After over two years of implementing CG norms for HVDLE on a ‘comply or explain’ basis, a new Chapter VA has been inserted in the LODR on March 28, 2025, governing CG norms for pure HVDLEs. Among other things, the new chapter outlines the requirements relating to board and committee composition, subsidiary governance, RPT framework for HVDLEs, etc.

As regards the RPT framework, the one for HVDLE (reg 62K) introduces an additional requirement: consent from debenture holders through NOC from the debenture trustees.

This criteria has been added to fix the “impossibility of compliance”(of getting approval from unrelated shareholders for material RPTs) in case of HVDLEs as most of these have either nil or negligible unrelated shareholders. This also underscores the requirement to protect the interest of the lenders, particularly the debenture holders – aligned with s. 186(5) of the Companies Act, 2013.

However, there are a few practical implementation issues and inconsistencies, possibly arising from the CG norms (prior to the LODR 3rd Amendment in 2024) for an equity listed entity (chapter IV) being the drafting template for this new chapter. This article highlights these issues, particularly those affecting 62K, given the structure of HVDLEs.

Structural difference between HVDLE and an equity listed company

Before beginning to list such inconsistencies, it is important to highlight the structural difference between an HVDLE and an equity listed company – the very reason why a separate chapter for CG has been rolled out for an HVDLE!

HVDLEs are mostly closely held companies with all or close to all shareholders being related parties, approval from unrelated shareholders often becomes an impossibility. Further, considering that the funding to HVDLEs is by the debenture holders, protection of their interest becomes paramount. Accordingly, approval from the debenture holders have been made mandatory for undertaking any material RPTs by a HVDLE.

13.3.3 Since, both banks and debenture holders are lenders to the borrowing entity, it is felt that a similar approach should be adopted for debenture holders. This provides a layer of protection to the debenture holders who might be at risk of unfair treatment due to some RPTs which may also have an impact on the repayment capability of an entity. It is noted that the debenture holders’ interest is intended to be safeguarded by a debenture trustee [SEBI Consultation Paper date October 31, 2024]

Present exemptions – some extra; some missing

Lets now discuss the inconsistencies that needs to be fixed:

Grant of exemptions w.r.t transaction between holding company and its wholly-owned subsidiaries and among WOS does not place well with HVDLEs.

The shareholders of the holding and its WOS are effectively the same and any benefit / resources, if at all transferred to the WOS, in case of an RPT between a holding and WOS, is to consolidate in the holding company and remain within the enterprise. Therefore, such transactions are exempted u/r 23(5). But this theory holds correct in case of an equity listed company only where the interest of equity shareholders needs to be protected.

However, in a debt-listed structure, the concern shifts from the ‘enterprise’ to the individual ‘entity’. The exposure of debenture holders is required to be protected. A debenture holder may have exposure only to the WOS, not the holding company. In such case, exempting RPTs between the holding company and its WOS (or between two WOS) overlooks the distinct legal and financial obligations of each entity. The interest of debenture holder can be considered only by seeking “their” approval for a RPT. The relationship of holding company and WOS between the transacting company does not ensure any protection to the debenture holders. The exemption in 62K(7), mirroring 23(5), places debenture holders at the mercy of equity shareholders in the holding company – contradicting the spirit of the rest of Regulation 62K, which otherwise mandates their approval.

Think of a situation where a WOS (which has issued the debentures) upstreams value to its parent. While equity shareholders in the parent may remain unaffected, the WOS may be left with insufficient resources to repay its debenture obligations. Debenture holders cannot claim recourse against the parent; their exposure is limited to the WOS.

Exemptions in reg 23 brought through LODR 3rd amendment viz. w.r.t remuneration to KMPs and SMPs who are not promoters etc is missing in Reg 62K

Remuneration paid to KMP and SMP who are not promoters, payment of statutory dues, transactions between PSU and CG / SG which are exempted for an equity listed entity have not been replicated under 62K. There is no reason why these exemptions which are provided to an equity listed entity, shall not be provided to an HVDLE, when the underlying intent of these exemptions aligns with an HVDLE.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-04-29 15:12:402025-04-29 17:26:35Misplaced exemptions in the RPT framework for HVDLEs

Enterprise Level v/s Entity Level: Paradox of a Wholly owned Subsidiary

Wholly owned Subsidiaries (WoS) form a particular paradox in corporate laws with two contradictory positions – (a) the transactions entered into between the holding company and its WoS are viewed as transactions within a group, thus, permitting a seamless flow of resources between the two without any objection, looking at an “enterprise” level whereas, (b) limiting the access of the shareholders and creditors of the holding company and the WoS to the respective entity’s resources, thereby separation of the two at an “entity” level.

Disregarding ‘entity’ concept over ‘enterprise’ concept: exemptions w.r.t. WoS

Section 185 of CA 2013 exempts any financial assistance to the WoS from the compliance requirements under the section, and the limits on loans, guarantees, investments or provision of security under section 186 do not apply for transactions with WoS. Section 177(4)(iv) and 188 of CA 2013, pertaining to RPT controls, also extend certain exemptions for transactions with WoS. Reg 23(5) of SEBI LODR also exempts transactions with WoS as well as between two WoS from approval requirements, at both the Audit Committee and shareholders’ level. Reg 37A of SEBI LODR contains an exemption from shareholders’ approval requirements for sale, lease or disposal of an undertaking to the WoS. In each of the aforesaid provisions, the underlying presumption remains the same – the accounts of the WoS are consolidated with that of the holding company, and hence, the flow of resources remain within the same ‘enterprise’, despite change of ‘entity’. Thus the law takes an ‘enterprise’ wide view instead of an ‘entity’ level view while providing for such exemptions.

Factors reinforcing the concept of separation of entity

On the other hand, the outreach of shareholders of a company is limited at an ‘entity’ level, that is to say, the shareholders of the holding company do not have access to the general meetings of the WoS. Similarly, the creditors of each entity do not have any recourse against the other entity. For instance, where the holding company has outstanding dues, but there are resources at the WoS level, can the creditors reach to the assets of the WoS? The answer is no. Similarly, a vice versa situation is also not possible. In fact, under the Insolvency and Bankruptcy Code too, the assets of the subsidiary are kept outside the purview of the liquidation estate of the holding corporate debtor [Section 36(4)(d)].

Further, the board of a WoS is different from its holding company. The board of the holding company does not have any rights over the board of the subsidiary. Therefore, under these situations, transactions between the holding company and its WoS, though between companies that are 100% belonging to the same group, cannot be viewed as completely seamless or free from any corporate governance concerns.

RPTs between holding company and WoS: can the ‘enterprise’ approach be taken?

The aforesaid discussion makes it clear that while an ‘enterprise’ wide approach is taken in granting exemptions to WoS, the separation of legal entities cannot be completely disregarded, because the outreach of the shareholders, creditors and the board of directors remain limited. Now from the point of view of related party transactions, can it be argued that the transactions between a holding company and WoS are without any restraint altogether? For example, does the concept of arm’s length has no relevance in case of a transaction between a holding company and WoS?

Concept of arm’s length and relevance in transactions with WoS

A light touch regulation or inapplicability of certain controls or approvals does not mean that arm’s length precondition becomes unnecessary. If such a view is taken, then the flow of resources between the holding company and the WoS will be completely without any fetters, thus breaching the concept of corporate governance at an entity level. For instance, can the board of directors of the holding company be absolved from its responsibilities to safeguard the assets of the holding company where the same flows to the subsidiary without any consideration? The answer surely is a no. Both ‘entity’ level and ‘enterprise’ level are significant, and hence, one cannot disregard the separation of legal entities, particularly, in the context of protection of assets of the entity (also see discussion under Role of Board below).

As regards the concept of arm’s length, the same is omnipresent – required to be ensured in transactions with related parties as well as unrelated entities. The meaning of arm’s length transaction, as defined under SA 550 pertaining to Related Parties, is as follows:

A transaction conducted on such terms and conditions as between a willing buyer and a willing seller who are unrelated and are acting independently of each other and pursuing their own best interests.

Therefore, ‘independence’ and ‘own interests’ are important elements of an arm’s length transaction. If compromised in RPTs with WoS, absence of arm’s length criteria could lead to uncontrolled flow of wealth from the holding company to WoS, and may also lead to abusive RPTs.

Are WoS structures immune from abuse?: Deploying WoS as a stop-over for abusive RPTs

The exemptions w.r.t. transactions with WoS make the same prone to misuse, through use of the WoS as a conduit or a stop-over for giving effect to arrangements with non-exempt RPs. For instance, a listed entity in the FMCG sector is required to provide financial assistance to its upstream entities (promoter group entities). There may be a lack of business rationale and commercial justification for such a transaction, and therefore, it is highly unlikely that such a transaction would get the approval of the AC. Therefore, in order to give effect to the transaction, the company may route the same through its WoS, and thus escape RPT controls at its AC level. The WoS may, in turn, pass on the benefit to the promoter group entities, through a series of transactions, in order to cover the real character of the transaction (see figure below).

A guidance note published by NFRA also, requires identification of indirect transactions, including through ‘connected parties’. In order to ensure no such indirect transactions have occurred, the management is expected to establish procedures to identify such transactions, and to obtain periodic confirmations from the directors, promoter group, large shareholders and other related parties that there are no transactions that have been undertaken indirectly with the listed company or its subsidiaries or its related parties.

Role of board

The role of the board towards avoiding conflicts of interests is deep-rooted under the corporate laws and securities laws, under various applicable provisions. For instance, the directors have a responsibility towards safeguarding the assets of the company and for preventing and detecting fraud and other irregularities [Section 134(5)(c) of CA 2013]. Section 166 of CA 2013 specifies the duties of directors. These include, among others, the duty to act in good faith in order to promote the objects of the company for the benefit of its members as a whole, and in the best interests of the company [Section 166(2)].

The key functions of the board, as contemplated under Reg 4 of LODR, also includes monitoring and managing potential conflicts of interest of management, members of the board of directors and shareholders, including misuse of corporate assets and abuse in related party transactions.

Scope of Exemption under Applicable Laws

As stated above, Reg 23(5) of SEBI LODR exempts RPTs entered into between a holding company and its WoS from the approval requirements of both the AC and the shareholders.

Apart from Reg 23 of LODR, the RPT provisions are contained under Section 177 and 188 of CA 2013. Under section 177(4)(iv) of CA 2013, all RPTs require approval of the AC. The fourth proviso to the said sub-section exempts RPTs entered into with WoS from AC approval requirements. However, the said exemption is not absolute. The proviso reads as follows:

Provided also that the provisions of this clause shall not apply to a transaction, other than a transaction referred to in section 188, between a holding company and its wholly owned subsidiary company.

Thus, the exemption for RPTs with WoS does not apply in case of a transaction referred u/s 188 of CA 2013. In other words, where an RPT with WoS triggers approval requirements u/s 188, the same will also be required to be approved by the AC u/s 177 first.

Meaning of “a transaction referred to in section 188”

Section 188(1) of CA 2013 provides a list of 7 types of transactions. The list is wide enough to cover almost all types of transactions, except financial assistance in the form of loans etc. However, section 188 becomes applicable, only, in cases where any one or more of the two most crucial elements of a transaction are missing – (i) ordinary course of business and (ii) arm’s length terms. In cases where a transaction does not meet the ordinary course of business or the arm’s length criteria, the same is referred to the board of directors u/s 188 of CA 2013, and requires prior approval of the board.

The fifth proviso to section 188(1) also contains an exemption for RPTs between the holding company and its WoS. Note that the said exemption is applicable only with respect to the approval of the shareholders, the approval of board is still required for RPTs that lack one of the two elements stated above, even though with WoS.

Provided that no contract or arrangement, in the case of a company having a paid-up share capital of not less than such amount, or transactions not exceeding such sums, as may be prescribed, shall be entered into except with the prior approval of the company by a resolution:

XXX

Provided also that the requirement of passing the resolution under first proviso shall not be applicable for transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval:

The conditional exemption given u/s 177 and the absence of any exemption from board’s approval u/s 188 clearly confirms the requirement of ensuring arm’s length terms in transactions with WoS.

Expectations from AC

The AC is the primary decision-making authority in respect of matters relating to related party transactions. NFRA, the audit regulator of the country, has published the Audit Committee – Auditor Interactions Series 3 dealing with audit of Related Parties. The guidance sets out potential points on which the AC may interact with the auditors in the context of RPTs. Where a company avails exemptions w.r.t. AC and shareholders’ approval, the guidance note requires documentation of the rationale for not obtaining Audit Committee’s and Shareholders’ approvals.

Thus, the AC is expected to be the scrutinising authority in ensuring that the terms on which a transaction is proposed to be entered into with a WoS are at an arm’s length, which, in turn, would require bringing the transaction before the AC, if not for approval, then for a pre-transaction scrutiny and information.

Disclosures in financial statements

Ind AS 24 pertaining to Related Party Disclosures require disclosures to be made in the financial statements that the RPTs were made on terms equivalent to those that prevail in arm’s length transactions. However, such disclosure can be made only if such terms can be substantiated. Note that the Ind AS 24 does not contain any exemption for WoS. In the absence of a strict scrutiny of RPTs with WoS for satisfaction of arm’s length basis of the terms of the transaction, such an assertive statement in the financial statements for arm’s length of the terms is not possible.

Dealings with WoS: the suggested approach

In view of the expectations from the AC, board and the auditors, and the potential risks of abusive RPTs using WoS as an intermediary, the following approach may be undertaken before entering into a transaction with WoS:

A pre-transaction scrutiny may be conducted by the AC for RPTs to be entered into between the holding company and its WoS. This should include all the necessary details as may be required by the AC, such as, nature of transaction, terms of the transaction, total expected value of the transaction etc.

Based on such scrutiny, the AC may give its comments or recommendations where the same has any concerns. Necessary modifications may be carried out to address the comments of the AC, in order to make the transaction commercially viable for the holding company.

Where the proposed transaction is not in (a) ordinary course of business or (b) not at an arm’s length basis, the same will require approval of the AC. The AC will refer the transactions to the board for approval u/s 188.

Every RPT entered into between the holding company and its WoS should, as a part of the quarterly review, be reported back to the AC. Any alteration in terms or value of the transactions should be brought to the notice of the AC.

As required under Reg 23(9) of the LODR, the transactions with WoS to be reported to the SEs on a half-yearly basis.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-04-28 15:14:372025-04-28 17:27:10RPTs: Wholly-owned but not wholly- exempt

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2025-04-21 20:15:522025-04-21 20:15:53Representation to SEBI on SEBI (LODR) (Amendment) Regulations, 2025

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-04-16 19:36:012025-04-16 23:12:48Presentation on CG Norms for HVDLEs

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2025-04-07 20:48:502025-04-08 17:17:12Webinar on CG Norms for HVDLEs

Notifies amendment as COREX timeline set to expire

– Team Corplaw | corplaw@vinodkothari.com

March 28, 2025 | Team Vinod Kothari & Company

Just before the expiry of the ‘Comply or Explain’ timeline of March 31, 2025 for HVDLEs, SEBI notified SEBI (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2025 inserting a separate chapter viz. Chapter VA: Corporate Governance Norms for a Listed Entity which has listed its Non-Convertible Debt Securities effective from March 27, 2025. The proposal for amendments were made in the Consultation Papers of October 31, 2024 and February 8, 2023, and was approved by SEBI in the board meeting held on December 18, 2024. A summary of the changes notified, comparison of the new compliance requirements vis-à-vis the earlier norms have been captured in this write-up.

HVDLEs: Meaning, Applicability, Sunset Clause

The only criteria for being categorized as an HVDLE is the amount of outstanding value of listed non-convertible debt securities, which has now been revised from Rs. 500 crores or more to Rs. 1,000 crores or more. This upward revision is aligned with the criteria for being identified as a Large Corporate, i.e. outstanding long-term borrowing amounting to Rs. 1,000 crores or more, and has been introduced with the dual objective of tightening the regulatory regimes for debt listed entities while simultaneously promoting ease of doing business in the corporate bond market.

The provisions of the Chapter VA, a chapter exclusive to entities having listed only their non-convertible debt securities, the outstanding value of which is exceeding Rs. 1,000 crores, and not specified securities, shall apply with effect from April 1, 2025. Explanation(1) appended to Regulation 62C clarifies that HVDLEs shall be determined on basis of value of principal outstanding of listed debt securities as on March 31, 2025, irrespective of the date of notification of this amendment.

A doubt may arise arise with regards the applicability of this chapter to an entity whose outstanding value of NCDs exceeds the threshold during the year, i.e. after March 31, 2025 – the Explanation(2) to the same regulation makes it clear that such entity shall ensure compliance with the provisions of Chapter VA within six months from the date of such trigger and the disclosures of such compliance may be made in corporate governance compliance report on and from third quarter, following the date of the trigger.

However, the earlier conception of “Once an HVDLE, always an HVDLE” has now been removed with the introduction of a sunset clause, in Regulation 62C(2), which specifies that the provisions of this chapter shall cease to be applicable, after three consecutive years of the value of outstanding NCDs being below the Rs. 1,000 crores threshold, as determined on March 31 of any given year.

Related Party Transactions by HVDLEs

While the scope of RP and RPTs continue to be the same as defined in regulation 2(1) (zb) and (zc) respectively, the present amendment introduces a revised RPT approval regime for HVDLEs particularly for Material RPTs. The restriction for related parties to not vote to approve the material RPT, provided under regulation 23, resulted in impossibility of compliance for HVDLEs as most HVDLEs were closely held companies. Accordingly, SEBI introduced a two step approval process for material RPTs with first obtaining NOC from the debenture holders (of listed debt securities issued on or after April 01, 2025) not related to the issuer and holding at least more than 50% of the debentures in value, on the basis of voting including e-voting, followed with approval of shareholders through ordinary resolution. The provisions of Reg. 62K is applicable to RPTs entered into on or after April 1, 2025. Refer to our FAQs to understand the implications and manner of seeking approval.

While the other requirements are similar to corresponding requirements under regulation 23 for equity listed entities (for e.g., framing of policy, prior approval of audit committee, half yearly disclosures etc.), recent amendments made in December, 2024 in relation to ratification of RPTs and exemption from approval requirements of audit committee and shareholders have not been inserted in reg. 62K.

Prior to this amendment, so long the debt was continued to be serviced and the terms and conditions of borrowing was met, the debenture holders were not required to intervene in the regular operations of the company. If there was a covenant to that effect in the debenture subscription agreement or Debenture Trust Deed or terms of issue, in that case, irrespective of whether the RPT is material or immaterial, the borrowing entity was required to comply. With this amendment, the debenture holders will also have a say in corporate governance, especially in case of material RPTs pursuant to a provision of law. Other lenders extending term loan and other facilities, and who have a larger exposure on such companies, will not have this opportunity.

Differing requirements under CG norms for an HVDLE vis-a-vis an equity listed entity

The provisions of Reg. 16 to 27 of Chapter IV have been suitably modified and inserted in the context of HVDLEs in Chapter VA. While largely the flow of the provisions and requirements are aligned, there exists certain gaps in certain provisions. The tabular comparison below highlights the same (excluding those differences that are linked with market capitalization related requirements/ outstanding SR equity shares related requirements that only apply to equity listed entities):

Particulars

Reqt. under Chapter IV for equity listed entities

Reqt. under Chapter VA for HVDLEs

Remarks

Meaning of IDs

Defined under Reg. 16(1)(b)

Reg. 62B (1) (b) refers to definition in Chapter IV and additionally provides for considering the NEDs other than nominee directors, in following listed entities: A body corporate mandated to constitute its board as per the law under which it is constituted; or Set up under public private partnership [PPP] model

In the case of the PPP model, the composition of the board is pre-decided or mutually decided between the public authority and private entity, hence the exemption. Further, for HVDLEs that are private limited companies, having IDs as per the criteria given under Chapter IV, becomes explicit.

Timeline for obtaining shareholders’ approval for board appointments

Reg. 17 (1C) To be obtained within 3 months from appointment or ensuing general meeting, whichever is earlier. Carve outs: Time taken for obtaining approval of regulatory, government or statutory authorities, shall be excluded.Provisions not applicable to appointment or re-appointment of a person nominated by a financial sector regulator, Court or Tribunal to the board of the listed entity

Reg. 62D To be obtained within 3 months from appointment or ensuing general meeting, whichever is earlier. Both the carve outs are not available for HVDLE.

The corrections made to corresponding provision in Reg. 17 (1D) vide LODR Third Amendment Regulations, 2024 have not been made in Chapter VA. The carve out under Reg. 62D (4) pertains to that sub-regulation and not the entire Reg. 62D.

Continuation of director on the board subject to shareholders’ approval once in every five years

Carve outs provided in provisos to Reg. 17 (1D): To the director appointed pursuant to the order of a Court or a Tribunal or to a nominee director of the Government on the board of a listed entity, other than a public sector company, or to a nominee director of a financial sector regulator on the board of a listed entity.To a director nominated by a financial institution registered with or regulated by RBI under a lending arrangement in its normal course of business or nominated by a SEBI registered DT under a subscription agreement for the debentures issued by the listed entity.

Carve outs in Reg. 62D (4) are broadly similar. Reg. 62D (4) additionally exempts director appointed under the public private partnership model/structure.

As composition is pre-decided or is as per mutual terms between the public authority and private entity.

Nature of listed entities considered and limits for maximum no. of directorships

Reg. 17A- LEs shall be cumulative of those whose equity shares are listed on a stock exchange and HVDLEs. Director in not more than 7 LEsID in not more than 7 LEsIf WTD/ MD in any LE, ID in not more than 3 LEs Further, to give sufficient time to all the listed entities to ensure compliance with the provision, a period of 6 months or till the time AGM is held from the date of applicability of the provision to the entity, whichever is later, has been provided.

Reg 62E provides the same limits. LEs shall be cumulative of those whose equity shares are listed on a stock exchange and HVDLEs. Carve out for directorships in PSUs and entities set up in PPP arrangements are not to be included.

In order to ensure that directors devote adequate time to listed entities including HVDLEs and in the interest of investor protection.

Composition of NRC, SRC and RMC

Reg. 19, 20 & 21:Each of the committees viz. Nomination and Remuneration Committee, Stakeholders Relationship Committee and Risk Management Committee (top 1000 based on market cap) are required to be constituted.

Reg. 62G – The functions of NRC may either be discharged by the board or by NRC.Reg. 62H – The functions of SRC may either be discharged by the board or by SRC.Reg. 62I – The functions of RMC may either be discharged by the board or by audit committee or by RMC.

In order to avoid the constitution of multiple committees by HVDLEs.

Exemption from prior approval of AC of the holding LE, in case, provisions of Reg 23 is applicable to the subsidiary

Reg 23(2)(d): Prior approval of the audit committee of the listed entity shall not be required for a related party transaction to which the listed subsidiary is a party but the listed entity is not a party, if regulation 23 and sub-regulation (2) of regulation 15 of these regulations are applicable to such listed subsidiary.

Reg 62K: Identical provisions, however, position is not clear where the subsidiary is also an HVDLE.

The exemption should be available even in case of an HVDLE subsidiary, as such a subsidiary will be required to independently comply with Regulation 62K, similar to that provided in Reg. 62K(6).

Exemption from approval of AC w.r.t. remuneration and sitting fees paid to Director, KMP and SMP (non-promoter)

Reg 23(2)(e): remuneration and sitting fees paid by the listed entity or its subsidiary to its Director, KMP and SMP (non-promote, shall not require approval of the audit committee provided that the same is not material.

No such carve out in Reg. 62K (3)

The amendments made in Reg. 23 vide LODR Third Amendment Regulations, 2024 have not been made in Reg. 62K.

Ratification of RPT

Reg 23(2)(f): The members of the audit committee, who are independent directors, may ratify related party transactions subject to the certain conditions and timelines

No such provisions are included in Reg. 62K (3)

The amendments made in Reg. 23 vide LODR Third Amendment Regulations, 2024 have not been made in Reg. 62K.

Omnibus approval proposed to be undertaken by subsidiary companies

Reg 23(3): Audit committee may grant omnibus approval for related party transactions proposed to be entered into by the listed entity or its subsidiary subject to the certain conditions

Reg 62K: Identical provisions, However, subsidiary companies of HVDLE are not included in the ambit of omnibus approval provisions for HVDLE

The amendments made in Reg. 23 vide LODR Third Amendment Regulations, 2024 have not been made in Reg. 62K.

Approval regime for material related party transactions

Reg 23(4): All material related party transactions and subsequent material modifications shall require prior approval of unrelated members.

Reg 62K(5): All material related party transactions and subsequent material modifications shall require prior NOC from the DT and the DT shall in turn obtain No-Objection/approval from the unrelated DH who hold atleast > 50% of the debentures in value, on the basis of present and voting including e-voting. 62K(6): approval of shareholders shall be required after obtaining NOC from DT, however, no restriction has been placed on shareholders that are RPs from voting to approve the resolution.

Several HVDLEs are closely held companies, holding a negligible portion of the equity or none at all, in which case the entity was not able to transact such RPTs because of ‘impossibility of compliance’ with the provisions of LODR Regulations. Therefore, taking cue from Sec. 186 (5), SEBI tried to address this issue by mandating NOC from debenture holders.

Exemption from Material RPT approval in case of listed subsidiaries

Reg 23(4): Available if regulations 23 and 15 (2) are applicable to such listed subsidiaries.

Reg 62K(6): Prior approval of the shareholders and NOC by DT of a HVDLE, shall not be required for a RPT to which the listed subsidiary is a party but the listed entity is not a party, if regulation 62K of these regulations is applicable to such listed subsidiary, however, position is not clear i.r.t. Listed subsidiary, if reg 23 is applicable to such subsidiary.

This situation is inverse for obtaining audit committee approval in case of HVDLE. In the context of equity listed entities, the exemption is not available in case of Material RPTs undertaken by an HVDLE subsidiary.

Exemption from AC & S/h approval requirements for certain RPTs

Reg 23(5): Following transactions are exempt from the applicability of approval provisions: (a) transactions entered into between two public sector companies;(b) transactions entered into between a holding company and its WOS (c) transactions entered into between two WOS of the LE(d) transactions which are in the nature of payment of statutory dues, statutory fees or statutory charges entered into between an entity on one hand and the Central Government or any State Government or any combination thereof on the other hand. (e) transactions entered into between a public sector company on one hand and the Central Government or any State Government or any combination thereof on the other hand.

Reg 62K(7): The exemptions are not identical:(i) under point (a) exemption available for government companies and not public sector companies;(ii) point (b) and (c) are identical(iii) point (d) and (e) are excluded.

The amendments made in Reg. 23 vide LODR Third Amendment Regulations, 2024 have not been made in Reg. 62K.

CG requirements with respect to subsidiary

Requirements of Reg. 24 apply to unlisted subsidiaries.Reg 24 (1) – appointment of atleast 1 ID of the parent listed entity on the board of the unlisted material subsidiary (whoseturnover or net worth exceeds 20% of the consolidated turnover or net worth respectively, of the listed entity and its subsidiaries in the immediately preceding accounting year) Reg 24(2): Review of financial statements of the unlisted subsidiary by the audit committee of the listed entity.Reg 24(3): Review of board minutes of the unlisted subsidiary by the board of the listed entity. Reg 24(4): Review by the board of significant transactions/arrangements entered into by the unlisted subsidiary.Reg 24 (5): Shareholders’ approval for disposal of shares of material subsidiary whoseturnover or net worth exceeds 10% of the consolidated turnover or net worth respectively, of the listed entity) resulting in reduction to less than or equal to 50% or cessation of control.Reg 24 (6): Shareholders’ approval for sale, disposal and leasing of assets of material subsidiary (whoseturnover or net worth exceeds 10% of the consolidated turnover or net worth respectively, of the listed entity)

Reg 62L: All requirements apply only to unlisted material subsidiary (whoseincome or net worth exceeds 20% of the consolidated income or net worth respectively, of the listed entity and its subsidiaries in the immediately preceding accounting year)

CG requirement pertaining to subsidiary is relaxed for HVDLE in comparison to that of equity listed entity

Secretarial Audit and Secretarial Compliance (ASC) Report

Reg 24A: LE and its material unlisted Indian subsidiaries ((whoseturnover or net worth exceeds 10% of the consolidated turnover or net worth respectively, of the listed entity) to undertake Secretarial audit by Peer Reviewed Secretarial Auditor. Further, the regulations also deal with tenure of appointment, rotation of secretarial auditors, eligibility, qualifications and disqualifications for appointment of a secretarial auditor, and prohibited services prescribed w.r.t Secretarial Auditors of the listed entity. ASC report to be submitted within 60 days from the end of FY by the listed entity.

Reg 62M: HVDLEs and its Indian material unlisted subsidiary (no definition provided) to undertake secretarial audit and annex the report in annual report. Further, HVDLEs to submit ASC report within 60 days. The requirement of peer reviewed CS to conduct Sec audit or issue ASC, tenure of appointment, rotation of secretarial auditors, eligibility, qualifications and disqualifications for appointment of a secretarial auditor, and prohibited services prescribed w.r.t Secretarial Auditors etc not applicable.

The amendments made in Reg. 24A vide LODR Third Amendment Regulations, 2024 have not been made in Reg. 62M. Further, the scope of material subsidiary is not provided as the definition under Reg. 16 and Reg. 62L may not apply unless expressly indicated.

Agreement pertaining to profit sharing or in connection with dealings in securities of the company

Reg 26(6): Any agreement entered into by the employees, KMP/director/promoter for himself/herself or on behalf of any other person with regard to compensation or profit sharing in connection with dealings in the securities of listed entity, requires prior approval by the board and public shareholders by way of ordinary resolution. Interested persons involved in the transaction are required to abstain from voting.

Reg 62O(5): The regulation is similar to that provided in Reg. 26(6) with the exception that there is no restriction for voting by the interested persons.

The amendments made in Reg. 26(6) vide LODR Third Amendment Regulations, 2024 have not been made in Reg. 62O.

Other Amendments

Related Party Transactions by SME Listed entities

A listed entity which has listed its specified securities on the SME Exchange are not required to comply with the CG norms otherwise applicable to a Main Board listed entity which have either paid up capital exceeding Rs. 10 crore or net worth exceeding Rs. 25 crore). In order to plug the risk of siphoning of funds to related parties, as observed by SEBI in certain instances, the present amendment harmonizes and aligns the RPT norms applicability by extending it to SME listed entities other than those which have paid up capital not exceeding Rs. 10 crores and net worth not exceeding Rs. 25 crores. Further, considering the size of SMEs, the threshold limit for Material RPTs have been set to Lower of INR 50 Cr or 10% of annual consolidated turnover as per last audited financial statements. Where the provisions become applicable at a later date, SMEs will have 6 months time to ensure compliance. The provisions shall continue to apply till both the conditions w.r.t equity share capital and networth falls below the threshold and remains below the threshold for 3 consecutive FYs.

Business Responsibility and Sustainability Reporting

Regulation 34(2)(f) of the Listing Regulations so far required assurance of the BRSR Core Report, which has now been modified to term it as ‘assessment or assurance of the specified parameters’ to prevent unwarranted association with a particular profession (specifically audit profession). Assessment defined as third-party assessment undertaken as per standards notified by the Industry Standards Note on BRSR Core, developed in consultation with SEBI.

Similar modification has been reproduced for obtaining BRSR Core Report from Value Chain Partners of the Listed Entity, and a clause of voluntary disclosure of the same for HVDLEs has been added in Regulation 62Q(3).

The applicability of CG norms (on a COREX basis) was extended to HVDLEs i.e. entities having an outstanding value of listed non-convertible debt securities of Rs. 500 Crore and above, by SEBI vide its notification dated 7th September, 2021. Following the extension thread for mandatory applicability of Corporate Governance (CG) norms under SEBI Listing Regulations (LODR) on High-Value Debt Listed Entities (HVDLEs) from FY 23-24 to FY 24-25 and again postponing it from 1st April, 2025, SEBI released another Consultation Paper (CP) on 31st October, 2024 containing several proposals to ease the compliance burden of HVDLEs. A similar CP was issued earlier on 8th October, 2024 to review the CG norms primarily focusing on related party transactions (RPTs) [Our analysis on the same can be read here].

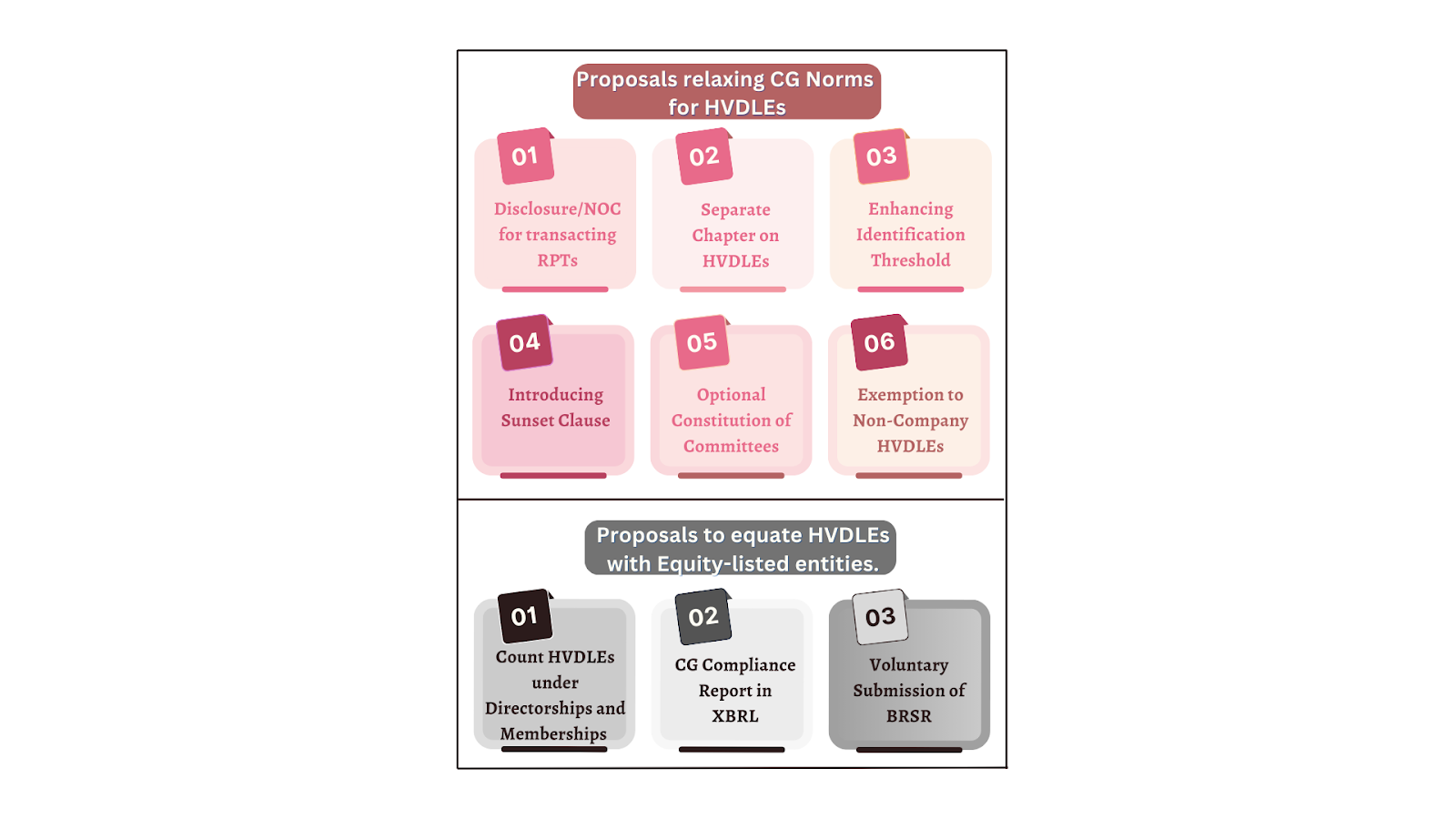

While the intent behind the CG norms being made applicable was to protect debenture holders and assimilate corporate governance amongst such issuer entities, the complexities associated with its implementation hindered the ease of doing business and increased the compliance burden manifold. The current CP delves into the comments received on the previous proposal as well as the issues that HVDLEs have been facing in practically implementing the CG norms (i.e. Regulations 16 to 27 of LODR, 2015). While it discusses the much needed and critical areas (CG chapter, mandatory committees, RPTs, etc.) where HVDLEs can be considered to be relieved and not be kept on the same pedestal as that of the equity listed entities, however, for some provisions (included for max no. of directorship, committee membership, XBRL filings, etc.), HVDLEs have been proposed to be roped in at par with entities with their specified securities listed. While each of the proposals have been discussed in detail below, a snapshot of the same can be seen in the diagram below:

Proposals relaxing CG Norms for HVDLEs

Providing In-Principle Declaration or obtaining No-Objection Certificate (NOC) from NCD holders in connection with RPTs:

One of the most crucial concerns for HVDLEs was the impossibility of compliance when it came to securing approvals for RPTs. The same was highlighted by SEBI in its earlier CP dated 8th February, 2023 wherein it was mentioned that 104 out of 138 HVDLEs as of 31st March, 2022, comprised of shareholders with more than 90% of them being related parties (RPs).

The current proposal is set against a reference to a banking transaction wherein the lender reserves the right to allow the borrower to enter into any transaction that might be unfavorable to the lender such as entering into RPTs. Thus, HVDLEs being of the nature of a borrower and the debenture holders being the lenders, it is paramount to protect the latter’s interests by enforcing such provisions as may be necessary and safeguarding them through a debenture trustee.

In view of the same, the proposition has the following features:

Either provide an upfront declaration in the offer document with respect to the amount of RPTs proposed to be entered over the tenure of the NCDs along with the percentage of the same when compared with the issue size or obtain an NOC from the debenture trustee, who in turn needs to obtain it from the debenture holders (the majority not being related to the issuer) for all the material RPTs as and when they are required to be transacted;

VKCo Comments – Until the fine print of the regulations is rolled out, it is understood that only the broader limits of the estimated RPTs are required to be mentioned unless otherwise finer details are required which can become extremely difficult for these entities.Further, for the alternative requirement, there does not seem to be any incentive to first approach the debenture trustee and thereafter the trustee to approach the NCD holders, which can actually be done directly.

monitoring of the issue proceeds by a credit rating agency; and

declare the following in the offer document upfront and be maintained over the tenure of the NCDs:

debt-equity ratio,

debt service coverage ratio;

interest service coverage ratio and;

such other financial/ non-financial covenants

VKCO Comments – Both the aforesaid proposals do not serve the exact purpose of maintaining controls over RPT. Also, these are also reflected in the financials to some extent.

Introduction of a separate chapter for the governance of HVDLEs

LODR in its present form consists of 12 Chapters, each having its purpose and application. As far as the CG norms are concerned, HVDLEs are required to follow the provisions primarily centered around equity listed entities which, inter alia, relate to the composition of the Board of Directors, the constitution of various specialized committees, stipulations regarding RPTs and so on. Having said that, these provisions are not completely relatable to HVDLEs since the majority of these entities are purely debt listed without any other security being listed. Accordingly, it has been proposed to introduce a separate chapter on CG norms for HVDLEs distinct from the existing one for equity listed entities.

VKCO Comments: While this proposal is noteworthy, however, instead of rolling out a new chapter, there could have been certain modifications in the existing regulations by way of a proviso to align with the needs of an HVDLE. Further, one also needs to wait to see the fine print of the provisions once the same is issued.

Increase in threshold for being identified as an HVDLE

Based on the data provided by NSDL as of 31st March, 2024, the number of pure debt listed entities with an outstanding of more than Rs. 500 crores is 166 (comprising of an aggregate outstanding of Rs. 13.54 lakh crores), of which 112 entities are those having an outstanding of more than Rs. 1,000 crores (comprising of an aggregate outstanding of Rs. 13.16 lakh crores).

Further, referring to SEBI’s circular dated 19th October, 2023 in which the threshold limit of outstanding long-term borrowing was enhanced from Rs.100 crore to Rs.1,000 Crore for the purpose of being identified as a Large Corporate called for introspection at the existing threshold of being identified as an HVDLE. Aligned with its objectives of tightening the regulatory regimes for debt listed entities and at the same time promoting ease of doing business in the corporate bond market, the proposal suggests doubling the limit from the present threshold of Rs. 500 crores to Rs. 1,000 crores.

VKCo Comments: The proposal to enhance the extant threshold is encouraging in terms of governing the maximum value of outstanding debt while at the same time achieving the same without bearing the burden of compliance by an increased number of purely debt listed entities. Subsequently, effective implementation of such a proposal aligns it with the identification criteria of Large Corporates.

Introduction of “sunset provisions” for non-applicability of CG norms:

The extant Regulation 3(3) of SEBI (LODR), 2015 provides for the applicability of the CG norms even when the value of the outstanding debt securities falls below the specified threshold forever. The same is in contradiction with respect to the period of applicability as compared to its equity counterpart wherein Regulation 15(2)(a) provides that the norms will have to be complied till such time that the equity share capital or net-worth of the listed entity falls and remains below the specified threshold for a period of three consecutive financial years. Accordingly, for the purpose of aligning the non-applicability, a similar sunset provision for HVDLEs too has been proposed. The proposal outlines that the CG norms shall continue to remain in force for HVDLEs till such time the value of outstanding debt listed securities (reviewed on the cutoff day being 31st March of every financial year) reduces and remains below the defined limits for a period of three consecutive financial years and further ensuring compliance within a period of six months from the date of a subsequent increase in the value above the trigger. The proposition also provides for disclosing such compliances in the Corporate Governance compliance report to be submitted on and following the third quarter of the trigger.

VKCO Comments: The proposal is welcome since it clearly sets the HVDLEs free from the barrier of once an HVDLE so always an HVDLE. This proposal sets a clear nexus between the compliance and the size of the debt outstanding, for the protection of which in the very first place, the compliance triggered.

Certain mandatory committees made optional

Regulations 19, 20 and 21 of LODR mandate the constitution of the Nomination and Remuneration Committee (NRC), Stakeholders Relationship Committee (SRC) and Risk Management Committee (RMC) respectively and provide for their composition, the number of meetings to be held, quorum, duties and responsibilities, among other things. The proposal recognises the difficulties of constituting multiple committees by HVDLEs and therefore, extends the option of either establishing such committees or ensuring delegation and discharge of their functions by the Audit Committee in the case of NRC and RMC and by the Board of Directors in case of SRC.

VKCo Comments: Given the close construct of debt listed entities, it is often observed that the constitution of such committees becomes more of a hardship than in smoothening compliance and discussing specific matters. Accordingly, it looks appropriate to redirect the functions of NRC and RMC to the Audit Committee and that of the SRC to the Board.

Exemption to entities not being a Company

Several entities are not incorporated in the form of companies and therefore, are regulated by specific acts of the Parliament. The rationale behind this move lies in the fact that the administration of these entities is governed by such specific Acts subject to approval from the concerned Ministries. An exclusion on similar lines was granted to equity listed entities by way of Regulation 15(2)(b) which was later omitted w.e.f. 1s September, 2021 vide notification dated 5th May, 2021.

Further, it is awaited as to how effective and permanent such an exemption would be, but SEBI’s working group has proposed for dispensation of entities like NABARD, SIDBI, NHB, EXIM Bank and such other entities fulfilling the criteria as laid out above and application of CG norms to the extent that it does not violate their respective regulatory framework formulated by the concerned authorities.

VKCo Comments: While SEBI refers to the introduction of similar exclusion for equity listed entities, however, it has also mentioned the subsequent amendment wherein the same was omitted. In any case, the instant proposal is a welcome change since it will help such entities to give preference to their principal statutes and not an ancillary one like LODR.

Proposals to equate certain CG Norms for HVDLEs to that of equity listed entities:

Count HVDLEs under no. of directorships, and memberships of Committees:

The extant provisions of Regulation 17A of LODR and Section 165 of the Companies Act, 2013 limit the number of directorship positions that a person can hold, with appropriate sub-limits being set out with respect to public companies and equity listed companies. Similarly, Regulation 26 of the SEBI (LODR), 2015 places ceiling limits on the number of memberships and chairmanships that a person can hold in committees across all listed entities, with explicit exclusion for such positions held in HVDLEs.

The instant proposal is for including the directors in HVDLEs as well as committee membership and chairpersonship positions held in HVDLE just as equity listed entities are included.

The same has been proposed in view of the fact that directorship is a significant position in any company and therefore, multiple directorships beyond a reasonable limit are likely to inhibit the ability of a person to allocate appropriate time to play an effective role in delivering its responsibilities including the timely repayment of debt..

Further, the initial proposal for inclusion of HVDLEs in max no. of directorship allows a period of six months or till the next AGM to ensure compliance.

VKCO Comments: The rationale completely aligns with the proposal made and seems to be justified.

Compulsory filing of CG Compliance Report in XBRL format:

Pursuant to Regulation 27(2), which mandates the submission of a quarterly report on complying with CG norms by listed entities, the format of the report has been supervised by Annexure 3 under Section II-B of the Master Circular for compliance with the provisions of SEBI (LODR), 2015 by listed entities in case of equity listed entities and Annexure VII-A under Chapter VII of the Master Circular for listing obligations and disclosure requirements for Non-convertible Securities, Securitized Debt Instruments and/or Commercial Paper in case of HVDLEs. The issue arises from the practice adopted by HVDLEs in the instant case, where filings made on the website of the stock exchange have been made in PDF format thereby affecting the readability and clause-wise compliance monitoring. Unlike the above-mentioned proposals which aim at bringing about relaxations for HVDLEs, this particular proposal tightens the regime by binding the XBRL format that is consistent with what is being filed by equity listed entities, for the report to be submitted on a quarterly basis.

VKCo Comments: This proposal is with an objective to align and standardize the filing of quarterly CG compliance report for bringing parity as in the case of equity listed entities.

Voluntary submission of Business Responsibility and Sustainability Report (BRSR):

This proposal originates from SEBI’s endeavour to inculcate good CG practices in HVDLEs, to be at par with equity listed entities. It is supported by Regulation 34(2)(f) which requires the top 1,000 listed entities (based on market capitalization) to include a BRSR in their annual report. It is pertinent to note in this respect that publishing of BRSR by HVDLEs is voluntary and not a mandatory requirement unless such an HVDLE also satisfies the criteria of the above-stated regulation.

VKCo Comments: The inclusion of a voluntary provision in the legislation with respect to a comprehensive report like BRSR is not likely to be submitted given the huge details under the BRSR. However, an opportunity to submit BRSR can be a game changer for an HVDLE from the perspective of being able to raise funds based on its reporting standards in this regard.

Concluding Remarks:

The proposal under the CP provides hope for a breather when it comes to compliance with CG norms and at the same time introduces certain new requirements to maintain uniformity whether it is for the XBRL filing or inclusion of directorship and committee membership as well as chairmanship in an HVDLE for the max no. of such positions. It will also be interesting to see what is rolled out under the new chapter for HVDLEs as well as the fine print of provisions as far as RPT controls are concerned.

Recently, SEBI rolled out stricter corporate governance (CG) norms for entities having its non-convertible debt security listed and having an outstanding value of Rs. 500 crore and above as on March 31, 2021 [referred as High Value Debt Listed Entities (HVLDEs)[1]]. One of CG norms applicable is to comply with the requirements that apply with respect to Related Party Transactions (RPTs). The approval requirement, stipulated for material RPTs mandates approval of shareholders and prohibits related parties to vote to approve the transaction. The intent of the law is to ensure approval by shareholders who are not related parties. As HVDLEs include private companies and closely held public companies that must have listed its debentures, this requirement resulted in an impossibility and deadlock. On being approached by one such entity, SEBI suggested a temporary carve out by advising ‘to explain’ and ‘not comply’.

On December 16, 2021, SEBI issued an informal guidance[2] under SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (Listing Regulations) relating to the applicability of CG requirements on HVLDEs.

Pursuant to the fifth amendment of the Listing Regulations, notified on September 07, 2021[3], the applicability of CG norms were extended to entities with non-convertible debt securities listed and the outstanding amount being Rs. 500 cr or more. While the provisions became applicable from September 07, 2021 the same was implemented on a ‘comply or explain’ basis until March 31, 2023. Accordingly, an HVDLE is expected to endeavour to comply with the provisions and achieve full compliance by March 31, 2023. In case the HVDLE is not able to achieve full compliance with the provisions, till such time, it shall explain the reasons for such non-compliance/ partial compliance and the steps initiated to achieve full compliance in the quarterly compliance report filed under clause (a), sub-regulation (2) of regulation 27 of these regulations.

RPTs by HVDLEs

An HVDLE, that were not equity listed, were only required to comply with Companies Act, 2013 (CA, 2013) requirements for the purpose of transacting with related parties. While CA, 2013 also provides for similar restrictions, it provides a carve out in case of closely held companies. The restriction of related parties not to vote in favor of a resolution, does not apply where ninety per cent. or more members, in number, are relatives of promoters or are related parties. However, there is no such carve out provided in Regulation 23 (4) of the Listing Regulations.

The present case

India Infradebt Limited (IIL), a joint venture company and an HVDLE, realised about this deadlock situation as all the shareholders, being venturers, were related parties in terms of Section 2 (76) of CA, 2013. Therefore, it approached SEBI seeking informal guidance for the procedure to be followed for obtaining shareholders’ approval in case of material RPTs.

SEBI provided a stop-gap solution and stated that in view of the ‘inherent difficulty’ by IIL in getting shareholders’ approval for material RPTs, it may choose to explain the reason for not complying.

Conclusion

A pertinent question that arises from the informal guidance and which has not been dealt with, is whether the HVLDEs that are closely held companies, be expected to be on the same pedestal as that of equity listed entities. Even if they are supposed to be, it cannot continue to explain for not complying as from April 1, 2023 these provisions will become mandatory and violation of the same will attract penalties from the stock exchanges.

Further, the RPT provision has been drastically amended and becomes effective from April 1, 2022[4]. The scope of related party and RPT has been widened and the threshold for material RPT has also been amended to impose a numerical threshold of Rs. 1000 crore along with the existing threshold of 10% of annual consolidated turnover. Additionally, the requirement to seek shareholder’s approval will be ‘prior’ to breaching the materiality thresholds.

Therefore, several HVDLEs may be required to seek shareholder’s approval for prospective transactions. SEBI should consider incorporating a carve out similar to that provided under CA, 2013 for closely held HVDLEs in Regulation 23 (4) of the Listing Regulations in order to resolve the issue permanently.