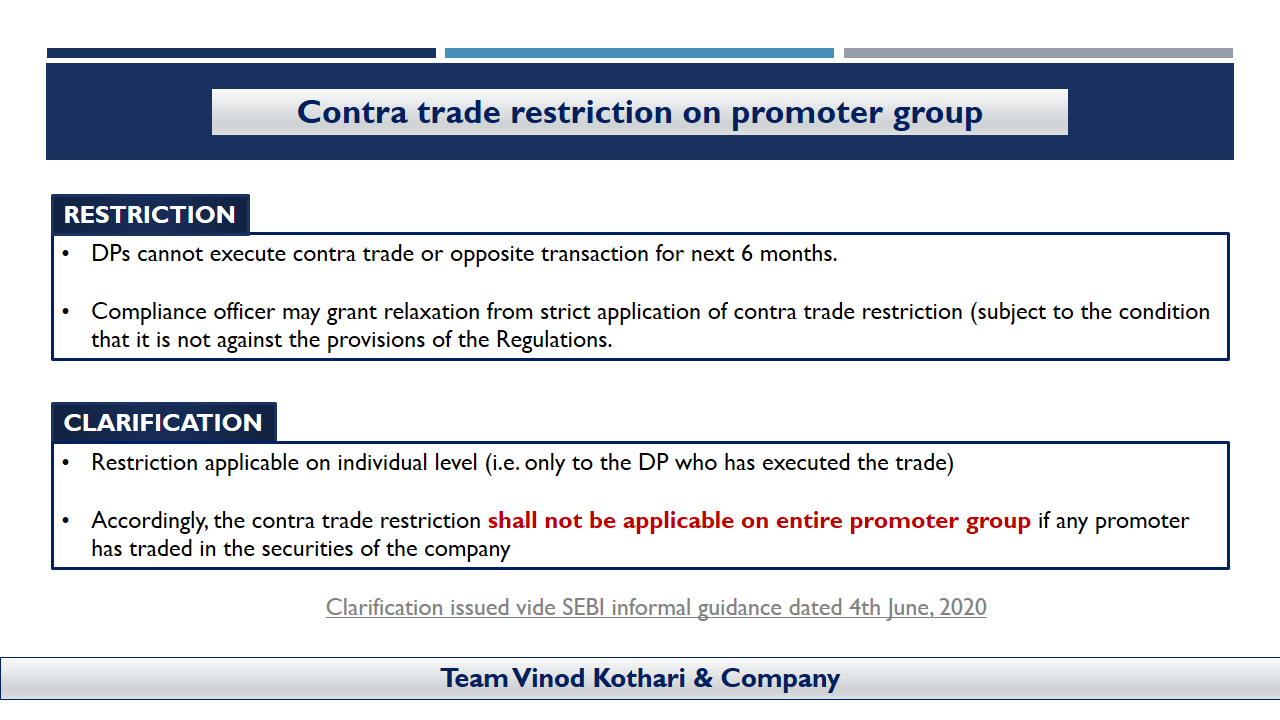

Contra trade restrictions on promoter group

Link to Informal Guidance by SEBI – https://www.sebi.gov.in/sebi_data/commondocs/sep-2020/SEBI%20let%20Raghav%20IG_p.pdf

Link to Informal Guidance by SEBI – https://www.sebi.gov.in/sebi_data/commondocs/sep-2020/SEBI%20let%20Raghav%20IG_p.pdf

Physical disclosures to continue in certain cases

Updated as on September 23, 2020, June 16, 2021, August 25, 2021 and March 07, 2022

– Team Vinod Kothari and Company

SEBI, in its Board meeting dated June 25, 2020, discussed and approved necessary amendments[1] in SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’) that were notified vide gazette notification[2] dated July 17, 2020. One of the amendments made pertained to insertion of enabling power to prescribe format for continual disclosures under PIT Regulations in order to mandate System Driven Disclosures (‘SDD’).

Earlier, in December 2015[3], SEBI had notified SDD in the first phase pertaining to acquisition/ disposal of equity shares by promoters/ promoter group based on specified thresholds under the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (‘SAST Regulations’) and PIT Regulations and pledge of equity shares by promoters/promoter group under the SAST Regulations. Thereafter, in May 2018[4] next phase of SDD was implemented for disclosure under Reg. 29(1) and 29(2) of SAST Regulations by non-promoters and continual disclosures under Reg. 7(2) of PIT Regulations for directors and employees. Refer Figure 1: Flow of events in relation to SDD.

Thereafter, SEBI vide circular[5] dated September 09, 2020, superseded the aforesaid circulars dated December 01, 2015, December 21, 2016 and May 28, 2018 with respect to implementation of SDDs under PIT Regulations and mandated SDD for trading in equity shares and equity derivative instruments i.e. Futures and Options of the listed company (wherever applicable) by the entities. Read more →

Youtube Video – https://www.youtube.com/watch?v=5DNOJDB9o0k

– Time given till last day of FY 2020-2021

-updated as on 3rd December, 2020

Pammy Jaiswal | Partner | Vinod Kothari and Company

Physical transfers of specified securities were prohibited w.e.f. 1st April, 2019 by virtue of amendment made in Reg. 40 vide SEBI LODR (Fourth Amendment) Regulations, 2018[1]. Listed entities were not allowed to process the transfer request for equity shares where shareholders held the same in physical form with effect from 1st April, 2019.

In order to address the issue of transfer requests filed prior to April 1, 2019 but rejected due to deficiency in documents etc, SEBI issued a press release on 27th March, 2019[2] permitting the shareholders, who had already lodged their transfer request before 1st April, 2019 and where the request was returned/ rejected due to deficiency in paperwork, to re-lodge their transfer request with the listed companies.

However, there was no specific deadline provided for re-lodgement of such requests. SEBI vide its Circular[3] dated 7th September, 2020 has provided a cut-off date of 31st March, 2021 for re-lodging the transfer request rejected/ returned earlier.

This Circular is only applicable in such cases where the transfer request for physical shares had been lodged prior to 1st April, 2019 and were rejected/ returned on grounds of deficiency in documents.

While the language of the Circular states – “Further, the shares that are re-lodged for transfer (including those request that are pending with the listed company / RTA, as on date), this cannot be interpreted to mean the inclusion of fresh transfer request post 1st April, 2019 since the same was prohibited by law itself.

Another important clarification that the Circular provides is that on effecting the transfer of such physical shares the transferee will be issued shares in demat mode only. This means that the transferee will have to have a demat account in order to give effect to the transfer, failing which the transfer will not be processed by the listed company.

For the purpose of processing the transfer request pursuant to the re-lodgement by the shareholders, the RTAs will be guided by the SEBI circular[4] dated 6th November, 2018 to follow the procedure provided therein. The said circular provides for the standard procedures including the document requirement for processing the transfer request of physical securities.

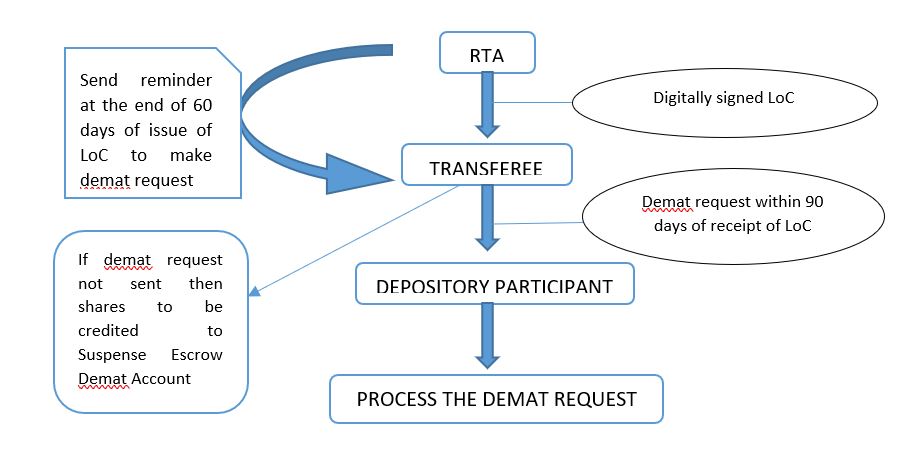

After processing the transfer of physical shares in accordance with the procedure mentioned above, SEBI on 2nd December, 2020 has issued the operational guidelines to credit the transferred shares in the demat account of the investor.

The guidelines involve issuing a Letter of Confirmation (LoC) in a prescribed format by the RTA on processing with the transfer request either physically or by an email to the investor (transferee). On receipt of LoC, the investor has been given a time of 90 days to send the demat request to the Depository Participant failing which, the shares are credited to Suspense Escrow Demat Account of the Company.

Further, the fact that the shares are subject to lock-in for a period of 6 months from the date of registration of transfer in terms of the SEBI circular dated 6th November, 2018, will have to be intimated by the RTA to the Depository while approving the demat request.

Enhanced due diligence for dematerialization of physical shares

For augmenting the integrity of the system in processing of dematerialization request in respect of physical shares, SEBI issued a circular on 5th November, 2019[5]. This requires the listed companies to share the static database (name of shareholders, folio numbers, certificate numbers, distinctive numbers and PAN etc.) of those shareholders who are holding physical shares.

The intent is to cross check the systems for validating dematerialization request of such shareholders.

By setting the deadline to re-lodge the transfer request, SEBI has put an end to allow the pending transfer request to be alive for an indefinite time period. In cases where the shareholder fails to re-lodge the transfer request on or before 31st March, 2021, such transfers will be deemed cancelled and will not be allowed to be transferred unless shares are dematerialised.

[1]https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/jun-2018/1528952919510.pdf#page=1&zoom=page-width,-16,792

[2] https://www.sebi.gov.in/media/press-releases/mar-2019/transfer-of-securities-held-in-physical-mode-clarification_42503.html

[3]https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/sep-2020/1599474275403.pdf#page=1&zoom=page-width,-15,842

[4] https://www.sebi.gov.in/web/?file=https://www.sebi.gov.in/sebi_data/attachdocs/nov-2018/1541503823022.pdf#page=1&zoom=page-width,-16,792

[5] https://www.sebi.gov.in/legal/circulars/nov-2019/enhanced-due-diligence-for-dematerialization-of-physical-securities_44863.html

Other reading materials on the similar topic:

Email id for further queries: corplaw@vinodkotahri.com

Our website: www.vinodkothari.com

Our Youtube Channel: https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

SEBI during FY 2018-19 conducted an investigation into the trading activities in illiquid stock options at BSE for a period of 1st April, 2014 to 30th September, 2015. As a result of the investigation, SEBI observed that there were large scale reversal trades executed in stock options by various entities.

Reversal trades refers to trading i.e. buying and selling of stocks from and to the same counterparty during a day which creates artificial trade units of stocks in the question. In such trades one party suffer losses and buy stock at higher rate and within seconds execute reversal trade and sell these stocks to the same counter party at a relatively lower rate thereby resulting to gains for other party. Supreme Court in the appeal no. 1969 dated 8th February, 2018 quoted:

“Trading is always with the aim to make profits. But if one party consistently makes loss and that too in pre-planned and rapid reverse trades, it is not genuine, it is an unfair trade practice.”

Such kind of transactions executed by entities were considered non-genuine by SEBI as they were not executed with the basic trading rationale. These transactions were prohibited pursuant to the provisions of section 4(2) of SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003 (‘PFUTP Regulations’) which provides:

“(2) Dealing in securities shall be deemed to be a fraudulent or an unfair trade practice if it involves fraud and may include all or any of the following, namely: —

(a) indulging in an act which creates false or misleading appearance of trading in the securities market;”

Pursuant to such restriction under the PFUTP Regulations, SEBI issued show cause notices to various entities (approximately 14000 entities) demanding justification for executing reversal trades at a loss. Entities who were involved in executing such trades were liable for penalty under section 15J of the SEBI Act. Generally, SEBI has levied a fine of approximately Rs. 5 lakhs on entities i.e. the minimum under section 15J of SEBI Act, however, the parameter of determination of fine was subjective and hence even higher fine has been levied to some entities.

SEBI was penalising entities for non-genuinely trading in illiquid stock options through price manipulation under the PFUTP Regulations and SEBI Act. However, tax evasion with respect to such trading activities were to be separately investigated and penalised by IT Authorities. Hence, most entities were contesting the SEBI order with higher authorities to avoid notice/regulatory action from the IT Authorities.

The Hon’ble SAT vide its order dated 14th October, 2019 in the matter of R S Ispat Ltd vs SEBI directed:

“We are adjourning this matter today, so that SEBI may consider holding a Lok Adalat or adopting other alternative dispute resolution process with regard to the illiquid stock options”

Hence, to settle the proceedings initiated for such entities, SEBI introduced a scheme to settle the matter.

Regulation 26 of SEBI (Settlement Proceedings) Regulations, 2018, empowers SEBI to specify settlement schemes as and when desirable for defaults conducted by entities. SEBI for the purpose of reducing the administrative burden of pending proceedings relating to trading in illiquid stock options, issued a public notice on 27th July, 2020 for introduction of Settlement Scheme, 2020.

Pursuant to the scheme a one-time settlement opportunity is being provided to entities involved in dealing of illiquid stock options during the period from 1st April, 2014 to 30th September, 2015. The validity of the scheme is for a period ranging from 1st August, 2020 to 31st October, 2020.

The scheme provides an indicative criteria for determining the settlement amount on the basis of:

Further, uniform consolidated settlement factor of 0.55 shall be applied to calculate the net settlement amount payable by entities. For the purpose of determination, SEBI has introduced a separate web page where settlement amount for the purpose of such orders can be calculated. This can be accessed at Link

| Process of determination of settlement amount | ||

| 1. | Company has to provide two information:

a) Category of payment i.e. for order or settlement b) PAN details of the entity |

|

| 2. | The following details gets auto filed by providing PAN details: | |

| i) Name of the entity | ||

| ii) Entity type | ||

| iii) Number of contracts reversed | ||

| iv) Number of non-genuine trades | ||

| v) Artificial volume of trades | ||

| 3. | The settlement amount gets automatically calculated. The payment amount is segregated as follows: | |

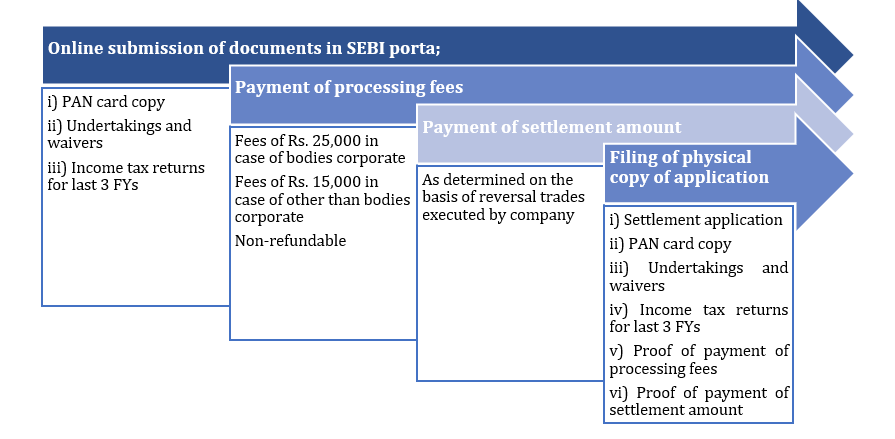

| a) Settlement amount (as calculated using the 0.55 factor) | b) Registration fees

For bodies corporate: Rs. 25,000 For individuals: Rs. 15,000 |

|

| 5. | Mandatory attachments:

1. Income tax returns for last 3 years 2. Copy of PAN card of the entity/individual 3. Undertaking and waivers as required under the SEBI (Settlement Proceedings) Regulations, 2018 |

|

| 5. | Payment process:

For the purpose of making payment under the settlement scheme, the entity has to withdraw any pending proceeding in the said matter. After withdrawal, entities can use this web page for payment of settlement amount. |

|

The settlement amount is directly proportionate to the artificial volume of trades executed by the entities. We have obtained data of 15 entities on sample basis for analysis of settlement amount. The same is represented below:

| Sl.No. | No. of contracts reversed | No. of non-genuine trades executed

|

Artificial volume of trades | Settlement amount |

| 1. | 107 | 970 | 7,97,21,572 | 39,77,500 |

| 2. | 85 | 750 | 2,76,68,000 | 35,12,500 |

| 3. | 21 | 396 | 2,00,25,000 | 25,72,500 |

| 4. | 83 | 492 | 2,75,50,000 | 33,57,500 |

| 5. | 210 | 512 | 1,21,77,000 | 39,77,500 |

| 6. | 165 | 612 | 2,55,25,750 | 39,77,500 |

| 7. | 1672 | 4968 | 30,70,27,560 | 83,17,500 |

| 8. | 191 | 526 | 2,91,34,000 | 39,77,500 |

| 9. | 12 | 92 | 2,79,61,000 | 21,17,500 |

| 10. | 252 | 666 | 7,17,69,750 | 42,87,500 |

| 11. | 14 | 83 | 1,22,92,500 | 19,62,500 |

| 12. | 682 | 1646 | 7,16,45,000 | 50,62,500 |

| 13. | 9 | 194 | 81,29,000 | 21,07,500 |

| 14. | 14 | 116 | 1,25,98,000 | 21,07,500 |

| 15. | 61 | 332 | 3,37,92,000 | 30,47,500 |

Hence, basis the aforesaid table, we understand that higher the artificial trades executed, the higher will be the settlement amount. However, the point of focus here is where SEBI has levied fine of approximately Rs. 5 lakhs on entities, why will entities pay a higher settlement amount then the actual fine. Further, the whole intent of settling a proceeding is to settle it at a lower cost than actual fine. Here, the fine ranges around Rs. 5 lakhs, however, the settlement amount ranges from Rs. 20 lakhs and may go upto Rs, 83 lakhs or even higher.

As regards penal provisions under IT provisions are concerned, the details of trading in illiquid stock options is linked to the PAN details of the entity. Further, the portal also requires to attach the ITR of last three years of the entity.

In this regard, whether the intent of the settlement proceeding is also to channelize information and link the proceedings with IT department, is still unknown. Further, the fate of intention of entities to delay/waive the IT proceedings by either challenging the SEBI order in higher court or settling the proceedings shall be seen only when IT departments start sending letters to such entities.

Generally, settlement refers to neither admitting nor denying any non-compliance. Therefore, entities opting for settlement scheme may have a better chance before the IT department. However, whether this can also safeguard entities them from being penalised by the IT authorities is uncertain.

The entities who opt for settlement scheme has to pay the settlement amount through the portal after withdrawing any pending proceedings. As regards, entities which do not opt for such schemes, the proceedings, as is, shall continue.

Our presentation can be viewed here: https://www.youtube.com/watch?v=CK6QOm4k8Rw

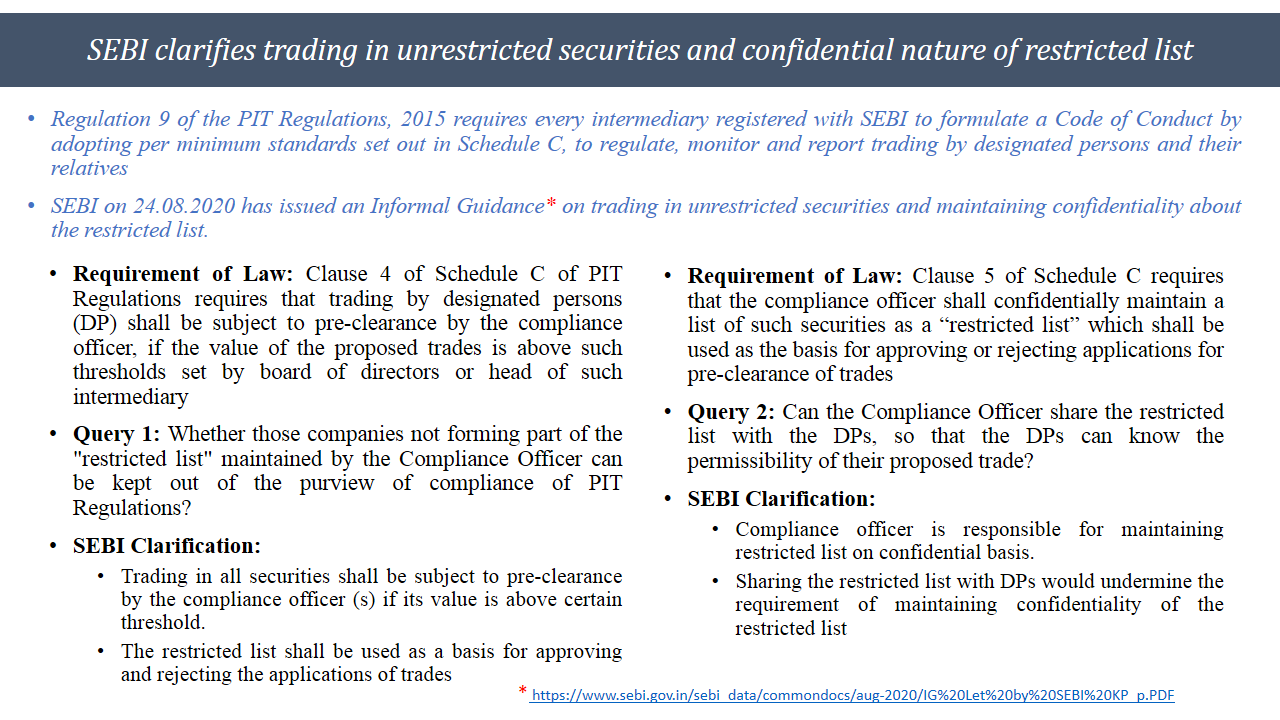

Link to Informal Guidance – https://www.sebi.gov.in/sebi_data/commondocs/aug-2020/IG%20Let%20by%20SEBI%20KP_p.PDF

– Amendment leads to ambiguity

By Megha Saraf

Manager | Corporate Law Division

The world has taken the hit due to the outbreak of the COVID-19 pandemic. The research institutes over the globe have been trying day and night to develop a suitable vaccine to fight against the novel COVID-19 pandemic. Further, various companies or institutes in the country which have also shown positive results towards the development of vaccines and have claimed the success in it by end of the year 2021. Naturally, it is not only large number of human resource that is essential but also a significant proportion of money to produce results. While the intent of corporate social responsibility (CSR) is to make the profit making companies to spend a specific portion for the society, various stakeholders have raised a question on whether such expenditure on the research and development (‘R&D’) for producing vaccines or medical devices should qualify as a CSR expenditure or not? Also, whether the same shall qualify even if it is in the normal course of business of such a company?

The answer to both the questions is in affirmative after the Ministry of Corporate Affairs (“MCA”) issued two Notifications[1][2] dated 24th August, 2020, amending the Companies (Corporate Social Responsibility Policy) Rules, 2014 (‘CSR Rules’). In light of the ongoing impact of the COVID-19 pandemic, the said Notifications have brought in two amendments:

The Article is a brief snapshot of the amendments.