must obtain satisfactory company ratings through GIIRS, a privately administered rating system.

- Issuer must conform to the SVX Issuer Manual. In addition to this reporting of expenditure and other financial transactions shall be done once capital is raised. Further the issuers are required to file financial statements annually in accepted accounting methods and shall not have any misleading information. Ratings are required to be obtained, however the provisions are silent on the periodicity of revision of ratings.

C. Singapore

- Singapore has established Impact Exchange (IX) which is operated by Stock Exchange of Mauritius and regulated by the Financial Service Commission of Mauritius.

- IX is the only SSE that is an actual public exchange. It is thus a public trading platform dedicated to connecting social enterprise with mission-aligned investment. Social enterprises, both for-profits and non-profits, are permitted to list their project. NGOs are allowed as issuers of debt securities (such as bonds).

- Listing requirements on the exchange are enumerated into social and financial categories. Following comprise the social criteria for listing:

- Specify social or economic impact as the reason for their primary existence.

- Articulate the purpose and intent of the company in the form of a theory of change- basis for demonstrating social performance.

- Commit to ongoing monitoring and evaluation of impact performance assessment and reporting.

- Minimum 1 year of impact reports prepared as per IX reporting principles.

- Certification of impact reports by an independent rating body 12 months prior listing.

Further the financial criteria entails the need for a fixed limit of minimum market capitalization, publication of financial statements and use of market-based approach for achieving its purpose.

D. South Africa

- The ‘South Africa Social Exchange’ or SASIX[8], offers ethical investors a platform to buy shares in social projects according to two classifications: by sector and by province[9]. Guidelines for listing prescribe compliance with SASIX’s good practice norms for each sector.

- In order to get listed, entities have to achieve a measurable social impact. The platform acts as a tool of research, evaluation and match-making to facilitate investments into social development projects

- NGOs can also list their social projects on the exchange. Value of the projects is assessed and then divided into shares. Following project implementation, investors are given access to financial and social reports.

- While social enterprises are required to have a social purpose as their primary aim, they are also expected to have a financially sustainable business model. The SASIX ceased functioning in 2017[10].

Key ingredients for a social enterprise

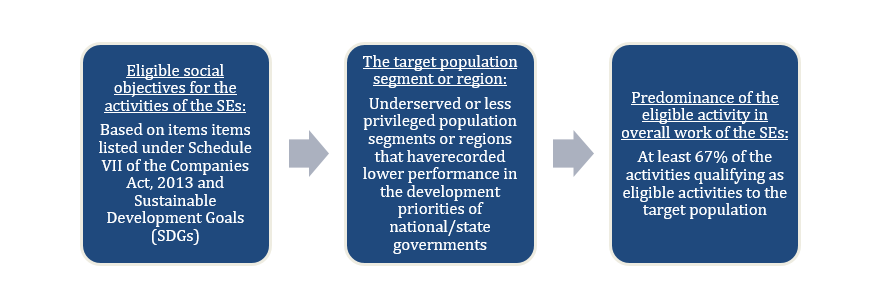

- The report of the TG[11] has categorised social enterprises into For Profit Enterprise (FPEs) and Not for Profit Organisation (NPOs). In order to qualify as a social enterprise the entities shall establish primacy of social impact which shall be determined by application of the following 3 filters:

- On establishment of the primacy of social impact through the three filters as stated above, the entity shall be eligible to qualify for on-boarding the SSE and access to the SSE for fund-raising upon submitting a declaration as prescribed.

Qualifying criteria and process for onboarding

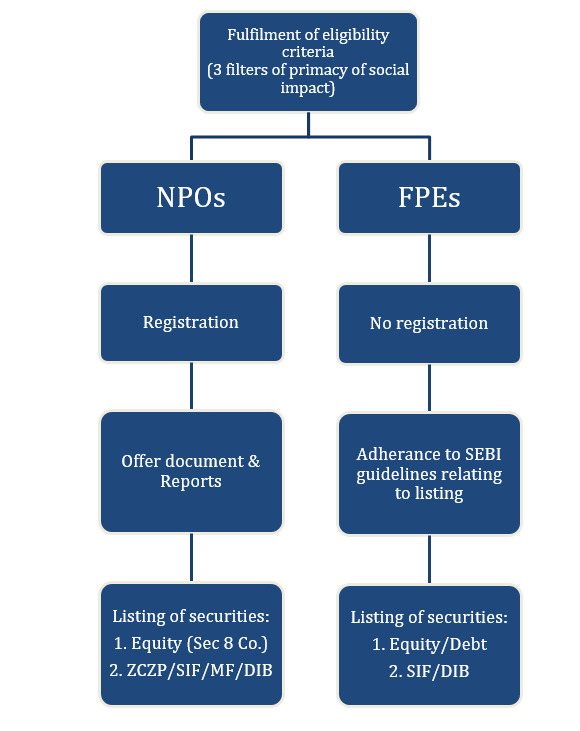

As per TG recommendation, an NPO is required to register on any of the Social Stock Exchange and thereafter, it may choose to list or not. However, an FPE can proceed directly for listing, provided it is a company registered under Companies Act and complies with the requirements in terms of SEBI Regulations for issuance and listing of equity or debt securities.

Further, the TG has recommended a set of mandatory criteria as mentioned below that NPOs shall meet in order to register.

A. Legal Requirements:

- Entity is legally registered as an NPO (Charitable Trust/ Society/Section-8 Co’s).

- Shall have governing documents (MoA & AoA/ Trust Deed/ Bye-laws/ Constitution) & Disclose whether owned and/or controlled by government or private.

- Shall have Registration Certificate under 12A/12AA/12AB under Income Tax.

- Shall have a valid IT PAN.

- Shall have a Registration Certificate of minimum 3 years of its existence.

- Shall have valid 80G registration under Income-Tax.

B. Minimum Fund Flows:

In order to ensure that the NPO wishing to register has an adequate track-record of operations.

- Receipts or payments from Audited accounts/ Fund Flow Statement in the last financial year must be at least Rs. 50 lakhs.

- Receipts from Audited accounts/ Fund Flow Statement in the last financial year must be at least Rs. 10 lakhs.

Framework for listing

Post establishment of the eligibility for listing and the additional registration criteria in case of NPOs, the social enterprises may list their securities in the manner discussed further. The listing procedures vary for NPOs and FPEs and is set forth as follows:

A. NPOs

- NPO shall be required to provide audited financial statements for the previous 3 years and social impact statements in the format prescribed. Further the offer document shall comprise of ‘differentiators’ which shall help the potential investors to assess the NPOs being listed and form a sound and well-informed investment decision. A list of 11 such differentiators has been provided in the report of the TG.

- Further in case of program-specific or project-specific listings, the NPO shall have to provide a greater level of detail in the listing document about its track record and impact created in the program target segment.

- All the information submitted as part of pre-listing and post-listing requirements, shall be duly displayed on the website of the NPO.

B. FPEs

- In case of an FPE, existing regulatory guidelines under various SEBI Regulations for listing securities such as equity, debt shall be complied with.

- The differentiators will be in addition to requirements as mandated in SEBI Regulations in respect of raising funds through equity or debt.

- Further, FPEs have been granted an option to list their securities on the appropriate existing boards. Thus the issuer may at their discretion list their debt securities on the main boards, while equity securities may be listed on the main boards, or on the SME or IGP.

Types of instruments

Depending on the type of organisation, SSEs shall allow a variety of financing instruments for NPOs and FPEs. As FPEs have already well-established instruments, these securities are permitted to be listed on the Main Board/IGP/SME, however visibility shall be given to such entities by identifying them as For Profit Social Enterprise (FPSE) on the respective stock exchanges.

Modes available for fundraising for NPOs shall be Equity (Section 8 Co’s.), Zero Coupon Zero Principal (ZCZP) bonds [this will have to be notified as a security under Securities Contracts (Regulation) Act, 1956 (SCRA)], Development Impact Bonds (DIB), Social Impact Fund (SIF) (currently known as Social Venture Fund) with 100% grants-in grants out provision and funding by investors through Mutual Funds. On the other hand, FPEs shall be able to raise funds through equity, debt, DIBs and SIFs.

While SVF is an existing model for fund-raising, the TG has proposed various changes in order to incentivise investors and philanthropists to invest in such instruments. In addition to change in nomenclature from SVF to SIF, minimum corpus size is proposed to be reduced from Rs. 20 Cr to Rs. 5 Cr. Further, minimum subscription shall stand at Rs. 2L from the current Rs. 1 Cr. The amendments shall also allow corporates to invest CSR funds into SVFs with a 100% grants-in, grants out model.

Disclosure and Reporting norms

Once the FPE or the NPO (registered/listed) has been demarcated by the exchange to be an SE, it needs to comply with a set of minimum disclosure and reporting requirements to continue to remain listed/registered. The disclosure requirements can be enlisted as follows:

For NPO:

- NPO’s (either registered or listed) will have to disclose on general, governance and financial aspects on an annual basis.

- The disclosures will include vision, mission, activities, scale of operations, board and management, related party transactions, remuneration policies, stakeholder redressal, balance sheet, income statement, program-wise fund utilization for the year, auditors report etc.

- NPO’s will have to report within 7 days any event that might have a material impact on the planned achievement of their outputs or outcomes, to the exchange in which they are registered/listed. This disclosure will include details of the event, the potential impact and what the NPO is doing to overcome the impact.

- NPO”s that have listed its securities will have to disclose Social Impact Report covering aspects such as strategic intent and planning, approach, impact score card etc. on annual basis.

For FPE:

FPE’s having listed equity/debt will have to disclose Social Impact Report on annual basis and comply with the disclosure requirements as per the applicable segment such as main board, SME, IGP etc.

Other factors of the SSE ecosystem

a. Capacity Building Fund

As per the recommendation of the WG, constitution of a Capacity Building Fund (CBF) has been proposed. The said fund shall be housed under NABARD and funded by Stock Exchanges, other developmental agencies such as SIDBI, other financial institutions, and donors (CSRs). The fund shall have a corpus of Rs. 100 Cr and shall be an entity registered under 80G, which shall make it eligible for receiving CSR donations pursuant to changes to Section 135/Schedule VII of Companies Act 2013. The role of the fund shall encompass facilitating NPOs for registration and listing procedures as well as proper reporting framework. These functions shall be carried out in the form awareness programs.

b. Social Auditors

Social audit of the enterprises shall compose of two components – financial audit and non-financial audit, which shall be carried out by financial or non-financial auditors. In addition to holding a certificate of practice from the Institute of Chartered Accountants of India (ICAI), the auditors will be required to have attended a course at the National Institute of Securities Markets (NISM) and received a certificate of completion after successfully passing the course examination. The SRO shall prepare the criteria and list of firms/institutions for the first phase soon after the formation of SSEs, and those firms/institutions shall register with the SRO.

c. Information Repositories

The platform shall function as a research tool for the various social enterprises to be listed, thus Information Repository (IR) forms an important component of the framework. It functions as an aggregator of information on NGOs, and provides a searchable electronic database in a comparable form. Thus it shall provide accurate, timely, reliable information required by the potential investors to make well informed decisions.

Conclusion

The social sector in India is getting increasingly powerful – this was evident during Covid-crisis based on the wonderful work done by several NGOs. Of course, all social work requires funding, and being able to crowd source funding in a legitimate and transparent manner is quintessential for the social sector. We find the report of the TG to be raising and addressing relevant issues. We are hoping that SEBI will now find it easy to come out with the needed regulatory platform to allow social enterprises to get funding through SSEs.

Our other article on the similar topic can be read here – http://vinodkothari.com/2019/09/social-stock-exchange-a-guide/

[1] https://www.sebi.gov.in/media/press-releases/sep-2019/sebi-constitutes-working-group-on-social-stock-exchanges-sse-_44311.html

[2] https://www.sebi.gov.in/media/press-releases/sep-2020/sebi-constitutes-technical-group-on-social-stock-exchange_47607.html

[3] https://www.sebi.gov.in/reports-and-statistics/reports/may-2021/technical-group-report-on-social-stock-exchange_50071.html

[4] https://www.sebi.gov.in/reports-and-statistics/reports/jun-2020/report-of-the-working-group-on-social-stock-exchange_46852.html

[5] https://scholarship.law.upenn.edu/cgi/viewcontent.cgi?article=1906&context=jil&httpsredir=1&referer=

[7] https://ssir.org/articles/entry/the_rise_of_social_stock_exchanges

[9] https://ssir.org/articles/entry/the_rise_of_social_stock_exchanges

[10] https://www.samhita.org/wp-content/uploads/2021/03/India-SSE-report-final.pdf

[11] https://www.sebi.gov.in/reports-and-statistics/reports/may-2021/technical-group-report-on-social-stock-exchange_50071.html

SEBI eliminates one-to-one analyst meets from the purview of LODR

-Recommendations of sub-group dropped under the LODR Amendment

By CS Aisha Begum Ansari, Assistant Manager, Vinod Kothari & Company

Background

Information symmetry is extremely important in a listed company since it helps in effective price discovery and builds the faith of the investors. Analyst and investor meets are one of the many ways used by the companies to disseminate information. The companies usually conduct analyst or investor meets after the disclosure of financial results to answer the questions relating to financial performance, future prospects, etc. based on generally available information without disclosing any unpublished price sensitive information (‘UPSI’). Such meets generally include conference calls or meeting with group of investors or group of analysts as per the prefixed schedule. Further, the same also includes one-to-one meet or calls with investors or analysts, which may either be prefixed or in the nature of walk-in.

While, SEBI mandates provisions under the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘Listing Regulations’) and SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’) to curb as well as regulate such leak of UPSI; one of the recent changes under the Listing Regulations vide SEBI Listing Regulations (Second Amendment) Regulations, 2021[1] (‘LODR Amendment’) issued on 7th May, 2021 seems to have completely excluded one-to-one meet from the regulatory ambit prescribing disclosure requirements.

This article discusses the regulatory requirement in relation to investor meet, phases of amendment, present requirement and international practice.

Compliance requirements under SEBI Regulations

Erstwhile Listing Agreement

Clause 49 of the Listing Agreement[2] which specified the reporting requirements, obligated the companies to disclose on its website or intimate the stock exchange the presentations made by it to the analysts. Also, the companies were required to disclose in its Report on Corporate Governance, presentations made to institutional investors or the analysts as a means of communication to shareholders.

Listing Regulations (prior to amendment)

The Listing Regulations mandated listed entities to disclose the schedule of analyst or investor meets and presentations to such analysts or investors –

- On the website of the listed entity [Regulation 46(2)(o) of Listing Regulations]

- On the website of the stock exchange where its securities are listed (Clause 15 of Para A, Part A of Schedule III of Listing Regulations).

- Means of communication in the form of presentations made to institutional investors or analyst in the annual corporate governance report. (Para C(8)(e) of Schedule V to Listing Regulations).

Erstwhile PIT Regulations (1992)

The 1992 regulations prescribed elaborate requirement in relation to analyst meets. Listed companies were required to follow the following guidelines while dealing with analysts and institutional investors:—

- Only Public information to be provided – Listed companies were required to provide only public information to the analyst/research persons/large investors like institutions. Alternatively, the information given to the analyst were required to be simultaneously made public at the earliest.

- Recording of discussion – In order to avoid misquoting or misrepresentation, it was suggested that at least two company representative to be present at meetings with analysts, brokers or institutional investors and discussion should preferably be recorded.

- Handling of unanticipated questions – A listed company were required to be careful when dealing with analysts’ questions that raise issues outside the intended scope of discussion. It was suggested that unanticipated questions could be taken on notice and a considered response could be given later. If the answer included price sensitive information, a public announcement was required to be made before responding.

- Simultaneous release of Information – When a company organized meetings with analysts, the company was required to make a press release or post relevant information on its website after every such meet. The company could also consider live webcasting of analyst meets.

PIT Regulations

PIT Regulations, presently, mandate listed entities to develop best practices to make transcripts or records of proceedings of meetings with analysts and other investor relations conferences on the official website to ensure official confirmation and documentation of disclosures made. Further, the listed entity needs to ensure that information shared with analysts and research personnel is not UPSI.

Discussion in working group/ committee reports

Report submitted by the Committee on Corporate Governance[3]

The Committee was of the view that the disclosure of schedules of analyst/ institutional investor meetings does not serve any practical purpose, and there have been instances of its misuse. Hence, the Committee recommended that the disclosure of schedules of analyst/institutional investor meetings may not be required. However, the information to be shared at such meetings has to be strictly in compliance with the SEBI PIT Regulations.

Report on disclosures pertaining to analyst/ investors meets[4]

The issue of information asymmetry between various classes of investors arising out of limited disclosures in respect of analyst meets/ institutional investors meet/ conference calls was discussed by Primary Markets Advisory Committee (PMAC) in the meeting in July, 2020. SEBI, based on the recommendation of PMAC, had formed sub-group which issued the ‘Report on disclosures pertaining to analyst meets, investor meets and conference calls’ (‘Report’) on November 20, 2020.

The Committee deliberated on best practice followed by listed entities in India, regulatory regime in developed countries and acknowledged the fact that existing regulations are not followed in letter and spirit by majority of listed companies thereby causing information asymmetry.

The Report explicitly distinguished between group analysts or investors meet and one-to-one in terms of the regulatory compliance. The Report recommended disclosure of transcripts and recordings of proceedings of group investors meet on the website of the company and to the stock exchange within a prescribed time frame whereas for one-to-one meetings, it recommended disclosing the number of such meetings in the quarterly compliance report on corporate governance along with a confirmation that no UPSI was shared with them.

The committee provided the rationale that the fundamental reason for analysts to seek meetings with the listed entity was to check their hypothesis that they have developed, based on controls and processes that have been built to comply with the public disclosures and complying with regulations relating to handling of private information and that premature public disclosure of these questions may lead to a regime of ‘’mandatory dissemination of proprietary information’’.

It is also important to note that the sub-group in its Report discussed that the content of the discussions for one-to-one meets, should not be intimated to the stock exchange due to following demerits:

- Invasion of privacy of the institutional investors;

- Allow third parties not a part of the meet to take speculative positions for trading decisions; and

- Lead to overload of information to retain investors

Based on the sub-group’s discussion, the following recommendations were made:

- Provide number of one-to-one meet as part of corporate governance report on a quarterly basis while submitting to the stock exchange;

- The same needs to carry an affirmation that no UPSI was shared by any official of the company in such meetings; and

- Company to maintain a record of all one-to-one meetings covering the name/names of the investor who were met, the name of the fund that he/ she represents, name of the brokerage firm which fixed the meeting (if any), the location, date and time of the meeting and a reference to the presentation made and preserve the same for a period of at least eight years.

Discussion in SEBI Board meeting of March 25, 2021[5]

The agenda provides details of recommendation made in relation to group analyst meet, however, does not provide any rationale/ discussion with respect to one-to-one meeting or reason for excluding the requirement from Listing Regulations altogether.

Anomaly in the LODR Amendment

Regulation 46(2)(o) and Clause 15(a) of Para A, Part A of Schedule III of Listing Regulations defines the term ‘meet’ as ‘group meetings or group conference calls’ for the purpose of disclosure of schedule of analyst/ investor meet and presentations made by the company to them.

Further, regulation 46(2)(oa) and Clause 15(b) of Para A, Part A of Schedule III provides for manner of disclosure of audio/ video recordings and transcripts of post earning calls or quarterly calls on the website of the company and to the stock exchange respectively. The said sub-clause has no reference of the term ‘meet’. The said provisions are reproduced below:

Regulation 46(2)(oa):

“(oa) Audio or video recordings and transcripts of post earnings/quarterly calls, by whatever name called, conducted physically or through digital means, simultaneously with submission to the recognized stock exchange(s), in the following manner:

- the presentation and the audio/video recordings shall be promptly made available on the website and in any case, before the next trading day or within twenty-four hours from the conclusion of such calls, whichever is earlier;

- the transcripts of such calls shall be made available on the website within five working days of the conclusion of such calls:

Provided that—

- The information under sub-clause (i) shall be hosted on the website of the listed entity for a minimum period of five years and thereafter as per the archival policy of the listed entity, as disclosed on its website.

- The information under sub-clause (ii) shall be hosted on the website of the listed entity and preserved in accordance with clause (a) of regulation 9.

The requirement for disclosure(s) of audio/video recordings and transcript shall be voluntary with effect from April 01, 2021 and mandatory with effect from April 01, 2022.”

Clause 15(b) of Para A, Part A of Schedule III

“(b) Audio or video recordings and transcripts of post earnings/quarterly calls, by whatever name called, conducted physically or through digital means, simultaneously with submission to the recognized stock exchange(s), in the following manner:

- the presentation and the audio/video recordings shall be promptly made available on the website and in any case, before the next trading day or within twenty-four hours from the conclusion of such calls, whichever is earlier;

- the transcripts of such calls shall be made available on the website within five working days of the conclusion of such calls:

The requirement for disclosure(s) of audio/video recordings and transcript shall be voluntary with effect from April 01, 2021 and mandatory with effect from April 01, 2022.”

Since, the term ‘meet’ is not mentioned in the above provisions, it leads to an interpretation that in case of post earning calls or quarterly calls, irrespective of the fact whether such meeting is with the group of investors or one-to-one meeting, audio/ video recordings and transcripts will be required to be submitted to the stock exchange.

Regulatory regime in other countries

1. United States of America

Regulation Fair Disclosure[6] (referred as ‘Regulation FD’) prohibits companies from selectively disclosing material non-public information (referred as ‘MNPI’) to analysts, institutional investors, and others without concurrently making widespread public disclosure.

Response to question 101.11 of the FAQs on Regulation FD[7] allows directors of the company to speak privately with a shareholder or group of shareholders by implementing policies and procedures to help avoid insider trading. Also, where a shareholder expressly agrees, through confidentiality agreement, to maintain confidentiality of MNPI, a private communication between the director and a shareholder does not violate Regulation FD norms.

2. Canada

Part V of the National Policy on Disclosure Standards[8] provides guidelines with respect to private briefings with analysts/ institutional investors. The Policy does not prohibit one-to-one discussions with analysts but identifies that the potential of selective disclosure of material non-public information is fraught with difficulties. It emphasizes on timely public disclosure of material information and entering into confidentiality agreements with the analysts.

3. United Kingdom

Market Abuse Regulation (“MAR”)[9] prevents selective disclosure of MNPI. MAR requires that the companies must not disclose MNPI selectively at the investor meetings. If they do, an immediate announcement would be required but it would still be a breach of the regulations.

4. Singapore

Rule 703(4) of the Singapore Exchange Listing Rules[10] requires the issuer to observe the Corporate Disclosure Policy as provided under Appendix 7.1. of Rule[11]. Para 23 under PART VIII of the Policy recommends the issuer to observe an “open door” policy in dealing with analysts, journalists, stockholders and others.

Issuer is required to abstain from disseminating material information which has not been disclosed to the public before. However, if such material information is inadvertently disclosed at meetings with analysts or others, it must be publicly disseminated as promptly as possible by the means described in Part VIII.

Conclusion

One-to-one meets carry a significant amount of risk with it for being a source / device for leak of UPSI especially where the same are not explicitly regulated. The intent behind recording and disclosing the same is to safeguard the company officials from any potential charge of breach of PIT Regulations. One will have to wait and watch if the relaxation results in any adverse implications. Further, SEBI will have to clarify on the ambiguity relating to disclosure requirements of one-to-one analysts meet w.e.f. post earning calls or quarterly calls if the intent is to restrict only to ‘meet’ as defined in the respective clauses.

[1] https://egazette.nic.in/WriteReadData/2021/226859.pdf

[2]https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/1293168356651.pdf#page=7&zoom=page-width,-16,792

[3] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/oct-2017/1509102194616.pdf#page=1&zoom=page-width,638,870

[4] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/nov-2020/1605853267317.pdf#page=1&zoom=page-width,-16,792

[5] https://www.sebi.gov.in/sebi_data/meetingfiles/apr-2021/1619067296590_1.pdf

[6] https://www.sec.gov/rules/final/33-7881.htm

[7] https://www.sec.gov/divisions/corpfin/guidance/regfd-interp.htm

[8] https://www.osc.ca/sites/default/files/pdfs/irps/pol_20020712_51-201.pdf

[9] https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014R0596&from=EN

[10] http://rulebook.sgx.com/rulebook/703-0

[11] http://rulebook.sgx.com/rulebook/appendix-71-corporate-disclosure-policy

Our article titled SEBI proposes enhanced disclosures for meetings with analyst, investors, etc. can be accessed through following link:

SEBI notifies substantial amendments in Listing Regulations

Proposals approved in SEBI BM of March, 2021 made effective

Payal Agarwal | Executive ( corplaw@vinodkothari.com ) May 07, 2021

Introduction

SEBI, the capital market regulator of India, vide a gazette notification dated 06th May, 2021 notified Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Second Amendment) Regulations, 2021 [“the Amendment Regulations”] that were approved in SEBI’s Board Meeting held on March 25, 2021. Most of the amendments were already rolled out earlier as consultation papers in 2020. The amendments become effective from May 06, 2021.

This article discusses the major amendments carried out and the likely impact and actionable for the listed entities.

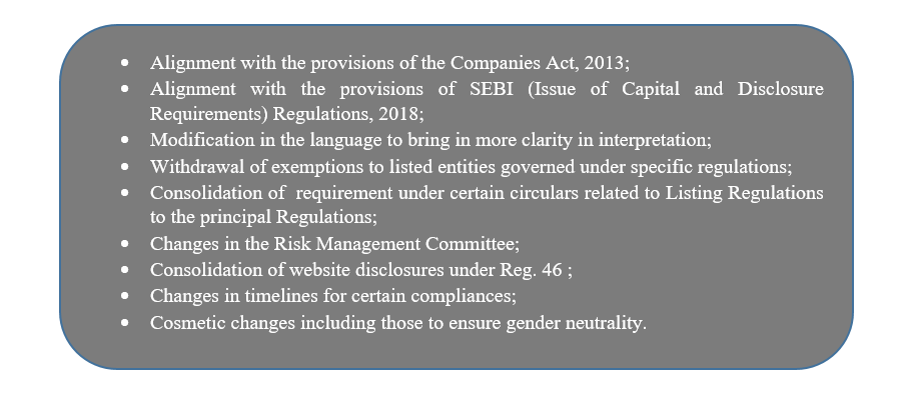

Brief of the amendments are as follows –

A gist of all the amendments under the Amendment Regulations have been captured in a snippet.

A gist of all the amendments under the Amendment Regulations have been captured in a snippet.

1. Applicability of the Listing Regulations

In terms of Regulation 3 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2013 (‘Listing Regulations’) the provisions of Listing Regulations are applicable to entities that list the designated securities on the stock exchange.

The Amendment Regulations clarify that the applicability of certain provisions of Listing Regulations based on market capitalisation will continue to apply even where the entities fall below the prescribed threshold.

While the market capitalisation may be derived for any day, the recognised stock exchanges viz. BSE Limited and National Stock Exchange of India Limited releases a list of listed entities based on market capitalisation periodically. However, the provisions under Listing Regulations become applicable based on market capitalisation as at the end of the immediate previous financial year.

The present amendment on the continuation of applicability of provisions even after the listed entity ceasing to be among the top 500, 1000, 2000 listed entities, as the case may be, seems inappropriate. The applicability of these provisions were originally introduced in view of the size of the listed entities that held major market cap. Indefinite applicability of the said provisions despite fall in the market capitalisation of the listed entity is more of a compliance burden. The provision should be amended by SEBI in line with the timeframe provided under Reg. 15 i.e. where a listed entity does not fall under the list of top 100, 500, 1000, 2000 for three consecutive financial years, the compliance requirement should cease to apply.

Therefore, a conjoint reading of both the provisions should be allowed to take a liberal interpretation in respect of the newly-inserted Regulation 3(2) as well, thereby relaxation of compliance requirements on completion of a look-back period of 3 consecutive financial years.

2. Risk Management Committee

Regulation 21 of Listing Regulations requires the listed entities to constitute a Risk Management Committee (RMC). A comparative study of the erstwhile and the amended provisions w.r.t RMC is given below –

| Topic | Erstwhile provisions | Amended provisions |

| Applicability of RMC | · On top 500 listed entities (Based on market capitalisation) | · On top 1000 listed entities based on market capitalisation |

| Composition | · Members of Board of Directors

· Senior executives of listed entity · 2/3rds IDs in case of SR Equity Shares |

· Minimum 3 members

· Majority being members of board of directors · Atleast 1 Independent Director (ID) · 2/3rds IDs in case of SR Equity Shares |

| Minimum no. of meetings | One | Two |

| Quorum | Not specified | · 2 or 1/3rds of total members of RMC, whichever is higher

· Including atleast 1 member of Board |

| Maximum gap between two meetings | Not specified | Not more than 180 days gap between two consecutive meetings |

| Roles and responsibilities | The board of directors were to define the role and responsibility and delegate monitoring and reviewing of the risk management plan and such other functions, including cyber security. | As provided under Part D of Schedule II, that inter alia includes:

· Formulating of risk management policy; · Oversee implementation of the same; · Monitor and evaluate risks basis appropriate methodology, processes and systems. · Appointment, removal and terms of remuneration of CRO. |

| Power to seek Information | No such power. The same was only available with Audit Committee under Reg. 18 (2) (c). | RMC has powers to seek information from any employee, obtain outside legal or other professional advice and secure attendance of outsiders with relevant expertise, if it considers necessary. |

The roles and responsibilities of the RMC has now been specified in the Regulations itself, which were once left at the discretion of Board. The formulation of Risk Management Policy has also been delegated to the RMC, with particular contents of the policy being specified under the Schedule.

An important role of the RMC, among others, include review of the appointment, removal and terms of remuneration of Chief Risk Officer (CRO). The appointment of CRO is not a mandatory requirement under Listing Regulations. CRO is required to be appointed for all banking companies, and non-banking financial companies (NBFCs) having asset size of Rs. 50 billions or more, being registered as an Investment and Credit company, Infrastructure Finance Companies, Micro Finance Institutions, Factors, or Infrastructure Debt Funds. Further, the Insurance Regulatory and Development Authority of India (IRDAI) Corporate Governance Guidelines requires the insurance companies to appoint CRO.

The role of RMC further provides for co-ordination with other committees where the roles overlap. It is seen that the risk management function is also laid upon the Audit Committee. Therefore, the roles of both the committees might be overlapping. In view of the same, some companies choose to constitute one joint committee combining the roles of both Audit Committee and RMC. From the provisions providing for co-ordination of activities, it may also be taken as a clear indication that the committees cannot be merged into one, but co-ordinate where the activities require so.

Actionables –

- Changes in the constitution of RMC / Constitution of RMC in case of first-time applicability;

- Modification of the Risk Management Policy as per the Amendment Regulations;

- Amending the existing charter of the Committee to align with the amendments.

While the Amendment Regulations are effective immediately, the changes cannot take place overnight. Therefore, it is advisable that the listed entities shall take the matter of constitution/ re-constitution of RMC in the ensuing Board Meeting. The modification of Risk Management Policy will be then taken up by the RMC and can be done within a reasonable period of time.

What should be this period? A probable answer to this should lie in the proviso to clause (a) of Reg. 15 that permits a timeline of six months from the applicability to comply with corporate governance requirements as stipulated under regulations 17 to 27, clauses (b) to (i) and (t) of sub-regulation (2) of regulation 46 and para C, D and E of Schedule V. However, that is applicable only in case of companies covered in Reg. 15 (2) (a). Therefore, the time available is till June 30, 2021 as thereafter, the companies will be required to confirm on RMC composition in the quarterly filings done under Reg. 27.

3. Overriding powers of LODR Regulations

Earlier, proviso to Regulation 15(2)(b) provided a clear stipulation of overriding effect of specific statute in case of conflicting provisions. The Amendment Regulations provides for deletion of the said proviso effective from September 1, 2021. No rationale seems to have been provided in the agenda[1] put up before SEBI at the board meeting for this major amendment.

Regulators viz. RBI, IRDA, PFRDA at times have specific corporate governance related compliances that are stricter and at times conflicting with the requirements of Listing Regulations. For eg. With respect to composition of Audit Committee for a public sector bank, RBI Circular of September, 1995 provides for following composition in case of public sector banks: (a) Executive Director of the Bank (Wholetime director in case of SBI) (b) two official directors (i.e. nominees of Government and RBI) and (c) Two non-official, non-executive directors (at least one of them should be a Chartered Accountant). Directors from staff will not be included in ACB. This is certainly conflicting with the composition provided in Reg. 18 of Listing Regulations.

Subsequent to September 1, 2021 these entities will be regarded as non-compliant of the provisions of Listing Regulations and may be subject to penalty in terms of SEBI Circular dated January, 2020.

4. Reclassification of promoters into public – related exemptions and procedural changes

Regulation 31A of the LODR Regulations specifies the conditions and approvals post which the promoters can be re-classified into public shareholders. SEBI had proposed changes to the same in a consultation paper dated 23rd November, 2020. The consultation paper was critically analysed in our article. Amendments have been made on similar lines in Regulation 31A.

5. Alignment with the provisions of the Companies Act, 2013

Certain amendments have been made to remove the gap between the provisions of LODR Regulations, with that of the Companies Act, 2013 as given below –

- Separate meeting of independent directors – The requirement of conducting a separate meeting of the independent directors without the presence of any other member of the Board of the company is required under both the Companies Act, 2013 as well as the LODR Regulations. However, whereas the Companies Act requires one meeting in a financial year, the LODR Regulations required one meeting in a year (calendar year). Therefore, the same has been substituted with a “financial year” so as to align the requirements of both the governing laws.

- Display of Annual Return on website – Section 92 read with allied rules requires the companies, having a website, to display its Annual Return on the website. New clause has been inserted under Regulation 46 of LODR Regulations that requires placing the Annual Return on the website of the company.

- Changes in requirements pertaining to placing of financial statements on website – The audited financial statements of each of the subsidiaries was required to be placed on the website prior to the Amendment Regulations. New provisos has been inserted under the same so as to avoid preparation of separate financial statements of the subsidiary company, where the requirements under the Companies Act, 2013 are met if the consolidated financial statements are placed instead of separate ones.

6. Mandatory website disclosures

Regulation 46 of the LODR Regulations provides the mandatory contents to be placed on the website of a listed entity. Most of the disclosures were already existing under respective regulations viz. Reg 30, 43A etc. However, the same has been consolidated under regulation 46. This will now enable stock exchanges to levy penalty in terms of SEBI circular dated 22nd January, 2020.

7. Analyst meet

The listed entity is required to disclose the schedule of analyst or institutional investor meet and the presentations made to them on its website under regulation 46 and on the website of the stock exchange under Schedule III. The Amendment Regulations have explained the term ‘meet’ to mean the group meetings and calls, whether digitally or by physical means. The Amendment Regulations will require the listed entity to upload the audio/ video recordings and the transcripts within the prescribed timeframe. The same is in line with SEBI’s Report on disclosures pertaining to analyst meets, investor meets and conference calls. However, the amendment does not cover disclosure of one-to-one investor/ analyst meet conducted with select investors recommended in the said Report.

8. Consolidation of various SEBI circulars

Certain circulars of SEBI lay down various requirements to be complied with in relation to the LODR Regulations. The Amendment Regulations have consolidated the requirements under the principal LODR Regulations.

- Requirement of Secretarial Compliance Report – While the requirement of Annual Secretarial Compliance report were applicable on the listed entities and its material subsidiaries since a few years back, the same has now been specifically provided under newly inserted sub-regulation (2) of Regulation 24A. Earlier, the practice came pursuant to a SEBI circular.

- Timeline for report of monitoring agency regarding deviation in use of proceeds – Pursuant to the requirements of Regulation 32 of the LODR Regulations, the monitoring agency is required to give a report on the utilisation of proceeds of issue on a quarterly basis. While timelines were not specified in the LODR Regulations, the report was required to be given within 45 days from the end of the quarter. This timeline was pursuant to the SEBI circular dated 24th December, 2019 . Now, with the Amendment regulations, the same is specified under regulation 32(6) of the LODR Regulations.

- Requirement of Business responsibility and sustainability report (BRSR)- SEBI had proposed a new format to replace the existing Business Responsibility Report. The proposal was finalised and the BRSR format has been made mandatorily applicable from FY 2022-23 onwards, vide SEBI circular dated April, 2021 . The same has also been consolidated under Regulation 34 of the LODR Regulations. A detailed discussion on BRSR is covered in our article.

Conclusion

The Amendment Regulations are very crucial and significant in nature. While on one hand, certain provisions are aligned with the Companies Act, 2013, whereas on the other hand, overriding powers have been given to LODR Regulations which will require the listed entities formed under special statute to comply with the LODR Regulations in entirety. Uniformity in timelines and relaxation in certain disclosure requirements will encourage ease of doing business, and the coverage of certain provisions extended to listed entities based on market capitalisation will have a remarkable impact on the corporate governance of listed entities.

[1] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/meetingfiles/apr-2021/1619067328922_1.pdf#page=18&zoom=page-width,-17,763

Our other materials on the relevant topic can be read here –

- http://vinodkothari.com/2021/06/presentation-on-lodr-amendments/

- http://vinodkothari.com/2020/09/companies-amendment-act-2020/

- http://vinodkothari.com/2019/07/sebi-amends-lodr-in-relation-to-equity-shares-with-superior-rights/

- http://vinodkothari.com/2019/02/overlap-in-reporting-of-secretarial-compliance/

- http://vinodkothari.com/2018/12/faqs-on-sebi-listing-obligations-and-disclosure-requirements-amendment-regulations-2018/

- http://vinodkothari.com/2016/01/sebi-faqs-on-listing-regulations-2015-brings-ambiguity-rather-than-clarity/

Rationalisation of KYC- Measures for relief or technical advancement?

-Kanakprabha Jethani and Anita Baid (finserv@vinodkothari.com)

Background

Considering the resurgence of the Covid-19 pandemic on the economy, the RBI Governor, on May 5, 2021, announced several measures with a view to infuse liquidity in the economy, avoid another wave of borrower defaults[1] as well as aid in ease of business during the lockdown.

Out of the several measures announced by the Governor, one was to simplify the KYC process, which is the initial step of any lending transaction. Some of the amendments seem to provide immediate relief from compliance requirements and some are intended to encourage carrying out KYC compliances electronically, given the social distancing norms.

In this regard, the RBI has issued the following notifications:

- Periodic Updation of KYC – Restrictions on Account Operations for Non-compliance dated May 5, 2021[2]

- Amendment to the Master Direction (MD) on KYC dated May 10, 2021[3]

In this article we intend to discuss the prima facie implications of the amendments introduced by the aforesaid notifications. Read more →

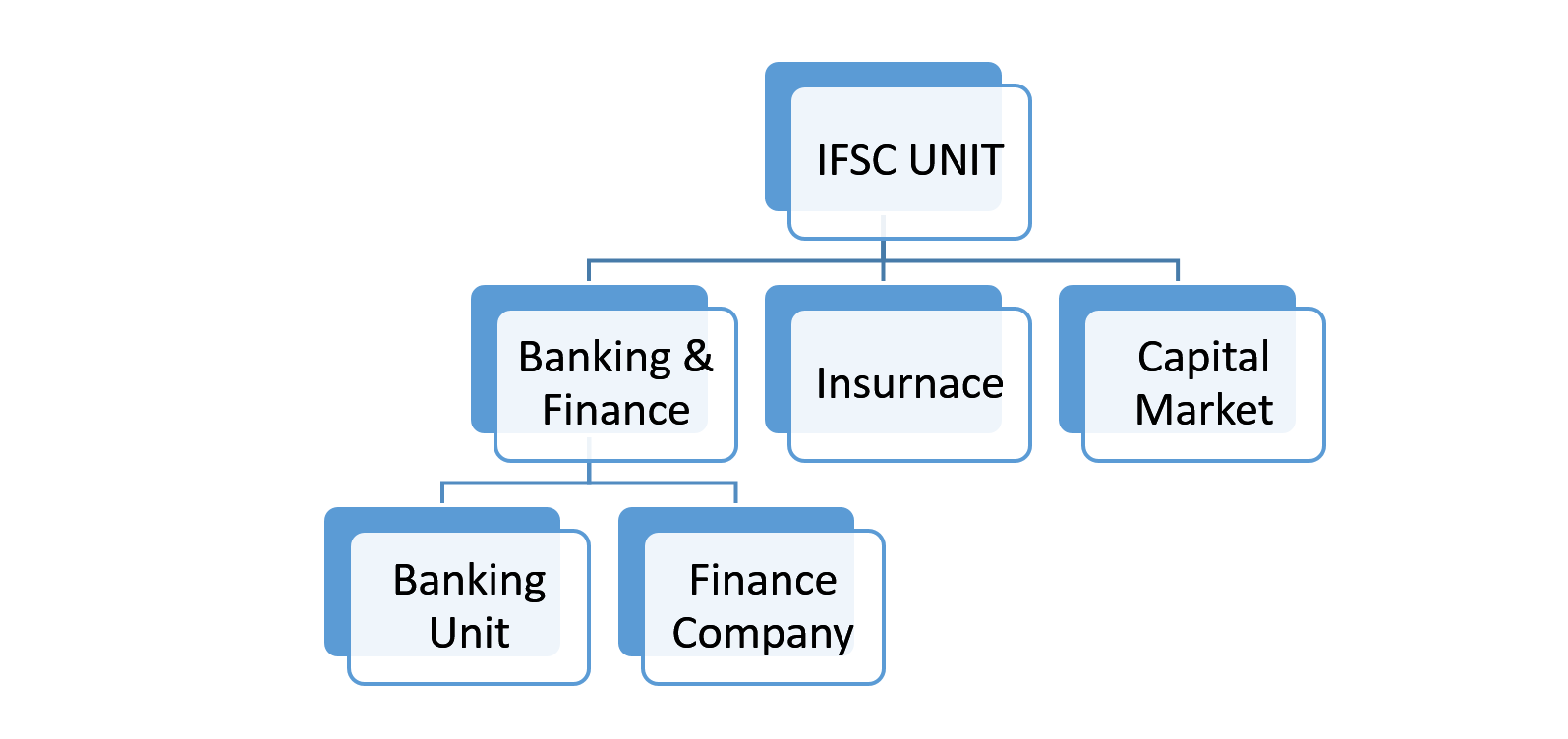

Banking & Finance units in IFSC- A regulatory overview

– Siddarth Goel (finserv@vinodkothari.com)

Introduction- IFSCs

The stage of development of financial markets infrastructure in a country, amongst many other things, is a mirror of sound legal regulations, corporate governance, judicial certainty, and debtor protection regime within the country. The inflow of global capital is quintessential for financial markets development and allocation of adequate capital resources in growth sectors. In a move to make India a hub for global capital flow, Gujarat International Finance Tech-City (GIFT) has been established as a globally benchmarked International Financial Service Centre (GIFT-IFSC). GIFT-IFSC is India’s first dominant gateway for global capital flows in and out of the country. The GIFT IFSC supports a gamut of financial services inter alia, banking, insurance, asset management, and other financial market activities. Prior to dealing with the regulatory framework governing financial units established in GIFT-IFSC, it is important to understand the broad function of an IFSC.

IFSCs are the Offshore Financial Centers (OFCs) that cater to customers outside their own jurisdiction. IMF defines OFCs as any financial center where the offshore activity takes place. However, this does not limit financial institutions in OFCs from undertaking domestic transactions. Therefore practical definition propounded by IMF is;

“OFC is a center where the bulk of financial sector activity is offshore on both sides of the balance sheet, (that is the counterparties of the majority of financial institutions liabilities and assets are non-residents), where the transactions are initiated elsewhere, and where the majority of the institutions involved are controlled by non-residents.”

Units set up in GIFT-IFSC can broadly be categorised on the basis of business activity intended to being undertaken by the entity.

This write-up covers regulations governing banking and financial services undertaken by Banking Units and Finance Companies set up in IFSC. The first part touches upon the benefits of setting up a unit in IFSC. The second part covers Banking Units and permitted financial activities. The third part covers Financial Companies in IFSC along with permissible activities and capital requirements. The fourth part covers financial service transactions to and fro between a financial unit based in IFSC and domestic tariff area (DTA). The last part deals with the applicable KYC/PMLA compliances and the currency of transactions with units based in IFSC.