Does new CSR Rules suggest activities in “normal course of business” to be covered under CSR?

– Amendment leads to ambiguity

By Megha Saraf

Manager | Corporate Law Division

The world has taken the hit due to the outbreak of the COVID-19 pandemic. The research institutes over the globe have been trying day and night to develop a suitable vaccine to fight against the novel COVID-19 pandemic. Further, various companies or institutes in the country which have also shown positive results towards the development of vaccines and have claimed the success in it by end of the year 2021. Naturally, it is not only large number of human resource that is essential but also a significant proportion of money to produce results. While the intent of corporate social responsibility (CSR) is to make the profit making companies to spend a specific portion for the society, various stakeholders have raised a question on whether such expenditure on the research and development (‘R&D’) for producing vaccines or medical devices should qualify as a CSR expenditure or not? Also, whether the same shall qualify even if it is in the normal course of business of such a company?

The answer to both the questions is in affirmative after the Ministry of Corporate Affairs (“MCA”) issued two Notifications[1][2] dated 24th August, 2020, amending the Companies (Corporate Social Responsibility Policy) Rules, 2014 (‘CSR Rules’). In light of the ongoing impact of the COVID-19 pandemic, the said Notifications have brought in two amendments:

- Bifurcation of clause (ix) under Schedule VII;

- Changes under the CSR Rules.

The Article is a brief snapshot of the amendments.

MCA widens CSR for defence personnel

Measures for the CAPF and CMPF veterans and dependants now a part of CSR activity

Ankit Vashishth, Executive, Vinod Kothari and Company; corplaw@vinodkothari.com

Introduction

Schedule VII of the Companies Act, 2013 (‘Act’) currently includes measures taken for the armed forces veterans, war widows and their dependants as one of the CSR activities. The Ministry of Corporate Affairs (“MCA”) vide its Notification[1] dated 23rd June, 2020 has included contribution made towards the benefit of Central Armed Police Forces (CAPF) and Central Para Military Forces (CPMF) veterans and their dependents including widows, within the ambit of CSR.

MCA has issued several notifications either to clarify or broaden the ambit of Schedule VII. This Notification is yet another step taken by the MCA for widening the scope of CSR activities to include CAPF and CMPF veterans and their dependants and war widows.

This note tries to provide a quick coverage on the said amendment.

Difference between Armed Forces and CAPF/CPMF

| Armed Forces | CAPF | CPMF |

| The term “armed forces” basically means – Indian Armed Forces which are the military forces of the Republic of India. It comprises three professional uniformed services :

1. The Indian Army 2. The Indian Navy 3. The Indian Air Force |

CAPF (Central Armed Police Force)[2] consists of :

1. Assam Rifles (AR); 2. Border Security Force (BSF); 3. Central Industrial Security Force (CISF); 4. Central Reserve Police Force (CRPF); 5. Indo Tibetan Border Police (ITBP); 6. National Security Guard (NSG); and 7. Sashastra Seema Bal (SSB) |

The nomenclature CAPF will be used uniformly for CPMF as per the Office Memorandum [3]issued by the Ministry of Home Affairs issued on March 18, 2011 |

Current CSR spending pattern and changes expected due to the amendment

The current pattern for CSR spending for armed forces veterans, war widows and their dependants include contributions to several funds like:

- Armed Forces Flag Day Fund (AFFDF)[4]

- Army Wives Welfare Association (AWWA)[5]

- The Army Welfare Fund Battle Casualties[6]

Apart from donating to these funds, companies have also provided financial relief to the martyr’s families and have conducted workshops for the children of war widows as a part of their CSR projects.

Further, in addition to the above, contribution to “National Defence Fund” which is used for the welfare of the members of the Armed Forces (including Para Military Forces) should be eligible for being a CSR activity.

As a result of the enhanced scope for CSR spending for CAPF/ CAMF, contribution to the fund “Bharat Ke Veer Corpus Fund”[7], which was previously not eligible for CSR considering the fact that it specifically benefits CAPF, will now be covered as per the amendment. Accordingly, any contribution to this fund will now qualify as a CSR activity.

High Level Committee on CSR

MCA had constituted[8] a High Level Committee (HLC) on CSR in February, 2015 under the Chairmanship of Secretary (Corporate Affairs) to review the existing CSR framework and formulate a coherent policy on CSR and further make recommendations on strengthening the CSR ecosystem, including monitoring implementation and evaluation of outcomes. Later, the HLC on CSR was re-constituted[9] in November, 2018. The scope of HLC was widened to include recommendation of guidelines for enforcement of CSR provisions. Though the Report discussed on amending Schedule VII in line with promoting sports, senior citizens’ welfare, welfare of differently abled persons, disaster management, and heritage, however, it did not consider widening the clause relating to the scope of armed forces in the Schedule.

Further, as evident from the data given in the HLC Committee Report[10], CSR expenditure made on armed force veterans, war widows/ dependents have seen an upward trend over the years, however it forms a very small proportion of the total CSR expenditure made.

Concluding Remarks

The service spirit of CAPF is no less than that of the Indian Army. Acknowledging this fact MCA has brought this amendment. While all the areas for CSR are extremely important for the overall socio-economic welfare and development, the measures taken for the benefit of veterans and dependants of the armed forces and CAPF/ CPMF is an extremely noble activity.

Link to our other articles:

CSR: A ‘Corporate Social Responsibility’ or a ‘Corporate Social Compulsion’?

Proposed changes in CSR Rules

https://vinodkothari.com/2020/03/proposed-changes-in-csr-rules/

FAQs on Corporate Social Responsibility

https://vinodkothari.com/2019/11/faqs-on-corporate-social-responsibility/

Read our other articles on Corplaw : https://vinodkothari.com/category/corporate-laws/

Link to our Youtube Channel : https://www.youtube.com/channel/UCgzB-ZviIMcuA_1uv6jATbg

[1] http://egazette.nic.in/WriteReadData/2020/220133.pdf

[2] https://www.mha.gov.in/about-us/central-armed-police-forces

[3] Office Memorandum can be viewed here

[4] http://ksb.gov.in/armed-forces-flag-day-fund.htm

[5] https://awwa.org.in/contribution-under-csr-awwa

[6] The Army Welfare Fund Battle Causalities

[7] https://www.bharatkeveer.gov.in/about

[8] https://www.mca.gov.in/Ministry/pdf/General_Circular_01_2015.pdf

[9] https://www.mca.gov.in/Ministry/pdf/OfficeOrderCommitteeOnCorporate_26112018.pdf

[10] https://www.mca.gov.in/Ministry/pdf/CSRHLC_13092019.pdf

Transacting by exception: Listed cos in India give substantive carve outs for RPTs

The article has been published in ICSI – WIRC-E Newsletter (June-July 2020 edition):

Refer page 43 of ICSI – WIRC-E Newsletter

Easing of DRF requirement

-by Smriti Wadehra

(smriti@vinodkothari.com)

-Updated as on 29th September, 2020

Pursuant the proposal of Union Budget of 2019-20, the MCA vide notification dated 16th August, 2019 amended the provisions of Companies (Share Capital and Debentures) Rules, 2014 [1].(You may also read our analysis on the notification at Link to the article) The said amended Rules faced a lot of apprehensions, especially, from the NBFCs as the notification which was initially expected to scrap off the requirement of creation of DRR for publicly issued debentures had on the contrary, rejuvenated a somewhat settled or exempted requirement of creation of debenture redemption fund as per Rule 18(7) for NBFCs as well.

As per the notification, the Ministry imposed the requirement for parking liquid funds, in form of a debenture redemption fund (DRF) to all bond issuers except unlisted NBFCs, irrespective of whether they are covered by the requirement of DRR or not. In this regard, considering the ongoing liquidity crisis in the entire financial system of the Country, parking of liquid funds by NBFCs was an additional hurdle for them.

Creation of DRR is somewhat a liberal requirement than creation of DRF, this is because, where the former is merely an accounting entry, the latter is investing of money out of the Company. Further, the fact the notification dated 16th August, 2019 casted exemption from the former and not from the latter, created confusion amidst companies. The whole intent of amending the Rule was to motivate NBFCs to explore bond markets, however, the requirement of parking liquid funds outside the Company as high as 15% of the amount of debentures of the Company was acting as a deterrent for raising funds by the NBFCs.

Considering the representations received from various NBFCs and the ongoing liquidity crunch in the economy of the Country along with added impact of COVID disruption, the Ministry of Corporate Affairs has amended the provisions of Rule 18 of Companies (Share Capital and Debenture) Rules, 2014 vide notification dated 5th June, 2020 [2]to exempt listed companies coming up with private placement of debt securities from the requirement of creation of DRF.

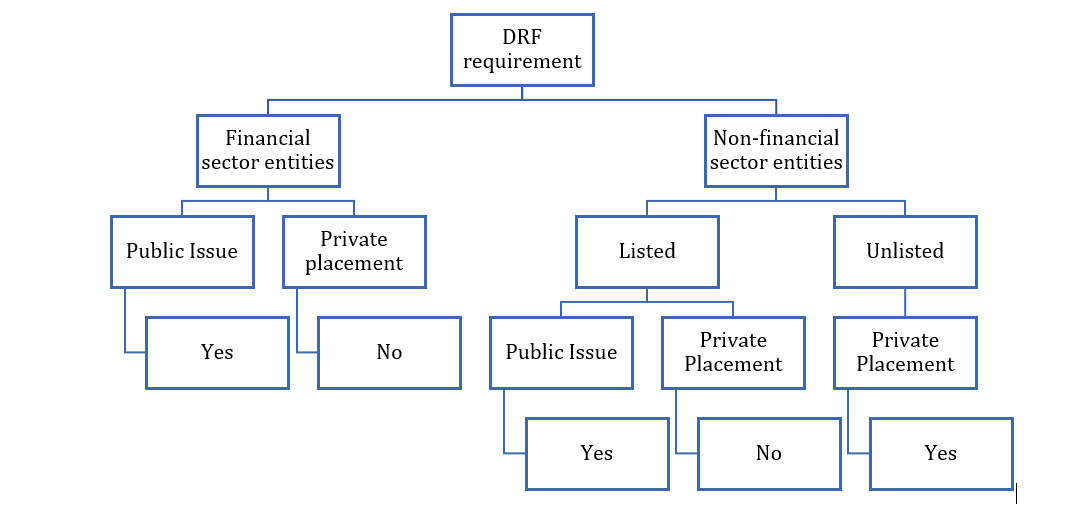

What is DRR and DRF?Section 71(4) read with Rule 18(1)(c) of the Companies (Share Capital and Debentures) Rules, 2014 requires every company issuing redeemable debentures to create a debenture redemption reserve (“referred to as DRR”) of at least 25%/10% (as the case maybe) of outstanding value of debentures for the purpose of redemption of such debentures. Some class of companies as prescribed, has to either deposit, before April 30th each year, in a scheduled bank account, a sum of at least 15% of the amount of its debentures maturing during the year ending on 31st March of next year or invest in one or more securities enlisted in Rule 18(1)(c) of Debenture Rules (‘referred to as DRF’). |

The notification has mainly exempted two class of companies from the requirement of creation of DRF:

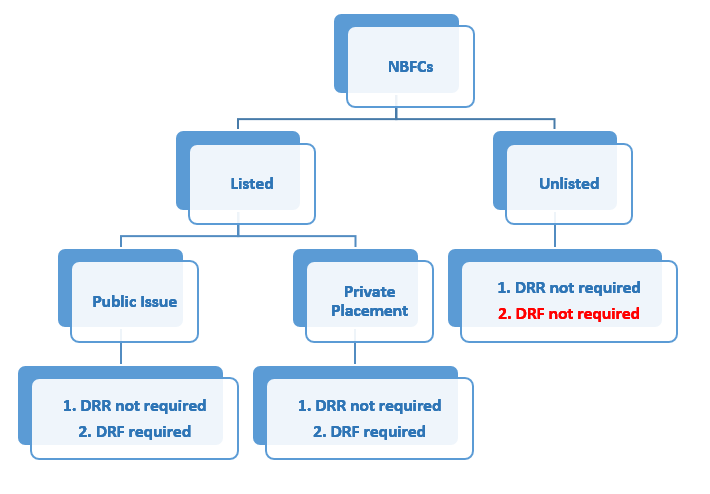

- Listed NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and for Housing Finance Companies registered with National Housing Bank and coming up with issuance of debt securities on private placement basis.

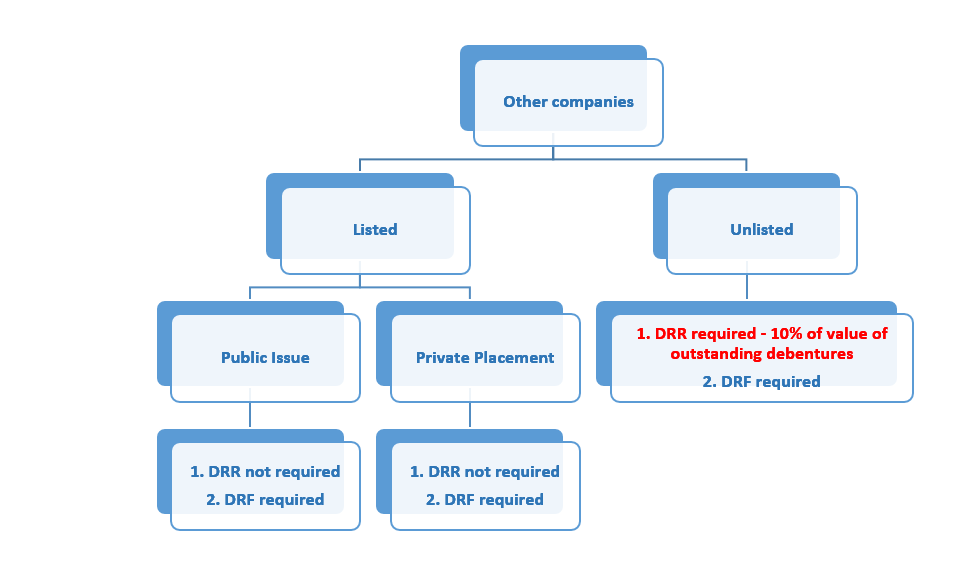

- Other listed companies coming up with issuance of debt securities on private placement basis.

However, the unlisted non-financial sector entities have been left out. In a private placement, the securities are issued to pre-selected investors. Raising debt through private placement is a midway between raising funds through loan and debt issuances to public. Like in case of bilateral loan arrangements, but unlike in case of public issue, the investors get sufficient time to assess the credibility of the issuer in private placements, since the investors are pre-identified.

The intent behind DRF is to protect the interests of the investors, usually when retail investors are involved, with respect to their claims on maturity falling due within a span of 1 year. This is not the case for investors who have invested in privately placed securities, where the investments are made mostly by institutional investors.

Further, companies chose issuance through private placement for allotment of securities privately to pre-identified bunch of persons with less hassle and compliances. Hence, the requirement of parking funds outside the Company frustrates the whole intent.

Further, it is a very common practice to roll-over the bond issuances, hence, it is not that commonly bonds are repaid out of profits; the funds are raised from issuance of another series of securities. This is a corporate treasury function, and it seems very unreasonable to convert this internal treasury function to a statutory requirement.

Though, in our view, the relaxation provided in case of private issuance of debt securities is definitely a relief, especially during this hour of crisis, but we are not clear about the logic behind excluding unlisted non-financial sector entities.

Even though, the financial sector (76%) entities dominate the issuance of corporate bonds, however, the share of the non-financial sector entities (24%) is not insignificant. Therefore, ideally, the exemption in case of private placements should be extended to unlisted non-financial sector entities as well.

A brief analysis of the amendments is presented below:

Practical implication

Pursuant to the MCA notification dated 16th August, 2019, the below mentioned class of companies were required to either deposit or invest atleast 15% of amount of debentures maturing during the year ending on 31st March, 2020 by 30th April, 2020. This has been extended till 31st December, 2020 for this FY 2019-20 by MCA due to the COVID-19 outbreak. However, pursuant to the amendment introduced by MCA notification dated 5th June, 2020 the status of DRF requirement stands as amended as follows:

| Particulars | DRF requirement as MCA circular dated 16th August, 2019 | DRF requirement as per MCA circular dated 5th June, 2020 |

| Listed NBFCs which have issued debt securities by way of public issue | Yes. | Yes. Deposit or invest before 31st December, 2020 |

| Listed NBFCs which have issued debt securities by way of private placement | Yes | Not required as exempted. |

| Listed entities other than NBFC which have issued debt securities by way of private placement | Yes | Not required as exempted |

| Listed entities other than NBFC which have issued debt securities by way of public issue | Yes | Yes. Deposit or invest before 31st December, 2020 |

| Unlisted companies other than NBFC | Yes. | Yes. Deposit or invest before 31st December, 2020 |

Please note that the aforesaid shall be applicable from 12th June, 2020 i.e. the date of publication of the notification in the official gazette. In this regard, if for instance companies which have been specifically exempted pursuant to the recent notification, have already invested or deposited their funds to fulfil the DRF requirement may liquidated the funds as they are no longer statutorily require to invest in such securities.

Synopsis of DRR and DRF provisions[2]

A brief analysis of the DRR and DRF provisions as amended by the MCA notification dated 16th August, 2019 and 5th June, 2020 has been presented below:

| Sl. No. | Particulars | Type of Issuance | DRR as per erstwhile provisions | DRR as per amended provisions | DRF as per erstwhile provisions | DRF as per amended provisions |

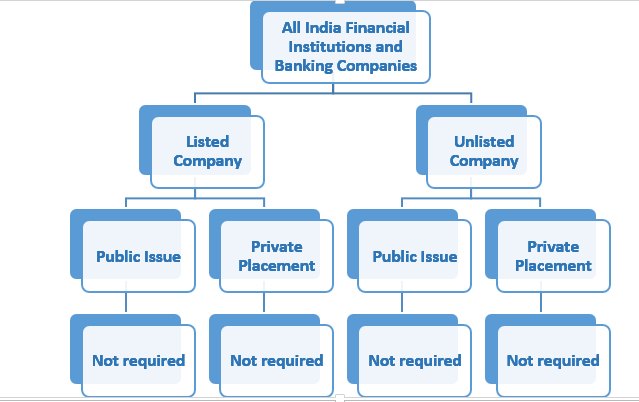

| 1. | All India Financial Institutions | Public issue/private placement | × | × | × | × |

| 2. | Banking Companies | Public issue/private placement | × | × | × | × |

| 3.

|

Listed NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank | Public issue | √

25% of value of outstanding debentures |

× | √ | √ |

| Private Placement | × | × | √ | × | ||

| 4. | Unlisted NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank | Private Placement |

× |

× |

× |

× |

| 5.

|

Other listed companies | Public Issue | √

25% of value of outstanding debentures |

× | √ | √ |

| Private Placement | √

25% of value of outstanding debentures |

× | √ | × | ||

| 6. | Other unlisted companies | Private Placement | √

25% of value of outstanding debentures |

√

10% of the value of outstanding debentures |

√ | √ |

[1] http://www.mca.gov.in/Ministry/pdf/Circular_25032020.pdf

[2] This table includes analysis of provisions of DRR and DRF as per CA, 2013 and amendments introduced vide MCA notification dated 16th August, 2019 and 5th June, 2020.

Erstwhile provisions- Provisions before amendment vide MCA circular dated 16th August, 2019

Amended provisions- Provisions after including amendments introduced vide MCA circular 5th June, 2020

[1] https://www.mca.gov.in/Ministry/pdf/ShareCapitalRules_16082019.pdf

Provisions relating to DVR & DRR- stands amended

Amendments introduced in Companies (Share Capital and Debentures) Amendment Rules, 2019

by Smriti Wadehra (smriti@vinodkothari.c0m)

The recent Notification of Ministry dated 16th August, 2019 has amended the provisions of Companies (Share Capital and Debentures) Rules, 2014 with respect to quantum of holding of equity shares with differential voting rights by a Company and provisions pertaining to creation of debenture redemption reserve. The amended provisions are applicable from the date of notification in the e-gazette i.e. 16th August, 2019.

Differential Voting Rights

SEBI in its Board Meeting dated 27th June, 2019 proposed insertion of the provisions of DVRs in SEBI ICDR Regulations. The proposal was w.r.t inter alia to cap the total voting rights of superior rights shareholders (including ordinary shares) at 74% of the total voting power. The respective amendments are still awaited. Meanwhile, the Ministry vide the aforesaid Notification amended the provisions under CA, 13 related to DVRs. The Notification has escalated the limit of DVR shares in the Company from 26% of total post-issue paid up equity capital of the Company to 74% of the total voting power.

The erstwhile provisions of the Companies (Share Capital and Debentures) Rules, 2014 permitted issuance of equity shares with differential rights subject to compliance of conditions mentioned in Rule 4(1) of the said Rules. One of criterion for issuance of equity shares with differential rights by a Company was that shares with differential rights should not exceed 26% of total post-issue paid up equity capital of the Company at any point of time. However, the amendment has increased this limit to 74% of the total voting power at any point of time. Notably, this is another significant highlight of the amendment that the erstwhile cap of 26% was based on the post-issue paid up equity capital which has now been changed to 74% of the voting power.

Further, in this regard, condition on companies issuing shares with differential rights having consistent track record of distributable profits for the last three years have been done away with.

Debenture Redemption Reserve

The erstwhile provisions of Section 71(4) read with Rule 18(1)(c) of the Companies (Share Capital and Debentures) Rules, 2014 required every company issuing redeemable debentures to create a debenture redemption reserve (“DRR”) of at least 25% of outstanding value of debentures for the purpose of redemption of such debentures. Apart from creation of DRR, such companies were required to either deposit, before April 30th each year, in a scheduled bank account, a sum of at least 15% of the amount of its debentures maturing during the year ending on 31st March of next year or invest in one or more securities enlisted in Rule 18(1)(c) of Debenture Rules.

Under the erstwhile framework, the following classes of companies were required to comply with the provisions relating to DRR:

- NBFCs registered with RBI under section 45-IA of RBI Act, 1934 issuing debentures through public issue;

- Other listed companies coming up with public issue or private placement;

- Unlisted companies issuing debentures on private placement basis.

With a view to liberalise the legal framework surrounding issuance of debentures by NBFCs, the FinMin proposed Union Budget of 2019-20 proposed to scrap off the requirement of creation of DRR for publicly issued debentures also so as to motivate NBFCs. Subsequently, the MCA came out with notification to amend the Companies (Share Capital and Debentures) Rules, 2014.

The amended provisions has exempted NBFCs registered with RBI and HFCs registered with National Housing Bank from creation of DRR in case of public issue of debentures. Further, the requirement of listed companies to create DRR has been done away with. The amended Rules have also lowered down the quantum of funds to be transferred to DRR by unlisted companies. However, as a flipside to the exemptions granted, the MCA has knowingly or unknowingly, unsettled an otherwise settled matter on creation of debenture redemption fund as per Rule 18(7).

Under the erstwhile provisions required creation of debenture redemption fund only by those companies on which DRR was applicable. However, under the current set of rules, the requirement to create DRF will apply to all listed companies, other than AIFIs or other FIs as per the clause of section 2(72). This new rule applies even to NBFCs.

It is pertinent to note that until now, NBFCs were required to create debenture redemption reserve only for publicly issued debt securities. However, under the new rule, all listed NBFCs will have to create a DRF even in case of private placement of debentures. This change in the rules seems to be contradicting the intention of proposal in the Union Budget.

The intention of the proposal was to promote NBFCs to explore Bond markets more often for fund raising, however, the language of the new rule has jeopardised the existing cases of debenture issuances, let alone be new debenture issuances. Considering the ongoing liquidity crisis, the entire financial system is going through, the implications of this requirement could be severe.

Creation of DRR is somewhat a liberal requirement then creation of DRF, this is because, where the former is merely an accounting entry, the latter is investing of money out of the Company and the fact the new rule casts an exemption from the first and not from the second makes the situation a bit awkward. Therefore, where there is no requirement even for annually conserving a part of their profits, the requirement of creating a fund out of the same becomes completely illogical.

Hence, in our view, the amendments have actually slashed the expectation to relax issuance of debentures by NBFCs and on the other hand has also taken away the available exemption to the NBFCs for not creating DRF in case of issuance of debt securities through private placement. The actual intent of the amendment would have been to reduce the requirement of DRR from somewhat say 25% to 10%, however, in a completely unexpected move, the requirement for parking liquid funds, in form of a debenture redemption fund (DRF) has been extended to all bond issuers except unlisted NBFCs (which are hardly any in India), irrespective of whether they are covered by the requirement of DRR or not.

In this regard, the notification also fails to clarify the basic question that is whether the requirement will be applicable to debentures/bonds already issued, before the date of the notification or only after the date of notification. Though, the language suggest that the same shall be applicable on debentures due for redemption after the date of notification, i.e. for debentures maturing during the year ending on 31st March, 2020. However, in our view, one should try to create a DRF for the debentures maturing within 31st March, 2020 itself. Lastly needless to say, the MCA notification needs to be considered immediately.

A brief analysis of the amendments are discussed below:

Applicability of DRR and Debenture Redemption Fund

a) All India Financial Institutions and Banking Companies

b) NBFCs registered with RBI under section 45-IA of RBI Act, 1934 and Housing Finance Companies registered with National Housing Bank

- Other companies

Synopsis of amendments in DRR provisions

| Sl. No. | Particulars | Type of Issuance | DRR as per erstwhile provisions | DRR as per amended provisions | DRF as per erstwhile provisions | DRF as per amended provisions |

| 1. | All India Financial Institutions | Public issue/private placement

|

× | × | × | × |

| 2. | Banking Companies | Public issue/private placement

|

× | × | × | × |

| 3.

|

Listed NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank

|

Public issue | √

25% of value of outstanding debentures |

× | √ | √ |

| Private Placement

|

× | × | × | √ | ||

| 4. | Unlisted NBFCs registered with RBI under section 45-IA of the RBI Act, 1934 and HFC registered with National Housing Bank

|

Private Placement

|

× |

× |

× |

× |

| 5.

|

Other listed companies

|

Public Issue

|

√

25% of value of outstanding debentures

|

× | √ | √ |

| Private Placement

|

√

25% of value of outstanding debentures

|

× | √ | √ | ||

| 6. | Other unlisted companies | Private Placement | √

25% of value of outstanding debentures

|

√

10% of the value of outstanding debentures |

√ | √ |

Provisions updated as on 5th June, 2020 maybe viewed here