The Ministry of Corporate Affairs (‘MCA’) in the year 2018, introduced the provision for declaration by individuals identified as Significant Beneficial Owners (‘SBOs’) for companies under section 90 of the Companies Act, 2013 (‘Act’). Subsequently, MCA extended the ambit of the said provisions to Limited Liability Partnerships (LLPs) through notification dated February 11, 2022. However, the notification prompted concerns and queries regarding the implementation of SBO provisions on LLPs. These concerns have been addressed by the recent notification dated November 9, 2023 (‘LLP SBO Rules’). The rationale behind this extension is to align the framework for identification of SBO’s of LLPs with that of companies.

While the provisions are on similar lines as that brought for companies under the Act, however, the difference is mostly in terms of the manner of determining the SBOs in case of LLPs. In case of LLPs it is calculated based on holding of capital contribution (shares in case of companies), voting rights in respect of management or policy decisions of LLP (shares in case of companies) and right to receive or participate in distributable profits (dividend in case of companies) or any other distribution besides, the right to exercise control or significantly influence in any manner other than direct holdings.

The article explains the requirements of the LLP SBO Rules, obligations of the LLPs, and the actionables to be taken in order to comply with the requirements.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-11-20 12:03:462023-11-23 11:27:06SBOs behind LLPs all set to be surfaced

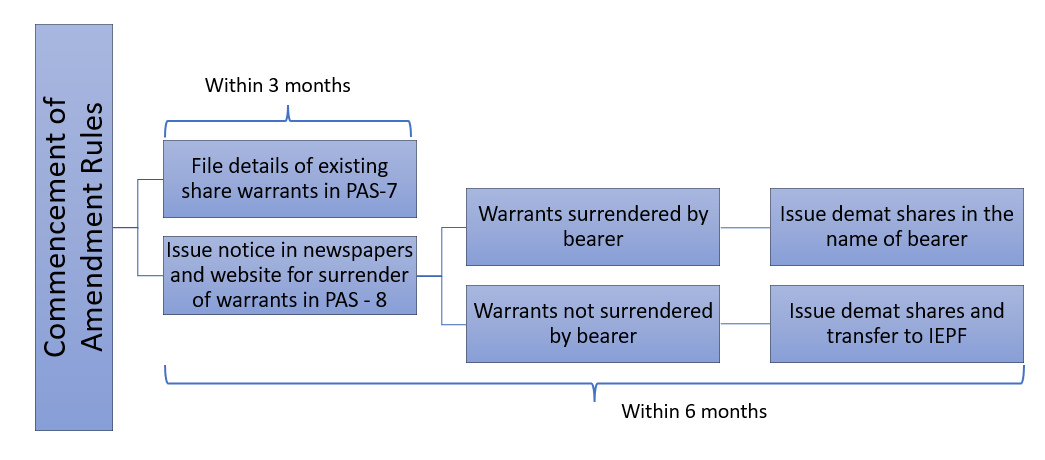

Share warrants are one of the widely used means to raise funds, particularly, in case of start-ups. MCA has recently notified the Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2023 (“Amendment Rules”) vide which Rule 9 has been amended to require mandatory conversion of the existing share warrants issued by public companies under the erstwhile Companies Act, 1956 (“Erstwhile Act”) into dematerialised form of securities.

Following this amendment, a significant question comes up to be addressed is whether public companies will not be allowed to issue share warrants altogether? We attempt to decode the implications of the present amendment in this write up.

Actionables under the present amendment

The newly inserted sub-rule (2) and (3) to Rule 9 of the PAS Rules requires every unlisted company to –

File the details of existing share warrants with the ROC in form PAS-7 within 3 months from the commencement of the Amendment Rules, i.e., by 27th January 2024,

Require bearers of the share warrants to surrender the same and issue dematerialised shares in the name of such bearer within 6 months from the commencement of the Amendment Rules, i.e., by 27th April, 2024, and

Convert the unsurrendered share warrants into demat shares and transfer the same to IEPF

The company shall be required to issue notice for the bearers of share warrants in form PAS-8 on its website as well as two newspapers – in vernacular language, having wide circulation in the district and in English language having wide circulation in the state in which the registered office of the company is situated.

Share warrants covered under the present amendment

In the context of the newly inserted sub-rule (2) of Rule 9, the term share warrants is to be interpreted in a much restricted sense. The provision refers to “share warrants prior to commencement of the Companies Act, 2013 and not converted into shares”, which implies share warrants issued under the Erstwhile Act only. In this regard, one may refer to section 114 of the Erstwhile Act that allowed public companies to issue “bearer warrants” entitling the bearer of such warrants to the shares specified therein. The same was referred to as “share warrants” under the said Act, and the shares contained therein can be transferred through mere delivery of the warrant.

The present amendment requires mandatory surrender of such “share warrants” in the form of “bearer warrants” against issuance of shares in dematerialised form.

Permissibility for issuance of share warrants under the Companies Act, 2013 (“Act”)?

As mentioned above, the “share warrants” referred to under the Amendment Rules are limited to the bearer warrants issued in accordance with the Erstwhile Act, and do not extend to all share warrants which companies issue under the various provisions of law.

In general context, share warrants are actually written options to subscribe to the shares of a company on pre-agreed terms at a future date. Such warrants are fairly common in the corporate world on account of the benefits associated with the same, and the present amendment cannot be said to rule out the possibility of issuance of such share warrants. Share warrants are directly or indirectly recognised under various provisions of law, for instance:

The definition of “securities” as provided for in section 2(h) of the Securities Contracts (Regulation) Act also includes “rights or interest in securities”. Share warrants are, in fact, a right to acquire securities at a future date, and therefore, well covered under the definition of securities

The SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 contains specific provisions with respect to issuance of share warrants.

The Foreign Exchange Management (Non Debt Instruments) Rules, 2019 also refers to the term “share warrants” within the overall definition of “equity instruments” and contains specific provisions with respect to the same.

The Act refers to the conversion of “warrants” as a permissible mode for issuance of shares during the restricted period post buyback u/s 68(8) of the Act. It also contains references to employee “stock options”, which, by nature are equivalent to share warrants.

While the Act does not mention at several places under it about share warrants, however, at few places, like the provisions under section 68 dealing with buy back of securities as well as reference to employee “stock options”, which, by nature are equivalent to share warrants are given the Act.

Therefore, there are no explicit provisions that prohibit the issuance of share warrants by unlisted companies, and the same, being a “security” can very well be issued by a company, whether listed or unlisted, in compliance with the applicable provisions of law to meet the required funding as well as investment objectives.

Concluding remarks

The Amendment Rules aim at the wiping out of the bearer share warrants, since the legal and beneficial ownership of the shares are non-traceable in such a case. However, that does not eliminate the concept of share warrants as a whole, that are issued to an identified set of persons, and follows a due procedure laid down in the law for transfer of such warrants. Although not expressly defined under the Act, the concept of share warrants is legally recognised under various laws and are being widely issued by Indian companies, whether listed or unlisted, including private companies. The current set of amendments will have no impact on the permissibility of issuing share warrants issued under the Act and other laws as mentioned hereinabove.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-10-28 23:55:412023-11-09 12:26:45Share warrants under cloud - are companies not allowed to issue share warrants?

The Insolvency and Bankruptcy (Amendment) Ordinance, 2021 (‘Ordinance’)[1] was promulgated on 5th April, 2021 to bring into force the prepackaged insolvency resolution framework for Micro, Small, Medium Enterprises (MSMEs). While the Ordinance put forth the structure of the prepack regime, a great deal was dependent upon the relevant rules and regulations. On 9th April, 2021, the Insolvency and Bankruptcy (Pre-packaged Insolvency Resolution Process) Regulations, 2021 (“Regulations”)[2] as well as the Insolvency and Bankruptcy (Pre-Packaged Insolvency Resolution Process) Rules, 2021 (“Rules”)[3] have been notified with immediate effect.

As one delves into the whole scheme of things, including the complicated provisions of the Ordinance and the even complication regulations, one gets to feel that the prepack framework will act only as a consolation for the MSMEs – while efforts aimed to increase the efficacy of insolvency resolution, the proposed Framework seems to do a little towards this end. In the author’s humble opinion, key elements of prepacks – cost and time efficiency and a Debtor-in-Possession approach, have been diluted amidst the micromanaged Rules and Regulations. In this article, we discuss how[4].

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kothari Consultantshttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari Consultants2021-04-15 22:15:362021-04-15 22:20:20Prepack for MSMEs – A Vaccine that doesn’t Work?