SEBI Informal Guidance Scheme, 2025

– Kunal Gupta | corplaw@vinodkothari.com

– Kunal Gupta | corplaw@vinodkothari.com

SEBI’s IG on RP identification by unlisted subsidiaries

Team Vinod Kothari & Company | corplaw@vinodkothari.com

October 14, 2024

Related Party Transactions (‘RPT’) regime under the Listing Regulations, consequent to substantial amendments made in November, 2021[1], is very wide and includes cross RPTs across the group. That is, transactions of a listed entity with related parties of its subsidiaries; as well as, transactions of a subsidiary (listed or unlisted) with related parties of the parent listed entity would come under the purview of “related party transactions”; and therefore, would be subject to enhanced controls at the parent level.

Therefore, the prerequisite for effective implementation of the RPT controls is the correct identification of the Related Party (‘RP’) at both levels – by the parent and by the subsidiary. While in the case of a listed entity, it is clear that the definition of RP under LODR has to be followed; there was a lack of clarity as to whether an unlisted subsidiary should also follow the same definition or it can simply go by the law as applicable to it.

In this regard, SEBI, in a recent Informal Guidance, has opined that unlisted subsidiaries of the listed entities are required to identify the RPs and RPTs as per the provisions of the LODR Regulations.

Read more: Subsidiaries to refer LODR definition of “related party” – going too far with relationships?Possible alternatives for identifying RPs of subsidiaries

The Listing Regulations under Reg. 2(1)(zb), defines an RP to mean the following:

While the listed entities identified RP based on the above definition, there was a lack of clarity on the manner of RP identification for unlisted subsidiaries in India and overseas. The Listing Regulations do not specify the approach to be followed for identifying RPs of unlisted subsidiaries.

Consequently, there could be two possible approaches – one, the subsidiaries maintain a list of their RPs as per Listing Regulations; alternatively, subsidiaries may be allowed to maintain an RP list as per their respective applicable/local laws[2]. The IG, however, states that the first approach needs to be followed for assessing the RPTs done by the subsidiary with its own RPs.

While the approach of applying an entity-agnostic definition of the Listing Regulations may seem to bring consistency and ease of collation of information across the group; however, there may be several arguments against this approach, as we discuss below.

Issues related to the approach

[Note: As for applicable accounting standards, it very clearly seems to be referring to standards applicable to the entity in question, and therefore, in our view, an entity-agnostic approach does not seem implied there. In the case of overseas entities, “applicable accounting standards” will mean accounting standards as may be applicable to the entity, therefore, entity-specific accounting standards.]

Alternatively, if the subsidiaries identify the RPs based on the definition applicable to it, the same would be more convenient for the subsidiaries as it would anyways maintain the list of RPs to comply with its applicable law.

Concluding remarks

The framework of RPTs requires accurate RP identification to ensure compliance and effective group governance. SEBI’s informal guidance on identifying RPs for unlisted subsidiaries, although provides a view on the approach to identification of related parties by subsidiaries for the purpose of enabling compliances by the listed parent; however, in our humble view, the approach may pose its own set of difficulties as discussed above. On the other hand, a group-wide approach to RPTs which simultaneously respects entity-specific boundaries might be more feasible in terms of ease of interpretation as well as ease of implementation of the law. It is to be noted that the views expressed in the IG are those of the department and do not constitute SEBI’s final decision, as explicitly stated in the IG. Therefore the views expressed in IG should not be seen as the regulators final take on the issue.

In any case, a clear explanation in the Regulations itself might be desired to ensure uniformity in the implementation of RPT controls by listed entities and their unlisted subsidiaries

[1] SEBI (Listing Obligations and Disclosure Requirements) (Sixth Amendment) Regulations, 2021, w.e.f. 1.4.2022

[2] We have discussed both approaches in our write-up, Identification Of Related Parties Of Subsidiaries.

[3] Needless to say that, if the unlisted subsidiary is tracking the RPTs between itself and RPs of its parent listed entity, it will have to the RP list of the parent listed entity prepared in accordance with Listing Regulations.

– HVDLE guided to explain and not comply!

Anushka Vohra | Manager (corplaw@vinodkothari.com)

Recently, SEBI rolled out stricter corporate governance (CG) norms for entities having its non-convertible debt security listed and having an outstanding value of Rs. 500 crore and above as on March 31, 2021 [referred as High Value Debt Listed Entities (HVLDEs)[1]]. One of CG norms applicable is to comply with the requirements that apply with respect to Related Party Transactions (RPTs). The approval requirement, stipulated for material RPTs mandates approval of shareholders and prohibits related parties to vote to approve the transaction. The intent of the law is to ensure approval by shareholders who are not related parties. As HVDLEs include private companies and closely held public companies that must have listed its debentures, this requirement resulted in an impossibility and deadlock. On being approached by one such entity, SEBI suggested a temporary carve out by advising ‘to explain’ and ‘not comply’.

On December 16, 2021, SEBI issued an informal guidance[2] under SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (Listing Regulations) relating to the applicability of CG requirements on HVLDEs.

Pursuant to the fifth amendment of the Listing Regulations, notified on September 07, 2021[3], the applicability of CG norms were extended to entities with non-convertible debt securities listed and the outstanding amount being Rs. 500 cr or more. While the provisions became applicable from September 07, 2021 the same was implemented on a ‘comply or explain’ basis until March 31, 2023. Accordingly, an HVDLE is expected to endeavour to comply with the provisions and achieve full compliance by March 31, 2023. In case the HVDLE is not able to achieve full compliance with the provisions, till such time, it shall explain the reasons for such non-compliance/ partial compliance and the steps initiated to achieve full compliance in the quarterly compliance report filed under clause (a), sub-regulation (2) of regulation 27 of these regulations.

An HVDLE, that were not equity listed, were only required to comply with Companies Act, 2013 (CA, 2013) requirements for the purpose of transacting with related parties. While CA, 2013 also provides for similar restrictions, it provides a carve out in case of closely held companies. The restriction of related parties not to vote in favor of a resolution, does not apply where ninety per cent. or more members, in number, are relatives of promoters or are related parties. However, there is no such carve out provided in Regulation 23 (4) of the Listing Regulations.

India Infradebt Limited (IIL), a joint venture company and an HVDLE, realised about this deadlock situation as all the shareholders, being venturers, were related parties in terms of Section 2 (76) of CA, 2013. Therefore, it approached SEBI seeking informal guidance for the procedure to be followed for obtaining shareholders’ approval in case of material RPTs.

SEBI provided a stop-gap solution and stated that in view of the ‘inherent difficulty’ by IIL in getting shareholders’ approval for material RPTs, it may choose to explain the reason for not complying.

A pertinent question that arises from the informal guidance and which has not been dealt with, is whether the HVLDEs that are closely held companies, be expected to be on the same pedestal as that of equity listed entities. Even if they are supposed to be, it cannot continue to explain for not complying as from April 1, 2023 these provisions will become mandatory and violation of the same will attract penalties from the stock exchanges.

Further, the RPT provision has been drastically amended and becomes effective from April 1, 2022[4]. The scope of related party and RPT has been widened and the threshold for material RPT has also been amended to impose a numerical threshold of Rs. 1000 crore along with the existing threshold of 10% of annual consolidated turnover. Additionally, the requirement to seek shareholder’s approval will be ‘prior’ to breaching the materiality thresholds.

Therefore, several HVDLEs may be required to seek shareholder’s approval for prospective transactions. SEBI should consider incorporating a carve out similar to that provided under CA, 2013 for closely held HVDLEs in Regulation 23 (4) of the Listing Regulations in order to resolve the issue permanently.

[1] Refer our write up at https://www.moneylife.in/article/bond-issuers-facing-disproportional-compliances-on-corporate-governance-as-sebi-move-nullifies-mca-exemption/65132.html

[2] https://www.sebi.gov.in/sebi_data/commondocs/dec-2021/SEBI%20Informal%20guidance%20letter%20to%20India%20Infradebt%20Limited%20-%20December%2016,%202021.pdf

[3] https://www.sebi.gov.in/legal/regulations/sep-2021/securities-and-exchange-board-of-india-listing-obligations-and-disclosure-requirements-fifth-amendment-regulations-2021_52488.html

[4] Refer our write up here:https://vinodkothari.com/article-corner-on-related-party-transactions/

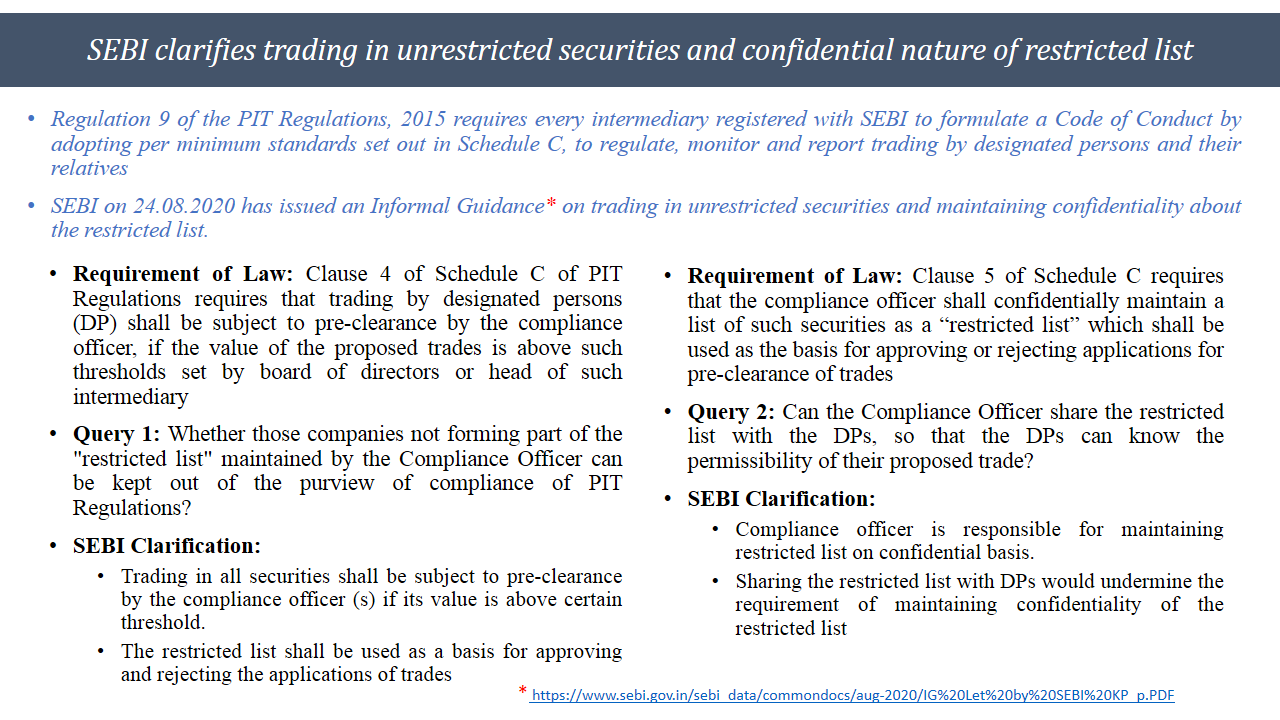

Link to Informal Guidance – https://www.sebi.gov.in/sebi_data/commondocs/aug-2020/IG%20Let%20by%20SEBI%20KP_p.PDF