SEBI notifies amendments to all modes of Buy-back

– Sanya Agrawal, Executive | executive@vinodkothari.com

Loading…

Loading…

– Sanya Agrawal, Executive | executive@vinodkothari.com

Loading…

– Promotes tender offer while holding back significant corporate slimming proposals

– Payal Agarwal, Deputy Manager (payal@vinodkothari.com)

Distribution of profits to shareholders may take up various forms, as also discussed in Distribution of accumulated profits to shareholders. One such manner of distribution is “buying back” the existing securities of the company from the shareholders. In addition to the provisions of section 68 of the Companies Act, 2013[1] (“the Act”), the provisions of SEBI (Buyback of Securities) Regulations, 2018 (“Buy-back Regulations”) are also applicable in case of buy-back of shares or other specified securities of a listed company. The Buy-back Regulations repealed the erstwhile Buyback Regulations, 1998 and our article on the same can be read at SEBI amends Buyback Regulations: -Aligning and re-framing with other laws. SEBI had brought a consultation paper on review of existing Buy-back Regulations (“Consultation Paper”) on 16th November, 2022. The Consultation Paper, based on a report of a sub-group headed by Mr Keki Mistry, makes some very significant recommendations for reform of the existing buy-back regime, including some statutory amendments too. On the basis of the suggestions received on the Consultation Paper, SEBI, in its meeting held on 20th December, 2022 (“Board Meeting”) approved amendments to the Buy-back Regulations.

The amendments have been notified on 7th February, 2023 vide SEBI (Buy-back of Securities) (Amendment) Regulations, 2023 (“Amendment Regulations”), and are applicable w.e.f. 30th day from publication in Official Gazette, being 9th March, 2023.

Various amendments have been notified to the existing Buy-back Regulations with the intent of removing the inefficiency of certain modes of buy-back, streamlining the timelines, assisting efficient price-discovery mechanisms and defying the prospects of manipulative market practices.

While most of the proposals under the Consultation Paper have been made part of the Buy-back Regulations through the Amendment Regulations, certain proposals such as scaling up the extent of permitted limits of buy-back or proposals on the tax treatment etc have been dropped currently, since the same may also require consent of other regulatory authorities such as MCA, MoF etc. and amendments to other related laws. The agenda note of the Board Meeting (“Agenda Note”) also specifies that SEBI will engage with MCA and MoF respectively to seek their views on such proposals. In this write-up, we attempt to put up an analysis of the amended regulatory framework with respect to the buy-back of securities by listed companies.

Reg 4(iv) of the Buy-back Regulations specifies various methods for buyback of securities being –

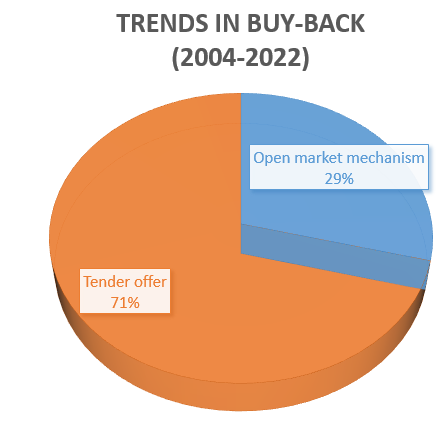

The market practice, as can be understood from the data available on the website of SEBI, tender offer is by far the most preferred method for buy-back of securities[2]. The same derives its preference from the fact that the same provides a chance of equal participation by all shareholders, since the repurchase takes place on a proportionate basis from all those shareholders who tender their shares for buyback.

On the other hand, open market buy-back, especially through stock exchanges, has been criticized due to several limitations. The Consultation Paper also discussed the existing limitations in the method and proposed gradual removal of the process, by way of a proposed “glide path”.

The existing book building process through open market mechanism is also a rarely used method, and a revision to the entire process of the same was also proposed vide the Consultation Paper.

The method of buy-back through purchase from odd lot holders has been omitted from the Buy-back Regulations in view of the absence of any practical relevance of the same.

The method for buy-back of securities from open market through stock exchanges suffers various limitations, for instance –

In view of the inherent limitations of the mechanism, it was proposed to reduce the maximum limit of buy-back and the offer period for buyback through such offer, in a phased manner, such that the same can be completely discontinued with effect from 1st April, 2025. The phases of the “glide path” is as follows –

| Parameter | Current thresholds | w.e.f April 01, 2023 | w.e.f April 01, 2024 | w.e.f April 01, 2025 |

| Maximum Limit | 15% | 10% | 5% | 0% |

| Time Period for completion of buyback offer | 6 months | 66 working days | 22 working days | NA |

One may doubt the possibility of availing the mode for buy-back through stock exchange in the event the closing of such offer extends to a period on or after 1st April, 2025. To this end, it has been expressly clarified that such option will still be available where the buy-back offer has been opened or before 31st March, 2025. Therefore, it may be said that the maximum thresholds and time limits for buy-back through stock exchanges will be applicable on the basis of provisions as on the opening of the offer, and not the closing.

Apart from the gradual closure of the method, some other amendments have also been notified till the time the same is existent.

The other changes proposed to the aforesaid method are as follows –

The Amendment Regulations contain various provisions pertaining to the buy-back through tender offer. These are mostly aimed towards increasing the efficiency of the process and providing operational convenience to listed companies, while also providing for a time-efficient process for the same.

The existing Buy-back Regulations does not facilitate the possibility of any subsequent revision in the buy-back price, than what is proposed in the explanatory statement at the time of obtaining shareholders’ approval. However, there is a time gap between the board/ shareholders’ approval and the actual commencement of buy-back offer. This time gap may demand some revision in the buy-back price in order to retain the attractiveness of the offer.

Therefore, clause (via) has been inserted under Reg 5 of the Buy-back Regulations to provide flexibility to the board of directors to make upward revision in the buy-back price and accordingly, decrease the maximum number of securities proposed to be bought back, till one working day prior to the opening of the buy-back offer, subject to the aggregate buy-back size remaining unchanged.

The extant Buy-back Regulations required review of the draft letter of offer by SEBI. The comments are required to be incorporated by the merchant bankers in the final letter of offer. This being a time-consuming process, the said requirement has been removed.

The Amendment Regulations require a company to file the final letter of offer to SEBI through a merchant banker not being an associate of the company. Further, the merchant banker is required to provide a certification with respect to the compliance with the Buy-back Regulations and the contents of the letter of offer are in conformity with the requirements of the Buy-back Regulations.

The explanation to clause (ii) of Reg 9 of the Buy-back Regulations has been amended to provide more clarity on the mode of dispatch of letter of offer to the shareholders of the company. The Amendment Regulations require that the public announcement shall disclose that the dispatch of letter of offer shall be made in electronic mode, within 2 working days from the record date. Physical copies of the same shall also be provided to the shareholder who requests for the same.

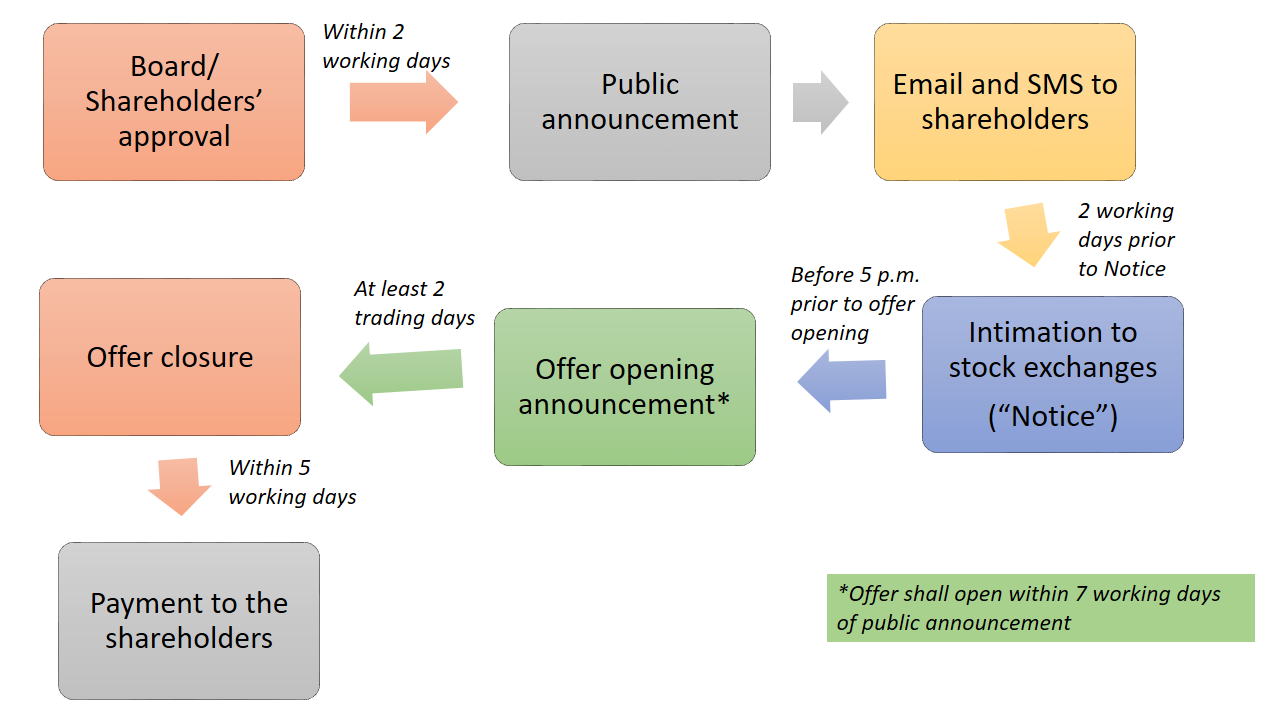

The Amendment Regulations also provide for certain changes in the existing timelines for buy-back through tender offer. The same is aimed at accelerating the entire process of buy-back through tender offer. This includes the following –

Post the Amendment Regulations coming into force, the timelines for the process of buy-back through tender offer will stand amended in the following manner (refer pg. 28 of the Agenda Note).

| Broad activity | Existing timelines | Amended timelines (in working days) |

| Public announcement | T | T |

| Submission of draft offer letter to SEBI | T+7 | NA |

| Receipt of observations from SEBI (tentative) | T+14 | NA |

| Record date | R | R = T+9 (7 working days in advance excluding date of intimation and record date) |

| Last day for dispatch of offer letter to shareholders | T+19 | R+2 = T+11 |

| Opening of offer | T+24 | R+4 = T+13 |

| Closure of offer | T+34 | T+18 (offer opening + 5) |

| Last day for payment of consideration to shareholders | T+41 | T+23 |

While the Consultation Paper contained proposals for increasing the limits of the maximum permissible buy-back size as well as number of times such an offer can be made, the same does not form part of the currently notified Amendment Regulations.

However, certain amendments have been notified for the sake of clarity in the existing Buy-back Regulations –

As discussed above, buy-back through the book building process is currently a rarely used process. The Agenda Note (refer pg. 24) also states that except for one company in the year 1988, no other company has undertaken buy-back through this route till date. In view of the same, a revised framework has been proposed in relation to buy-back through the book building process. Following the recommendations laid down in the Consultation Paper, the Amendment Regulations provide a revised mechanism for effecting open market buy-back through the book building process. The major revisions include –

Under the extant Buy-back Regulations, the buy-back consideration is required to be deposited in the escrow account either in the form of cash or through permitted forms other than cash, on or before the opening of the offer. The same has been amended to require a company to make such a deposit within two working days of the public announcement.

Certain additional forms/modes of deposit have also been prescribed to provide flexibility to the company to commit its security for performance of its obligations towards the buy-back. The amended sub-clause (c) of clause (xi) of Reg 9 reads as –

“(i)cash deposited with cash including bank deposits deposited with any scheduled commercial bank or

(ii)bank guarantee issued in favour of the merchant banker by any scheduled commercial bank, or

(iii)deposit of frequently traded and freely transferable equity shares or other freely transferable securities , or

(iiia) government securities, or

(iiib) units of mutual funds invested in gilt funds and overnight schemes, or

(iv)a combination of above”

For such part of escrow account that is held in a form other than cash, the company is also required to “deposit with a scheduled commercial bank, in cash, a sum of not less than two and half per cent of the total amount earmarked for buyback as specified in the resolution of the Board of Directors or the special resolution, as the case may be, as security for the fulfillment of its obligations under the regulations”. Prior to the Amendment Regulations, the same read as “one percent of the total consideration payable”.

In view of the various post buy-back compliances applicable on a company, the minimum required validity of the bank guarantee has been extended to the LATER of –

The reference of days, wherever it appears, have been replaced with “working days” to bring about a consistency and streamline the timelines. Further, the timelines for various actionables such as public announcement, deposit in escrow account etc have been amended in alignment of the same with the existing timelines under the SEBI (Substantial Acquisition of Securities and Takeover Regulations), 2011, SEBI (Delisting of Equity Shares) Regulations, 2021 etc.

The extant Regulations required the public announcement for buy-back be published in at least one English National Daily, one Hindi National Daily and one Regional language daily, all with wide circulation at the place where the Registered Office of the company is situated. Further, the same was required to be submitted to SEBI, through the merchant banker.

Along with the newspaper publications of the public announcement, the Amendment Regulations require the filing of the same by the Company directly to the SEBI as well as the stock exchanges on which its shares or other specified securities are listed. The same will also be published on the website of the stock exchanges, the company as well as the merchant banker.

The Amendment Regulations have the impact of dispensing with the existing requirement of submission of physical documents with SEBI, and substituting the same with the requirement of filing in electronic form digitally signed by the Company Secretary or the person authorized by the board of the company undertaking buy-back.

Where the buy-back offer of a company requires approval from its lenders, the same shall be specified in the public announcement, offer letter and explanatory statement to the shareholders. Prior written consent of the lenders is also required to be obtained in case of breach of any covenant with such lender.

The reference to the Statutory Auditor has been replaced with Secretarial Auditor for ensuring the following compliances –

The same has been done in view of the fact that the secretarial auditor is required to ensure compliance in terms of SEBI regulations and other allied laws, and therefore, would be better placed to ensure post buy-back compliances.

The existing Buy-back Regulations require at least 50% of the earmarked buy-back amount (kept in a separate escrow account), to be actually utilized for the buy-back offer, failure of which attracts forfeiture of a percentage of the escrow amount. The forfeiture is subject to certain exemptions such as for instances where the buy-back offer becomes unattractive to the shareholders due to price, or otherwise, for any other reason not in the control of the company such as non-receipt of sufficient interest for buy-back from the existing shareholders.

In view of the foregoing exemptions, the minimum utilization amount has been increased to 75% of the earmarked amount, instead of the existing 50% threshold. Further, on the Amendment Regulations becoming effective, the company shall be required to ensure that at least 40% of the earmarked amount is utilized within the initial half of the specified duration.

The same is applicable to open market buy-back offers either through stock exchange or book-building.

The Amendment Regulations are mostly inclined towards providing a more efficient process for buy-back of securities of listed companies and do away with the existing loopholes in the same. It seeks to provide convenience to the listed companies on one hand, while ensuring no compromise with the stakeholders’, especially the public shareholders’ interests on the other. Some of the most welcoming proposals under the Consultation Paper have currently been dropped, particularly, the proposal for increase in limits of maximum buy-back size, which, if implemented, would have resulted in many matured companies to distribute their surplus funds effectively to the existing shareholders and scale down appropriately. The same is pending consultation with the respective ministries.

[1] The provisions of allied rule (Rule 17 of the Share Capital and Debentures Rules) does not apply to listed companies, except pertaining to the filing of declaration of solvency and return of buy-back.

[2] Buy-back from the open market through stock exchange stands at 519 as opposed to 1269 instances of buy-back through tender offer. Source: SEBI website