As a part of the governor’s statement dated October 1, 2025, it was highlighted that banks and NBFCs continue to exhibit financial stability, by way of strong liquidity positions, capital adequacy, and sustained profitability. Further, NBFCs have shown improvement with better asset quality and declining GNPA ratios. Against this backdrop, the RBI has maintained a cautious yet forward-looking stance, keeping policy rates unchanged while focusing on strengthening financial stability, enhancing risk management, and reinforcing consumer protection through regulatory measures affecting banks and NBFCs. Some of thedevelopmental and regulatory policy measures introduced by the RBI, which are expected to impact financial entities such as banks and NBFCs, have been discussed below:

Key Highlights:

Particular

Change and Impact

Expected Credit Loss (ECL) Framework

Applicability: Banks Impact/Change: RBI plans to implement an ECL-based provisioning framework for banks, effective from April 2027.Under this framework, banks will be required to make provisions upfront for potential losses based on expected credit deterioration, in alignment with that being followed by NBFCs under IndAS.The ECL approach is intended to strengthen credit risk management and promote more forward-looking provisioning practices.You can read our analysis on the same here.

Basel III Guidelines – Standardised Approach

Applicability: Scheduled Commercial Bank, excluding Small Finance Banks, Payments Banks, and Regional Rural Banks Impact/Change: RBI has proposed draft guidelines on the Revised Basel Framework – Standardised Approach for Credit Risk. Accordingly, the approach for arriving at risk weight for computation of capital ratios will be revisited. While guidelines are awaited, IIRB approach may be introduced for Indian Banks, in line with global practices. Guidelines are awaited.

Risk-Based Premium Framework for Deposit Insurance

Applicability: All Commercial Banks, All State, Central and Primary Cooperative Banks Impact/Change: At present, the Deposit Insurance and Credit Guarantee Corporation (DICGC) operates the deposit insurance scheme where each depositor in a bank is insured up to a maximum of ₹5,00,000. Currently, DIGC levies a uniform flat premium of 12 paise per ₹100 of deposits from all banks, irrespective of the financial strength of the bank. The RBI has now proposed a shift to a Risk-Based Premium Framework, which would reduce the premium payable by banks that are financially sound. Guidelines are awaited.

Risk Weights on Infrastructure Lending by NBFCs

Applicability: NBFCs engaged in project finance, HFCs with LAP exposure, and banks with large infrastructure portfolios Impact/Change: “Infrastructure lending” (as per para 5.1.14, SBR Master Directions) refers to credit extended by way of term loans, project loans, or investment in bonds/debentures/preference/equity shares of a project company, where the subscription is treated as an advance or other long-term funded facility in the sub-sectors as may be notified by the Ministry of Finance. Under SBR, provisioning norms did not differentiate between construction and operational phases, overlooking the higher risks during construction. The Project Finance Directions, 2025 addressed this by mandating higher provisioning for under-construction projects. Presently, NBFCs can apply lower risk weights to operational PPP projects (50% for operating vs. 100% for construction). RBI now proposes a principle-based framework to better align risk weights with the actual risk profile of operational projects. Guidelines are awaited.

Review of the External Commercial Borrowing Framework

Applicability: Entities intending to avail an External Commercial Borrowing. Impact/Change: RBI has proposed a review of the External Commercial Borrowing (ECB) framework to rationalise and simplify existing regulations. The proposed changes include Expanding eligible borrower and lender categories, Relaxing borrowing limits and maturity restrictions, Removing cost ceilings, Revising end-use conditions, Simplifying reporting requirements. Draft regulations are yet to be issued for the same.

Strengthening the Internal Ombudsman (IO) Mechanism

Applicability: NBFCs-NDs with an asset size of ₹5000 crore and above, and having public customer interface; Deposit-taking NBFCs with 10 or more branches. Impact/Change: The RBI intends to enhance the effectiveness of the IO framework introduced for the REs in 2018 (revised direction was introduced in 2023). As per the extant regulatory requirements, the IO serves as an independent authority within the applicable REs to review complaints that are rejected by the REs. The proposed revisions seek to strengthen this mechanism by: Empowering IOs with compensation powers and granting them the ability to directly interact with complainants, thereby aligning their role more closely with that of the RBI Ombudsman. Introducing a two-tier grievance redress structure within applicable REs, to ensure that complaints are first addressed at multiple levels internally before being escalated to the IO. The draft of the revised master direction on the internal ombudsman is yet to be released, which will then be open for wider analysis of the changes and their implication.

Review of Reserve Bank – Integrated Ombudsman Scheme, 2012

Applicability: The Scheme applies to services rendered by Regulated Entities in India to their customers under the RBI Act, 1934; Banking Regulation Act, 1949; Payment and Settlement Systems Act, 2007; and the Credit Information Companies (Regulation) Act, 2005. Impact/Change: The RBI has conducted a comprehensive review of the RBI – Integrated Ombudsman Scheme, and will be releasing the draft of the revised Scheme for stakeholder feedback. The revision of the scheme is related to the following: To extend its applicability to State Co-operative Banks and District Central Cooperative Banks (previously under NABARD), thereby the customers of these rural co-operative banks can now approach the RBI Ombudsman for complaints related to banking services instead of NABARD. To enhance clarity, simplify procedures and reduce timelines to ensure more effective handling of complaints. Considering the publications, there is expectation of cross reporting between RBI Ombudsman and Internal Ombudsman.

Consolidation of Regulatory Instructions

RBI is streamlining and consolidating its regulatory instructions into Master Directions for easier access and compliance. Around 250 draft Master Directions, covering 30 regulatory areas across 11 types of regulated entities, will be published on the RBI website, and stakeholders will be given an opportunity to review them and give feedback on their completeness and accuracy.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Finservhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Finserv2025-10-01 18:27:512025-10-03 18:50:58RBI Monetary Policy Update: Enhancing Financial Stability for Banks and NBFCs

Project loans, used to finance large infrastructure and industrial ventures like highways, power plants and railways etc., are fundamentally different from regular business or personal loans. Unlike typical loans that are repaid from either the borrower’s existing operations and balance sheet (in case of the former) or the borrower’s own credit worthiness (in case of the latter), project loans are forward-looking: they primarily rely on cash flows of the project, generated onlyafterthe project becomes operational. Because of this, delays in project completion due to various factors such as land acquisition issues and regulatory delays which may be beyond the control of the developer are common. These may arise from. Such delays, though being routine and not necessarily indicating borrower’s stress, triggered adverse asset classifications under the existing rules.

When the RBI introduced its 2019 prudential framework to enable early recognition and time bound resolution of stressed assets, it excluded such project loans from its scope (see para 25). As a result, these continued to be governed by old norms, specifically para 4.2.5 of the 2015 IRCAP and later, para 3 of Annex III under the RBI SBR Directions. However, these norms did not reflect the unique risks faced by project finance especially during the construction phase.

To address these issues, the RBI released the Draft Project Finance Directions in May 2024, proposing a dedicated regulatory framework tailored to project loans. The Project Finance Directions(‘Directions’) have been issued on 19 June, 2025. This article explores the need for such a framework, the changes brought in the regulatory regime, and their impact on borrowers and lenders.

Project finance vs other kinds of finance

In corporate lending, credit decisions are primarily based on the borrower’s balance sheet strength, existing cash flows and overall financial health. where the lender primarily assumes credit risk

In contrast, in project finance, repayments as well as the primary security depend primarily on the successful implementation and projected cash flows of a specific project, rather than the borrower’s overall financial position. Accordingly, the lender takes two different risks:

Project riski.e. the risk that the project may face commencement delays due to factors like regulatory bottlenecks, land acquisition issues or construction delays and;

Credit riski.e. the risk of inadequacy of cashflows to make the scheduled contractual payouts.

Importantly, in project finance, delays in cashflows often happen due to non-credit factors linked to project execution, mainly project delays. As a result, automatic downgrading of classification due to any project delay may not only fail to provide a true risk profile of the loan but also cause increased provisioning burden on the lender.

Overview of the Directions

The Directions deal with the following broad aspects:

Classification of projects and project finance;

Prudential requirements for extending project loans including:

Provisioning requirements;

Conditions for sanction, disbursement and monitoring.

Resolution and restructuring of project loans

Either due to stress;

Extension/ delays in DCCO.

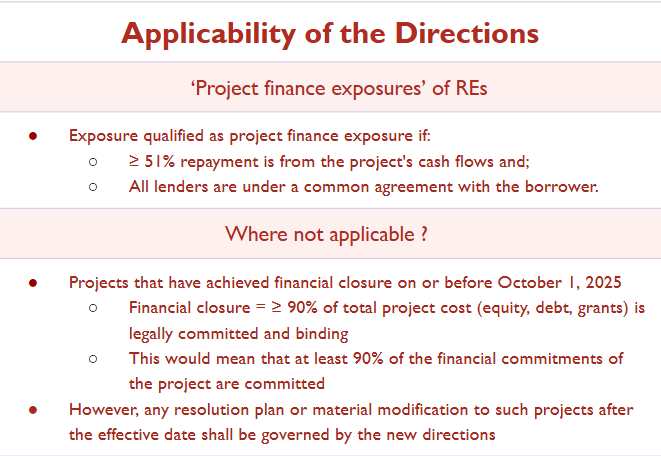

Applicability

Classification of ‘project’ and ‘project finance’

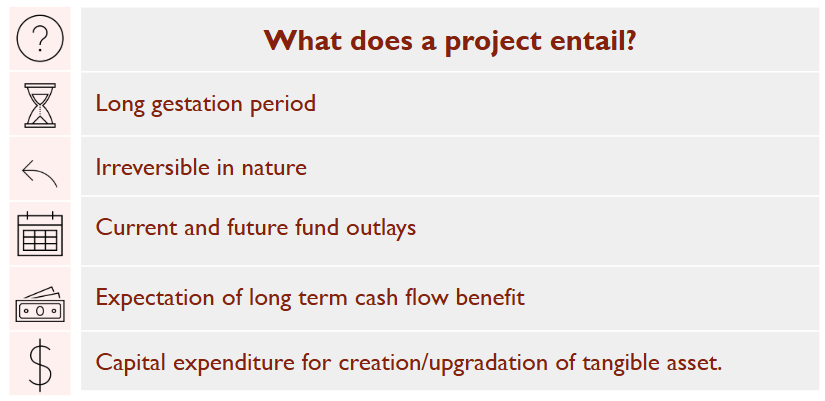

Under the Directions, a project is defined as to involve capital expenditure for the creation, expansion or upgradation of tangible assets or facilities, with the expectation of long-term cash flow benefits [see para 9(l)], with the following features:

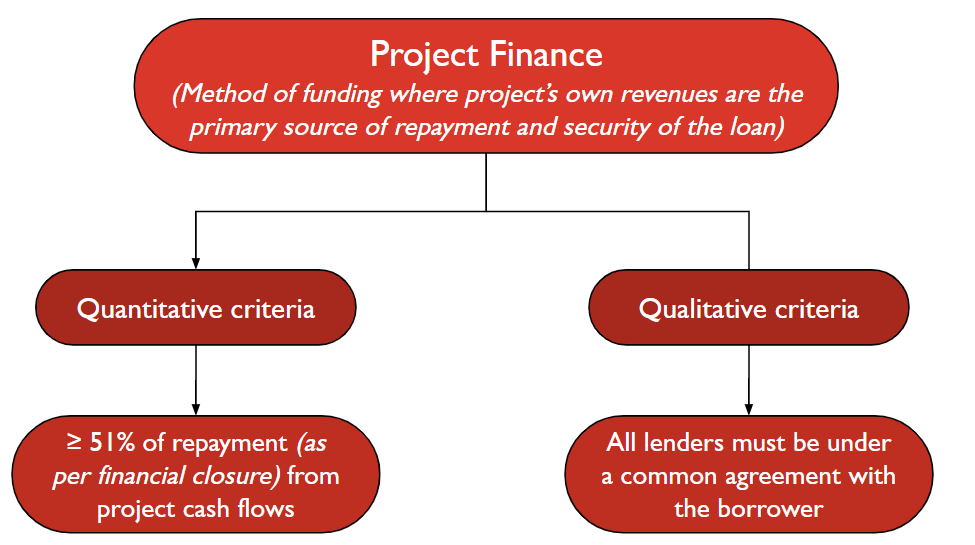

Project finance is a method of funding where the project’s cash flows/ revenue own revenues are the primary source of repayment as well as the and security for the loan [see para 9(m)].

It can be:

Greenfield (new project);

Brownfield (existing project enhancement).

To qualify as project finance under the Directions:

Note: Loan terms can differ across lenders if agreed by all parties

The earlier definition of project finance under the SBR Directions was generic and vague, referring merely to a “project loan” as any term loan extended for setting up an economic venture. The Directions have provided more clarity on what would be considered as project finance and have linked it to the definition of project finance under the Basel Framework, while also providing a quantitative threshold of 51%.

Project finance envisages the lender’s exposure in a project, which is typically in the process of being set up. The repayment will be from the project cashflow i.e. the payout structure is connected with the commencement of commercial operations of the project. The lending is based on the projected cash flows of the project rather than the balance sheet of the developer. It is distinct from asset finance, where loans are backed by existing assets generating income. Further, project finance differs from a working capital loan/general corporate purpose loan where the latter is towards financing the working capital needs of the developer entity based on the overall health of the entity.

Would it mean that project loans cannot have any other collateral and must solely rely on the project as the security? The answer is negative since the threshold specified allows to have other/ additional collateral, say, personal guarantee of the developer etc., however, the primary security shall be the project cashflows.

Other important terminology

DCCO

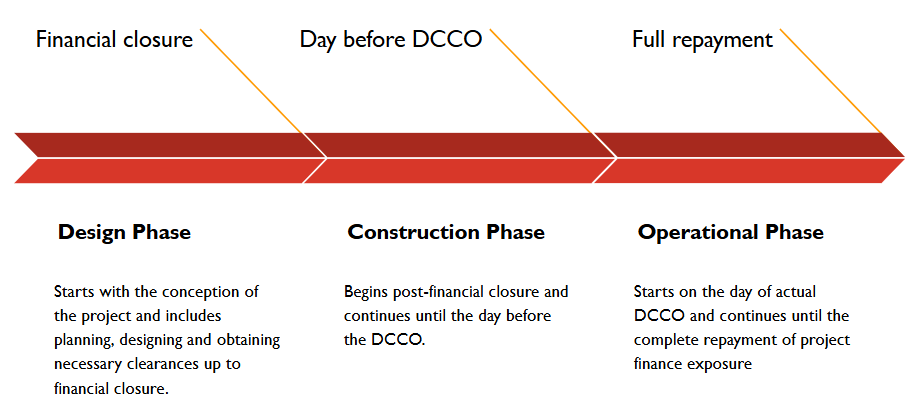

The Date of Commencement of Commercial Operations (DCCO) is a key milestone in project finance, marking the transition from construction to operational phase when a project begins to generate revenue.The Directions recognises three forms of DCCO. [see Para 9(e) to (m)]

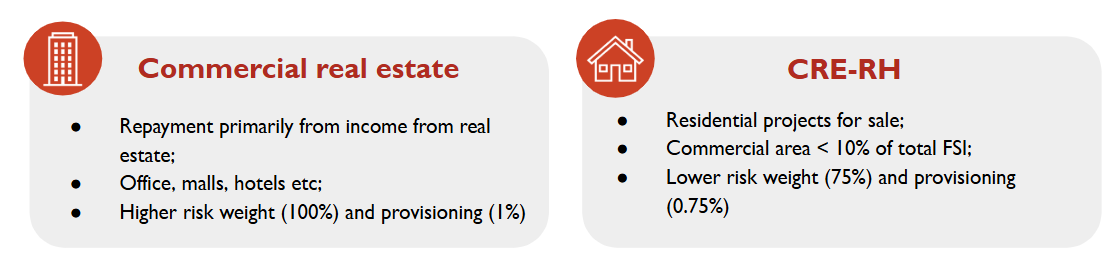

CRE and its sub-category CRE-RH

Defined in Directions on Classification of Exposures as Commercial Real Estate Exposures, CRE refers to loans or exposures where repayment primarily depends on income generated by the real estate asset itself. This typically includes office spaces, malls, warehouses, hotels and multi-family housing complexes that are leased or sold in the open market. Since CRE is a sub-head of project finance, it also follows similar characteritics of project finance i.e.both repayment of the loan and recovery in case of default are closely tied to the cash flows from the real estate asset such as rental income or sale proceeds. [see para 9(b)]. The definition is aligned with the definiton of income-producing real estate (IPRE) under Basel norms. Our article discussing CRE can be assessed here. https://vinodkothari.com/2023/04/commercial-real-estate-lending-risks-and-regulatory-focus/

Commercial Real Estate – Residential Housing (CRE-RH) [see para 9(c)]

Since residential housing projects generally pose lesser risk and volatility compared to commercial properties, the RBI created a distinct sub-category within CRE called CRE-RH vide notification dated June 21, 2013. CRE-RH includes loans given to builders or developers for residential housing projects meant for sale.To classify as CRE-RH, the project must be predominantly residential and commercial components like shops or schools should not exceed 10% of the total built-up area (FSI). If the commercial area crosses this 10% threshold, the entire project will be CRE. This distinction isn’t just semantic, it has regulatory benefits. Since CRE-RH are subject to lower risk due to various reasons such as diversified cash flows and lower dependency on a single occpnt, RBI has assigned lower capital risk weights i.e. 75% to CRE-RH compared to standard CRE 100% and lower provisioning provisioning requirements (0.75% vs. 1%).

Prudential requirements

Provisioning requirements

In the context of project finance, where risks vary across different phases of a project’s lifecycle, a one-size-fits-all provisioning approach throughout the project life may not be relevant. .

Under the SBR, provisioning norms made no distinction between the construction and operational phases of a project. A uniform provisioning rate was applied i.e. 0.75% for CRE-RH and 1% for CRE while other loans were provisioned at 0.4% irrespective of whether the project was just starting construction or had already begun generating revenue. This approach, while simple, failed to reflect the heightened risks associated during the construction phase , such as delays, cost overruns, or regulatory hurdles.

To address this gap, the Draft Directions, proposed a conservative approach calling for a 5% provision during the construction phase and 2.5% during the operational phase, with the operational rate reducible to 1% if following conditions were met:

the project demonstrated positive net operating cash flows sufficient to service all current repayment obligations, and

there was a minimum 20% reduction in long-term debt from the level outstanding at the time of achieving DCCO.

These draft norms were considered overly harsh, particularly for long-gestation infrastructure projects where cash flows stabilise gradually.

Taking stakeholder feedback into account, the Directions adopted a more balanced g structure as follows:

Project type

Construction Phase

Operational phase – after commencement of repayment interest and principle

Commercial real estate (CRE)

1.25%

1%

CRE – Residential Housing

1%

0.75%

Other projects

1%

0.40%

DCCO deferred projects:

Additional provisioning to be maintained depending on the type of project:0.375% per quarter for infra projects0.5625% per quarter for non-infra projects

NPA project finance accounts

As per extant instructions

Provisionig for existing projects

Continued to be governed by extant norms;If resolution is done for any fresh credit event or change in terms occur after the effective date of these directions, then provisioning as per these Directions

RBI’s draft proposal for lower risk-weights for high quality infrastructure projects

The RBI has issued a draft amendment to the Scale Based Regulations, 2023 on 27th October, 2025, proposing a lower risk weight framework for ‘High-Quality Infrastructure Projects’. Once finalised, the provisions would be applicable from April 1, 2026, or from an earlier date when adopted by an NBFC in entirety. The intent of the amendment is to recognise and incentivise lending to stable, well-performing infrastructure projects by prescribing reduced risk weights for such exposures. Under the draft, “High-Quality Infrastructure Projects” are defined as infrastructure projects meeting all of the following conditions:

The project has completed at least one year of satisfactory operations post achievement of the actual DCCO;

The exposure is classified as ‘standard’ in the books of the lender;

The obligor’s revenue depend on one main primary counterparty, which shall be the Central Government or a Public Sector Entity, and the contractual terms ensure certainty of payment, such as through availability-based1 or take-or-pay arrangements2;

The contractual provisions offer strong creditor protection such as escrow of cash flows, legal first charge on project assets and other appropriate safeguards in case of early termination;

The obligor has adequate internal or external funding arrangements to meet current and future working capital or other funding needs, as assessed by the lender;

The obligor is restricted from undertaking actions detrimental to creditors, such as raising additional debt secured by the project’s cash flows or assets without lender’s consent.

Projects meeting all of the above criteria will qualify as high-quality infrastructure assets and will attract lower risk weights, as follows:

50%, where the obligor has repaid at least 10% of the sanctioned amount;

75%, where the obligor has repaid at least 5% but less than 10% of the sanctioned amount.

If a project subsequently fails to meet any of the qualifying conditions, it will cease to be treated as a high-quality asset and will instead attract the standard risk weight of 100% applicable to regular infrastructure exposures.

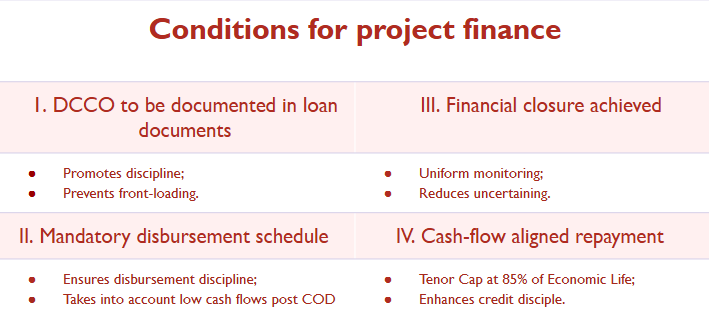

Conditions of project finance

The onus is on the lender to ensure that the following conditions are met before extending any project finance. These conditions will ensure that the facility is structured prudently and is aligned with the implementation as well as cash flows of the project, thereby mitigating both credit as well as project risk. The requirements are more or less similar to the earlier Directions.

Repayment schedule during operational phase is designed to factor initial cash flows

Repayment tenor, including the moratorium period, if any, shall not exceed 85% of the economic life of a project.

This means there is a mandatory 15% tail period i.e. if the project has an economic life of 20 years and the loans are to be repaid in 17 years, the last 3 years are the tail period.Tail period gives comfort to the lender that in case of any default or delay in repayment by the time of maturity, there is still some period left to recover dues from the project cash flows after the scheduled loan maturity.

Would this mean that a borrower cannot obtain a top-up loan after the expiry of 85% of the loan tenure?

The requirement applies to loans with all kinds of tenures, either short or long.

One borrower, multiple lenders

If a project is financed by more than one lender, RBI mandates that the DCCO, whether original, extended or actual, shall be the same across all lenders. This will ensure that:

DCCO is uniform across all lenders

Project progress as well as any delays are uniform across all lenders

Uniform asset classification, preventing any lender from having a different provisioning status.

To ensure balanced risk sharing, the Directions have put consortium lending limits (Para 15): Where projects are under-construction:

Aggregate exposure of all lenders is ≤ ₹1,500 crore: each lender shall hold at least 10% of total exposure;

For projects with exposure > ₹1,500 crore: each lender must hold at least 5% or ₹150 crore, whichever is higher.

These caps essentially require participating lenders to hold sufficient skin in the game and thereby promote responsible credit appraisal as well as avoid risk from being concentrated in a few lenders, especially where other lenders have negligible exposure and hence, less incentive to ensure monitoring.

Inter-lender transfer

These minimum exposure norms will not apply to operational phase projects;

In design or construction phase, lenders are permitted buy/sell exposure only under syndication arrangements as per TLE, and within the exposure limits

In operational phase, exposures can be freely transferred as per TLE norms.

This may be because construction and pre-operational stages are inherently more uncertain and riskier, and therefore, the regulator requires lenders who are willing to remain committed and not exit easily to avoid creating instability.

Project lifecycle – 3 different phases

A project has been divided into 3 phased viz Design, Construction and Operational.

Why does this classification matter?

The regulatory framework treats each phase differently for various risk, compliance and prudential reasons.

Disbursement discipline (Para 21)

Disbursal of funds must be linked to project completion milestones i.e. completion of phases.

Lenders must also track progress in equity infusion and other financing sources as agreed at financial closure

Asset classification (Para 22 & 29)

In design and construction phases, loans can be classified as NPA based on recovery performance, as per IRACP norms.

Once an account is classified as NPA, it can only be upgraded after demonstrating satisfactory performance during the operational phase

Resolution trigger (Para 23)

If any credit event (e.g., default) occurs with any lender during the construction phase, a collective resolution process is triggered

Provisioning norms (Para 32)

Provisioning rates are higher for projects under construction

Once the project enters the operational phase, provisioning reduces, reflecting lower credit risk.

Mandatory requirements before sanctioning a project finance loan: (13)

Achievement of financial closure and documentation of original DCCO;

Project specific disbursement schedule vis a vis stage of completion is included in loan agreement

Post DCCO repayment schedule designed to factor initial cash flows

Prudential conditions related to disbursement and monitoring:

Lender to ensure the following:

Clearances are obtained by the lender:

All requisite approvals/clearances for implementing/constructing the project are obtained before financial closure.(examples: environmental clearance, legal clearance, regulatory clearances, etc.)

Approvals/clearances contingent upon achievement of certain milestones would be deemed to be applicable when such milestones are achieved.

Availability of sufficient (prescribed) minimum land/right of way with the lender before disbursal of funds

This would mean that lender must ensure that the builder executing the project has either:

Ownership of the land (through purchase, lease etc.) or

Legal rights to use/access the land i.e. Right of Way.

For PPP projects, disbursal of funds to occur only after declaration of the appointed date.

Except where non-fund based facilities are mandated by the concessioning authority as a pre-requisite for declaration of the appointed date itself;

Disbursal to be proportionate

To stages of completion of project, infusion of equity or other sources of finance and receipt of clearances

Lender’s Independent Engineer/Architect to certify the stages

Creation and maintenance of a project finance database (see para 37):

Every lender to capture and maintain, on an ongoing basis, project specific information relating to:

Debtor and project profile;

Change in DCCO;

Credit events other than deferment of DCCO;

Specifications of project

Any updation shall be made within 15 days from any change in information;

Necessary systems to be placed within 3 months from the effective date ie by 1st January, 2026

Resolution of Project Loans

Prudential norms for resolution

Lender to monitor performance of project on on-going basis;

Expected to initiate a resolution plan well in advance.

Collective resolution to be initiated by the lenders in case credit event happens with any one lender

In case of any credit event;

Lender to report the same:

to the Central Repository of Information on Large Credit and;

to all other lenders, in case of consortium lending.

Lender to take a review of debtor account within 30 days.

Inter creditor agreement and decision to implement a resolution plan may be done during this period.

Implement the resolution plan within 180 days from the end of the review period.

Resolution plans involving extension of DCCO

Paragraphs 26 to 28 provide a structured framework under which project loans may continue to be classified as ‘standard’ despite delays in project completion, provided specific conditions are met. The objective is to offer flexibility to lenders and borrowers in addressing genuine project delays or cost escalations, without triggering an immediate downgrade to NPA so long as the resolution is timely and prudently implemented.

Permitted DCCO deferment

The DCCO may be deferred, with a corresponding adjustment in the repayment schedule. However, such deferment is subject to the following maximum limits:

Up to 3 years for infrastructure projects

Up to 2 years for non-infrastructure projects (including commercial real estate)

Cost overrun associated with the DCCO deferment:

A cap of 10% of the original project cost, over and above Interest During Construction (IDC)

The overrun must be financed through a Standby Credit Facility sanctioned at the time of financial closure

Post-funding, key financial metrics such as the Debt-Equity ratio and credit rating must remain unchanged or show improvement in favour of the lender

Deferment in DCCO associated with change in scope and size

Rise in project cost (excluding cost overrun) is at least 25% or more of the original project outlay

Reassessment of project viability by the lender before approving the revised scope and DCCO

If the project has an existing credit rating, the new rating must not deteriorate by more than one notch; if unrated and aggregate lender exposure is ₹100 crore or more, the revised project must obtain an investment-grade rating

This benefit of maintaining ‘Standard’ classification due to a change in scope can be availed only once during the project’s life

Resolution plan (‘RP’) deemed successfully implemented only if:

Necessary documentation completed within 180 days from the end of the Review Period and;

Revised capital structure and financing terms are duly reflected in the books of both the lender and the borrower.

Immediate downgrading to NPA if the resolution plan is not implemented within the timeline and conditions above

Once NPA, account can be upgraded only after:

Satisfactory performance post actual DCCO, in case of non-compliance with conditions of resolution plan;

Successful implementation of resolution plan, in case of non-implementation of RP within the specified time.

See a detailed PPT on the Project Finance Directions here

A contractual model where the project earns fixed payments from the counterparty based on the asset’s availability and performance, irrespective of actual usage or demand ↩︎

A contract under which the buyer agrees to pay for a specified quantity of output (e.g., power, gas, water) whether or not it actually takes delivery, ensuring predictable cash flows for the project. ↩︎

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-06-23 16:44:502025-10-28 18:11:30Balancing flexibility and discipline: Analysis of RBI’s Project Finance Directions, 2025